Has Digital Financial Inclusion Narrowed the Urban–Rural Income Gap? A Study of the Spatial Influence Mechanism Based on Data from China

Abstract

:1. Introduction

2. Literature Review and Theoretical Analysis

2.1. Digital Financial Inclusion and Urban–Rural Income Gap

2.2. The Spatial Spillover Effect of Digital Financial Inclusion on Urban–Rural Income Gap

2.3. Transmission Mechanism: The Mediating Role of Industrial Structure Upgrading

3. Methods

3.1. Variables and Data

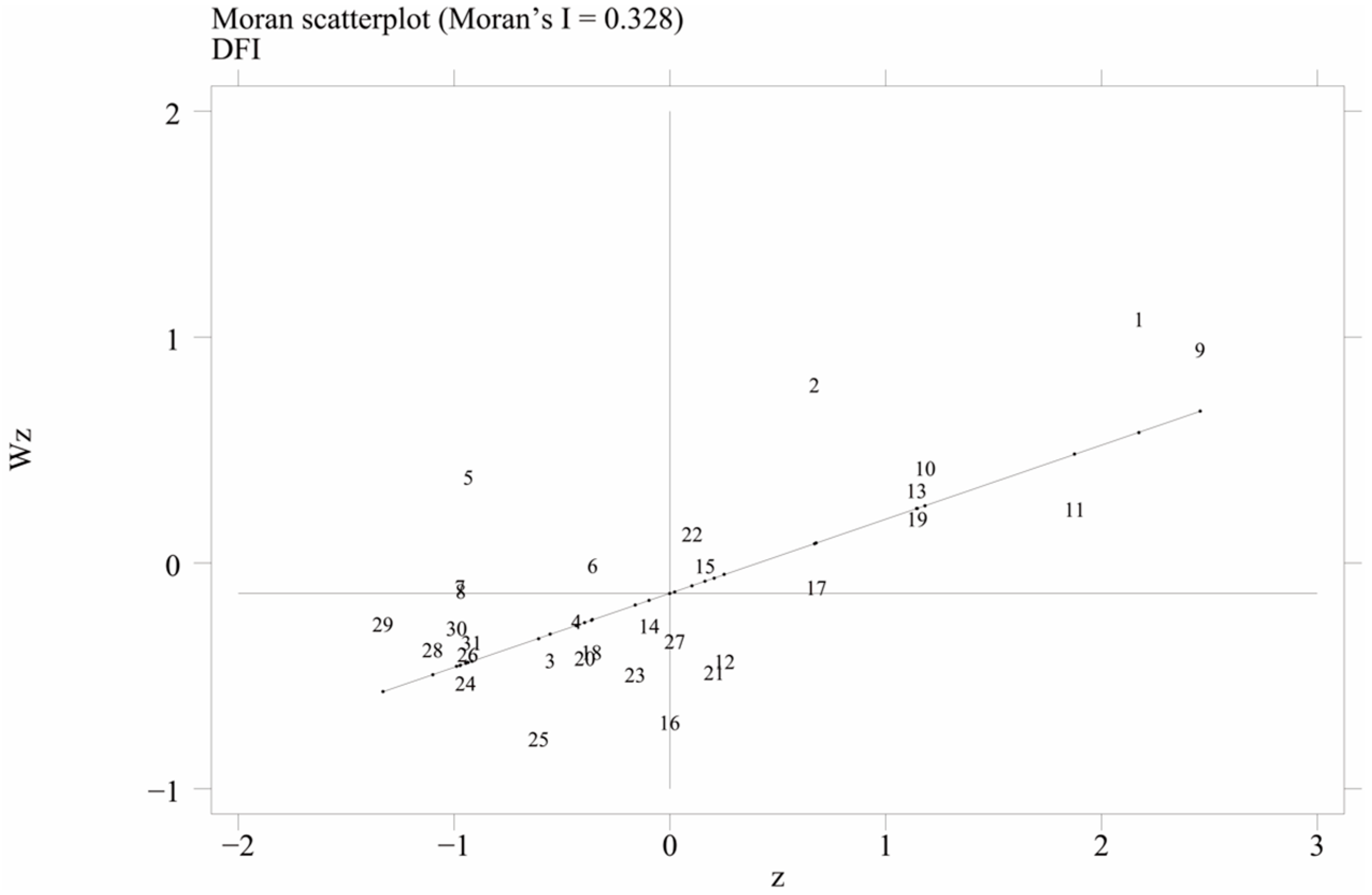

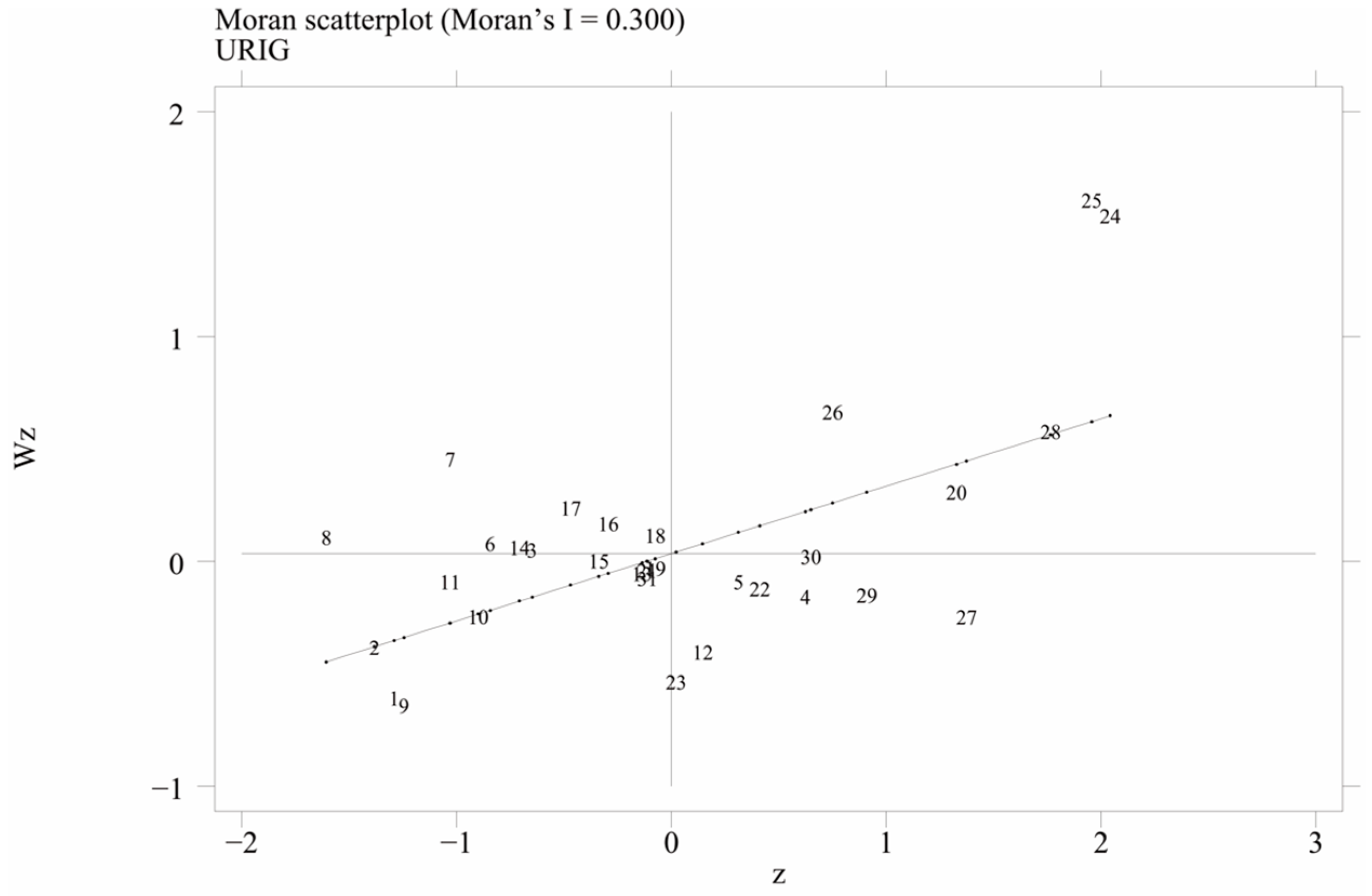

3.2. Spatial Correlation Test

3.3. Model Formulation

4. Results and Discussion

4.1. Main Findings

4.2. Test of Robustness

4.3. Test of Endogeneity

4.4. Test of the Spatial Influence Mechanism

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- World Bank. China Systematic Country Diagnostic: Towards a More Inclusive and Sustainable Development. 2018. Available online: https://openknowledge.worldbank.org/handle/10986/29422 (accessed on 1 May 2022).

- Chen, J.; Fang, F.; Hou, W.; Li, F.; Pu, M.; Song, M. Chinese Gini Coefficient from 2005 to 2012, Based on 20 Grouped Income Data Sets of Urban and Rural Residents. J. Appl. Math. 2015, 2015, 939020. [Google Scholar] [CrossRef] [Green Version]

- Wan, G.H. Understanding Regional Poverty and Inequality Trends in China: Methodological Issues and Empirical Findings. Rev. Income Wealth 2007, 53, 25–34. [Google Scholar] [CrossRef]

- Yuan, Y.; Wang, M.; Zhu, Y.; Huang, X.; Xiong, X. Urbanization’s effects on the urban-rural income gap in China: A meta-regression analysis. Land Use Policy 2020, 99, 104995. [Google Scholar] [CrossRef]

- Su, C.-W.; Liu, T.-Y.; Chang, H.-L.; Jiang, X.-Z. Is urbanization narrowing the urban-rural income gap? A cross-regional study of China. Habitat Int. 2015, 48, 79–86. [Google Scholar] [CrossRef]

- Wang, L.J.; Zhang, M. Exploring the Impact of Narrowing Urban-Rural Income Gap on Carbon Emission Reduction and Pollution Control. PLoS ONE. 2021, 16, e0259390. [Google Scholar] [CrossRef] [PubMed]

- Yin, Z.H.; Choi, C.H. Does e-commerce narrow the urban–rural income gap? Evidence from Chinese provinces. Internet Res. 2022, 32, 1427–1452. [Google Scholar] [CrossRef]

- Ji, X.; Wang, K.; Xu, H.; Li, M. Has Digital Financial Inclusion Narrowed the Urban-Rural Income Gap: The Role of Entrepreneurship in China. Sustainability 2021, 13, 8292. [Google Scholar] [CrossRef]

- Bittencourt, M. Financial development and inequality: Brazil 1985–1994. Econ. Chang. Restruct. 2010, 43, 113–130. [Google Scholar] [CrossRef] [Green Version]

- Park, C.Y.; Mercado, R.V. Does Financial Inclusion Reduce Poverty and Income Inequality in Developing Asia? Financ. Incl. Asia 2016, 61–92. Available online: https://link.springer.com/chapter/10.1057/978-1-137-58337-6_3#citeas (accessed on 9 May 2022). [CrossRef]

- Chibba, M. Financial Inclusion, Poverty Reduction and the Millennium Development Goals. Eur. J. Dev. Res. 2009, 21, 213–230. [Google Scholar] [CrossRef]

- Dabla-Norris, E.; Ji, Y.; Townsend, R.M.; Unsal, D.F. Distinguishing constraints on financial inclusion and their impact on GDP, TFP, and the distribution of income. J. Monetary Econ. 2021, 117, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Park, C.-Y.; Mercado, R., Jr. Financial Inclusion, Poverty, and Income Inequality. Singap. Econ. Review. 2018, 63, 185–206. [Google Scholar] [CrossRef]

- Śledzik, K. Schumpeter’s Theory of Economic Development: An Evolutionary Perspective; Young Scientists Revue; Hittmar, S., Ed.; Faculty of Management Science and Informatics, University of Zilina: Žilina, Slovakia, 2015; Forthcoming; Available online: https://ssrn.com/abstract=2671179 (accessed on 22 May 2022).

- Gabor, D.; Brooks, S. The digital revolution in financial inclusion: International development in the fintech era. New Politi. Econ. 2017, 22, 423–436. [Google Scholar] [CrossRef] [Green Version]

- Wang, X.; Fu, Y. Digital financial inclusion and vulnerability to poverty: Evidence from Chinese rural households. China Agric. Econ. Rev. 2021, 14, 64–83. [Google Scholar] [CrossRef]

- Koomson, I.; Villano, R.A.; Hadley, D. Effect of Financial Inclusion on Poverty and Vulnerability to Poverty: Evidence Using a Multidimensional Measure of Financial Inclusion. Soc. Indic. Res. 2020, 149, 613–663. [Google Scholar] [CrossRef]

- Krumer-Nevo, M.; Gorodzeisky, A.; Saar-Heiman, Y. Debt, poverty, and financial exclusion. J. Soc. Work. 2017, 17, 511–530. [Google Scholar] [CrossRef]

- Jiang, X.; Wang, X.; Ren, J.; Xie, Z. The Nexus between Digital Finance and Economic Development: Evidence from China. Sustainability 2021, 13, 7289. [Google Scholar] [CrossRef]

- Kotarski, K. Financial Deepening and Income Inequality: Is there any Financial Kuznets Curve in China? The Political Economy Analysis. China Econ. J. 2015, 8, 18–39. [Google Scholar] [CrossRef]

- Li, J.; Gu, Y.; Zhang, C. Hukou-Based Stratification in Urban China’s Segmented Economy. Chin. Sociol. Rev. 2015, 47, 154–176. [Google Scholar] [CrossRef]

- Liu, Y.; Lu, S.; Chen, Y. Spatio-temporal change of urban–rural equalized development patterns in China and its driving factors. J. Rural. Stud. 2013, 32, 320–330. [Google Scholar] [CrossRef]

- Huang, Y.; Zhang, Y. Financial Inclusion and Urban–Rural Income Inequality: Long-Run and Short-Run Relationships. Emerg. Mark. Financ. Trade 2020, 56, 457–471. [Google Scholar] [CrossRef]

- Williams, J.W. Feeding finance: A critical account of the shifting relationships between finance, food and farming. Econ. Soc. 2014, 43, 401–431. [Google Scholar] [CrossRef]

- Kabakova, O.; Plaksenkov, E. Analysis of factors affecting financial inclusion: Ecosystem view. J. Bus. Res. 2018, 89, 198–205. [Google Scholar] [CrossRef]

- Anand, S.; Chhikara, K.S. A Theoretical and Quantitative Analysis of Financial Inclusion and Economic Growth. Manag. Labour Stud. 2013, 38, 103–133. [Google Scholar] [CrossRef]

- Song, J.; Zhou, H.; Gao, Y.; Guan, Y. Digital Inclusive Finance, Human Capital and Inclusive Green Development—Evidence from China. Sustainability 2022, 14, 9922. [Google Scholar] [CrossRef]

- Ebong, J.; George, B. Financial Inclusion through Digital Financial Services (DFS): A Study in Uganda. J. Risk Financ. Manag. 2021, 14, 393. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Berger, A.N. The Economic Effects of Technological Progress: Evidence from the Banking Industry. J. Money Crédit. Bank. 2003, 35, 141–176. [Google Scholar] [CrossRef] [Green Version]

- Lashitew, A.A.; van Tulder, R.; Liasse, Y. Mobile phones for financial inclusion: What explains the diffusion of mobile money innovations? Res. Policy 2019, 48, 1201–1215. [Google Scholar] [CrossRef]

- Mushtaq, R.; Bruneau, C. Microfinance, Financial Inclusion and ICT: Implications for Poverty and Inequality. Technol. Soc. 2019, 59, 101154. [Google Scholar] [CrossRef]

- Polloni-Silva, E.; da Costa, N.; Moralles, H.F.; Neto, M.S. Does Financial Inclusion Diminish Poverty and Inequality? A Panel Data Analysis for Latin American Countries. Soc. Indic. Res. 2021, 158, 889–925. [Google Scholar] [CrossRef] [PubMed]

- Senyo, P.; Osabutey, E.L. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 2020, 98, 102155. [Google Scholar] [CrossRef]

- Malladi, C.M.; Soni, R.K.; Srinivasan, S. Digital financial inclusion: Next frontiers—Challenges and opportunities. CSI Trans. ICT 2021, 9, 127–134. [Google Scholar] [CrossRef]

- Vasile, V.; Panait, M.; Apostu, S.A. Financial Inclusion Paradigm Shift in the Postpandemic Period. Digital-Divide and Gender Gap. Int. J. Environ. Res. Public Health 2021, 18, 10938. [Google Scholar] [CrossRef]

- Bernardí, C.B.; Guadalupe, S.D. Innovation and R&D Spillover Effects in Spanish Regions: A Spatial Approach. Res. Policy 2007, 36, 1357–1371. [Google Scholar] [CrossRef]

- Wang, C.; Wang, L.; Xue, Y.; Li, R. Revealing Spatial Spillover Effect in High-Tech Industry Agglomeration from a High-Skilled Labor Flow Network Perspective. J. Syst. Sci. Complex. 2022, 35, 839–859. [Google Scholar] [CrossRef]

- Song, X.-L.; Jing, Y.-G.; Akeba’Erjiang, K. Spatial econometric analysis of digital financial inclusion in China. Int. J. Dev. Issues 2020, 20, 210–225. [Google Scholar] [CrossRef]

- Liu, X.; Zhu, J.; Guo, J.; Cui, C. Spatial Association and Explanation of China’s Digital Financial Inclusion Development Based on the Network Analysis Method. Complexity 2021, 2021, 6649894. [Google Scholar] [CrossRef]

- Xu, L.; Tan, J. Financial development, industrial structure and natural resource utilization efficiency in China. Resour. Policy 2020, 66, 101642. [Google Scholar] [CrossRef]

- Yu, X.; Li, M.; Huang, S. Financial Functions and Financial Development in China: A Spatial Effect Analysis. Emerg. Mark. Finance Trade 2017, 53, 2052–2062. [Google Scholar] [CrossRef]

- Yu, C.; Jia, N.; Li, W.; Wu, R. Digital Inclusive Finance and Rural Consumption Structure—Evidence from Peking University Digital Inclusive Financial Index and China Household Finance Survey. China Agric. Econ. Rev. 2022, 14, 165–183. [Google Scholar] [CrossRef]

- Li, J.; Li, B. Digital inclusive finance and urban innovation: Evidence from China. Rev. Dev. Econ. 2021, 26, 1010–1034. [Google Scholar] [CrossRef]

- Yang, L.; Zhang, Y. Digital Financial Inclusion and Sustainable Growth of Small and Micro Enterprises—Evidence Based on China’s New Third Board Market Listed Companies. Sustainability 2020, 12, 3733. [Google Scholar] [CrossRef]

- Wang, X.; Guan, J. Financial inclusion: Measurement, spatial effects and influencing factors. Appl. Econ. 2017, 49, 1751–1762. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alshirah, M.; Alshira’H, A.; Abutaber, T.; Almarashdah, M. Digital Financial Inclusion Sustainability in Jordanian Context. Sustainability 2021, 13, 6312. [Google Scholar] [CrossRef]

- Lu, Y.L. Does Hukou Still Matter? The Household Registration System and its Impact on Social Stratification and Mobility in China. Soc. Sci. China 2008, 29, 56–75. [Google Scholar] [CrossRef]

- Wu, J.; Yu, Z.; Wei, Y.D.; Yang, L. Changing distribution of migrant population and its influencing factors in urban China: Economic transition, public policy, and amenities. Habitat Int. 2019, 94, 102063. [Google Scholar] [CrossRef]

- Su, Y.; Li, Z.; Yang, C. Spatial Interaction Spillover Effects between Digital Financial Technology and Urban Ecological Efficiency in China: An Empirical Study Based on Spatial Simultaneous Equations. Int. J. Environ. Res. Public Health 2021, 18, 8535. [Google Scholar] [CrossRef]

- Lyu, L.; Sun, F.; Huang, R. Innovation-Based Urbanization: Evidence from 270 Cities at the Prefecture Level or above in China. J. Geogr. Sci. 2019, 29, 1283–1299. [Google Scholar] [CrossRef]

- Xie, W.; Wang, T.; Zhao, X. Does Digital Inclusive Finance Promote Coastal Rural Entrepreneurship? J. Coast. Res. 2020, 103, 240–245. [Google Scholar] [CrossRef]

- Aisaiti, G.; Liu, L.; Xie, J.; Yang, J. An Empirical Analysis of Rural Farmers’ Financing Intention of Inclusive Finance in China: The Moderating Role of Digital Finance and Social Enterprise Embeddedness. Ind. Manag. Data Syst. 2019, 119, 1535–1563. [Google Scholar] [CrossRef]

- Sun, Y.; Tang, X.W. The Impact of Digital Inclusive Finance on Sustainable Economic Growth in China. Finance Res. Lett. 2022, 50, 103234. [Google Scholar] [CrossRef]

- Bruhn, M.; Love, I. The Real Impact of Improved Access to Finance: Evidence from Mexico. J. Financ. 2014, 69, 1347–1376. [Google Scholar] [CrossRef]

- Wang, X.; He, G. Digital Financial Inclusion and Farmers’ Vulnerability to Poverty: Evidence from Rural China. Sustainability 2020, 12, 1668. [Google Scholar] [CrossRef] [Green Version]

- Sasidharan, S.; Lukose, P.J.J.; Komera, S. Financing Constraints and Investments in R&D: Evidence from Indian Manufacturing Firms. Q. Rev. Econ. Financ. 2015, 55, 28–39. [Google Scholar] [CrossRef]

- Liang, C.; Du, G.; Cui, Z.; Faye, B. Does Digital Inclusive Finance Enhance the Creation of County Enterprises? Taking Henan Province as a Case Study. Sustainability 2022, 14, 14542. [Google Scholar] [CrossRef]

- Liu, J.; Li, X.; Liu, S.; Rahman, S.; Sriboonchitta, S. Addressing Rural-Urban Income Gap in China through Farmers’ Education and Agricultural Productivity Growth via Mediation and Interaction Effects. Agriculture 2022, 12, 1920. [Google Scholar] [CrossRef]

- Liu, Y.; Liu, C.; Zhou, M. Does Digital Inclusive Finance Promote Agricultural Production for Rural Households in China? Research based on the Chinese family database (CFD). China Agric. Econ. Rev. 2021, 13, 475–494. [Google Scholar] [CrossRef]

- Ge, H.; Li, B.; Tang, D.; Xu, H.; Boamah, V. Research on Digital Inclusive Finance Promoting the Integration of Rural Three-Industry. Int. J. Environ. Res. Public Health 2022, 19, 3363. [Google Scholar] [CrossRef]

- Li, K.; He, M.M.; Huo, J.J. Digital Inclusive Finance and Asset Allocation of Chinese Residents: Evidence from the China Household Finance Survey. PLoS ONE 2022, 17, e0267055. [Google Scholar] [CrossRef] [PubMed]

- Su, J.; Su, K.; Wang, S. Does the Digital Economy Promote Industrial Structural Upgrading?—A Test of Mediating Effects Based on Heterogeneous Technological Innovation. Sustainability 2021, 13, 10105. [Google Scholar] [CrossRef]

- Kang, X. The Impact of Family Social Network on Household Consumption. Mod. Econ. 2019, 10, 679. [Google Scholar] [CrossRef] [Green Version]

- Guan, H.; Guo, B.; Zhang, J. Study on the Impact of the Digital Economy on the Upgrading of Industrial Structures—Empirical Analysis Based on Cities in China. Sustainability 2022, 14, 11378. [Google Scholar] [CrossRef]

- Li, Y.; Wang, M.; Liao, G.; Wang, J. Spatial Spillover Effect and Threshold Effect of Digital Financial Inclusion on Farmers’ Income Growth—Based on Provincial Data of China. Sustainability 2022, 14, 1838. [Google Scholar] [CrossRef]

- Sun, Z.S.; Cao, C.S.; He, Z.X.; Feng, C. Examining the Coupling Coordination Relationship between Digital Inclusive Finance and Technological Innovation from a Spatial Spillover Perspective: Evidence from China. Emerg. Mark. Financ. Trade 2022, 1–13. Available online: https://www.tandfonline.com/doi/abs/10.1080/1540496X.2022.2120766 (accessed on 10 October 2022). [CrossRef]

- Shen, Y.; Hueng, C.J.; Hu, W.X. Measurement and Spillover Effect of Digital Financial Inclusion: A Cross-Country Analysis. Appl. Econ. Lett. 2021, 28, 1738–1743. [Google Scholar] [CrossRef]

- Yang, R.; Zhong, C.; Yang, Z.; Wu, Q. Analysis on the Effect of the Targeted Poverty Alleviation Policy on Narrowing the Urban-Rural Income Gap: An Empirical Test Based on 124 Counties in Yunnan Province. Sustainability 2022, 14, 12560. [Google Scholar] [CrossRef]

- Guo, F.; Wang, J.Y.; Wang, F.; Kong, T.; Zhang, X.; Cheng, Z.Y. Evaluating the Development of China’s Digital Financial Inclusion: Index Compilation and Spatial Characteristics. China Econ. Q. 2020, 19, 1401–1418. (In Chinese) [Google Scholar] [CrossRef]

- Corrado, G.; Corrado, L. Inclusive Finance for Inclusive Growth and Development. Curr. Opin. Environ. Sustain. 2017, 24, 19–23. [Google Scholar] [CrossRef]

- Han, J.; Wang, J.; Ma, X. Effects of Farmers’ Participation in Inclusive Finance on their Vulnerability to Poverty: Evidence from Qinba Poverty-Stricken Area in China. Emerg. Mark. Financ. Trade 2019, 55, 998–1013. [Google Scholar] [CrossRef]

- Kelikume, I. Digital Financial Inclusion, Informal Economy and Poverty Reduction in Africa. J. Enterprising Communities People Places Glob. Econ. 2021, 15, 626–640. [Google Scholar] [CrossRef]

- Peng, H.; Wang, J.J.; Wen, L.; Ding, P.; Zhu, Y.J. Is the Development of Inclusive Finance Truly Able to Alleviate Poverty? An Empirical Study Based on Spatial Effect and Threshold Effect. Emerg. Mark. Financ. Trade 2022, 58, 2505–2521. [Google Scholar] [CrossRef]

- Liu, T.; He, G.; Turvey, C.G. Inclusive Finance, Farm Households Entrepreneurship, and Inclusive Rural Transformation in Rural Poverty-Stricken Areas in China. Emerg. Mark. Financ. Trade 2021, 57, 1929–1958. [Google Scholar] [CrossRef]

- Shao, S.; Li, X.; Cao, J.H.; Yang, L.L. China’s Economic Policy Choices for Governing Smog Pollution Based on Spatial Spillover Effects. Econ. Res. J. 2016, 51, 73–88. (In Chinese) [Google Scholar]

- Elhorst, J.P. Matlab Software for Spatial Panels. Int. Reg. Sci. Rev. 2014, 37, 389–405. [Google Scholar] [CrossRef] [Green Version]

- Lesage, J.; Pace, R.K. Introduction to Spatial Econometrics; CRC Press: Boca Raton, FL, USA, 2009. [Google Scholar]

- Baron, R.M.; Kenny, D.A. The Moderator-Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Control Variables | Definition |

|---|---|

| open | ratio of actual amount of foreign investment to GDP |

| urban | ratio of urban employed population to total population |

| GDP | log value of per capita GDP |

| social | ratio of social security and employment expenditures to total fiscal expenditures |

| fiscal | ratio of local government fiscal revenue to total fiscal expenditures |

| government | ratio of fiscal expenditures to GDP |

| edu | ratio of illiterate population to the population aged 15 and over |

| ageing | ratio of elderly population to working population |

| unemployment | ratio of unemployed population to working population |

| Variables | Obs | Mean | Std. | Min | Max | |

|---|---|---|---|---|---|---|

| Explained Variable | URIG | 279 | 2.6556 | 0.4217 | 1.8451 | 3.9792 |

| Main Explanatory Variables | DFI | 279 | 5.1432 | 0.6785 | 2.7862 | 6.0168 |

| breadth | 279 | 4.9790 | 0.8518 | 0.6729 | 5.9523 | |

| depth | 279 | 5.1265 | 0.6487 | 1.9110 | 6.0866 | |

| level | 279 | 5.4581 | 0.7166 | 2.0255 | 6.1361 | |

| Other Explanatory Variables (control variables) | open | 279 | 0.1117 | 0.1688 | 0.0000 | 1.0084 |

| urban | 279 | 0.5666 | 0.1314 | 0.2271 | 0.8960 | |

| GDP | 279 | 1.5837 | 0.4361 | 0.4969 | 2.7986 | |

| social | 279 | 0.1270 | 0.0325 | 0.0548 | 0.2747 | |

| fiscal | 279 | 0.4909 | 0.1997 | 0.0722 | 0.9314 | |

| government | 279 | 0.2827 | 0.2119 | 0.1103 | 1.3792 | |

| edu | 279 | 0.0608 | 0.0620 | 0.0123 | 0.4418 | |

| ageing | 279 | 0.1383 | 0.0341 | 0.0671 | 0.2382 | |

| unemployment | 279 | 0.0324 | 0.0064 | 0.0120 | 0.0450 | |

| Year | URIG | DFI | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Geographic Distance Weight Matrix | Economic Distance Weight Matrix | Nested Weight Matrix | Geographic Distance Weight Matrix | Economic Distance Weight Matrix | Nested Weight Matrix | |||||||

| Moran’s I | Geary’s C | Moran’s I | Geary’s C | Moran’s I | Geary’s C | Moran’s I | Geary’s C | Moran’s I | Geary’s C | Moran’s I | Geary’s C | |

| 2011 | 0.192 *** | 0.775 *** | 0.300 *** | 0.663 *** | 0.246 *** | 0.719 *** | 0.109 *** | 0.838 *** | 0.364 *** | 0.543 *** | 0.237 *** | 0.690 *** |

| 2012 | 0.189 *** | 0.782 *** | 0.300 *** | 0.662 *** | 0.245 *** | 0.722 *** | 0.132 *** | 0.835 *** | 0.390 *** | 0.518 *** | 0.261 *** | 0.676 *** |

| 2013 | 0.156 *** | 0.820 *** | 0.241 *** | 0.685 *** | 0.199 *** | 0.753 *** | 0.127 *** | 0.841 *** | 0.398 *** | 0.494 *** | 0.263 *** | 0.668 *** |

| 2014 | 0.152 *** | 0.826 *** | 0.234 *** | 0.692 *** | 0.193 *** | 0.759 *** | 0.127 *** | 0.847 *** | 0.421 *** | 0.473 *** | 0.274 *** | 0.660 *** |

| 2015 | 0.152 *** | 0.821 *** | 0.220 *** | 0.703 *** | 0.186 *** | 0.762 *** | 0.100 *** | 0.881 *** | 0.431 *** | 0.460 *** | 0.266 *** | 0.671 *** |

| 2016 | 0.149 *** | 0.824 *** | 0.221 *** | 0.710 *** | 0.180 *** | 0.767 *** | 0.129 *** | 0.854 *** | 0.422 *** | 0.468 *** | 0.275 *** | 0.661 *** |

| 2017 | 0.147 *** | 0.829 *** | 0.203 *** | 0.717 *** | 0.175 *** | 0.773 *** | 0.134 *** | 0.845 *** | 0.376 *** | 0.510 *** | 0.255 *** | 0.678 *** |

| 2018 | 0.144 *** | 0.830 *** | 0.207 *** | 0.716 *** | 0.176 *** | 0.773 *** | 0.144 *** | 0.837 *** | 0.323 *** | 0.565 *** | 0.234 *** | 0.701 *** |

| 2019 | 0.142 *** | 0.832 *** | 0.207 *** | 0.715 *** | 0.175 *** | 0.774 *** | 0.148 *** | 0.832 *** | 0.328 *** | 0.564 *** | 0.238 *** | 0.698 *** |

| Inspection Index | Data | Significant Value |

|---|---|---|

| Moran’s I | 0.328 | 0.043 |

| LM test no spatial error | 35.486 | 0.000 |

| Robust LM test no spatial error | 47.147 | 0.000 |

| LM test no spatial lag | 33.179 | 0.000 |

| Robust LM test no spatial lag | 44.839 | 0.000 |

| Hausman test | 18.51 | 0.070 |

| LR test ind both | 43.55 | 0.000 |

| LR test time both | 690.16 | 0.000 |

| LR test spatial lag | 86.88 | 0.000 |

| LR test spatial error | 87.89 | 0.000 |

| Wald test spatial lag | 100.58 | 0.000 |

| Wald test spatial error | 95.27 | 0.000 |

| Variables | SDM | Effect Decomposition of SDM | |||

|---|---|---|---|---|---|

| Explanatory Variables | Spatial Variables | Direct Effect | Indirect Effect | Total Effect | |

| DFI | −0.3804 *** (0.0688) | −0.7084 *** (0.1780) | −0.3055 *** (0.0688) | −0.5128 *** (0.1846) | −0.8183 *** (0.1833) |

| open | −0.2358 (0.1959) | −0.6551 (0.6381) | −0.2528 (0.1938) | −0.6889 (0.7370) | −0.9418 (0.7885) |

| urban | −2.2467 *** (0.6417) | 3.9581 ** (1.8755) | −2.1431 *** (0.6234) | 3.9223 ** (1.9611) | 1.7792 ** (1.9473) |

| GDP | −0.1377 ** (0.1000) | −1.6860 *** (0.3881) | −0.1219 ** (0.0974) | −1.7415 *** (0.4308) | −1.8634 *** (0.4521) |

| social | 0.0661 (0.4959) | −4.7409 ** (1.9777) | 0.0439 (0.4937) | −5.1054 ** (2.0851) | −5.0614 ** (2.2755) |

| fiscal | −0.5975 *** (0.2219) | 3.1123 *** (0.7107) | −0.5646 *** (0.2186) | 3.2991 *** (0.8680) | 2.7345 *** (0.9435) |

| government | −0.6498 (0.3611) | −0.6757 (1.5235) | −0.6200 (0.3718) | −0.7173 (1.7802) | −1.3372 (1.9123) |

| edu | −0.3511 (0.5528) | −2.7359 (2.4204) | −0.3899 (0.5413) | −3.0954 (2.5582) | −3.4853 (2.7252) |

| ageing | 2.5916 *** (0.5219) | 7.0567 *** (2.0157) | 2.7031 *** (0.5260) | 7.6934 *** (2.2720) | 10.3965 *** (2.5744) |

| unemployment | 3.7925 * (2.1177) | 3.5081 (7.5710) | 3.8899 * (2.1113) | 4.4392 (8.2044) | 8.3291 (9.1743) |

| ρ | 0.2613 *** | ||||

| Log-likelihood | 331.4688 | ||||

| Fixed Effect | Fixed | ||||

| Observation | 279 | ||||

| Variables | Dimension (1) | Dimension (2) | Dimension (3) |

|---|---|---|---|

| breadth | −0.1082 *** (0.0278) | ||

| depth | −0.0837 ** (0.0422) | ||

| level | −0.1028 *** (0.0347) | ||

| W*breadth | −0.2535 *** (0.0600) | ||

| W*depth | −0.0455 * (0.1535) | ||

| W*level | −0.1265 * (0.0992) | ||

| Direct effect | −0.1080 *** (0.0279) | −0.0849 ** (0.0433) | −0.1034 *** (0.0356) |

| Indirect effect | −0.2619 *** (0.0615) | −0.0401 ** (0.1482) | −0.1168 * (0.0947) |

| Total effect | −0.3700 *** (0.0565) | −0.1250 * (0.1679) | −0.2203 ** (0.1030) |

| Control variables | Controlled | Controlled | Controlled |

| ρ | 0.2451 *** | 0.2381 *** | 0.3275 *** |

| Log-likelihood | 327.9449 | 318.9391 | 321.9079 |

| Fixed effect | Fixed | Fixed | Fixed |

| Observation | 279 | 279 | 279 |

| Variables | Replace the Weight Matrix | Replace Core Explanatory Variables | Replace Explained Variable | |

|---|---|---|---|---|

| Geographic Distance Weight Matrix | Nested Weight Matrix | |||

| DFI | −0.1570 ** (0.0700) | −0.3097 *** (0.0702) | −0.5188 ** (0.5634) | −0.0446 *** (0.0138) |

| W*DFI | −0.8535 * (0.5193) | −1.0853 *** (0.3144) | −0.2179 ** (1.9927) | −0.1658 *** (0.0310) |

| Control variables | Controlled | Controlled | Controlled | Controlled |

| ρ | 0.2443 *** | 0.2329 *** | 0.4218 *** | 0.5258 *** |

| Log-likelihood | 305.5942 | 327.8636 | 351.9830 | 716.9037 |

| Fixed effect | Fixed | Fixed | Fixed | Fixed |

| Observation | 279 | 279 | 279 | 279 |

| Variables | SDM Estimated Results | Test 1 | Test 2 |

|---|---|---|---|

| DFI | −0.3804 *** (0.0688) | −0.2768 *** (0.0591) | −0.3685 *** (0.0731) |

| W*DFI | −0.7084 *** (0.1780) | −0.9084 *** (0.1653) | −0.5024 *** (0.1033) |

| Control variables | Controlled | Controlled | Controlled |

| ρ | 0.2613 *** | 0.2962 *** | |

| Log-likelihood | 331.4688 | 349.2438 | 97.5324 |

| F-Test | 54.8121 | ||

| Fixed effect | Fixed | Fixed | Fixed |

| Observation | 279 | 248 | 279 |

| Variables | Formula (8) URIG | Formula (9) IS | Formula (10) URIG |

|---|---|---|---|

| DFI | −0.3804 *** (0.0688) | 0.6390 *** (0.0538) | −0.2297 *** (0.0687) |

| IS | −0.1249 ** (0.0169) | ||

| W*DFI | −0.7084 *** (0.1780) | 0.5456 ** (0.1426) | −0.4995 *** (0.1848) |

| W*IS | −0.2119 *** (0.0923) | ||

| Control variables | Controlled | Controlled | Controlled |

| ρ | 0.2613 *** | 0.2648 *** | 0.0468 *** |

| Log-likelihood | 331.4688 | 393.0842 | 332.8508 |

| Fixed effect | Fixed | Fixed | Fixed |

| Observation | 279 | 279 | 279 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, P.; Zhang, Y.; Zhou, S. Has Digital Financial Inclusion Narrowed the Urban–Rural Income Gap? A Study of the Spatial Influence Mechanism Based on Data from China. Sustainability 2023, 15, 3548. https://doi.org/10.3390/su15043548

Liu P, Zhang Y, Zhou S. Has Digital Financial Inclusion Narrowed the Urban–Rural Income Gap? A Study of the Spatial Influence Mechanism Based on Data from China. Sustainability. 2023; 15(4):3548. https://doi.org/10.3390/su15043548

Chicago/Turabian StyleLiu, Pengju, Yitong Zhang, and Shengqi Zhou. 2023. "Has Digital Financial Inclusion Narrowed the Urban–Rural Income Gap? A Study of the Spatial Influence Mechanism Based on Data from China" Sustainability 15, no. 4: 3548. https://doi.org/10.3390/su15043548

APA StyleLiu, P., Zhang, Y., & Zhou, S. (2023). Has Digital Financial Inclusion Narrowed the Urban–Rural Income Gap? A Study of the Spatial Influence Mechanism Based on Data from China. Sustainability, 15(4), 3548. https://doi.org/10.3390/su15043548