The Effects of Financial Attitudes, Financial Literacy and Health Literacy on Sustainable Financial Retirement Planning: The Moderating Role of the Financial Advisor

, ,

, ,

Abstract

:1. Introduction

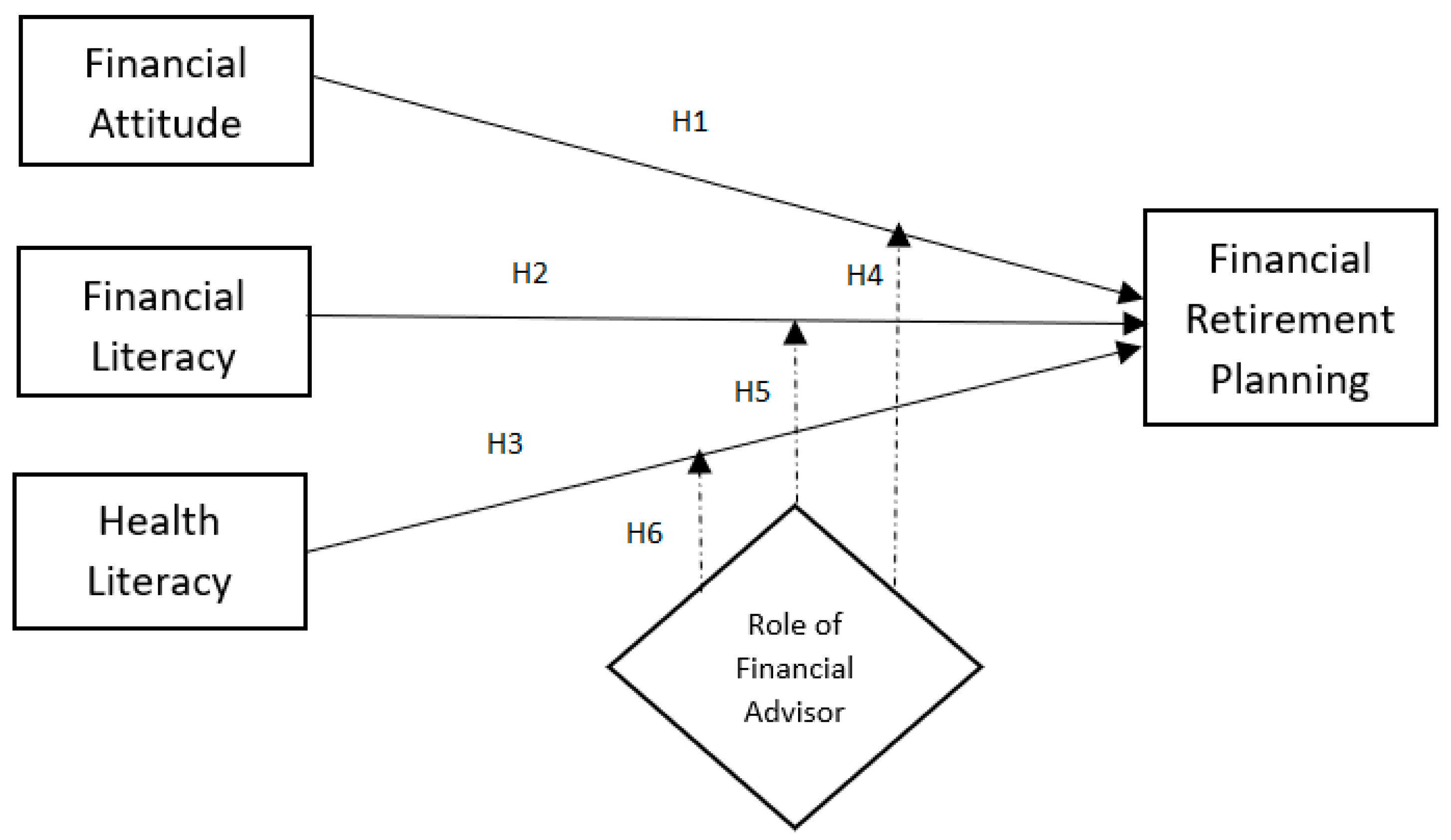

2. Literature Review and Hypotheses Development

2.1. Financial Attitude

2.2. Financial Literacy

2.3. Health Literacy

2.4. Role of a Financial Advisor

3. Methodology

4. Findings and Discussion

4.1. Assessment of Measurement Model

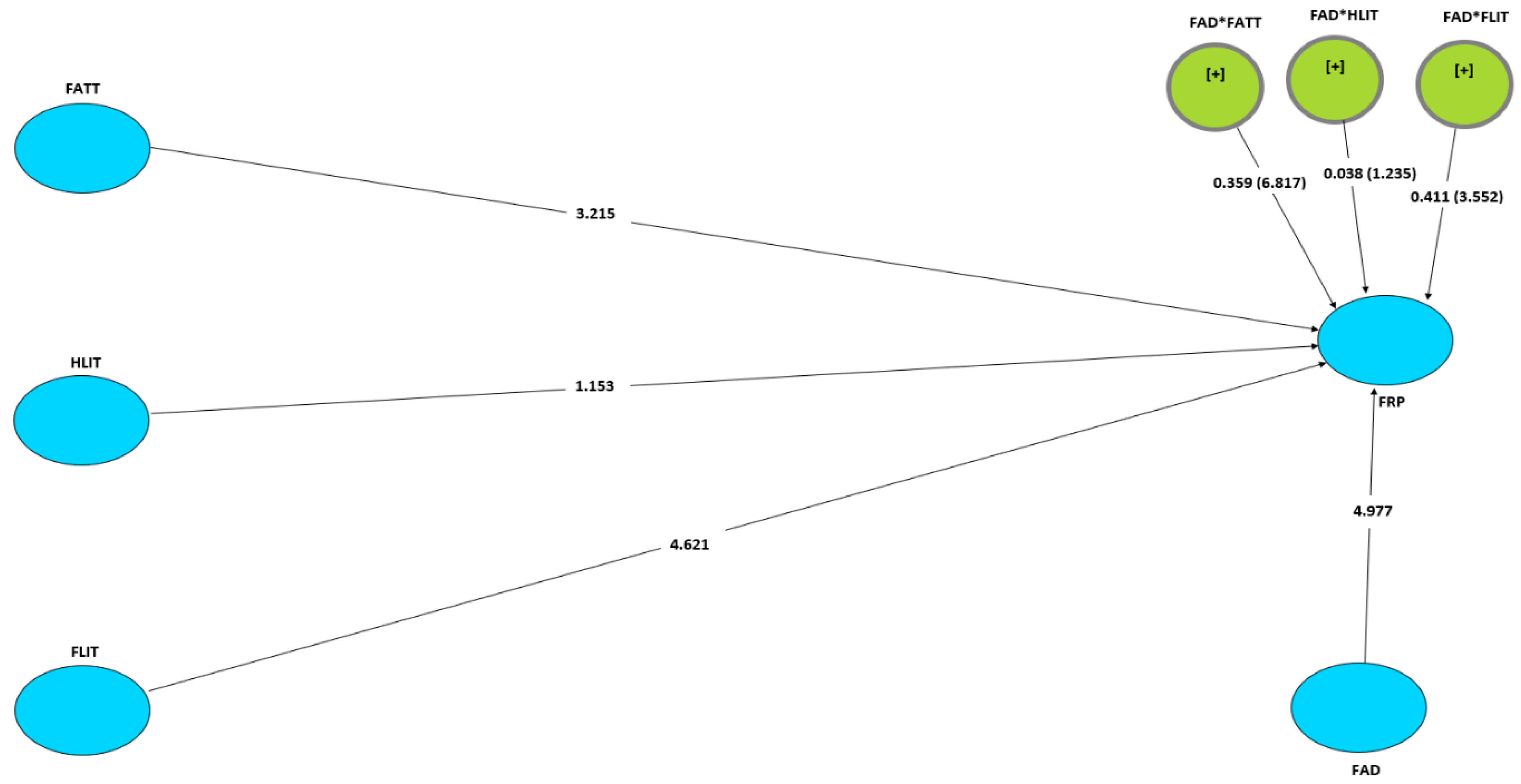

4.2. Assessment of Structural Model

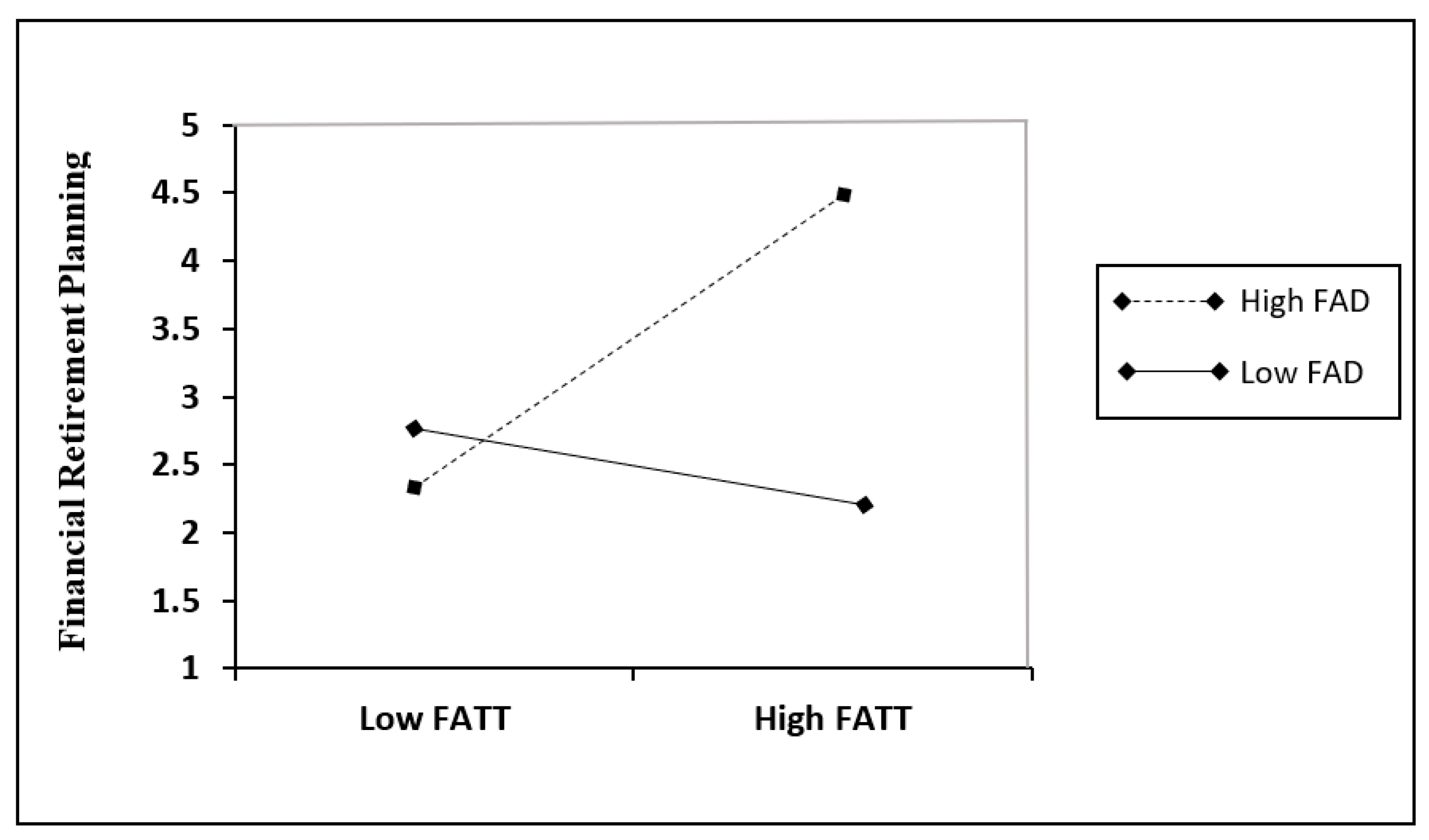

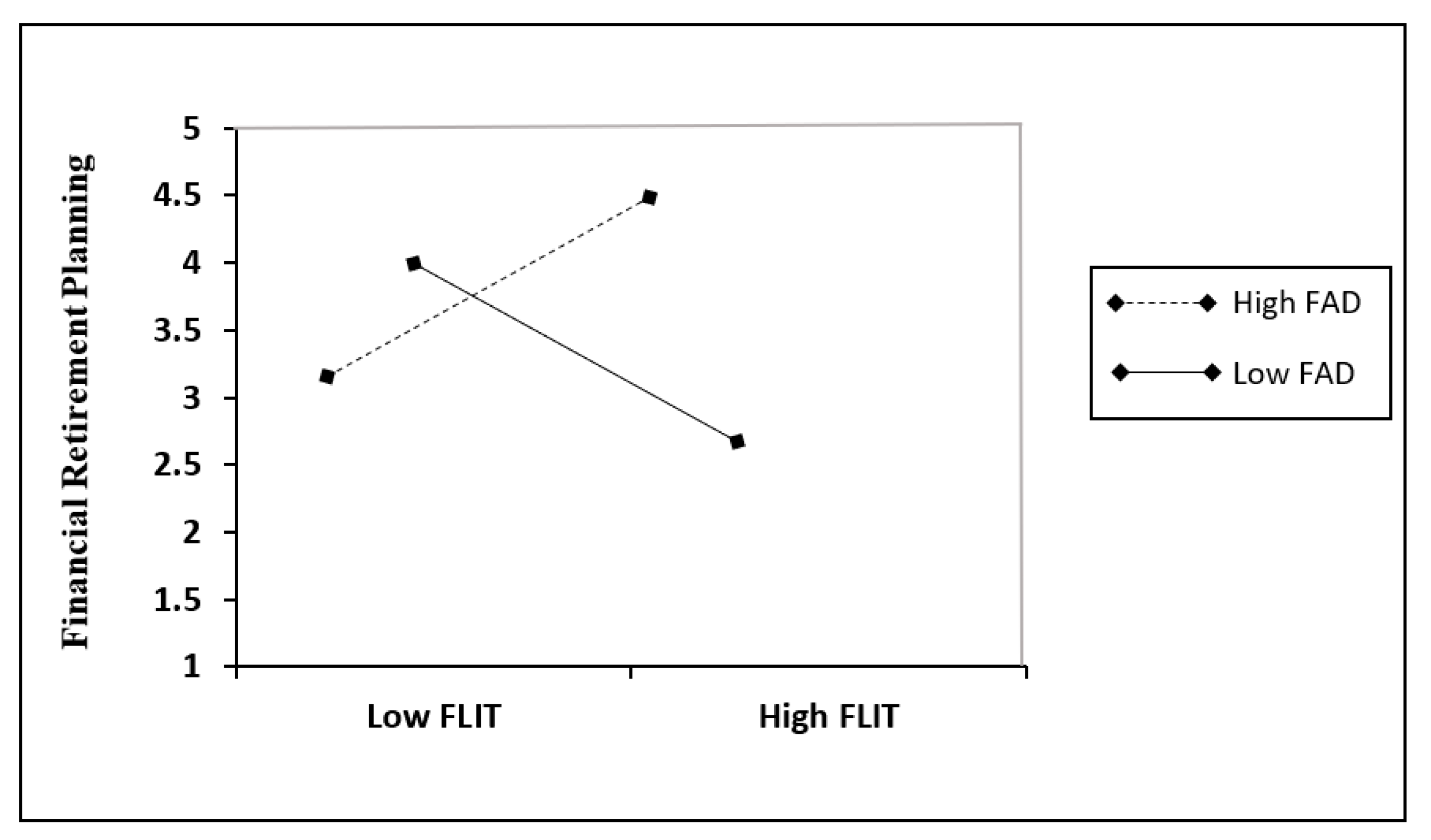

4.3. Moderating Path Coefficient Assessment

4.4. Discussion

5. Conclusions

5.1. Managerial Implications

5.2. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Items |

|---|---|

| Financial Retirement Planning | Financially, my living standard is better compared to five years ago. |

| Financially, I am confident I could sustain the current living standards throughout my retirement. | |

| Overall, I am confident I will have enough money to live comfortably throughout my retirement years. | |

| My savings are enough to sustain my household and myself after retirement. | |

| I already figured out how much I would need to save for life after retirement. | |

| I often keep track of my actual monthly spending. | |

| I often set budget targets for my spending. | |

| I am able to stick to my budget plan. | |

| Financial Attitude | Before I buy something, I carefully consider whether I can afford it. |

| I tend to live for today and let tomorrow take care of itself. | |

| I find it more satisfying to spend money than to save it for the long term. | |

| I pay my bills on time. | |

| I am prepared to risk some of my own money when saving or making an investment. | |

| I keep a close personal watch on my financial affairs. | |

| I set long-term financial goals and strive to achieve them. | |

| Money is there to be spent | |

| Financial Literacy | In the last 12 months, my income did not quite cover my living costs. |

| In the past 12 months, I have been saving money. | |

| If I lost my main source of income, my savings could cover living expenses, without borrowing any money or moving house. | |

| An investment with a high return is likely to be high risk. | |

| High inflation means that the cost of living is increasing rapidly. | |

| It is usually possible to reduce the risk of investing in the stock market by buying a wide range of stocks and shares. | |

| I have a regular source of income coming into my household each month. | |

| I manage my monthly expenditure well. | |

| I have the ability to find good health information | |

| I understand health information well enough to know what to do | |

| Role of a financial Advisor | I believed the financial advisor has sufficient knowledge about financial planning for retirement. |

| I believed a financial advisor could provide me with creative solutions for my financial needs after retirement. | |

| A financial advisor could give me proper advice on retirement planning. | |

| A financial advisor is easily accessible to me. | |

| I consult a financial advisor for reliable advice on financial planning for my retirement. | |

| A financial advisor is able to give me the best possible solution to my financial question. | |

| My financial advisor is able to disentangle relevant information from so much irrelevant information about financial products that I cannot understand. | |

| Advice given by a financial advisor will allow me to have a full understanding of the consequences of my financial choices. | |

| A financial advisor is able to give a full overview of the financial products that are relevant to me. | |

| The financial advice from an advisor could allow me to plan for my retirement needs. | |

| The advice of a financial advisor is crucial for my retirement planning. | |

| A financial advisor’s solution could go beyond my financial possibilities. | |

| I am willing to pay a fee for good financial advice. | |

| The higher the fee for financial advice, the better it is. | |

| Verbal advice from an advisor is more important than written information for my choice of financial product for retirement. | |

| An advisor’s advice is crucial for my purchase decision of any financial products for my retirement. |

References

- Society of Actuaries. Key Findings and Issues: Working in Retirement. 2011 Risks and Process of the Retirement Survey Report. Available online: https://www.soa.org/globalassets/assets/files/research/projects/research-key-finding-working-retire.pdf (accessed on 20 November 2022).

- Clark, T. Handbook of Social Gerontology: Societal Aspects of Aging; University of Chicago Press: Chicago, IL, USA, 1960. [Google Scholar]

- Mitchell, O. Retirement system in developed and developing countries: Institutional features, Economic effects, and lessons for economies in transition. NBER Working Paper No.4424. 1992. Available online: https://www.nber.org/papers/w4424 (accessed on 20 November 2022). [CrossRef]

- HSBC. Retirement: Have You Thought about It Lately? Available online: https://sp.hsbc.com.my/liquid/855.html (accessed on 20 November 2022).

- Miller, K.; Madland, D.; Weller, C.E. The Reality of the Retirement Crisis; Center for American Progress: Washington, DC, USA, 2015. [Google Scholar]

- Uccello, C.E. Are Americans saving Enough for Retirement? Center for Retirement Research at Boston College. Chest-Nut Hill, MA: Center for Retirement Research at Boston College. U.S. Department of Labour, Pension and Welfare Benefit Administration, 2001. Available online: https://crr.bc.edu/briefs/are-americans-saving-enough-for-retirement/ (accessed on 20 November 2022).

- Boisclair, D.; Lusardi, A.; Michaud, P.C. Financial literacy and retirement planning in Canada. J. Pension Econ. Financ. 2017, 16, 277–296. [Google Scholar] [CrossRef]

- Sutherland, P.H. A Veterinarian’s Guide to Financial Planning: From School to Retirement; American Animal Hosp Assocation: Lakewood, CA, USA, 2014. [Google Scholar]

- Fontinelle, A. Setting Financial Goals for Your Future. Investopedia. Available online: https://www.investopedia.com/articles/personal-finance/100516/settingfinancial-goals/fromhttps://www.churchillretirement.co.uk/assets/ResearchPublications/hsbcreport-6.pdf (accessed on 20 November 2022).

- Hastings, J.S.; Madrian, B.C.; Skimmyhorn, W.L. Financial literacy, financial education, and economic outcomes. Annu. Rev. Econ. 2013, 5, 347–373. [Google Scholar] [CrossRef] [PubMed]

- Act 753: Minimum Retirement Age Act 2012. Laws of Malaysia. Available online: http://www.mohr.gov.my/pdf/MINRETIREAGE/ACT_753_MRA_%202012.pdf (accessed on 20 November 2022).

- Ambigga, K.S.; Ramli, A.S.; Ariaratnam, S.; Norlaili, T.; Clearihan, L.; Colette, B. Bridging the gap in ageing: Translating policies into practice in Malaysian primary care. Asia Pac. Fam. Med. 2011, 10. [Google Scholar] [CrossRef]

- Nilsson, K.; Hydbom, A.R.; Rylander, L. Factors influencing the decision to extend working life or retire. Scand J. Work Environ. Health 2011, 37, 473–480. [Google Scholar] [CrossRef] [PubMed]

- Surendran, S. Malaysian Investors most Indebted in Asia-Manulife Survey. Available online: https://www.theedgemarkets.com/article/malaysian-investors-most-indebted-asia-manulife-survey (accessed on 20 November 2022).

- Ling, G.S.; Fernandez, J.L. Labour force participation of elderly persons in Penang. In Proceedings of the International Conference on Business and Economic Research Sarawak, Sarawak, Malaysia, 15 March 2010; pp. 15–16. [Google Scholar]

- Van Rooij, M.C.J.; Lusardi, A.; Alessie, R.J.M. Financial literacy, retirement planning and household wealth. Econ. J. 2012, 122, 449–478. [Google Scholar] [CrossRef]

- Suzman, R.; Beard, J. World Health Organization Webpage. Available online: http://www.who.int/ageing/publications/global_health.pdf (accessed on 20 November 2022).

- Tan, S.; Singaravelloo, K. Financial literacy and retirement planning among government officers in Malaysia. Int. J. Public Adm. 2020, 43, 486–498. [Google Scholar] [CrossRef]

- Gallego-Losada, R.; Montero-Navarro, A.; Rodríguez-Sánchez, J.L.; González-Torres, T. Retirement planning and financial literacy, at the crossroads. A bibliometric analysis. Financ. Res. Lett. 2022, 44, 102109. [Google Scholar] [CrossRef]

- Boon, T.H.; Yee, H.S.; Ting, H.W. Financial literacy and personal financial planning in Klang Valley, Malaysia. Int. J. Econ. Manag. 2011, 5, 149–168. [Google Scholar]

- Moorthy, K.; Durai, T.; Chiau, S.S.; Lai, C.L.; Ng, Z.K.; Wong, C.R.; Wong, Y.T. A study on the retirement planning behaviour of working individuals in Malaysia. Int. J. Acad. Res. Econ. Manag. Sci. 2012, 1. [Google Scholar]

- Mutran, E.J.; Reitzes, D.C.; Fernandez, M.E. Factors that influence attitudes toward retirement. Res. Aging 1997, 19, 251–273. [Google Scholar] [CrossRef]

- Safari, K.; Njoka, C.; Munkwa, M.G. Financial literacy and personal retirement planning: A socioeconomic approach. J. Bus. Socio-Econ. Dev. 2021, 1, 121–134. [Google Scholar] [CrossRef]

- Selvadurai, V.; Kenayathulla, H.B.; Siraj, S. Financial literacy education and retirement planning in Malaysia. MOJEM Malays. Online J. Educ. Manag. 2018, 6, 41–66. [Google Scholar] [CrossRef]

- Chaffin, C.R. The Financial Planning Competency Handbook; John Wiley& Sons, Inc.: Toronto, ON, Canada, 2013. [Google Scholar]

- Crown, W.H. Life Cycle Theories of Savings and Consumption. Encyclopedia of Aging, 2002. Available online: https://medicine.jrank.org/pages/983/Life-Cycle-Theories-Savings-Consumption-Implications-aggregate-savings-consumption-patterns.html (accessed on 25 November 2022).

- Baranzini, M. (2005). Modigliani’s life-cycle theory of savings fifty years later. PSL Q. Rev. 2005, 58, 233–234. [Google Scholar] [CrossRef]

- Gythfeldt, K. Modigliani’s Life Cycle Hypothesis Presence amongst Norwegian Pensioners. Unpublished Master Thesis, Lund University, Lund, Sweden, 2008. [Google Scholar]

- Chowa, G.A.N.; Despard, M.; Osei-Akoto, I. Financial Knowledge and Attitudes of Youth in Ghana. (YouthSave Research Brief No. 12-37). Available online: https://csd.wustl.edu/publications/Documents/RB12-37.pdf (accessed on 25 November 2022).

- Atkinson, A.; Messy, F.A. Measuring Financial Literacy: Results of the OECD; OECD Publishing: Paris, France, 2012. [Google Scholar]

- Cabler, J. Celebrating Financial Freedom. Available online: https://www.cfinancialfreedom.com/9-tips-creating-discipline-with-money/ (accessed on 26 November 2022).

- Mohidin, R.; Jamal, A.A.A.; Geetha, C.; Sang, L.T.; Karim, M.R.A.; Abdul Karim, M. Revisiting the relationship between attitudes and retirement planning behavior: A study on personal financial planning. Int. J. Multidiscip. Thought 2013, 3, 449–461. [Google Scholar]

- Talib, N.F.M.; Manaf, H.A. Attitude towards retirement planning behaviour among employee’s. Int. J. Bus. Manag. 2017, 1, 12–17. [Google Scholar]

- Hassan, K.H.; Rahim, R.A.; Ahmad, F.; Zainuddin, T.N.A.T.; Merican, R.R.; Bahari, S.K. Retirement planning behaviour of working individuals and legal proposition for new pension system in Malaysia. J. Pol. L. 2016, 9, 43. [Google Scholar] [CrossRef]

- Hung, A.A.; Parker, A.M.; Yoong, J.K. Defining and Measuring Financial Literacy. (RAND Working Paper 708). Available online: https://www.rand.org/content/dam/rand/pubs/working_papers/2009/RAND_WR708.pdf (accessed on 26 November 2022).

- Van Dijk, N. The Effect of Financial Literacy on Retirement Planning among Dutch Students. Unpublished Master Thesis, University of Amsterdam, Amsterdam, The Netherlands, 2012. [Google Scholar]

- Lusardi, A.; Mitchell, O. Financial Literacy and Planning: Implications for Retirement Wellbeing (Working Paper No. 17078). National Bureau of Economic Research. Available online: http://www.nber.org/papers/w17078.pdf (accessed on 20 November 2022).

- Moure, N.G. Financial literacy and retirement planning in Chile. J. Pension Econ. Financ. 2016, 15, 203. [Google Scholar] [CrossRef]

- Nguyen, T.A.N.; Belás, J.; Habánik, J.; Schönfeld, J. Preconditions of financial safety during lifecycle: The financial literacy and retirement planning in Vietnam. J. Secur. Sustain. Issues 2017, 6, 627–636. [Google Scholar] [CrossRef]

- Naccarella, L.; Wraight, B.; Gorman, D. Is health workforce planning recognising the dynamic interplay between health literacy at an individual, organisation and system level? Aust. Health Rev. 2016, 40, 33–35. [Google Scholar] [CrossRef]

- Vaillant, N.; Wolff, F.C. On the reliability of self-reported health: Evidence from Albanian data. J. Epidemiol. Glob. Health 2012, 2, 83–98. [Google Scholar] [CrossRef] [PubMed]

- James, B.D.; Boyle, P.A.; Bennett, J.S.; Bennett, D.A. The impact of health and financial literacy on decision making in community-based older adults. Gerontology 2012, 58, 531–539. [Google Scholar] [CrossRef]

- Carr, N.A.; Sages, R.A.; Fernatt, F.R.; Nabeshima, G.G.; Grable, J.E. Health information search and retirement planning. J. Financ. Couns. Plan. 2015, 26, 3–16. [Google Scholar] [CrossRef]

- Amoah, P.A. Social participation, health literacy, and health and well-being: A cross-sectional study in Ghana. SSM-Popul. Health 2018, 4, 263–270. [Google Scholar] [CrossRef] [PubMed]

- Wilson, R.S.; Yu, L.; James, B.D.; Bennett, D.A.; Boyle, P.A. Association of financial and health literacy with cognitive health in old age. Aging Neuropsychol. Cogn. 2017, 24, 186–197. [Google Scholar] [CrossRef] [PubMed]

- Yap, M.H. Set Yourself Free: How to Optimise your Money and Become Wealthy with Minimum Effort and Risk; Whitman Independent Advisors Sdn Bhd: Selangor, Malaysia, 2012. [Google Scholar]

- Marsden, M.; Zick, C.D.; Mayer, R.N. The value of seeking financial advice. J. Fam. Econ. Issues 2011, 32, 625–643. [Google Scholar] [CrossRef]

- Azjen. I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211.

- Kim, K.T.; Pak, T.Y.; Shin, S.H.; Hanna, S.D. The relationship between financial planner use and holding a retirement saving goal: A propensity score matching analysis. Financ. Plan. Rev. 2018, 1. [Google Scholar] [CrossRef]

- Rickwood, C.M.; Johnson, L.W.; Worthington, S.; White, L. Customer intention to save for retirement using a professional financial services planner. Financ. Plan. Res. J. 2017, 1, 47–67. [Google Scholar]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business, 6th ed.; Wiley: Oxford, UK, 2013. [Google Scholar]

- Hassan, M.; Islam, M.A.; Sobhani, F.A.; Hassan, M.M.; Hassan, M.A. Patients’ Intention to Adopt Fintech Services: A Study on Bangladesh Healthcare Sector. Int. J. Environ. Res. Public Health 2022, 19, 15302. [Google Scholar] [CrossRef] [PubMed]

- Mahlanza, T.J. Factors Influencing Retirement Savings Intentions in Botswana. Unpublish Doctoral Dissertation, Deakin University, Melbourne, VIC, Australia , 2015. [Google Scholar]

- Fernandes, D.; Lynch Jr, J.G.; Netemeyer, R.G. Financial literacy, financial education, and downstream financial behaviours. Manag. Sci. 2014, 60, 1861–1883. [Google Scholar] [CrossRef]

- Nga, K.H.; Yeoh, K.K. An exploratory model on retirement savings behaviour: A Malaysian study. Int. J. Bus. Soc. 2018, 19, 637–659. [Google Scholar]

- Vlam, A. Customer First? The Relationship between Advisors and Consumers of Financial Products. Doctoral Dissertation, Erasmus University Rotterdam, Rotterdam, The Netherlands.

- Hair, J.F.; Hult, M.T.G.; Ringle, M.C.; Sarstedt, M. A Premier on Partial Least Squares Structural Equation Modeling (PLS-SEM); SAGE Publications Asia-Pacific Pte. Ltd.: Singapore, 2017. [Google Scholar]

- Tabachnick, B.G.; Fidell, L.S. Experimental Designs Using ANOVA (Vol. 724); Thomson/Brooks/Cole: Belmont, CA, USA, 2007. [Google Scholar]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1986, 18. [Google Scholar] [CrossRef]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Erlbaum: Hillsdale, NJ, USA, 1988. [Google Scholar]

- Preacher, K.J.; Rucker, D.D.; Hayes, A.F. Addressing moderated mediation hypotheses: Theory, methods, and prescriptions. Multivar. Behav. Res. 2007, 42, 185–227. [Google Scholar] [CrossRef]

- Forbes. The Five Biggest Financial Regrets in America (And How to Avoid Them). Available online: https://www.forbes.com/sites/forbesfinancecouncil/2017/06/15/the-five-biggest-financial-regrets-in-america-and-how-to-avoid-them/?sh=45f3964a1058 (accessed on 20 November 2022).

- García, J.M.; Vila, J. Financial literacy is not enough: The role of nudging toward adequate long-term saving behavior. J. Bus. Res. 2020, 112, 472–477. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Older Adult Debt and Financial Frailty. Michigan Retirement Research Center Research Paper, 2013. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2376493 (accessed on 20 November 2022).

- OECD. Pensions at a Glance 2013: OECD and G20 Indicators Older Workers. CAEL. Available online: http://www.cael.org/pdfs/tmt_financial_literacy (accessed on 20 November 2022).

- Thakur, R.; Hale, D.; AlSaleh, D. Retirement planning: Its application to marketing practices. Health Mark. Q. 2020, 37, 91–107. [Google Scholar] [CrossRef]

- Grable, J.E.; Chatterjee, S. Reducing Wealth Volatility: The Value of Financial Advice as Measured by Zeta. J. Financ. Plan. 2014, 27, 45–51. [Google Scholar]

- Robb, C.A.; Babiarz, P.; Woodyard, A. The demand for financial professionals’ advice: The role of financial knowledge, satisfaction, and confidence. Financ. Serv. Rev. 2012, 21, 291–305. [Google Scholar]

- Hanna, S.D.; Lindamood, S. Quantifying the economic benefits of personal financial planning. Financ. Serv. Rev. 2010, 19, 111–127. [Google Scholar]

- Newton, C.; Corones, S.; Irving, K.; Thomas, D. The Value of Financial Planning Advice: Process and Outcome Effects on Consumer Well-Being [Time 1 and 2 Survey Summary Results]; Queensland University of Technology: Brisbane, QLD, Australia, 2015. [Google Scholar]

| Respondent Description | Frequency | Percentage % |

|---|---|---|

| Age 30–39 years 40–50 years Above 51 years | 40 259 117 | 9.6 62.3 28.1 |

| Gender Male Female | 328 88 | 78.8 21.2 |

| Academic Qualifications SPM STPM Diploma Degree and above | 178 123 90 25 | 42.8 29.6 21.6 6.0 |

| Types of Business Sole proprietorship Partnership Private limited | 17 106 293 | 4.1 25.5 70.4 |

| Business Experience 0–14 years 15–24 years More than 25 years | 83 273 60 | 20 65.6 14.4 |

| Place of Business Urban Rural | 383 33 | 92.1 7.9 |

| CONSTRUCTS | ITEMS | LOADINGS | CR | AVE |

|---|---|---|---|---|

| FINANCIAL ATTITUDE | FATT01 | 0.841 | ||

| FATT02 | 0.847 | |||

| FATT03 | 0.822 | |||

| FATT04 | 0.812 | 0.852 | 0.763 | |

| FATT05 | 0.735 | |||

| FATT06 | 0.897 | |||

| FATT07 | 0.768 | |||

| FATT08 | 0.901 | |||

| FINANCIAL LITERACY | FLIT01 | 0.878 | ||

| FLIT02 | 0.803 | |||

| FLIT03 | 0.839 | |||

| FLIT04 | 0.767 | 0.876 | 0.726 | |

| FLIT05 | 0.854 | |||

| FLIT06 | 0.861 | |||

| FLIT07 | 0.807 | |||

| FLIT08 | 0.825 | |||

| FINANCIAL RETIREMENT PLANNING | FRP01 | 0.825 | ||

| FRP02 | 0.871 | |||

| FRP03 | 0.853 | |||

| FRP04 | 0.911 | 0.903 | 0.805 | |

| FRP05 | 0.808 | |||

| FRP06 | 0.812 | |||

| FRP07 | 0.832 | |||

| FRP08 | 0.922 | |||

| HEALTH LITERACY | HLIT01 | 0.781 | ||

| HLIT02 | 0.862 | |||

| HLIT04 | 0.774 | |||

| HLIT05 | 0.811 | 0.746 | 0.715 | |

| HLIT06 | 0.849 | |||

| HLIT07 | 0.881 | |||

| HLIT08 HLIT09 | 0.879 0.853 | |||

| ROLE OF FINANCIAL ADVISOR | FAD02 | 0.819 | ||

| FAD03 | 0.793 | |||

| FAD04 | 0.821 | |||

| FAD05 | 0.879 | |||

| FAD06 | 0.754 | |||

| FAD08 | 0.833 | |||

| FAD09 | 0.865 | 0.878 | 0.726 | |

| FAD10 FAD11 | 0.844 0.881 | |||

| FAD12 FAD13 | 0.802 0.825 | |||

| FAD14 FAD16 | 0.855 0.872 |

| FATT | FLIT | FRP | HLIT | FAD | |

|---|---|---|---|---|---|

| FATT | 0.873 | ||||

| FLIT | 0.713 | 0.852 | |||

| FRP | 0.702 | 0.727 | 0.897 | ||

| HLIT | 0.647 | 0.698 | 0.717 | 0.846 | |

| FAD | 0.451 | 0.485 | 0.453 | 0.427 | 0.852 |

| Construct | VIF |

|---|---|

| Financial Attitude | 2.743 |

| Financial Literacy | 2.619 |

| Financial Retirement Planning | 2.833 |

| Health Literacy | 2.524 |

| Role of Financial Advisor | 2.738 |

| Hypotheses | Relationship | Beta | T-Values | p-Values | R2 | f2 | Q2 |

|---|---|---|---|---|---|---|---|

| H1 | FATT → FRP | 0.437 | 6.138 | 0.001 | 0.369 | ||

| H2 | FLIT → FRP | 0.391 | 5.836 | 0.001 | 0.663 | 0.383 | 0.431 |

| H3 | HLIT → FRP | 0.093 | 1.124 | 0.126 | 0.012 |

| Hypotheses | Relationship | Beta | T-Values | p-Values |

|---|---|---|---|---|

| H4 | FAD*FATT → FRP | 0.359 | 6.817 | 0.001 |

| H5 | FAD*FLIT → FRP | 0.411 | 3.552 | 0.001 |

| H6 | FAD*HLIT → FRP | 0.038 | 1.235 | 0.104 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mustafa, W.M.W.; Islam, M.A.; Asyraf, M.; Hassan, M.S.; Royhan, P.; Rahman, S. The Effects of Financial Attitudes, Financial Literacy and Health Literacy on Sustainable Financial Retirement Planning: The Moderating Role of the Financial Advisor. Sustainability 2023, 15, 2677. https://doi.org/10.3390/su15032677

Mustafa WMW, Islam MA, Asyraf M, Hassan MS, Royhan P, Rahman S. The Effects of Financial Attitudes, Financial Literacy and Health Literacy on Sustainable Financial Retirement Planning: The Moderating Role of the Financial Advisor. Sustainability. 2023; 15(3):2677. https://doi.org/10.3390/su15032677

Chicago/Turabian StyleMustafa, Wan Mashumi Wan, Md. Aminul Islam, Muhammad Asyraf, Md. Sharif Hassan, Pradip Royhan, and Shafiqur Rahman. 2023. "The Effects of Financial Attitudes, Financial Literacy and Health Literacy on Sustainable Financial Retirement Planning: The Moderating Role of the Financial Advisor" Sustainability 15, no. 3: 2677. https://doi.org/10.3390/su15032677

APA StyleMustafa, W. M. W., Islam, M. A., Asyraf, M., Hassan, M. S., Royhan, P., & Rahman, S. (2023). The Effects of Financial Attitudes, Financial Literacy and Health Literacy on Sustainable Financial Retirement Planning: The Moderating Role of the Financial Advisor. Sustainability, 15(3), 2677. https://doi.org/10.3390/su15032677