Circular Economy Projects and Firm Disclosures in an Encouraging Institutional Environment

,

,  ,

,  and

and

Abstract

:1. Introduction

2. Theoretical Framework

3. Research Design

3.1. Population and Sample

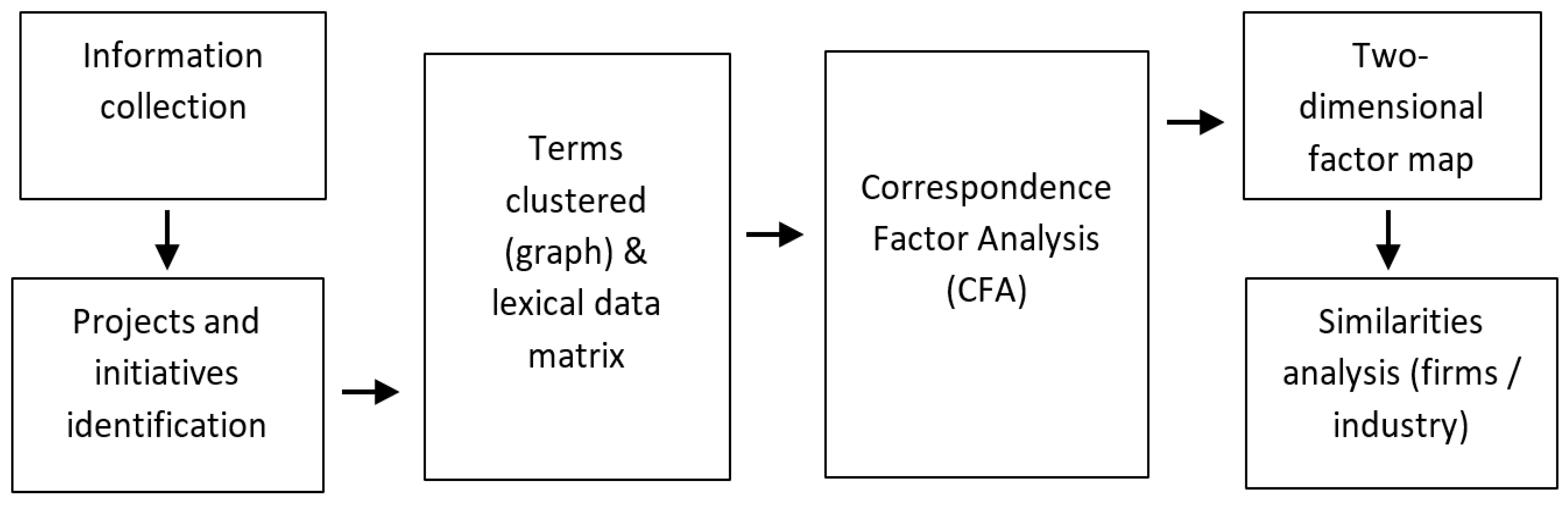

3.2. Methodology

4. Results

4.1. Descriptive Textual Analysis

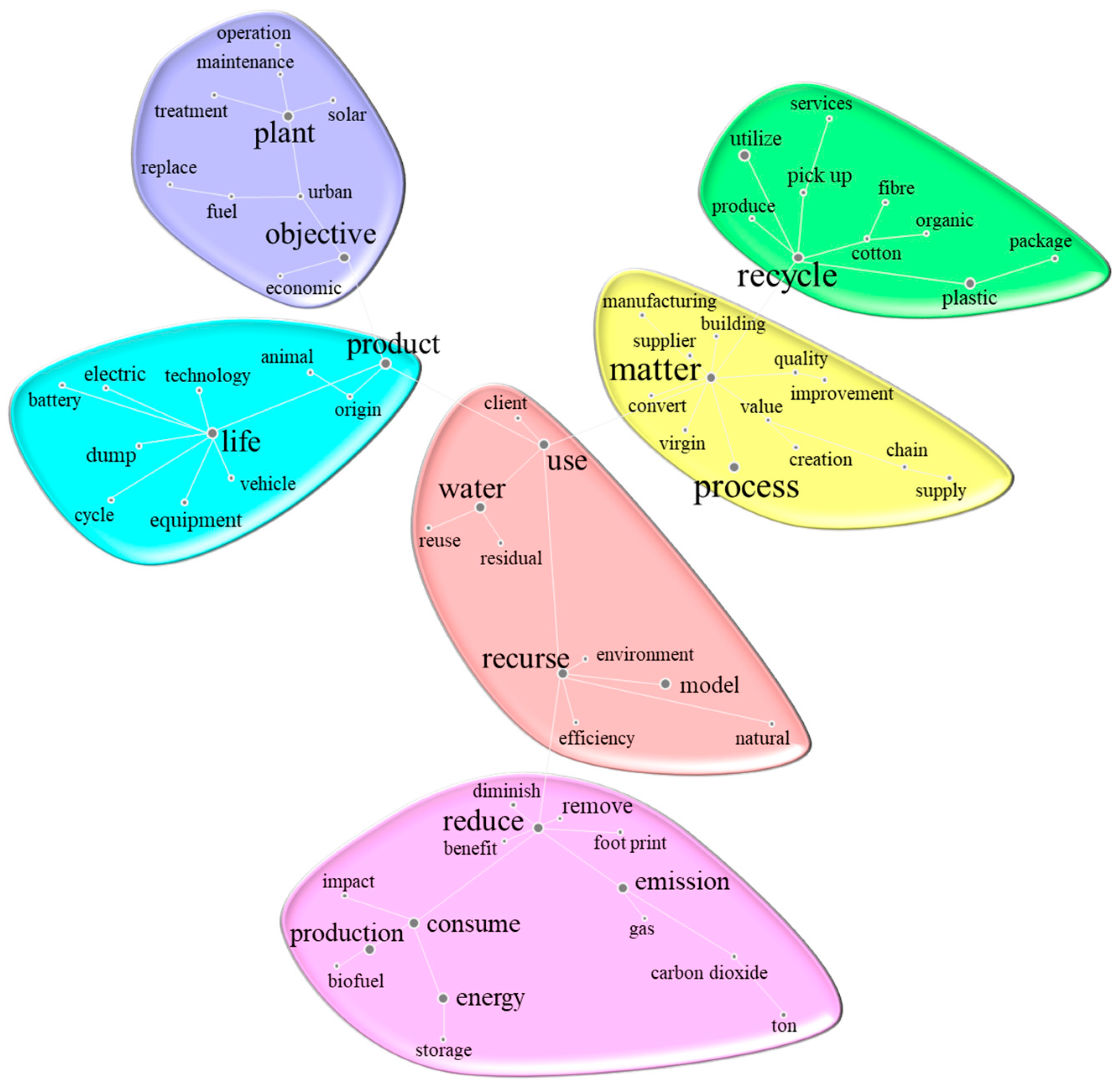

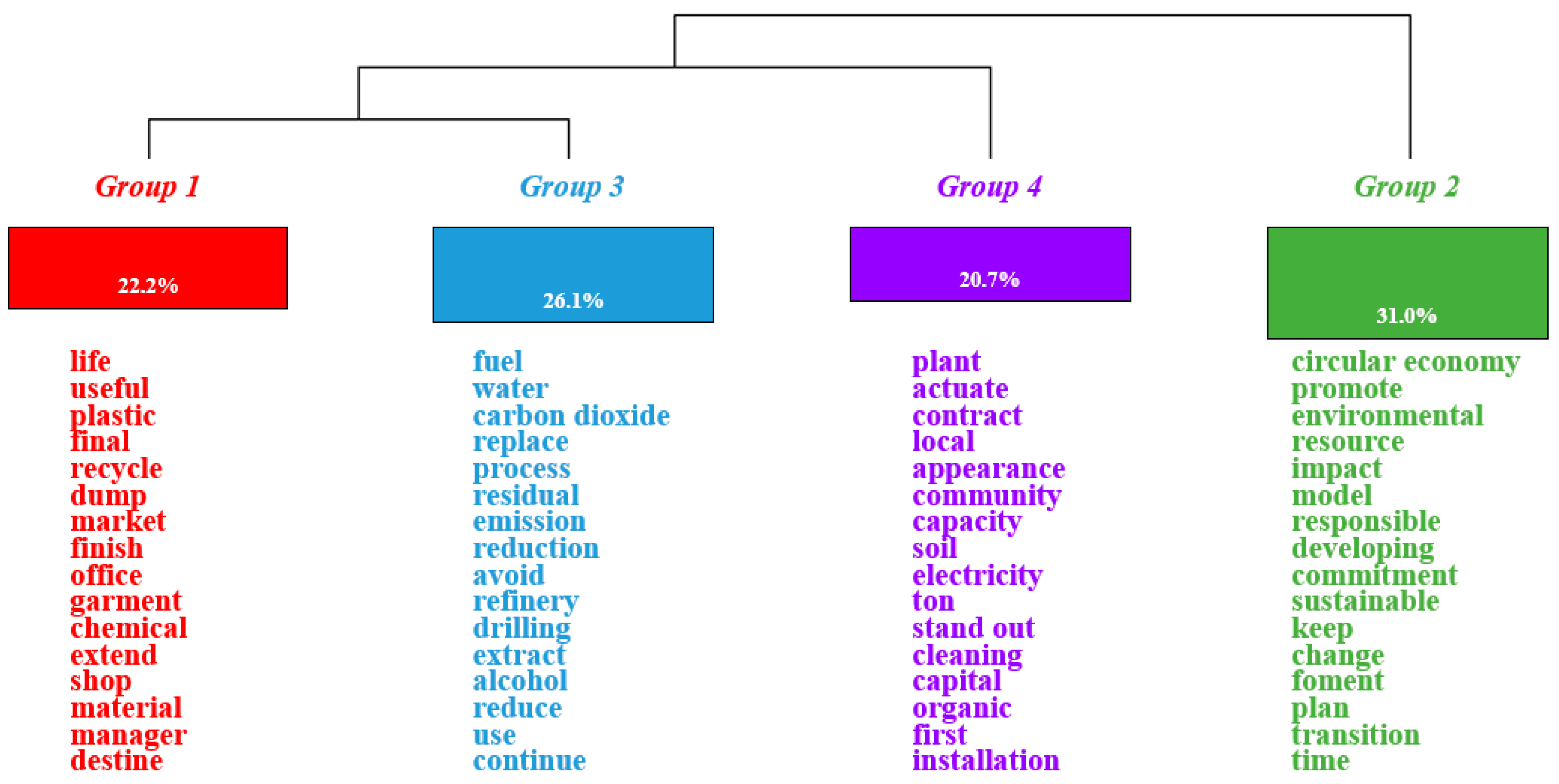

- Red cluster: represents 22.2% of companies’ discourses, focussed on extending the useful life of products, with a notable emphasis on recycling, especially plastic.

- Blue cluster: companies focus 26.1% of their reports on pollution, with the aim of avoiding or reducing gas emissions (carbon dioxide, fuel, refinery, etc.) and favouring processes for prudent water consumption.

- Purple cluster: occupying 20.7% of the reports, this cluster focuses on business actions. There are references to electrical installations, community relations and many references to the management (cleaning) of generated waste.

- Green cluster: companies use 31% of their discourse explaining the importance of the CE for a sustainable future. They focus on the search for a commitment to and the development of sustainable activities, where they prioritise and promote models, make plans to change the environmental impact of their current activities and promote the adequate use of resources over time.

4.2. Analysis of CE Projects

4.3. Business Strategies in CE Reporting

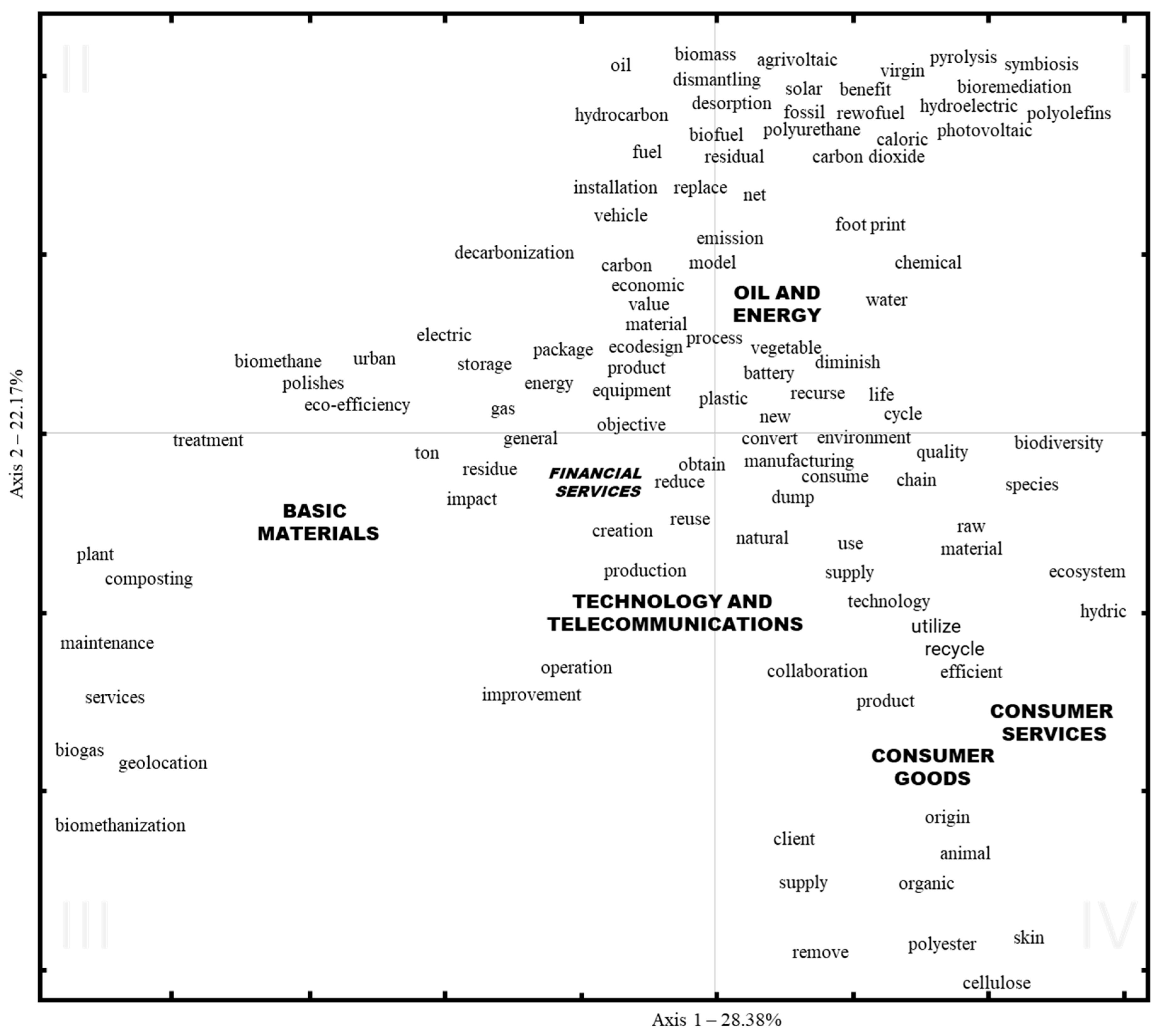

4.4. Industrial Strategies in CE Reporting

- Oil and energy: these companies are environmentally sensitive industries [51]. They focus on the negative effects of emissions and pollution, the footprint left by their actions, carbon dioxide, plastics, chemical agents, vehicles, and so on, but they also comment on their new sustainable processes and models based on the substitution of fuels or methods of generating energy, placing emphasis on eco-design, the use of biofuels, the construction of solar plants, hydroelectric plants, electric vehicles, and others, with the idea of planning tomorrow’s energy transitions today.

- Basic materials: the companies belonging to this sector are environmentally sensitive industries [51] and focus on the impact of the tons of waste produced. Their objective is to treat this waste and reduce and reuse materials before recycling. They speak about the importance of treating plastic containers or the use of alternative energies. An important part of this discourse is directed towards reducing environmental impacts, the treatment and maintenance of gas, switching from biogas to biomethane, the importance of composting and eco-efficiency.

- Financial services: these companies make concise and vague speeches about the CE.

- Technology and telecommunications: these companies talk about improvements in production, creation and transport operations and the search for innovative technologies to help improve global waste management, reduce environmental impact and optimise costs.

- Consumer goods: these companies focus their reports on products. They explain that we live in an age of consumption, anchored to an economic model based on “produce, buy, use, discard” and, in turn, they urge us to move towards a new model where products and raw materials can have a second life without the need to produce new consumer goods. In this way, waste and waste reduction, reuse and recycling result in increased resource efficiency, respecting ecosystems and biodiversity.

- Consumer services: these companies make similar speeches to those of companies in the consumer goods sector, proclaiming the importance of product life. Although they are true, the reports analysed were very concise, with little specific information.

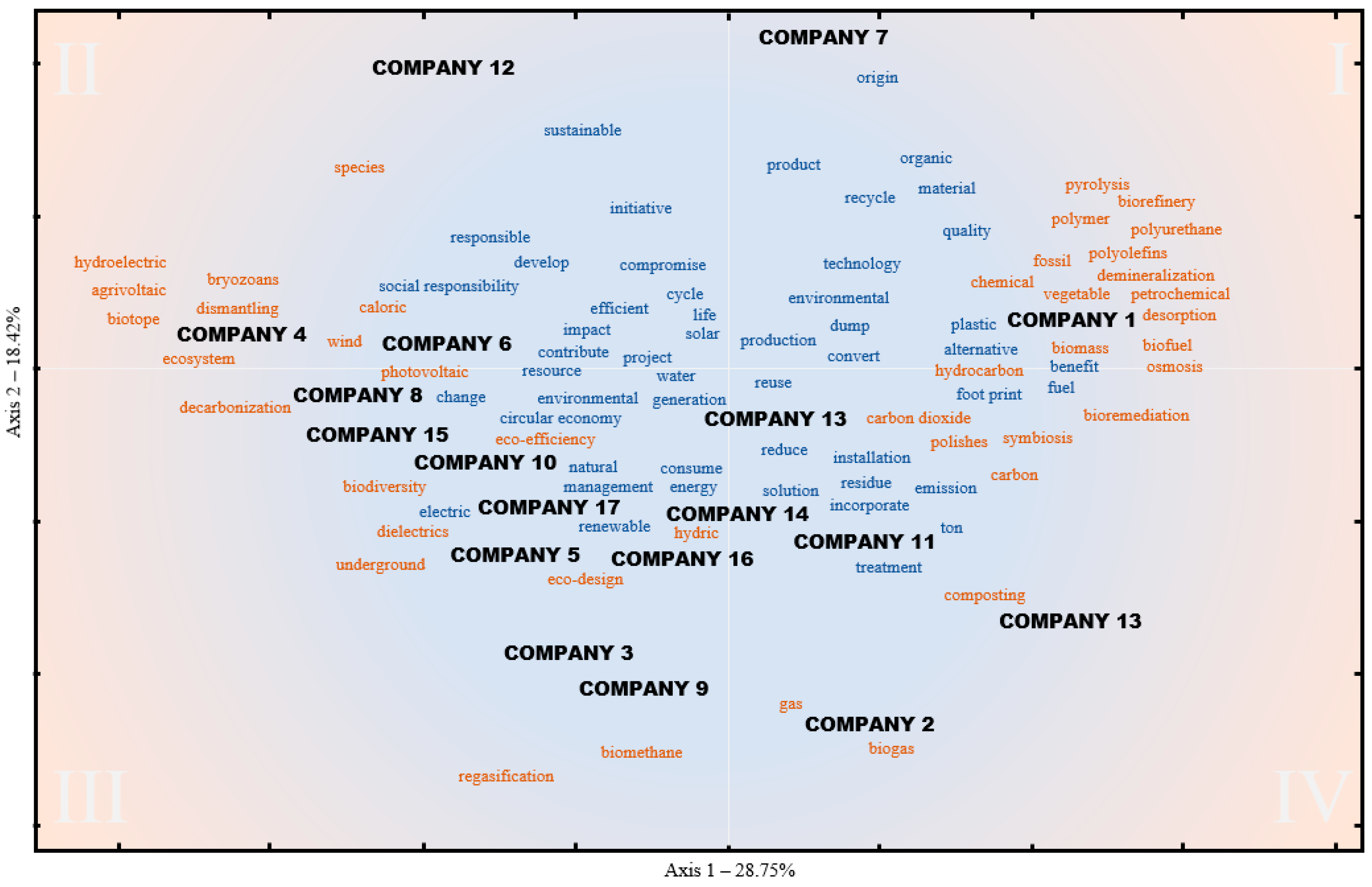

- On the right side of Figure 5, we can see a discourse on the waste and footprint that different emissions, such as carbon dioxide, leave on the road, compared to alternative fuel for the sake of environmental benefit, such as the use of biomass and biofuel. Company 1 stands out in this regard.

- Other discourses, such as that of Company 7, are more closely related to the product, establishing its origin, the quality standards in production, responsible use of material, and everything related to recycling.

- Company 2, Company 3 and Company 9 are the main energy companies, and their speeches are related to biogas or biomethane and regasification.

- Company 4 and Company 6, two large electricity companies in the Spanish energy market, focus on social responsibility and seek to contribute to change, so they promote photovoltaic solar energy and wind energy, refer to decarbonisation and talk about the use of hydroelectric energy and harming any ecosystem (bryozoans, biotope etc.) as little as possible.

- The rest of the companies produce a less specific discourse, where they prioritise the term circular economy, the efficient use of resources and water, and speak of eco-efficiency, biodiversity, ecodesign, etc.

5. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| COMPANY | INDUSTRY | Nº PROJECTS | CE STAGES | DESCRIPTION | CIRCULAR BENEFITS |

|---|---|---|---|---|---|

| COMPANY 1 | Oil and energy | More than 230 CE projects in the different business units. | Efficiency and process innovation, renewable energy and alternative raw materials | FUEL GENERATION FROM URBAN WASTE. Through the use of technology, different waste is heated to high temperatures and in the absence of oxygen, produces gas that can be used to replace traditional fuels. | Remove 10,000 tons per year of urban waste from landfills in the first phase. Remove 100,000 tons of waste per year in the following phases. |

| COMPANY 2 | Basic materials, industry and construction | 13 projects | Reuse | ECOPARK. It is a plant designed and built by Company 2 for the mechanical-biological treatment of solid urban waste to produce biogas and compost that are later converted into energy and fertiliser, respectively. | 10,000 tons per year of garbage from selective collection 35,000 tons per year of dehydrated sludge Biogas generation: 8,900,000 Nm3/year6 composting tunnels with a capacity of 35,000 tons per year |

| COMPANY 3 | Oil and gas | Unknown | Reuse | It is launching a project to take advantage of the cold from liquefied natural gas that allows it to be channelled to refrigeration facilities. | Unknown |

| COMPANY 4 | Oil and gas | 17 Projects in Spain | Reuse | ELECTRIC VEHICLE BATTERIES TO LIGHT UP A CITY. This project is based on an energy storage system using electric vehicle batteries at the City X thermal power plant to guarantee the city’s electricity supply in the event of a power outage. In this way, a second life is being given to the batteries of electric vehicles. | It is a more economical and sustainable alternative to stationary power storage batteries Contributes to improving the quality of supply Extends the life of already spent batteries in electric vehicles |

| COMPANY 5 | Basic materials, industry and construction | Unknown | Reuse | Zero Waste to Landfill project: a project in collaboration with Ford that seeks to reduce the waste that is taken to the landfill to zero by looking for a new location for the waste that is generated. | Unknown |

| COMPANY 6 | Oil and gas | Not available | Ecodesign | Green Hydrogen Plant This project will consist of a photovoltaic solar plant, a lithium-ion battery system and a hydrogen production system through electrolysis. The green hydrogen produced at this plant will be used in Brand’s ammonia factory to produce green fertilisers. | It will avoid emissions of 39,000 tons per year of CO2. It will reduce the plant’s natural gas needs by more than 10%. |

| COMPANY 7 | Consumer goods | Unknown | Reuse and recycle | CLOSING THE LOOP. Installing collection points, mitigating the generation of waste and promoting the reuse of clothing, marketing it for social purposes and recycling for industrial materials. This initiative is carried out through cooperation with nonprofit organisations and research programs in technologies to create new textile fibres from recycled garments. | 100% of the company’s waste is recycled or treated with another environmentally sustainable management method. 1201 million security alarms recycled. 120 million hangers recycled. |

| COMPANY 8 | Financial services | Unknown | Recycle | Company 8 has a Road Safety and Experimentation Centre. This is a global technological centre for the design, insurance, use, maintenance, repair and recycling of vehicles and other solutions for the mobility of goods and people. | Unknown |

| COMPANY 9 | Oil and gas | Unknown | Unknown | Unknown | Unknown |

| COMPANY 10 | Oil and gas | Unknown | Reuse | Obsolete Machines Marketing Project. This project promotes the relocation of power machines that are no longer used in the value chain as resources or raw materials, giving them a second life and preventing them from ending up in a landfill. | Unknown |

| COMPANY 11 | Technology and telecommunications | Unknown | Ecodesign | ECO SMART It is a project of digital solutions for Company 11 client companies that helps them to see their contribution to the environment when they are installed. Based on a 100% renewable and low-emission network to reduce energy, water and CO2 consumption. | 15% reduction in fuel consumption with fleet management services 20% reduction in water consumption in agriculture with Smart Agro 30% reduction in public lighting consumption with Smart Lighting 43% reduction in the average time spent searching for parking with Smart Parking, 26.6% reduction of energy consumption with the Energy Efficiency service and LUCA Energy, 10% reduction in fuel and 85% development of black spots where there is poor waste separation, thanks to Smart Waste |

| COMPANY 12 | Basic materials, industry and construction | Unknown | Unknown | Company 12’s Positive Impact 360º project is a plan approved by the Board of Directors that summarises a series of actions that add value in five main areas: ethical, responsible and transparent governance, eco-efficiency and the fight against climate change, the CE and sustainable products, committed teams, culture, diversity and safety, supply chain and community impact. | Unknown |

| COMPANY 13 (Resulted of the acquisition of one financial company that purchases another outright) | Financial services | Unknown | Reuse and recycle | It carries out a selective collection of waste that allows it to be recovered and recycled both in corporate buildings and in the office network. The comprehensive plan for the revaluation of technology equipment also promotes the transfer of said equipment to nonprofit organisations, and in 2020 this plan was extended to office furniture. | Unknown |

| COMPANY 14 | Technology and telecommunications | Unknown | Consume | Zero Plastic InitiativeThis consists of gradually eliminating single-use plastics in all the entity’s offices. | Unknown |

| COMPANY 15 | Consumer services | Unknown | Unknown | Unknown | Unknown |

| COMPANY 16 | Oil and Gas | Unknown | Unknown | Unknown | Unknown |

| COMPANY 17 | Consumer goods | Unknown | Unknown | Unknown | Unknown |

References

- Yuan, Z.; Bi, J.; Moriguichi, Y. The Circular Economy: A New Development Strategy in China. J. Ind. Ecol. 2013, 2, 23–44. [Google Scholar] [CrossRef] [Green Version]

- Aranda-Usón, A.; Portillo-Tarragona, P.; Scarpellini, S.; Llena-Macarulla, F. The progressive adoption of a circular economy by businesses for cleaner production: An approach from a regional study in Spain. J. Clean. Prod. 2020, 247, 119648. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M.; Raimo, N.; Vitolla, F. Are Environmentally Innovative Companies Inclined towards Integrated Environmental Disclosure Policies? Adm. Sci. 2021, 11, 29. [Google Scholar] [CrossRef]

- Weisz, H.; Krausmann, F.; Amann, C.; Eisenmenger, N.; Erb, K.-H.; Hubacek, K.; Fischer-Kowalski, M. The physical economy of the European Union: Cross-country comparison and determinants of material consumption. Ecol. Econ. 2006, 58, 676–698. [Google Scholar] [CrossRef]

- Preston, F. A global redesign? Shaping the circular economy. Energy Environ. Resour. Gov. 2012, 2, 1–20. [Google Scholar]

- West, J.; Schandl, H.; Krausmann, F.; Kovanda, J.; Hak, T. Patterns of change in material use and material efficiency in the successor states of the former Soviet Union. Ecol. Econ. 2014, 105, 211–219. [Google Scholar] [CrossRef] [Green Version]

- Ranta, V.; Aarikka-Stenroos, L.; Ritala, P.; Mäkinen, S.J. Exploring institutional drivers and barriers of the circular economy: A cross-regional comparison of China, the US, and Europe. Resour. Conserv. Recycl. 2018, 135, 70–82. [Google Scholar] [CrossRef]

- Dong, L.; Dai, M.; Liang, H.; Zhang, N.; Mancheri, N.; Ren, J.; Dou, Y.; Mingming, H. Material flows and resource productivity in China, South Korea and Japan from 1970 to 2008: A transitional perspective. J. Clean. Prod. 2017, 141, 1164–1177. [Google Scholar] [CrossRef]

- Awasthi, A.K.; Cucchiella, F.; D’Adamo, I.; Li, J.; Rosa, P.; Terzi, S.; Wei, G.; Zeng, X. Modelling the correlations of e-waste quantity with economic increase. Sci. Total Environ. 2018, 613 (Suppl. C), 46–53. [Google Scholar] [CrossRef]

- Robaina, M.; Villar, J.; Pereira, E.T. The determinants for a circular economy in Europe. Environ. Sci. Pollut. Res. 2020, 27, 12566–12578. [Google Scholar] [CrossRef]

- Di Maio, F.; Rem, P.C. A robust indicator for promoting circular economy through recycling. J. Environ. Prot. 2015, 6, 1095. [Google Scholar] [CrossRef] [Green Version]

- Smol, M.; Kulczycka, J.; Avdiushchenko, A. Circular economy indicators in Relation to eco-innovation in European regions. Clean Technol. Environ. Policy 2017, 19, 669–678. [Google Scholar] [CrossRef] [Green Version]

- Elia, V.; Gnoni, M.G.; Tornese, F. Measuring circular economy strategies through index methods: A critical analysis. J. Clean. Prod. 2017, 142, 2741–2751. [Google Scholar] [CrossRef]

- Linder, M.; Sarasini, S.; van Loon, P. A Metric for Quantifying Product-Level Circularity. J. Ind. Ecol. 2017, 21, 545–558. [Google Scholar] [CrossRef] [Green Version]

- Katz-Gerro, T.; Sintas, J.L. Mapping circular economy activities in the European Union: Patterns of implementation and their correlates in small and medium-sized enterprises. Bus. Strat. Environ. 2018, 28, 485–496. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M.; Somohano-Rodríguez, F.-M.; Amor-Esteban, V.; Frías-Aceituno, J.-V. Which region and which sector leads the circular economy? CEBIX, a multivariant index based on business actions. J. Environ. Manag. 2021, 297, 113299. [Google Scholar] [CrossRef]

- Moraga, G.; Huysveld, S.; Mathieux, F.; Blengini, G.A.; Alaerts, L.; Van Acker, K.; DeMeester, S.R.; Dewulf, J. Circular economy indicators: What do they measure? Resour. Conserv. Recycl. 2019, 146, 452–461. [Google Scholar] [CrossRef] [PubMed]

- Geissdoerfer, M.; Savaget, P.; Bocken, N.M.; Hultink, E.J. The Circular Economy—A new sustainability paradigm? J. Clean. Prod. 2017, 143, 757–768. [Google Scholar] [CrossRef] [Green Version]

- Gunarathne, N.; Wijayasundara, M.; Senaratne, S.; Kanchana, P.K.; Cooray, T. Uncovering corporate disclosure for a circular economy: An analysis of sustainability and integrated reporting by Sri Lankan companies. Sustain. Prod. Consum. 2021, 27, 787–801. [Google Scholar] [CrossRef]

- Kuo, L.; Chang, B.G. The affecting factors of circular economy information and its impact on corporate economic sustainability-Evidence from China. Sustain. Prod. Consum. 2021, 27, 986–997. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M. Corporate social reporting and assurance: The state of the art. Rev. Contab. 2021, 24, 241–269. [Google Scholar] [CrossRef]

- North, D. Transaction Costs, Institutions, and Economic Performance; ICS Press: San Francisco, CA, USA, 1992. [Google Scholar]

- Walker, K.; Wan, F. The Harm of Symbolic Actions and Green-Washing: Corporate Actions and Communications on Environmental Performance and Their Financial Implications. J. Bus. Ethics 2011, 109, 227–242. [Google Scholar] [CrossRef] [Green Version]

- Dagiliene, L.; Frendzel, M.; Sutiene, K.; Wnuk-Pel, T. Wise managers think about circular economy, wiser report and analyze it. Research of environmental reporting practices in EU manufacturing companies. J. Clean. Prod. 2020, 274, 121968. [Google Scholar] [CrossRef]

- Ramus, C.A.; Montiel, I. When are corporate environmental policies a form of greenwashing? Bus. Soc. 2005, 44, 377–414. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling Theory: A Review and Assessment. J. Manag. 2010, 37, 39–67. [Google Scholar] [CrossRef]

- Delmas, M.A. The diffusion of environmental management standards in Europe and in the United States: An institutional perspective. Policy Sci. 2002, 35, 91–119. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M.; Amor-Esteban, V.; Galindo-Álvarez, D. Communication Strategies for the 2030 Agenda Commitments: A Multivariate Approach. Sustainability 2020, 12, 10554. [Google Scholar] [CrossRef]

- Tate, W.L.; Dooley, K.J.; Ellram, L.M. Transaction cost and institutional drivers of supplier adoption of environmental practices. J. Bus. Logist. 2011, 32, 6–16. [Google Scholar] [CrossRef]

- Parra-Domínguez, J.; David, F.; Azevedo, T. Family Firms and Coupling among CSR Disclosures and Performance. Adm. Sci. 2021, 11, 30. [Google Scholar] [CrossRef]

- Boulding, K.E. The Economics of the Coming Spaceship Earth; Taylor & Francis: New York, NY, USA, 1966. [Google Scholar]

- Ellen MacArthur Foundation. Towards a Circular Economy: Business Rationale for an Accelerated Transition. 2015. Available online: www.ellenmacarthurfoundation.org (accessed on 1 July 2021).

- Zeng, H.; Chen, X.; Xiao, X.; Zhou, Z. Institutional pressures, sustainable supply chain management, and circular economy capability: Empirical evidence from Chinese eco-industrial park firms. J. Clean. Prod. 2017, 155, 54–65. [Google Scholar] [CrossRef]

- Oliver, C. Strategic responses to institutional processes. Acad. Manag. Rev. 1991, 16, 145–179. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar]

- Scott, W.R. The adolescence of institutional theory. Adm. Sci. Q. 1987, 32, 493–511. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Molina-Azorín, J.F. Microfoundations of strategic management: Toward micro-macro research in the resource-based theory. BRQ Bus. Res. Q. 2014, 17, 102–114. [Google Scholar] [CrossRef]

- Daddi, T.; Todaro, N.M.; De Giacomo, M.R.; Frey, M. A Systematic Review of the Use of Organization and Management Theories in Climate Change Studies. Bus. Strat. Environ. 2018, 27, 456–474. [Google Scholar] [CrossRef]

- Aibar-Guzmán, B.; Frías-Aceituno, J.-V. Is It Necessary to Centralize Power in the CEO to Ensure Environmental Innovation? Adm. Sci. 2021, 11, 27. [Google Scholar] [CrossRef]

- Aibar-Guzmán, C.; Somohano-Rodríguez, F.M. Do Consumers Value Environmental Innovation in Product? Adm. Sci. 2021, 11, 33. [Google Scholar] [CrossRef]

- Pérez-Calderón, E.; Pache-Durán, M.; Milanés-Montero, P. Inversión ecoeficiente: Efectos sobre el desempeño económico y financiero de los grupos empresariales del Dow Jones Sustainability World Index. Rev. Contab. 2021, 24, 220–230. [Google Scholar] [CrossRef]

- Widmer, T.; Prior, D. Institutional Isomorphism, Institutional Logics and Organisational Fields: An Institutionalist Perspective on Circular Economy. In Proceedings of the Spring Servitization, Linköping, Sweden, 13–15 May 2019. [Google Scholar]

- Escobar, L.F.; Vredenburg, H. Multinational oil companies and the adoption of sustainable development: A resource-based and institutional theory interpretation of adoption heterogeneity. J. Bus. Ethics 2011, 98, 39–65. [Google Scholar] [CrossRef]

- Amran, A.; Ooi, S.K.; Wong, C.Y.; Hashim, F. Business strategy for climate change: An ASEAN perspective. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 213–227. [Google Scholar] [CrossRef]

- Wahyuni, D.; Ratnatunga, J. Carbon strategies and management practices in an uncertain carbonomic environment—Lessons learned from the coal-face. J. Clean. Prod. 2015, 96, 397–406. [Google Scholar] [CrossRef]

- Liu, Q.; Li, H.M.; Zuo, X.L.; Zhang, F.F.; Wang, L. A survey and analysis on public awareness and performance for promoting circular economy in China: A case study from Tianjin. J. Clean. Prod. 2009, 17, 265–270. [Google Scholar] [CrossRef]

- Elzinga, R.; Reike, D.; Negro, S.O.; Boon, W.P. Consumer acceptance of circular business models. J. Clean. Prod. 2020, 254, 119988. [Google Scholar] [CrossRef]

- Bag, S.; Pretorius, J.H.C.; Gupta, S.; Dwivedi, Y.K. Role of institutional pressures and resources in the adoption of big data analytics powered artificial intelligence, sustainable manufacturing practices and circular economy capabilities. Technol. Forecast. Soc. Chang. 2020, 163, 120420. [Google Scholar] [CrossRef]

- Radu, C.; Smaili, N. Corporate performance patterns of Canadian listed firms: Balancing financial and corporate social responsibility outcomes. Bus. Strat. Environ. 2021, 30, 3344–3359. [Google Scholar] [CrossRef]

- BS 8001:2017—Framework for Implementing the Principles of the Circular Economy in Organizations. Guide. Available online: www.aenor.com (accessed on 23 September 2021).

- Etzion, D.; Pe’Er, A. Mixed signals: A dynamic analysis of warranty provision in the automotive industry, 1960–2008. Strat. Manag. J. 2013, 35, 1605–1625. [Google Scholar] [CrossRef] [Green Version]

- Scott, W.R. Institutions and Organizations: Ideas, Interests, and Identities; Sage Publications: Thousand Oaks, CA, USA, 2013. [Google Scholar]

- Bocken, N.M.P.; Short, S.W.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef] [Green Version]

- Teece, D.J. Technological innovation and the theory of the firm: The role of enterprise-level knowledge, complementarities, and (dynamic) capabilities. In Handbook of the Economics of Innovation, 1st ed.; Elsevier B.V.: Amsterdam, The Netherlands, 2010; Volume 1. [Google Scholar]

- Milios, L. Advancing to a circular economy: Three essential ingredients for a comprehensive policy mix. Sustain. Sci. 2018, 13, 861–878. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Benner, M.J.; Tushman, M.L. Exploitation, exploration, and process management: The productivity dilemma revisited. Acad. Manag. Rev. 2003, 28, 238–256. [Google Scholar] [CrossRef] [Green Version]

- Jalonen, H. The uncertainty of innovation: A systematic review of the literature. J. Manag. Res. 2011, 4, 1. [Google Scholar] [CrossRef] [Green Version]

- Berthiaume, A. Use of the National Pollutant Release Inventory in environmental research: A scoping review. Environ. Rev. 2021, 29, 329–339. [Google Scholar] [CrossRef]

- Reverte, C. Corporate social responsibility disclosure and market valuation: Evidence from Spanish listed firms. Rev. Manag. Sci. 2014, 10, 411–435. [Google Scholar] [CrossRef]

- Li, Y.; Richardson, G.D.; Thornton, D.B. Corporate disclosure of environmental liability information: Theory and evidence. Contemp. Acc. Res. 1997, 14, 435–474. [Google Scholar] [CrossRef]

- Karahanna, E.; Straub, D.W.; Chervany, N.L. Information Technology Adoption Across Time: A Cross-Sectional Comparison of Pre-Adoption and Post-Adoption Beliefs. MIS Q. 1999, 23, 183. [Google Scholar] [CrossRef]

- Rogers, E.M. Evolution: Diffusion of Innovations. In International Encyclopedia of the Social & Behavioral Sciences, 2nd ed.; Wright, J.D., Ed.; Elsevier: Oxford, UK, 2015; pp. 378–381. [Google Scholar]

- Luhmann, N. Social Systems; Stanford University Press: Stanford, CA, USA, 1995. [Google Scholar]

- Melón-Izco, Á.; Ruiz-Cabestre, F.J.; Ruiz-Olalla, C. Readabilty in management reports: Extension and good governance practices. Rev. Contab. 2021, 24, 19–30. [Google Scholar] [CrossRef]

- Hadro, D.; Klimczak, K.M.; Pauka, M. Management’s choice of tone in letters to shareholders: Sincerity, bias and incentives. Rev. Contab. 2021, 24, 202–219. [Google Scholar] [CrossRef]

- Reinert, M. Système Alceste: Une méthodologie d’analyse des données textuelles. Actes Jornades Int. D’analisi Dades Textuals 1991, 44–161. [Google Scholar]

- Benzécri, J.P. L’analyse des Données; Dunod: Paris, France, 1973; Volume 2, p. 1. [Google Scholar]

- Zarbà, C.; Chinnici, G.; La Via, G.; Bracco, S.; Pecorino, B.; D’Amico, M. Regulatory Elements on the Circular Economy: Driving into the Agri-Food System. Sustainability 2021, 13, 8350. [Google Scholar] [CrossRef]

| Industry | Freq. | % |

|---|---|---|

| Consumer goods | 2 | 11.8% |

| Basic materials, industry and construction | 3 | 17.6% |

| Oil and energy | 7 | 41.2% |

| Consumer services | 1 | 5.8% |

| Financial services | 2 | 11.8% |

| Technology and telecommunications | 2 | 11.8% |

| Total | 17 | 100% |

| Level 0 | Freq. | Level 1 | Freq. | Level 2 | Freq. | |||

|---|---|---|---|---|---|---|---|---|

| 1 | Water | 9 | 1 | Residual | 51 | 1 | Residual | 147 |

| 2 | Consume | 9 | 2 | Objective | 22 | 2 | Raw material | 108 |

| 3 | Residual | 8 | 3 | Recurse | 17 | 3 | Life | 48 |

| 4 | Emission | 8 | 4 | Use | 15 | 4 | New | 48 |

| 5 | Reduce | 6 | 5 | Material | 15 | 5 | Use | 43 |

| 6 | Energy | 6 | 6 | Electronic | 13 | 6 | Water | 43 |

| 7 | Carbon dioxide | 6 | 7 | Equipment | 13 | 7 | Reduce | 42 |

| 8 | Efficiency | 5 | 8 | Recycle | 12 | 8 | Product | 42 |

| 9 | Recurse | 4 | 9 | Consume | 11 | 9 | Recycle | 41 |

| 10 | Model | 4 | 10 | Model | 11 | 10 | Process | 40 |

| 11 | Impact | 4 | 11 | Generation | 11 | 11 | Recurse | 37 |

| 12 | Gas | 4 | 12 | Net | 11 | 12 | Material | 37 |

| 13 | Environment | 4 | 13 | Product | 11 | 13 | Objective | 36 |

| 14 | Use | 3 | 14 | Raw Material | 10 | 14 | Plant | 36 |

| 15 | Generate | 3 | 15 | Process | 9 | 15 | Plastic | 33 |

| 16 | Natural | 3 | 16 | Life | 9 | 16 | Energy | 31 |

| 17 | Foot Print | 3 | 17 | Natural | 8 | 17 | Reuse | 28 |

| 18 | Biodiversity | 3 | 18 | Building | 8 | 18 | Pick up | 25 |

| 19 | Material | 2 | 19 | Value | 8 | 19 | Production | 24 |

| 20 | Plant | 2 | 20 | Reduce | 7 | 20 | Ton | 24 |

| 21 | Building | 2 | 21 | Impact | 7 | 21 | Consume | 23 |

| 22 | Production | 2 | 22 | Pick Up | 7 | 22 | Model | 22 |

| 23 | Ton | 2 | 23 | Dump | 7 | 23 | Building | 22 |

| 24 | Ecoeffiency | 2 | 24 | New | 6 | 24 | Emission | 22 |

| 25 | Hydric | 2 | 25 | Plastic | 6 | 25 | Service | 22 |

| 26 | Raw material | 2 | 26 | Economic | 6 | 26 | Produce | 22 |

| 27 | Objective | 1 | 27 | Ecodesign | 6 | 27 | Urban | 22 |

| 28 | Recycle | 1 | 28 | Gas | 5 | 28 | Technology | 22 |

| 29 | Process | 1 | 29 | Reuse | 5 | 29 | Fuel | 22 |

| 30 | Production | 1 | 30 | Chain | 5 | 30 | Dump | 21 |

| 31 | Urban | 1 | 31 | Use | 5 | 31 | Animal | 21 |

| 32 | Technology | 1 | 32 | Maintenance | 5 | 32 | Obtain | 20 |

| 33 | Reuse | 1 | 33 | Water | 4 | 33 | Quality | 20 |

| 34 | Origen | 1 | 34 | Efficiency | 4 | 34 | Cotton | 19 |

| 35 | Treatment | 1 | 35 | Services | 4 | 35 | Electric | 17 |

| 36 | Organic | 1 | 36 | Energy | 3 | 36 | Carbon dioxide | 17 |

| 37 | Solar | 1 | 37 | Treatment | 3 | 37 | Origin | 17 |

| 38 | Client | 1 | 38 | Oil | 3 | 38 | Manufacturing | 17 |

| 39 | Chain | 1 | 39 | Operation | 3 | 39 | Generate | 16 |

| 40 | Creation | 1 | 40 | Convert | 3 | 40 | Equipment | 16 |

| 41 | Net | 1 | 41 | Dangerous | 3 | 41 | Value | 16 |

| 42 | Collaboration | 1 | 42 | Plant | 2 | 42 | Use | 16 |

| 43 | Remove | 1 | 43 | Production | 2 | 43 | Treatment | 16 |

| 44 | Residual | 1 | 44 | Produce | 2 | 44 | Organic | 16 |

| 45 | Storage | 1 | 45 | Origin | 2 | 45 | Vehicle | 16 |

| 46 | Supply | 1 | 46 | Client | 2 | 46 | Cycle | 15 |

| 47 | Species | 1 | 47 | Creation | 2 | 47 | Benefit | 15 |

| 48 | Symbiosis | 1 | 48 | Collaboration | 2 | 48 | Solar | 15 |

| 49 | Photovoltaic | 1 | 49 | Remove | 2 | 49 | Package | 15 |

| 50 | Biomethane | 1 | 50 | Residual | 2 | 50 | Efficiency | 14 |

| 51 | Ecosystem | 1 | 51 | Supply | 2 | 51 | Economic | 14 |

| 52 | Life | 0 | 52 | Biomethane | 2 | 52 | Supplier | 14 |

| 53 | New | 0 | 53 | Obtain | 2 | 53 | Biofuel | 14 |

| 54 | Product | 0 | 54 | Cycle | 2 | 54 | Foot print | 13 |

| 55 | Plastic | 0 | 55 | Diminish | 2 | 55 | Fibre | 13 |

| 56 | Use | 0 | 56 | Improvement | 2 | 56 | Battery | 13 |

| 57 | Pick up | 0 | 57 | Decarbonisation | 2 | 57 | Garments | 13 |

| 58 | Electric | 0 | 58 | Underground | 2 | 58 | Oil | 12 |

| 59 | Equipment | 0 | 59 | Regasification | 2 | 59 | Client | 12 |

| 60 | Dump | 0 | 60 | Emissions | 1 | 60 | Operation | 12 |

| Level | Level 0 | Level 1 | Level 2 |

|---|---|---|---|

| Average words | 211 | 393 | 2254 |

| % Numbers | 1.7% | 1.4% | 1.7% |

| % Techniques | 4.9% | 3.5% | 6.2% |

| CEO training | |||

| % Engineers or chemists (CEO) | 50.0% | 37.5% | 50.0% |

| % Lawyers (CEO) | 0.0% | 25.0% | 16.7% |

| % Economists and managers (CEO) | 50.0% | 33.3% | 33.3% |

| Board member training | |||

| % Male | 72.4% | 68.0% | 70.1% |

| Total with training information (M) | 7 | 9 | 8 |

| % Engineers or chemists (M) | 35.9% | 19.4% | 21.9% |

| % Lawyers (M) | 25.1% | 28.4% | 30.9% |

| % Economists and managers (M) | 39.0% | 52.2% | 47.1% |

| % Female | 27.6% | 32.0% | 29.9% |

| Total with training information (F) | 3 | 4 | 3 |

| % Engineers or chemists (F) | 25.0% | 23.8% | 15.0% |

| % Lawyers (F) | 6.3% | 23.8% | 18.6% |

| % Economists and managers (F) | 68.8% | 52.5% | 66.4% |

| Total Board Members | 10 | 14 | 12 |

| Sectors | Consumer Goods | Basic Materials | Oil and Energy | Consumer Services | Financial Services | Technology and Telecom |

|---|---|---|---|---|---|---|

| Average words | 1195 | 785 | 1561 | 185 | 187 | 545 |

| % Numbers | 1.1% | 1.5% | 1.8% | 0.0% | 1.7% | 2.1% |

| % Techniques | 5.3% | 6.4% | 4.9% | 7.0% | 2.7% | 2.8% |

| CEO training | ||||||

| % Engineers or chemists (CEO) | 0.0% | 66.7% | 85.7% | 0.0% | 0.0% | 0.0% |

| % Lawyers (CEO) | 50.0% | 0.0% | 0.0% | 0.0% | 33.3% | 50.0% |

| % Economists and managers (CEO) | 50.0% | 33.3% | 14.3% | 100.0% | 66.7% | 50.0% |

| Board member training | ||||||

| % Male | 61.8% | 76.8% | 72.7% | 70.0% | 63.9% | 65.1% |

| Total with training information (M) | 7 | 8 | 7 | 7 | 10 | 10 |

| % Engineers or chemists (M) | 12.5% | 20.4% | 33.5% | 28.6% | 16.7% | 15.6% |

| % Lawyers (M) | 32.5% | 16.2% | 29.2% | 42.9% | 36.7% | 21.1% |

| % Economists and managers (M) | 55.0% | 63.4% | 37.3% | 28.6% | 46.7% | 63.3% |

| % Female | 38.2% | 23.2% | 27.3% | 30.0% | 36.1% | 34.9% |

| Total with training information (F) | 4 | 3 | 3 | 3 | 4 | 5 |

| % Engineers or chemists (F) | 25.0% | 16.7% | 20.7% | 0.0% | 25.0% | 30.0% |

| % Lawyers (F) | 29.2% | 0.0% | 18.3% | 0.0% | 33.3% | 20.0% |

| % Economists and managers (F) | 45.8% | 83.3% | 61.0% | 100.0% | 41.7% | 50.0% |

| Board Members | 11 | 11 | 11 | 10 | 16 | 15 |

| Average Level | 1.0 | 1.3 | 1.1 | 0.0 | 1.0 | 1.5 |

| Level 0 | 50.0% | 0.0% | 28.6% | 100.0% | 0.0% | 0.0% |

| Level 1 | 0.0% | 66.7% | 28.6% | 0.0% | 100.0% | 50.0% |

| Level 2 | 50.0% | 33.3% | 42.9% | 0.0% | 0.0% | 50.0% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

García-Sánchez, I.-M.; Somohano-Rodríguez, F.-M.; Amor-Esteban, V.; Gonzalez-Valdueza, B. Circular Economy Projects and Firm Disclosures in an Encouraging Institutional Environment. Sustainability 2022, 14, 1149. https://doi.org/10.3390/su14031149

García-Sánchez I-M, Somohano-Rodríguez F-M, Amor-Esteban V, Gonzalez-Valdueza B. Circular Economy Projects and Firm Disclosures in an Encouraging Institutional Environment. Sustainability. 2022; 14(3):1149. https://doi.org/10.3390/su14031149

Chicago/Turabian StyleGarcía-Sánchez, Isabel-María, Francisco-Manuel Somohano-Rodríguez, Víctor Amor-Esteban, and Benito Gonzalez-Valdueza. 2022. "Circular Economy Projects and Firm Disclosures in an Encouraging Institutional Environment" Sustainability 14, no. 3: 1149. https://doi.org/10.3390/su14031149

APA StyleGarcía-Sánchez, I. -M., Somohano-Rodríguez, F. -M., Amor-Esteban, V., & Gonzalez-Valdueza, B. (2022). Circular Economy Projects and Firm Disclosures in an Encouraging Institutional Environment. Sustainability, 14(3), 1149. https://doi.org/10.3390/su14031149