Heterogeneous Impact of Economic Policy Uncertainty on Provincial Environmental Pollution Emissions in China

Abstract

:1. Introduction

2. Data Selection and Model Selection

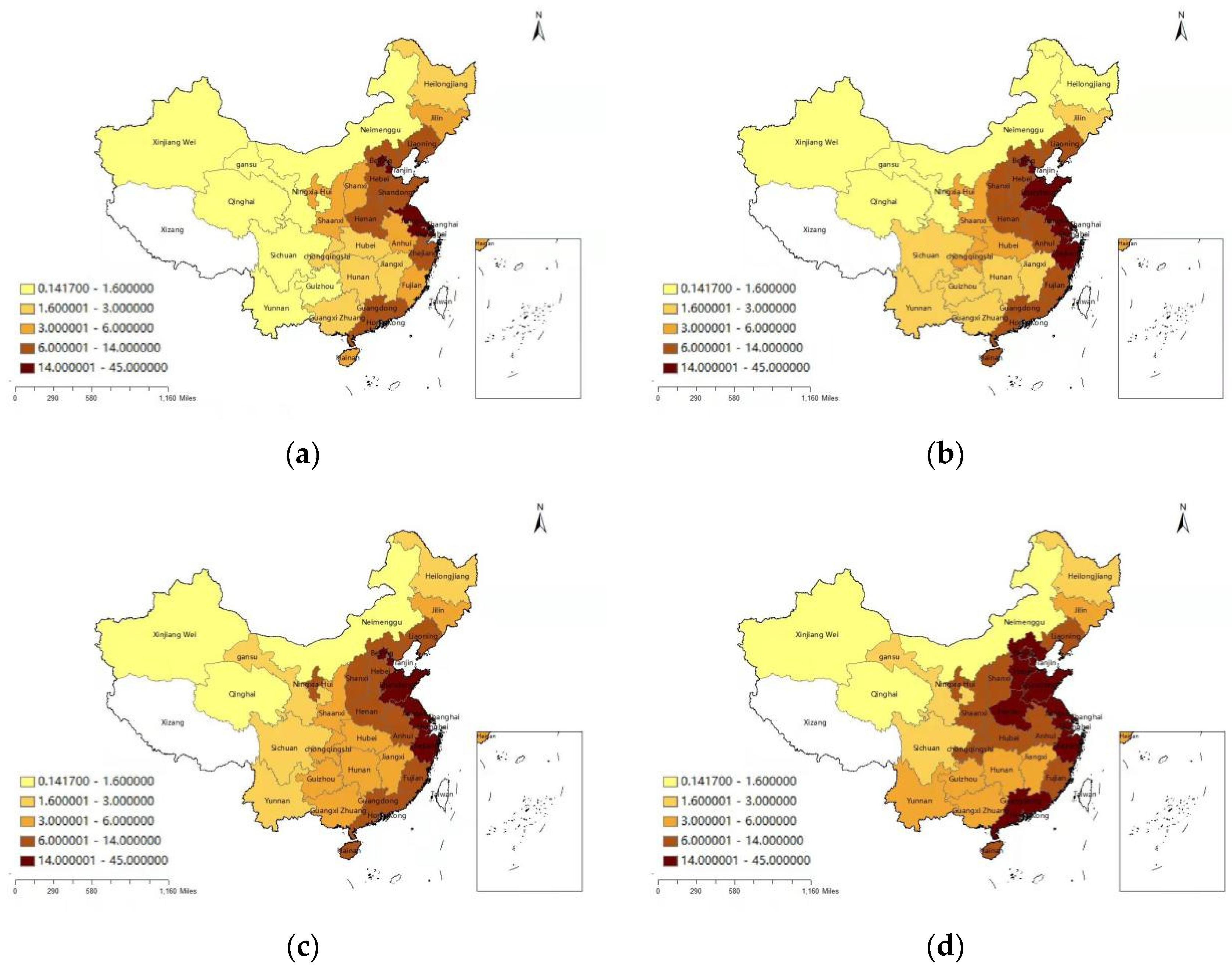

2.1. Variable Selection and Data Sources

2.2. Empirical Model

3. Empirical Results of the Impact of EPU on Pollution Emissions

3.1. Unit Root Test and Co-Integration Test

3.2. Model Selection and Parameter Estimation

3.3. Analysis of Regression Results

4. Robustness Test

5. Discussion and Conclusions

5.1. Discussion

5.2. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Pirgaip, B.; Dincergok, B. Economic policy uncertainty, energy consumption and carbon emissions in G7 countries: Evidence from a panel Granger causality analysis. Environ. Sci. Pollut. Res. Int. 2020, 27, 30050–30066. [Google Scholar] [CrossRef] [PubMed]

- Wang, Q.; Xiao, K.; Lu, Z. Does Economic Policy Uncertainty Affect CO2 Emissions? Empirical Evidence from the United States. Sustainability 2020, 12, 9108. [Google Scholar] [CrossRef]

- Jiang, Y.; Zhou, Z.; Liu, C. Does economic policy uncertainty matter for carbon emission? Evidence from US sector level data. Environ. Sci. Pollut. Res. Int. 2019, 26, 24380–24394. [Google Scholar] [CrossRef] [PubMed]

- Adams, S.; Adedoyin, F.; Olaniran, E.; Bekun, F.V. Energy consumption, economic policy uncertainty and carbon emissions; causality evidence from resource rich economies. Econ. Anal. Policy 2020, 68, 179–190. [Google Scholar] [CrossRef]

- Chen, Y.; Shen, X.; Wang, L. The Heterogeneity Research of the Impact of EPU on Environmental Pollution: Empirical Evidence Based on 15 Countries. Sustainability 2021, 13, 4166. [Google Scholar] [CrossRef]

- Danish; Ulucak, R.; Khan, S.U.D. Relationship between energy intensity and CO2 emissions: Does economic policy matter? Sustain. Dev. 2020, 28, 1457–1464. [Google Scholar] [CrossRef]

- Adedoyin, F.F.; Zakari, A. Energy consumption, economic expansion, and CO2 emission in the UK: The role of economic policy uncertainty. Sci. Total Environ. 2020, 738, 140014. [Google Scholar] [CrossRef] [PubMed]

- Rehman, M.U. Do oil shocks predict economic policy uncertainty? Phys. A Stat. Mech. Its Appl. 2018, 498, 123–136. [Google Scholar] [CrossRef]

- Degiannakis, S.; Filis, G.; Panagiotakopoulou, S. Oil price shocks and uncertainty: How stable is their relationship over time? Econ. Model. 2018, 72, 42–53. [Google Scholar] [CrossRef] [Green Version]

- Li, L.; Yin, L.; Zhou, Y. Exogenous shocks and the spillover effects between uncertainty and oil price. Energy Econ. 2016, 54, 224–234. [Google Scholar] [CrossRef]

- Kang, W.; Ratti, R.A. Oil shocks, policy uncertainty and stock market return. J. Int. Financ. Mark. Inst. Money 2013, 26, 305–318. [Google Scholar] [CrossRef]

- Ji, Q.; Liu, B.-Y.; Nehler, H.; Uddin, G.S. Uncertainties and extreme risk spillover in the energy markets: A time-varying copula-based CoVaR approach. Energy Econ. 2018, 76, 115–126. [Google Scholar] [CrossRef]

- Lin, B.; Bai, R. Oil prices and economic policy uncertainty: Evidence from global, oil importers, and exporters’ perspective. Res. Int. Bus. Financ. 2021, 56, 101357. [Google Scholar] [CrossRef]

- Davis, S.J.; Bloom, N.; Baker, S.R. Measuring Economic Policy Uncertainty; National Bureau of Economic Research: Cambridge, MA, USA, 2016. [Google Scholar] [CrossRef]

- Brogaard, J.; Detzel, A. The Asset-Pricing Implications of Government Economic Policy Uncertainty. Manag. Sci. 2015, 61, 3–18. [Google Scholar] [CrossRef] [Green Version]

- Pástor, Ľ.; Veronesi, P. Political uncertainty and risk premia. J. Financ. Econ. 2013, 110, 520–545. [Google Scholar] [CrossRef] [Green Version]

- Liu, L.; Zhang, T. Economic policy uncertainty and stock market volatility. Financ. Res. Lett. 2015, 15, 99–105. [Google Scholar] [CrossRef] [Green Version]

- Arouri, M.; Teulon, F.; Rault, C. Equity risk premium and regional integration. Int. Rev. Financ. Anal. 2013, 28, 79–85. [Google Scholar] [CrossRef] [Green Version]

- Bloom, N.; Bond, S.; Van Reenen, J. Uncertainty and investment dynamics. Rev. Econ. Stud. 2007, 74, 391–415. [Google Scholar] [CrossRef] [Green Version]

- Farzin, Y.H.; Kort, P.M. Pollution Abatement Investment When Environmental Regulation Is Uncertain. J. Public Econ. Theory 2000, 2, 183–212. [Google Scholar] [CrossRef]

- Claeys, P. Uncertainty spillover and policy reactions. Ens. Sobre Política Económica 2017, 35, 64–77. [Google Scholar] [CrossRef]

- Mumtaz, H.; Surico, P. Policy uncertainty and aggregate fluctuations. J. Appl. Econ. 2018, 33, 319–331. [Google Scholar] [CrossRef]

- Coibion, O.; Georgarakos, D.; Gorodnichenko, Y.; Kenny, G.; Weber, M. The Effect of Macroeconomic Uncertainty on Household Spending; National Bureau of Economic Research: Cambridge, MA, USA, 2021. [Google Scholar] [CrossRef]

- Wu, H.X. The Chinese GDP growth rate puzzle: How fast has the Chinese economy grown. Asian Econ. Pap. 2006, 6, 1–23. [Google Scholar] [CrossRef]

- Ghosh, T.; Anderson, S.; Powell, R.; Sutton, P.; Elvidge, C. Estimation of Mexico’s Informal Economy and Remittances Using Nighttime Imagery. Remote Sens. 2009, 1, 418–444. [Google Scholar] [CrossRef] [Green Version]

- Chand, T.R.K.; Badarinath, K.V.S.; Elvidge, C.D.; Tuttle, B.T. Spatial characterization of electrical power consumption patterns over India using temporal DMSP-OLS night-time satellite data. Int. J. Remote Sens. 2009, 30, 647–661. [Google Scholar] [CrossRef]

- Chen, X.; Nordhaus, W.D. Using luminosity data as a proxy for economic statistics. Proc. Natl. Acad. Sci. USA 2011, 108, 8589–8594. [Google Scholar] [CrossRef] [Green Version]

- Henderson, J.V.; Storeygard, A.; Weil, D.N. Measuring Economic Growth from Outer Space. Am. Econ. Rev. 2012, 102, 994–1028. [Google Scholar] [CrossRef] [Green Version]

- Yun, W.; Xiao Hua, S. The Mechanism of Industrial Transformation and Upgrading Driven by Government Subsidies. China Ind. Econ. 2017, 10, 99–117. [Google Scholar] [CrossRef]

- Jieqi, Z.; Yin, H.; Ying, Z. Foreign investment, environmental regulation, and carbon efficiency in China: Theory and empirical evidence. J. China Univ. Geosci. 2016, 16, 50–62. [Google Scholar] [CrossRef]

- Wu, K.; Wang, X. Aligning Pixel Values of DMSP and VIIRS Nighttime Light Images to Evaluate Urban Dynamics. Remote Sens. 2019, 11, 1463. [Google Scholar] [CrossRef] [Green Version]

- Zheng, Q.; Weng, Q.; Wang, K. Developing a new cross-sensor calibration model for DMSP-OLS and Suomi-NPP VIIRS night-light imageries. ISPRS J. Photogramm. Remote Sens. 2019, 153, 36–47. [Google Scholar] [CrossRef]

- Ma, J.; Guo, J.; Ahmad, S.; Li, Z.; Hong, J. Constructing a New Inter-Calibration Method for DMSP-OLS and NPP-VIIRS Nighttime Light. Remote Sens. 2020, 12, 937. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Variables | CE (Principal Component Analysis) | CE (Entropy Weight Method) | EPU | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Provinces | Mean | Max | Min | Mean | Max | Min | Mean | Max | Min |

| Beijing | −1.087 | −0.979 | −1.226 | 0.073 | 0.116 | 0.045 | 319.345 | 791.470 | 98.890 |

| Tianjin | −1.168 | −1.065 | −1.301 | 0.067 | 0.095 | 0.037 | |||

| Hebei | 1.442 | 1.862 | 0.612 | 0.663 | 0.728 | 0.486 | |||

| Shanxi | 0.918 | 1.299 | 0.676 | 0.565 | 0.603 | 0.477 | |||

| Inner Mongolia | 0.802 | 1.599 | 0.517 | 0.518 | 0.636 | 0.429 | |||

| Liaoning | 0.890 | 1.172 | 0.547 | 0.523 | 0.635 | 0.431 | |||

| Jilin | −0.727 | −0.700 | −0.785 | 0.158 | 0.182 | 0.141 | |||

| Heilongjiang | −0.449 | −0.131 | −0.588 | 0.214 | 0.257 | 0.184 | |||

| Shanghai | −0.682 | −0.365 | −0.927 | 0.143 | 0.235 | 0.097 | |||

| Jiangsu | 1.408 | 1.678 | 0.808 | 0.526 | 0.599 | 0.435 | |||

| Zhejiang | 0.283 | 0.575 | −0.094 | 0.307 | 0.378 | 0.256 | |||

| Anhui | 0.009 | 0.142 | −0.180 | 0.311 | 0.349 | 0.277 | |||

| Fujian | −0.179 | 0.103 | −0.400 | 0.250 | 0.307 | 0.194 | |||

| Jiangxi | −0.032 | 0.354 | −0.225 | 0.306 | 0.382 | 0.257 | |||

| Shandong | 1.823 | 2.200 | 1.253 | 0.648 | 0.709 | 0.570 | |||

| Henan | 0.996 | 1.340 | 0.399 | 0.479 | 0.580 | 0.386 | |||

| Hubei | 0.073 | 0.149 | −0.040 | 0.299 | 0.341 | 0.268 | |||

| Hunan | 0.176 | 0.318 | 0.000 | 0.311 | 0.371 | 0.271 | |||

| Guangdong | 1.701 | 2.045 | 1.134 | 0.533 | 0.641 | 0.470 | |||

| Guangxi | −0.109 | 0.703 | −0.456 | 0.268 | 0.432 | 0.205 | |||

| Hainan | −1.425 | −1.314 | −1.562 | 0.020 | 0.026 | 0.017 | |||

| Chongqing | −0.535 | −0.295 | −0.656 | 0.176 | 0.241 | 0.142 | |||

| Sichuan | 0.607 | 0.925 | 0.418 | 0.413 | 0.489 | 0.350 | |||

| Guizhou | 0.026 | 0.867 | −0.285 | 0.309 | 0.444 | 0.244 | |||

| Yunnan | 0.026 | 0.634 | −0.510 | 0.334 | 0.440 | 0.238 | |||

| Shaanxi | −0.183 | −0.037 | −0.265 | 0.267 | 0.303 | 0.229 | |||

| Gansu | −0.745 | −0.583 | −0.906 | 0.159 | 0.176 | 0.141 | |||

| Qinghai | −1.027 | −0.650 | −1.445 | 0.138 | 0.206 | 0.053 | |||

| Ningxia | −0.978 | −0.749 | −1.206 | 0.114 | 0.162 | 0.092 | |||

| Xinjiang | −0.318 | 0.142 | −0.735 | 0.244 | 0.356 | 0.173 | |||

| Variables | LLC Test Value | ADF Test Value | Fisher PP Test Value | Conclusion |

|---|---|---|---|---|

| lnEPU | 2.5869 (0.9952) | 7.4034 (1.0000) | 5.8223 (1.0000) | No stability |

| lnVIIRS | −3.7943 (0.0001) | 32.7924 (0.9984) | 27.3430 (0.9999) | No stability |

| lnFDI | −10.0644 *** (0.0000) | 129.5047 *** (0.0000) | 29.6681 (0.9996) | No stability |

| CE | −2.4696 *** (0.0068) | 63.2166 (0.3635) | 83.6318 ** (0.0236) | No stability |

| ΔlnEPU | −20.4110 *** (0.0000) | 398.4523 *** (0.0000) | 241.0424 *** (0.0000) | Stability |

| ΔlnVIIRS | −11.1694 (0.0000) | 217.8185 (0.0000) | 367.5354 (0.0000) | Stability |

| ΔlnFDI | −6.1521 *** (0.0000) | 125.2790 *** (0.0014) | 217.3059 *** (0.0000) | Stability |

| ΔCE | −3.7093 *** (0.0001) | 135.7208 *** (0.0000) | 526.3521 *** (0.0000) | Stability |

| Statistic | p-Value | |

|---|---|---|

| Modified Phillips–Perron t | 2.7811 | 0.0027 |

| Phillips–Perron t | −12.0940 | 0.0000 |

| Augmented Dickey–Fuller t | −11.4681 | 0.0000 |

| Statistic | p-Value | |

|---|---|---|

| F test | 153.19 | 0.000 |

| Hausman test | 36.20 | 0.000 |

| Variables | Coefficient | Standard Error | T Statistic | p-Value |

|---|---|---|---|---|

| C | −0.90995 | 0.260322 | −3.50 | 0.000 |

| lnEPU | −0.10537 | 0.0573 | −1.84 | 0.066 |

| lnVIIRS | 0.315095 | 0.085816 | 3.67 | 0.000 |

| lnFDI | −0.07175 | 0.02336 | −3.07 | 0.002 |

| Deve*lnEPU | −0.20816 | 0.041825 | −4.98 | 0.000 |

| Yunnan | 1.473401 | 0.277508 | 5.31 | 0.000 |

| Inner Mongolia | 2.619426 | 0.35334 | 7.41 | 0.000 |

| Beijing | −0.21481 | 0.101734 | −2.11 | 0.035 |

| Jilin | 0.647823 | 0.251551 | 2.58 | 0.010 |

| Sichuan | 2.240113 | 0.285604 | 7.84 | 0.000 |

| Tianjin | −0.40822 | 0.087541 | −4.66 | 0.000 |

| Ningxia | 0.071763 | 0.232847 | 0.31 | 0.758 |

| Anhui | 1.221871 | 0.174383 | 7.01 | 0.000 |

| Shandong | 3.967948 | 0.257148 | 15.43 | 0.000 |

| Shanxi | 2.01754 | 0.186097 | 10.84 | 0.000 |

| Guangdong | 3.958936 | 0.264439 | 14.97 | 0.000 |

| Guangxi | 1.227498 | 0.257793 | 4.76 | 0.000 |

| Xinjiang | 1.421676 | 0.389035 | 3.65 | 0.000 |

| Jiangsu | 3.504186 | 0.249844 | 14.03 | 0.000 |

| Jiangxi | 1.452037 | 0.246462 | 5.89 | 0.000 |

| Hebei | 2.532601 | 0.155007 | 16.34 | 0.000 |

| Henan | 2.1377 | 0.154104 | 13.87 | 0.000 |

| Zhejiang | 2.446262 | 0.258527 | 9.46 | 0.000 |

| Hainan | −0.32775 | 0.185984 | −1.76 | 0.078 |

| Hubei | 1.449128 | 0.22138 | 6.55 | 0.000 |

| Hunan | 1.678508 | 0.247464 | 6.78 | 0.000 |

| Gansu | 0.665623 | 0.338097 | 1.97 | 0.049 |

| Fujian | 2.142641 | 0.284653 | 7.53 | 0.000 |

| Guizhou | 1.337405 | 0.270246 | 4.95 | 0.000 |

| Liaoning | 2.115718 | 0.177887 | 11.89 | 0.000 |

| Chongqing | 0.795016 | 0.227269 | 3.5 | 0.000 |

| Shaanxi | 1.077528 | 0.206605 | 5.22 | 0.000 |

| Qinghai | 0.881767 | 0.472653 | 1.87 | 0.062 |

| Heilongjiang | 1.108825 | 0.286334 | 3.87 | 0.000 |

| Statistic | p-Value | |

|---|---|---|

| F test | 139.35 | 0.0000 |

| Hausman test | 16.43 | 0.0025 |

| Variables | Coefficient | Standard Error | T Statistic | p-Value |

|---|---|---|---|---|

| C | 0.259815 | 0.054492 | 4.77 | 0.000 |

| lnEPU | −0.05430 | 0.011994 | −4.53 | 0.000 |

| lnVIIRS | 0.071134 | 0.017964 | 3.96 | 0.000 |

| lnFDI | −0.01259 | 0.00489 | −2.57 | 0.010 |

| Deve*lnEPU | −0.02066 | 0.008755 | −2.36 | 0.018 |

| Yunnan | 0.373003 | 0.05809 | 6.42 | 0.000 |

| Inner Mongolia | 0.637148 | 0.073963 | 8.61 | 0.000 |

| Beijing | −0.02496 | 0.021296 | −1.17 | 0.241 |

| Jilin | 0.179138 | 0.052656 | 3.40 | 0.001 |

| Sichuan | 0.487379 | 0.059784 | 8.15 | 0.000 |

| Tianjin | −0.05626 | 0.018325 | −3.07 | 0.002 |

| Ningxia | 0.070661 | 0.048741 | 1.45 | 0.147 |

| Anhui | 0.289955 | 0.036503 | 7.94 | 0.000 |

| Shandong | 0.692221 | 0.053828 | 12.86 | 0.000 |

| Shanxi | 0.524457 | 0.038955 | 13.46 | 0.000 |

| Guangdong | 0.600296 | 0.055354 | 10.84 | 0.000 |

| Guangxi | 0.283129 | 0.053963 | 5.25 | 0.000 |

| Xinjiang | 0.354054 | 0.081435 | 4.35 | 0.000 |

| Jiangsu | 0.556081 | 0.052299 | 10.63 | 0.000 |

| Jiangxi | 0.346526 | 0.051591 | 6.72 | 0.000 |

| Hebei | 0.615754 | 0.032447 | 18.98 | 0.000 |

| Henan | 0.441246 | 0.032258 | 13.68 | 0.000 |

| Zhejiang | 0.355041 | 0.054117 | 6.56 | 0.000 |

| Hainan | −0.02073 | 0.038931 | −0.53 | 0.594 |

| Hubei | 0.315809 | 0.046341 | 6.81 | 0.000 |

| Hunan | 0.35518 | 0.051801 | 6.86 | 0.000 |

| Gansu | 0.200169 | 0.070773 | 2.83 | 0.005 |

| Fujian | 0.336904 | 0.059585 | 5.65 | 0.000 |

| Guizhou | 0.320878 | 0.05657 | 5.67 | 0.000 |

| Liaoning | 0.505039 | 0.037236 | 13.56 | 0.000 |

| Chongqing | 0.185263 | 0.047573 | 3.89 | 0.000 |

| Shaanxi | 0.260138 | 0.043248 | 6.02 | 0.000 |

| Qinghai | 0.292821 | 0.098939 | 2.96 | 0.003 |

| Heilongjiang | 0.274615 | 0.059937 | 4.58 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, W.; Zhang, Y.; Hu, Y. Heterogeneous Impact of Economic Policy Uncertainty on Provincial Environmental Pollution Emissions in China. Sustainability 2022, 14, 4923. https://doi.org/10.3390/su14094923

Yang W, Zhang Y, Hu Y. Heterogeneous Impact of Economic Policy Uncertainty on Provincial Environmental Pollution Emissions in China. Sustainability. 2022; 14(9):4923. https://doi.org/10.3390/su14094923

Chicago/Turabian StyleYang, Wei, Yifu Zhang, and Yuan Hu. 2022. "Heterogeneous Impact of Economic Policy Uncertainty on Provincial Environmental Pollution Emissions in China" Sustainability 14, no. 9: 4923. https://doi.org/10.3390/su14094923

APA StyleYang, W., Zhang, Y., & Hu, Y. (2022). Heterogeneous Impact of Economic Policy Uncertainty on Provincial Environmental Pollution Emissions in China. Sustainability, 14(9), 4923. https://doi.org/10.3390/su14094923