Institutional Pressures and Environmental Management Accounting Adoption: Do Environmental Strategy Matter?

Abstract

:1. Introduction

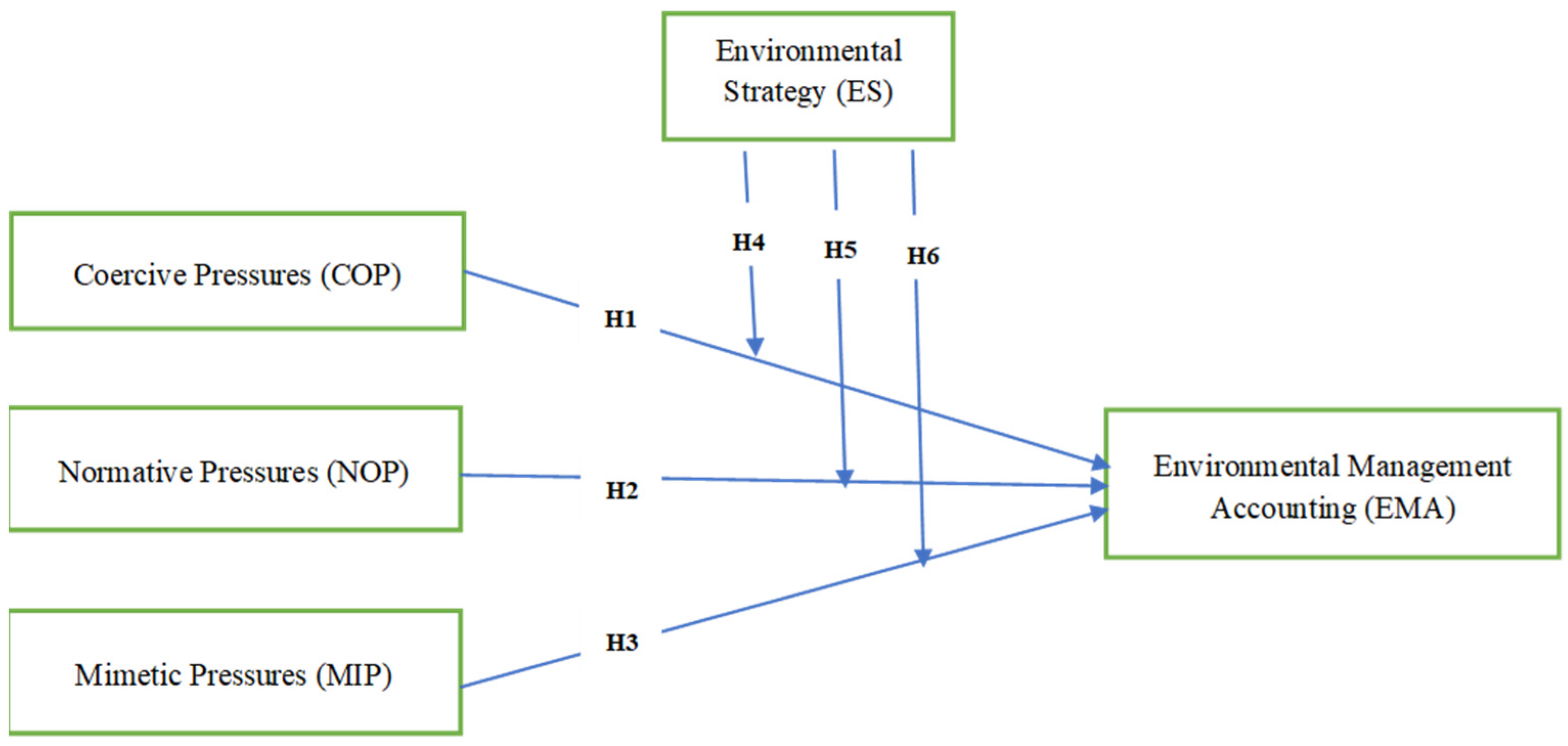

2. Theoretical Framework

3. Literature Review and Hypotheses Development

3.1. Institutional Pressures and EMA Adoption

3.1.1. Coercive Pressure and EMA Adoption

3.1.2. Normative Pressure and EMA Adoption

3.1.3. Mimetic Pressure and EMA Adoption

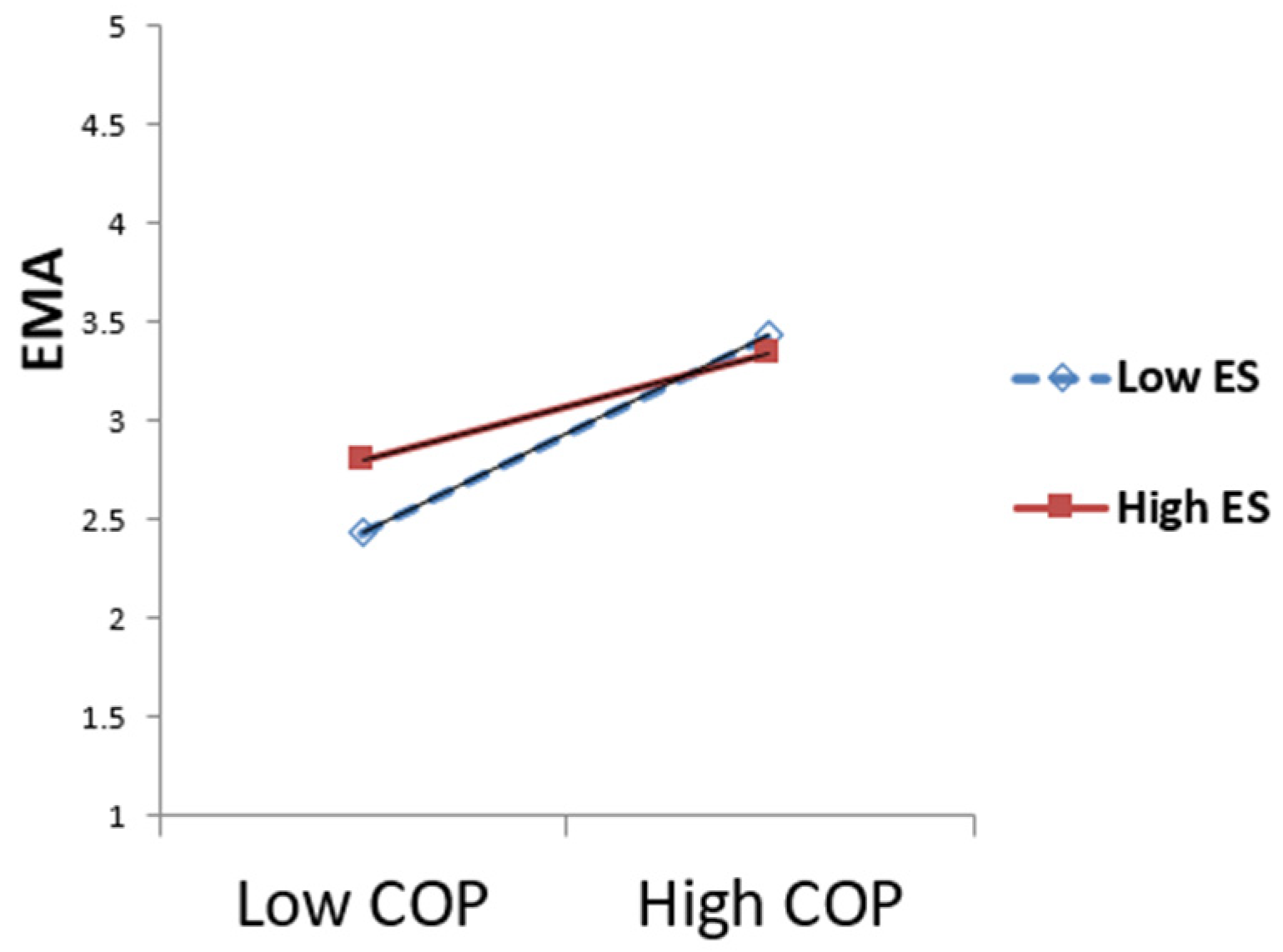

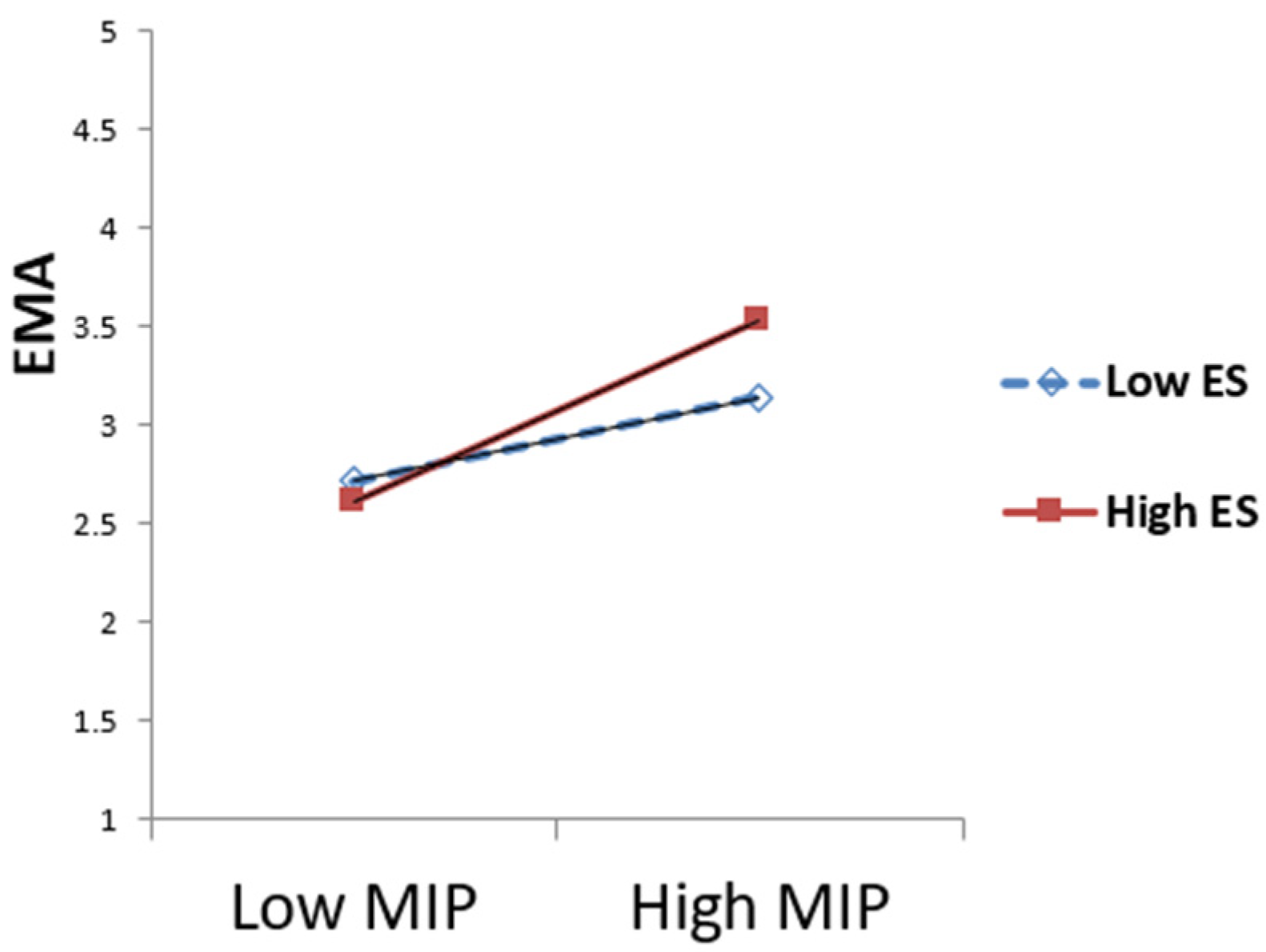

3.2. The Impact of Environmental Strategy: ES Moderating Role

4. Methodology

4.1. Data Collection and Survey Design

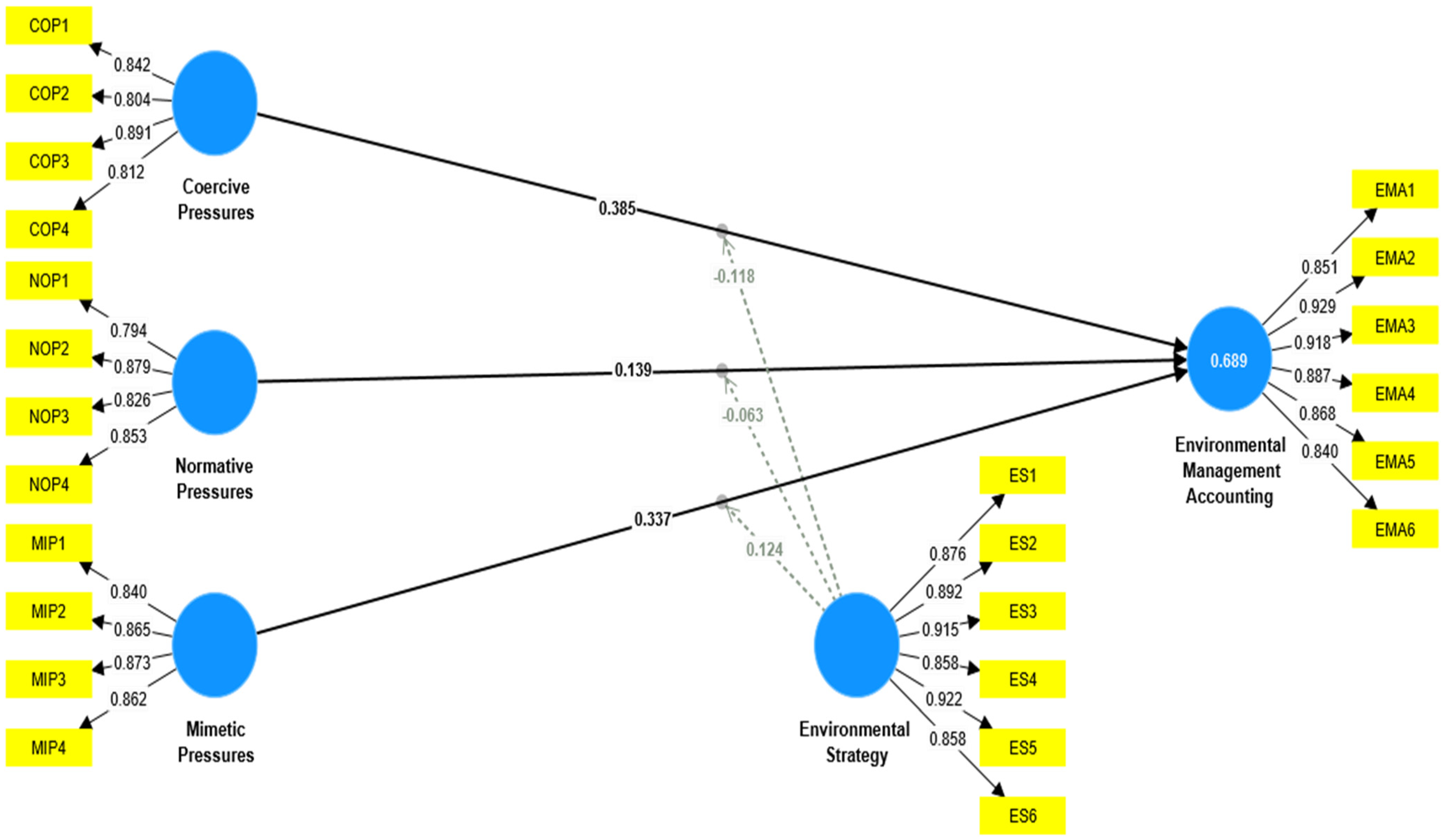

4.2. Measures and Scale Development

4.3. Data Analysis Methods

5. Results

5.1. Measurement Model Assessment

5.2. Hypotheses Testing

6. Discussion and Conclusions

7. Implications, Limitations, and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Cai, W.; Li, G. The drivers of eco-innovation and its impact on performance: Evidence from China. J. Clean. Prod. 2018, 176, 110–118. [Google Scholar] [CrossRef]

- Yu, W.; Chavez, R.; Feng, M.; Wong, C.Y.; Fynes, B. Green human resource management and environmental cooperation: An ability-motivation-opportunity and contingency perspective. Int. J. Prod. Econ. 2020, 219, 224–235. [Google Scholar] [CrossRef]

- Tang, M.; Walsh, G.; Lerner, D.; Fitza, M.A.; Li, Q. Green Innovation, Managerial Concern and Firm Performance: An Empirical Study. Bus. Strategy Environ. 2018, 27, 39–51. [Google Scholar] [CrossRef]

- Singh, S.K.; Giudice, M.D.; Chierici, R.; Graziano, D. Green innovation and environmental performance: The role of green transformational leadership and green human resource management. Technol. Forecast. Soc. Chang. 2020, 150, 119762. [Google Scholar] [CrossRef]

- Gunarathne, A.D.N.; Lee, K.-H.; Hitigala Kaluarachchilage, P.K. Institutional pressures, environmental management strategy, and organizational performance: The role of environmental management accounting. Bus. Strategy Environ. 2021, 30, 825–839. [Google Scholar] [CrossRef]

- Hanif, S.; Ahmed, A.; Younas, N. Examining the impact of Environmental Management Accounting practices and Green Transformational Leadership on Corporate Environmental Performance: The mediating role of Green Process Innovation. J. Clean. Prod. 2023, 414, 137584. [Google Scholar] [CrossRef]

- Che Ku Kassim, C.K.H.; Adnan, N.L.; Ali, R. Institutional pressures influencing environmental management accounting adoption by Malaysian local governments. J. Account. Organ. Chang. 2022, 18, 440–460. [Google Scholar] [CrossRef]

- Cheng, M.M.; Perego, P.; Soderstrom, N.S. Sustainability and Management Accounting Research. J. Manag. Account. Res. 2023, 35, 1–11. [Google Scholar] [CrossRef]

- Kang, A.; Ren, L.; Hua, C.; Song, H.; Dong, M.; Fang, Z.; Zhu, M. Environmental management strategy in response to COVID-19 in China: Based on text mining of government open information. Sci. Total Environ. 2021, 769, 145158. [Google Scholar] [CrossRef]

- Begum, S.; Ashfaq, M.; Xia, E.; Awan, U. Does green transformational leadership lead to green innovation? The role of green thinking and creative process engagement. Bus. Strategy Environ. 2022, 31, 580–597. [Google Scholar] [CrossRef]

- Channa, N.A.; Hussain, T.; Casali, G.L.; Dakhan, S.A.; Aisha, R. Promoting environmental performance through corporate social responsibility in controversial industry sectors. Environ. Sci. Pollut. Res. 2021, 28, 23273–23286. [Google Scholar] [CrossRef] [PubMed]

- Metwally, A.B.M.; Diab, A.; Mohamed, M.K. Telework operationalization through internal CSR, governmentality and accountability during the COVID-19: Evidence from a developing country. Int. J. Organ. Anal. 2022, 30, 1441–1464. [Google Scholar] [CrossRef]

- Diab, A.; Metwally, A.B.M. Institutional complexity and CSR practices: Evidence from a developing country. J. Account. Emerg. Econ. 2020, 10, 655–680. [Google Scholar] [CrossRef]

- Abdelfattah, T.; Elfeky, M. Earnings management, corporate social responsibility and governance structure: Further evidence from Egypt. Int. J. Account. Audit. Perform. Eval. 2021, 17, 173–201. [Google Scholar] [CrossRef]

- Sial, M.S.; Chunmei, Z.; Khan, T.; Nguyen, V.K. Corporate social responsibility, firm performance and the moderating effect of earnings management in Chinese firms. Asia-Pac. J. Bus. Adm. 2018, 10, 184–199. [Google Scholar] [CrossRef]

- Abdelmotaleb, M.; Mohamed Metwally, A.B.E.; Saha, S.K. Exploring the impact of being perceived as a socially responsible organization on employee creativity. Manag. Decis. 2018, 56, 2325–2340. [Google Scholar] [CrossRef]

- Rodrigue, M.; Magnan, M.; Boulianne, E. Stakeholders’ influence on environmental strategy and performance indicators: A managerial perspective. Manag. Account. Res. 2013, 24, 301–316. [Google Scholar] [CrossRef]

- Ali, M.A.S.; Aly, S.A.S.; Abdelazim, S.I.; Metwally, A.B.M. Cash holdings, board governance characteristics, and Egyptian firms’ performance. Cogent Bus. Manag. 2024, 11, 2302205. [Google Scholar] [CrossRef]

- Perego, P.; Hartmann, F. Aligning Performance Measurement Systems with Strategy: The Case of Environmental Strategy. Abacus 2009, 45, 397–428. [Google Scholar] [CrossRef]

- Gunarathne, N.; Lee, K.-H. Environmental Management Accounting (EMA) for environmental management and organizational change. J. Account. Organ. Chang. 2015, 11, 362–383. [Google Scholar] [CrossRef]

- Lisi, I.E. Translating environmental motivations into performance: The role of environmental performance measurement systems. Manag. Account. Res. 2015, 29, 27–44. [Google Scholar] [CrossRef]

- Metwally, A.B.M.; Diab, A. Risk-based management control resistance in a context of institutional complexity: Evidence from an emerging economy. J. Account. Organ. Chang. 2021, 17, 416–435. [Google Scholar] [CrossRef]

- Metwally, A. The Materiality of Corporate Governance Report Disclosures: Investigating the Perceptions of External Auditors working in Egypt. Sci. J. Financ. Commer. Stud. Res. 2022, 3, 547–582. [Google Scholar]

- Solovida, G.T.; Latan, H. Linking environmental strategy to environmental performance. Sustain. Account. Manag. Policy J. 2017, 8, 595–619. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Othman, M.S.H.; Saeidi, P.; Saeidi, S.P. The moderating role of environmental management accounting between environmental innovation and firm financial performance. Int. J. Bus. Perform. Manag. 2018, 19, 326–348. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R. Business Cases and Corporate Engagement with Sustainability: Differentiating Ethical Motivations. J. Bus. Ethics 2018, 147, 241–259. [Google Scholar] [CrossRef]

- Burritt, R.L. Environmental reporting in Australia: Current practices and issues for the future. Bus. Strategy Environ. 2002, 11, 391–406. [Google Scholar] [CrossRef]

- Qian, W.; Burritt, R.; Chen, J. The potential for environmental management accounting development in China. J. Account. Organ. Chang. 2015, 11, 406–428. [Google Scholar] [CrossRef]

- Burritt, R.L.; Herzig, C.; Tadeo, B.D. Environmental management accounting for cleaner production: The case of a Philippine rice mill. J. Clean. Prod. 2009, 17, 431–439. [Google Scholar] [CrossRef]

- Doorasamy, M.; Garbharran, H. The role of environmental management accounting as a tool to calculate environmental costs and identify their impact on a company’s environmental performance. Asian J. Bus. Manag. Decis. 2015, 3, 8–30. [Google Scholar]

- Ali, W.; Frynas, J.G.; Mahmood, Z. Determinants of Corporate Social Responsibility (CSR) Disclosure in Developed and Developing Countries: A Literature Review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- Mahmood, Z.; Kouser, R.; Ali, W.; Ahmad, Z.; Salman, T. Does Corporate Governance Affect Sustainability Disclosure? A Mixed Methods Study. Sustainability 2018, 10, 207. [Google Scholar] [CrossRef]

- Latif, B.; Mahmood, Z.; Tze San, O.; Mohd Said, R.; Bakhsh, A. Coercive, Normative and Mimetic Pressures as Drivers of Environmental Management Accounting Adoption. Sustainability 2020, 12, 4506. [Google Scholar] [CrossRef]

- Mahmood, Z.; Ahmad, Z.J. Quest for alternative sociological perspectives on corporate social and environmental reporting. J. Account. Financ. Emerg. Econ. 2015, 1, 135–153. [Google Scholar] [CrossRef]

- Wang, S.; Wang, H.; Wang, J. Exploring the effects of institutional pressures on the implementation of environmental management accounting: Do top management support and perceived benefit work? Bus. Strategy Environ. 2019, 28, 233–243. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Asiaei, K.; Bontis, N.; Alizadeh, R.; Yaghoubi, M. Green intellectual capital and environmental management accounting: Natural resource orchestration in favor of environmental performance. Bus. Strategy Environ. 2022, 31, 76–93. [Google Scholar] [CrossRef]

- Freudenreich, B.; Lüdeke-Freund, F.; Schaltegger, S. A Stakeholder Theory Perspective on Business Models: Value Creation for Sustainability. J. Bus. Ethics 2020, 166, 3–18. [Google Scholar] [CrossRef]

- Peng, B.; Chen, S.; Elahi, E.; Wan, A. Can corporate environmental responsibility improve environmental performance? An inter-temporal analysis of Chinese chemical companies. Environ. Sci. Pollut. Res. 2021, 28, 12190–12201. [Google Scholar] [CrossRef]

- Bouma, J.J.; Kamp-Roelands, N. Stakeholders expectations of an environmental management system: Some exploratory research. Eur. Account. Rev. 2000, 9, 131–144. [Google Scholar] [CrossRef]

- Chen, Y.-C.; Hung, M.; Wang, Y. The effect of mandatory CSR disclosure on firm profitability and social externalities: Evidence from China. J. Account. Econ. 2018, 65, 169–190. [Google Scholar] [CrossRef]

- Bhandari, A.; Javakhadze, D. Corporate social responsibility and capital allocation efficiency. J. Corp. Financ. 2017, 43, 354–377. [Google Scholar] [CrossRef]

- McCarthy, S.; Oliver, B.; Song, S. Corporate social responsibility and CEO confidence. J. Bank. Financ. 2017, 75, 280–291. [Google Scholar] [CrossRef]

- Abdullah, M.; Zailani, S.; Iranmanesh, M.; Jayaraman, K. Barriers to green innovation initiatives among manufacturers: The Malaysian case. Rev. Manag. Sci. 2016, 10, 683–709. [Google Scholar] [CrossRef]

- Zailani, S.; Govindan, K.; Iranmanesh, M.; Shaharudin, M.R.; Sia Chong, Y. Green innovation adoption in automotive supply chain: The Malaysian case. J. Clean. Prod. 2015, 108, 1115–1122. [Google Scholar] [CrossRef]

- Caldera, H.T.S.; Desha, C.; Dawes, L. Exploring the role of lean thinking in sustainable business practice: A systematic literature review. J. Clean. Prod. 2017, 167, 1546–1565. [Google Scholar] [CrossRef]

- Mallak, S.K.; Ishak, M.B.; Mohamed, A.F.; Iranmanesh, M. Toward sustainable solid waste minimization by manufacturing firms in Malaysia: Strengths and weaknesses. Environ. Monit. Assess. 2018, 190, 575. [Google Scholar] [CrossRef] [PubMed]

- Zailani, S.; Iranmanesh, M.; Sean Hyun, S.; Ali, M.H. Applying the Theory of Consumption Values to Explain Drivers’ Willingness to Pay for Biofuels. Sustainability 2019, 11, 668. [Google Scholar] [CrossRef]

- Hofer, C.; Eroglu, C.; Rossiter Hofer, A. The effect of lean production on financial performance: The mediating role of inventory leanness. Int. J. Prod. Econ. 2012, 138, 242–253. [Google Scholar] [CrossRef]

- Jalaludin, D.; Sulaiman, M.; Nazli Nik Ahmad, N. Understanding environmental management accounting (EMA) adoption: A new institutional sociology perspective. Soc. Responsib. J. 2011, 7, 540–557. [Google Scholar] [CrossRef]

- Diab, A.A.A.; Mohamed Metwally, A.B. Institutional ambidexterity and management control. Qual. Res. Account. Manag. 2019, 16, 373–402. [Google Scholar] [CrossRef]

- Burns, J.; Scapens, R.W. Conceptualizing management accounting change: An institutional framework. Manag. Account. Res. 2000, 11, 3–25. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized organizations: Formal structure as myth and ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef]

- Ball, A.; Craig, R. Using neo-institutionalism to advance social and environmental accounting. Crit. Perspect. Account. 2010, 21, 283–293. [Google Scholar] [CrossRef]

- Ferdous, M.I.; Adams, C.A.; Boyce, G. Institutional drivers of environmental management accounting adoption in public sector water organisations. Account. Audit. Account. J. 2019, 32, 984–1012. [Google Scholar] [CrossRef]

- Metwally, A.B.M.; Diab, A. An institutional analysis of the risk management process during the COVID-19 pandemic: Evidence from an emerging market. J. Account. Organ. Chang. 2023, 19, 40–62. [Google Scholar] [CrossRef]

- Colwell, S.R.; Joshi, A.W. Corporate Ecological Responsiveness: Antecedent Effects of Institutional Pressure and Top Management Commitment and Their Impact on Organizational Performance. Bus. Strategy Environ. 2013, 22, 73–91. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. Extrinsic and Intrinsic Drivers of Corporate Social Performance: Evidence from Foreign and Domestic Firms in Mexico. J. Manag. Stud. 2010, 47, 1–26. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Amoako, G.K.; Adam, A.M.; Arthur, C.L.; Tackie, G. Institutional isomorphism, environmental management accounting and environmental accountability: A review. Environ. Dev. Sustain. 2021, 23, 11201–11216. [Google Scholar] [CrossRef]

- Heugens, P.P.M.A.R.; Lander, M.W. Structure! Agency! (And Other Quarrels): A Meta-Analysis of Institutional Theories of Organization. Acad. Manag. J. 2009, 52, 61–85. [Google Scholar] [CrossRef]

- Teo, H.H.; Wei, K.K.; Benbasat, I. Predicting Intention to Adopt Interorganizational Linkages: An Institutional Perspective. MIS Q. 2003, 27, 19–49. [Google Scholar] [CrossRef]

- Brammer, S.; Hoejmose, S.; Marchant, K. Environmental Management in SMEs in the UK: Practices, Pressures and Perceived Benefits. Bus. Strategy Environ. 2012, 21, 423–434. [Google Scholar] [CrossRef]

- Liang, H.; Saraf, N.; Hu, Q.; Xue, Y. Assimilation of Enterprise Systems: The Effect of Institutional Pressures and the Mediating Role of Top Management. MIS Q. 2007, 31, 59–87. [Google Scholar] [CrossRef]

- Chaudhry, N.I.; Amir, M. From institutional pressure to the sustainable development of firm: Role of environmental management accounting implementation and environmental proactivity. Bus. Strategy Environ. 2020, 29, 3542–3554. [Google Scholar] [CrossRef]

- Hu, R.; Shahzad, F.; Abbas, A.; Liu, X. Decoupling the influence of eco-sustainability motivations in the adoption of the green industrial IoT and the impact of advanced manufacturing technologies. J. Clean. Prod. 2022, 339, 130708. [Google Scholar] [CrossRef]

- Shahzad, F.; Du, J.; Khan, I.; Wang, J. Decoupling institutional pressure on green supply chain management efforts to boost organizational performance: Moderating impact of big data analytics capabilities. Front. Environ. Sci. 2022, 10, 911392. [Google Scholar] [CrossRef]

- Berrone, P.; Fosfuri, A.; Gelabert, L.; Gomez-Mejia, L.R. Necessity as the mother of ‘green’ inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 2013, 34, 891–909. [Google Scholar] [CrossRef]

- Roxas, B.; Coetzer, A. Institutional Environment, Managerial Attitudes and Environmental Sustainability Orientation of Small Firms. J. Bus. Ethics 2012, 111, 461–476. [Google Scholar] [CrossRef]

- Latan, H.; Chiappetta Jabbour, C.J.; Lopes de Sousa Jabbour, A.B.; Wamba, S.F.; Shahbaz, M. Effects of environmental strategy, environmental uncertainty and top management’s commitment on corporate environmental performance: The role of environmental management accounting. J. Clean. Prod. 2018, 180, 297–306. [Google Scholar] [CrossRef]

- Christ, K.L.; Burritt, R.L. Environmental management accounting: The significance of contingent variables for adoption. J. Clean. Prod. 2013, 41, 163–173. [Google Scholar] [CrossRef]

- Zhang, Y.; Wei, Y.; Zhou, G. Promoting firms’ energy-saving behavior: The role of institutional pressures, top management support and financial slack. Energy Policy 2018, 115, 230–238. [Google Scholar] [CrossRef]

- Beckert, J. Institutional Isomorphism Revisited: Convergence and Divergence in Institutional Change. Sociol. Theory 2010, 28, 150–166. [Google Scholar] [CrossRef]

- Joseph, C.; Taplin, R. Local government website sustainability reporting: A mimicry perspective. Soc. Responsib. J. 2012, 8, 363–372. [Google Scholar] [CrossRef]

- Masocha, R.; Fatoki, O. The Role of Mimicry Isomorphism in Sustainable Development Operationalisation by SMEs in South Africa. Sustainability 2018, 10, 1264. [Google Scholar] [CrossRef]

- Codagnone, C.; Misuraca, G.; Savoldelli, A.; Lupiañez-Villanueva, F. Institutional isomorphism, policy networks, and the analytical depreciation of measurement indicators: The case of the EU e-government benchmarking. Telecommun. Policy 2015, 39, 305–319. [Google Scholar] [CrossRef]

- Yang, M.; Hyland, M. Re-examining mimetic isomorphism. Manag. Decis. 2012, 50, 1076–1095. [Google Scholar] [CrossRef]

- Wu, T.; Daniel, E.M.; Hinton, M.; Quintas, P. Isomorphic mechanisms in manufacturing supply chains: A comparison of indigenous Chinese firms and foreign-owned MNCs. Supply Chain Manag. Int. J. 2013, 18, 161–177. [Google Scholar] [CrossRef]

- Kauppi, K. Extending the use of institutional theory in operations and supply chain management research. Int. J. Oper. Prod. Manag. 2013, 33, 1318–1345. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why Companies Go Green: A Model of Ecological Responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar] [CrossRef]

- Journeault, M.; De Ronge, Y.; Henri, J.-F. Levers of eco-control and competitive environmental strategy. Br. Account. Rev. 2016, 48, 316–340. [Google Scholar] [CrossRef]

- Ormazabal, M.; Rich, E.; Sarriegi, J.M.; Viles, E. Environmental Management Evolution Framework: Maturity Stages and Causal Loops. Organ. Environ. 2016, 30, 27–50. [Google Scholar] [CrossRef]

- Ormazabal, M.; Sarriegi, J.M. Environmental Management Evolution: Empirical Evidence from Spain and Italy. Bus. Strategy Environ. 2014, 23, 73–88. [Google Scholar] [CrossRef]

- González-Benito, J.; González-Benito, Ó. A review of determinant factors of environmental proactivity. Bus. Strategy Environ. 2006, 15, 87–102. [Google Scholar] [CrossRef]

- Gunarathne, N.; Lee, K.-H. Institutional pressures and corporate environmental management maturity. Manag. Environ. Qual. Int. J. 2019, 30, 157–175. [Google Scholar] [CrossRef]

- Mårtensson, K.; Westerberg, K. Corporate Environmental Strategies Towards Sustainable Development. Bus. Strategy Environ. 2016, 25, 1–9. [Google Scholar] [CrossRef]

- Wijethilake, C. Proactive sustainability strategy and corporate sustainability performance: The mediating effect of sustainability control systems. J. Environ. Manag. 2017, 196, 569–582. [Google Scholar] [CrossRef] [PubMed]

- Christ, K.L. Water management accounting and the wine supply chain: Empirical evidence from Australia. Br. Account. Rev. 2014, 46, 379–396. [Google Scholar] [CrossRef]

- Qian, W.; Burritt, R.; Monroe, G. Environmental management accounting in local government. Account. Audit. Account. J. 2011, 24, 93–128. [Google Scholar] [CrossRef]

- Bui, B.; de Villiers, C. Business strategies and management accounting in response to climate change risk exposure and regulatory uncertainty. Br. Account. Rev. 2017, 49, 4–24. [Google Scholar] [CrossRef]

- Qian, W.; Burritt, R.L.; Monroe, G.S. Environmental management accounting in local government: Functional and institutional imperatives. Financ. Account. Manag. 2018, 34, 148–165. [Google Scholar] [CrossRef]

- Mokhtar, N.; Jusoh, R.; Zulkifli, N. Corporate characteristics and environmental management accounting (EMA) implementation: Evidence from Malaysian public listed companies (PLCs). J. Clean. Prod. 2016, 136, 111–122. [Google Scholar] [CrossRef]

- Hart, S.L. A Natural-Resource-Based View of the Firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Daddi, T.; Testa, F.; Frey, M.; Iraldo, F. Exploring the link between institutional pressures and environmental management systems effectiveness: An empirical study. J. Environ. Manag. 2016, 183, 647–656. [Google Scholar] [CrossRef] [PubMed]

- Ferreira, A.; Moulang, C.; Hendro, B. Environmental management accounting and innovation: An exploratory analysis. Account. Audit. Account. J. 2010, 23, 920–948. [Google Scholar] [CrossRef]

- Phan, T.N.; Baird, K.; Su, S. The use and effectiveness of environmental management accounting. Australas. J. Environ. Manag. 2017, 24, 355–374. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Hair, J., Jr.; Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: Thousand Oaks, CA, USA, 2021. [Google Scholar]

- Fornell, C.; Larcker, D.F. Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Freq. | % | ||

|---|---|---|---|

| Gender | Male | 355 | 72.3 |

| Female | 136 | 27.7 | |

| Experience (years) | 1–5 years | 16 | 3.2 |

| 6–10 years | 131 | 26.7 | |

| 11–15 years | 151 | 30.7 | |

| More than 15 years | 193 | 39.4 | |

| Educational Level | Bachelor’s degree | 192 | 39.1 |

| Post-graduate Degree | 299 | 60.9 | |

| Industry Type | Industrial Goods, Services, and Automobiles | 84 | 17 |

| Basic Resources | 73 | 14.9 | |

| Healthcare and Pharmaceuticals | 60 | 12.3 | |

| Food, Beverages, and Tobacco | 135 | 27.5 | |

| Building Materials | 103 | 21 | |

| Textile and Durables | 36 | 7.3 | |

| Total | 491 | 100 | |

| Scale Variables and Items | Outer Loading | Alpha | CR | AVE |

|---|---|---|---|---|

| Coercive Pressures (COP) | 0.860 | 0.873 | 0.702 | |

| Our company endeavors to mitigate the threat from environmental regulations by incorporating environmental management accounting. | 0.842 | |||

| Our company considers environmental regulations to be crucial in driving the implementation of environmental management accounting. | 0.804 | |||

| Our company must adhere to the stringent environmental regulations established by the local government. | 0.891 | |||

| Companies that break environmental standard and regulations face a number of penalties. | 0.812 | |||

| Normative Pressures (NOP) | 0.859 | 0.862 | 0.703 | |

| Our company has been prompted to adopt environmental management accounting due to the growing environmental awareness among consumers. | 0.794 | |||

| For our company to be part of this industry, it is fundamentally necessary to provide environmental information and being environmentally responsible. | 0.879 | |||

| The nongovernmental organizations in our community expect that environmental management accounting be used by all companies in the industry. | 0.826 | |||

| Without implementing environmental management accounting, stakeholders might not support our company. | 0.853 | |||

| Mimetic Pressures (MIP) | 0.883 | 0.886 | 0.740 | |

| Leading firms in our industry serve as role models for the application of environmental management accounting. | 0.840 | |||

| It is common knowledge that the top firms in our industry successfully implementation of environmental management accounting. | 0.865 | |||

| The top firms in our industry intent to use environmental management accounting to reduce their environmental effects. | 0.873 | |||

| Implementing environmental management accounting has given the top firms in our industry a competitive edge. | 0.862 | |||

| Environmental Strategy (ES) | 0.946 | 0.948 | 0.787 | |

| Our company’s environmental strategic plan promotes sustainable resource management and creates a long-term commitment to the environment. | 0.876 | |||

| Our company’s environmental strategic plan works to reduce the environmental impacts of products and services. | 0.892 | |||

| Our company’s environmental strategic plan employs environmental management systems. | 0.915 | |||

| Our company’s environmental strategic plan sets performance indicators to measure the level of pollution and reduce emissions (air, water, energy, waste). | 0.858 | |||

| Our company’s environmental strategic plan seeks to invest in research and development activities related to environmental protection. | 0.922 | |||

| Our company’s environmental strategic plan is working towards obtaining ISO certificates and environmental awards. | 0.858 | |||

| Environmental Management Accounting (EMA) | 0.943 | 0.945 | 0.779 | |

| The accounting system of our firm diligently captures and records all physical inputs and outputs, encompassing such as energy, water, materials, wastes, and emissions. | 0.851 | |||

| The accounting system utilized by our firm is capable of conducting product inventory analyses, product improvement analyses, and assessments of product environmental impacts. | 0.929 | |||

| Our firm employs environmental performance targets for monitoring and managing physical inputs and outputs. | 0.918 | |||

| Environmentally linked costs and liabilities can be recognized, estimated, and categorized by our company’s accounting system. | 0.887 | |||

| The accounting system within our firm has the capability to establish and utilize Cost accounts relating to the environment. | 0.868 | |||

| The accounting system employed by our firm has the capability to allocate environmental-related costs to products. | 0.840 | |||

| Average variance extracted (AVE) and composite reliability (CR). | ||||

| COP | EMA | ES | MIP | NOP | |

|---|---|---|---|---|---|

| COP-1 | 0.842 | 0.613 | 0.422 | 0.459 | 0.534 |

| COP-2 | 0.804 | 0.498 | 0.416 | 0.557 | 0.398 |

| COP-3 | 0.891 | 0.600 | 0.406 | 0.542 | 0.589 |

| COP-4 | 0.812 | 0.646 | 0.426 | 0.548 | 0.634 |

| EMA-1 | 0.601 | 0.851 | 0.420 | 0.592 | 0.571 |

| EMA-2 | 0.633 | 0.929 | 0.464 | 0.596 | 0.631 |

| EMA-3 | 0.595 | 0.918 | 0.418 | 0.582 | 0.608 |

| EMA-4 | 0.554 | 0.887 | 0.446 | 0.507 | 0.571 |

| EMA-5 | 0.569 | 0.868 | 0.398 | 0.545 | 0.569 |

| EMA-6 | 0.565 | 0.840 | 0.430 | 0.502 | 0.514 |

| ES-1 | 0.437 | 0.469 | 0.876 | 0.386 | 0.393 |

| ES-2 | 0.427 | 0.464 | 0.892 | 0.401 | 0.405 |

| ES-3 | 0.399 | 0.412 | 0.915 | 0.465 | 0.358 |

| ES-4 | 0.457 | 0.420 | 0.858 | 0.395 | 0.359 |

| ES-5 | 0.475 | 0.422 | 0.922 | 0.502 | 0.392 |

| ES-6 | 0.454 | 0.391 | 0.858 | 0.422 | 0.316 |

| MIP-1 | 0.639 | 0.622 | 0.359 | 0.840 | 0.487 |

| MIP-2 | 0.519 | 0.574 | 0.392 | 0.865 | 0.426 |

| MIP-3 | 0.597 | 0.624 | 0.462 | 0.873 | 0.550 |

| MIP-4 | 0.542 | 0.613 | 0.436 | 0.862 | 0.581 |

| NOP-1 | 0.437 | 0.535 | 0.301 | 0.451 | 0.794 |

| NOP-2 | 0.603 | 0.591 | 0.389 | 0.556 | 0.879 |

| NOP-3 | 0.594 | 0.518 | 0.324 | 0.460 | 0.826 |

| NOP-4 | 0.568 | 0.557 | 0.388 | 0.534 | 0.853 |

| Fornell-Larcker | HTMT | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| COP | ES | EMA | MIP | NOP | COP | ES | EMA | MIP | NOP | |

| 1. COP | 0.838 | |||||||||

| 2. ES | 0.498 | 0.887 | 0.553 | |||||||

| 3. EMA | 0.778 | 0.487 | 0.883 | 0.845 | 0.513 | |||||

| 4. MIP | 0.785 | 0.481 | 0.742 | 0.860 | 0.831 | 0.526 | 0.809 | |||

| 5. NOP | 0.657 | 0.419 | 0.657 | 0.559 | 0.839 | 0.747 | 0.462 | 0.728 | 0.680 | |

| Hypotheses | Beta (β) | T-Statistics | Results | |

|---|---|---|---|---|

| H-1 | COP → EMA | 0.385 *** | 6.366 | Accepted |

| H-2 | NOP → EMA | 0.139 *** | 3.386 | Accepted |

| H-3 | MIP → EMA | 0.337 *** | 5.049 | Accepted |

| ES → EMA | 0.069 * | 2.118 | Accepted | |

| H-4 | COP × ES → EMA | −0.118 * | 2.124 | Accepted |

| H-5 | NOP × ES → EMA | −0.063 | 1.015 | Not Accepted |

| H-6 | MIP × ES → EMA | 0.124 * | 2.233 | Accepted |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alnaim, M.; Metwally, A.B.M. Institutional Pressures and Environmental Management Accounting Adoption: Do Environmental Strategy Matter? Sustainability 2024, 16, 3020. https://doi.org/10.3390/su16073020

Alnaim M, Metwally ABM. Institutional Pressures and Environmental Management Accounting Adoption: Do Environmental Strategy Matter? Sustainability. 2024; 16(7):3020. https://doi.org/10.3390/su16073020

Chicago/Turabian StyleAlnaim, Musaab, and Abdelmoneim Bahyeldin Mohamed Metwally. 2024. "Institutional Pressures and Environmental Management Accounting Adoption: Do Environmental Strategy Matter?" Sustainability 16, no. 7: 3020. https://doi.org/10.3390/su16073020

APA StyleAlnaim, M., & Metwally, A. B. M. (2024). Institutional Pressures and Environmental Management Accounting Adoption: Do Environmental Strategy Matter? Sustainability, 16(7), 3020. https://doi.org/10.3390/su16073020