An Analysis of the Relationship between Energy Trilemma and Economic Growth

Abstract

:1. Introduction

2. Literature Review

3. Methodology and Data

3.1. World Energy Trilemma Index (WETI) and Current Situation

3.2. Model of Energy Trilemma with Economic Growth

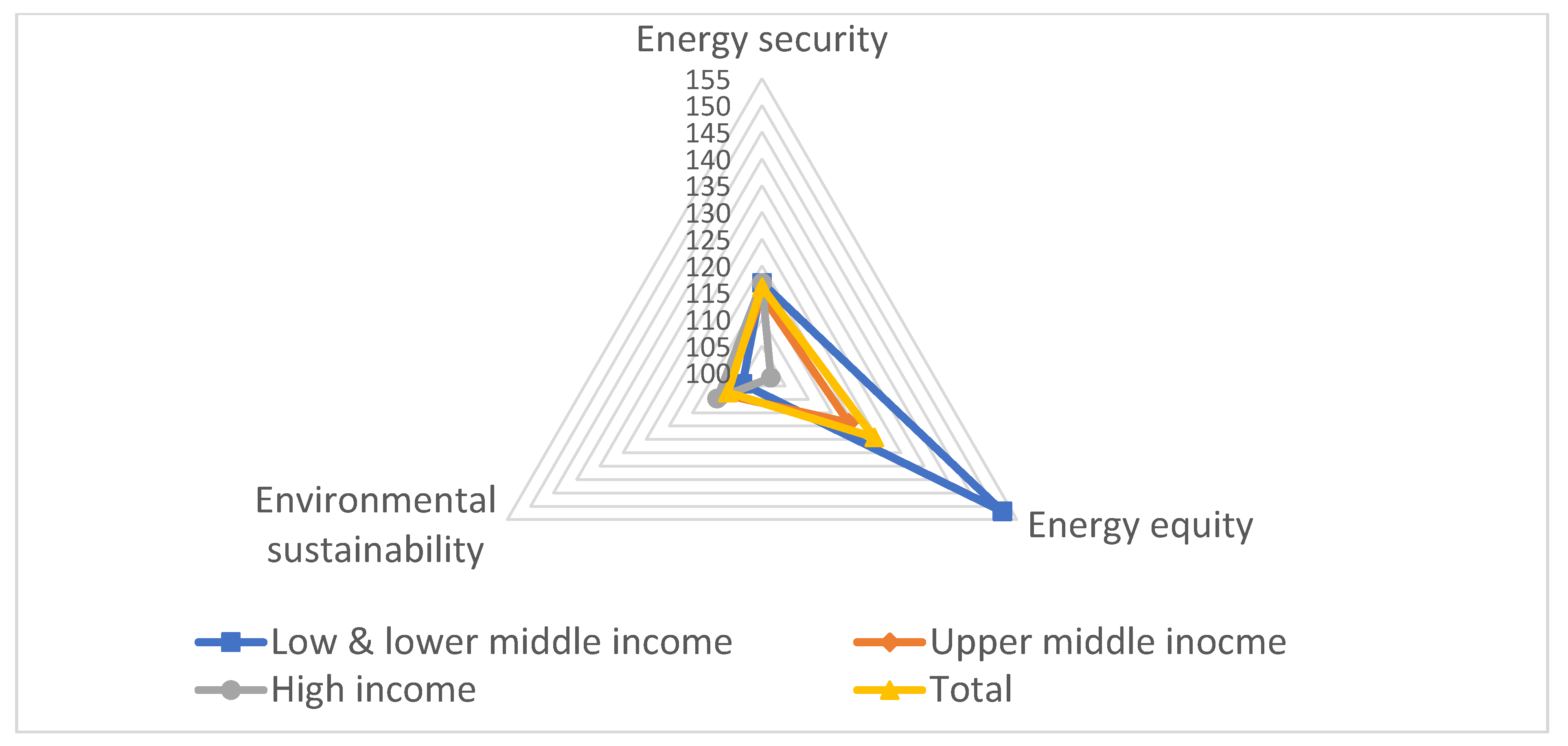

3.3. Descriptive Data

4. Empirical Results

4.1. Panel Analysis Results

4.2. Time Series Analysis Results

5. Conclusions and Implications

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

Appendix A. Estimation Results of Simple Relationship (Time Series Analysis)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | ln(ES) | ln(EE) | ln(ESUS) | R2 | |||

|---|---|---|---|---|---|---|---|

| Coefficient | t−Value | Coefficient | t−Value | Coefficient | t−Value | ||

| Algeria | 0.64 | 1.66 | 0.22 | 1.3 | −0.35 | −1.2 | 0.98 |

| Angola | −0.26 | −0.92 | 5.49 ** | 2.21 | −0.81 * | −2.1 | 0.97 |

| Bangladesh | 0.16 * | 2.12 | 0.02 | 0.79 | 0.02 | 0.46 | 0.99 |

| Benin | 0.21 | 1.74 | −0.03 | −1.67 | −0.01 | −0.47 | 0.99 |

| Bolivia | 0.71 | 1.06 | 0.33 | 1.2 | −0.22 | −0.79 | 0.98 |

| Cambodia | 0.10 * | 1.88 | −0.20 ** | −2.24 | −0.03 | −0.29 | 0.99 |

| Cameroon | 0.07 | 0.97 | 0.03 | 0.6 | 0.03 | 0.73 | 0.99 |

| Chad | 1.45 | 1.5 | 0.28 | 1.27 | −0.93 *** | −3.13 | 0.94 |

| Congo | −0.15 | −0.26 | −0.09 | −0.56 | −0.44 | −0.95 | 0.98 |

| Cote d’Ivoire | 0.38 | 0.91 | 0.41 ** | 2.54 | −0.5 | −1.11 | 0.98 |

| Egypt | 0.21 | 0.36 | 0.58 *** | 3.27 | 0.22 | 0.94 | 0.98 |

| El Salvador | −0.06 | −0.42 | 0.15 | 0.97 | 0.67 *** | 3.21 | 0.96 |

| Eswatini | −0.05 | −0.58 | 1.07 ** | 2.96 | 0.16 ** | 2.36 | 0.99 |

| Ethiopia | −0.11 | −0.33 | 0.12 ** | 2.15 | −0.02 | −0.07 | 0.99 |

| Ghana | 0.1 | 0.71 | 0.16 | 0.76 | −0.15 | −0.87 | 0.99 |

| Honduras | −0.46 * | −2.12 | 0.1 | 0.58 | 0.13 | 0.59 | 0.97 |

| India | −0.12 | −0.09 | 0.2 | 1.46 | −0.34 | −0.95 | 0.99 |

| Indonesia | −0.62 | −1.34 | 0.33 ** | 2.25 | −0.57 * | −1.97 | 0.99 |

| Iran | −0.2 | −0.08 | 0.47 * | 2.14 | −0.04 | −0.14 | 0.95 |

| Kenya | 0.28 ** | 2.8 | −0.05 | −1.45 | 0.23 ** | 2.5 | 0.99 |

| Madagascar | 0.03 | 0.11 | 0.08 | 1.35 | −0.29 * | −1.78 | 0.98 |

| Mauritania | 1.43 | 0.67 | −0.1 | −0.87 | −0.07 | −0.18 | 0.97 |

| Mongolia | −1.21 | −0.87 | 0.56 ** | 2.33 | −0.51 | −1.28 | 0.98 |

| Morocco | 0.28 ** | 2.31 | 0.37 *** | 4.41 | −0.04 | −0.1 | 0.99 |

| Mozambique | −0.99 *** | −3.89 | 0.21 ** | 2.19 | −0.03 | −0.13 | 0.98 |

| Nepal | −0.11 | −1.01 | 0.05 | 1.06 | −0.24 ** | −2.79 | 0.99 |

| Nicaragua | 0.13 * | 1.98 | −0.02 | −0.5 | −0.33 ** | −2.83 | 0.99 |

| Niger | 0.28 *** | 4.98 | 0.02 | 1.16 | −0.20 *** | −6.56 | 0.99 |

| Nigeria | 0.02 | 0.02 | −0.01 | −0.13 | 1.25 *** | 3.2 | 0.96 |

| Pakistan | −0.06 | −0.98 | 0.02 | 0.62 | −0.06 | −0.63 | 0.99 |

| Philippines | −0.31 | −0.46 | −0.05 | −0.24 | −0.43 | −1.46 | 0.99 |

| Senegal | −0.03 | −0.71 | 0.04 | 1.25 | −0.07 | −0.85 | 0.99 |

| Sri Lanka | −0.33 | −1.57 | 0.38 *** | 5.14 | −0.01 | −0.05 | 0.99 |

| Tanzania | −0.08 | −1.65 | 0.06 * | 1.85 | −0.11 | −1.59 | 0.99 |

| Tunisia | −0.36 | −1.04 | 0.16 | 0.58 | 0.17 | 0.64 | 0.97 |

| Ukraine | −0.25 | −0.63 | 1.53 *** | 4.44 | 0.51 | 1.32 | 0.86 |

| Vietnam | −0.05 | −0.32 | 0.51 *** | 6.76 | 0.03 | 0.43 | 0.99 |

| Country | ln(ES) | ln(EE) | ln(ESUS) | R2 | |||

|---|---|---|---|---|---|---|---|

| Coefficient | t−Value | Coefficient | t−Value | Coefficient | t−Value | ||

| Albania | 0.51 *** | 3.19 | 1.44 *** | 3.60 | 0.32 | 1.43 | 0.97 |

| Argentina | −0.03 | −0.06 | 0.20 | 1.00 | −0.91 ** | −2.79 | 0.98 |

| Armenia | −1.39 | −1.70 | 2.31 *** | 3.68 | 0.49 | 0.63 | 0.91 |

| Bosnia and Herzegovina | −0.90 * | −2.11 | 0.60 | 1.29 | −0.30 * | −1.98 | 0.92 |

| Botswana | 0.46 | 0.75 | 0.78 | 0.99 | 0.07 | 0.41 | 0.98 |

| Brazil | 0.24 * | 2.13 | 0.04 | 0.65 | −0.12 | −1.42 | 0.99 |

| Bulgaria | 0.04 | 0.15 | 0.87 | 1.43 | 0.17 | 0.28 | 0.91 |

| China | 1.32 ** | 2.22 | 0.78 *** | 3.27 | 0.12 | 1.30 | 0.99 |

| Colombia | 0.09 | 0.32 | −0.14 | −0.62 | 0.13 | 0.50 | 0.98 |

| Costa Rica | −0.53 * | −1.84 | 0.06 | 0.30 | −0.19 | −0.59 | 0.99 |

| Dominican Rep | 0.01 | 0.03 | 0.11 | 1.01 | 0.30 *** | 3.87 | 0.99 |

| Ecuador | 0.10 | 0.21 | 0.10 | 0.31 | −0.41 * | −1.92 | 0.98 |

| Gabon | 0.29 | 1.55 | 0.54 | 1.69 | −0.27 * | −1.91 | 0.98 |

| Guatemala | 0.41 * | 1.94 | 0.28 | 1.67 | 0.30 ** | 2.65 | 0.99 |

| Jamaica | −0.11 | −1.39 | 0.02 | 0.14 | −0.02 | −0.15 | 0.68 |

| Jordan | 0.25 *** | 3.32 | 0.33 | 1.70 | 0.58 ** | 2.44 | 0.99 |

| Kazakhstan | −0.01 | −0.01 | 0.48 * | 2.05 | 0.20 | 1.21 | 0.99 |

| Lebanon | −0.12 | −1.42 | 0.70 *** | 7.05 | 0.12 | 1.45 | 0.99 |

| Malaysia | 0.67 *** | 3.92 | 0.26 | 1.49 | 0.01 | 0.04 | 0.99 |

| Mauritius | −0.01 | −0.09 | −0.09 | −0.38 | 0.06 | 0.49 | 0.99 |

| Mexico | −0.06 | −0.20 | 0.17 * | 2.04 | 0.05 | 0.22 | 0.98 |

| Moldova | −0.06 | −0.27 | 0.21 | 0.96 | 0.61 | 1.63 | 0.96 |

| Montenegro | 0.61 ** | 2.76 | −0.22 | −0.34 | 0.03 | 0.12 | 0.92 |

| Namibia | −0.02 | −0.07 | 0.04 | 0.03 | −0.03 | −0.10 | 0.98 |

| North Macedonia | 0.05 | 0.24 | −0.01 | −0.03 | 0.03 | 0.16 | 0.98 |

| Panama | −0.02 | −0.10 | 0.20 | 0.81 | −0.28 | −1.25 | 0.99 |

| Paraguay | 0.40 | 0.82 | 0.37 | 1.31 | −0.05 | −0.34 | 0.98 |

| Peru | 0.75 | 1.65 | 0.87 *** | 4.36 | 0.46 ** | 2.17 | 0.99 |

| Romania | 0.91 *** | 3.60 | 0.61 ** | 2.66 | −0.32 | −1.09 | 0.97 |

| Russia | −0.74 | −0.88 | 1.06 *** | 4.98 | 0.09 | 0.21 | 0.98 |

| Serbia | −0.40 | −0.42 | −0.77 | −1.07 | −0.12 | −0.41 | 0.90 |

| South Africa | 0.29 ** | 2.69 | 0.45 *** | 3.37 | 0.12 | 1.01 | 0.98 |

| Country | ln(ES) | ln(EE) | ln(ESUS) | R2 | |||

|---|---|---|---|---|---|---|---|

| Coefficient | t−Value | Coefficient | t−Value | Coefficient | t−Value | ||

| Austria | −0.21 ** | −2.27 | 0.18 | 0.22 | 0.07 | 0.56 | 0.98 |

| Bahrain | 0.70 *** | 5.28 | 4.48 ** | 2.59 | 0.02 | 0.18 | 0.99 |

| Belgium | 0.11 | 1.46 | −0.95 ** | −2.42 | 0.05 | 0.48 | 0.98 |

| Brunei | 0.26 | 1.18 | −0.40 | −1.60 | −0.22 | −0.82 | 0.73 |

| Canada | 0.16 | 1.28 | −0.21 | −0.31 | 0.36 ** | 2.60 | 0.99 |

| Chile | 0.02 | 0.14 | 0.20 | 1.42 | 0.31 | 1.70 | 0.99 |

| Cyprus | 0.06 | 1.43 | 1.91 *** | 3.67 | −0.03 | −0.33 | 0.99 |

| Czech Rep | 0.24 | 0.99 | 0.93 | 1.74 | 0.40 * | 1.84 | 0.98 |

| Denmark | 0.22 * | 1.91 | −0.86 | −1.07 | 0.24 *** | 4.01 | 0.98 |

| Estonia | 0.13 | 0.87 | 1.78 *** | 4.27 | −0.10 | −0.71 | 0.98 |

| Finland | −0.31 | −1.32 | −0.60 | −1.10 | −0.02 | −0.19 | 0.94 |

| France | 0.01 | 0.24 | −0.11 | −0.30 | −0.10 | −0.79 | 0.98 |

| Germany | 0.28 ** | 2.26 | −0.48 | −0.78 | −0.13 | −0.92 | 0.97 |

| Greece | 0.03 | 0.16 | −0.03 | −0.07 | 0.54 ** | 2.62 | 0.96 |

| Hungary | −0.08 | −0.47 | 1.36 ** | 2.39 | 0.78 *** | 3.02 | 0.96 |

| Iceland | 1.59 *** | 3.70 | 6.68 * | 1.78 | −0.05 | −0.26 | 0.98 |

| Israel | −0.01 | −0.17 | −0.61 | −1.60 | 0.07 | 1.54 | 0.99 |

| Italy | −0.05 | −1.10 | 0.34 | 1.24 | 0.08 | 0.70 | 0.92 |

| Japan | 0.17 *** | 3.26 | −0.42 | −1.06 | −0.32 ** | −2.95 | 0.97 |

| Korea Rep | −0.27 | −1.48 | 0.24 | 0.36 | 0.15 | 1.24 | 0.99 |

| Latvia | 0.58 | 1.46 | −0.02 | −0.02 | −0.33 | −0.40 | 0.90 |

| Lithuania | 0.10 | 0.29 | 1.42 | 1.17 | −0.22 | −0.38 | 0.93 |

| Luxembourg | 0.09 | 0.88 | −10.29 | −0.84 | −0.44 ** | −2.35 | 0.97 |

| Malta | 0.01 | 0.01 | −0.14 | −0.20 | −0.14 | −0.34 | 0.98 |

| Netherland | −0.19 | −1.30 | 0.19 | 0.11 | 0.19 | 1.36 | 0.96 |

| New Zealand | 0.01 | 0.14 | 0.07 | 0.23 | 0.16 | 1.56 | 0.99 |

| Norway | −0.45 ** | −2.30 | 0.21 | 0.31 | 0.12 | 1.07 | 0.98 |

| Oman | 0.21 | 1.14 | −0.28 | −1.30 | 0.15 | 1.64 | 0.99 |

| Poland | 0.45 | 1.07 | −0.48 | −0.82 | −0.17 | −0.44 | 0.98 |

| Portugal | 0.23 *** | 3.24 | −0.41 | −1.08 | −0.01 | −0.16 | 0.90 |

| Saudi Arabia | 0.11 | 0.45 | −0.18 | −0.78 | −0.03 | −0.26 | 0.99 |

| Slovak Rep | 0.63 | 1.42 | −2.14 | −1.09 | 1.07 | 1.41 | 0.94 |

| Slovenia | 1.49 ** | 2.95 | 0.04 | 0.08 | 0.43 | 1.48 | 0.96 |

| Spain | 0.02 | 0.15 | −0.68 | −1.38 | 0.43 * | 1.79 | 0.96 |

| Sweden | −0.65 | −1.45 | 0.25 | 0.04 | 0.19 | 1.25 | 0.98 |

| Switzerland | −0.11 | −0.57 | −2.19 | −1.41 | 0.08 | 0.39 | 0.99 |

| United Arab Emirates | −1.33 *** | −5.11 | 0.91 ** | 2.37 | −0.47 ** | −2.15 | 0.98 |

| United Kingdom | 0.03 | 0.23 | 2.12 | 1.76 | −0.18 | −0.79 | 0.98 |

| United States | −0.02 | −0.29 | −0.61 | −0.89 | 0.15 | 1.22 | 0.99 |

| Uruguay | 0.42 *** | 3.65 | 0.05 | 0.42 | 0.35 *** | 3.30 | 0.99 |

Appendix B

| Region | (+) ES | (−) ES | (+) EE | (−) EE | (+) ESUS | (−) ESUS | |

|---|---|---|---|---|---|---|---|

| Africa | Northern Africa | Morocco | Egypt, Morocco | ||||

| Sub-Saharan Africa | |||||||

| (1) Middle Africa | Angola | Chad, Angola, Gabon | |||||

| (2) Eastern Africa | Kenya | Mozambique | Ethiopia, Mozambique, Tanzania | Kenya | Madagascar | ||

| (3) Western Africa | Niger | Côte d’Ivoire | Nigeria | Niger | |||

| (4) Southern Africa | South Africa | Eswatini, South Africa | Eswatini | ||||

| Number of country (% of full sample country) | 4 (3.67%) | 1 (0.92%) | 9 (8.26%) | 0 | 3 (2.75%) | 5 (4.59%) | |

| Asia | Central Asia | Kazakhstan | |||||

| Eastern Asia | China, Japan | Mongolia, China | Japan | ||||

| South-eastern Asia | Cambodia, Malaysia | Indonesia, Vietnam | Cambodia | Indonesia | |||

| Southern Asia | Bangladesh | Iran, Sri Lanka | Nepal | ||||

| Western Asia | Jordan, Bahrain | United Arab Emirates | Armenia, Lebanon Bahrain, Cyprus United Arab Emirates | Jordan | United Arab Emirates | ||

| Number of country (% of full sample country) | 7 (6.42%) | 1 (0.92%) | 12 (11.01%) | 1 (0.92%) | 1 (0.92%) | 4 (3.67%) | |

| Americas | Caribbean | Dominican, Republic | |||||

| Central America | Nicaragua, Guatemala | Honduras, Costa Rica | Mexico | El Salvador, Guatemala | Nicaragua | ||

| Northern America | Canada | ||||||

| South America | Brazil, Uruguay | Peru | Peru, Uruguay | Argentina, Ecuador | |||

| Number of country (% of full sample country) | 4 (3.67%) | 2 (1.83%) | 2 (1.83%) | 0 | 6 (5.5%) | 3 (2.75%) | |

| Europe | Eastern Europe | Romania | Austria | Ukraine, Romania, Russia, Hungary | Czech, Hungary | ||

| Northern Europe | Denmark, Iceland | Norway | Estonia, Iceland | Denmark | |||

| Southern Europe | Albania, Montenegro Portugal, Slovenia | Bosnia and Herzegovina | Albania | Greece, Spain | Bosnia and Herzegovina | ||

| Western Europe | Germany | Belgium | Luxembourg | ||||

| Number of country (% of full sample country) | 8 (7.34%) | 3 (2.75%) | 7 (6.42) | 1 (0.92%) | 5 (4.59%) | 2 (1.83%) | |

References

- International Energy Agency (IEA). World Energy Outlook. 2020. Available online: https://www.iea.org/reports/world-energy-outlook-2020 (accessed on 5 January 2022).

- Oliver, J.; Sovacool, B. The energy trilemma and the smart grid: Implications beyond the United State. Asia Pac. Policy Stud. 2017, 4, 70–84. [Google Scholar] [CrossRef]

- Ekins, P. Economic Growth and Environmental Sustainability: The Prospects for Green Growth; Routledge: London, UK, 1999. [Google Scholar]

- Le, T.H.; Nguyen, C.P. Is energy security a driver for economic growth? Evidence from a global sample. Energy Policy 2019, 129, 436–451. [Google Scholar] [CrossRef]

- Demaria, F. Why Economic Growth is not Compatible with Environmental Sustainability, Ecologist. 2018. Available online: https://theecologist.org/2018/feb/22/why-economic-growth-not-compatible-environmental-sustainability (accessed on 20 January 2022).

- Khan, I.; Hou, F.; Irfan, M.; Zakari, A.; Le, H.P. Does energy trilemma a driver of economic growth? The roles of energy use, population growth, and financial development. Renew. Sustain. Energy Rev. 2021, 146, 111157. [Google Scholar] [CrossRef]

- Grigoryev, L.M.; Medzhidova, D.D. Global energy trilemma. Russ. J. Econ. 2020, 6, 437–462. [Google Scholar] [CrossRef]

- Asghar, Z. Energy-GDP relationship: A causal analysis for the five countries of South Asia. Appl. Econom. Int. Dev. 2008, 8, 915. Available online: https://ssrn.com/abstract=1308260 (accessed on 20 January 2022).

- Sharma, S.S. The relationship between energy and economic growth: Empirical evidence from 66 countries. Appl. Energy 2010, 87, 3565–3574. [Google Scholar] [CrossRef]

- Ayres, R.U.; van den Bergh, J.C.J.M.; Lindenberger, D.; Warr, B. The underestimated contribution of energy to economic growth. Struct. Chang. Econ. Dyn. 2013, 27, 79–88. [Google Scholar] [CrossRef]

- Gasparatos, A.; Gadda, T. Environmental support, energy security and economic growth in Japan. Energy Policy 2009, 37, 4038–4048. [Google Scholar] [CrossRef]

- Qasim Alabed, Q.M.; Said, F.F.; Abdul Karim, Z.; Shah Zaidi, M.A.; Alshammary, M.D. Energy–Growth Nexus in the MENA Region: A Dynamic Panel Threshold Estimation. Sustainability 2021, 13, 12444. [Google Scholar] [CrossRef]

- Ozturk, I.; Aslan, A.; Kalyoncu, H. Energy consumption and economic growth relationship: Evidence from panel data for low and middle income countries. Energy Policy 2010, 38, 4422–4428. [Google Scholar] [CrossRef]

- Szustak, G.; Dabrowski, P.; Gradon, W.; Szewczyk, Ł. The Relationship between Energy Production and GDP: Evidence from Selected European Economies. Energies 2022, 15, 50. [Google Scholar] [CrossRef]

- Ullah, S.; Khan, M.; Yoon, S.-M. Measuring Energy Poverty and Its Impact on Economic Growth in Pakistan. Sustainability 2021, 13, 10969. [Google Scholar] [CrossRef]

- Myszczyszyn, J.; Supron, B. Relationship among Economic Growth (GDP), Energy Consumption and Carbon Dioxide Emission: Evidence from V4 Countries. Energies 2021, 14, 7734. [Google Scholar] [CrossRef]

- Ziolo, M.; Jednak, S.; Savić, G.; Kragulj, D. Link between Energy Efficiency and Sustainable Economic and Financial Development in OECD Countries. Energies 2020, 13, 5898. [Google Scholar] [CrossRef]

- Chien, T.; Hu, L.J. Renewable energy: An efficient mechanism to improve GDP. Energy Policy 2008, 36, 3045–3052. [Google Scholar] [CrossRef]

- Akram, R.; Chen, F.; Khalid, F.; Ye, Z.; Majeed, M.T. Heterogeneous effects of energy efficiency and renewable energy on carbon emissions: Evidence from developing countries. J. Clean. Prod. 2020, 247, 119122. [Google Scholar] [CrossRef]

- Ekins, P.; Jacobs, M. Environmental sustainability and the growth of GDP: Conditions for compatibility. In The North the South and the Environment: Ecological Constraints and Global Economy; Bhaskar, V., Glyn, A., Eds.; Earthscan: New York, NY, USA, 1995; pp. 9–46. [Google Scholar]

- Stjepanović, S.; Tomic, D.; Skare, M. A new approach to measuring green GDP: A cross-country analysis. Entrep. Sustain. 2017, 4, 574–590. [Google Scholar] [CrossRef]

- Fu, F.Y.; Alharthi, M.; Bhatti, Z.; Sun, L.; Rasul, F.; Hanif, I.; Iqbal, W. The dynamic role of energy security, energy equity and environmental sustainability in the dilemma of emission reduction and economic growth. J. Environ. Manag. 2021, 280, 111828. [Google Scholar] [CrossRef]

- Asbahi, A.A.M.H.A.; Gang, F.Z.; Iqbal, W.; Abass, Q.; Mohsin, M.; Iram, R. Novel approach of Principal Component Analysis method to assess the national energy performance via Energy Trilemma Index. Energy Rep. 2019, 5, 704–713. [Google Scholar] [CrossRef]

- Babamoradi, H.; van den Berg, F.; Rinnan, A. Bootstrap based confidence limits in principal component analysis: A case study. Chemom. Intell. Lab. Syst. 2013, 120, 97–105. [Google Scholar] [CrossRef]

- Mohammed, M.S.H.; Alhawsawi, A.; Soliman, A.Y. An Integrated Approach to the Realization of Saudi Arabia’s Energy Sustainability. Sustainability 2021, 13, 205. [Google Scholar] [CrossRef]

- Barnes, D.F.; Floor, W.M. Rural energy in developing countries: A challenge for economic development. Annu. Rev. Energy Environ. 1996, 21, 497–530. [Google Scholar] [CrossRef]

- Hanna, R.; Oliva, P. 2 Moving up the energy ladder: The effect of an increase in economic well-being on the fuel consumption choices of the poor in India. Am. Econ. Rev. 2015, 105, 242–246. [Google Scholar] [CrossRef] [Green Version]

- Stern, D.I.; Cleveland, C.J. Energy and Economic Growth; Rensselaer Working Papers in Economics; Department of Economics, Rensselaer Polytechnic Institute: Troy, NY, USA, 2004. [Google Scholar]

- Mahmood, T.; Ayaz, M.T. Energy security and economic growth in Pakistan. Pak. J. Appl. Econ. 2018, 28, 47–64. [Google Scholar]

- Dovis, M.; Milgram-Baleix, J. Trade, tariff and total factor productivity: The case of Spanish firms. World Econ. 2009, 32, 575–605. [Google Scholar] [CrossRef] [Green Version]

- Arellano, M.; Bond, S. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equation. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef] [Green Version]

- Blundell, R.; Bond, S. GMM estimation with persistent panel data: An application to production function. Econom. Rev. 2000, 19, 321–340. [Google Scholar] [CrossRef] [Green Version]

- Radmehr, R.; Henneberry, S.R.; Shaynmehr, S. Renewable energy consumption, CO2 emissions, and economic growth nexus: A simultaneity spatial modeling analysis of EU countries. Struct. Chang. Econ. Dyn. 2021, 57, 13–27. [Google Scholar] [CrossRef]

- Hundie, S.K.; Daksa, M.D. Does energy-environmental Kuznets curve hold for Ethiopia? The relationship between energy intensity and economic growth. J. Econ. Struct. 2019, 8, 1–21. [Google Scholar] [CrossRef]

- Zhang, J.; Alharthi, M.; Abbas, Q.; Li, W.; Mohsin, M.; Jamal, K.; Taghizadeh-Hesary, F. Reassessing the environmental Kuznets curve in relation to energy efficiency and economic growth. Sustainability 2020, 12, 8346. [Google Scholar] [CrossRef]

- Kim, S.; Baek, J.; Heo, E. A new look at the democracy–environment nexus: Evidence from panel data for high- and low-Income countries. Sustainability 2019, 11, 2353. [Google Scholar] [CrossRef] [Green Version]

- Khanm, I.; Zakari, A.; Zhang, J.; Dagar, V.; Singh, S. A study of trilemma energy balance, clean energy transitions, and economic expansion in the midst of environmental sustainability: New insights from three trilemma leadership. Energy 2022, 248, 123619. [Google Scholar] [CrossRef]

| Dimension | Definition | Indicator Category | Indicator |

|---|---|---|---|

| Energy security | Reflects a nation’s capacity to meet current and future energy demand reliably, withstand and bounce back swiftly from system shocks with minimal disruption to supplies | A1: Security of supply and energy demand | a: Diversity of primary energy supply |

| b: Import dependence | |||

| A2: Resilience of energy systems | a: Diversity of electricity generation | ||

| b: Energy storage | |||

| c: System stability and recovery capacity | |||

| Energy equity | Assesses a country’s ability to provide universal access to affordable, fairly priced and abundant energy for domestic and commercial use | B1: Energy access | a: access to electricity |

| b: access to clean cooking | |||

| B2: Quality energy access | a: access to “modern” energy | ||

| B3: Affordability | a: Electricity prices | ||

| b: Gasoline and diesel prices | |||

| c: Natural gas prices | |||

| d: Affordability of electricity for residents | |||

| Environmental sustainability | Represents the transition of a country’s energy system towards mitigating and avoiding potential environmental harm and climate change impacts | C1: Energy resource productivity | a: Final energy intensity |

| b: Efficiency of power generation and T&D | |||

| C2: Decarbonization | a: Low carbon electricity generation | ||

| b: GHG emissions trend | |||

| C3: Emissions and pollution | a: CO2 intensity | ||

| b: CO2 emissions per capita | |||

| c: CH4 emissions per capita | |||

| d: PM2.5 mean annual exposure | |||

| e: PM10 mean annual exposure |

| Top five overall performers and improvers | |||||||

| Rank | Performers | Improvers | |||||

| Country | Score | Country | Improvement since 2000 | ||||

| 1 | Switzerland | 84.3 | Cambodia | 77% | |||

| 2 | Sweden | 84.2 | Myanmar | 50% | |||

| 3 | Denmark | 84.0 | Kenya | 41% | |||

| 4 | Austria | 82.1 | Bangladesh | 38% | |||

| 5 | Finland | 82.1 | Honduras | 36% | |||

| Top five energy trilemma performers | |||||||

| Rank | Energy Security | Energy Equity | Environmental Sustainability | ||||

| Country | Score | Country | Score | Country | Score | ||

| 1 | Canada | 77.1 | Luxembourg | 99.9 | Switzerland | 90.0 | |

| 2 | Finland | 75.4 | Qatar | 99.8 | Sweden | 87.5 | |

| 3 | Romania | 74.5 | Kuwait | 99.8 | Norway | 87.2 | |

| 4 | Denmark | 74.4 | UAE | 99.8 | Albania | 85.8 | |

| 5 | Latvia | 74.1 | Oman | 99.7 | France | 85.5 | |

| Hypothesis | Meaning and Policy Implication |

|---|---|

| Neutrality | -No relationship between energy consumption and output a particular nation -Neither conservative nor established expansive energy policies have any effect on economic output |

| Growth hypothesis | -Unidirectional causality from energy use to economic output -Any regulations on the amount of energy to be consumed will have an effect on the overall growth and development |

| Conservation hypothesis | -Unidirectional causality from economic output to energy consumption -Approach to reduce the energy demand has little or no impact at all on economic output |

| Feedback hypothesis | -Bidirectional causality between energy use and economic growth -Both variables are inseparable as each one of them has simultaneous impact on the other |

| Variable | Definition (Units) | Source |

|---|---|---|

| GDP | GDP constant 2015 (US $) | World Bank Open Data (https://data.worldbank.org/, (accessed on 20 January 2022)) |

| L | Labor force (total) | |

| K | Gross capital formation constant 2015 (US $) | |

| T | Trade (% of GDP) | |

| ES | Energy security index (2000 = 100) | World Energy Council Energy Trilemma Index (https://trilemma.worldenergy.org/#!/energy-index, (accessed on 20 January 2022)) |

| EE | Energy equity index (2000 = 100) | |

| ESUS | Environmental sustainability index (2000 = 100) |

| Income Levels | Country | Number |

|---|---|---|

| Low-income countries ($1045 or less by GNI per capita) | Chad, Congo, Dem. Rep, Ethiopia, Madagascar, Mozambique, Niger | 6 |

| Lower middle-income countries ($1046 to $4095 by GNI per capita) | Angola, Algeria, Bangladesh, Benin, Bolivia, Cambodia, Cameroon, Cote d’Ivoire, Egypt, El Salvador, Eswatini, Ghana, Honduras, India, Indonesia, Iran, Kenya, Mauritania, Mongolia, Morocco, Nepal, Nicaragua, Nigeria, Pakistan, Philippines, Senegal, Sri Lanka, Tanzania, Tunisia, Ukraine, Vietnam | 31 |

| Upper middle-income countries ($4096 to $12,695 by GNI per capita) | Albania, Argentina, Armenia, Bosnia and Herzegovina, Botswana, Brazil, Bulgaria, China, Colombia, Costa Rica, Dominican Rep, Ecuador, Gabon, Guatemala, Jamaica, Jordan, Kazakhstan, Lebanon, Malaysia, Mauritius, Mexico, Moldova, Montenegro, Namibia, North Macedonia, Panama, Paraguay, Peru, Romania, Russia, Serbia, South Africa | 32 |

| High income countries ($12,696 or more by GNI per capita) | Austria, Bahrain, Belgium, Brunei, Canada, Chile, Cyprus, Czech Rep, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Israel, Italy, Japan, Korea Rep, Latvia, Lithuania, Luxembourg, Malta, Netherland, New Zealand, Norway, Oman, Poland, Portugal, Saudi Arabia, Slovak Rep, Slovenia, Spain, Sweden, Switzerland, United Arab Emirates, United Kingdom, United States, Uruguay | 40 |

| Total | 109 | |

| GDP | L | K | T | ES | EE | ESUS | |||

|---|---|---|---|---|---|---|---|---|---|

| Full sample (N = 2289, n = 109, T = 21) | Mean | 84.17 | 105.12 | 110.40 | 104.12 | ||||

| Std. Dev. | Overall | 45.53 | 13.02 | 22.75 | 9.10 | ||||

| Between | 43.40 | 7.96 | 16.08 | 6.85 | |||||

| Within | 3,951,747 | 14.35 | 10.33 | 16.16 | 6.02 | ||||

| Min | Overall | 156,006 | 19.55 | 75.04 | 48.54 | 59.63 | |||

| Between | 188,832.2 | 26.21 | 88.98 | 80.42 | 79.76 | ||||

| Within | − | − | − | 19.85 | 74.22 | 9.10 | 82.66 | ||

| Max | Overall | 380.10 | 213.43 | 310.53 | 135.19 | ||||

| Between | 390.29 | 130.90 | 201.30 | 121.46 | |||||

| Within | 154.98 | 196.84 | 219.63 | 125.49 | |||||

| Low & lower middle income countries (N = 777, n = 37, T = 21) | Mean | 69.43 | 104.95 | 121.54 | 101.97 | ||||

| Std. Dev. | Overall | 31.90 | 12.83 | 34.05 | 9.50 | ||||

| Between | 29.21 | 8.05 | 21.95 | 7.24 | |||||

| Within | 5,705,248 | 13.64 | 10.06 | 26.26 | 6.25 | ||||

| Min | Overall | 290,519 | 20.72 | 82.25 | 48.54 | 59.63 | |||

| Between | 328,115.3 | 30.23 | 92.15 | 80.42 | 79.76 | ||||

| Within | − | − | − | 23.31 | 75.16 | 20.23 | 81.84 | ||

| Max | Overall | 211.49 | 197.92 | 310.53 | 127.38 | ||||

| Between | 157.53 | 129.78 | 201.30 | 117.56 | |||||

| Within | 133.87 | 173.79 | 230.76 | 122.21 | |||||

| Upper-middle income countries (N = 672, n = 32, T = 21) | Mean | 78.59 | 104.75 | 109.30 | 104.34 | ||||

| Std. Dev. | Overall | 32.50 | 12.42 | 11.51 | 9.33 | ||||

| Between | 29.66 | 8.38 | 7.41 | 7.04 | |||||

| Within | 3,683,355 | 14.22 | 9.28 | 8.90 | 6.24 | ||||

| Min | Overall | 234,186 | 21.85 | 75.04 | 88.12 | 74.84 | |||

| Between | 250,806 | 26.21 | 91.61 | 97.30 | 86.51 | ||||

| Within | − | −2,403,450 | 20.34 | 73.84 | 82.71 | 82.87 | |||

| Max | Overall | 220.40 | 193.23 | 147.73 | 135.19 | ||||

| Between | 165.18 | 130.90 | 124.12 | 121.46 | |||||

| Within | 133.82 | 167.07 | 132.91 | 125.71 | |||||

| High income countries (N = 840, n = 40, T = 21) | Mean | 102.27 | 105.58 | 100.98 | 105.94 | ||||

| Std. Dev. | Overall | 57.57 | 13.65 | 5.31 | 8.09 | ||||

| Between | 56.23 | 7.71 | 4.24 | 5.87 | |||||

| Within | 1,276,862 | 15.09 | 11.32 | 3.27 | 5.63 | ||||

| Min | Overall | 156,006 | 19.55 | 76.33 | 88.99 | 75.46 | |||

| Between | 188,832.2 | 26.75 | 89.98 | 96.73 | 88.31 | ||||

| Within | − | 3,199,535 | − | 37.95 | 75.75 | 78.71 | 89.16 | ||

| Max | Overall | 380.10 | 213.43 | 137.99 | 132.02 | ||||

| Between | 309.29 | 121.71 | 122.27 | 116.78 | |||||

| Within | 173.08 | 197.29 | 116.70 | 125.35 | |||||

| POLS | FGLS | Fixed Effect | DIF-GMM | SYS-GMM | |

|---|---|---|---|---|---|

| 0.77 *** (9.68) | 0.87 *** (8.42) | ||||

| ln(L) | 0.01 (1.06) | 0.01 *** (3.65) | 0.43 *** (19.40) | 0.09 *** (6.19) | 0.01 *** (3.70) |

| ln(K) | 0.94 *** (184.55) | 0.92 *** (205.41) | 0.35 *** (40.87) | 0.10 *** (23.34) | 0.09 *** (21.92) |

| ln(T) | −0.17 *** (−10.44) | −0.15 *** (−13.36) | −0.03 ** (−2.51) | 0.06 *** (12.11) | 0.05 *** (9.62) |

| ln(ES) | 0.02 (0.42) | 0.01 (0.63) | 0.32 *** (11.72) | 0.04 *** (3.88) | 0.02 *** (2.62) |

| ln(EE) | 0.42 *** (11.55) | 0.41 *** (27.65) | 0.40 *** (18.58) | 0.03 *** (3.51) | 0.05 *** (7.52) |

| ln(ESUS) | 0.92 *** (13.01) | 0.81 *** (17.51) | 0.26 *** (6.79) | −0.03 *** (−3.71) | −0.08 *** (−6.16) |

| constant | 1.27 *** (3.19) | 1.71 *** (7.38) | 5.57 *** (6.79) | 1.37 *** (12.48) | 1.35 *** (16.26) |

| 0.98 | 0.82 | ||||

| Observation | 2289 | 2289 | 2289 | 2071 | 2180 |

| Hausman | Chi2(6) = 50.24, Prob > Chi2 = 0.00 | ||||

| Pasaran | Pr = 0.37 | ||||

| AR(1) | −5.15 *** Prob > z = 0.00 | −5.39 *** Prob > z = 0.00 | |||

| AR(2) | −0.51 Prob > z = 0.60 | −0.35 Prob > z = 0.72 | |||

| Sargan | Prob > Chi2 = 0.21 | Prob > Chi2 = 0.19 |

| POLS | FGLS | Fixed Effect | DIF-GMM | SYS-GMM | |

|---|---|---|---|---|---|

| 0.82 *** (52.05) | 0.89 *** (11.87) | ||||

| ln(L) | 0.14 *** (8.59) | 0.15 *** (36.11) | 1.14 *** (21.89) | 0.15 *** (4.56) | 0.03 *** (6.13) |

| ln(K) | 0.77 *** (56.31) | 0.76 *** (233.32) | 0.21 *** (14.31) | 0.07 *** (12.54) | 0.07 *** (13.53) |

| ln(T) | −0.22 *** (−6.77) | −0.21 *** (−39.62) | −0.06 *** (−2.66) | 0.02 ** (2.55) | 0.02 *** (3.30) |

| ln(ES) | 0.08 (0.69) | 0.06 ** (2.22) | 0.15 *** (2.69) | 0.05 *** (2.82) | 0.08 *** (4.42) |

| ln(EE) | −0.12 ** (−2.55) | −0.12 *** (−11.77) | −0.23 *** (−8.38) | −0.81 (−0.81) | −0.02 *** (−2.98) |

| ln(ESUS) | 1.20 *** (9.44) | 1.18 *** (49.77) | −0.01 (−0.15) | −0.03 (−1.51) | −0.05 *** (−2.90) |

| constant | 0.67 (0.85) | 0.66 *** (5.38) | −0.57 (−0.85) | 0.41 * (1.81) | 0.99 *** (7.60) |

| 0.94 | 0.86 | ||||

| Observation | 777 | 777 | 777 | 703 | 740 |

| Hausman | Chi2(6) = 41.11 Prob > Chi2 = 0.00 | ||||

| Pasaran | Pr = 0.34 | ||||

| AR(1) | −3.08 *** Prob > z = 0.00 | −3.47 *** Prob > z = 0.00 | |||

| AR(2) | −1.27 Prob > z = 0.20 | −1.24 Prob > z = 0.21 | |||

| Sargan | Prob > Chi2 = 0.30 | Prob > Chi2 = 0.34 |

| POLS | FGLS | Fixed Effect | DIF-GMM | SYS-GMM | |

|---|---|---|---|---|---|

| 0.79 *** (8.60) | 0.85 *** (8.14) | ||||

| ln(L) | 0.18 *** (8.91) | 0.19 *** (58.20) | 0.21 *** (5.77) | 0.02 (1.17) | 0.07 *** (8.89) |

| ln(K) | 0.79 *** (43.05) | 0.78 *** (280.62) | 0.41 *** (31.58) | 0.10 *** (13.99) | 0.07 *** (10.71) |

| ln(T) | −0.21 *** (−8.51) | −0.20 *** (−46.83) | −0.08 *** (−3.97) | 0.08 *** (7.49) | 0.10 *** (9.70) |

| ln(ES) | 0.22 *** (2.82) | 0.20 *** (16.89) | 0.18 *** (3.89) | 0.06 *** (3.14) | 0.04 *** (3.22) |

| ln(EE) | −0.57 *** (−6.56) | −0.55 *** (−42.34) | −0.90 *** (−14.60) | 0.09 (1.24) | −0.07 *** (−3.24) |

| ln(ESUS) | 0.29 *** (3.16) | 0.30 *** (29.66) | 0.38 *** (6.80) | 0.01 (0.44) | −0.04 *** (−2.23) |

| constant | 4.65 *** (7.29) | 4.68 *** (5.95) | 5.30 *** (10.33) | 1.36 *** (5.91) | 0.68 *** (4.45) |

| 0.98 | 0.88 | ||||

| Observation | 672 | 672 | 672 | 608 | 640 |

| Hausman | Chi2(6) = 89.59 Prob > Chi2 = 0.00 | ||||

| Pasaran | Pr = 0.51 | ||||

| AR(1) | −3.07 *** Prob > z = 0.00 | −2.90 *** Prob > z = 0.00 | |||

| AR(2) | −1.47 Prob > z = 0.14 | −1.38 Prob > z = 0.16 | |||

| Sargan | Prob > Chi2 = 0.48 | Prob > Chi2 = 0.36 |

| POLS | FGLS | Fixed Effect | DIF-GMM | SYS-GMM | |

|---|---|---|---|---|---|

| 0.67 *** (5.78) | 0.77 *** (8.29) | ||||

| ln(L) | 0.11 *** (8.02) | 0.12 *** (32.75) | 0.21 *** (9.30) | 0.05 *** (3.80) | 0.11 *** (10.10) |

| ln(K) | 0.87 *** (71.83) | 0.84 *** (49.44) | 0.35 *** (26.54) | 0.13 *** (23.19) | 0.12 *** (21.96) |

| ln(T) | 0.04 ** (2.40) | 0.04 *** (9.41) | 0.21 *** (10.28) | 0.01 *** (13.32) | 0.01 ** (2.41) |

| ln(ES) | 0.06 (1.03) | 0.07 *** (4.53) | 0.33 *** (10.94) | 0.10 *** (8.66) | 0.02 ** (2.06) |

| ln(EE) | 1.05 *** (7.21) | 1.05 *** (5.39) | 0.39 *** (4.64) | 0.12 *** (3.18) | 0.21 *** (5.86) |

| ln(ESUS) | 0.40 *** (3.90) | 0.39 *** (19.27) | 0.22 *** (4.13) | 0.05 *** (2.76) | 0.11 *** (5.78) |

| constant | 6.34 *** (7.34) | 6.37 *** (5.67) | 8.83 *** (18.90) | 3.10 *** (16.63) | 2.27 *** (11.98) |

| 0.98 | 0.80 | ||||

| Observation | 840 | 840 | 840 | 760 | 800 |

| Hausman | Chi2(6) = 72.61 Prob > Chi2 = 0.00 | ||||

| Pasaran | Pr = 0.22 | ||||

| AR(1) | −4.59 *** Prob > z = 0.00 | −3.86 *** Prob > z = 0.00 | |||

| AR(2) | −0.54 Prob > z = 0.58 | −1.40 Prob > z = 0.16 | |||

| Sargan | Prob > Chi2 = 0.29 | Prob > Chi2 = 0.13 |

| Dependent Variable | ||||

|---|---|---|---|---|

| ln(ES) | ln(EE) | ln(ESUS) | ||

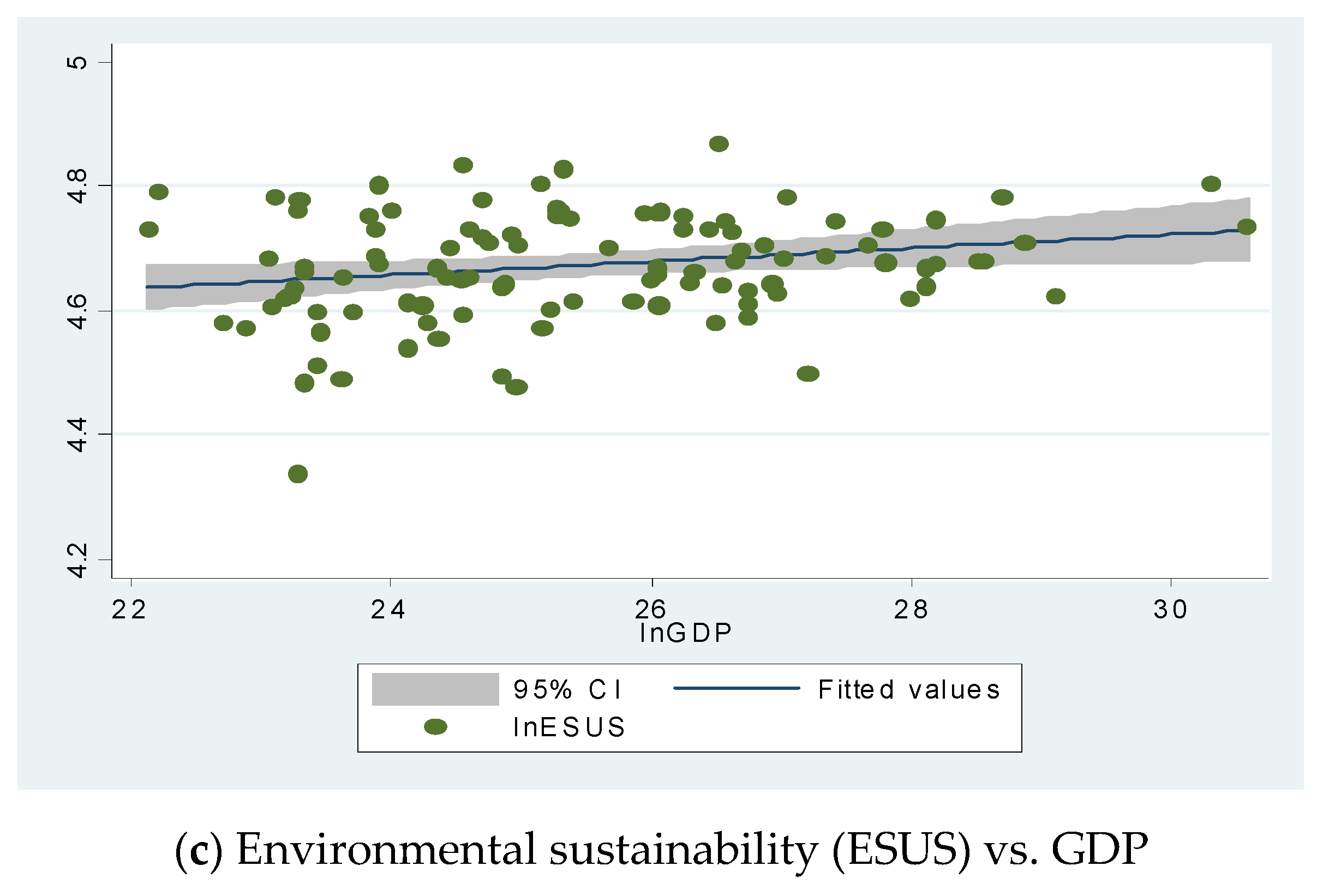

| Full sample | ln(GDP) | 0.01 (1.02) | −0.12 *** (−10.85) | 0.07 *** (12.52) |

| ln(L) | 0.01 (0.53) | 0.03 *** (9.99) | −0.01 (−0.20) | |

| ln(K) | −0.01 (−1.41) | 0.08 *** (7.74) | −0.05 *** (−10.43) | |

| ln(T) | 0.01 *** (3.17) | −0.01 * (−1.93) | 0.03 *** (7.77) | |

| constant | 4.59 *** (85.15) | 5.17 *** (64.52) | 4.08 *** (97.95) | |

| 0.01 | 0.11 | 0.08 | ||

| Low and lower-middle income countries | ln(GDP) | −0.01 (−1.15) | −0.02 (−1.17) | 0.08 *** (9.10) |

| ln(L) | 0.01 (0.53) | −0.03 ** (−2.59) | −0.01 (−1.57) | |

| ln(K) | 0.01 (0.76) | 0.06 *** (3.12) | −0.06 *** (−7.95) | |

| ln(T) | 0.01 * (1.82) | −0.02 (−1.13) | 0.05 *** (5.69) | |

| constant | 4.66 *** (48.10) | 4.58 *** (20.1) | 3.93 *** (47.55) | |

| 0.01 | 0.02 | 0.11 | ||

| Upper-middle income countries | ln(GDP) | 0.05 *** (2.72) | −0.10 *** (−6.50) | 0.06 *** (4.52) |

| ln(L) | −0.03 *** (−3.62) | −0.04 *** (−4.74) | −0.01 (−0.58) | |

| ln(K) | −0.01 (−1.12) | 0.14 *** (10.31) | −0.05 *** (−4.13) | |

| ln(T) | 0.01 (0.39) | −0.04 (−3.54) | 0.02 ** (2.54) | |

| constant | 4.39 *** (33.17) | 4.67 *** (40.35) | 4.19 *** (37.91) | |

| 0.03 | 0.16 | 0.03 | ||

| High income countries | ln(GDP) | 0.02 ** (2.33) | −0.05 *** (−7.56) | 0.05 *** (4.47) |

| ln(L) | 0.03 *** (4.23) | 0.02 *** (8.54) | 0.02 *** (4.58) | |

| ln(K) | −0.05 *** (−3.06) | 0.03 *** (4.38) | −0.06 *** (−5.19) | |

| ln(T) | 0.02 ** (2.49) | 0.01 (1.02) | 0.38 *** (5.76) | |

| constant | 4.74 *** (40.96) | 4.89 *** (106.25) | 4.20 *** (55.67) | |

| 0.03 | 0.11 | 0.09 | ||

| ES on Economic Growth | EE on Economic Growth | ESUS on Economic Growth | ||||

|---|---|---|---|---|---|---|

| (+) | (−) | (+) | (−) | (+) | (−) | |

| Low and lower-middle income countries (number of country) | Bangladesh Cambodia Kenya Morocco Nicaragua Niger (6) | Honduras Mozambique (2) | Angola Cote d’Ivoire Egypt Eswatini Ethiopia Indonesia Iran Mongolia Morocco Mozambique Sri Lanka Tanzania Ukraine Vietnam (14) | Cambodia (1) | El Salvador Eswatini Kenya Nigeria (4) | Angola Chad Indonesia Madagascar Nepal Nicaragua Niger (7) |

| % of sub-sample country | 16.21% | 5.41% | 37.83% | 2.70% | 10.81% | 18.91 |

| Upper-middle income countries (number of country) | Albania Brazil China Guatemala Jordan Malaysia Montenegro Romania South Africa (9) | Bosnia and Herzegovina Costa Rica (2) | Albania Armenia China Kazakhstan Lebanon Mexico Peru Romania Russia South Africa (10) | Dominican Rep Guatemala Jordan Peru (4) | Argentina Bosnia and Herzegovina Ecuador Gabon (4) | |

| % of sub-sample country | 28.12% | 6.25% | 31.25% | 0% | 12.5% | 12.5% |

| High income countries (number of country) | Bahrain Denmark Germany Iceland Japan Portugal Slovenia Uruguay (8) | Austria Norway United Arab Emirates (3) | Bahrain Cyprus Estonia Hungary Iceland United Arab Emirates (6) | Belgium (1) | Canada Czech Rep Denmark Greece Hungary Spain Uruguay (7) | Japan Luxembourg United Arab Emirates (3) |

| % of sub-sample country | 20% | 7.5% | 15% | 2.5% | 17.5% | 7.5% |

| Sum (% of full sample country) | 23 (21.1%) | 7 (6.42%) | 30 (27.52%) | 2 (1.83%) | 15 (13.76%) | 14 (12.84%) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kang, H. An Analysis of the Relationship between Energy Trilemma and Economic Growth. Sustainability 2022, 14, 3863. https://doi.org/10.3390/su14073863

Kang H. An Analysis of the Relationship between Energy Trilemma and Economic Growth. Sustainability. 2022; 14(7):3863. https://doi.org/10.3390/su14073863

Chicago/Turabian StyleKang, Hyunsoo. 2022. "An Analysis of the Relationship between Energy Trilemma and Economic Growth" Sustainability 14, no. 7: 3863. https://doi.org/10.3390/su14073863

APA StyleKang, H. (2022). An Analysis of the Relationship between Energy Trilemma and Economic Growth. Sustainability, 14(7), 3863. https://doi.org/10.3390/su14073863