1. Introduction

Water ports and water access cities have been critical locations for human settlement and economic growth throughout history, but many port areas have gone through phases of decline in the past few decades, and only some cities are able to adapt to and sustain development through creative sector stimulation and sustainable development [

1]. Factors for the success of such development have been investigated using a benchmarking analysis of Spain, Germany, the Netherlands and Norway [

2].

Working waterfronts are usually among the engines of sustainable development in port cities or coastal areas due to their strong linkages with economic and social structures. Working waterfronts are defined as parcels of real property that provide access to water-dependent and water-related commercial activities or to the public to the navigable waters of a state. Economic activities dependent on working waterfronts play important roles in the development and sustainability of different coastal economies [

3]. Both endogenous and exogenous changes in the final demand for working waterfront output (also known as the direct economic impact) can be expected to show up as changes in the gross output of water-related industries (e.g., seafood processing, boat and ship building, water transportation).

Evidence regarding the economic significance of working waterfronts across the U.S. is compelling [

4,

5]. Water-dependent industries have tremendous economic impacts on the Alabama and Mississippi coastal economy developments; annual values for both states have been estimated as follows: (1) dockside value of commercial landings at $80.5 million; (2) value of dockside landings, processing and wholesale at $738 million; (3) economic output of recreational saltwater fishing at $561.8 million; and (4) saltwater fishing jobs at 6480 [

6]. As economic interests of different stakeholders are at stake, assessment of the opportunity costs and benefits of working waterfront conversion to other land uses is not only challenging, but also contentious [

7].

Commercial developers are increasingly buying traditional working waterfronts and converting them into non-industrial residential use. These changes decrease the availability of waterfront property necessary to sustain traditional economic activities and increase alternative values of nearby working waterfront properties, causing working waterfronts to be less profitable for traditional industrial uses. While in Alabama, the tax is still based on valuation of its current use value instead of market value, the pressure to convert to the “highest and best” use of the property is still there when the value of alternative use has been significantly increasing. While such conversions initially invigorate the local economy, the associated positive benefits diminish over the long term [

8,

9,

10]. The government does receive some rise in property taxes and jobs for real estate development, but negative externalities and poor economic linkage with other sectors will appear gradually following the conversion. More importantly, the impacts are often not in favor of the traditional users and stakeholders of the working waterfronts.

In the Alabama coastal area, working waterfronts contribute significantly to the state’s economy in tourism, shipping, fishing and other activities. Increasing development pressures in coastal areas are threatening to displace traditional water-dependent industries, like fishing and public recreation. Even though fishing is still important in these regions, water-related tourism, nature-based tourism, birding and real estate are among the emerging important economic activities in the Gulf Coast economy that are gradually replacing the manufacturing industry as important sources of economic growth (

Table 1). The contribution of the working waterfronts has been evolving along with the changing economy and sustainability framework [

11,

12].

For our research, we used this insight to simulate changes in working waterfronts and their implications on the Alabama coastal economy development and sustainability considering the limited primary data on working waterfront resources. We also attempted to characterize economic trends and evolutions of working waterfronts and water-dependent industries in the Alabama coastal counties and to provide a historical perspective on developments in the region in order to highlight the genesis of the problems that working waterfronts currently face. To demonstrate the relative significance of water-dependent industries, economic contribution and location quotients were estimated using IMPLAN-V3 (Impact Analysis for Planning, Version 3). This commonly-used software package enables the construction of input-output (I-O) models and social accounting matrices that show linkages among different sectors, households and governments in the economy and allows for assessing economic effects for specific industries [

2].

2. Changing Waterfront-Relevant Industries and Their Contributions

The history of the Alabama Gulf Coast has been strongly associated with water. Mobile Bay has been essential to the coastal area in Alabama, and the city of Mobile is the center of the regional economy. Mobile Bay is an inlet of the Gulf of Mexico, lying within the state of Alabama in the United States. The Mobile and Tensaw rivers flow into Mobile Bay. Spanish explorers sailed into the area as early as 1500, but it was the French who established a settlement in 1702. Later, it was ruled by the British and Spanish. During the Antebellum period from 1820 to 1860, Mobile enjoyed prosperity as the second-largest international seaport on the Gulf Coast, after New Orleans.

Mobile was one of the four busiest ports in the U.S. by the 1850s. It was an important port for slave trade from Africa, as well as for the export of cotton to Europe. Mobile grew substantially in the period leading up to the Civil War, when the Confederates heavily fortified it, but it declined after the Civil War. During and after World War I, manufacturing became increasingly vital to Mobile’s economic health, with ship building and steel production being two of the most important industries. World War II led to a massive military effort causing a considerable increase in Mobile's population, largely due to the huge influx of workers coming into Mobile to work in the shipyards and military fields. The pulp and paper industry became a major player in the 1960s and 1970s. The emerging recreational boating market promoted the boat building industry beginning in the 1990s. Mobile suffered from a few large fires at early times, but was more recently affected by hurricanes (e.g., Hurricane Frederic in 1979, Hurricane Ivan in 2004, Hurricane Katrina in 2005) and the Deepwater Horizon oil spill in 2010.

Gulf Shores (a popular tourism destination) and the surrounding industries in Alabama are increasingly dependent on waterfront-relevant activities, which have fueled much of their rapid development [

13]. For instance, in 2009, the state’s two coastal counties (Mobile and Baldwin) generated 12% of Alabama’s total output, contributing $19.96 billion to the GDP and employing 223,783 people. Employment related to the waterfront or ocean economy sector amounted to 8736 and contributed $1.57 billion to the GDP. Water transportation, fishing, seafood processing and ship and boat building make a considerable impact on the local economies [

13].

In their long history, waterfront-relevant industries in this area were mainly concentrated on the ship building and fishing sectors. Over recent decades, most of the Alabama shoreline has been rapidly developed for residences, recreation and tourism. Other areas, such as Mobile Bay and the seaport of Mobile, have long been important industrial sites and transportation hubs. Mineral extraction has become the largest sector in waterfront-relevant industries. Since the 2000s, mineral extraction and tourism have been the leaders, respectively, of providing production and jobs in Mobile Bay.

To identify the roles of working waterfronts, we classified the coastal waterfront-relevant economies into six sectors, comprising 23 industries, following a Quarterly Census of Employment and Wages (QCEW) (

Table 1). National and regional data sources developed by the National Ocean Economics Program (NOEP) were collected to analyze and allow meaningful comparisons of waterfront-relevant industries.

Table 1.

Waterfront-relevant industries by category.

Table 1.

Waterfront-relevant industries by category.

| Sector | Industry |

|---|

| Construction | Marine-Related Construction |

| Ship and Boat Building | Boat Building and Repair; Ship Building and Repair |

| Tourism and Recreation | Amusement and Recreation Services; Boat Dealers; Eating and Drinking Places; Hotels and Lodging Places; Marinas; Recreational Vehicle Parks and Campsites; Scenic Water Tours; Sporting Goods Retailers; Zoos, Aquaria |

| Living Resources | Fish Hatcheries and Aquaculture; Fishing; Seafood Markets; Seafood Processing |

| Minerals | Limestone, Sand and Gravel; Oil and Gas Exploration and Production |

| Transportation | Deep Sea Freight Transportation; Marine Passenger Transportation; Marine Transportation Services; Search and Navigation Equipment; Warehousing |

Table 2 displays Alabama’s waterfront-relevant economy by its sectors in 2009. The waterfront economy in the Alabama Gulf Coast generated more than 18,000 jobs and contributed over $1.47 billion to the GDP (

Table 2). Minerals, tourism and recreation, ship and boat building, and transportation are particularly important. The ship and boat building sector dominated in the county of Mobile, while the tourism and recreation sector dominated in Baldwin County.

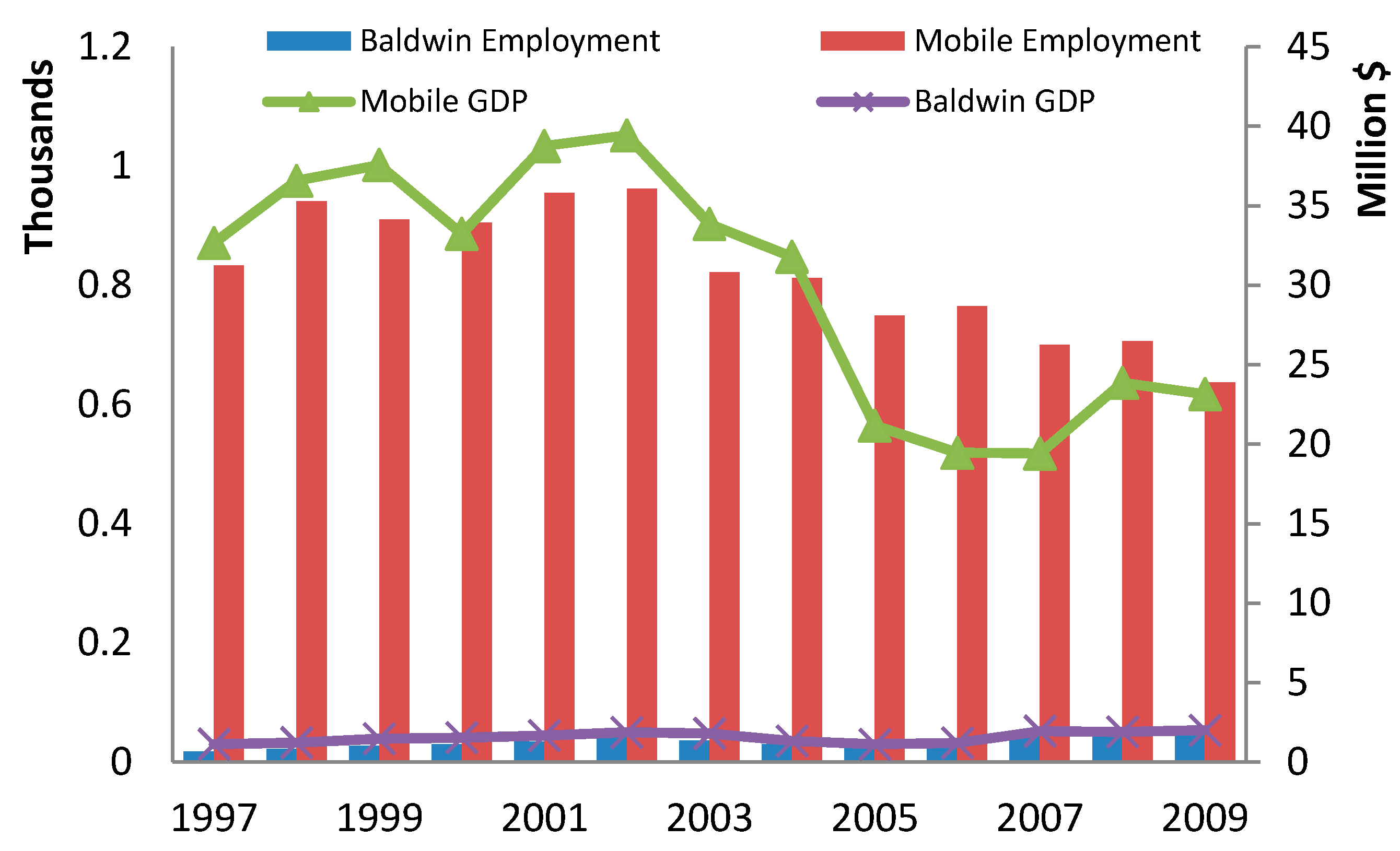

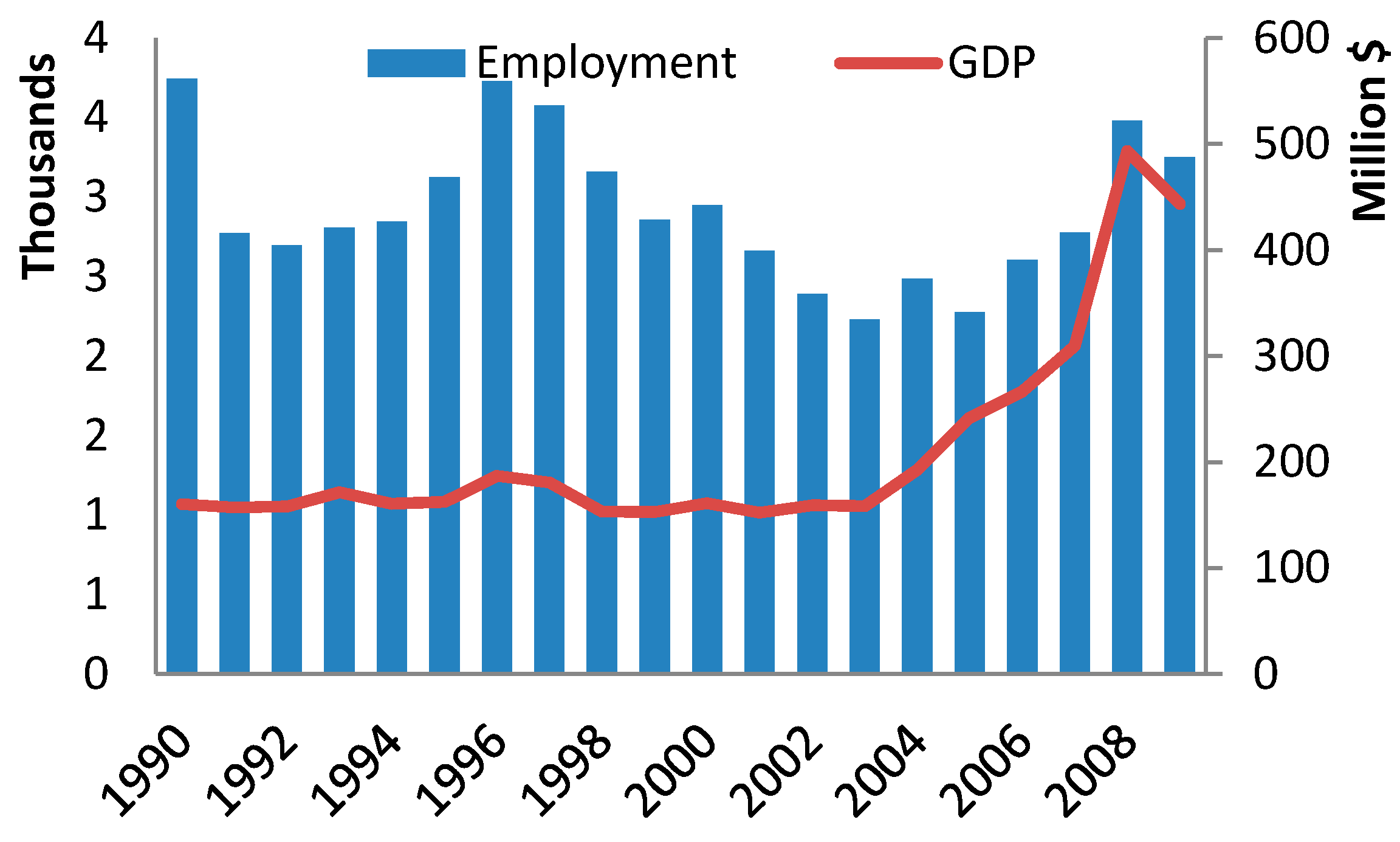

Figure 1,

Figure 2,

Figure 3 and

Figure 4 show the economic development in the main waterfront-relevant industries from 1990 to 2009. Jobs added in the waterfront sectors over this period totaled 3543, or 18% growth, contributing to an increase in GDP of $1.18 billion, or 128.6% growth. The living resources sector remains popular, but has high volatility over time due to extreme weather, changes in fish stocks and regulations, as well as the oil spill effects. For example, because of the hurricanes in 2000 and 2005, the fish landings peaked in 2000 at 30.1 million pounds. Since then, the landings have declined to 20 million pounds, a decline of just over 30%, and then increased to 34 million pounds suddenly in 2006. However, since then, fishery landings declined to their lowest in 2010 at 14.5 million pounds, a 51% reduction since the oil spill in the Gulf.

Table 2.

Waterfront-relevant economy by sectors, Alabama, 2009.

Table 2.

Waterfront-relevant economy by sectors, Alabama, 2009.

| Baldwin County | Mobile County | Total |

|---|

| Sector | Jobs | GDP (million $) | Jobs | GDP | Jobs | GDP |

| Construction | 49 | 2.6 | 302 | 21.2 | 351 | 23.8 |

| Living Resources | 55 | 2.1 | 637 | 27.2 | 692 | 29.3 |

| Minerals | 225 | 17.7 | 341 | 505 | 3962 | 838 |

| Ship and Boat Building | 3396 | 315.3 |

| Tourism and Recreation | 6859 | 214.8 | 4141 | 118.1 | 11,000 | 332.9 |

| Transportation | 87 | 7 | 2163 | 241.8 | 2250 | 248.8 |

| Total | 7275 | 244.2 | 10,980 | 1228.60 | 18,255 | 1472.80 |

Figure 1.

Economic changes in the living resources sector, 1997–2009.

Figure 1.

Economic changes in the living resources sector, 1997–2009.

Figure 2.

Economic changes in the ship and boat building sector, 1990–2009.

Figure 2.

Economic changes in the ship and boat building sector, 1990–2009.

Figure 3.

Economic changes in the tourism and recreation sector, 1990–2009.

Figure 3.

Economic changes in the tourism and recreation sector, 1990–2009.

Figure 4.

Economic changes in the marine transportation sector, 1990–2009. Data sources for

Figure 1,

Figure 2,

Figure 3 and

Figure 4: data during 1990–2004 from the National Ocean Economics Program (NOEP) [

15] and 2005–2009 from ENOW based on data from the Bureau of Labor Statistics and the Bureau of Economic Analysis Charleston, SC: NOAA Office for Coastal Management. Available at:

http://www.oceaneconomics.org/ [

14].

Figure 4.

Economic changes in the marine transportation sector, 1990–2009. Data sources for

Figure 1,

Figure 2,

Figure 3 and

Figure 4: data during 1990–2004 from the National Ocean Economics Program (NOEP) [

15] and 2005–2009 from ENOW based on data from the Bureau of Labor Statistics and the Bureau of Economic Analysis Charleston, SC: NOAA Office for Coastal Management. Available at:

http://www.oceaneconomics.org/ [

14].

Ship building in the United States is primarily oriented toward building, maintaining and repairing ships for the U.S. Navy. In the study area, over 98% of outputs are generated by Mobile County. Ship building activity increased significantly between 1997 and 2009, although there was a slight reduction in GDP at the beginning of 2000. Similarly, employment consistently displayed an increasing trend. This sector is one of the most important parts of the state’s waterfront-relevant economy. The majority of the activity in boat building was the recreational boating market and was thus another aspect of the overall growth in ocean-related tourism and recreation activities. This means that the productivity in that industry is relatively higher. Traditional ship building might be “eroded” by the service-related sectors.

Tourism and recreation is the most important source of the economic growth in the waterfront. It has exhibited the most consistent growth in the past few decades. For example, though it was affected by the 2000 and 2008 recessions, the sector averaged nearly 76% growth in employment and over 155% growth in GDP from 1990–2009. The minerals sector and ship and boat building sector have accounted for most of the GDP in Mobile County, but the employment growth was concentrated on the ship and boat building sector. The minerals sector is concentrated in Mobile County, which generates $505 million in outputs and 341 jobs. The oil and gas exploration and production industries dominate this sector in the county: these two industries account for over 85% of the employment and 99% of the GDP in the minerals sector. Employment and output growth has risen and fallen with oil prices, usually with a one-year lag.

However, working waterfronts are vulnerable to disturbances by both natural and human disasters. For example, Hurricane Katrina inflicted significant damage in the Gulf in 2005. In a short time, Alabama GDP growth decreased from 5.1% in 2004 to 3.1% in 2005 and the unemployment rate jumped from 3.8% in 2005 to 4.3% in July, 2006; most of the newly unemployed were from Mobile and Baldwin counties [

16]. Up to 80% of the homes in the area were flooded, and many suffered substantial damage or were destroyed. Alabama’s seafood industry, including the charter boat sector, was estimated to have lost $112.3 million as a result of the 2005 hurricane season [

17]. Large numbers of fishing boats were sunk, damaged or grounded on land. Many boat owners did not have insurance. Income in the tourism and recreation sector in the coastal area decreased by 17% and still has not recovered to the income level in 2004 until 2011.

Similarly, the Deepwater Horizon oil spill began on April 20, 2010, and had serious adverse effects on marine and wildlife habitats, fishing and tourism industries on the coast of Alabama and relevant working waterfront industries. Total Gulf landings for all shrimp species in 2010 decreased by 56% compared to the same period in 2009 [

18]. Forty percent of Alabama coastal waters was closed to fishing during the spill. Predicted present total revenues lost in Alabama recreational fisheries are around $111–185 million. The U.S. Fish and Wildlife Service) also estimates that 36 national wildlife refuges are at risk from the 2010 oil spill, and more than 7000 birds were collected in the spill area [

19]. The U.S. Travel Association estimates that the economic impact of the oil spill on tourism across the Gulf Coast over a three-year period could exceed approximately $23 billion, in a region that supports more than 400,000 travel industry jobs generating $34 billion in revenue annually [

20]. The impact on tourism revenues was predicted to be $0.3 billion to $0.8 billion in coastal Alabama, lasting 15 to 36 months [

21].

3. Integrated Waterfront-Relevant Economy: Input-Output Analysis

To make a quantitative assessment of sectorial contributions, input-output models were constructed using IMPLAN-V3 for the state of Alabama and the two study counties in order to analyze the impacts of the coastal waterfront-relevant economy in the coastal area of Alabama. This analysis used 2010 IMPLAN data, which were gathered from the U.S. Bureau of Economic Analysis, the Bureau of Labor Statistics and other sources to provide a complete set of balanced social accounting matrices for every zip code, county and state in the U.S. These data were more accurate than the national average in terms of measuring the effects of specific industries on a regional or local economy.

Five IMPLAN sectors were identified as related to waterfront production: boat building, commercial fishing, seafood production, ship building and repairing, and transport by water. Note that most of the industry sectors in this input-output analysis were consistent with Quarterly Census of Employment and Wages (QCEW) classification in the previous section. For example, the ship building sector consists of North American Industry Classification System (NAICS) 336,611 for both QCEW and IMPLAN classification. However, unlike QCEW, which provides data for each NAICS six-digit industry, IMPLAN groups industries into 440 sectors, and economic data for some specific waterfront-related industries are not available. Therefore, waterfront-related industries in input-output analysis are slightly different from the previous analysis using QCEW data.

Consistent with input-output analysis conventions, all transactions were measured in producer prices (cost of production plus indirect business taxes). Where transactions between consumers and water-dependent industries are in purchasers’ prices, margining procedures were employed [

22]. Specifically, items (commodities) sold at the retail level with known producers were margined to isolate the relative shares of production, transportation and wholesale and retail distribution. Initial expenditures (direct impacts) were adjusted for leakages from the study area by using local purchase coefficients (the proportion of expenditures locally spent). Leakages of expenditures from the impact region were accounted for by using the IMPLAN default values for regional purchase coefficients (the share of demand that can be met with local supply), because of the lack of better information on regional shares of commodity supplies.

The input-output models built are a classification of economic impacts and multipliers and distinguish three types of impacts of exogenous economic stimuli: (1) direct impacts are the immediate impacts within an economy when final demand for a particular industry output changes; (2) indirect impacts capture changes in economic indicators (e.g., industry output, employment, value added) when the system of industries responds to initial spending by the originally impacted industry. For (originally impacted) industries to deliver goods and services, they must first produce them, which leads to purchases of intermediate and primary factor inputs. This affects a number of industries, depending on how interlinked the economy is. Conceptually, this forms the backward linkage impact of initial expenditures. (3) Induced impacts arise when workers employed in the industries spend portions of the incremental earnings; they set off additional rounds of spending and associated impacts on the economy [

23,

24].

The economic multipliers calculated were then used to estimate secondary effects (including indirect and induced effects) generated by waterfront-relevant industries. The greater the share of incremental earnings spent locally, the larger the induced impacts [

23,

24]. Secondary effects of each industry estimated with county I-O models were adjusted proportionally based on multipliers of the state I-O model to represent its impacts on the state economy. The total economic impacts are the sum of direct and secondary effects.

The direct output of waterfront-related industries was approximately $1.5 billion in both Mobile and Baldwin counties in 2010. The total output impact (including direct output, indirect effects and induced effects) was estimated to be $3.1 billion, doubling direct sales of these industries (

Table 3). This impact is much greater than the output impact of sectors, such as agricultural production ($0.7 billion), food and kindred products manufacturing ($1.0 billion) and food and kindred products distribution ($1.9 billion), suggesting that the regional waterfront-related industries significantly affect other sectors and play important roles in the economic growth in this area. Two of the largest sectors were ship building and repairing and transport by water. Their impacts accounted for 80% of the total impact for waterfront-related industries. Compared to Baldwin County, Mobile County clearly dominated waterfront-related industries in Alabama, accounting for 97% of the total impact.

Table 3.

Output and employment impacts of waterfront-related industries in Mobile and Baldwin counties in 2010.

Table 3.

Output and employment impacts of waterfront-related industries in Mobile and Baldwin counties in 2010.

| Sectors | Mobile County | Baldwin County | Total |

|---|

| Direct Output | Output Impact | Direct Output | Output Impact | Direct Output | Output Impact |

|---|

| Output Impact (million $) |

| Boat building | 20.1 | 40.3 | 0.3 | 0.6 | 20.4 | 40.8 |

| Commercial fishing | 54.3 | 90.7 | 3.7 | 5.9 | 58.0 | 96.6 |

| Seafood product | 221.0 | 407.9 | 42.7 | 64.5 | 263.7 | 472.5 |

| Ship building | 606.5 | 1272.2 | / | / | 606.5 | 1272.2 |

| Transport by water | 520.0 | 1180.8 | 10.9 | 21.3 | 531.0 | 1202.2 |

| Total | 1421.9 | 2992.0 | 57.6 | 92.3 | 1479.5 | 3084.3 |

| Employment Impact (Employment) |

| Boat building | 103 | 291 | 2 | 4 | 104 | 294 |

| Commercial fishing | 1492 | 1861 | 121 | 144 | 1613 | 2005 |

| Seafood product | 698 | 2773 | 132 | 366 | 830 | 3139 |

| Ship building | 2860 | 9182 | / | / | 2860 | 9182 |

| Transport by water | 1145 | 7534 | 25 | 129 | 1170 | 7663 |

| Total | 6297 | 21,641 | 280 | 643 | 6576 | 22,284 |

The direct employment through waterfront-related industries totaled 6576 jobs. Commercial fishing was the most labor-intensive sector, directly generating around 28 jobs per million dollars of output, which is much higher than the average of the five sectors (four jobs per million dollars of output). The total employment impact (including direct employment, indirect effects and induced effects) of waterfront-related industries was estimated to be 22,284 jobs in 2010 (

Table 3). Although less labor-intensive, the ship building and repairing, transport by water and seafood product sectors play significant roles in the labor market. These three industries generated an impact of approximately 20,000 full- and part-time jobs (90% of the total jobs of the five waterfront-related industries) due to their higher industry sales and significant effects on other non-waterfront-related industries.

To demonstrate the relative significance of water-dependent industries, we estimated a location quotient on employment for each individual sector with IMPLAN [

2]. This is defined as the percent employment share of industry j in a region of interest divided by the percent employment share of industry j in some reference economy. A location quotient in excess of one means that the industry in question produces more than is locally needed, and it can be considered as an export-producing industry. Thus, location quotients for Mobile County exceed one for all water-dependent industries (

Table 4), suggesting that these industries are considered to be export-producing industries for adjacent counties, states and even world markets. These industries bring new money into Mobile County’s economy and are extremely important for the economic sustainability of the county. Likewise, Baldwin County has an above-average concentration of seafood processing and packaging economic activities and therefore is important to the regional economy.

Table 4.

Location quotients of waterfront-related industries in Alabama/coastal counties, 2010.

Table 4.

Location quotients of waterfront-related industries in Alabama/coastal counties, 2010.

| Region 1 | Fishing | Seafood processing | Ship building | Boat building | Water transportation |

|---|

| Alabama (AL) | 0.80 | 3.09 | 1.71 | 0.47 | 0.56 |

| Baldwin/AL | 0.35 | 3.56 | 0.00 | 1.03 | 0.88 |

| Mobile/AL | 11.43 | 3.79 | 11.68 | 2.29 | 5.33 |

4. Discussions and Conclusions

This study characterizes the socio-economics, demographics and evolution of working waterfronts and water-dependent industries in the Alabama coastal counties, providing both a historical perspective on developments in the region and highlighting the genesis of the problems that working waterfronts are facing. Tourism, ship building and repairing and transportation are three dominating sources contributing to the waterfront-related economy. The ship building and tourism and recreation sectors have been replacing the living resources sector to become the most important parts of the state’s waterfront-relevant economy. The majority of the activity in boat building was the recreational boating market and was thus another aspect of the overall growth in ocean-related tourism and recreation activities. Meanwhile, working waterfronts in these counties have unique problems (e.g., hurricanes, oil spills) because of their location. For example, the largest influence of Hurricane Andrew (2004) was on the tourism and recreation sector, which experienced more than 30% depreciation in GDP and employment after this event. Another sector influenced by that event was fishing. The landing fish weight was estimated to have reduced by 10% in 2005. The consequences of climate change, particularly the frequency of extreme weather (e.g., hurricanes, storms) and sea level rise, are already occurring and will continue to occur through this century regardless of what steps are taken to mitigate further change.

The impacts on economic development have been measured from the overall evaluation of the waterfront rather than a singular industry, such as the real estate industry. Different sectors contribute different multiplier effects to the total economy. The input-output model was applied to further quantitatively assess the direct and secondary effects of output and employment of the waterfront economy. It also demonstrated significant output impacts on or strong linkage to other sectors from ship and boat building, commercial fishing and seafood product industry and transportation (See

Table 3 and

Table 4). The findings further suggest the overall economic contribution of working waterfronts to the Alabama coastal economy. These results may influence perceptions and attitudes toward the importance of working waterfronts for governments, business communities and the general public and serve as a reference to be applied in state and county planning and regional development strategies. The findings of the research can also have applications beyond the Alabama coastal regional economy. Economic impacts can be similarly estimated for waterfronts in other coastal regions of the nation.

Despite the significance of the water-related economy, a challenge facing sustainability of this area is the reduced resilience and increased vulnerability to both natural and human disasters, due to the damages associated with the loss of ecosystem services. Such impacts have been demonstrated following Hurricane Katrina and the Deepwater Horizon oil spill. Creativity and willingness to adapt to new economic activities, particularly within the tourism industry, will be important [

25]. A healthier environment, society and economy were identified as goals by the Coastal Recovery Commission of Alabama, a citizen-led organization created by executive order of the governor following the Deepwater Horizon oil spill [

26]. The impacts of the changing economic structure on the resilience and vulnerability of the coastal economy have been investigated adequately. Future studies and strategies should include ecosystem services as input factors, as well as outputs in the study of sustainability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}