Sustainable CSR: Legal and Managerial Demands of the New EU Legislation (CSRD) for the Future Corporate Governance Practices

Abstract

:1. Introduction

2. Theoretical Basis

2.1. Non-Financial Reporting and Corporate Social Responsibility

2.2. Development of the EU Legislation on the Non-Financial Reporting

2.2.1. Directive 2003/51/EU

2.2.2. Directive 2006/46/ES

2.2.3. NFRD

Obligation on Non-Financial Information Disclosure

Diversity Policy

Non-Financial Statement

2.3. Implementation of the NFRD in Slovenia

2.4. Commission’s Proposal on New Legislation

- (i)

- Equal opportunities for all, including gender equality and equal pay for similar work, training and skills development, and employment and inclusion of people with disabilities.

- (ii)

- Working conditions, including secure and adaptable employment, wages, social dialogue, collective bargaining and the involvement of workers, work–life balance, and a healthy, safe, and well-adapted work environment.

- (iii)

- Respect for the human rights, fundamental freedoms, democratic principles, and standards established in the International Bill of Human Rights and other core UN human rights conventions, the International Labour Organization’s Declaration on Fundamental Principles and Rights at Work, and the ILO fundamental conventions and the Charter of Fundamental Rights of the European Union (19b/2/b article of the CSRD).

- The role of the undertaking’s administrative, management and supervisory bodies, including sustainability matters and their composition;

- Business ethics and corporate culture, including anti-corruption and anti-bribery;

- Political engagements of the undertaking, including its lobbying activities;

- The management and quality of relationships with business partners, including payment practices;

- The undertaking’s internal control and risk management systems, including the undertaking’s reporting process (the second paragraph of the new Article 19b of the CSRD proposal).

2.5. Conclusion of the Theoretical Basis

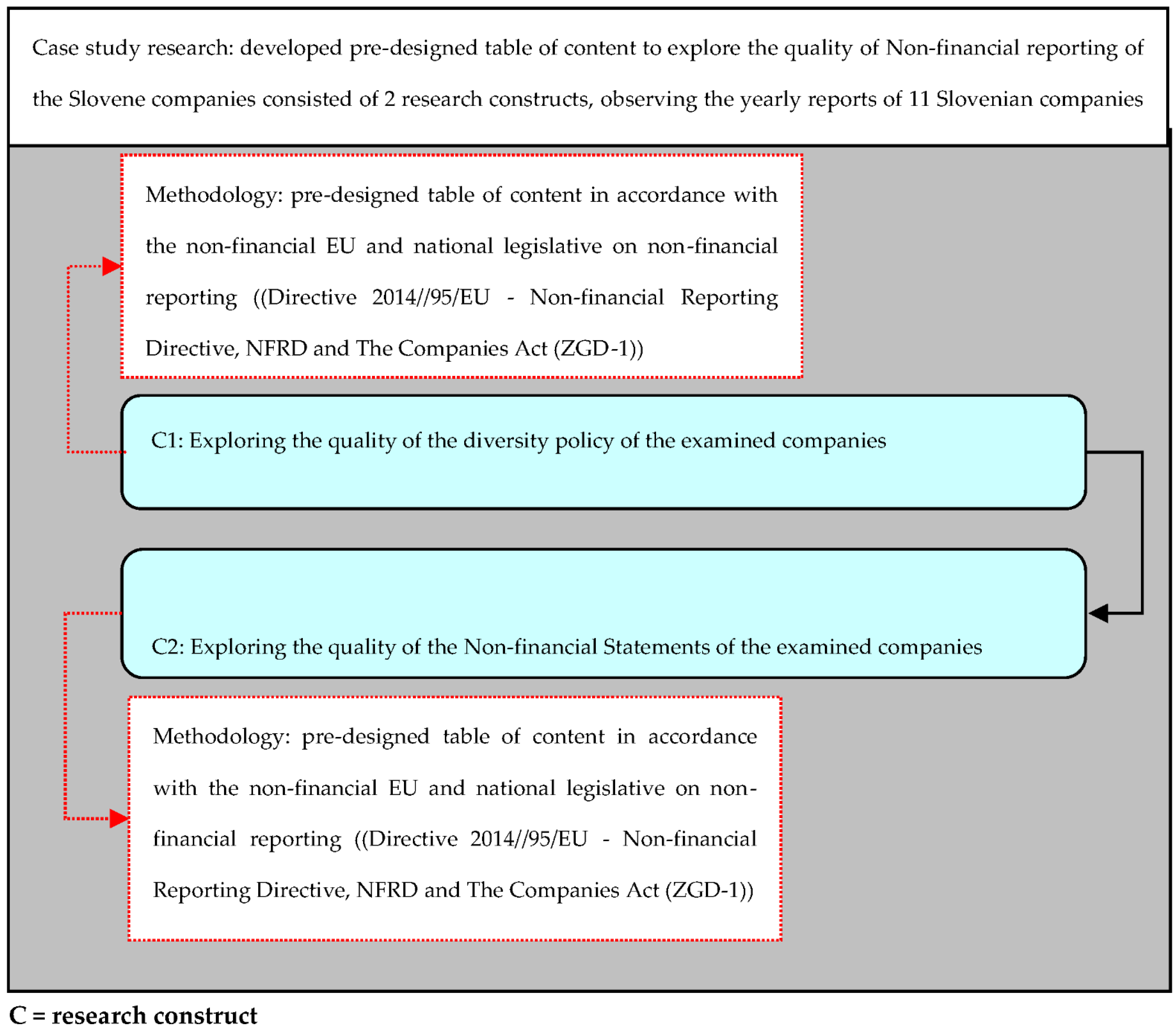

3. Research Methodology and Research Sample Used

4. Research Results

5. Conclusions and Further Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| 1. Does the company have a defined diversity policy? |

|---|

| YES: 11 NO: |

| 2. Does the company ensure diversity in its management and supervisory bodies: |

- Sex YES: 9 NO: 2 - Age YES: 9 NO: 2 - Education YES: 11 NO: |

| 3. In what way does the observed company implement a diversity policy? - Company 1: The annual report did not specify how diversity is implemented. However, considering the annual report, the diversity policy is implemented. - Company 2:/ - Company 3: The Diversity Policy is implemented through: Recruitment, selection of candidates and consent for members of the management bodies; In accordance with EU Regulation No. 575/2013 (CRR) and the provisions of the Banking Act; The Bank publicly discloses and, at least annually, reviews and updates information on the diversity policy for the selection of members of the management body; The Diversity Policy for the Management Body and Senior Management sets out the framework for diversity and gender representation in the management and supervisory bodies; The Diversity Policy for the Management Body and Senior Management sets out the framework for diversity and gender representation in the management and supervisory bodies; The management body is composed in such a way that it as a whole has the appropriate knowledge, skills and experience needed to have a thorough understanding of the bank’s strategy and challenges and the risks to which it is exposed; Recruitment, selection of candidates and proposal of candidates to the founder/community as members of the supervisory bodies; Selection of candidates and selection of appropriate members; Self-evaluation of the work of the Supervisory Board and its committees. - Company 4: The company’s corporate governance statement includes a commitment to non-discrimination, which states that Krka provides equal opportunities to its employees regardless of gender, race, colour, age, medical condition or disability, religious, political or other beliefs, trade union membership, national or social origin, marital status, property, sexual orientation or other personal circumstances. The company’s diversity policy respects the principle of inclusion and equal opportunities, including in the composition of supervisory and management bodies. Candidates for these positions are considered gender, age, education, professional experience and skills. They also consider professional diversity and international experience to ensure complementarity in the highest governance bodies for the continuous functioning of the Krka Group. - Company 5: The stakeholders commit to implementing the objectives of the Diversity Policy by taking into account the best practices of the Diversity Policy in the composition of these bodies, combined with the need to ensure continuity in their composition and the need to manage the areas and skills within their competence. All selected diversity aspects, as well as any other identifiable aspects, are taken into account when proposing and deciding on the appointment of candidates to the Management Board or the Supervisory Board, all to ensure the optimum structure of the Management Board or the Supervisory Board necessary for the successful operation of the Company, respectively, in combination with the requirements of Article 6. The diversity policy is implemented through an appropriate recruitment and selection process for candidates to the Supervisory Board and the Management Board. - Company 6: In its Corporate Governance Statement, the company states that it implements a diversity policy in the management and supervisory bodies, mainly through an appropriate recruitment and selection process, with the participation of the Human Resources or Nomination Committee. The company’s bodies implement it following the legislation in force, by the Labour Relations Act (ZDR-1), and by complying with the principles and provisions of the codes that set out the content and make recommendations in this area. The company does not specify the exact code(s) followed in its diversity policy (“...with due regard to the principles and provisions of the codes which state their content and make recommendations in this area”). As the company does not explicitly state which codes it follows, we cannot verify the ethical guidelines—or the principles and provisions of the regulations—that it claims to follow. - Company 7: The Diversity Policy is implemented in particular in the following activities: • Recruitment, selection of candidates and selection/approval of members of management bodies; • Recruitment, selection and proposal of candidates for members of supervisory bodies to the founder/group; • Recruitment, selection of candidates and selection of candidates in the succession procedure; • Conduct a self-assessment of the work of the Supervisory Board, which should include an assessment of the composition of the management and Supervisory Board in terms of ensuring diversity. - Company 8: It is implemented in a way that: respects the cultural, ethical, social, political and legal diversity of peoples and communities, taking into account the need for a business model that will be consistent with social, economic and environmental practices and that will serve to meet today’s needs while taking into account the provision of living and working space for future generations. It recognises its responsibility as a leading global telecommunications company, putting its technology, products and services to promote respect for human rights. - Company 9: They are committed to fairness, equal treatment and opportunity for individuals and business partners and tolerate and embrace diversity. The company respects the value of diversity. Employees, customers, business partners, suppliers and other members of external stakeholders are citizens of many different countries with a multitude of different nationalities, religions, beliefs, cultures and social characteristics. They foster cultural diversity and the creation of international teams and business communities. - Company 10: Through an appropriate search and selection process for management and Supervisory Board candidates. To this end, the Implementing Agents shall use one or more recruitment channels to apply a suitable number of competent candidates of different sexes and ages. - Company 11: For the members of the management body, the experience criterion, the personal reliability and reputation criterion and the governance criterion are defined, with emphasis on the management of conflicts of interest and independence, and the time availability criterion; the Fit & Proper Committee of the company is also defined as the evaluation body, and at least one member of the management board must be a female. |

| 4. Results of the diversity policy achieved for the reporting period: - Company 1: The Annual Report does not contain the information to answer this question. The Diversity Policy is implemented, but the results achieved are not presented. - Company 2: Company provides equal opportunities to its employees regardless of gender, race, colour, age, health or disability, religion, political or other beliefs, trade union membership, national or social origin, marital status, property, sexual orientation or other personal circumstances. Any form of discrimination against employees is not permitted. - Company 3: On behalf of the Governing Body’s assessment, the diversity screening exercise has been analysed according to the following criteria: gender, age, education, work experience (both in and outside the business) and banking knowledge. The 2019 analysis concluded that the company’s diversity policy was adequately reflected in the composition of the governing body. During the 2018 analysis, the company established an accompanying maturity model with target values for each substantive item. The target values were regularly monitored as part of the periodic assessments of the suitability and effectiveness of the body. This system should allow them to be assessed retrospectively in a comparable way and monitor progress and improvements regularly. The company does not have any results related to the Diversity Policy shown. Based on the diversity policy document, the governing body of Abanka d.d. notes that the diversity principle has not yet been fully implemented. However, the bank has made efforts to do so. They point out that effective management and control of business conduct is nevertheless ensured and that the governing body selected is appropriate. - Company 4: In 2019, the Management Board and Supervisory Board of the company did not adopt a specific document entitled Diversity Policy, but the company implements the principles of the Diversity Policy through other internal acts, policies and procedures, including the Code of Conduct, the Corporate Governance Policy, the Rules of Procedure of the Supervisory Board regarding the procedures for nominating Supervisory Board members, and the methods and commitments of the Human Resources Committee of the Supervisory Board and the Nomination Committee for the preparation of the election proposal for the members of the Supervisory Board. Diversity is ensured in practice in the nomination and nomination procedures for members of the management and supervisory bodies, as the company always strives to provide equal opportunities for candidates and prohibits any discrimination. - Company 5: Until October 2019, the composition of the Management Board and Supervisory Board remained unchanged in 2017. However, on 25 October 2019, the Chair of the Supervisory Board, Nada Drobne Popović, became interim Chair of the Management Board, following the early termination of the term of office of three members of the Management Board based on agreements. Therefore, the gender diversity of the two bodies changed significantly as of that date. As of 1 January 2020, the company’s Management Board will be headed by three women and the Supervisory Board by a man. There was considerable dynamism in the composition of the Management Board and the Supervisory Board throughout the year. The Management Board was composed of three women, then two women and two men, then three men and two women, and at the end of the year, when the Management Board was completed, one of the five members was a woman. At the end of the year, the Supervisory Board carried out a recruitment procedure to select candidates for the Supervisory Board. Still, it did not propose any women to the General Meeting held, which is not in line with the Diversity Policy of the Management Board and the Supervisory Board of the company, which also identifies gender diversity as one of the six essential aspects of diversity. In addition to the above, the Works Council did not appoint any female employee representatives to the Supervisory Board at the end of 2020, whose term of office will start in 2021. The Works Council also proposed to the Supervisory Board the appointment of a male as Works Director, whose term of office began on 11 December 2020. The energy business is otherwise characterised by low female gender representation in management positions. Based on a counter-proposal at the abovementioned General Meeting, it was voted that the Supervisory Board would be composed of eight males and one female member after 11 April 2021. In 2019, the Supervisory Board also signed up to the 40/30 2026 voluntary gender diversity target initiative of the Slovenian Supervisory Board Association, which was supported by, among others, Slovenian State Holding d.d. and the Ljubljana Stock Exchange d.d., and which pledges to voluntarily achieve the gender diversity target of 40 per cent for supervisory board members and 33 per cent in total for supervisory board members and management boards of the underrepresented gender in publicly traded and state-owned companies by the end of 2026. The initiative was also signed by the Supervisory Board of the Association of Supervisory Boards of Slovenia. Even though SDH, d.d. made a counter-proposal at the General Meeting, the fundamental commitments of that initiative were not respected, and only one female representative was proposed for appointment. Given that the members of the Supervisory Board were appointed for a four-year term and the members of the Management Board for five years in 2020, no significant changes in gender diversity are expected in the coming years. - Company 6: There is no record of the results achieved under the Diversity Policy for the reporting period (i.e., the 2019 performance and operational period). - Company 7: In the 2019 Annual Report, the company does not report on the results achieved under the Diversity Policy. - Company 8: In 2019, the company achieved another successful financial year, consolidating its leading position in all telecommunications market segments. In addition to the growth of all key financial indicators, last year was marked by a substantial investment cycle, as one of the country’s leading investors was positively influenced by the changes in the investment climate. With investments in the modernization of fixed and mobile networks, the focus remains on further growth in all business segments, developing innovative products, and raising the quality of service for all users. For years, the company has promoted sustainable development, set best practices in setting standards for superior communications, and taken a leading role in recognizing the importance of environmental protection. The company is an excellent company with a great team of employees. Over the last five years, the company has become one of the largest investors in the country and one of the most important employers contributing to the country’s overall development. - Company 9: For many years, the company has placed great emphasis on employee development, both in professional areas and in the development of individual competencies. Employee development and training are therefore planned according to the employee’s needs. In 2019, several individual and group training sessions were also organized. In 2019, within the framework of the company’s international project called XXX, in-depth training sessions for female and male employees at the points of sale were continued. - Company 10:/ - Company 11:/ |

| 8. Does the declaration on diversity policy contain all the required information (adequate, partially adequate, inadequate), describing it in words and illustrating it with concrete examples (see questions 2, 3, and 4 for details)? |

| (a) CONSISTENT: 5 (b) PARTIALLY CONSISTENT: 5 (c) INCONSISTENT: 1 |

| 9. Is the diversity policy implemented in the observed company? YES: 11 NO: |

| 10. Suppose the diversity policy is not implemented in the observed company. Is there an explanation of why the company is not implemented (describe in words and illustrate with a concrete example)? - Company 1: The company has a diversity policy but does not have a specific document for this due to the current situation in the company. This is made clear in the annual report. They also said that this report would be prepared when the time comes. - Company 2:/ - Company 3:/ - Company 4:/ - Company 5:/ - Company 6:/ - Company 7:/ - Company 8:/ - Company 9:/ - Company 10:/ - Company 11:/ |

| 1. Does the Company’s Non-Financial Statement the observed company exist? |

|---|

| YES: 10 NO: 1 |

| 2. Does the company’s Statement of non-financial performance contain all the required information (see answers to questions 3 to 9)? |

| (a) CONSISTENT: 9 (b) PARTIALLY CONSISTENT: 1 (c) INCONSISTENT: 1 |

| 3. Does the company’s Statement of non-financial performance disclose information on the following: |

| (a) Environmental YES: 11 NO: (b) Social YES: 11 NO: (c) Human resurse matters YES: 11 NO: (d) Respect for human rights; and YES: 10 NO: 1 (e) Anti-corruption and anti-bribery matters YES: 9 NO: 2 |

| 4. Does the company’s Statement of non-financial performance include a brief description of the existing business model? |

| YES: 8 NO: 3 |

| 5. Does the company’s Statement of non-financial performance include a description of the company’s policies on the matters referred to in question 3 (environmental, social, human resources, etc.)? |

| YES: 11 NO: It contains a description of only some of the policies: - Company 1:/ - Company 2:/ - Company 3:/ - Company 4: Yes, the company’s Statement of non-financial performance contains a description of the company’s policies regarding the matters referred to in question 3 - Company 5:/ - Company 6: The Non-Financial Statement of the company includes descriptions of the company’s policies on the matters set out in question 3. The Non-financial Statement of the company apart from: • description of the environmental policy, • a description of the social policy, • a definition of the human resources policy and occupational health and safety, • a description of the human rights policy, and • a description of the anti-corruption and anti-bribery policy also includes: • a description of the business model in the non-financial business area, • occupational health and safety and fire protection costs, • key non-financial indicators, • key risks and their management, and • due diligence. The policy descriptions refer mainly to how each policy was implemented (for the reporting year), what activities were carried out, their objectives, and how successful they were. Environmental policy For 2019, the company has set four annual targets with the company’s environmental objectives, namely: • meeting environmental protection requirements, • define measures to reduce emissions to the environment in the event of an emergency, • identify and analyse process risks that may harm the external environment, • sustainable management of resources and products. Regarding environmental factors, the company’s operations significantly negatively impact the surrounding area. As a metallurgical and chemical industry, its activities (production of titanium dioxide, sulphuric acid, zinc processing, fluorinated polymers and elastomers, etc.) cause significant pollution in the surrounding area—emissions, waste, air and water pollution, noise,... In the past year, they have been confronted with many environmental requirements (mainly of a regulatory nature), such as new chemical requirements, export of TENORM waste to the USA, etc. Also, in 2019, various projects were implemented for sustainable management of resources and products: replacement of lights with energy-saving LED lamps (in the business units), elimination of compressed air leaks, improved waste management system, etc. In 2019, 22 process risks were identified and analysed in each business unit that could harm the environment. In the previous year, 2 amendments to the environmental permit and 8 applications or modifications to OVD applications were submitted to the Environment Agency (3 for the amendment of the water permit and ecologically acceptable flow, 1 statement of facts regarding the pipeline to the Savinja, 3 amendments regarding the Bukovžlak non-hazardous waste landfill and an application for the Sulphuric Acid Plant). In 2019, six inspections were carried out in the fields of environment and chemicals—five in the background and one in the area of chemicals. As mentioned above, the operation of the Zinc Plant has a significant impact on the local population, as confirmed by two complaints to the Environmental Protection Service, one related to perceived odour and the other to noise. The company responded to both complaints. The complaint about excessive night noise disturbing a resident from a nearby street is gradually being resolved. In 2019, they prepared their nineteenth report on responsible environmental management (for 2018), which, according to the Association of the Chemical and Rubber Industry of Slovenia, demonstrates their attitude towards the environment, health and society. The Responsible Care Programme aligns with the principles of the voluntary initiative promoted by ICCA—International Council of Chemical Associations and CEFIC—European Chemical Industry Council. Human resources policy The Statement of Non-Financial Performance contains a detailed description of the HR policy. As of 31 December 2019, the company employed 846 people, 77.4% men and 22.6% women. The average age structure on that date was 46.89 years. In 1985, the management started a long-term restrictive HR strategy—interestingly, the number of employees has more than halved since then. In the recruitment process, the company puts a lot of attention into staff development and training, for which resources are also allocated annually. In 2019, the company realised an average of 19.49 h of training per employee, with 446.08 h earmarked for implementation. The training was mainly aimed at raising the level of knowledge and renewing the employees’ existing knowledge. In social work, the company pays particular attention to individual solutions to disability issues—more and more employees have limitations at work due to their health conditions. At the end of last year, the company had 63 persons with disabilities, representing 7.4% of the workforce. The structural percentage of disabled people has been decreasing over the years. The company is committed to an employment and education policy that positively impacts the qualification structure. The company strives to increase the qualification level of its employees, which it manages to do through the retirement of less qualified employees, internal training, recruitment of staff with higher qualifications and general staff optimisation (reorganisation of jobs, internal reassignment and mergers). In 2019, they reduced the share of unskilled labour (from 48.7% to 9.9%) and increased the highly educated labour force (3.5% to 18.2%). Within the HR policy, the company pays a lot of attention to health and safety, where it has set itself (for 2019) three indicative objectives, namely: • zero injuries at work (long-term goal), • identification and breakdown of risks that may harm occupational safety and health, • organising and implementing employee health promotion (healthy snacks, yoga workshops, team building, blood sugar and fat control, etc.) Human rights policy The company is committed to tolerance, mutual respect and respect for human rights. To ensure human rights, they pay attention to protecting personal data, the Code of Ethics, and compliance with the Policy on the Prohibition of Sexual and Other Harassment and Ill-treatment in the Workplace. They respect the right to form workers’ organisations (Trade unions of the company) and strive to ensure that the dialogue between social partners is conducted professionally by the legal framework. Anti-corruption and anti-bribery policy In their work to fight corruption and bribery, all employees are obliged to consider the Company’s best interests before their interests or those of third parties in performing their duties and exercising their rights and obligations. To prevent corruption or bribery, the Company has its own Code of Ethics, which guides all employees’ ethical conduct and actions. It is also reflected in the ethics of the Company’s relations with its business partners and competitors. Social policy The company attaches great importance to social policy. The company is aware of the great importance of developing intergenerational cooperation, transfer of knowledge and joint building of the value system in our society. Therefore, special care is given to collaborating with young people in Slovenian primary and secondary schools, educational institutions and universities. They regularly organise visits and presentations and produce various assignments—research, seminars, etc. In the context of social projects, the non-financial report records all past and active cooperation (excursions, competitions, various actions, etc.), of which there are many. They try to keep all their stakeholders regularly informed of their plans and achievements through various forms of communication. For internal communication purposes, they have issued 23 Cinco and Cinka notices, their mascots, which encourage employees to be more productive, economical and safe and inform them of important information. In addition, they have also published 3 Newsletters and 1 issue of Current News for their employees. They pay great attention to the importance of donations and sponsorships, which they also cite as one of the ways of risk management in their social policy, anti-corruption, and anti-bribery policy (ironically). The company states that it must operate and do business long-term and sustainably in environmental impact and relation to the broader social community. They know their role and importance and generously promote, support, and finance activities that improve people’s quality of life, work, and the community. In 2019, they spent €741 thousand on various sponsorships and donations, or just over 0.43% of total sales. As a socially responsible company, they support sports, cultural, and environmentally oriented activities. In line with their strategy, 92.7% of sponsorship and donation funds are allocated to sports, 1.6% to culture and 5.7% to other activities. The essential areas and activities in which they invest resources and develop responsibly together with their promoters are: • Sports associations and clubs (the company is the general sponsor of the Celje Women’s Basketball Club and the Kladivar Athletics Club; they also sponsor KK Domžale, RK Gorenje Velenje, etc.) • Artistic creation, the work of cultural institutions and artistic associations (Celeia Institute, SLG Celje), • Educational, educational and charitable organisations and associations (volunteer fire brigades, primary schools, secondary schools, etc.). Occupational health and safety and fire protection costs In 2019, the company spent EUR 507,497.06 on occupational health and safety and fire protection costs (excluding preventive maintenance on work equipment), 16% less than the previous year. - Company 7:/ - Company 8:/ - Company 9:/ - Company 10:/ - Company 11:/ |

| 6. Does the company’s Statement of non-financial performance include a description of implementing the company’s due diligence procedures to the above policies? |

| YES: 10 NO: 1 |

| 7. Does the company’s Statement of non-financial performance include a description of |

| (a) the results of those policies, YES: 11 NO: (b) the principal risks about those matters associated with the Company’s activities YES: 9 NO: 2 (c) including, where appropriate and proportionate, the company’s business relationships, products or services that could cause serious adverse effects in those areas; and YES: 7 NO: 4 (d) how the company manages the above risks YES: 10 NO: 1 |

| 8. Does the Company’s Statement of Non-Financial Performance include key non-financial performance indicators relevant to individual activities? (Article 70c(1) of the CGD-1) |

| YES: 9 NO: 2 |

| 9. If the company under review does not apply any of the above policies, it shall provide a clear and reasoned explanation in the Company’s Statement of Non-Financial Performance. |

| YES: 5 NO: 6 |

| 10. Does the audited company refer to the accounting part of the annual report in its Statement on the Non-Financial Performance of Companies? |

| YES: 3 NO: 8 |

References

- World Commission on Environment and Development. Our Common Future: Report of the World Commission on Environment and Development; Oxford University Press: Oxford, UK, 1987; pp. 1–91. [Google Scholar]

- Monciardini, D. The ‘Coalition of the Unlikely’ Driving the EU Regulatory Process of Non-Financial Reporting. Soc. Environ. Account. J. 2016, 36, 76–89. [Google Scholar] [CrossRef] [Green Version]

- Bratina, B.; Primec, A. Izdelava poslovnih poročil, izjav o upravljanju ter izjav o nefinančnih informacijah pri konsolidiranih letnih poročilih in letnih poročilih posameznih gospodarskih družb. In Proceedings of the Dnevi Slovenskih Pravnikov, Podjetje in delo, Portorož, Slovenija, 12–14 October 2017; pp. 977–988. [Google Scholar]

- Baumüller, J.; Grbenic, S.O. Moving from non-financial to sustainability reporting: Analyzing the EU Commission’s proposal for a Corporate Sustainability Reporting Directive (CSRD). Facta Univ. Ser. Econ. Organ. 2021, 18, 369–381. [Google Scholar] [CrossRef]

- European Commission. Proposal for a Directive of the European Parliament and of the Council Amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as Regards Corporate Sustainability Reporting. 2021. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52021PC0189 (accessed on 26 March 2022).

- Carroll, A.B. A History of Corporate Social Responsibility: Concepts and Practices. In The Oxford Handbook of Corporate Social Responsibility; Crane, A., Matten, D., McWilliams, A., Moon, J., Siegel, D.S., Eds.; Oxford University Press: Oxford, UK, 2008; pp. 19–46. [Google Scholar]

- Murphy, P.E. Corporate social responsiveness: An evolution. Univ. Mich. Bus. Rev. 1978, 6, 19–25. [Google Scholar]

- Maak, T. Undivided corporate responsibility: Towards a theory of corporate integrity. J. Bus. Ethics 2008, 82, 353–368. [Google Scholar] [CrossRef]

- Bowen, H.R. Social Responsibilities of the Businessman; Harper & Row: New York, NY, USA, 1953. [Google Scholar]

- Eels, R.; Walton, C. Conceptual Foundations of Business, 3rd ed.; Richard D. Irwin: Burr Ridge, IL, USA, 1974. [Google Scholar]

- Carroll, A.B. A Three-Dimensional Conceptual Model of Corporate Social Performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Maignan, I.; Ferrell, O.C. Corporate Social Responsibility and Marketing: An Integrative Framework. J. Acad. Mark. Sci. 2004, 32, 3–19. [Google Scholar] [CrossRef]

- Balmer, J.; Fukukawa, K.; Gray, E. The Nature and Management of Ethical Corporate Identity: A Commentary on Corporate Identity, Corporate Social Responsibility and Ethics. J. Bus. Ethics 2007, 76, 7–15. [Google Scholar] [CrossRef] [Green Version]

- Buchholz, R.A. The Natural Environment: Does it Count? Acad. Manag. Exec. 2004, 18, 130–133. [Google Scholar] [CrossRef]

- Dahlsrud, A. How Corporate Social Responsibility Is Defined: An Analysis of 37 Definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Primec, A. Upravljanje Delniških Družb in Kodeks Upravljanja Javnih Delniških Družb. Gradivo za Izobraževanje za Pridobitev Strokovnih Znanj za Opravljanje Nalog Pooblaščenega Revizorja in Pooblaščenega Ocenjevalca Vrednosti Podjetij ter Strokovnega Naziva Preizkušeni Računovodja, Preizkušeni Notranji Revizor, Preizkušeni Davčnik; Slovenski Institut za Revizijo: Ljubljana, Slovenia, 2017. [Google Scholar]

- Fatemi, A.; Glaum, M.; Kaiser, S. ESG performance and firm value: The moderating role of disclosure. Glob. Finance J. 2018, 35, 45–64. [Google Scholar] [CrossRef]

- Kim, D.; Go, S. Human Capital and Environmental Sustainability. Sustainability 2020, 12, 4736. [Google Scholar] [CrossRef]

- EFRAG. Public Consultation on the First Set of Draft ESRS. Available online: https://www.efrag.org/lab3 (accessed on 20 May 2022).

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and social responsibility: A review of ESG and CSR research in corporate finance. J. Corp. Finance 2021, 66, 101889. [Google Scholar] [CrossRef]

- Cini, A.C.; Ricci, C. CSR as a Driver where ESG Performance will Ultimately Matter. Symph. Emerg. Issues Manag. 2018, 1, 68–75. [Google Scholar] [CrossRef] [Green Version]

- European Parliament. Corporate Social Responsibility (CSR) and Its Implementation Into EU Company Law. 2020. Available online: https://www.europarl.europa.eu/thinktank/en/document/IPOL_STU(2020)658541 (accessed on 25 March 2022).

- European Parliament and the Council. Directive 2003/51/EC of the European Parliament and of the Council of 18 June 2003 Amending Directives 78/660/EEC, 83/349/EEC, 86/635/EEC and 91/674/EEC on the Annual and Consolidated Accounts of Certain Types of Companies, Banks and Other Financial Institutions and Insurance Undertakings. Off. J. Eur. Union 2003, 178, 16–22. [Google Scholar]

- Primec, A.; Belak, J. Corporate governance and management: Institutional and formal approach for achieving socially rsponsible and corporate governance of a higher quality. In Proceedings of the Paradoxes of Leadership and Governance in the Postmodern Society, 5th International OFEL Conference on Corporate Governance, Management and Entrepreneurship, Dubrovnik, Croatia, 7–8 April 2017; CIRU—Governance Research and Development Centre: Zagreb, Croatia, 2017; pp. 154–164. [Google Scholar]

- European Parliament and the Council. Directive 2006/46/EC of the European Parliament and of the Council of 14 June 2006 amending Council Directives 78/660/EEC on the annual accounts of certain types of companies, 83/349/EEC on consolidated accounts, 86/635/EEC on the annual accounts and consolidated accounts of banks and other financial institutions and 91/674/EEC on the annual accounts and consolidated accounts of insurance undertakings. Off. J. Eur. Union 2006, 224, 1–7. [Google Scholar]

- Commission. Proposal for a Directive of the European Parliament and the Council on Improving the Gender Balance among Non-Executive Directors of Companies Listed on Stock Exchanges and Related Measures. 2012. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52012PC0614 (accessed on 24 March 2022).

- Rao, K.; Tilt, C. Board Composition and Corporate Social Responsibility: The Role of Diversity, Gender, Strategy and Decision Making. J. Bus. Ethics 2016, 138, 327–347. [Google Scholar] [CrossRef]

- EIGD. Statistical Brief: Gender Balance in Corporate Boards 2020. 2021. Available online: https://eige.europa.eu/publications/statistical-brief-gender-balance-corporate-boards-2020 (accessed on 23 March 2022).

- Kirsch, A. The gender composition of corporate boards: A review and research agenda. Leadersh. Q. 2017, 29, 346–364. [Google Scholar] [CrossRef]

- Smith, N. Quota Regulations of Gender Composition on Boards of Directors. DICE Rep. 2004, 12, 42–48. [Google Scholar]

- Kang, H.; Cheng, M.M.; Gray, S. Corporate Governance and Board Composition: Diversity and Independence of Australian Boards. Corp. Gov. Int. Rev. 2007, 15, 194–207. [Google Scholar] [CrossRef]

- Eagly, A.H.; Johannesen-Schmidt, M.C.; Van Engen, M.L. Transformational, Transactional, and Laissez-Faire Leadership Styles: A Meta-Analysis Comparing Women and Men. Psychol. Bull. 2003, 129, 569–591. [Google Scholar] [CrossRef]

- Zelechowski, S.; Bilimoria, D. Characteristics of CEOs and boards with women inside directors. Corp. Board Role Duties Compos. 2006, 2, 14–21. [Google Scholar] [CrossRef]

- Commission. Communication from the Commission—Guidelines on Non-Financial Reporting (Methodology for Reporting Non-Financial Information). 2017. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52017XC0705(01) (accessed on 25 March 2022).

- The University of Cambridge. The Cadbury Report. 2014. Available online: http://cadbury.cjbs.archios.info/report (accessed on 12 April 2022).

- Cosma, S.; Leopizzi, R.; Nobile, L.; Schwizer, P. Revising the non-financial reporting directive and the role of board of directors: A lost opportunity? J. Appl. Account. Res. Emerald Group Hold. 2022, 23, 207–226. [Google Scholar] [CrossRef]

- Nicolo, G.; Zampone, G.; Sannino, G.; De Iorio, S. Sustainable corporate governance and non-financial disclosure in Europe: Does the gender diversity matter? J. Appl. Account. Res. Emerald Group Hold. 2022, 23, 227–249. [Google Scholar] [CrossRef]

- Ministry of Economic Development and Technology of the Republic of Slovenia. Proposal of the Act Amending the Companies Act. 2016. Available online: https://e-uprava.gov.si/drzava-in-druzba/e-demokracija/predlogi-predpisov/predlog-predpisa.html?id=7120 (accessed on 24 March 2022).

- De Roo, K.H. Role of the EU directive on non-financial disclosure in human rights reporting. Eur. Co. Law 2015, 12, 278–285. [Google Scholar] [CrossRef]

- Commission. Study on the Non-Financial Reporting Directive. 2020. Available online: https://op.europa.eu/en/publication-detail/-/publication/1ef8fe0e-98e1-11eb-b85c-01aa75ed71a1/language-en (accessed on 25 March 2022).

- Achim, M.V.; Borea, N.S.; Miron, G.M. Corporate governance, corporate social responsibility and business performances. A global perspective. Economica 2017, 2, 1–9. [Google Scholar]

- Achim, M.V.; Văidean, V.L.; Sabau, A.I.; Safta, I.L. The impact of the quality of corporate governance on sustainable development: An analysis based on development level. Econ. Res. Ekon. Istraž. 2022, 1–30. [Google Scholar] [CrossRef]

- Bell, E.; Willmot, H. Qualitative Research in Business and Management; SAGE Publications Ltd.: Thousand Oaks, CA, USA, 2014. [Google Scholar]

- Yin, R.K. Qualitative Research from Start to Finish; Routledge: London, UK, 2016. [Google Scholar]

| 1. Does the company have a defined diversity policy? |

|---|

| 2. Does the company ensure diversity in its management and supervisory bodies: |

- Sex YES: NO: - Age YES: NO: - Education YES: NO: |

| 3. In what way does the observed company implement a diversity policy? |

| 4. Results of the diversity policy achieved for the reporting period: |

| 5. Does the declaration on diversity policy contain all the required information (adequate, partially adequate, inadequate), describing it in words and illustrating it with concrete examples (see questions 2, 3, and 4 for details)? |

(a) CONSISTENT: (b) PARTIALLY CONSISTENT: (c) INCONSISTENT: |

| 6. Is the diversity policy implemented in the observed company? YES: NO: |

| 7. Suppose the diversity policy is not implemented in the observed company. Is there an explanation of why the company is not implemented (describe in words and illustrate with a concrete example)? |

| 1. Does the Company’s Non-Financial Statement the observed company exist? |

|---|

| YES: NO: |

| 2. Does the company’s Statement of non-financial performance contain all the required information (see answers to questions 3 to 9)? |

(a) CONSISTENT: (b) PARTIALLY CONSISTENT: (c) INCONSISTENT: |

| 3. Does the company’s Statement of non-financial performance disclose information on the following: |

| (a) Environmental YES: NO: (b) Social YES: NO: (c) Human resource matters YES: NO: (d) Respect for human rights; and YES: NO: (e) Anti-corruption and anti-bribery matters YES: NO: |

| 4. Does the company’s Statement of non-financial performance include a brief description of the existing business model? |

| YES: NO: |

| 5. Does the company’s Statement of non-financial performance include a description of the company’s policies on the matters referred to in question 3 (environmental, social, human resources, etc.)? |

| YES: NO: It contains a description of only some of the policies: |

| 6. Does the company’s Statement of non-financial performance include a description of implementing the company’s due diligence procedures to the above policies? |

| YES: NO: |

| 7. Does the company’s Statement of non-financial performance include a description of |

| (a) the results of those policies, YES: NO: (b) the principal risks about those matters associated with the Company’s activities YES: NO: (c) Including, where appropriate and proportionate, the company’s business relationships, products or services that could cause serious adverse effects in those areas; and YES: NO: (d) How the company manages the above risks YES: NO: |

| 8. Does the Company’s Statement of Non-Financial Performance include key non-financial performance indicators relevant to individual activities? (Article 70c(1) of the ZGD-1) |

| YES: NO: |

| 9. If the company under review does not apply any of the above policies, it shall provide a clear and reasoned explanation in the Company’s Statement of Non-Financial Performance. |

| YES: NO: |

| 10. Does the audited company refer to the accounting part of the annual report in its Statement on the Non-Financial Performance of Companies? |

| YES: NO: |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Primec, A.; Belak, J. Sustainable CSR: Legal and Managerial Demands of the New EU Legislation (CSRD) for the Future Corporate Governance Practices. Sustainability 2022, 14, 16648. https://doi.org/10.3390/su142416648

Primec A, Belak J. Sustainable CSR: Legal and Managerial Demands of the New EU Legislation (CSRD) for the Future Corporate Governance Practices. Sustainability. 2022; 14(24):16648. https://doi.org/10.3390/su142416648

Chicago/Turabian StylePrimec, Andreja, and Jernej Belak. 2022. "Sustainable CSR: Legal and Managerial Demands of the New EU Legislation (CSRD) for the Future Corporate Governance Practices" Sustainability 14, no. 24: 16648. https://doi.org/10.3390/su142416648

APA StylePrimec, A., & Belak, J. (2022). Sustainable CSR: Legal and Managerial Demands of the New EU Legislation (CSRD) for the Future Corporate Governance Practices. Sustainability, 14(24), 16648. https://doi.org/10.3390/su142416648