Why Corporate Sustainability Is Not Yet Measured

Abstract

:1. Introduction

1.1. Background

1.2. Objectives

2. Measurements of Corporate Sustainability

2.1. Methodology

- The concept must be properly defined in its constitutive pillars;

- The constitutive pillars are necessary conditions and imply non-substitutability;

- Proposed measures must be properly linked to the identified concept and data aggregation must align;

- The concept must be defined in its highest extension, referred to as the ideal type guideline. For example, in order to know how full a glass is, we need to know the glass’s full capacity, or in order to know how tall a person is, we need to have knowledge of the highest height.

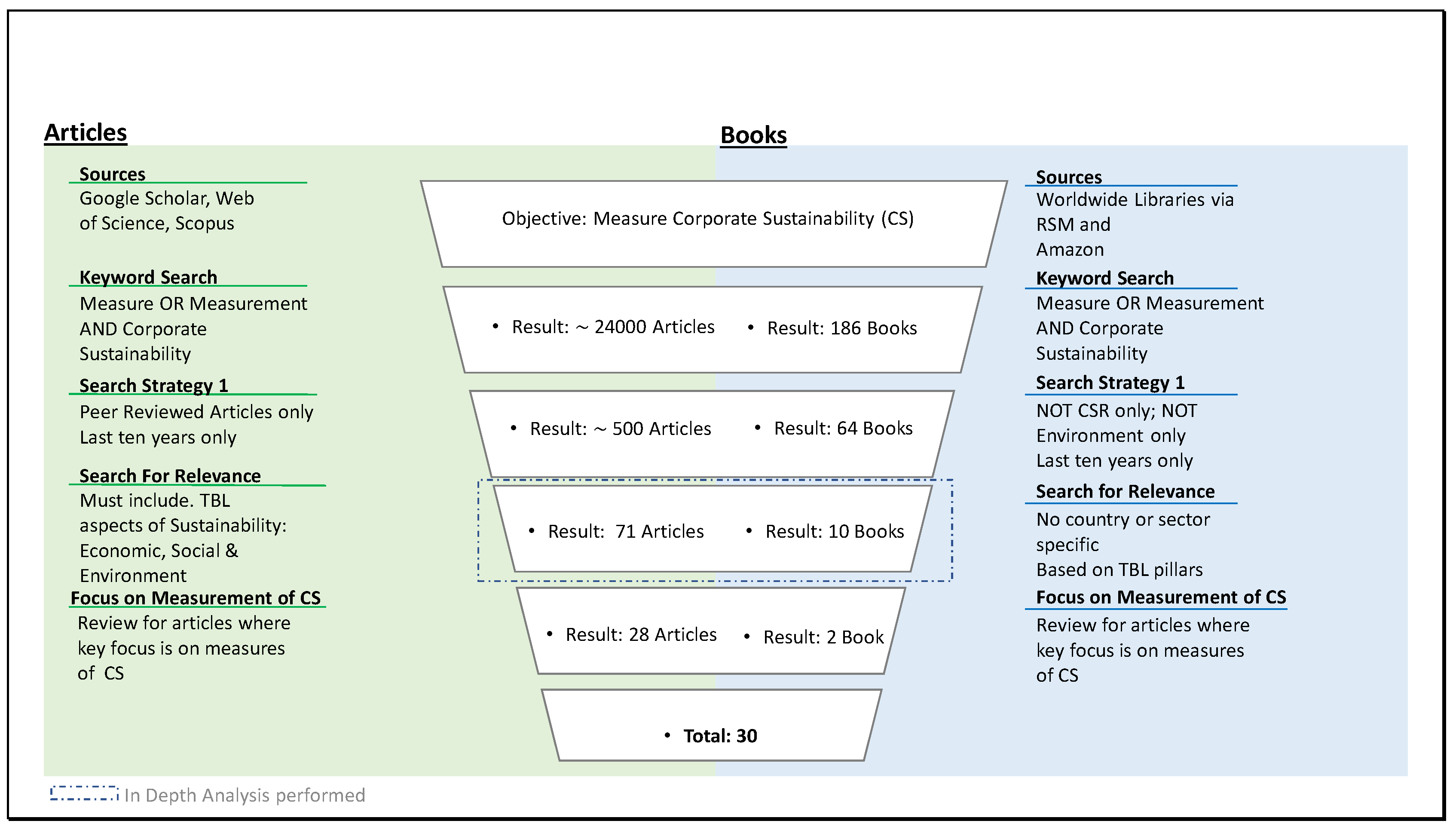

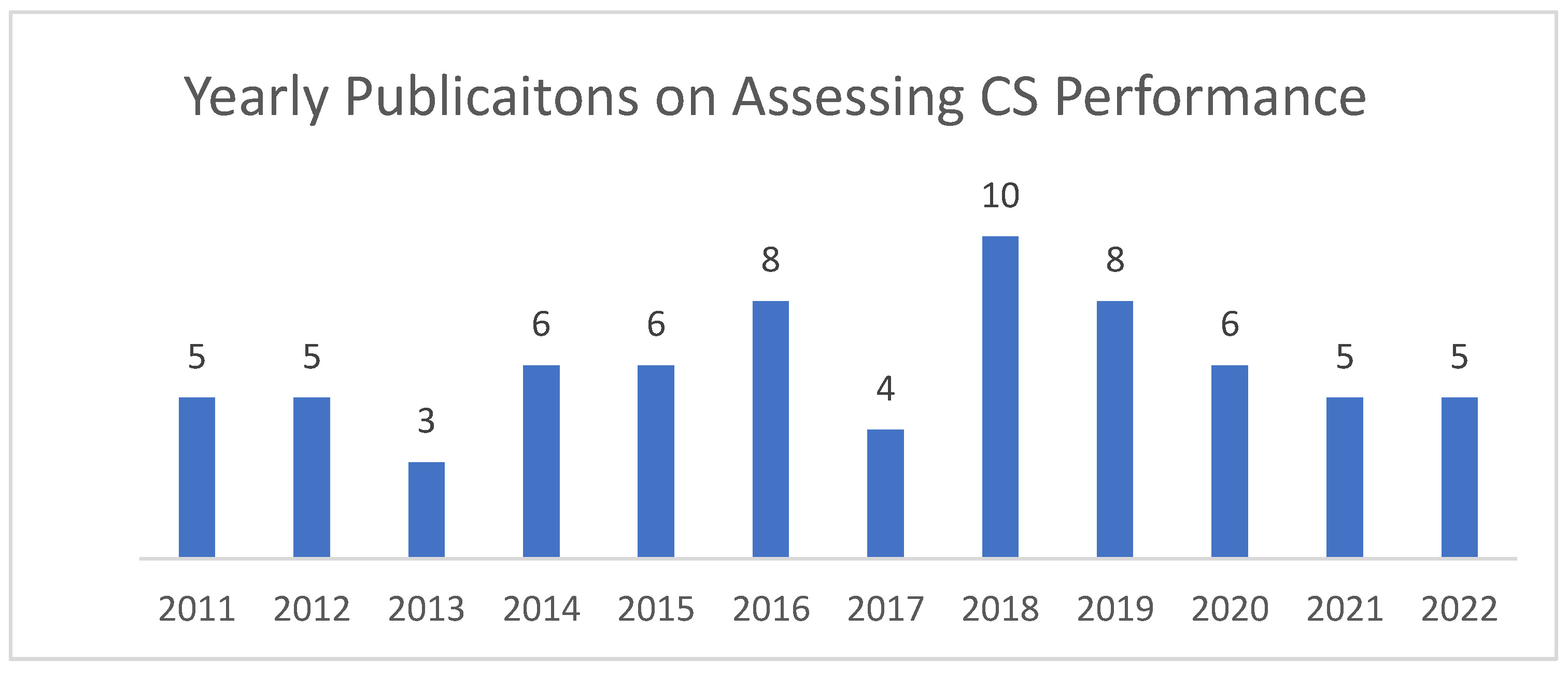

2.2. Search Strategy

3. Findings and Discussion

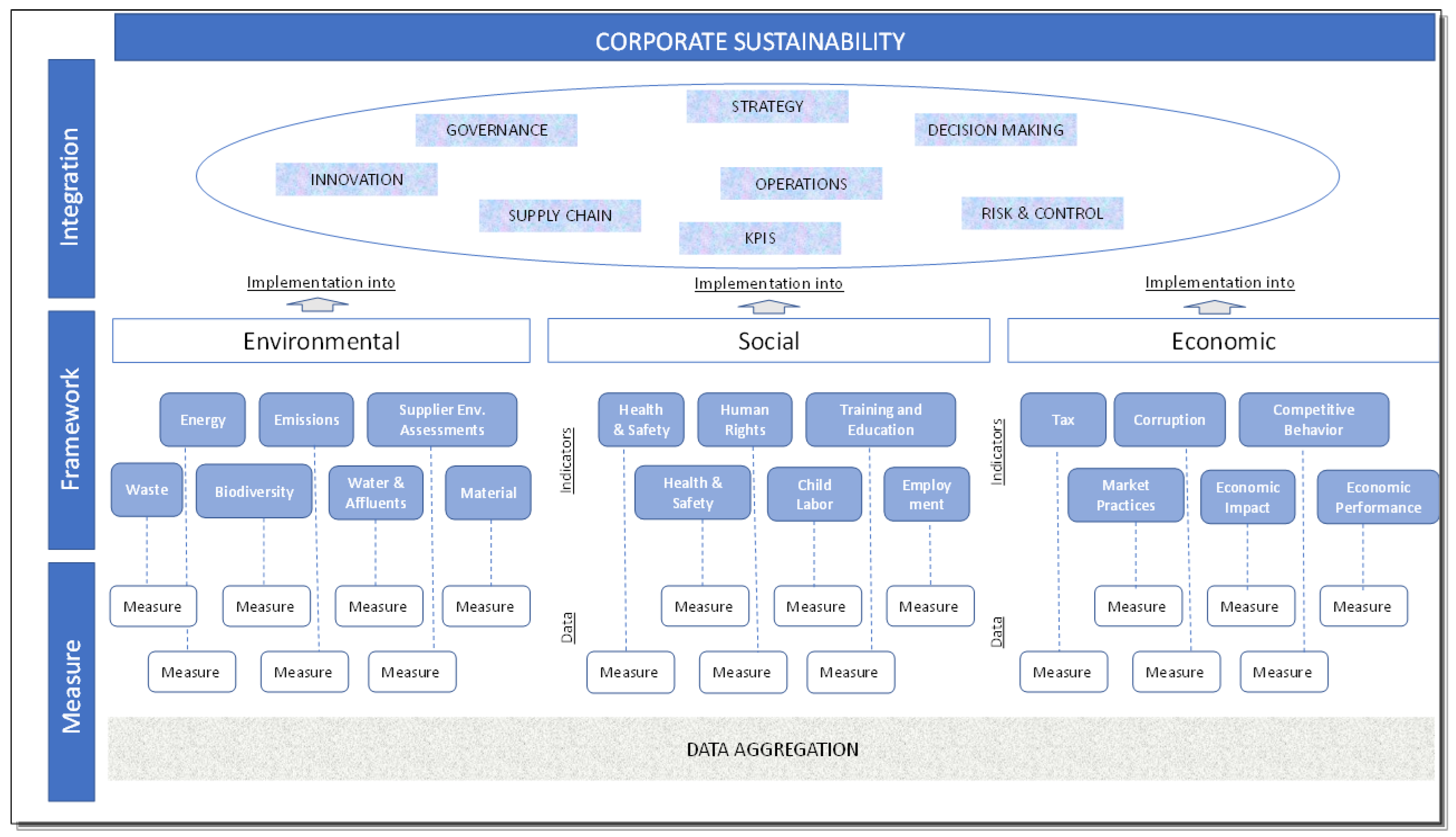

3.1. Frameworks

3.2. Integration

3.3. Measure

3.4. Other Subjects

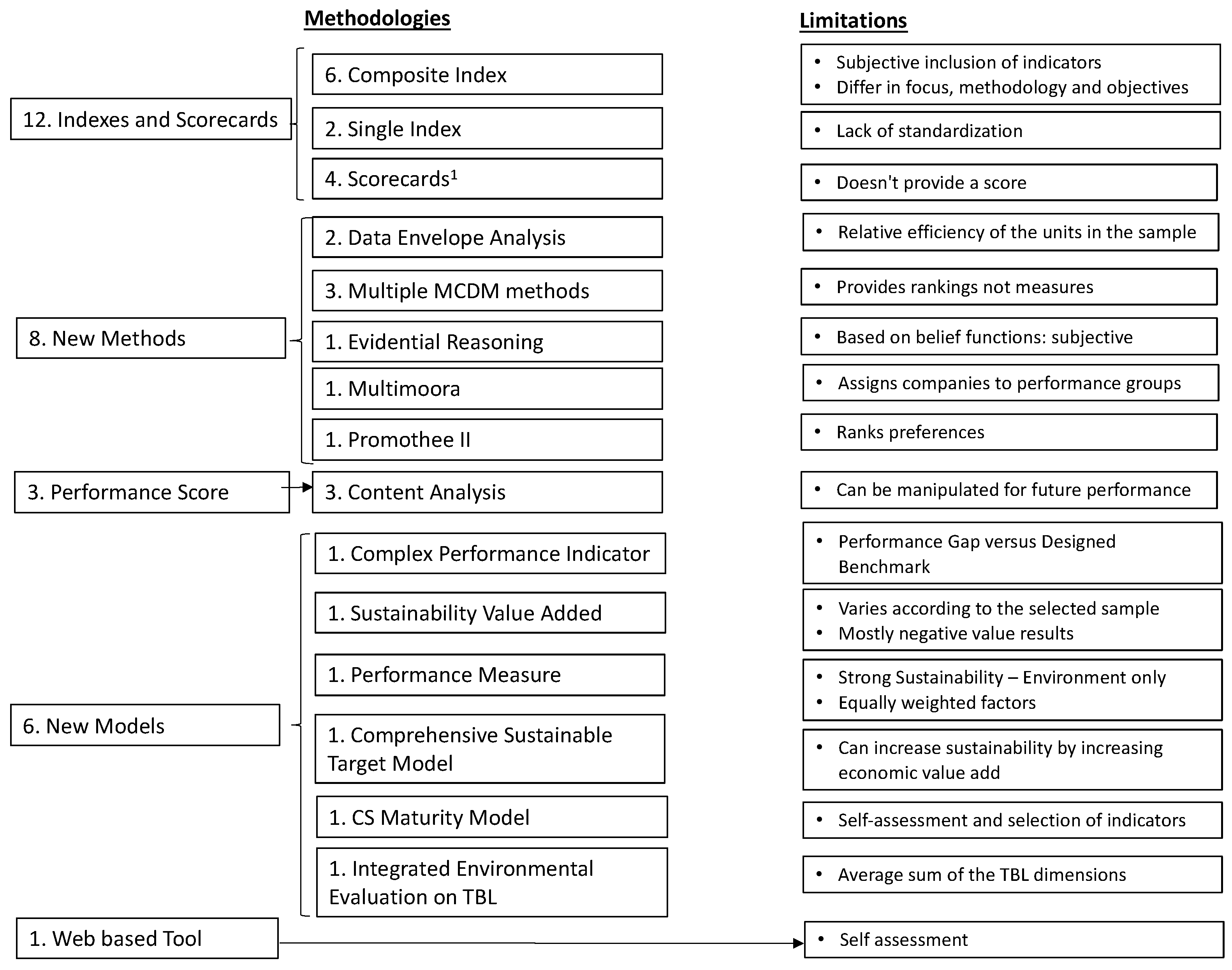

4. Analysis of the Existing Measurement Methodologies of CS

- 1.

- Composite and Single Indexes, and Scorecards;

- 2.

- Performance score based on content analysis;

- 3.

- New methodologies;

- 4.

- New models/tools.

4.1. Indexes and Scorecards

4.2. Content Analysis

4.3. New Methodologies

4.4. New Models

5. Why CS Is Not Yet Measured

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Pazienza, M.; de Jong, M.; Schoenmaker, D. Clarifying the concept of corporate sustainability and providing convergence for its definition. Sustainability 2022, 14, 7838. [Google Scholar] [CrossRef]

- Nicolăescu, E.; Alpopi, C.; Zaharia, C. Measuring corporate sustainability performance. Sustainability 2015, 7, 851–865. [Google Scholar] [CrossRef] [Green Version]

- Neely, A.; Gregory, M.; Platts, K. Performance measurement system design: A literature review and research agenda. Int. J. Oper. Prod. Manag. 2005, 25, 1228–1263. [Google Scholar] [CrossRef]

- Searcy, C. Updating corporate sustainability performance measurement systems. Meas. Bus. Excell. 2011, 15, 44–56. [Google Scholar] [CrossRef]

- Lobos, V.; Partidario, M. Theory versus practice in strategic environmental assessment (SEA). Environ. Impact Assess. Rev. 2014, 48, 34–46. [Google Scholar] [CrossRef]

- Adams, C.A.; Muir, S.; Hoque, Z. Measurement of sustainability performance in the public sector. Sustain. Account. Manag. Policy J. 2014, 5, 46–67. [Google Scholar] [CrossRef]

- Čuček, L.; Klemeš, J.J.; Kravanja, Z. A review of footprint analysis tools for monitoring impacts on sustainability. J. Clean. Prod. 2012, 34, 9–20. [Google Scholar] [CrossRef]

- Azadi, M.; Jafarian, M.; Mirhedayatian, S.M.; Saen, R.F. A novel fuzzy data envelopment analysis for measuring corporate sustainability performance. Int. J. Product. Qual. Manag. 2015, 16, 312–324. [Google Scholar] [CrossRef]

- Milne, M.J.; Gray, R. W(h)ither ecology? The triple bottom line, the global reporting initiative, and corporate sustainability reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Tregida, H.; Milne, M.; Kearins, K. (Re)presenting ‘sustainable organizations. Account. Organ. Soc. 2014, 39, 477–494. [Google Scholar] [CrossRef]

- Mahoney, L.S.; Thorne, L.; Cecil, L.; LaGore, W. A research note on standalone corporate social responsibility reports: Signaling or greenwashing? Crit. Perspect. Account. 2013, 24, 350–359. [Google Scholar] [CrossRef]

- Antolín-López, R.; Delgado-Ceballos, J.; Montiel, I. Deconstructing corporate sustainability: A comparison of different stakeholder metrics. J. Clean. Prod. 2016, 136, 5–17. [Google Scholar] [CrossRef]

- Caiado, R.G.G.; Quelhas, O.L.G.; Nascimento, D.L.M.; Anholon, R.; Leal Filho, W. Measurement of sustainability performance in Brazilian organizations. Int. J. Sustain. Dev. World Ecol. 2018, 25, 312–326. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef]

- Molina-Azorín, J.F.; Claver-Cortés, E.; López-Gamero, M.D.; Tarí, J.J. Green management and financial performance: A literature review. Manag. Decis. 2009, 47, 1080–1100. [Google Scholar] [CrossRef]

- Silva, S.; Nuzum, A.-K.; Schaltegger, S. Stakeholder expectations on sustainability performance measurement and assessment. A systematic literature review. J. Clean. Prod. 2019, 217, 204–215. [Google Scholar] [CrossRef]

- Bamford, D.; Yang, J.-B.; Sureeyatanapas, P. Evaluation of corporate sustainability. Front. Eng. Manag. 2014, 1, 176–194. [Google Scholar]

- Howard-Grenville, J.; Davis, J.; Dyllick, T.; Joshi, A.; Miller, C.; Thau, S.; Tsui, A.S. Sustainable development for a better world: Contributions of leadership, management and organizations: Submission deadline: July 1 to July 30, 2018. Acad. Manag. Discov. 2017, 3, 107–110. [Google Scholar] [CrossRef] [Green Version]

- Engida, T.G.; Rao, X.; Berentsen, P.B.; Lansink, A.G.O. Measuring corporate sustainability performance–the case of European food and beverage companies. J. Clean. Prod. 2018, 195, 734–743. [Google Scholar] [CrossRef]

- Morioka, S.N.; Iritani, D.R.; Ometto, A.R.; Carvalho, M.M.d. Systematic review of the literature on corporate sustainability performance measurement: A discussion of contributions and gaps. Gestão Produção 2018, 25, 284–303. [Google Scholar] [CrossRef]

- Montiel, I.; Delgado-Ceballos, J. Defining and measuring corporate sustainability: Are we there yet? Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Harik, R.; El Hachem, W.; Medini, K.; Bernard, A. Towards a holistic sustainability index for measuring sustainability of manufacturing companies. Int. J. Prod. Res. 2015, 53, 4117–4139. [Google Scholar] [CrossRef]

- Helleno, A.L.; de Moraes, A.J.I.; Simon, A.T. Integrating sustainability indicators and Lean Manufacturing to assess manufacturing processes: Application case studies in Brazilian industry. J. Clean. Prod. 2017, 153, 405–416. [Google Scholar] [CrossRef]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainable operations: Their impact on the triple bottom line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Pagell, M.; Gobeli, D. How plant managers’ experiences and attitudes toward sustainability relate to operational performance. Prod. Oper. Manag. 2009, 18, 278–299. [Google Scholar] [CrossRef]

- Trianni, A.; Cagno, E.; Neri, A. Modelling barriers to the adoption of industrial sustainability measures. J. Clean. Prod. 2017, 168, 1482–1504. [Google Scholar] [CrossRef]

- Garcia, S.; Cintra, Y.; Rita de Cássia, S.; Lima, F.G. Corporate sustainability management: A proposed multi-criteria model to support balanced decision-making. J. Clean. Prod. 2016, 136, 181–196. [Google Scholar] [CrossRef]

- Mura, M.; Longo, M.; Micheli, P.; Bolzani, D. The evolution of sustainability measurement research. Int. J. Manag. Rev. 2018, 20, 661–695. [Google Scholar] [CrossRef]

- Büyüközkan, G.; Karabulut, Y. Sustainability performance evaluation: Literature review and future directions. J. Environ. Manag. 2018, 217, 253–267. [Google Scholar] [CrossRef]

- Searcy, C. Corporate sustainability performance measurement systems: A review and research agenda. J. Bus. Ethics 2012, 107, 239–253. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The sustainability balanced scorecard–linking sustainability management to business strategy. Bus. Strategy Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Kolk, A.; Hong, P.; Van Dolen, W. Corporate social responsibility in China: An analysis of domestic and foreign retailers’ sustainability dimensions. Bus. Strategy Environ. 2010, 19, 289–303. [Google Scholar] [CrossRef] [Green Version]

- Pranugrahaning, A.; Donovan, J.D.; Topple, C.; Masli, E.K. Corporate sustainability assessments: A systematic literature review and conceptual framework. J. Clean. Prod. 2021, 295, 126385. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research: Literature review and future research agenda. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Chowdhury, P.; Paul, S.K. Applications of MCDM methods in research on corporate sustainability: A systematic literature review. Manag. Environ. Qual. Int. J. 2020, 31, 385–405. [Google Scholar] [CrossRef]

- Schaltegger, S.; Christ, K.L.; Wenzig, J.; Burritt, R.L. Corporate sustainability management accounting and multi-level links for sustainability—A systematic review. Int. J. Manag. Rev. 2022, 24, 480–500. [Google Scholar] [CrossRef]

- Pencle, N. Motivating Corporate Sustainability Research in Management Accounting Through the Lens of Paradox Theory. Account. Perspect. 2022, 21, 663–696. [Google Scholar] [CrossRef]

- Goertz, G. Social Science Concepts and Measurement. Available online: https://press.princeton.edu/books/hardcover/9780691205465/ (accessed on 2 March 2022).

- Baumgartner, R.J. Managing corporate sustainability and CSR: A conceptual framework combining values, strategies and instruments contributing to sustainable development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Maas, K.; Schaltegger, S.; Crutzen, N. Reprint of Advancing the integration of corporate sustainability measurement, management and reporting. J. Clean. Prod. 2016, 136, 1–4. [Google Scholar] [CrossRef]

- Pádua, S.I.D.; Jabbour, C.J.C. Promotion and evolution of sustainability performance measurement systems from a perspective of business process management: From a literature review to a pentagonal proposal. Bus. Process Manag. J. 2015, 21, 403–418. [Google Scholar] [CrossRef]

- Sala, S.; Ciuffo, B.; Nijkamp, P. A systemic framework for sustainability assessment. Ecol. Econ. 2015, 119, 314–325. [Google Scholar] [CrossRef]

- Delai, I.; Takahashi, S. Sustainability measurement system: A reference model proposal. Soc. Responsib. J. 2011, 7, 438–471. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z. Corporate sustainability performance assessment: An analytical hierarchy process approach. Int. J. Intercult. Inf. Manag. 2014, 4, 1–14. [Google Scholar] [CrossRef]

- Kocmanová, A.; Šimberová, I. Determination of environmental, social and corporate governance indicators: Framework in the measurement of sustainable performance. J. Bus. Econ. Manag. 2014, 15, 1017–1033. [Google Scholar] [CrossRef] [Green Version]

- Moldavska, A.; Welo, T. A Holistic approach to corporate sustainability assessment: Incorporating sustainable development goals into sustainable manufacturing performance evaluation. J. Manuf. Syst. 2019, 50, 53–68. [Google Scholar] [CrossRef]

- Cagno, E.; Neri, A.; Howard, M.; Brenna, G.; Trianni, A. Industrial sustainability performance measurement systems: A novel framework. J. Clean. Prod. 2019, 230, 1354–1375. [Google Scholar] [CrossRef]

- Mal, H.; Varma, M.; Vishvakarma, N.K. An empirical study to prioritize the determinants of corporate sustainability performance using analytic hierarchy process. Meas. Bus. Excell. 2022. [Google Scholar] [CrossRef]

- Morioka, S.N.; Carvalho, M.M. Measuring sustainability in practice: Exploring the inclusion of sustainability into corporate performance systems in Brazilian case studies. J. Clean. Prod. 2016, 136, 123–133. [Google Scholar] [CrossRef]

- Ihlen, Ø.; Roper, J. Corporate reports on sustainability and sustainable development: ‘We have arrived’. Sustain. Dev. 2014, 22, 42–51. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Zutshi, A.; Ahmad, N. An integrated management systems approach to corporate sustainability. Eur. Bus. Rev. 2011, 56, 7–17. [Google Scholar]

- Medel-González, F.; García-Ávila, L.F.; Salomon, V.A.P.; Marx-Gómez, J.; Hernández, C.T. Sustainability performance measurement with Analytic Network Process and balanced scorecard: Cuban practical case. Production 2016, 26, 527–539. [Google Scholar] [CrossRef] [Green Version]

- Kocmanová, A.; Pavláková Dočekalová, M.; Škapa, S.; Smolíková, L. Measuring corporate sustainability and environmental, social, and corporate governance value added. Sustainability 2016, 8, 945. [Google Scholar] [CrossRef] [Green Version]

- Dočekalová, M.P.; Kocmanová, A. Composite indicator for measuring corporate sustainability. Ecol. Indic. 2016, 61, 612–623. [Google Scholar] [CrossRef]

- Aras, G.; Tezcan, N.; Furtuna, O.K. Multidimensional comprehensive corporate sustainability performance evaluation model: Evidence from an emerging market banking sector. J. Clean. Prod. 2018, 185, 600–609. [Google Scholar] [CrossRef]

- Ahi, P.; Searcy, C.; Jaber, M.Y. A quantitative approach for assessing sustainability performance of corporations. Ecol. Econ. 2018, 152, 336–346. [Google Scholar] [CrossRef]

- Sari, Y.; Hidayatno, A.; Suzianti, A.; Hartono, M.; Susanto, H. A corporate sustainability maturity model for readiness assessment: A three-step development strategy. Int. J. Product. Perform. Manag. 2021, 70, 1162–1186. [Google Scholar] [CrossRef]

- Siew, R.Y. A review of corporate sustainability reporting tools (SRTs). J. Environ. Manag. 2015, 164, 180–195. [Google Scholar] [CrossRef] [PubMed]

- Christofi, A.; Christofi, P.; Sisaye, S. Corporate sustainability: Historical development and reporting practices. Manag. Res. Rev. 2012, 35, 157–172. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones Sustainability Index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Delmas, M.; Blass, V.D. Measuring corporate environmental performance: The trade-offs of sustainability ratings. Bus. Strategy Environ. 2010, 19, 245–260. [Google Scholar] [CrossRef]

- Pryshlakivsky, J.; Searcy, C. A heuristic model for establishing trade-offs in corporate sustainability performance measurement systems. J. Bus. Ethics 2017, 144, 323–342. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. The sustainability balanced scorecard: A systematic review of architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Ye, C.; Song, X.; Liang, Y. Corporate sustainability performance, stock returns, and ESG indicators: Fresh insights from EU member states. Environ. Sci. Pollut. Res. 2022, 29, 87680–87691. [Google Scholar] [CrossRef] [PubMed]

- Schneider, A.; Meins, E. Two dimensions of corporate sustainability assessment: Towards a comprehensive framework. Bus. Strategy Environ. 2012, 21, 211–222. [Google Scholar] [CrossRef]

- Mamede, P.; Gomes, C.F. Corporate sustainability measurement in service organizations: A case study from Portugal. Environ. Qual. Manag. 2014, 23, 49–73. [Google Scholar] [CrossRef]

- Delmas, M.A.; Clark, K.; Timmer, T.; McClellan, M. The State of Corporate Sustainability Disclosure. SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Iyer, J.R. Corporate Citizenship and Sustainability: Measuring Intangible, Fiscal, and Ethical Assets (Issn) Paperback; Business Expert Press: New York, NY, USA, 2020. [Google Scholar]

- Diez-Cañamero, B.; Bishara, T.; Otegi-Olaso, J.R.; Minguez, R.; Fernández, J.M. Measurement of corporate social responsibility: A review of corporate sustainability indexes, rankings and ratings. Sustainability 2020, 12, 2153. [Google Scholar] [CrossRef] [Green Version]

- Boiral, O.; Talbot, D.; Brotherton, M.C. Measuring sustainability risks: A rational myth? Bus. Strategy Environ. 2020, 29, 2557–2571. [Google Scholar] [CrossRef]

- Lee, K.-H.; Saen, R.F. Measuring corporate sustainability management: A data envelopment analysis approach. Int. J. Prod. Econ. 2012, 140, 219–226. [Google Scholar] [CrossRef]

- Saisana, M.; Tarantola, S. State-of-the-Art Report on Current Methodologies and Practices for Composite Indicator Development; European Commission, Joint Research Centre: Brussels, Belgium, 2002; Volume 214.

- Nikolaou, I.E.; Tsalis, T.A.; Evangelinos, K.I. A framework to measure corporate sustainability performance: A strong sustainability-based view of firm. Sustain. Prod. Consum. 2019, 18, 1–18. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. Development of composite sustainability performance index for steel industry. Ecol. Indic. 2007, 7, 565–588. [Google Scholar] [CrossRef]

- Saisana, M.; Saltelli, A.; Tarantola, S. Uncertainty and sensitivity analysis techniques as tools for the quality assessment of composite indicators. J. R. Stat. Soc. Ser. A (Stat. Soc.) 2005, 168, 307–323. [Google Scholar] [CrossRef]

- Sridhar, K.; Jones, G. The three fundamental criticisms of the Triple Bottom Line approach: An empirical study to link sustainability reports in companies based in the Asia-Pacific region and TBL shortcomings. Asian J. Bus. Ethics 2013, 2, 91–111. [Google Scholar] [CrossRef] [Green Version]

- Salvati, L.; Zitti, M. Assessing the impact of ecological and economic factors on land degradation vulnerability through multiway analysis. Ecol. Indic. 2009, 9, 357–363. [Google Scholar] [CrossRef]

- Morrison-Saunders, A.; Pope, J. Conceptualising and managing trade-offs in sustainability assessment. Environ. Impact Assess. Rev. 2013, 38, 54–63. [Google Scholar] [CrossRef] [Green Version]

- Olsthoorn, X.; Tyteca, D.; Wehrmeyer, W.; Wagner, M. Environmental indicators for business: A review of the literature and standardisation methods. J. Clean. Prod. 2001, 9, 453–463. [Google Scholar] [CrossRef]

- Rahdari, A.H.; Rostamy, A.A.A. Designing a general set of sustainability indicators at the corporate level. J. Clean. Prod. 2015, 108, 757–771. [Google Scholar] [CrossRef]

- Maltz, A.C.; Shenhar, A.J.; Reilly, R.R. Beyond the balanced scorecard:: Refining the search for organizational success measures. Long Range Plan. 2003, 36, 187–204. [Google Scholar] [CrossRef]

- Journeault, M. The Integrated Scorecard in support of corporate sustainability strategies. J. Environ. Manag. 2016, 182, 214–229. [Google Scholar] [CrossRef]

- Möller, A.; Schaltegger, S. The sustainability balanced scorecard as a framework for eco-efficiency analysis. J. Ind. Ecol. 2005, 9, 73–83. [Google Scholar] [CrossRef]

- Epstein, M.J.; Roy, M.-J. Sustainability in action: Identifying and measuring the key performance drivers. Long Range Plan. 2001, 34, 585–604. [Google Scholar] [CrossRef]

- Jensen, M.C. Value maximisation, stakeholder theory and the corporate objective function. In Unfolding Stakeholder Thinking; Routledge: Abingdon, UK, 2017; pp. 65–84. [Google Scholar]

- Molla, M.S.; Ibrahim, Y.B.; Ishak, Z.B. Corporate sustainability practices: A review on the measurements, relevant problems and a proposition. Glob. J. Manag. Bus. Res. 2019, 19, 1–8. [Google Scholar]

- Weber, R.P. Measurement models for content analysis. Qual. Quant. 1983, 17, 127–149. [Google Scholar] [CrossRef]

- Ng, L. Social Responsibility Disclosures of Selected New Zealand Companies for 1981, 1982 and 1983, Occasional Paper; Massey University: Palmerston North, New Zealand, 1985; Volume 54. [Google Scholar]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Milne, M.J.; Adler, R.W. Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar] [CrossRef] [Green Version]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes Ii, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Küçükbay, F.; Sürücü, E. Corporate sustainability performance measurement based on a new multicriteria sorting method. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 664–680. [Google Scholar] [CrossRef]

- Bezerra, P.R.S.; Schramm, F.; Schramm, V.B. A multicriteria model, based on the PROMETHEE II, for assessing corporate sustainability. Clean Technol. Environ. Policy 2021, 23, 2927–2940. [Google Scholar] [CrossRef]

- Vivas, R.; Sant’anna, Â.; Esquerre, K.; Freires, F. Measuring sustainability performance with multi criteria model: A case study. Sustainability 2019, 11, 6113. [Google Scholar] [CrossRef] [Green Version]

- Aktaş, N.; Demirel, N. A hybrid framework for evaluating corporate sustainability using multi-criteria decision making. Environ. Dev. Sustain. 2021, 23, 15591–15618. [Google Scholar] [CrossRef]

- Rao, S.-H. A hybrid MCDM model based on DEMATEL and ANP for improving the measurement of corporate sustainability indicators: A study of Taiwan High Speed Rail. Res. Transp. Bus. Manag. 2021, 41, 100657. [Google Scholar] [CrossRef]

- Wright, J.M.; Caudill, R.J. A more comprehensive and quantitative approach to corporate sustainability. Environ. Impact Assess. Rev. 2020, 83, 106409. [Google Scholar] [CrossRef]

- Dickinson, D. A Proposed Universal Environmental Metric; Lucent Technologies Bell Laboratories Technical Memorandum: Murray Hill, NJ, USA, 1999. [Google Scholar]

- Zenya, A.; Nystad, Ø. Assessing corporate sustainability with the enterprise sustainability evaluation tool (E-SET). Sustainability 2018, 10, 4661. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors | Year | Subject | Journal | |

|---|---|---|---|---|

| 1 | Baumgartner | 2013 | Offers a conceptual framework of the relevance of sustainability aspects of firms | CSR and Environmental Management |

| 2 | Cagno et al. | 2019 | Develops a new framework for the evaluation of industrial sustainability performance | Journal of Cleaner Production |

| 3 | Delai and Takahashi | 2011 | Develops a reference model for measuring | CS Social Responsibility Journal |

| 4 | Goyal et al. | 2013 | Identify the CS practices to improve sustainability performance | Journal of Modelling in Management |

| 5 | Kocmanová and Šimberová | 2014 | Determines CS indicators as a key framework of sustainable performance | Journal of Business Economics and Management |

| 6 | Maas et al. | 2016 | Proposes a comprehensive Framework | Journal of Cleaner Production |

| 7 | Moldavska and Welo | 2018 | Develops a framework to assist companies with identification of improvements to meet GSD goals | Sustainability |

| 8 | Pádua and Jabbour | 2015 | Identifies relevant aspects to guide promotion of CS | Business Process Management Journal |

| 9 | Sala et al. | 2015 | Presents a novel methodological framework for sustainability assessment | Ecological Economics |

| 10 | Searcy | 2014 | Identifies key requirements for measuring enterprise sustainability | Business Strategy & Environment |

| 11 | Mal | 2022 | Assesses and prioritize the numerous factors that influence CS performance | Measuring Business Excellence |

| Authors | Year | Subject | Journal | |

|---|---|---|---|---|

| 1 | Asif et al. | 2011 | Describes an integrated management system for the integration of CS into business processes | European Business Review |

| 2 | Baumgartner and Rauter | 2016 | Connects three dimensions of strategic management to encourage the integration of sustainability into corporate activities and strategies | International Journal of Business Insight and Transformation |

| 3 | Maas et al. | 2016 | Responds to how to integrate sustainability assessment, management accounting, control, and reporting. | Journal of Cleaner Production |

| 4 | Moldavska and Welo | 2019 | Develops a new CS assessment method to incorporate SDGs into corporate operations | Journal of Manufacturing Systems |

| 5 | Morioka and Carvalho | 2016 | Investigate incorporation of sustainability in corporate performance | Journal of Cleaner Production |

| Authors | Year | Category | Provides or Embraces a Definition or Concept of CS | CS Links the Measure to the Concept of CS | Determines the Highest Extension | |

|---|---|---|---|---|---|---|

| 1 | Engida et al. | 2018 | Composite Index | No | No | No |

| 2 | Goyal and Rahman | 2014 | Composite Index | No | No | No |

| 3 | Jiang et al. | 2018 | Composite Index | Strategy for the corporates to seek the balance among the economic profit, environmental and social responsibility, and other stakeholders. | No | No |

| 4 | Kocmanova et al. | 2017 | Composite Index | Aim is to achieve a balanced relationship between environmental, economic, and social pillars | No | No |

| 5 | Li et al. | 2012 | Composite Index | Sustainability is characterized into such three dimensions as economic, environmental, and social, | No | No |

| 6 | Nikolau et al. | 2019 | Composite Index | No- Highlights the multiplicity of CS definitions | No | No |

| 7 | Ngai et al. | 2014 | Single Index | No- Offer multiple considerations of it | No | No |

| 8 | Schirppe and Ribeiro | 2018 | Single Index | Sustainability factors: environmental limitations, sustainable development, and requirements of the society–TBL, WCED 87 | No | No |

| 9 | Journeault | 2016 | Scorecard | No- Reports some of the existing definitions | No | No |

| 10 | Medel-Gonzalez et al. | 2016 | Scorecard | CS is a multidimensional concept which includes business strategies, financial returns, costumer’s satisfaction, stakeholder’s interests, internal process, and human factor. | No | No |

| 11 | Aras et al. | 2018 | Performance Score | Sustainability includes Social, Environmental, Economic, Governance and Profitability dimensions | No | No |

| 12 | Aras, Tezcan, Furtuna | 2017 | Performance Score | Sustainability includes Social, Environmental, Economic, Governance and Profitability dimensions | No | No |

| 13 | Molla et al. | 2019 | Performance Score | No- Provides overview of the multiple definitions | No | No |

| 14 | Azadi et al. | 2015 | New Method | No | No | No |

| 15 | Bamford et al. | 2015 | New Method | No | No | No |

| 16 | Küçükbay and Sürücü | 2019 | New Method | The concept of sustainability deals with protecting and sustaining society and environment for future generations while trying to meet the maximization of market capitalization | No | No |

| 17 | Lee and Sean | 2012 | New Method | No- Offer multiple considerations of it | No | No |

| 18 | Vival et al. | 2019 | New Method | No- Reports WCED 1987 as the most popular | No | No |

| 19 | Aktaş and Demirel | 2021 | New Method | No- Provides overview of the multiple definitions | No | No |

| 20 | Bezerra et al. | 2021 | New Method | No- Specifies the proposed model will assess environment, social, economic and governance based on popularity | No | No |

| 21 | Rao | 2021 | New Method | Adopts Mauer definition and concept | No | No |

| 22 | Ahi, Searcy, Jaber | 2018 | New Model | Long term capability of wellbeing by encompassing the responsible management of all resources, which results in meeting the needs of the present without compromising those of future generations | Yes—linked to strong sustainability | No |

| 23 | Docekalova et al. | 2016 | New Model | No- It offers many definitions, but it highlights that its measurement is the extent of integration of social, economic environmental, and governance pillars | No | No |

| 24 | Kocmanova et al. | 2016 | New Model | No- specifies ESG factors are important for corporate strategy | No | No |

| 25 | Garcia et al. | 2016 | New Model | TBL | No | No |

| 26 | Wright and Caudill | 2020 | New Model | No- indicates that debates still continue about the definition of CS | No | No |

| 27 | Sari et al. | 2020 | New Model | No- Mentions a few definitions. | No | No. Process implementation only |

| 28 | Zenya and Nystad | 2016 | New Tool | No- Highlights the multitude of interpretations | No | No |

| Author | Year | Title | Classification | Subject | |

|---|---|---|---|---|---|

| 1 | Epstein et al. | 2014 | List of cases, figures on table. Making Sustainability Work | Framework | Provides an output vs outcome model. Variety of Self Developed IT tools. |

| 2 | Epstein et al. | 2018 | Making Sustainability Work | Framework | How to put ideas into practice. Guide for managers. Builds on previous works |

| 3 | Iyer | 2020 | Corporate Citizenship & Sustainability. Measuring intangible, physical and assets | Discourse | Measuring ethical asset usage is crucial for corporate to bring the abstraction into reality, acknowledge value when present and deconstruct what is valueless. |

| 4 | Starke | 2011 | Current trends & Policy Toolbox for clear solutions | Framework | Island Press-Center for Resource Economics |

| 5 | Bouma | 2018 | Captures emerging new business models and capabilities that firms need to develop to implement sustainability | Framework | Routledge |

| 6 | Ahmed | 2012 | It implies CSR is the base of Sustainability in all realms: doing the right thing | Discourse | Lambert Academy Publishing |

| 7 | Schaltegger | 2017 | Body of knowledge on the state of theory and practice: Conceptual framework for interaction of SEE in business environment | Integration | Taylor and Francis |

| 8 | Herriott | 2016 | Steps for doing a sustainable assessment. Compares available frameworks | Framework | Routledge |

| 9 | Hedstrom | 2018 | Scorecard: used by more than 50 companies to rate themselves | Measure | DeG Press |

| 10 | Hedstrom | 2017 | Summary of how business leaders should think about the risks and opportunities associated with sustainability. Based on Scorecard | Measure | CreateSpace Independent Publishing Platform |

| Institution-Conference | Title | Classification | Subject | Year | Notes |

|---|---|---|---|---|---|

| WEF, IBC, BoA, KPMG, E&Y, PwC | Measuring stakeholder capitalism | Project | Core metrics and recommendations into the 4P to be implemented in annual report and meet SDG. Outcome: expanded metrics | 2020 | Focus on ESG. Exclude economic |

| UN SDG | Sustainable Development Goals | Project | 17 SDG defined in a list of 169 SDG targets. Progress towards the targets agreed to be tracked by 232 unique indicators | 2015 | Based on countries |

| OECD | Better policies for 2030 | Project | An OECD Action Plan on the SDG | N/A | Based on Countries |

| The Economist Unit Intelligence | The Heinrich Sustainable Trade Index | Project | Measure capacity of 20 Economies (US as benchmark and 19 in Asia) to participate in trading system to support long term SEE goals | 2020 | Based on countries, focused on trades |

| ECSEE | European Conferences on Sustainability, Energy and the Environment | Annual | Provides prospects from Keynote Speakers from academic and professionals | 2013 | Last 6 conferences, no focus on measurement of S |

| BSR | A new blupring for business | Annual | Conversations to identify solutions to complex global challenges | 2012 | Last 8 conferences, no focus on measurement of S |

| Sustainable Development Conference | N/A | Annual | No Mission Statement from the website | 2013 | Last 6 conferences, no focus on measurement of S |

| International Conference on Sustainable Development | N/A | Annual | Forum for academia, government, civil society, UN agencies and private sector to shrae practical solutions to achieve SDG SB Transformation Roadmap: self assessment tool that provides a comprehensive tool for continous improvement in sustainability Through Technology, radical shift in business and consumer behaviour pave the way for more sustainable SEE practices | 2013 | Last 6 conferences, no focus on measurement of S |

| SB | Sustainable Brand | Ongoing | An OECD Action Plan on the SDG | 2006 | Specific on Brand Power/Image |

| Reuters Events | Broad thematic, including sustainability | Ad-Hoc | Measure capacity of 20 Economies (US as benchmark and 19 in Asia) to participate in trading system to support long term SEE goals | N/A | No focus on measurement of S |

| Authors | Year | Category | Subject | Journal | |

|---|---|---|---|---|---|

| 1 | Engida et al. | 2018 | Composite Index | Composite Index for European Food and Beverage | Journal of Cleaner Production |

| 2 | Goyal and Rahman | 2014 | Composite Index | Composite Index for Oil and Gas Industry | International Journal of Intercultural Information Mng |

| 3 | Jiang et al. | 2018 | Composite Index | CS Index for China Manufacturing | Journal of Cleaner Production |

| 4 | Kocmanova et al. | 2017 | Composite Index | Ranking of best and worst companies versus benchmark | Commerce of Engineering Decisions |

| 5 | Li et al. | 2012 | Composite Index | Composite Index for Manufacturing companies | Sustainable Development |

| 6 | Nikolau et al. | 2019 | Composite Index | Composite Index Strong sustainability | Sustainable Production and Consumption |

| 7 | Ngai et al. | 2014 | Single Index | Focus on social aspects. | Journal of Engineering Technology Management |

| 8 | Schirppe and Ribeiro | 2018 | Single Index | Focus on Environment | Journal of Cleaner Production |

| 9 | Journeault | 2016 | Scorecard | Scorecard which addresses the issues of the previous ones | Journal of Environmental Management |

| 10 | Medel-Gonzalez et al. | 2016 | Scorecard | Network of measures including scorecard, MCDM, AHP | Production |

| 11 | Aras et al. | 2018 | Performance Score | Content Analysis | Journal of Cleaner Production |

| 12 | Aras, Tezcan, Furtuna | 2017 | Performance Score | Content Analysis | Meditari Accounting Research |

| 13 | Molla et al. | 2019 | Performance Score | Content Analysis | Global Journal of Management and Business Research |

| 14 | Azadi et al. | 2015 | New Method | Numerical Example of DEA to measure CS | International Journal of Productivity and Quality Management |

| 15 | Bamford et al. | 2015 | New Method | Math formulation based on ER. Argues that AHP is not valid | Frontier in Engineering Management |

| 16 | Küçükbay and Sürücü | 2019 | New Method | Multimoora Sort. Assigns companies to success groups | CSR and Environmental Management |

| 17 | Lee and Sean | 2012 | New Method | Data Enveolope Analysis International | Journal of Production Economics |

| 18 | Vival et al. | 2019 | New Method | Hybrid MCDA model: PCA, MLR and PROMETHEE | Sustainability |

| 19 | Aktaş and Demirel | 2021 | New Method | MCDM to evaluate degree of achieving sustainability goals Environment, | Development and Sustainability |

| 20 | Bezerra et al. | 2021 | New Method | MCDM, PROMETEE II | Clean Technologies and Environmental Policy |

| 21 | Rao | 2021 | New Method | DEMATEL- ANP to construct a synthetic index | Research in transportation business and management |

| 22 | Ahi, Searcy, Jaber | 2018 | New Model | Strong sustainability. Challenges versus capacity model | Ecologic Economics |

| 23 | Docekalova et al. | 2016 | New Model | Complex performance Indicator, 17 indicators into a ratio | Ecological Indicators |

| 24 | Kocmanova et al. | 2016 | New Model | Sustainable Value Creation | Sustainability |

| 25 | Garcia et al. | 2016 | New Model | Integrated Environmental Evaluation model on TBL | Journal of Cleaner Production |

| 26 | Wright and Caudill | 2020 | New Model | Comprehensive Sustainability Target Model—CSTM | Environmental Impact Assessment Review |

| 27 | Sari et al. | 2020 | New Model | Corporate Sustainability Maturity Model—CSMM | International Journal of Productivity and Performance Management |

| 28 | Zenya and Nystad | 2016 | New Tool | E_SET with indicator from six global CS reporting, web based | Sustainability |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pazienza, M.; de Jong, M.; Schoenmaker, D. Why Corporate Sustainability Is Not Yet Measured. Sustainability 2023, 15, 6275. https://doi.org/10.3390/su15076275

Pazienza M, de Jong M, Schoenmaker D. Why Corporate Sustainability Is Not Yet Measured. Sustainability. 2023; 15(7):6275. https://doi.org/10.3390/su15076275

Chicago/Turabian StylePazienza, Mariapia, Martin de Jong, and Dirk Schoenmaker. 2023. "Why Corporate Sustainability Is Not Yet Measured" Sustainability 15, no. 7: 6275. https://doi.org/10.3390/su15076275

APA StylePazienza, M., de Jong, M., & Schoenmaker, D. (2023). Why Corporate Sustainability Is Not Yet Measured. Sustainability, 15(7), 6275. https://doi.org/10.3390/su15076275