The Quality of Environmental KPI Disclosure in ESG Reporting for SMEs in Hong Kong

Abstract

:1. Introduction

The Values of the Study

2. ESG Reporting in Hong Kong

2.1. ESG Reporting for SMEs in Hong Kong

* The constituent stocks ranked within the top 80% of the cumulative market value will be included in the Large-Cap. Index.(from “Index Methodology”, Hang Seng Indexes)

** The constituent stocks ranked within the next 15% of the cumulative market value will be included in the Mid-Cap. Index.(from “Index Methodology”, Hang Seng Indexes)

* Analysis of Environment, Social and Governance Practice Disclosure in 2016/2017 and Analysis of Environmental, Social and Governace Practice Disclosure in 2018.

2.2. Quality of ESG Disclosure

3. Literature Review

3.1. General Challenges of ESG Reporting

3.2. The Impact of Mandatory ESG Reporting

3.3. Specific Challenges for SMEs

3.4. Disclosure Quality of ESG Reports

4. Research Methodology

4.1. Quantitative Method—Scoring Exercise and Descriptive Statistical Analysis

4.2. Stratified Sampling Methodology

4.3. Sampling Procedure

- -

- A full list of 2328 listed company stock codes in Hong Kong Stock Exchange was collected from AAStock (a renowned stock information provider in Hong Kong).

- -

- A total of 405 stock codes from Table 1 below were filtered out because they were not company stocks or they were stocks traded on Growth Enterprise Market (GEM).

- -

- The 111 large-cap and 193 mid-cap companies were then removed.

- -

- In the end, 1619 small-cap companies traded on the Main Board remained as the target population.

{kind=link}

{kind=link}

{kind=link}

| Nature | Stock Codes |

|---|---|

| Exchange Traded Funds | 02800–02849 03000–03199 |

| Hong Kong Monetary Authority Exchange Fund Notes | 04000–04199 |

| HKSAR Government Bonds | 04200–04299 |

| Debt Securities to professional investor only | 04300–04329 04400–04599 05000–06029 |

| Professional Preference Share | 04600–04699 |

| Hong Kong Depositary Receipts (HDRs) | 06200–06499 |

| HDRs which are restricted securities under US federal securities laws | 06300–06399 |

| Bonds of Ministry of the Finance of the People’s Republic of China | 06750–06799 |

| Leveraged and Inverse Products | 07200–07399 |

| GEM Securities | 08000–08999 |

| Exchange Trade Funds (Traded in USD) | 09000–09199 09800–09849 |

| Leveraged and Inverse Products | 09200–09399 |

| Total number of stock codes: | 405 |

4.4. Summary of Calculating the Target Population

- -

- A list of a total of 2328 stock codes (i.e., all securities listed on the Main Board and the GEM) in HKEx was retrieved from AAStock as of 29 November 2018.

- -

- All 405 stock codes in the above table were removed.

- -

- All of the 111 large-cap companies were removed.

- -

- All of the 193 mid-cap companies were removed.

- -

- That is, 2328 − 405 − 111 − 193 = 1619 (i.e., the target population for this research is 1619; they are small-cap companies traded on the Main Board of HKEx).

- -

- Each sample size is rounded up to the integer.

- -

- The original sample size was 137. The sample size of the “Information Technology” industry was 9.4, which was rounded up to 10 for prudence. This resulted in a total of 138 samples.

* Random number table reference: The Rand Corporation, A Million Random Digits with 100,000 Normal Deviates(New York, NY, USA: The Free Press, 1955)

| Industry Category | Number of Small-Cap Companies | Sample Size |

|---|---|---|

| Conglomerates | 13 | 1 |

| Consumer Goods | 412 | 35 |

| Energy | 66 | 6 |

| Financials | 146 | 12 |

| Industrial Goods | 140 | 12 |

| Information Technology | 110 | 10 |

| Materials | 121 | 10 |

| Properties and Constructions | 315 | 27 |

| Services | 221 | 19 |

| Telecommunication | 27 | 2 |

| Utilities | 48 | 4 |

| Total | 1619 | 138 |

4.5. Quantifying the Quality Issue

- 0—No disclosure;

- 1—Only provide anecdotal information (i.e., only provide general description, not specific to the disclosure requirement of the Guide);

- 2—Limited information (i.e., fail to meet all the disclosure requirement of the Guide);

- 3—Complete information (i.e., meet the disclosure requirement of the Guide);

- 4—Beyond disclosure requirement of the Guide.

4.6. Collection of Data

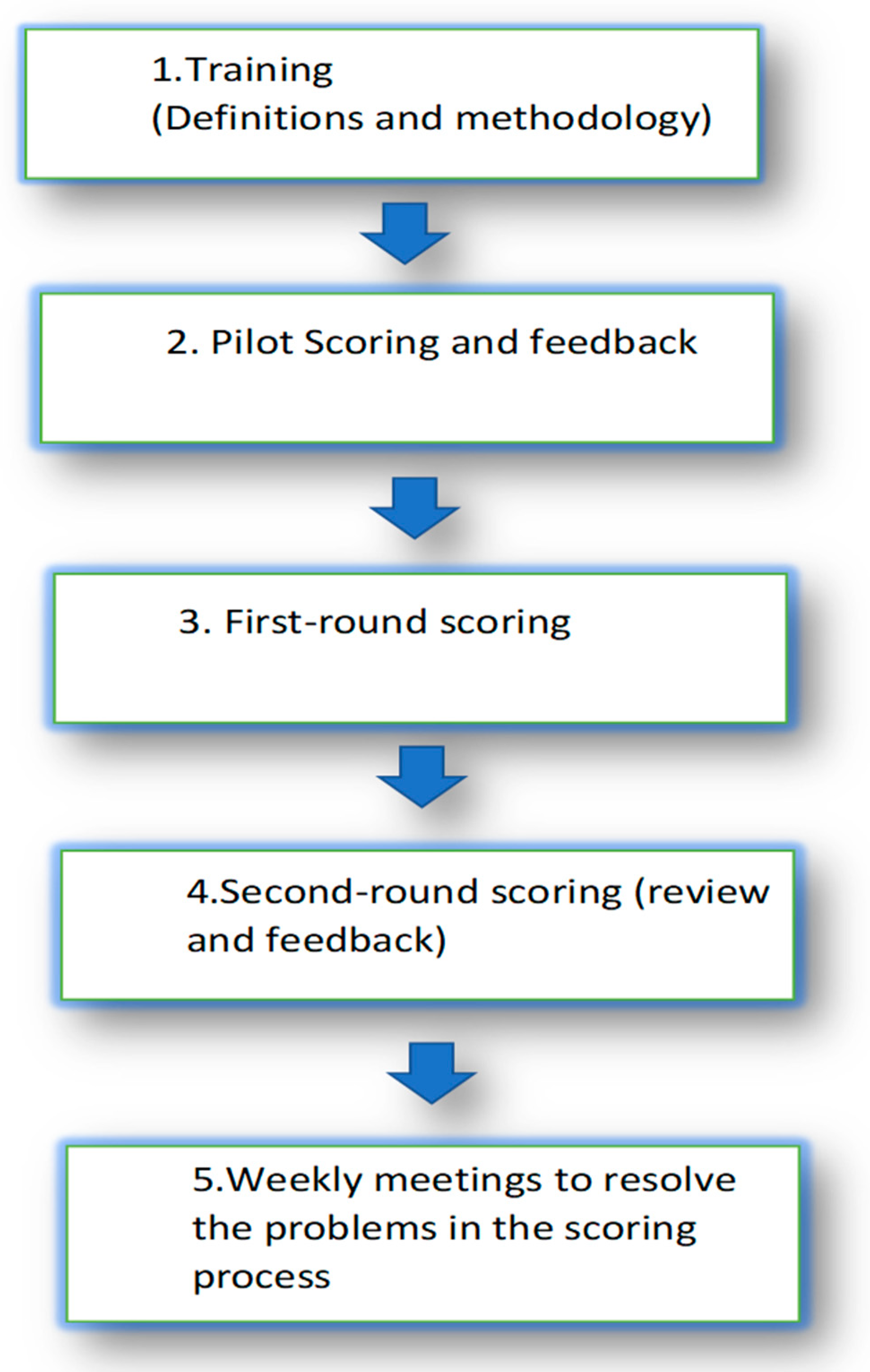

4.7. Inter-Rater and Intra-Rater Reliability

5. Data Analysis and Discussion

- Best reported KPI:

- 2.

- Worst reported KPI:

- 3.

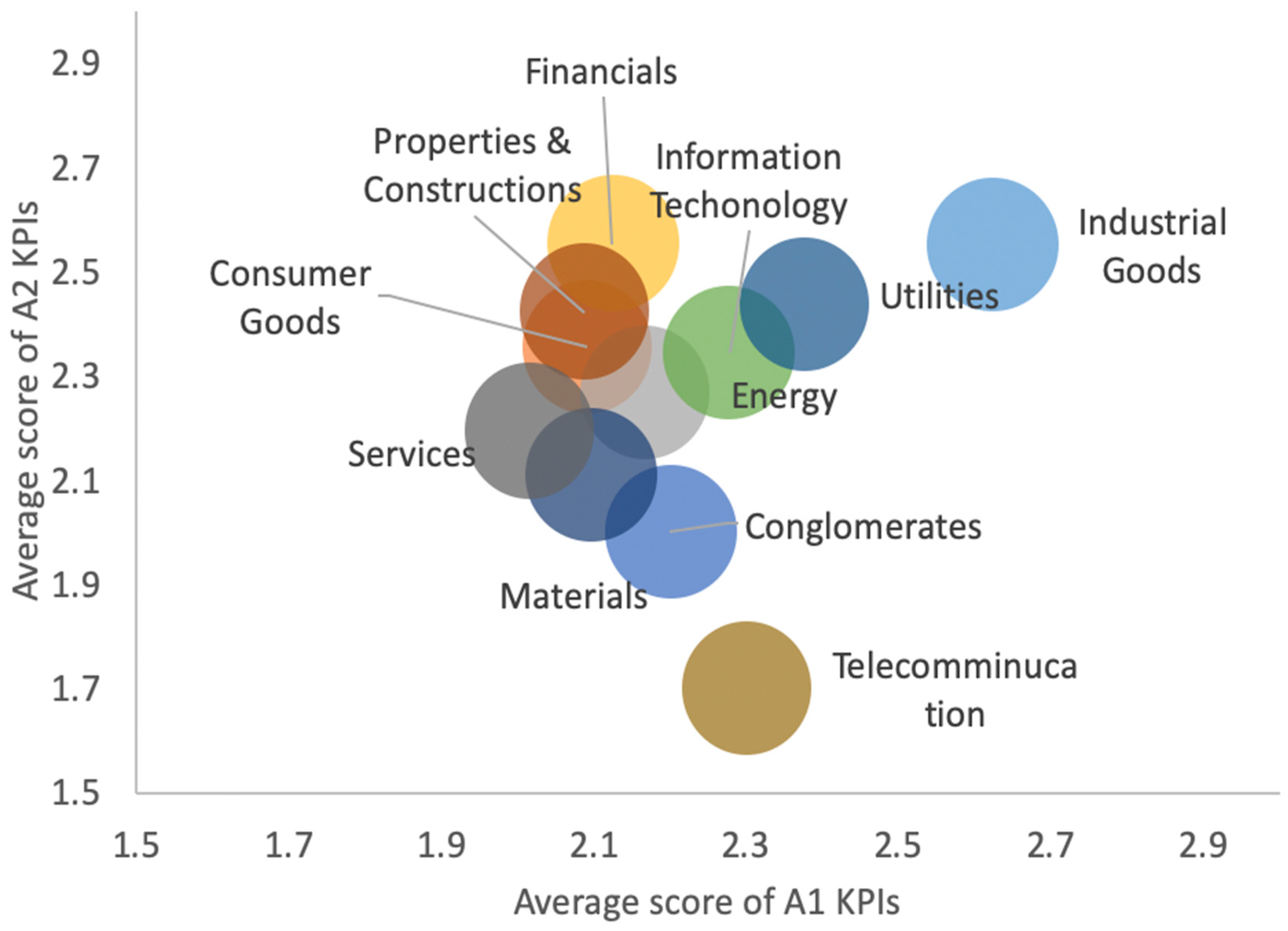

- Best performer: Industrial Goods

- 4.

- Worst performer: Telecommunication

- 5.

- Comparison between Aspect A1 (Emissions) KPIs and Aspect A2 (Use of Resources) KPIs (Figure 2)

- 6.

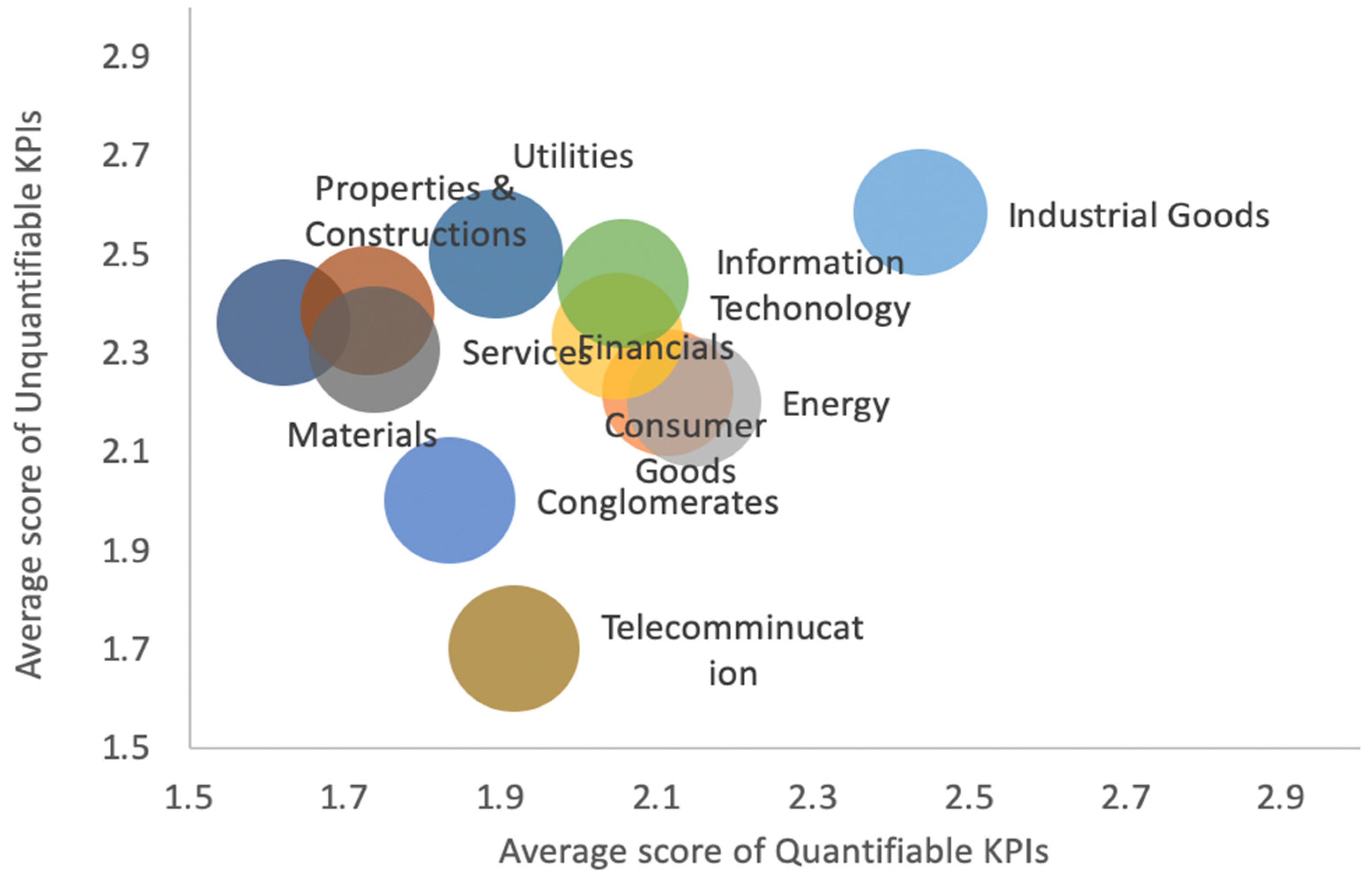

- Quantitative KPIs vs. qualitative KPIs

5.1. Common Problems for Reporting Environmental KPIs

5.1.1. Limited Reporting Scope

5.1.2. Insufficient Evidence

5.1.3. Potential Manipulation of the Intensity Calculation

5.1.4. Over-Generalized Presentation

5.1.5. Incomplete Disclosure

5.1.6. Irrelevant Information in the Report

5.2. The Contributions and Implications of the Research

6. Conclusions

6.1. Limitations of the Study

* According to the Hang Seng Industry Classification System, conglomerates are diversified companies engaged in three or more businesses classified into different sectors with each business contributing more than 10% but not substantially to turnover.

6.2. Suggestions for Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Burritt, R.L.; Schaltegger, S. Sustainability accounting and reporting: Fad or trend? Account. Audit. Account. J. 2010, 23, 829–846. [Google Scholar] [CrossRef]

- Cho, C.H.; Laine, M.; Roberts, R.W.; Rodrigue, M. Organized hypocrisy, organizational façades, and sustainability reporting. Account. Organ. Soc. 2015, 40, 78–94. [Google Scholar] [CrossRef]

- Bansal, P.; DesJardine, M.R. Business sustainability: It is about time. Strateg. Organ. 2014, 12, 70–78. [Google Scholar] [CrossRef]

- Ferrell, A.; Liang, H.; Renneboog, L. Socially responsible firms. J. Financ. Econ. 2016, 122, 585–606. [Google Scholar] [CrossRef] [Green Version]

- CSR Asia Advisory. Hong Kong Exchange, Environmental. Social and Governance Reporting Guide; CSR Asia Advisory: Hong Kong, China, 2013. [Google Scholar]

- Badia, F.; Bracci, E.; Tallaki, M. Quality and diffusion of social and sustainability reporting in Italian public utility companies. Sustainability 2020, 12, 4525. [Google Scholar] [CrossRef]

- Buhr, N. Histories of and rationales for sustainability reporting. In Sustainability Accounting and Accountability; Routledge: Oxfordshire, UK, 2007; pp. 57–69. [Google Scholar]

- Barnea, A.; Rubin, A. Corporate social responsibility as a conflict between shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Elkington, J. Enter the triple bottom line. In The Triple Bottom Line: Does It All Add Up; Routledge: Oxfordshire, UK, 2004; Volume 11, pp. 1–16. [Google Scholar]

- Nesbit, J.C.; Adesope, O.O. Learning with concept and knowledge maps: A meta-analysis. Rev. Educ. Res. 2006, 76, 413–448. [Google Scholar] [CrossRef] [Green Version]

- Neu, D.; Warsame, H.; Pedwell, K. Managing public impressions: Environmental disclosures in annual reports. Account. Organ. Soc. 1998, 23, 265–282. [Google Scholar] [CrossRef]

- De Klerk, M.; De Villiers, C.; Van Staden, C. The influence of corporate social responsibility disclosure on share prices. Pac. Account. Rev. 2015, 27. [Google Scholar] [CrossRef]

- Barometer, E.T. The Edelman Trust Barometer. 2009. Available online: http://www.edelman.com/assets/uploads/2014/01/2009-Trust-Barometer-Global-Deck.pdf (accessed on 15 September 2018).

- Boffo, R.; Patalano, R. Esg Investing: Practices, Progress and Challenges. OECD. Available online: https://www.oecd.org/finance/ESG-Investing-Practices-Progress-Challenges.Pdf (accessed on 25 May 2021).

- Ferns, B.; Emelianova, O.; Sethi, S.P. In his own words: The effectiveness of CEO as spokesperson on CSR-Sustainability issues—Analysis of Data from the Sethi CSR monitor. Corp. Reput. Rev. 2008, 11, 116–129. [Google Scholar] [CrossRef]

- Burlea, A.S.; Popa, I. Legitimacy theory. In Encyclopedia of Corporate Social Responsibility; Springer: Berlin/Heidelberg, Germany, 2013; pp. 1579–1584. [Google Scholar]

- Consultation Paper on ESG Reporting Guide (December 2011), Hong Kong Exchange. Available online: https://www.hkex.com.hk/-/media/HKEX-Market/Listing/Rules-and-Guidance/Other-Resources/Environmental-Social-and-Governance/Exchange-Publications-on-ESG/cp201112.pdf?la=en (accessed on 15 September 2018).

- Freedman, M.; Stagliano, M.J. European unification, accounting harmonisation, and social disclosure. Int. J. Account. 1992, 27, 112–122. [Google Scholar]

- The Wall Street Journal (1 December 2015). Hong Kong Is No. 1 again for IPOs Globally. Available online: http://www.wsj.com/articles/hong-kong-is-no-1-again-for-ipos-globally-1449120929 (accessed on 15 September 2018).

- Novak, J.D. Concept mapping to facilitate teaching and learning. Prospects 1995, 25, 79–86. [Google Scholar] [CrossRef]

- Thompson, L., Jr. Toward Better Sustainability Reporting. 2012. Available online: www.complianceweek.com (accessed on 20 December 2022).

- Consultation Paper on Review of ESG Reporting Guide (July 2015), Hong Kong Exchange. Available online: https://www.hkex.com.hk/-/media/HKEX-Market/Listing/Rules-and-Guidance/Other-Resources/Environmental-Social-and-Governance/Exchange-Publications-on-ESG/cp201507.pdf?la=en (accessed on 15 September 2018).

- Decker, M.; Schiefer, G.; Bulander, R. Specific challenges for small and medium-sized enterprises (SME) in M-business. In Proceedings of the International Conference on E-Business (ICE-B 2006), Setúbal, Portugal, 7–10 August 2006; INSTICC Press: Setúbal, Portugal, 2006; pp. 169–174. [Google Scholar]

- El Madani, A. SME policy: Comparative analysis of SME definitions. Int. J. Acad. Res. Bus. Soc. Sci. 2018, 8, 103–114. [Google Scholar] [CrossRef] [PubMed]

- Freeman, R.E. The politics of stakeholder theory: Some future directions. Bus. Ethics Q. 1994, 4, 409–421. [Google Scholar] [CrossRef]

- European Union. Commission Recommendation of 6 May 2003 Concerning the Definition of Micro, Small and Medium-Sized Enterprises, 2003. Available online: https://op.europa.eu/en/publication-detail/-/publication/6ca8d655-126b-4a42-ada4-e9058fa45155 (accessed on 28 September 2020).

- Marwede, E. Die Abgrenzungsproblematik Mittelständischer Unternehmen: Eine Literaturanalyse; Volkswirtschaftliches Institut, Universität Augsburg: Augsburg, Germany, 1983. [Google Scholar]

- Man, T.W.; Lau, T. Entrepreneurial competencies of SME owner/managers in the Hong Kong services sector: A qualitative analysis. J. Enterprising Cult. 2000, 8, 235–254. [Google Scholar] [CrossRef]

- Chan, K.; Yao, C. The Effect of a Closing auction on Market Quality and Market Efficiency in the Stock Exchange of Hong Kong. HKIMR Appl. Res. Pap. 2021. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3839185 (accessed on 3 March 2021).

- Ahmad, Z.; Hassan, S.; Mohammad, J. Determinants of Environmental Reporting in Malaysia. Int. J. Bus. Stud. 2003, 11, 69–90. [Google Scholar]

- Alsayegh, M.F.; Abdul Rahman, R.; Homayoun, S. Corporate economic, environmental, and social sustainability performance transformation through ESG disclosure. Sustainability 2020, 12, 3910. [Google Scholar] [CrossRef]

- Romero, S.; Jeffers, A.E.; Aquilino, F.; DeGaetano, L. Using ESG ratings to build a sustainability investing strategy. CPA J. 2018, 88, 36–43. [Google Scholar]

- Fogg, B.J. Persuasive ’09 Proceedings of the 4th International Conference on Persuasive Technology; ACM: New York, NY, USA, 2009. [Google Scholar]

- Michael, S. Job market signaling. Q. J. Econ. 1973, 87, 355–374. [Google Scholar]

- Watson, L.A.; Monterio, B.J. The next stage in the evolution of business reporting-the journey towards an interlinked, integrated report. Chart. Account. 2011, 75–78. [Google Scholar]

- Abdul Rahman, R.; Alsayegh, M.F. Determinants of Corporate Environment, Social and Governance (ESG) Reporting among Asian Firms. J. Risk Financ. Manag. 2021, 14, 167. [Google Scholar] [CrossRef]

- Eccles and Saltzman. Achieving Sustainability through Integrated Reporting, Stanford Social Innovation Review, Summer 2011. Available online: https://studylib.net/doc/10546175/achieving-sustainability-through-integrated-reporting (accessed on 22 August 2020).

- Corporate Register. Available online: http://www.corporateregister.com/ (accessed on 15 September 2018).

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of 21st Century Business; New Society Publishers: Gabriola Island, BC, Canada, 1997. [Google Scholar]

- Kassel, K.; Rimanoczy, I.; Mitchell, S. The sustainable mindset: Connecting being, thinking, and doing in management education. In Proceedings of the Academy of Management Annual Meeting 2016, Anaheim, CA, USA, 5–9 August 2016. [Google Scholar]

- Kolk, A. Trends in sustainability reporting by the Fortune Global 250. Bus. Strategy Environ. 2003, 12, 279–291. [Google Scholar] [CrossRef]

- Le Lievre, R. Friedman was right about the Corporation, but can the free market solve Global Warming? In Proceedings of the 2009 Committee for the Australasian Postgraduate Philosophy Conference Sydney, Sydney, Australia, 15–17 April 2009; p. 30. [Google Scholar]

- Asia, C.S.R. CSR in Asia the Real Picture. 2010. Available online: https://www.elevatelimited.com/ (accessed on 29 April 2019).

- Eliwa, Y.; Aboud, A.; Saleh, A. ESG practices and the cost of debt: Evidence from EU countries. Crit. Perspect. Account. 2019, 79, 102097. [Google Scholar] [CrossRef]

- Environmental Finance, Sustainable Bonds Insights 2021. Available online: https://www.environmental-finance.com/assets/files/research/sustainable-bonds-insight-2021.pdf (accessed on 15 April 2022).

- Healy, P.M.; Palepu, K.G. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. J. Account. Econ. 2001, 31, 405–440. [Google Scholar] [CrossRef]

- Hoffelder, K. The value of sustainability. Account. Tax 2012, 17–18. [Google Scholar]

- Dobbs, S.; Van Staden, C. Motivations for corporate social and environmental reporting: New Zealand evidence. Sustain. Account. Manag. Policy J. 2016, 7, 449–472. [Google Scholar] [CrossRef]

- MacLean, R.; Rebernak, K. Closing the credibility gap: The challenges of corporate responsibility reporting. In Environmental Quality Management, Summer; Wiley Periodicals, LLC: Hoboken, NJ, USA, 2007. [Google Scholar]

- Bentham, J. Principles of Penal Law; Tait: Edinburgh, UK, 1843. [Google Scholar]

- Brennan, N.M.; Merkl-Davies, D.M. Rhetoric and argument in social and environmental reporting: The Dirty Laundry case. Account. Audit. Account. J. 2014, 27, 602–633. [Google Scholar] [CrossRef] [Green Version]

- Patten, D.M. The accuracy of financial report projections of future environmental capital expenditures: A research note. Account. Organ. Soc. 2005, 30, 457–468. [Google Scholar] [CrossRef]

- Peng, L.S.; Isa, M. Environmental, Social and Governance (ESG) Practices And Performance In Shariah Firms: Agency or Stakeholder Theory? Asian Acad. Manag. J. Account. Financ. 2020, 16, 1–34. [Google Scholar]

- Poh, J. ESG-Linked Loan Boom Hit by Pandemic Push for Short-Term Funds. Bloom. News 2020. Available online: https://www.bloomberg.com/news/articles/2020-10-20/esg-linked-loan-boom-hit-by-pandemic-push-for-short-term-funds#xj4y7vzkg (accessed on 26 June 2021).

- Prencipe, A. Proprietary costs and determinants of voluntary segment disclosure: Evidence from Italian listed companies. Eur. Account. Rev. 2004, 13, 319–340. [Google Scholar] [CrossRef]

- PRI. Principles for Responsible Investment. 2006. Available online: https://www.unpri.org/about (accessed on 15 September 2018).

- Kim, E.H.; Lyon, T.P. Greenwash vs. brownwash: Exaggeration and undue modesty in corporate sustainability disclosure. Organ. Sci. 2015, 26, 705–723. [Google Scholar] [CrossRef] [Green Version]

- Donaldson, T.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Brown, W.O.; Helland, E.; Smith, J.K. Corporate philanthropic practices. J. Corp. Financ. 2006, 12, 855–877. [Google Scholar] [CrossRef] [Green Version]

- Khan, H.Z.; Bose, S.; Mollik, A.T.; Harun, H. “Green washing” or “authentic effort”? An empirical investigation of the quality of sustainability reporting by banks. Account. Audit. Account. J. 2020, 34, 338–369. [Google Scholar] [CrossRef]

- Rensburg, R.; Botha, E. Is Integrated Reporting the silver bullet of financial communication? A stakeholder perspective from South Africa. Public Relat. Rev. 2014, 40, 144–152. [Google Scholar] [CrossRef]

- Shacklett, M. Sustainability, greenwashing, and the road ahead for the supply chain. World Trade 2011, 24, 32. [Google Scholar]

- Becker, G.S. Crime and punishment: An economic approach. J. Political Econ. 1968, 76, 169–217. [Google Scholar] [CrossRef] [Green Version]

- Dye, R.A. Disclosure of nonproprietary information. J. Account. Res. 1985, 23, 123–145. [Google Scholar] [CrossRef]

- Konigs, A.; Schiereck, D. Intangibles reporting—The financial communication challenge in response to corporate responsibility requirements. zfwu Zeitschrift für Wirtschafts-und Unternehmensethik 2008, 9, 193–195. [Google Scholar]

- Rezaee, Z. Business sustainability research: A theoretical and integrated perspective. J. Account. Lit. 2016, 36, 48–64. [Google Scholar] [CrossRef]

- Amaeshi, K.; Grayson, D. The Challenges of Mainstreaming Environmental, Social and Governance (ESG) Issues in Investment Decision, Working Paper, 2009. Available online: https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=0660e46c233bc99f28b75c10b3429988a33f7e9d (accessed on 20 December 2022).

- Harte, G.; Lewis, L.; Owen, D. Ethical investment and the corporate reporting function. Crit. Perspect. Account. 1991, 2, 227–253. [Google Scholar] [CrossRef]

- De Villiers, C.; Van Staden, C.J. Where firms choose to disclose voluntary environmental information. J. Account. Public Policy 2011, 30, 504–525. [Google Scholar] [CrossRef]

- Dienes, D.; Sassen, R.; Fischer, J. What are the drivers of sustainability reporting? A systematic review. Sustain. Account. Manag. Policy J. 2016, 7, 154–189. [Google Scholar] [CrossRef]

- Doane, D. Market Failure: The Case for Mandatory Social and Environmental Reporting; Presentation at Institute for Public Policy Research Seminar; New Economics Foundation: London, UK, 2004. [Google Scholar]

- Hossain, M.; Perera, M.H.B.; Rahman, A.R. Voluntary disclosure in the annual reports of New Zealand companies. J. Int. Financ. Manag. Account. 1995, 6, 69–87. [Google Scholar] [CrossRef]

- Watson, A.; Shrives, P.; Marston, C. Voluntary disclosure of accounting ratios in the UK. Br. Account. Rev. 2002, 34, 289–313. [Google Scholar] [CrossRef]

- Cotter, J.; Lokman, N.; Najah, M.M. Voluntary disclosure research: Which theory is relevant? J. Theor. Account. Res. 2011. Available online: https://www.researchgate.net/profile/Norziana-Lokman/publication/281390648_Voluntary_Disclosure_Research_Which_Theory_Is_Relevant/links/588425bc4585150dde41f6dc/Voluntary-Disclosure-Research-Which-Theory-Is-Relevant.pdf (accessed on 6 December 2021). [CrossRef] [Green Version]

- Guthrie, J.; Parker, L.D. Corporate social reporting: A rebuttal of legitimacy theory. Account. Bus. Res. 1989, 19, 343–352. [Google Scholar] [CrossRef]

- Murphy, D.; McGrath, D. ESG reporting-class actions, deterrence, and avoidance. Sustain. Account. Manag. Policy J. 2013, 4, 216–235. [Google Scholar] [CrossRef]

- Nussim, J.; Tabbach, A. Deterrence or avoidance. Int. Rev. Law Econ. 2009, 29, 314–323. [Google Scholar] [CrossRef]

- Rezaee, Z.; Tuo, L. Voluntary disclosure of non-financial information and its association with sustainability performance. Adv. Account. 2017, 39, 47–59. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The consequences of Mandatory Corporate Sustainability Reporting. Harvard Business School Research Working Paper No. 11-100. 2011. Available online: https://www.albertoandreu.com/uploads/2011/05/The-consequences-of-mandatory-corporate-sustainability-reporting.pdf (accessed on 21 November 2021).

- Trevor, D.W.; Geoffrey, R.F. Corporate environmental reporting. A test of legitimacy theory. Account. Audit. Account. J. 2000, 13, 10–26. [Google Scholar]

- Van Zijl, W.; Wöstmann, C.; Maroun, W. Strategy disclosures by listed financial services companies: Signalling theory, legitimacy theory and South African integrated reporting practices. S. Afr. J. Bus. Manag. 2017, 48, 73–85. [Google Scholar] [CrossRef]

- Dawkins, C.; Ngunjiri, W.F. Corporate Social Responsibility Reporting in South Africa. J. Bus. Commun. 2008, 45, 286–307. [Google Scholar] [CrossRef]

- IR Council. The International <IR> Framework; IR Council: Zurich, Switzerland, 2013. [Google Scholar]

- Wang, J.; Song, L.; Yao, S. The determinants of corporate social responsibility disclosure: Evidence from China. J. Appl. Bus. Res. JABR 2013, 29, 1833–1848. [Google Scholar] [CrossRef]

- Watts, R.L.; Zimmerman, J.L. Towards a positive theory of the determination of accounting standards. Account. Rev. 1978, 53, 112–134. [Google Scholar]

- Doane, M.A. The Emergence of Cinematic Time: Modernity, Contingency, the Archive; Harvard University Press: Cambridge, MA, USA, 2002. [Google Scholar]

- Integrated Reporting Committee of South Africa (IRCSA). Framework for Integrated Reporting and the Integrated Report; Integrated Reporting Committee of South Africa: Craighall, South Africa, 2011. [Google Scholar]

- Verrecchia, R.E. Discretionary disclosure. J. Account. Econ. 1983, 5, 179–194. [Google Scholar] [CrossRef]

- Verrecchia, R.E. Information quality and discretionary disclosure. J. Account. Econ. 1990, 12, 365–380. [Google Scholar] [CrossRef]

- Verrecchia, R.E. Essays on disclosure. J. Account. Econ. 2001, 32, 97–180. [Google Scholar] [CrossRef]

- Kent, P.; Monem, R. What drives TBL reporting: Good governance or threat to legitimacy? Aust. Account. Rev. 2008, 18, 297–309. [Google Scholar] [CrossRef] [Green Version]

- Said, R.; Zainuddin, Y.H.; Haron, H. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Soc. Responsib. J. 2009, 5, 212–226. [Google Scholar] [CrossRef] [Green Version]

- Condon, L. Sustainability and small to medium sized enterprises-How to engage them. Aust. J. Environ. Educ. 2004, 20, 57–67. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 77–132. [Google Scholar] [CrossRef]

- Van der Sandra, L. The role of theory in explaining motivation for corporate social disclosure: Voluntary disclosures vs “solicited” disclosures. Australas. Account. Bus. Financ. J. 2009, 3, 15–29. [Google Scholar]

- Jonkutė, G.; Staniškis, J.K.; Dukauskaitė, D. Social responsibility as a tool to achieve sustainable development in SMEs. Environ. Res. Eng. Manag. 2011, 57, 67–81. [Google Scholar]

- Lauterbach, B.; Vaninsky, A. Ownership structure and firm performance: Evidence from Israel. J. Manag. Gov. 1999, 3, 189–201. [Google Scholar] [CrossRef]

- Schein, S. A New Psychology for Sustainability Leadership: The Hidden Power of Ecological Worldviews; Greenleaf Publishing: Austin, TX, USA, 2015. [Google Scholar]

- Schuler, D.A.; Cording, M. A corporate social performance–corporate financial performance behavioral model for consumers. Acad. Manag. Rev. 2006, 31, 540–558. [Google Scholar] [CrossRef]

- Sillanpää, M. The Body Shop values report–Towards integrated stakeholder auditing. J. Bus. Ethics 1998, 17, 1443–1456. [Google Scholar] [CrossRef]

- Audretsch, D.B. Small Firms and Efficiency. In Are Small Firms Important? Their Role and Impact; Acs, Z.J., Ed.; Kluwer Academic Publishers: London, UK, 1999; pp. 21–37. [Google Scholar]

- Consultation Conclusions on ESG Guide (August 2012), Hong Kong Exchange. Available online: https://www.hkex.com.hk/-/media/HKEX-Market/Listing/Rules-and-Guidance/Other-Resources/Environmental-Social-and-Governance/Exchange-Publications-on-ESG/cp201112cc.pdf?la=en (accessed on 15 September 2018).

- George, E. Yes, SMEs Can Be Sustainable—And Here’s How” in the Book “Yes, Business Can”; Llodys Banking Group: Edinburgh, UK, 2021. [Google Scholar]

- Li, Y.; Gong, M.; Zhang, X.Y.; Koh, L. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. Br. Account. Rev. 2018, 50, 60–75. [Google Scholar] [CrossRef] [Green Version]

- Arend, R.J. Social and environmental performance at SMEs: Considering motivations, capabilities, and instrumentalism. J. Bus. Ethics 2014, 125, 541–561. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. The causal effect of corporate governance on corporate social responsibility. J. Bus. Ethics 2012, 106, 53–72. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Anderson, A.B.; Harris, A.R.; Miller, J. Models of deterrence theory. Soc. Sci. Res. 1983, 12, 236–262. [Google Scholar] [CrossRef]

- Beccaria, C. Essays on Crimes and Punishment; Bobbs-Merrill: Indianaopolis, IN, USA, 1809. [Google Scholar]

- Beck, C.T. Qualitative research: The evaluation of its credibility, fittingness, and auditability. West. J. Nurs. Res. 1993, 15, 263–266. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard—Measures That Drive Performance; Harvard Business Review: Boston, MA, USA, 1992; pp. 71–79. [Google Scholar]

- Gillan, S.; Hartzell, J.C.; Koch, A.; Starks, L.T. Firms’ environmental, social and governance (ESG) choices, performance and managerial motivation. 2010. (Unpublished Work).

- Vormedal, I.; Ruud, A. Sustainability reporting in Norway—An assessment of performance in the context of legal demands and socio-political drivers. Bus. Strategy Environ. 2009, 18, 207–222. [Google Scholar] [CrossRef]

- Handy, C. Understanding Organizations; Oxford University Press: Oxford, UK, 1976. [Google Scholar]

- Lock, I.; Seele, P. The credibility of CSR (corporate social responsibility) reports in Europe. Evidence from a quantitative content analysis in 11 countries. J. Clean. Prod. 2016, 122, 186–200. [Google Scholar] [CrossRef] [Green Version]

- Allouche, J.; Laroche, P. A meta-analytical investigation of the relationship between corporate social and financial performance. Rev. Gest. Ressour. Hum. 2005, 57, 18. [Google Scholar]

- King, R.R. Reputation formation for reliable reporting: An experimental investigation. Account. Rev. 1996, 71, 375–396. [Google Scholar]

- Diamond, D.W.; Verrecchia, R.E. Disclosure, liquidity, and the cost of capital. J. Financ. 1991, 46, 1325–1359. [Google Scholar] [CrossRef]

- Hopkins, P.E. The effect of financial statement classification of hybrid financial instruments on financial analysts’ stock price judgments. J. Account. Res. 1996, 34, 33–50. [Google Scholar] [CrossRef]

- Beattie, V.; McInnes, B.; Fearnley, S. A methodology for analysing and evaluating narratives in annual reports: A comprehensive descriptive profile and metrics for disclosure quality attributes. In Accounting Forum; Elsevier: Amsterdam, The Netherlands, 2004; Volume 28, pp. 205–236. [Google Scholar]

- Haddock-Fraser, J.; Fraser, I. Assessing corporate environmental reporting motivations: Differences between ‘close-to-market’and ‘business-to-business’ companies. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 140–155. [Google Scholar] [CrossRef]

- Mion, G.; Loza Adaui, C.R. Mandatory nonfinancial disclosure and its consequences on the sustainability reporting quality of Italian and German companies. Sustainability 2019, 11, 4612. [Google Scholar] [CrossRef] [Green Version]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M. Environmental reporting management: A continental European perspective. J. Account. Public Policy 2003, 22, 43–62. [Google Scholar] [CrossRef]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR reporting practices and the quality of disclosure: An empirical analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef] [Green Version]

- Global Reporting Initiative. Sustainability Reporting Guidelines; GRI: Amsterdam, The Netherlands, 2006. [Google Scholar]

- Michelon, G.; Pilonato, S.; Ricceri, F.; Roberts, R.W. Behind camouflaging: Traditional and innovative theoretical perspectives in social and environmental accounting research. Sustain. Account. Manag. Policy J. 2016, 7, 2–25. [Google Scholar] [CrossRef] [Green Version]

- Beretta, S.; Bozzolan, S. A framework for the analysis of firm risk communication. Int. J. Account. 2004, 39, 265–288. [Google Scholar] [CrossRef]

- Chauvey, J.N.; Giordano-Spring, S.; Cho, C.H.; Patten, D.M. The normativity and legitimacy of CSR disclosure: Evidence from France. J. Bus. Ethics 2015, 130, 789–803. [Google Scholar] [CrossRef]

- Baalouch, F.; Ayadi, S.D.; Hussainey, K. A study of the determinants of environmental disclosure quality: Evidence from French listed companies. J. Manag. Gov. 2019, 23, 939–971. [Google Scholar] [CrossRef] [Green Version]

- Patton, M.Q. Qualitative Evaluation and Research Methods; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 1990. [Google Scholar]

- Patton, M.Q. Qualitative Research & Evaluation Methods: Integrating Theory and Practice; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2015. [Google Scholar]

- Creswell, J.W.; Hanson, W.E.; Clark Plano, V.L.; Morales, A. Qualitative research designs: Selection and implementation. Couns. Psychol. 2007, 35, 236–264. [Google Scholar] [CrossRef]

- Creswell, J.W.; Poth, C.N. Qualitative inquiry and research design (international student edition): Choosing among five approaches. Language 2018, 25, 23. [Google Scholar]

- Glasser, B.; Strauss, A. The Discovery of Grounded Theory: Strategies for Qualitative Research; Routledge: Oxfordshire, UK, 1977. [Google Scholar]

- Glasser, B.G. Naturalist Inquiry and Grounded Theory; Sociology: Mill Valley, CA, USA, 2004. [Google Scholar]

- Hammersley, M. A historical and comparative note on the relationship between analytic induction and grounded theorising. Forum Qual. Soc. Res. 2010, 11. [Google Scholar] [CrossRef]

- Ho Jennifer, L.C.; Taylor, M.E. An empirical analysis of triple bottom-line reporting and its determinants: Evidence from the United States and Japan. J. Int. Financ. Manag. Account. 2007, 18, 123–150. [Google Scholar] [CrossRef]

- Sandelowski, M. Tables or tableaux? The challenges of writing and reading mixed methods studies. In Handbook of Mixed Methods in Social and Behavioral Research; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2003; pp. 321–350. [Google Scholar]

- Strauss, A.; Corbin, J. Basics of Qualitative Research Techniques; Sage Publications: Thousand Oaks, CA, USA, 1998. [Google Scholar]

- Timmermans, S.; Tavory, I. Theory construction in qualitative research: From grounded theory to abductive analysis. Sociol. Theory 2012, 30, 167–186. [Google Scholar] [CrossRef]

- Bryman, A.; Bell, E. Business Research Methods 3e; Oxford University Press: Oxford, UK, 2011. [Google Scholar]

- McCallin, A.M. Designing a grounded theory study: Some practicalities. Nurs. Crit. Care 2003, 8, 203–208. [Google Scholar] [CrossRef]

- Kwok, J.K. Does switching trading venues create value? Evidence from Hong Kong. J. Asian Bus. Econ. Stud. 2020, 27, 209–222. [Google Scholar] [CrossRef]

- Sharma, G. Pros and cons of different sampling techniques. Int. J. Appl. Res. 2017, 3, 749–752. [Google Scholar]

- Anzai, Y.; Simon, H.A. The theory of learning by doing. Psychol. Rev. 1979, 86, 124. [Google Scholar] [CrossRef]

- Holloway, I.; Wheeler, S. Qualitative Research for Nurses; Blackwell Science: Oxford, UK, 1996; pp. 115–129. [Google Scholar]

- Cuesta, M.; Valor, C. Evaluation of the environmental, social and governance information disclosed by Spanish listed companies. Soc. Responsib. J. 2013, 9, 220–240. [Google Scholar] [CrossRef]

- Olesen, V.L.; Bryant, A.; Charmaz, K. Feminist qualitative research and grounded theory: Complexities, criticisms, and opportunities. In The SAGE Handbook of Grounded Theory; SAGE Publications Ltd.: Thousand Oaks, CA, USA, 2010; pp. 417–435. [Google Scholar]

- Walton, S.; Tregidga, H.; Milne, M.J. The Triple-Bottom-Line: Benchmarking New Zealand’s Early Reporters; University of Otago: Dunedin, New Zealand, 2003. [Google Scholar]

- SustainAbility and UNEP. The Global Reporters: The 2000 Benchmark Survey; SustainAbility and UNEP: London, UK, 2000. [Google Scholar]

- Guenther, E.; Hoppe, H.; Poser, C. Environmental Corporate Social Responsibility of Firms in the Mining and Oil and Gas Industries: Current Status Quo of Reporting Following GRI Guidelines. Greener Manag. Int. 2007, 53, 7–25. [Google Scholar]

- Holder-Webb, L.; Cohen, J.R.; Nath, L.; Wood, D. The supply of corporate social responsibility disclosures among US firms. J. Bus. Ethics 2009, 84, 497–527. [Google Scholar] [CrossRef]

- Morhardt, J.E.; Baird, S.; Freeman, K. Scoring corporate environmental and sustainability reports using GRI 2000, ISO 14031 and other criteria. Corp. Soc. Responsib. Environ. Manag. 2002, 9, 215–233. [Google Scholar] [CrossRef]

- Scheel, C.; Mecham, J.; Zuccarello, V.; Mattes, R. An evaluation of the inter-rater and intra-rater reliability of OccuPro’s functional capacity evaluation. Work 2018, 60, 465–473. [Google Scholar] [CrossRef] [Green Version]

- Corden, A.; Sainsbury, R. Exploring ‘quality’: Research participants’ perspectives on verbatim quotations. Int. J. Soc. Res. Methodol. 2006, 9, 97–110. [Google Scholar] [CrossRef]

- Gomer, S.; Jones, A. Survey: How Companies Manage Sustainability: McKinsey Global Survey Result; McKinsey & Company: Atlanta, GA, USA, 2010. [Google Scholar]

- Grayson, D. Business-Led Corporate Responsibility Coalitions: Learning from the Example of Business in the Community. 2007. Available online: http://hdl.handle.net/1826/3428 (accessed on 20 December 2022).

- Hill, Z.; Tawiah-Agyemang, C.; Kirkwood, B.; Kendall, C. Are verbatim transcripts necessary in applied qualitative research: Experiences from two community-based intervention trials in Ghana. Emerg. Themes Epidemiol. 2022, 19, 5. [Google Scholar] [CrossRef] [PubMed]

- Gray, R. Thirty years of Social Accounting, Reporting and Auditing: What (if anything) Have We Learnt? Bus. Ethics A Eur. Rev. 2001, 10, 9–15. [Google Scholar] [CrossRef]

- Gray, R.; Owen, D.; Adams, C. Accounting and Accountability; Prentice Hall: Edinburgh, UK, 1996. [Google Scholar]

- Gray, R.; Kouhy, R.; Lavers, S. Constructing a research database of social and environmental reporting by UK companies. Account. Audit. Account. J. 1995, 8, 78–101. [Google Scholar] [CrossRef]

- Kozminsky, L.; Nathan, N.; Kozminsky, E. Using concept mapping to construct new knowledge while analyzing research data: The case of the grounded theory method. In Concept Mapping: Connecting Educators: Proceedings of the Third International Conference on Concept Mapping; Tallinn University: Tallinn, Estonia, 2008; Volume 2, pp. 704–708. [Google Scholar]

- Eccles, R.G.; Krzus, M.P.; Rogers, J.; Serafeim, G. The need for sector-specific materiality and sustainability reporting standards. J. Appl. Corp. Financ. 2012, 24, 65–71. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The power of transparency. Bus. Strategy Rev. 2011. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1467-8616.2011.00780.x (accessed on 10 January 2021). [CrossRef]

- Alasuutari, P. Researching Culture: Qualitative Method and Cultural Studies; Sage: Singapore, 1995. [Google Scholar]

- Bryant, A.; Charmaz, K. (Eds.) The Sage Handbook of Grounded Theory; Sage: Singapore, 2007. [Google Scholar]

- Corbin, J.M.; Strauss, A. Grounded theory research: Procedures, canons, and evaluative criteria. Qual. Sociol. 1990, 13, 3–21. [Google Scholar] [CrossRef]

| Scope of Reporting | Scoring Guide | ||

|---|---|---|---|

| Assess the reporting scope & coverage |

| ||

| 1 | Emissions/Consumptions | Required Reporting Items | Scoring Guide |

| 1.1 | Fuel Consumption Only some sectors need to report their fuel consumption, e.g., restaurants with fuel-cooking facilities and manufacturing with own power generators, etc.) | The volume of

| 0—no disclosure 1—limited scope and fail to report all three items, i.e., limited disclosure) or general mention (provide no actual figures but only descriptions) 2—limited disclosure or limited scope 3—Complete disclosure, no limitation on the reporting scope and report all the three items. 4—beyond the requirement—provided a clear and detailed breakdown, etc. |

| 1.1 | Vehicle Consumption Companies are not required to report if not owning any vehicles or only owning electric vehicles | The volume of

| 0—no disclosure 1—limited scope and fail to report all three items, i.e., limited disclosure) or general mention (provide no actual figures but only descriptions) 2—limited disclosure or limited scope 3—Complete disclosure, no limitation on the reporting scope and report all the three items. 4—beyond the requirement—provided a clear and detailed breakdown, etc. |

| 1.2 | Greenhouse Gases Emission | Volume (in tons) of GHG emission (including CO2, CH4/H2O) The emission can be classified by three scopes:

| 0—no disclosure 1—limited scope and fail to report any items i.e., limited disclosure or general mention (provide no actual figures but only descriptions) or no scope classification when reporting figures (provide only a lump sum figure) 2—limited disclosure—missing any of the items on the left; or fail to report emission figures of all required scopes 3—Complete disclosure, no limitation on the reporting scope and report all the two items mentioned on the left. 4—beyond the requirement—provided a clear and detailed breakdown, etc. |

| 1.3 | Total Hazardous waste produced |

| 0—no disclosure 1—limited scope and limited disclosure (fail to report all the two items, e.g., missing the intensity figure) or general mention (provide no actual figures but only descriptions) 2—limited disclosure or limited scope 3—Complete disclosure, no limitation on the reporting scope and report all the items mentioned on the left. 4—beyond requirement—provided a clear and detail breakdown (e.g., breakdown by waste disposal method) |

| 1.4 | Total non-Hazardous waste produced |

| 0—no disclosure 1—limited scope and limited disclosure (fail to report all the indicators, e.g., missing the intensity figure) or general mention (provide no actual figures but only descriptions) 2—limited disclosure or limited scope 3—Complete disclosure, no limitation on the reporting scope and report all the items mentioned on the left. 4—beyond requirement—provided a clear and detail breakdown (e.g., breakdown by waste disposal method) |

| 1.5 | Emission control/Measures | Set up a concrete measure controlling and reducing emission mentioned above. This section includes:

| 0—no disclosure 1—provide a brief and general description only 2—limited disclosure—missing target or measure 3—Complete disclosure (include 1, 2) 4—A concrete/detailed initiative is formed |

| 1.6 | Waste disposal initiative (Need to mention both hazardous and non-hazardous—otherwise, is considered incomplete disclosure) | Set up a concrete measure controlling and reducing waste mentioned above. This section includes 4 items:

| 0—no disclosure 1—provide a brief and general description only—abstract narrative statement or mention only one item of 1, 2, 3 on the left. 2—Missing 1 items of 1, 2, 3 on the left 3—Complete disclosure (include 1, 2, 3) 4—A concrete/detailed initiative is formed |

| 2 | Use of Resources | Indicators | Scoring Guide |

| 2.1 | Energy Consumption | Energy Consumption by

| 0—no disclosure 1—provide a brief and general description only or missing intensity information and fail to break down the energy consumption by type (only providing a lump sum figure) or Limited disclosure, i.e., missing volume or intensity figure and limited scope 2—Limited disclosure or limited scope 3—complete disclosure 4—detailed breakdown |

| 2.2 | Water Consumption | Water Consumption by

| 0—no disclosure 1—provide a brief and general description only 2—Limited disclosure or limited scope 3—complete disclosure 4—detailed breakdown |

| 2.3 | Energy use efficiency | Set up a concrete energy use initiative This section includes 2 items:

| 0—no disclosure 1—provide a brief and general description only 2—Missing any of the items on the left 3—complete disclosure 4—A concrete/detailed initiative is formed |

| 2.4 | Water use efficiency | Set up a concrete water use initiative This section includes 3 items:

| 0—no disclosure 1—Missing more than 1 items on the left 2—Missing any of the items on the left 3—complete disclosure 4—A concrete/detailed initiative is formed |

| 2.5 | Total packaging material used (if applicable) only applicable to particular industries |

| 0—no disclosure 1—provide a brief and general description only Or Limited disclosure, i.e., missing volume or intensity figure and limited scope 2.—Limited disclosure or limited scope 3—Complete disclosure 4—beyond requirement—detailed breakdown |

| 3.1 | The environment and natural resources | Required Reporting Items | Scoring Guide |

| Description of the Significant impacts of activities on the environmental and natural resources and the actions taken to manage. | Two items are included:

| 0—fail to perform a specific assessment of the significant impact on environmental and natural resources. No discussion on the impact. 1—general mention—provide a substantive description of the significant impacts w/o evidence or fail to address the policies/measure on the issue. 2—identify the significant impacts w/evidence and list the policies/measure regarding the issue. 3—fully comply with the requirement: state the significant impacts and address the detailed policies that are closely related to the impacts. 4—beyond requirement—provided a detailed and clear explanations | |

| Aspects and KPIs | Short form | Average Score |

|---|---|---|

| Aspect A1 | Emissions | 2.16 |

| A1.1 | Air emissions | 1.54 |

| A1.2 | Greenhouse gases | 2.16 |

| A1.3 | Hazardous waste | 1.94 |

| A1.4 | Non-hazardous waste | 1.83 |

| A1.5 | Emission mitigants | 2.64 |

| A1.6 | Wastes mitigants | 2.74 |

| Aspect A2 | Use of resources | 2.35 |

| A2.1 | Energy consumption | 2.49 |

| A2.2 | Water consumption | 2.49 |

| A2.3 | Energy efficiency | 2.85 |

| A2.4 | Water efficiency | 1.98 |

| A2.5 | Packaging material | 1.58 |

| Aspect A3/A3.1 | Environment and natural resources | 1.44 |

| 12 KPI Overall Average Score | 1.98 |

| Average Score | |

|---|---|

| Aspect “A2 Use of Resources” | 2.35 |

| A2.1 Direct and/or indirect energy consumption by type (e.g., electricity, gas or oil) in total (kWh in ‘000s) and intensity (e.g., per unit of production volume, per facility). | 2.49 |

| A2.2 Water consumption in total and intensity (e.g., per unit of production volume, per facility). | 2.49 |

| A2.3 Description of energy use efficiency initiatives and results achieved | 2.85 |

| Industry | Overall Average Score |

|---|---|

| Conglomerates | 1.40 |

| Consumer Goods | 2.01 |

| Energy | 2.03 |

| Financials | 2.03 |

| Industrial Goods | 2.17 |

| Information Technology | 2.04 |

| Materials | 1.94 |

| Properties and Constructions | 1.94 |

| Services | 1.89 |

| Telecommunication | 1.33 |

| Utilities | 2.10 |

| Quantitative KPIs | Average Score | |

|---|---|---|

| A1.1 | Air emissions | 1.54 |

| A1.2 | Greenhouse gases | 2.16 |

| A1.3 | Hazardous waste | 1.94 |

| A1.4 | Non-hazardous waste | 1.83 |

| A2.1 | Energy consumption | 2.49 |

| A2.2 | Water consumption | 2.49 |

| A2.5 | Packaging material | 1.58 |

| Overall Average Score | 2.00 | |

| Qualitative KPIs | Average Score | |

| A1.5 | Emission mitigants | 2.64 |

| A1.6 | Waste mitigant | 2.74 |

| A2.3 | Energy efficiency | 2.85 |

| A2.4 | Water efficiency | 1.98 |

| A3.1 | Environment and natural resources | 1.58 |

| Overall Average Score | 2.36 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yip, A.W.H.; Yu, W.Y.P. The Quality of Environmental KPI Disclosure in ESG Reporting for SMEs in Hong Kong. Sustainability 2023, 15, 3634. https://doi.org/10.3390/su15043634

Yip AWH, Yu WYP. The Quality of Environmental KPI Disclosure in ESG Reporting for SMEs in Hong Kong. Sustainability. 2023; 15(4):3634. https://doi.org/10.3390/su15043634

Chicago/Turabian StyleYip, Angus W. H., and William Y. P. Yu. 2023. "The Quality of Environmental KPI Disclosure in ESG Reporting for SMEs in Hong Kong" Sustainability 15, no. 4: 3634. https://doi.org/10.3390/su15043634

APA StyleYip, A. W. H., & Yu, W. Y. P. (2023). The Quality of Environmental KPI Disclosure in ESG Reporting for SMEs in Hong Kong. Sustainability, 15(4), 3634. https://doi.org/10.3390/su15043634