5.1. Evaluation of the Value Chain

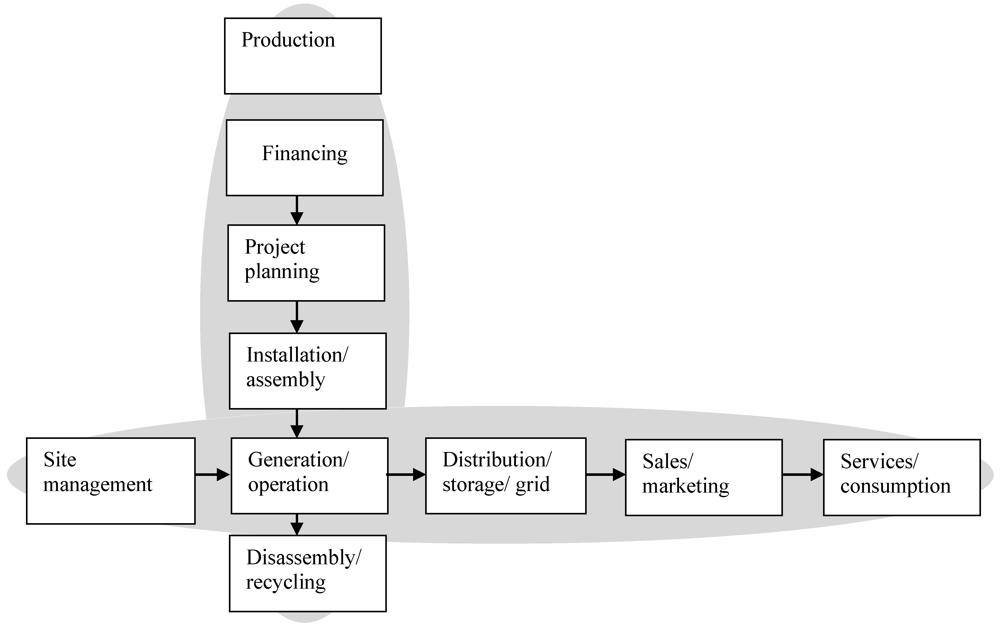

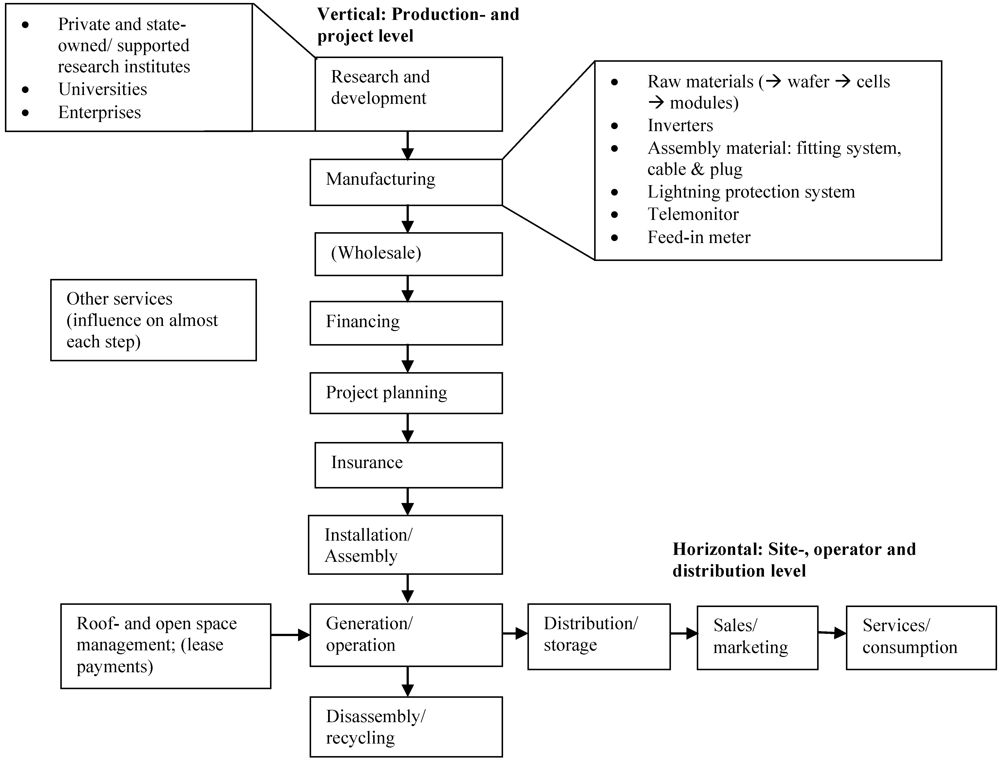

As one of the first steps, the value chain for solar power systems was identified. The existing literature was a starting point (

cf. Section 2) but it showed that some aspects of the chain were not considered. Especially R&D as an initiator and driver of innovations and some parts of the services sector were not covered. Both aspects had already been added (see

Figure 3) before value chain experts were interviewed. The interviewees stated that the depiction of the value chain was complete but that some features or ambiguities needed to be understood and explained: For the manufacturing it needs to be considered that the production steps for crystalline and thin-film PV are different. The distribution of PV systems occurs through different channels. Some producers deliver through wholesalers and others directly to their end-consumers. Wholesalers can also act as importers of systems but ultimately this has no influence on the generation of added value as only the distribution is considered at this step of the chain. Small and large systems at the project planning step must be differentiated. Small rooftop systems are usually planned by the installer, larger rooftop or open space systems are often planned by a project planner who also takes care of other aspects like financing, administrative authorization

etc. These differences are considered by Hirschl

et al. [

2] and can be seen in

Table 1 where project planning is one of the few steps that are more costly for larger systems. The positioning of insurances in the value chain has also been discussed. It can be argued whether an insurance contract should be closed before or after the assembly of the system. One expert mentioned that the more professional the planner, the earlier a contract is signed. This point is negligible, as added value, which is only very small on this step, is generated anyway. It was noted that the installation can be done by enterprises that are specialized in solar systems only or by conventional electricians, roofers or heating installers that offer PV panels in addition to their usual systems. This differentiation is vital for the data collection on this step of the value chain. Interviewing each single enterprise that offers solar systems would have been very time consuming and the return of answers would probably have been incomplete. Instead, the large specialized enterprises were interviewed and the others covered through the official number of PV-systems in Freiburg.

Several actors gave statements about general aspects concerning the added value chain. One expert strongly emphasized the different market segments: Private investors who build rather small systems, medium-sized investors with larger systems and professional investors that build many systems on a large scale with a strong profit-orientation. These categories can be found in Hirschl

et al.’s [

2] method.

Therefore it seems that

Figure 3 shows the added value chain completely and appropriately, but it has to be taken into account that different market segments with different characteristics exist. It also seems advisable to re-examine the value chain at certain intervals, as new developments like an increasing own electricity consumption and the possibly entailed introduction of battery systems can change the value chain.

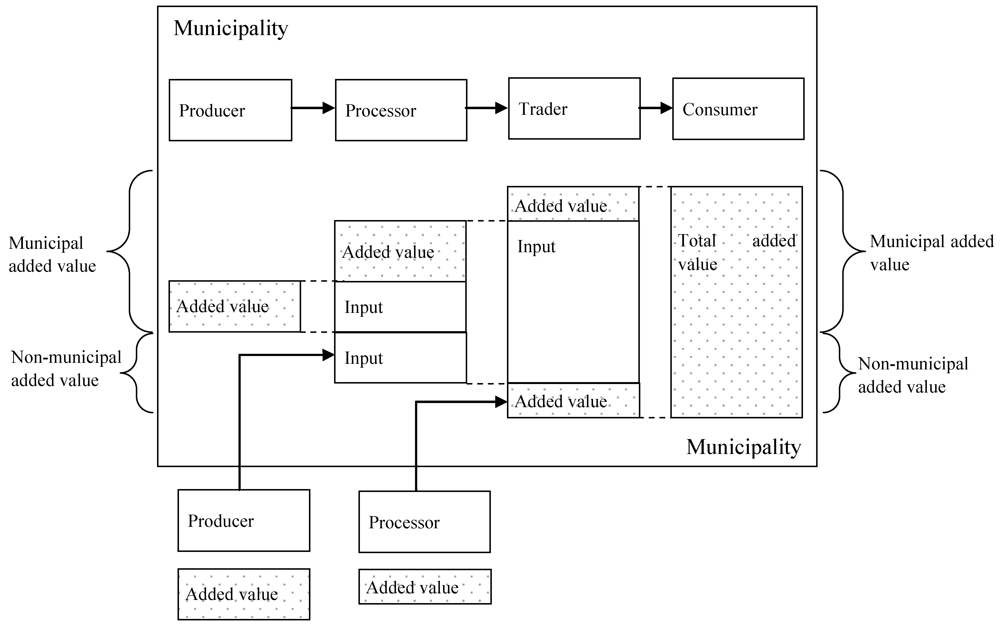

Two experts mentioned the export of goods and services from Freiburg. Wholesale and production can be mentioned here as two examples that generate only a small share of their revenues in Freiburg. These export effects are covered in this paper.

Some experts and enterprise representatives also mentioned that the assumed system prices (€/kWp) by Hirschl

et al. [

2] were considerably too low in comparison to the situation in Freiburg in 2009. These values were corrected, as they have a significant influence on the generated municipal added value (

cf. Section 4.2.1).

5.2. Direct Added Value Through the Solar Power Sector

The municipal added value through direct effects of the solar power sector in Freiburg in 2009 adds up to 30.8 million euros (

cf. Table 5).

Table 5.

Direct added value through solar power systems in Freiburg 2009.

Table 5.

Direct added value through solar power systems in Freiburg 2009.

| Value chain step | Direct added value [€*] | Share [%] |

|---|

| R&D | 7,440,000 | 24.1 |

| Manufacturing | 10,325,000 | 33.5 |

| Wholesale | 3,990,000 | 12.9 |

| Financing | 235,000 | 0.8 |

| Project planning | 4,055,000 | 13.2 |

| Installation/assembly | 1,940,000 | 6.3 |

| Generation/operation | 2,400,000 | 7.8 |

| Services | 425,000 | 1.4 |

| Sum | 30,810,000 | 100 |

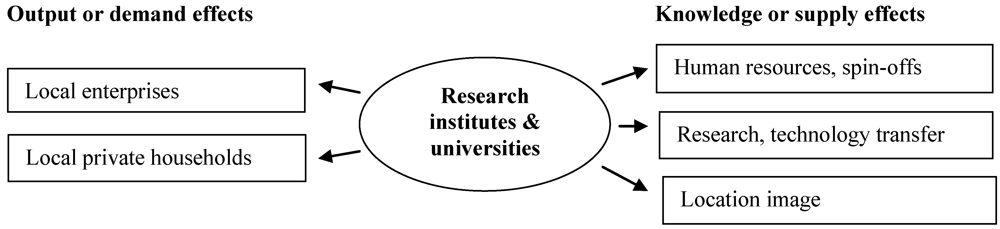

R&D generates a direct added value of almost 7.5 million euros, which represents 24 percent of the total sum. With a share of ca. 34 percent, manufacturing is responsible for the largest single share. Wholesale, project planning, installation/assembly and generation/operation contribute between 6 and 14 percent each, while financing and services have relatively small shares with about 1 percent each.

The values, which are presented in

Table 5, will be explained in more detail next. R&D in Freiburg is carried out by private enterprises and institutions, which are at least partly publicly funded. Only the latter are considered on this step of the value chain, as all privately initiated R&D is included in the price of the product and thereby considered in the respective step of the value chain. In Freiburg, the Fraunhofer Institute for Solar Energy Systems (Fraunhofer ISE: The world’s second largest solar research institute with about 900 employees in 2009) and the university need to be considered. The added value on this step is generated by 439 employees who have a 50 percent job on average. The rather high investments were strongly influenced by an economic stimulus package in 2009. The results for R&D in

Table 6 are presented in an aggregated form for both institutions.

Table 6.

Detailed information about direct added value through solar power systems in Freiburg.

Table 6.

Detailed information about direct added value through solar power systems in Freiburg.

| Value chain step | After-tax earnings [€] | Net income effects [€] | Municipal share business tax [€] | Municipal share income tax [€] | Municipal share investments [€] |

|---|

| R&D | / | 4,990,000 | / | 195,000 | 2,260,000 |

| Manufacturing | 2,460,000 | 7,040,000 | 430,000 | 395,000 | / |

| Wholesale | 1,270,000 | 2,350,000 | 235,000 | 135,000 | / |

| Financing | 115,000 | 90,000 | 20,000 | 10,000 | / |

| Project planning | 555,000 | 3,210,000 | 130,000 | 160,000 | / |

| Installation/ assembly | 260,000 | 1,550,000 | 70,000 | 60,000 | / |

| Generation/ operation | 1,980,000 | 190,000 | 130,000 | 100,000 | / |

| Services | 60,000 | 330,000 | 20,000 | 15,000 | / |

| Sum | 6,700,000 | 19,750,000 | 1,035,000 | 1,070,000 | 2,260,000 |

Two module manufacturers are located in Freiburg. For Manufacturer 1 (M1), the added value could be calculated using the method by Hirschl

et al. [

2]. Manufacturer 2 (M2) is a spin-off from Fraunhofer ISE and is at the stage of introducing its products into the market which is why the added value generated by this enterprise could not be calculated in the unit €/kWp but with the employment method.

There are two wholesalers located in Freiburg. Wholesaler 1 (W1) also operates as a project planner, the added value associated with that is considered at the relevant step of the value chain. As it was not possible to conduct an interview with Wholesaler 2 (W2), data was taken from their website and the employment method was applied.

Three banks and one project financer were questioned for the quantification of the added value effects through financing. Another enterprise on this step of the chain was not willing to disclose any information. The bank representatives mentioned that no internal statistics about financing PV-systems existed. Therefore, the calculation was done according to Hirschl

et al. [

2] with the assumption that small rooftop systems are financed by 50 percent, and large rooftop and open space systems with 75 percent borrowed capital. These assumptions were confirmed in the interviews. Financer 1 (F1) only finances systems within the city boundaries, Financer 2 (F2) and Financer 3 (F3) also outside. As no exact data on the financed capacity is available and there are effects of systems that are financed in Freiburg but installed outside, it is assumed that all existing PV-systems are financed according to the aforementioned conditions.

Several enterprises are active on the project-planning step. There are some large companies specialized in solar systems which also offer their services outside the city boundaries, and there are also conventional enterprises that offer PV apart from their usual services and take on the planning together with the installation; usually small scale systems (

cf. Section 5.1). The publicly available numbers for new PV systems in 2009 (

cf. Table 3) were applied for the small companies, as it was assumed that services offered from Freiburg but carried out outside the city equaled those that were built inside the city by enterprises from outside. Only the large companies are considered separately and their planned capacity is deducted and calculated individually. This means that from a total capacity of 3,180 kWp, 702 kWp were planned by the large specialists and the rest, 2,478 kWp, by the small enterprises. This separate consideration allows reliable data to be obtained without interviewing every single small business in this field.

Insurance is important for the owner of a PV-system in order to protect themselves against possible damages. This step of the value chain is very difficult to quantify, as insurance can be taken out with any insurer in Germany and they are most likely not located in the study area. Even if all local systems were insured by companies in Freiburg, the generation of added value would be below 10,000 euros. The added value of this step is not included in the calculations as its influence is small and the uncertainty high.

For the step of installation/assembly, the same assumptions made regarding the relevant companies in the project planning step are valid. The only difference is that not all specialized companies install all their planned systems themselves. Installer 1 (I1) planned 34.7 megawatts but only 3.4 were installed by their employees.

The aspects operator or operating company as well as maintenance of existing systems is considered on the step generation and operation. Systems in the city boundaries as well as systems that are operated from Freiburg but are located outside are considered. The latter are difficult to cover completely, as it is not possible to collect data about investments of individual citizens into PV-systems outside of Freiburg. Therefore, only one large enterprise that operates PV-systems with a capacity of almost 11 megawatts outside Freiburg is included in the calculations. The maintenance is carried out by the companies that also install the systems.

The step disassembly and recycling is acknowledged in this paper but is not included in the calculations as a recycling possibility, which can be used free of charge, only started to exist in 2010. In the future, this aspect might become more important when old systems need to be disposed of more frequently.

The service sector in Freiburg consists of enterprises in the fields of legal consultation, public relations and advertising, consulting as well as lobbying which are not covered by the other steps. The added value is calculated with the employment method, as no outputs in kWp are generated.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}