1. Introduction

States are increasingly interested in encouraging sustainable energy generation through various policies and financial support mechanisms. One of the most popular policies in the United States for promoting renewables is the renewable portfolio standard (RPS). As of April 2010, 29 states and the District of Columbia have RPSs, while six states have non-binding renewable goals [

1]. An RPS requires that electricity providers procure a portion of their electricity from renewable sources. The provider is typically obligated to show compliance with the standard via the purchase of renewable energy certificates/credits (RECs) that correspond to a unit (e.g., megawatt-hour) of renewable electricity. The provider can purchase these certificates at the same time that it purchases the renewable power or it can purchase the RECs independently.

In states with regulated electricity markets and an RPS, utilities typically purchase RECs bundled with electricity under long-term contracts [

2]. In electricity markets where an RPS has been established in tandem with retail electricity competition, however, RECs are often procured under short-term contracts or on spot markets. Many of the New England and Mid-Atlantic states, along with Texas have unbundled REC markets. For renewable energy developers and investors, one challenge to doing business in a short-term or spot REC market is REC price uncertainty over the project life. REC price volatility leads to higher investment risk, higher capital costs [

3], and can serve as a significant barrier to market growth. Spot market price risk has led a number of states to explore mechanisms to stabilize volatile REC markets. Examples of these mechanisms include long-term contracting with administratively set prices or through competition, price floors, utility-sponsored loan programs, and partial upfront payments [

4].

Another distinct trend in RPS policy design in the United States is the emergence of support for specific technologies. While early RPS designs tended not to favor one technology over the other, many states are now establishing specific targets, or carve-outs, for priority technologies such as solar photovoltaics (PV). Of the US jurisdictions with mandatory RPS policies, 14 states and the District of Columbia have established carve-outs for solar energy and many of these utilize solar renewable energy credits (SRECs) as the primary compliance mechanism [

5]. Massachusetts established an SREC market in 2010 and has taken a unique approach to market design and securitization. This article reviews the modeling process that Massachusetts decision makers employed to inform their SREC policy design decisions.

2. Massachusetts Solar Energy Market

2.1. Solar Energy in Massachusetts

There are more than 2,000 PV installations in the Commonwealth comprising over 22 MW of solar capacity. The primary driver for these installations has been the Commonwealth Solar rebate program. Building on Governor Deval Patrick’s commitment in 2007 to install 250 MW of solar PV by 2017, the Commonwealth Solar program was established as a successor to earlier state PV incentives [

6] to jumpstart market development. Commonwealth Solar provided rebates to PV projects in order to reduce the upfront cost of solar installations. The program launched in 2007 with a $68 million budget and a goal of reaching 27 MW of solar installations within three years. All program funds were obligated ahead of schedule by the end of 2009. As the Commonwealth Solar rebate program was ending, Massachusetts policymakers explored transitioning from rebates to a performance based program that would provide incentives for solar energy generation. The opportunity for this transition was created by legislation which modified the state RPS (see 2.3 below).

2.2. Massachusetts RPS

Massachusetts has one of the oldest RPS programs in the United States. The RPS compliance schedule began in 2003 with a requirement that renewable energy sources account for 1% of state electricity sales, increasing by 0.5% percent annually until 2009. The Green Communities Act of 2008 then set an RPS target of 15% by 2020, with scheduled increases of 1% annually starting in 2009. Although RPS supply lagged behind demand for the first several years of the program, Massachusetts has met its growing RPS standard each year since 2007 with a sufficient supply of new renewable energy generation. Generation from landfill gas, biomass and wind are the dominant contributors, with units scattered throughout New England and adjacent electric grid control areas, including New York and provinces in eastern Canada [

7].

2.3. SREC Market Proposal

The Green Communities Act of 2008 also provided the opportunity to develop a specific solar target under the existing state RPS. The legislation required the Massachusetts Department of Energy Resources (DOER) to develop a carve-out for renewable energy generators smaller than 2 MW. In developing regulations, the DOER determined that the carve-out would focus exclusively on photovoltaic systems. The DOER also determined the amount of solar that would be targeted (400 MW), as well as the structure of the carve-out, through iterative rounds of analysis supported by stakeholder workshops and public comment. SREC price volatility was a key concern of both policy makers and solar stakeholders. Given the price risk associated with a standard REC market, the DOER proposed an SREC market design that would provide greater revenue certainty than typical REC-based RPS programs.

In early 2010, the DOER promulgated final rules for the solar RPS carve-out. The program requires obligated load serving entities (LSEs) [

8] to purchase a small portion of their yearly electricity load from qualified in-state solar PV generators. This PV load requirement will increase on a yearly basis until 400 MW of PV are built in the state. If LSEs are unable to comply with the requirements of the carve-out through SREC purchases, they may pay an alternative compliance payment (ACP) of $600 per MWh. As in other RPS markets, it is expected that the ACP price will serve as a price ceiling for the Massachusetts SREC market. The DOER expects that most solar generators will either contract with LSEs to sell their SRECs or will be able to sell their generation certificates on the spot market. However, a unique securitization feature of the Massachusetts solar-carve-out is an auction into which generators can place SRECs if they are unable to sell them to LSEs during the compliance year. Each solar installation, as part of its RPS solar carve-out qualification by the DOER, will be given a set term of years during which it will have the right (but not the requirement) to deposit SRECs into a DOER-managed auction account. The DOER will attempt to auction SRECs deposited in this account to obligated LSEs at a minimum clearing price. The intent of the auction account is to serve as an SREC price floor and provide greater revenue certainty to solar developers and investors. Qualifying solar PV systems built during 2010 will be granted the right to deposit SRECs into the auction account for 40 quarters (

i.e., 10 years), effectively ensuring developers the ability to sell SRECs at the DOER set minimum price for 10 years. The DOER will adjust the auction account term eligibility in future compliance years based on SREC market conditions. If SREC market prices indicate that the solar market is oversupplied with SRECs, the DOER can decrease the length of the auction account eligibility to temper market growth. Conversely, if too few PV systems are being built in the state to meet the solar RPS target, the DOER can extend the length of the auction eligibility for new systems (not to exceed 10 years).

The DOER will establish the auction account on the NEPOOL GIS system [

9]. The auction account will be open to accept deposits of eligible, unsold SRECs during the final 31 days of an RPS compliance year. Only SRECs that have been generated within the auction opt-in term for a particular project are eligible to be deposited into the auction account. Once deposited in the auction account, SRECS cannot be used by LSEs to meet their compliance obligations for the year in which the SRECs were generated. The DOER, in coordination with the NEPOOL GIS, will re-issue the SRECs deposited into the auction account as re-minted auction account attributes. Unlike non-auction account SRECs, these newly re-minted SRECs will have a shelf life of two years, which allows LSEs to count them towards compliance for either one of the next two compliance years. The DOER can adjust the shelf life of re-minted auction account SRECs based on auction outcomes.

The DOER will hold an auction for SRECs from the auction account within 30 days after the submission of each LSE’s annual RPS compliance filings. Under the SREC program, the DOER has the ability to adjust future year LSE SREC obligations based on solar market conditions. Adjustments to the minimum standard growth rate allow the DOER to increase or decrease PV installation growth to reflect market conditions. If, in a given year, all SREC generators are able to sell their certificates before the end of the compliance year, and no SRECs are deposited in the auction account, the DOER will not hold an SREC auction.

The auction will have a fixed price at $300/MWh. Bids are for the volume of re-minted auction account SRECs that bidders are willing to buy at the fixed price. Revenues received by the state from the auction are distributed to the generators who deposited SRECs into the auction account, minus an auction fee (5% or $15/MWh). The DOER will manage the auction fees, which will be used to defer any auction costs and to benefit the continued development of renewable energy in the Commonwealth.

This new RPS program design, which was adopted through emergency regulation by the DOER in January 2010, has not been implemented in other RPS policies or in other RPS carve-outs. Given the nature of the market design and the potentially complex interactions between market participants, the DOER elected to build a system dynamics model to inform its policy analysis and design. The next section discusses efforts by the DOER to use system dynamics to better understand the market implications of the program.

3. Methodology

System dynamics modeling is useful for understanding the underlying behavior of complex systems over time, taking into account time delays and feedback loops. Developing the design for an innovative auction concept required extensive computer modeling, which was carried out using Excel spreadsheets and system dynamics software. The DOER employed system dynamics to better understand the potential market behavior, including how PV developers might make decisions about initiating new installations, what strategies LSEs would use to purchase SRECs, and how adjustments to the minimum standard growth rate could meet policy goals while minimizing ratepayer impact. The DOER also used the model to fine tune the program adjustments (such as auction opt-in terms) used as policy levers to respond to market conditions.

The model was built using Vensim DSS system dynamics software from Ventana Systems.

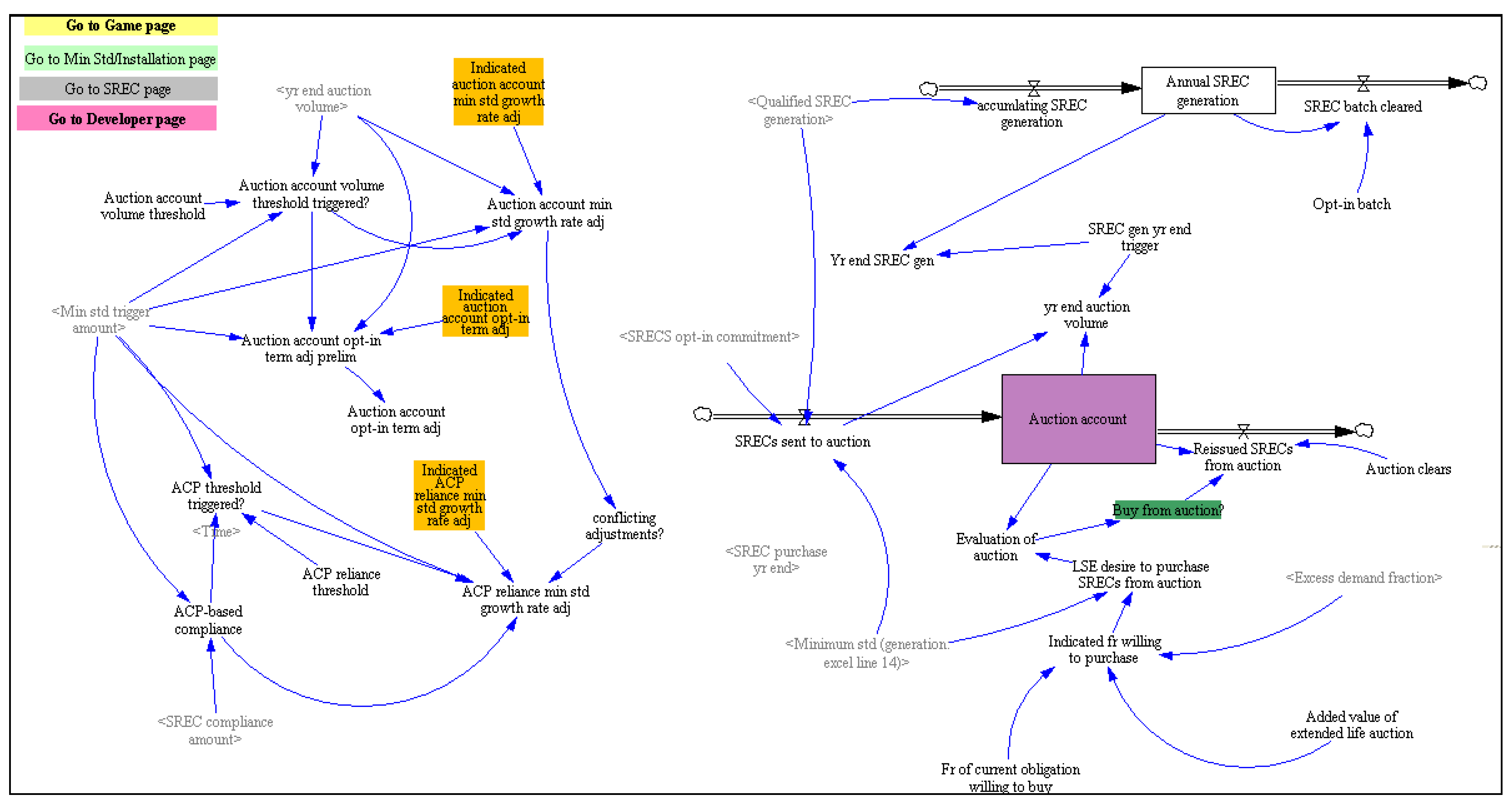

Figure 1 shows a section of the DOER SREC market model with variables for the auction and minimum standard growth rate levers. The boxes with solid outlines (e.g., “Auction account”) represent stocks (parameters that have a specific volume at a point in time) while the arrows going into and out of the boxes that are named (e.g., “SRECs sent to auction”) represent flows (parameters that are rates indicating volume per unit of time). The arrows represent a relationship between parameters and contain underlying equations. Non-stock variables are simply shown as names in the model (e.g., “Evaluation of auction”). Highlighted non-stock variables (“Indicated auction account min std growth rate adj”) represent variables for which the DOER had a particular interest in testing for optimal values. By defining each of the stocks, flows, and relationships, the possible evolution of the SREC market could be projected and visualized and used to more accurately inform policy decisions.

Figure 1.

Screenshot of model layer for SREC auction and minimum standard levers.

Figure 1.

Screenshot of model layer for SREC auction and minimum standard levers.

3.1. Modeling SREC Market Design Parameters

Once the market reaches 400 MW of installed PV capacity, new PV-based generation is not eligible, in other words not “qualified”, to receive SRECs.

Figure 2 shows the SREC generation and minimum standard layer of the model.

Figure 2.

Screenshot of model layer for SREC generation and minimum standard.

Figure 2.

Screenshot of model layer for SREC generation and minimum standard.

Qualified SREC generation (referred to later in the article as simply SREC generation) is calculated using the following equation:

where the capacity factor in Massachusetts is 13% and MS Cap is 400 MW

Although the minimum standard growth rate would typically be represented as a variable, the DOER had designed the program such that the growth rate was adjusted every year using two variables that were influenced by the level of ACP reliance (suggesting SREC undersupply) and auction reliance (suggesting SREC oversupply). The DOER wanted the market to follow a steady 30% growth rate until it achieved 400 MW, and to do this it designed the program to have a variable growth rate that would be adjusted in order to keep the market on this growth trajectory as much as possible. Therefore, this approach required that the model use a stock for increasing and decreasing the growth rate every year. The details of the adjustors are too complex to describe in this paper, however, the stock adjustment (“adjustments to growth rate flow” equation) was straightforward:

where the minimum standard growth rate max is 999%

4. Results

Once the initial model was constructed, the project team used sensitivity analysis to determine the most significant program parameters. This analysis identified the minimum standard growth rate a as a critical factor in market stability. The DOER was also interested in the impact of different opt-in terms on market stability. This section focuses on these two parameters as illustrative of how the DOER used the model to optimize its market design. Initial modeling parameters matched the initial program design, including a 30% per year minimum standard growth rate and an initial 10-year auction opt-in term. The opt-in term can be reduced in subsequent years depending on the level of excess SREC volume that was sent to the auction. The maximum decrease in opt-in term in any given year is two years. The minimum opt-in eligibility is five years (or goes to zero when the market reaches the final 400 MW goal).

4.1. Minimum Standard and SREC Generation

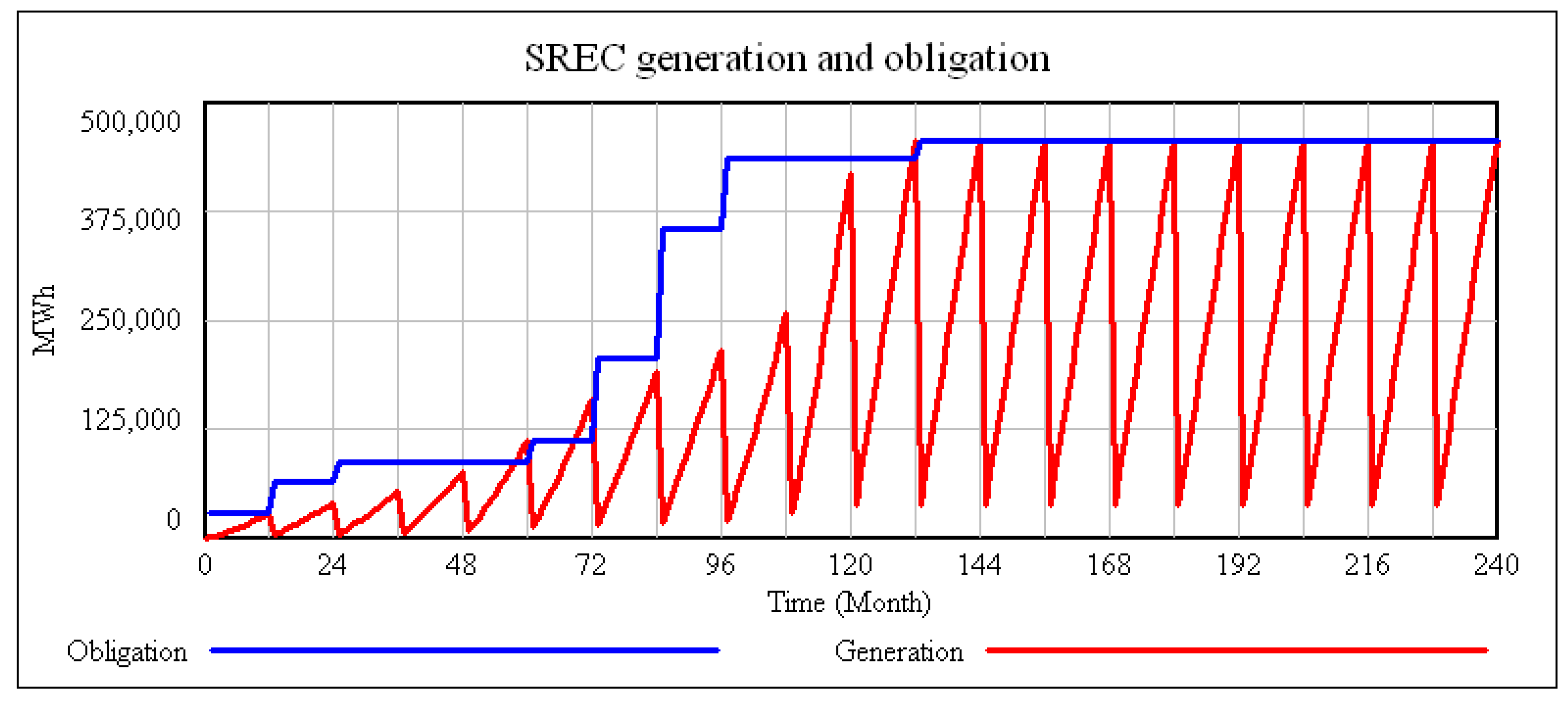

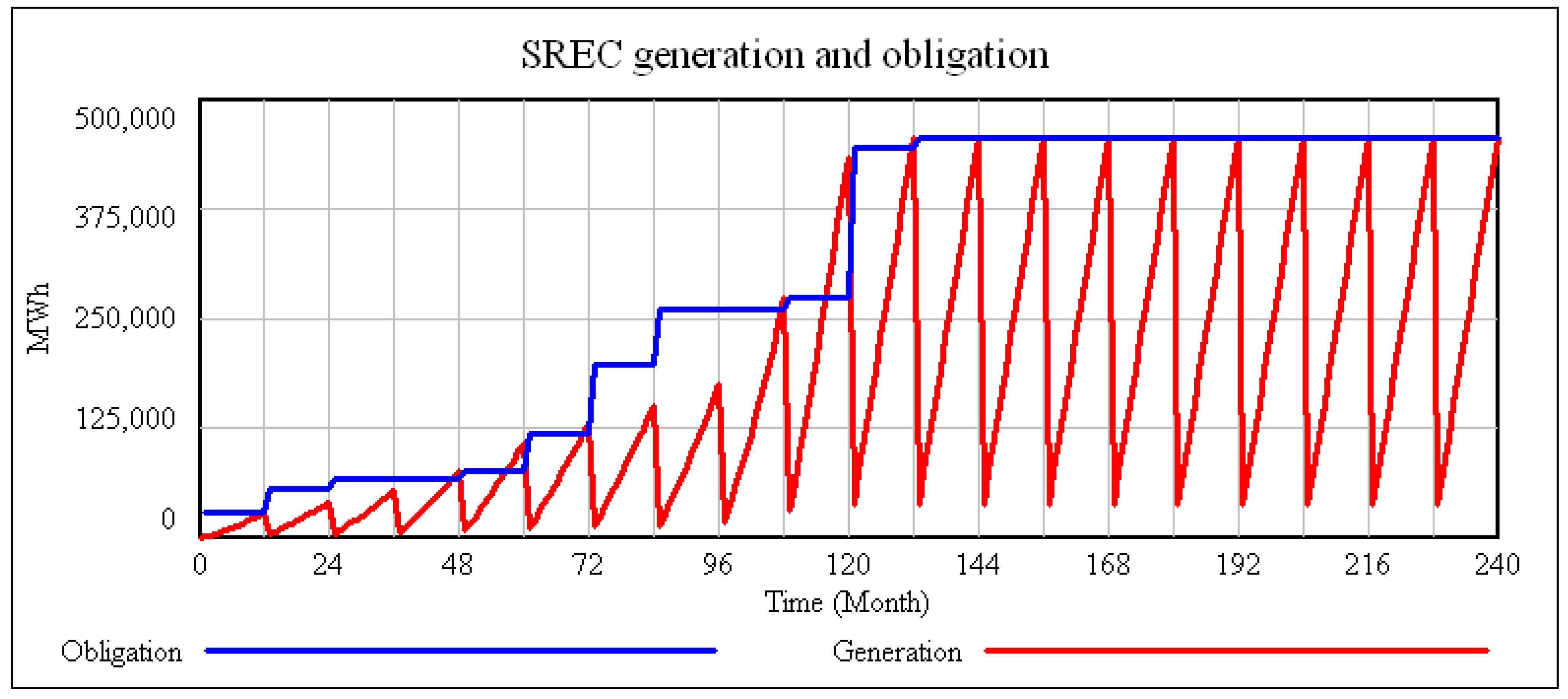

The DOER was interested in examining the relationship between the minimum standard growth rate and SREC generation over the course of the program. The base case results for SREC generation and minimum standard, or LSE obligation, are shown in

Figure 3. The blue stepwise line represents the minimum standard, while the red jagged line represents the cumulative SREC generation (equal to the volume of electricity generated by PV) through each year (the model runs on a monthly basis). The drop in the red line each year indicates that a new compliance year has begun and a new vintage of SRECs are accumulating. The growth of SREC generation (labeled in the figure as simply “generation”) follows a pattern one would expect under such a market design where SRECs are generated for a given year and then are retired to meet compliance. The SREC generation line does not always fall to zero because electricity suppliers are allowed to bank up to 10% of their obligation—banking some of their SRECs provides flexibility to LSEs to still meet their obligation if the market is in undersupply and thus they attempt to hold this amount. As

Figure 3 shows in months 24 to 48, the number of SRECs generated is below the minimum standard and thus the minimum standard does not change over this time. Once generation catches up to the standard, (month 60), the standard is increased the following year (month 72).

Figure 3.

Qualified SREC generation and minimum standard (LSE obligation) over time.

Figure 3.

Qualified SREC generation and minimum standard (LSE obligation) over time.

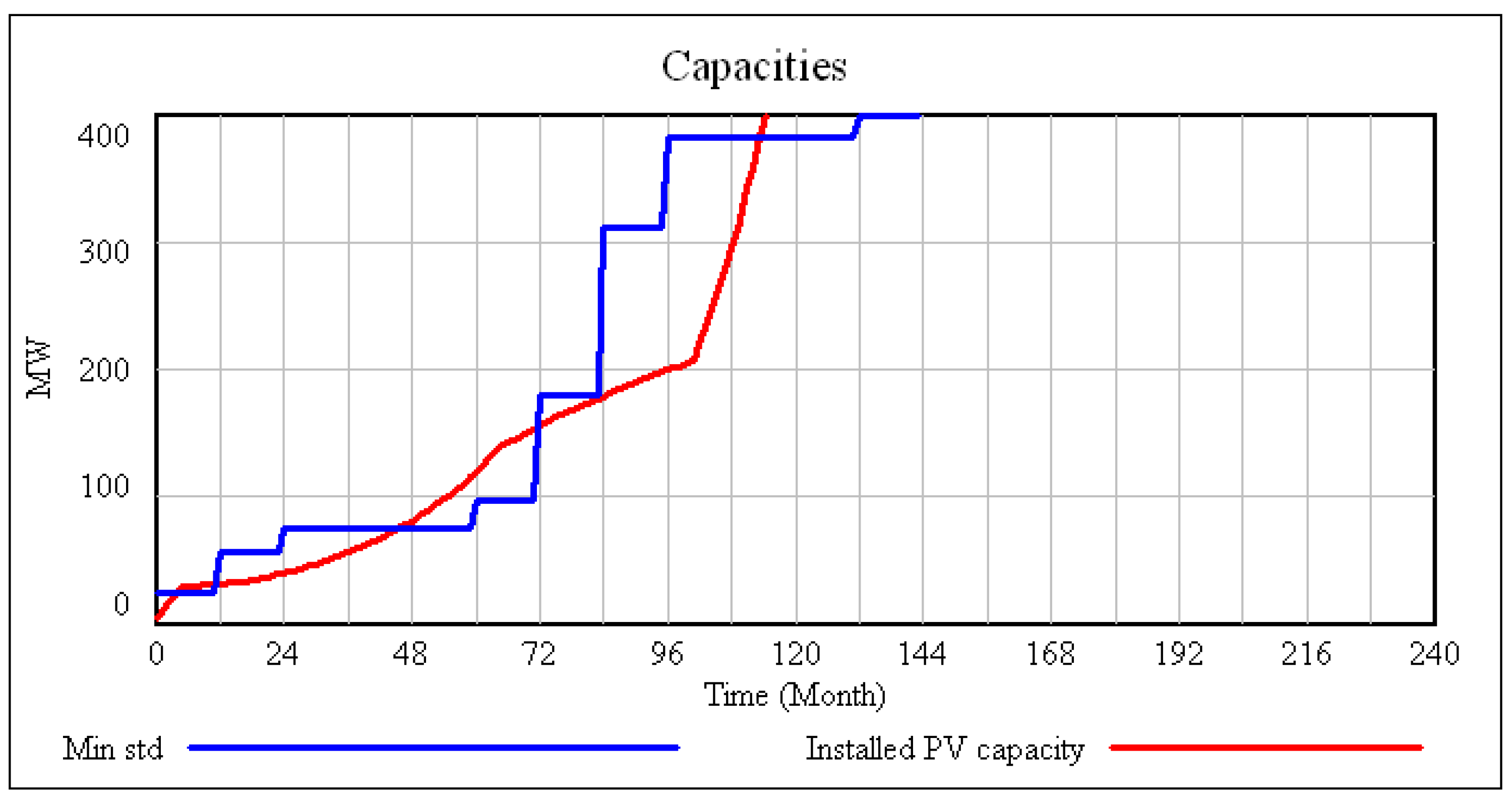

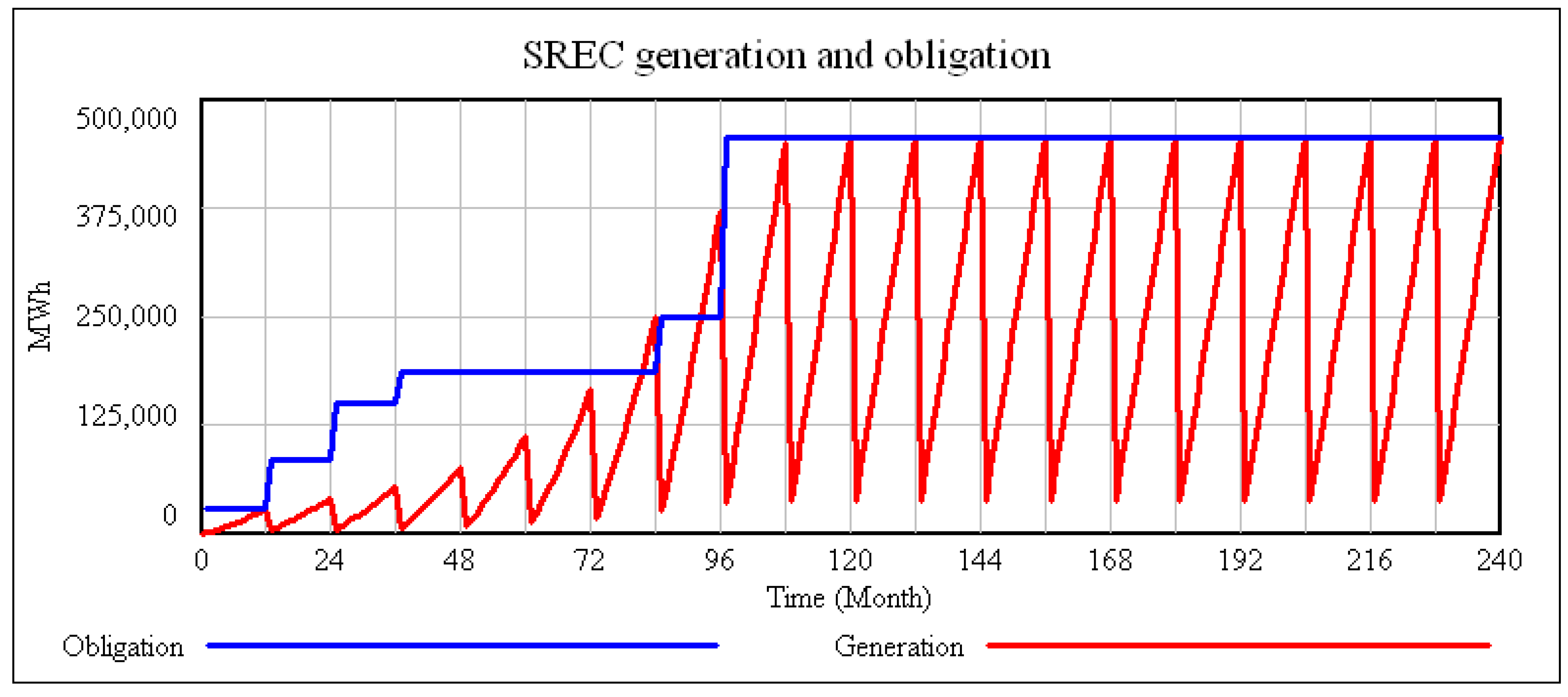

The capacity of installed PV (in MW) and the minimum standard over time are shown in

Figure 4. The target capacity of 400 MW is reached in just under 10 years in the base case, although the target SREC generation is not achieved until the following year because some installations that come online during the course of the year (rather than at the beginning of the year) do not produce a full years’ worth of generation.

Figure 4.

Capacity of installed PV and minimum standard over time.

Figure 4.

Capacity of installed PV and minimum standard over time.

Both

Figure 3 and

Figure 4 indicate that there are times during the program where qualified installations and SRECs will be either above (such as in month 60) or below (such as in month 24) the standard. However, SREC generation remains close to the standard during most years of the base case scenario model run.

One of the most important insights gained from these simulations was the potentially problematic structure of setting the minimum standard. The model showed that by changing the minimum standard each year based on threshold triggers (i.e., based on the percent of SREC volume in the auction or ACP payments relative to the minimum standard) and by making adjustments based on percentages (i.e., adjusting the minimum standard using percentage increments) the market tended to react with more volatility than other approaches simulated in the model. Given these results, the DOER revised the policy structure such that the minimum standard each year follows a 30% growth rate, but is increased in any given year by the excess amount of SRECs from the previous year (in the case when there is an auction) or decreased by the amount equal to the volume on which ACPs were paid, rather than by percentages. This simpler approach is not only easier to implement, but also results in a more stable market because it dampens the fluctuations in the minimum standard, which could be quite large under the initial program design.

4.2. SREC Price

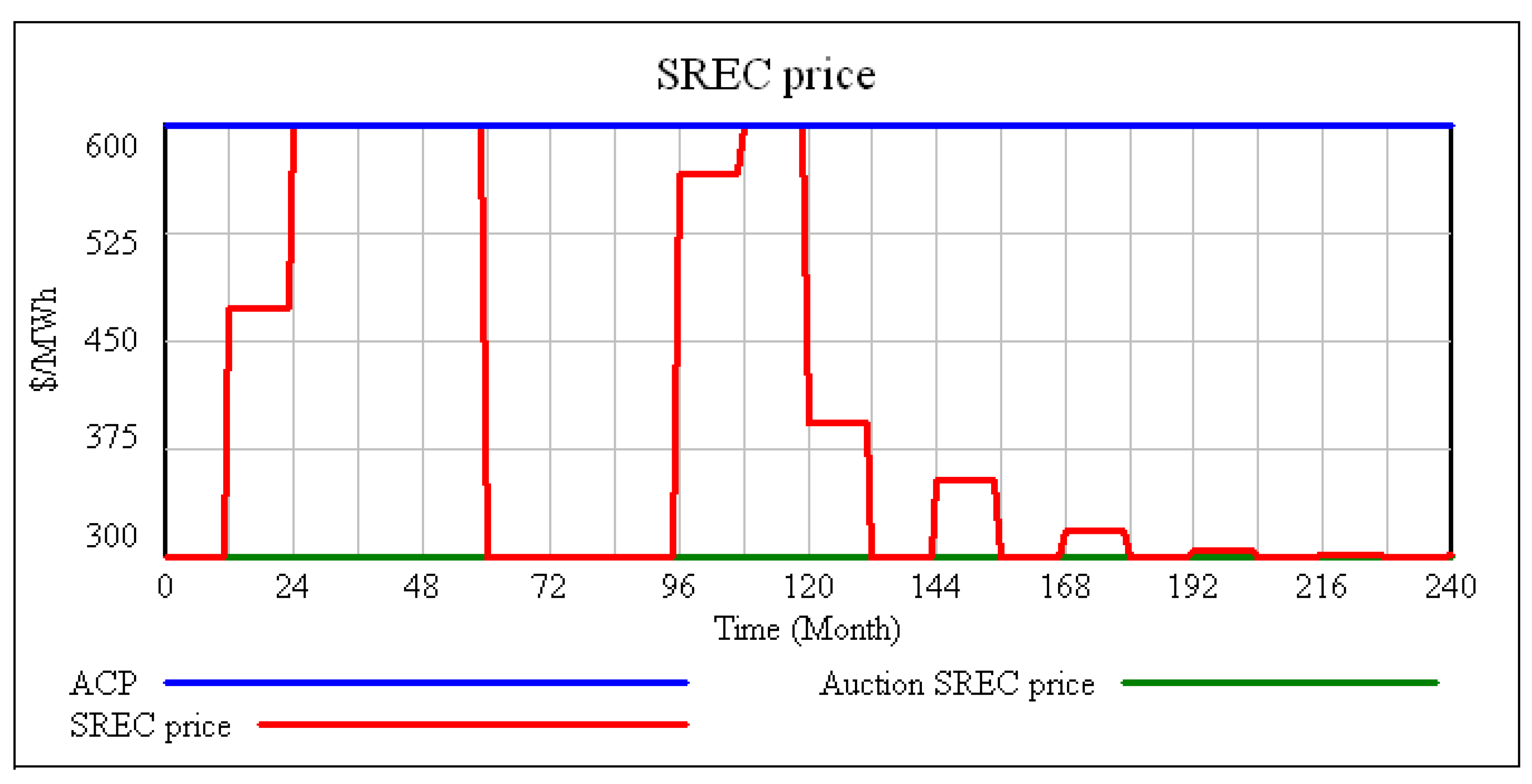

The DOER also used the model to examine potential fluctuations in SREC market prices.

Figure 5 shows the price pattern of the market with $600 (ACP) marked in blue and $300 (auction price) marked in green. SREC price is one of the primary drivers of new installations, along with the return on equity that investors can expect given the PV system cost and opt-in term for each year.

In the base case, the SREC price fluctuates between the auction price and ACP price as the market is in over- and undersupply, respectively. Toward the end of the program, the price primarily rests at the auction price as there continue to be SRECs eligible for the auction, with a few slight increases in price as LSEs try to build holdings (they are allowed to bank up to 10% of the current year obligation) in a tight SREC market.

Figure 5.

SREC price over time.

Figure 5.

SREC price over time.

While the model is not meant to predict specific prices, SREC price will likely rise to the ACP price fairly quickly after the start of the program then decline to the auction price as solar installations catch up to the standard, then will rise and drop again as SRECs oscillate between over- and undersupply. This oscillating price pattern has been seen in other REC modeling efforts [

13] and is due to the time lag to bring new installations online.

4.3. Parameter Testing

The DOER requested further analysis of several parameters to better understand their impact on the market and to determine if a different value should be applied. Two of these parameters will be discussed here: the minimum standard growth rate and the opt-in terms (both the minimum term and the maximum change in the term for any given year). The results of this analysis are provided below.

4.3.1. Minimum Standard Growth Rate

A minimum standard growth range of 0–100% over last year’s growth was compared to the proposed growth of 30% per year (0% growth implies that the same amount of incremental capacity is added each year—in the base case this would be 20 MW added each year). Applying zero incremental growth to the minimum standard results in a pattern similar to the proposed 30% growth rate, whereby the market oscillates between under- and oversupply of SRECs, however, the key difference of these scenarios was that there were more SRECs sold in the auction (

Figure 6).

On the other extreme, applying a growth rate of 100% each year resulted in five years of significant undersupply early in the program, and thus five years of ACP reliance, followed by three years of oversupply and auction reliance (

Figure 7).

Figure 6.

Parameter testing: 0% growth of incremental increase in minimum standard each year.

Figure 6.

Parameter testing: 0% growth of incremental increase in minimum standard each year.

Figure 7.

Parameter testing of 100% incremental growth in minimum standard.

Figure 7.

Parameter testing of 100% incremental growth in minimum standard.

The results of this analysis indicate that 30% is a reasonable growth rate to reach the target 400 MW while avoiding excessive ACP reliance at the beginning of the market. The model confirmed the DOER’s original program design and led to the 30% base case growth being adopted in the final regulations.

4.3.2. Opt-in Term

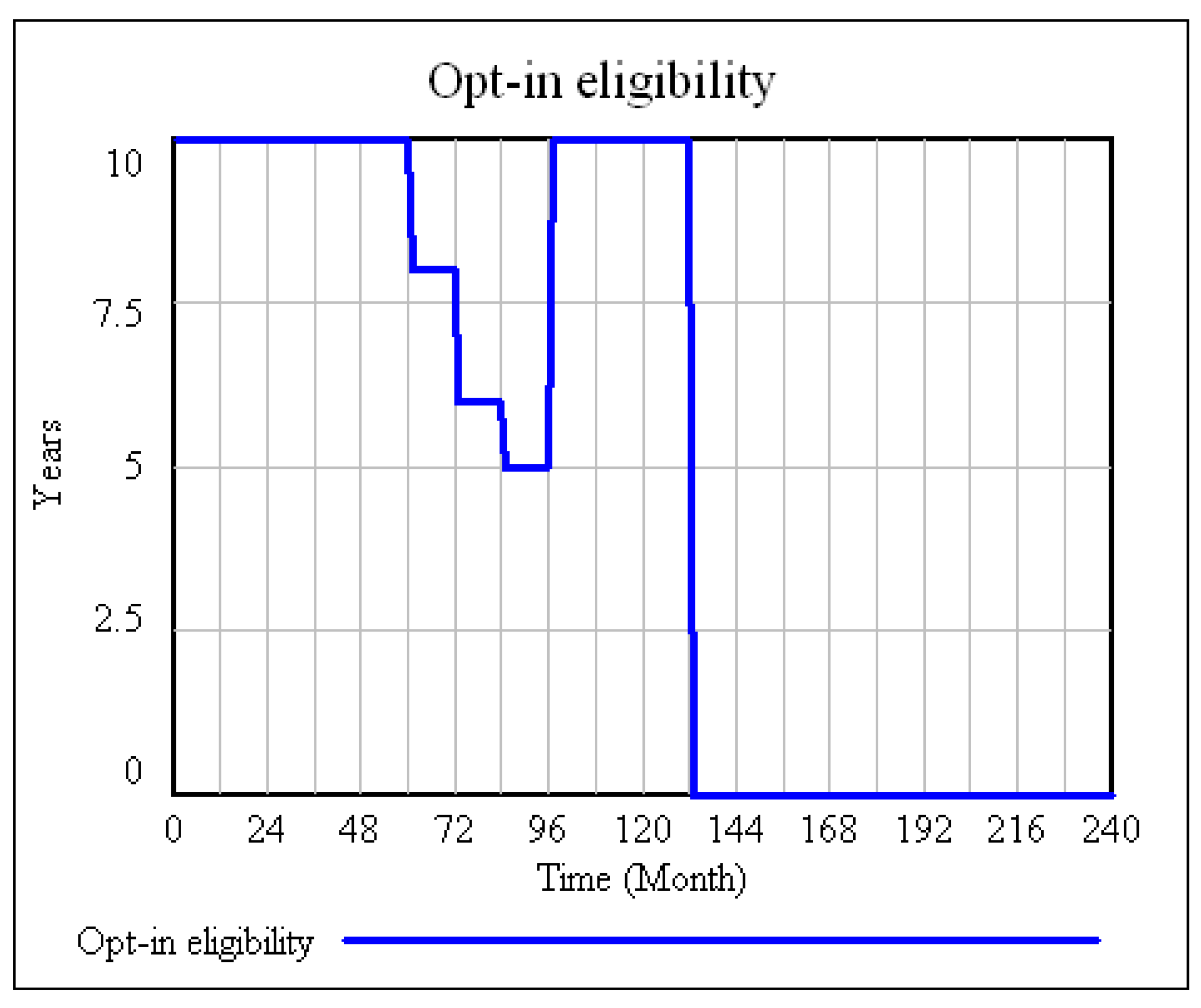

In the base case scenario, the opt-in eligibility declines to 8 years after the first 5 years (

i.e., month 60) of the program when the market enters a slight oversupply situation (

Figure 8).

The opt-in eligibility continues to decline until the market enters an undersupply situation and the ACP is paid, at which time it is reset to 10 years (shown in

Figure 8 at 96 months after the start of the program). Once the target 400 MW is reached, opt-in term falls to zero (at 132 months).

Figure 8.

Opt-in eligibility in model base case.

Figure 8.

Opt-in eligibility in model base case.

Parameter testing was performed for both the maximum number of years the opt-in term could decline in any given year as well as the minimum opt-in term. In extreme cases (but not in the base case) where the installations grew much more rapidly than expected, the minimum term of five years resulted in SREC prices staying at the auction level of $300/MWh for a longer period of time relative to a scenario where opt-in term was allowed to fall to zero.

Testing was also performed on the maximum change in opt-in term for any given year. The proposed maximum decrease is two years. Allowing the opt-in term to decline by 10 years in any given year did not affect the outcome in the base case because at a time when there is a substantial oversupply that would drive the opt-in term lower, the following year is in undersupply and pushes the opt-in term back to 10 years. Even in extreme growth scenarios, lowering the maximum change to −10 had little impact on the outcome. Therefore, the opt-in minimum term and maximum change are not highly influential parameters. Yet, having a minimum of five years as an opt-in, at least throughout the initial years of the program, as well as a maximum yearly decline of two years, provides investors with a narrower range of possibilities that may reduce the perceived risk of the program.

4.4. Auction Behavior

Interviews with stakeholders indicated that many were concerned that the DOER supported auction would not clear. Since the concept of an SREC auction is new, stakeholder feedback on potential behavior in the auction was limited. Nevertheless, a basic approach to modeling bidder behavior indicated that there are some scenarios when the auction may not clear. Even though the model does not fully simulate bidder behavior, the DOER took these results and the concerns from stakeholders into consideration and developed alternative adjustments (beyond extending the life of the SREC) to reduce this concern.

5. Conclusions

The system dynamics model described above allowed the state to consider a broad range of complex market interactions and permitted the DOER to make a series of refinements to its proposed regulations. One major change that the DOER made to the program design was to take a different approach to calculating the minimum standard each year. Originally, each new year’s standard was calculated by applying a percentage incremental change to the previous year’s standard, and which was based on the degree to which the market was in over- or undersupply in that year. This produced model results that, in some runs, indicated widely fluctuating market dynamics. This level of volatility made it difficult for the market to return to the desired equilibrium growth rate of 30%. The DOER changed the model design to add or subtract the prior year’s over- or undersupply of SRECs from a baseline growth of 30%. This change in the program led to simulations with a market that was better able to balance the minimum standard with the growth of installations without causing extreme fluctuations in the market. It is also a simpler approach to comprehend, which may help build stakeholder confidence in the market. The minimum standard growth target of 30% appears to be a reasonable one given that a lower rate results in a greater reliance on the auction in later years of the program, while a higher growth rate results in greater reliance on ACP payments initially and then more auctions later in the program. The SREC price will likely fluctuate between the ACP ($600/MWh) and the auction price ($300/MWh) for most of the life of program until the 400 MW cap is reached. This fluctuation provides the opportunity for generators and LSEs to engage in price stabilizing bilateral contracts of various terms.

The model also helped the DOER determine the terms it set for the auction eligibility of SRECs. The simulations showed that the minimum opt-in term and maximum change each year in the term have little influence on the overall outcome of the program. In some extreme scenarios, setting the minimum term to five years could cause SREC prices to stay at the auction price for a longer period of time. However, this risk needs to be balanced with the added certainty a five year minimum could provide investors—this would be particularly relevant in early years of the program. Therefore, the DOER was free to set terms that offered more security to investors without compromising the desired outcome of the market. The DOER made slight modifications to the terms by setting the minimum term to five years (it originally could be as low as one year) and setting a two-year maximum change in the term from one year to the next.

The dynamics of true bidder behavior in the auction and analysis of market conditions in which the auction does not clear were beyond the scope of this model. Nevertheless, the model did provide some indication of scenarios where the auction did not clear. The DOER took this into consideration and developed further adjustments to the auction to increase the likelihood that the auction would clear, such as increasing the obligation of the electricity suppliers.

Subsequent to the modeling and discussions with stakeholders, the DOER filed emergency regulations in January 2010. Draft proposed amended regulations were released by the DOER in February 2010 and were the subject of a Public Hearing and comment period in March 2010. As of April 2010, the DOER is in receipt of its first applications for qualification for the RPS Solar Carve-Out from solar developers, which the DOER expects to approve.

As more public attention turns to the issues of climate change, energy security and green jobs, policymakers are actively engaged in scaling up the deployment renewable energy. Many programs have been implemented at the state level, and the number of support mechanisms for renewables, and particularly solar, are continually growing. It is often difficult to ascertain how these complex programs will actually operate once implemented, causing policymakers to turn to sophisticated modeling to be reassured that innovative designs can be successful. As this paper shows, system dynamics modeling is well suited for sustainable energy policy analysis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}