The Development of a Measurement Instrument for the Organizational Performance of Social Enterprises

Abstract

:1. Introduction

2. Performance Measurement in Social Enterprises

3. Methodology

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Research Process | Objectives | Results |

|---|---|---|

| Phase 1: Literature review |

|

|

| Phase 2: Focus groups |

|

|

| Phase 3: Delphi panel |

|

|

| Phase 4: Survey instrument development and administration |

|

|

| Phase 5: Validation of relevant indicators and the assessment tool |

|

|

3.1. Phase 1: Literature Review

3.2. Phase 2: Focus Groups

3.3. Phase 3: Delphi Panel

| Indicators Identified through Literature Review and Focus Groups (53) | Consensus in Delphi Panel (40) |

|---|---|

| Economic performance | |

| Literature and approved by focus groups | |

| Market share in comparison to important competitors | |

| Growth in market share | |

| Additional indicators focus groups | |

| Received subsidies and donations | |

| Innovativeness | X |

| Proactiveness | X |

| Risk Taking | X |

| Environmental performance | |

| Literature and approved by focus groups | |

| Use of renewable energy | X |

| Transportation of materials and goods | X |

| Transportation of the members of the organization’s workforce | X |

| Waste reduction | X |

| Use of sustainable materials | X |

| Environmental policy | X |

| Environmental performance measurement | X |

| Community performance | |

| Literature and approved by focus groups | |

| Offering job opportunities | |

| Hiring disadvantaged people | X |

| Local suppliers | X |

| Local customers | |

| Philanthropy | |

| Partnerships | X |

| Being responsive to complaints of customers | |

| Adaptation of products and services to satisfy complaints of customers | |

| Additional indicators focus groups | |

| Informing the local community | X |

| Offering traineeships to students | X |

| Offering products/services to vulnerable people | X |

| Addressing unsolved problems in society | X |

| Human performance | |

| Literature and approved by focus groups | |

| Supporting learning initiative | X |

| Policy on education and training | X |

| Providing education and training | X |

| Diversity management | X |

| Equal opportunities for minorities | X |

| Involvement of personnel in education and training | X |

| Age sensitive personnel policy | |

| Work-life balance | X |

| Interaction between employees | X |

| Goal oriented HRM | X |

| Additional indicators focus groups | |

| Development/personal growth of personnel | X |

| Absenteeism through illness | |

| Support on the work floor | X |

| Job satisfaction | X |

| Governance performance | |

| Literature and approved by focus groups | |

| Board diversity | |

| No CEO duality | |

| Independent board members | X |

| Adaptation of the composition of the board | X |

| Clear organizational mission and goals | X |

| Engagement of board members toward the mission and goals of the organization | X |

| Involvement of the board in strategic initiatives | X |

| Clarity of roles (of board members and management team) | X |

| Participative decision-making | X |

| Goals meeting the needs of the stakeholders | X |

| Adaptation to changes in the environment | X |

| Efficient, well prepared board meetings | |

| Preparedness to learn from mistakes | X |

| External communication to stakeholders | X |

3.4. Phase 4: Survey Instrument Development and Administration

| Population | Sample | |

|---|---|---|

| Sheltered an Social Workshops | 80 (8%) | 44 (18%) |

| Local service economy initiatives | 206 (20%) | 60 (25%) |

| Work experience enterprises/Work care initiatives | 278 (27%) | 81 (34%) |

| Work integration enterprises | 293 (29%) | 35 (15%) |

| Cooperatives | 161 (16%) | 21 (9%) |

| Total | 1018 (100%) | 241 (100%) |

3.5. Phase 5: Validation of Relevant Indicators and the Assessment Tool

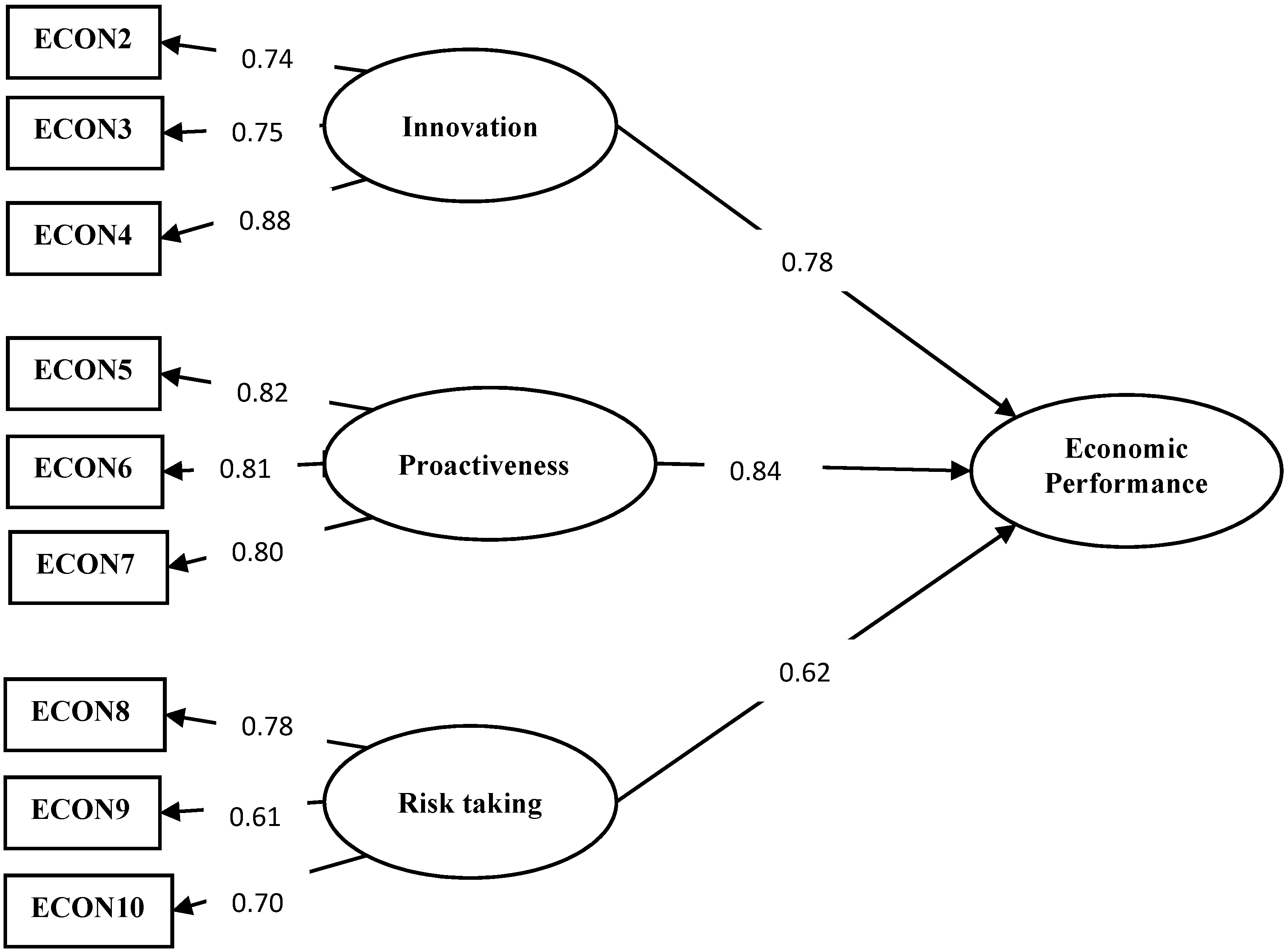

3.5.1. Economic Performance

| Innovation | |

| Presently and during the last five years my organization has: | |

| ECON1* | Placed a strong emphasis on the maintenance of tried-and-true products or services– Placed a strong emphasis on the development of new products or services |

| ECON2 | Placed a strong emphasis on the maintenance of established organizational processes– Placed a strong emphasis on the development of new organizational processes |

| ECON3 | Introduced no new processes, policies, products or services– Introduced many new processes, policies, products and services |

| ECON4 | Made only minor changes in processes, policies, products or services– Made major changes in processes, policies, products or services |

| Proactiveness | |

| Presently and during the last five years my organization: | |

| ECON5 | Is very seldom the first organization to introduce new products/services, administrative techniques, operating technologies, etc.– Is very often the first organization to introduce new products/services, administrative techniques, operating technologies, etc. |

| ECON6 | Been reticent to exploit changes in the field—Exploited changes in the field |

| ECON7 | Followed the lead of similar service providers—Provided the lead for similar service providers |

| Risk Taking | |

| Presently and during the last five years my organization: | |

| ECON8 | Conducted itself consistently with the behavioral norms of the operating environment, industry or sector– Conducted itself in conflict with the behavioral norms of the operating environment, industry or sector |

| ECON9 | Selected projects that support the organization's public image– Selected projects that may alter the organization's public image |

| ECON10 | Made decisions that maintain staff stability– Made decisions that created changes in staff stability |

| ECO1 Innovation | ECO2 Proactiveness | ECO3 Risk Taking | |

|---|---|---|---|

| ECON1 | 0.561 | 0.505 | 0.304 |

| ECON2 | 0.812 | 0.122 | 0.265 |

| ECON3 | 0.803 | 0.249 | 0.045 |

| ECON4 | 0.806 | 0.350 | 0.094 |

| ECON5 | 0.226 | 0.832 | 0.195 |

| ECON6 | 0.333 | 0.805 | 0.044 |

| ECON7 | 0.179 | 0.822 | 0.225 |

| ECON8 | 0.092 | 0.320 | 0.745 |

| ECON9 | 0.036 | 0.129 | 0.824 |

| ECON10 | 0.327 | 0.029 | 0.757 |

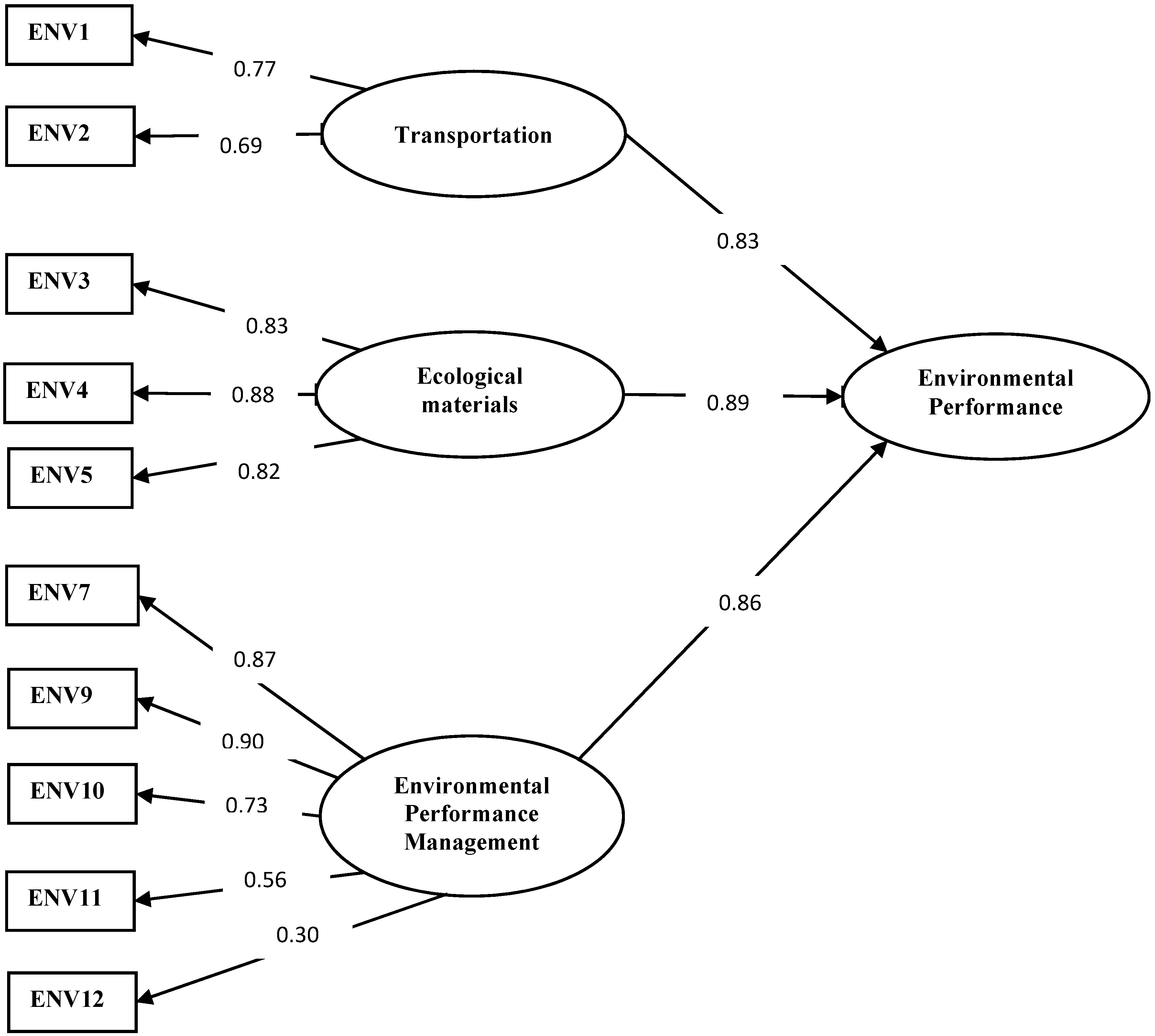

3.5.2. Environmental Performance

| Transportation of Materials and Goods | |

| ENV1 | Our organization deliberately selects cleaner transportation methods for materials and goods Mishra and Suar (2010) [71] |

| Transportation of the members of the organization’s workforce | |

| ENV2 | Our organization encourages employees to use ecological transportation modes Adaptation based on GRI [27] |

| Use of sustainable materials | |

| ENV3 | Our organization uses recycled input materials Adaptation based on GRI [27] |

| ENV4 | Our organization takes the initiative to use environmental-friendly natural resources Chen et al. (2008) [72] |

| ENV5 | Our organization has a preference for green products in purchasing Mishra and Suar (2010) [71] |

| ENV6* | Our organization has implemented sustainability criteria for the procurement of goods and services Adaptation based on GRI [27] |

| Environmental policy | |

| ENV7 | Our organization has incorporated environmental performance objectives in organizational plans Rettab et al. (2009) [73] |

| ENV8* | Our organization is concerned about the protection of the natural environment Adaptation based on GRI [27] |

| ENV9 | Our organization has a clear environmental policy Mishra and Suar (2010) [71] |

| Waste reduction | |

| ENV10 | Our organization has reduced the amount of waste in recent years Adaptation based on GRI [27] |

| Environmental performance measurement | |

| ENV11 | Does your organization measure the organization’s environmental performance? Rettab et al. (2009) [73] |

| Use of renewable energy | |

| ENV12 | Does your organization use energy produced from renewable sources? O’Connor & Spangenberg (2008) [74] |

| EN1 Transportation | EN2 Ecological Materials | EN3 Environmental Performance Management | |

|---|---|---|---|

| ENV1 | 0.757 | 0.186 | 0.344 |

| ENV2 | 0.832 | 0.286 | 0.120 |

| ENV3 | 0.264 | 0.747 | 0.301 |

| ENV4 | 0.215 | 0.843 | 0.292 |

| ENV5 | 0.278 | 0.790 | 0.257 |

| ENV6 | 0.004 | 0.568 | 0.626 |

| ENV7 | 0.274 | 0.400 | 0.717 |

| ENV8 | 0.408 | 0.548 | 0.347 |

| ENV9 | 0.231 | 0.366 | 0.812 |

| ENV10 | 0.283 | 0.168 | 0.766 |

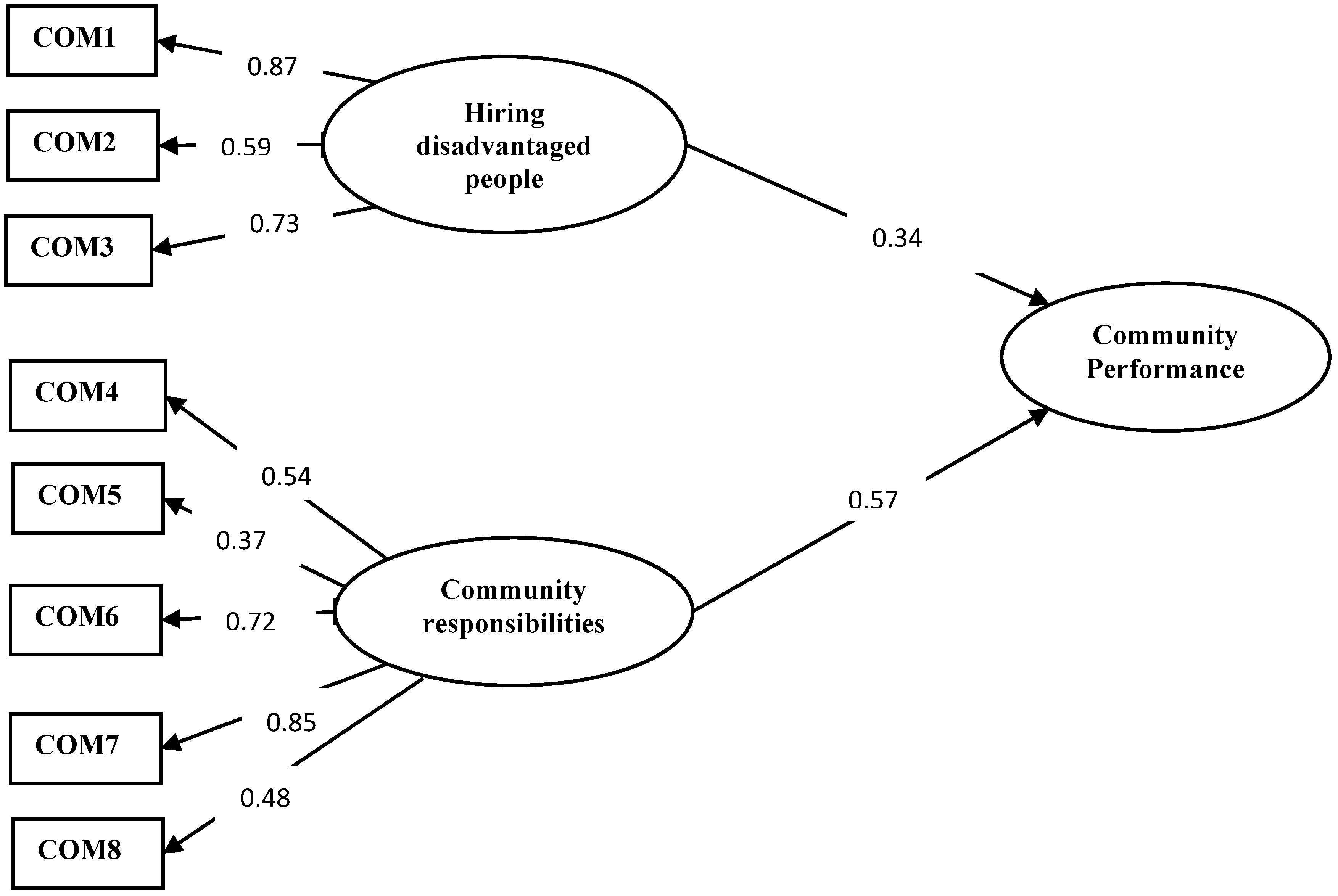

3.5.3. Community Performance

| Hiring disadvantaged people | |

| COM1 | Our organization actively hires immigrants Adaptation based on Graafland et al. (2004) [75] |

| COM2 | Our organization actively hires low skilled people Adaptation based on Graafland et al. (2004) [75] |

| COM3 | Our organization actively hires elderly people Adaptation based on Graafland et al. (2004) [75] |

| Informing the local community | |

| COM4 | Our organization informs the local community by organizing presentations, company visits Adaptation based on CAF [76] |

| Offering traineeships to students | |

| COM5 | Our organization offers traineeships to students Adaptation based on CAF [76] |

| Offering products/services to vulnerable people | |

| COM6 | Our organization offers products and/or services to vulnerable people Adaptation based on CAF [76] |

| Addressing unsolved problems in society | |

| COM7 | Our organization addresses unsolved societal problems Adaptation based on CAF [76] |

| Partnerships | |

| COM8 | Our organization pursues partnerships with:

|

| Local suppliers | |

| COM9 * | Our organization mainly has local (Flemish) or regional (Belgian) suppliers Adaptation based on GRI [27] |

| C1 Hiring Disadvantaged People | C2 Community Responsibilities | |

|---|---|---|

| COM1 | 0.887 | 0.059 |

| COM2 | 0.727 | 0.092 |

| COM3 | 0.845 | 0.041 |

| COM4 | −0.040 | 0.695 |

| COM5 | 0.200 | 0.459 |

| COM6 | 0.126 | 0.766 |

| COM7 | 0.057 | 0.848 |

| COM8 | −0.013 | 0.639 |

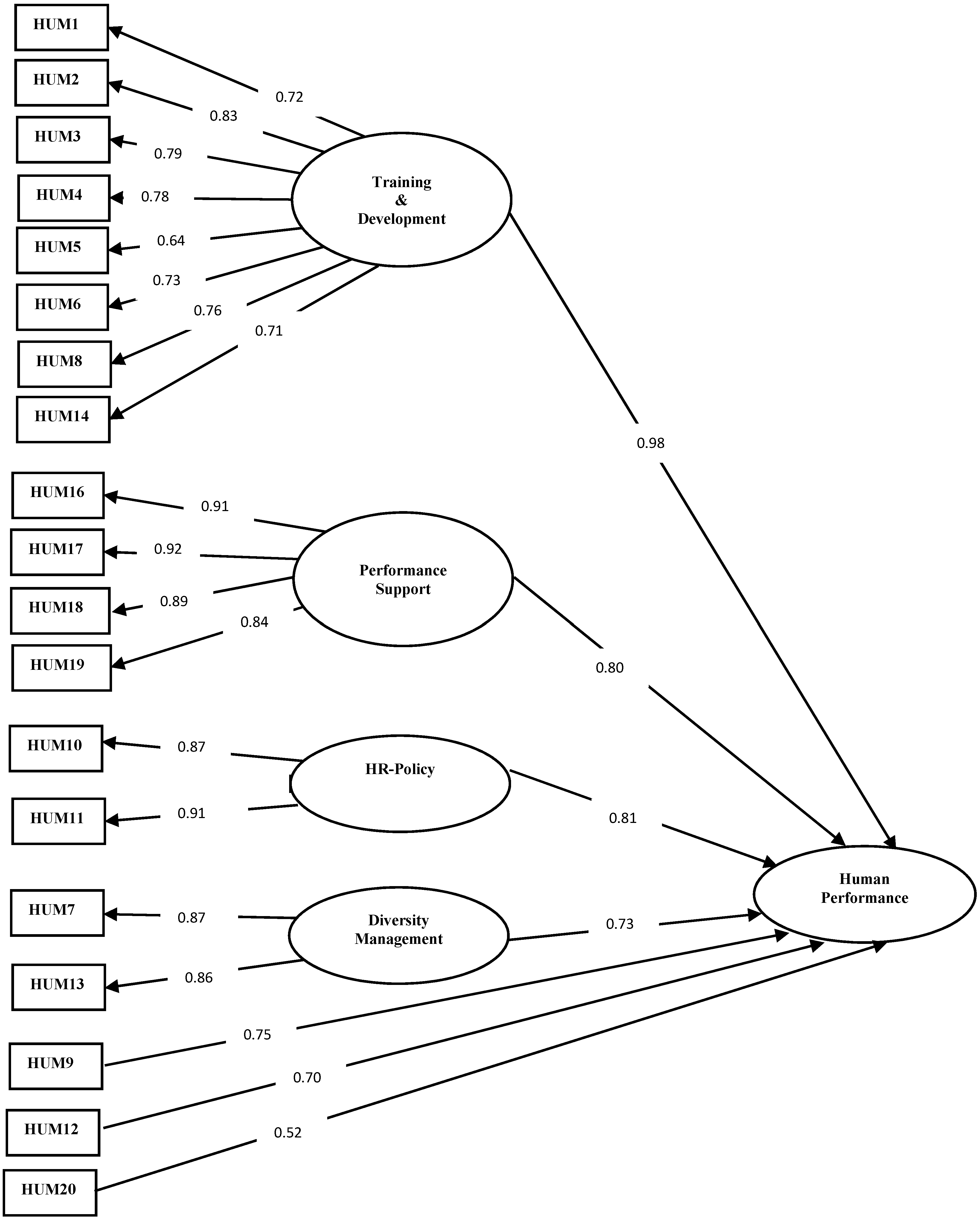

3.5.4. Human Performance

| Providing education and training Calantone et al. (2002) [77] | |

| HUM1 | Our organization has a strong ability to learn and this offers us a competitive advantage |

| HUM2 | The basic values of this organization include learning as key to improvement |

| HUM3 | The sense around here is that employee learning is an investment, not an expense |

| HUM4 | Learning in my organization is seen as a key commodity necessary to guarantee organizational survival |

| Development/ personal growth of employees | |

| HUM5 | We develop our employees aiming at job rotation within our organization Adaptation based on GRI [27] |

| Supporting learning initiative | |

| HUM6 | Our organization supports all employees who want to pursue further education Rettab et al. (2009) [73] |

| Equal opportunities for minorities | |

| HUM7 | Our organizations has a policy concerning equal rights and non-discrimination O’Connor & Spangenberg (2008) [74] |

| Involvement of personnel in education and training | |

| HUM8 | Our organization involves the employees in the planning of education and training Adaptation based on CAF [76] |

| Interaction between employees | |

| HUM9 | We pay attention to good relationships between our employees Adaptation based on ISO26000 [78] |

| Goal oriented HRM | |

| HUM10 | Our HR-policy is carefully planned Adaptation based on GRI [27] |

| HUM11 | Our HR-policy is carefully evaluated Adaptation based on GRI [27] |

| Job satisfaction | |

| HUM12 | Our organization pays attention to individual job satisfaction Adaptation based on GRI [27] |

| Diversity management | |

| HUM13 | Our organization has a policy on diversity management Cuesta Gonzalez et al. (2006) [79] |

| Policy on education and training | |

| HUM14 | Our organization has a policy for the training and development of employees Mishra and Suar (2010) [71] |

| Support on the work floor Adaptation based on Heslin et al. (2006) [80] | |

| HUM15* | We support our employees in taking on new challenges |

| HUM16 | We offer useful suggestions regarding how employees can improve their performance |

| HUM17 | We provide constructive feedback to employees regarding areas for improvement |

| HUM18 | We help employees to analyze their performance |

| HUM19 | We provide guidance regarding performance expectations |

| Work-life balance | |

| HUM20 | Our organization is successful in balancing paid work and family life Adaptation based on Milkie & Peltola (1999) [81] |

| H1 Performance Support | H2 Training & Development | H3 HR-Policy | H4 Diversity Management | |

|---|---|---|---|---|

| HUM1 | 0.263 | 0.650 | 0.301 | 0142 |

| HUM2 | 0.318 | 0.835 | 0.207 | 0.111 |

| HUM3 | 0.287 | 0.718 | 0.151 | 0.352 |

| HUM4 | 0.235 | 0.770 | 0.303 | 0.116 |

| HUM8 | 0.318 | 0.729 | 0.204 | 0.122 |

| HUM16 | 0.805 | 0.362 | 0.199 | 0.096 |

| HUM17 | 0.805 | 0.338 | 0.191 | 0.157 |

| HUM18 | 0.786 | 0.278 | 0.247 | 0.140 |

| HUM19 | 0.814 | 0.244 | 0.186 | 0.137 |

| HUM10 | 0.239 | 0.319 | 0.758 | 0.256 |

| HUM11 | 0.274 | 0.340 | 0.746 | 0.239 |

| HUM7 | 0.144 | 0.317 | 0.309 | 0.772 |

| HUM13 | 0.160 | 0.266 | 0.367 | 0.743 |

| HUM15 | 0.686 | 0.299 | 0.400 | 0.036 |

| HUM5 | 0.255 | 0.413 | 0.418 | 0.226 |

| HUM6 | 0.604 | 0.377 | 0.112 | 0.324 |

| HUM14 | 0.582 | 0.243 | 0.472 | 0.128 |

| HUM9 | 0.291 | 0.663 | 0.092 | 0.390 |

| HUM20 | 0.593 | 0.093 | −0.109 | 0.514 |

| HUM12 | 0.261 | 0.545 | 0.312 | 0.243 |

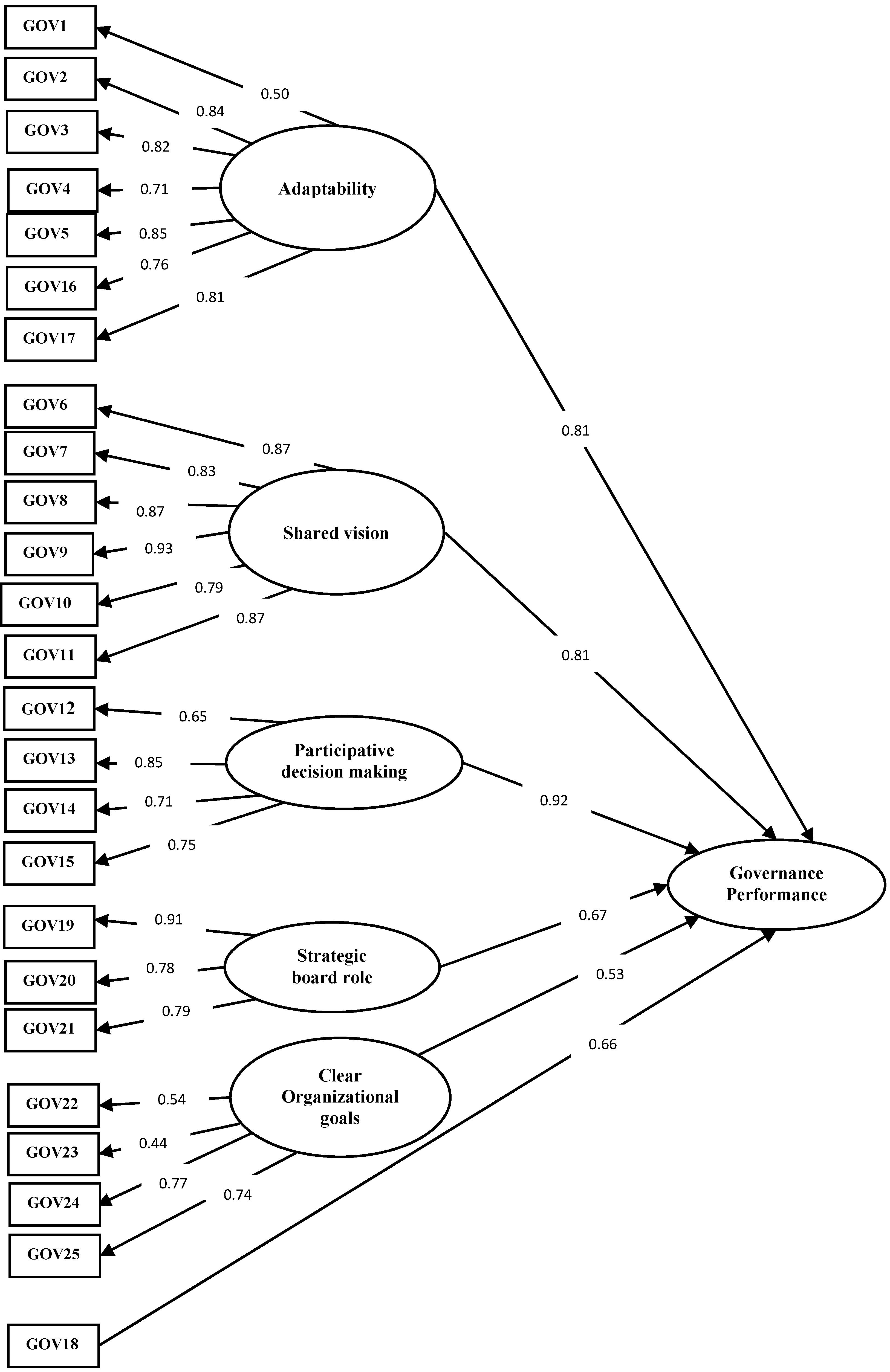

3.5.5. Governance Performance

| Adaptation of the composition of the board | |

| GOV1 | New board member are selected to meet the organization's changing needs Adaptation based on Herman and Renz (2004) [82] |

| Adaptation to changes in the environment Adaptation based on Jackson and Holland (1998) [83] | |

| GOV2 | The board of directors is able to cope with changes in the legal environment. |

| GOV3 | The board of directors is able to cope with changes in the economic environment. |

| GOV4 | The board of directors is able to cope with changes in the political environment. |

| GOV5 | The board of directors is able to cope with changes in the needs of stakeholders. |

| Engagement of board members toward the mission and vision of the organization Fredette and Bradshaw (2012) [84] | |

| GOV6 | Board members share the same ambitions and vision for the organization. |

| GOV7 | Board members enthusiastically pursue collective goals and mission. |

| GOV8 | Board members are committed to the goals of the organization. |

| GOV9 | Board members view themselves as partners in charting the organization direction. |

| GOV10 | There is a commonality of purpose among board members of this organization. |

| GOV11 | Everyone in the board of directors is in total agreement on our organization's vision. |

| Participative decision-making Li and Hambrick (2005) [85] | |

| GOV12 | All the board members have a voice in major decisions. |

| GOV13 | Communications among board members can best be described as open and fluid. |

| GOV14 | When major decisions are made, board members collectively exchange their points of view. |

| GOV15 | Board members frequently share their experience and expertise. |

| Clarity of roles Gill et al. (2005) [86] | |

| GOV16 | Board members demonstrate clear understanding of the respective roles of the board and CEO |

| Preparedness to learn from mistakes Jackson and Holland (1998) [83] | |

| GOV17 | In the board of directors we discuss about what we can learn from a mistake we have made |

| External communication to stakeholders Jackson and Holland (1998) [83] | |

| GOV18 | This board communicates its decisions to everyone who is affected by them |

| GOV19 | The board is actively involved in long-term strategic decision-making |

| GOV20 | The board is actively involved in implementing long-term strategic decision-making |

| GOV21 | The board is actively involved in promoting strategic initiatives |

| Goals meeting the needs of the stakeholders Rettab et al. (2009) [73] | |

| GOV22 | The goals of our organization meet the needs and requests of all our stakeholders |

| Clear organizational mission and goals Wright (2007) [88] | |

| GOV23 | It is easy to explain the goals of this organization to outsiders |

| GOV24 | This organization's mission is clear to everyone who works here |

| GOV25 | This organization has clearly defined goals |

| Independent board members Hillman et al. (2000) [89], Haynes and Hillman (2010) [90] | |

| GOV26 * | Does the organization has outside, independent directors? |

| G1 Shared Vision | G2 Adaptability | G3 Strategic Board Role | G4 Participative Decision-Making | G5 Clear Organizational Goals | |

|---|---|---|---|---|---|

| GOV1 | 0.127 | 0.553 | 0.140 | 0.071 | 0.003 |

| GOV2 | 0.184 | 0.834 | 0.210 | 0.184 | 0.077 |

| GOV3 | 0.210 | 0.764 | 0.315 | 0.082 | 0.158 |

| GOV4 | 0.174 | 0.789 | 0.044 | 0.099 | 0.156 |

| GOV5 | 0.237 | 0.771 | 0.236 | 0.161 | 0.166 |

| GOV6 | 0.781 | 0.259 | 0.171 | 0.191 | 0.095 |

| GOV7 | 0.799 | 0.232 | 0.108 | 0.121 | 0.162 |

| GOV8 | 0.761 | 0.154 | 0.176 | 0.293 | 0.228 |

| GOV9 | 0.784 | 0.309 | 0.200 | 0.231 | 0.045 |

| GOV10 | 0.876 | 0.167 | 0.060 | 0.105 | 0.123 |

| GOV11 | 0.874 | 0.215 | 0.083 | 0.177 | 0.111 |

| GOV12 | 0.402 | 0.143 | 0.154 | 0.567 | 0.076 |

| GOV13 | 0.656 | 0.320 | 0.072 | 0.454 | 0.018 |

| GOV14 | 0.369 | 0.265 | 0.070 | 0.658 | 0.042 |

| GOV15 | 0.421 | 0.279 | 0.210 | 0.569 | −0.002 |

| GOV16 | 0.280 | 0.722 | 0.103 | 0.130 | 0.098 |

| GOV17 | 0.286 | 0.554 | 0.212 | 0.454 | 0.042 |

| GOV18 | 0.247 | 0.501 | 0.007 | 0.482 | 0.099 |

| GOV19 | 0.277 | 0.302 | 0.693 | 0.328 | 0.141 |

| GOV20 | 0.150 | 0.264 | 0.866 | 0.064 | 0.078 |

| GOV21 | 0.140 | 0.253 | 0.889 | 0.093 | 0.103 |

| GOV22 | 0.005 | −0.041 | 0.134 | 0.508 | 0.540 |

| GOV23 | 0.014 | 0.083 | 0.066 | 0.036 | 0.690 |

| GOV24 | 0.288 | 0.145 | 0.048 | −0.025 | 0.810 |

| GOV25 | 0.169 | 0.188 | 0.065 | 0.066 | 0.769 |

3.5.6. Overview of Selected Indicators Based on the Results of the Exploratory and Confirmatory Factor Analyses

| Economic performance | |

| Innovation | Proactiveness |

| Risk taking | |

| Environmental performance | |

| Transportation | Environmental performance management |

| Ecological materials | |

| Community performance | |

| Hiring disadvantaged people | Community responsibilities |

| Human performance | |

| Performance support | Interaction between employees |

| Training & Development | Job satisfaction |

| HR-policy | Work-life balance |

| Diversity management | |

| Governance performance | |

| Shared vision | Participative decision-making |

| Adaptability of the board | Clear organizational goals |

| Strategic board role | External communication to stakeholders |

4. Discussion and Conclusion

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix

| Global Reporting Initiative (GRI) | Kinder, Lydenberg, Domini (KLD) | ISO 26000 | Dow Jones Sustainability Index (DJSI) | |

|---|---|---|---|---|

| Economic | X | X Part of “Product” | X | |

| Environmental | X | X | X | X |

| Community | X Part of “Category social”: Human rights Product Responsibility Society | X Encompassing: Human Rights Product Community | X Encompassing: Human Rights Fair Operation Practices Consumer issues Community Involvement and Development | X Part of “Social dimension” |

| Human | X Part of “Category social”: Labour practices and decent work | X Encompassing: Employee relations Diversity | X Labour Practices | X Part of “Social dimension” |

| Governance | X Part of “General standard disclosures” | X | X | X Part of “Economic dimension” |

| Journals screened on articles with “Social” and “Performance” in the title. Period: 1990–2013 |

| Part 1: |

| Academy of Management Journal |

| Academy of Management Review |

| Administrative Science Quarterly |

| Business Ethics Quarterly |

| Entrepreneurship: Theory & Practice |

| Journal of Management |

| Journal of Management Studies |

| Organizational Science |

| Organizational Studies |

| Strategic Management Journal |

| Part 2: |

| Journal of Business Ethics |

| Social Enterprise Journal |

References and Notes

- Manetti, G. The role of blended value accounting in the evaluation of socio-economic impact of social enterprises. VOLUNTAS: Int. J. Volunt. Nonprofit Organ. 2014, 25, 443–464. [Google Scholar] [CrossRef]

- Grieco, C.; Michelini, L.; Iasevoli, G. Measuring value creation in social enterprises: A cluster analysis of social impact assessment models. Nonprofit Volunt. Sect. Q. 2014, 44, 1173–1193. [Google Scholar] [CrossRef]

- Arvidson, M.; Lyon, F. Social impact measurement and non-profit organisations: Compliance, resistance, and promotion. VOLUNTAS: Int. J. Volunt. Nonprofit Organ. 2014, 25, 869–886. [Google Scholar] [CrossRef]

- Mair, J.; Marti, I. Social entrepreneurship research: A source of explanation, prediction, and delight. J. World Bus. 2006, 41, 36–44. [Google Scholar] [CrossRef]

- Moss, T.W.; Short, J.C.; Payne, G.T.; Lumpkin, G.T. Dual identities in social ventures: An exploratory study. Entrepren. Theor. Pract. 2011, 35, 805–830. [Google Scholar] [CrossRef]

- Santos, F.M. A positive theory of social entrepreneurship. J. Bus. Ethics 2012, 111, 335–351. [Google Scholar] [CrossRef]

- Wilson, F.; Post, J.E. Business models for people, planet (& profits): Exploring the phenomena of social business, a market-based approach to social value creation. Small Bus. Econ. 2013, 40, 715–737. [Google Scholar]

- Arena, M.; Azzone, G.; Bengo, I. Performance measurement for social enterprises. VOLUNTAS: Int. J. Volunt. Nonprofit Organ. 2015, 26, 649–672. [Google Scholar] [CrossRef]

- Doherty, B.; Haugh, H.; Lyon, F. Social enterprises as hybrid organizations: A review and research agenda. Int. J. Manag. Rev. 2014, 16, 417–436. [Google Scholar] [CrossRef]

- Smith, W.K.; Gonin, M.; Besharov, M.L. Managing social-business tensions: A review and research agenda for social enterprise. Bus. Ethics Q. 2013, 23, 407–442. [Google Scholar] [CrossRef]

- Pache, A.-C.; Santos, F. Inside the hybrid organization: Selective coupling as response to conflicting institutional logics. Acad. Manag. J. 2013, 56, 972–1001. [Google Scholar] [CrossRef]

- Battilana, J.; Metin, S.; Pache, A.-C.; Jacob, M. Harnessing productive tensions in hybrid organizations: The case of work integration social enterprises. Acad. Manag. J. 2014, 34, 81–100. [Google Scholar] [CrossRef]

- Miller, T.L.; Grimes, M.G.; McMullen, J.S.; Vogus, T.J. Venturing for others with heart and head: How compassion encourages social entrepreneurship. Acad. Manag. Rev. 2012, 37, 616–640. [Google Scholar] [CrossRef]

- Ebrahim, A.; Battilana, J.; Mair, J. The governance of social enterprises: Mission drift and accountability challenges in hybrid organizations. Res. Organ. Behav. 2014, 34, 81–100. [Google Scholar] [CrossRef]

- Ramus, T.; Vaccaro, A. Stakeholders matter: How social enterprises address mission drift. J. Bus. Ethics 2014, 1–16. [Google Scholar] [CrossRef]

- Battilana, J.; Lee, M. Advancing research on hybrid organizing—insights from the study of social enterprises. Acad. Manag. Ann. 2014, 8, 397–441. [Google Scholar] [CrossRef]

- Mair, J.; Mayer, J.; Lutz, E. Navigating institutional plurality: Organizational governance in hybrid organizations. Organ. Stud. 2015, 36, 713–739. [Google Scholar] [CrossRef]

- Spear, R.; Cornforth, C.; Aiken, M. The governance challenges of social enterprises: Evidence from a uk empirical study. Ann. Public Cooper. Econ. 2009, 80, 247–273. [Google Scholar] [CrossRef]

- Pache, A.-C.; Santos, F. When worlds collide: The internal dynamics of organizational responses to conflicting institutional demands. Acad. Manag. Rev. 2010, 35, 455–476. [Google Scholar] [CrossRef]

- Boyne, G.A. Performance management: Does it work? In Public Management and Performance; Walker, R.M., Boyne, G.A., Brewer, G.A., Eds.; Cambridge University Press: Cambridge, UK, 2010; pp. 207–226. [Google Scholar]

- Meadows, M.; Pike, M. Performance management for social enterprises. Syst. Pract. Action Res. 2010, 23, 127–141. [Google Scholar] [CrossRef]

- Ebrahim, A.; Rangan, V.K. What impact? A framework for measuring the scale and scop of social performance. Calif. Manag. Rev. 2014, 56, 118–141. [Google Scholar] [CrossRef]

- Nicholls, A. ‘We do good things, don’t we?’: ‘Blended value accounting’ in social entrepreneurship. Account. Organ. Soc. 2009, 34, 755–769. [Google Scholar] [CrossRef]

- Bellucci, M.; Bagnoli, L.; Biggeri, M.; Rinaldi, V. Performance measurement in solidarity economy organizations: The case of fair trade shops in italy. Ann. Publ. Cooper. Econ. 2012, 83, 25–59. [Google Scholar] [CrossRef]

- Bagnoli, L.; Megali, C. Measuring performance in social enterprises. Nonprofit Volunt. Sect. Q. 2011, 40, 149–165. [Google Scholar] [CrossRef]

- Van Loon, J.H.M.; Bonham, G.S.; Peterson, D.D.; Schalock, R.L.; Claes, C.; Decramer, A.E.M. The use of evidence-based outcomes in systems and organizations providing services and supports to persons with intellectual disability. Eval. Program Plann. 2013, 36, 80–87. [Google Scholar] [CrossRef] [PubMed]

- GRI. Global reporting initiative. Available online: https://www.globalreporting.org/resourcelibrary/GRIG4-Part1-Reporting-Principles-and-Standard-Disclosures.pdf (accessed on 3 February 2016).

- Dumay, J.; Guthrie, J.; Farneti, F. Gri sustainability reporting guidelines for public and third sector organizations. Publ. Manag. Rev. 2010, 12, 531–548. [Google Scholar] [CrossRef]

- GRI. Ngo sector disclosures. Available online: https://www.globalreporting.org/resourcelibrary/GRI-G4-NGO-Sector-Disclosures.pdf (accessed on 3 February 2016).

- Heras-Saizarbitoria, I.; Casadesús, M.; Marimón, F. The impact of iso 9001 standard and the efqm model: The view of the assessors. Total Qual. Manag. Bus. Excel. 2011, 22, 197–218. [Google Scholar] [CrossRef]

- DeVellis, R.F. Scale Development: Theory and Applications; Sage: Thousand Oaks, CA, USA, 2003. [Google Scholar]

- Hinkin, T.R. A review of scale development practices in the study of organizations. J. Manag. 1995, 21, 967–988. [Google Scholar] [CrossRef]

- Hinkin, T.R. A brief tutorial on the development of measures for use in survey questionnaires. Organ. Res. Meth. 1998, 1, 104–121. [Google Scholar] [CrossRef]

- Van Opstal, W.; Deraedt, E.; Gijselinckx, C. Monitoring profile shifts and differences among wises in flanders. Soc. Enterp. J. 2009, 5, 229–258. [Google Scholar] [CrossRef] [Green Version]

- Defourny, J.; Nyssens, M. Conceptions of social enterprise and social entrepreneurship in europe and the united states: Convergences and divergences. J. Soc. Entrepreneurship 2010, 1, 32–53. [Google Scholar] [CrossRef]

- Defourny, J.; Nyssens, M. Social enterprise in europe: Recent trends and developments. Soc. Enterp. J. 2008, 4, 202–228. [Google Scholar] [CrossRef]

- Wood, D.J. Measuring corporate social performance: A review. Int. J. Manag. Rev. 2010, 12, 50–84. [Google Scholar] [CrossRef]

- Laplume, A.O.; Sonpar, K.; Litz, R.A. Stakeholder theory: Reviewing a theory that moves us. J. Manag. 2008, 34, 1152–1189. [Google Scholar] [CrossRef]

- Consolandi, C.; Jaiswal-Dale, A.; Poggiani, E.; Vercelli, A. Global standards and ethical stock indexes: The case of the dow jones sustainability stoxx index. J. Bus. Ethics 2009, 87, 185–197. [Google Scholar] [CrossRef]

- Robinson, M.; Kleffner, A.; Bertels, S. Signaling sustainability leadership: Empirical evidence of the value of djsi membership. J. Bus. Ethics 2011, 101, 493–505. [Google Scholar] [CrossRef]

- Hahn, R.; Lulfs, R. Legitimizing negative aspects in gri-oriented sustainability reporting: A qualitative analysis of corporate disclosure strategies. J. Bus. Ethics 2014, 123, 401–420. [Google Scholar] [CrossRef]

- Levy, D.L.; Szejnwald Brown, H.; de Jong, M. The contested politics of corporate governance: The case of the global reporting initiative. Bus. Soc. 2010, 49, 88–115. [Google Scholar] [CrossRef]

- Helms, W.S.; Oliver, C.; Webb, K. Antecedents of settlement on a new institutional practice: Negotiation of the iso 26000 standard on social responsibility. Acad. Manag. J. 2012, 55, 1120–1145. [Google Scholar] [CrossRef]

- Balzarova, M.A.; Castka, P. Stakeholders’ influence and contribution to social standards development: The case of multiple stakeholder approach to iso 26000 development. J. Bus. Ethics 2012, 111, 265–279. [Google Scholar] [CrossRef]

- Wiklund, J.; Shepherd, D. Entrepreneurial orientation and small business performance: A configurational approach. J. Bus. Venturing 2005, 20, 71–91. [Google Scholar] [CrossRef]

- Chang, H.-T.; Chi, N.-W. Human resource managers’ role consistency and hr performance indicators: The moderating effect of interpersonal trust in taiwan. Int. J. Hum. Resour. Manag. 2007, 18, 665–683. [Google Scholar] [CrossRef]

- Andersson, L.; Jackson, S.E.; Russell, S.V. Greening organizational behavior: An introduction to the special issue. J. Organ. Behav. 2013, 34, 151–155. [Google Scholar] [CrossRef]

- Niehm, L.S.; Swinney, J.; Miller, N.J. Community social responsibility and its consequences for family business performance. J. Small Bus. Manag.t 2008, 46, 331–350. [Google Scholar] [CrossRef]

- Cornforth, C. Nonprofit governance research: The need for innovative perspectives and approaches. In Nonprofit Governance, Innovative Perspectives and Approaches; Cornforth, C., Brown, W.A., Eds.; Routledge: Abingdon, UK, 2014; pp. 1–14. [Google Scholar]

- Hambrick, D.C.; Werder, A.; Zajac, E.J. New directions in corporate governance research. Organ. Sci. 2008, 19, 381–385. [Google Scholar] [CrossRef]

- Daily, C.M.; Dalton, D.R.; Cannella, A.A. Corporate governance: Decades of dialogue and data. The Acad. Manag. Rev. 2003, 28, 371–382. [Google Scholar]

- Chan, M.C.; Watson, J.; Woodliff, D. Corporate governance quality and csr disclosures. J. Bus. Ethics 2014, 125, 59–73. [Google Scholar] [CrossRef]

- Huang, C.J. Corporate governance, corporate social responsibility and corporate performance. J. Manag. Organ. 2010, 16, 641–655. [Google Scholar] [CrossRef]

- Arora, P.; Dharwadkar, R. Corporate governance and corporate social responsibility (csr): The moderating roles of attainment discrepancy and organization slack. Corp. Govern. Int. Rev. 2011, 19, 136–152. [Google Scholar] [CrossRef]

- Cowton, C.J.; Downs, Y. Use of focus groups in business ethics research: Potential, problems and paths to progress. Bus. Ethics Eur. Rev. 2015, 24, S54–S66. [Google Scholar] [CrossRef]

- Bruggen, E.; Willems, P. A critical comparison of offline focus groups, online focus groups and e-delphi. Int. J. Market Res. 2009, 51, 363–381. [Google Scholar] [CrossRef]

- Caffey, R.H.; Kazmierczak, R.F.; Avault, J.W. Developing Consensus Indicators of Sustainability for Southeastern United States Aquaculture; Louisiana Agricultural Experiment Station, LSU Agricultural Center: Baton Rouge, LA; USA, 2001. [Google Scholar]

- Landeta, J. Current validity of the delphi method in social sciences. Technol. Forecast. Soc. Change 2006, 73, 467–482. [Google Scholar] [CrossRef]

- Okoli, C.; Pawlowski, S.D. The delphi method as a research tool: An example, design considerations and applications. Inf. Manag. 2004, 42, 15–29. [Google Scholar] [CrossRef] [Green Version]

- Schmidt, R.C. Managing delphi surveys using nonparametric statistical techniques*. Decis. Sci. 1997, 28, 763–774. [Google Scholar] [CrossRef]

- Rowe, G.; Wright, G.; McColl, A. Judgment change during delphi-like procedures: The role of majority influence, expertise, and confidence. Technol. Forecast. Soc. Change 2005, 72, 377–399. [Google Scholar] [CrossRef]

- Von Der Gracht, H.A. Consensus measurement in delphi studies: Review and implications for future quality assurance. Technol. Forecast. Soc. Change 2012, 79, 1525–1536. [Google Scholar] [CrossRef]

- Worrell, J.L.; Di Gangi, P.M.; Bush, A.A. Exploring the use of the delphi method in accounting information systems research. Int. J. Account. Inform. Syst. 2013, 14, 193–208. [Google Scholar] [CrossRef]

- Spear, R. Governance in democratic member-based organisations. Ann. Publ. Cooper. Econ. 2004, 75, 33–59. [Google Scholar] [CrossRef]

- Janssens, W.; Wijnen, K.; De Pelsmacker, P.; Van Kenhove, P. Marketing Research with SPSS; Prentice Hall: London, UK, 2008. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis; Pearson: Upper Saddle River NJ, USA, 2006. [Google Scholar]

- Rosseel, Y. Lavaan: An r package for structural equation modeling. J. Stat. Software 2012, 48, 1–36. [Google Scholar] [CrossRef]

- Brown, T. Confirmatory Factor Analysis for Applied Research; The Guilford Press: Londen, UK, 2006. [Google Scholar]

- Hu, L.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Struct. Equ. Model. Multidiscip. J. 1999, 6, 1–55. [Google Scholar] [CrossRef]

- Helm, S.T.; Andersson, F.O. Beyond taxonomy. An empirical validation of social entrepreneurship in the nonprofit sector. Nonprofit Manag. Leader. 2010, 20, 259–276. [Google Scholar] [CrossRef]

- Mishra, S.; Suar, D. Does corporate social responsibility influence firm performance of indian companies? J. Bus. Ethics 2010, 95, 571–601. [Google Scholar] [CrossRef]

- Chen, J.; Patten, D.M.; Roberts, R. Corporate charitable contributions: A corporate social performance or legitimacy strategy? J. Bus. Ethics 2008, 82, 131–144. [Google Scholar] [CrossRef]

- Rettab, B.; Brik, A.; Mellahi, K. A study of management perceptions of the impact of corporate social responsibility on organisational performance in emerging economies: The case of dubai. J. Bus. Ethics 2009, 89, 371–390. [Google Scholar] [CrossRef]

- O’Connor, M.; Spangenberg, J.H. A methodology for csr reporting: Assuring a representative diversity of indicators across stakeholders, scales, sites and performance issues. J. Clean. Prod. 2008, 16, 1399–1415. [Google Scholar] [CrossRef]

- Graafland, J.; Eijffinger, S.C.W.; SmidJohan, H. Benchmarking of corporate social responsibility: Methodological problems and robustness. J. Bus. Ethics 2004, 53, 137–152. [Google Scholar] [CrossRef]

- CAF. Common assessment framework. Available online: http://www.eipa.eu/files/File/CAF/CAF_2013.pdf (accessed on 3 February 2016).

- Calantone, R.J.; Cavusgil, S.T.; Zhao, Y. Learning orientation, firm innovation capability, and firm performance. Ind. Market. Manag. 2002, 31, 515–524. [Google Scholar] [CrossRef]

- ISO26000. Available online: https://www.iso.org/obp/ui/#iso:std:iso:26000:ed-1:v1:en (accessed on 3 February 2016).

- De la Cuesta-González, M.; Muñoz-Torres, M.; Fernández-Izquierdo, M.Á. Analysis of social performance in the spanish financial industry through public data. A proposal. J. Bus. Ethics 2006, 69, 289–304. [Google Scholar] [CrossRef]

- Heslin, P.A.; Vandewalle, D.O.N.; Latham, G.P. Keen to help? Managers’ implicit person theories and their subsequent employee coaching. Person. Psychol. 2006, 59, 871–902. [Google Scholar] [CrossRef]

- Milkie, M.A.; Peltola, P. Playing all the roles: Gender and the work-family balancing act. J. Marriage Fam. 1999, 61, 476–490. [Google Scholar] [CrossRef]

- Herman, R.D.; Renz, D.O. Doing things right: Effectiveness in local nonprofit organizations, a panel study. Publ. Admin. Rev. 2004, 64, 694–704. [Google Scholar] [CrossRef]

- Jackson, D.K.; Holland, T.P. Measuring the effectiveness of nonprofit boards. Nonprofit Volunt. Sect. Q. 1998, 27, 159–182. [Google Scholar] [CrossRef]

- Fredette, C.; Bradshaw, P. Social capital and nonprofit governance effectiveness. Nonprofit Manag. Leadersh. 2012, 22, 391–409. [Google Scholar] [CrossRef]

- Li, J.; Hambrick, D.C. Factional groups: A new vantage on demographic faultlines, conflict, and disintegration in work teams. Acad. Manag. J. 2005, 48, 794–813. [Google Scholar] [CrossRef]

- Gill, M.; Flynn, R.J.; Reissing, E. The governance self-assessment checklist: An instrument for assessing board effectiveness. Nonprofit Manag. Leadersh. 2005, 15, 271–294. [Google Scholar] [CrossRef]

- Minichilli, A.; Zattoni, A.; Zona, F. Making boards effective: An empirical examination of board task performance. Br. J. Manag. 2009, 20, 55–74. [Google Scholar] [CrossRef] [Green Version]

- Wright, B.E. Public service and motivation: Does mission matter? Publ. Admin. Rev. 2007, 67, 54–64. [Google Scholar] [CrossRef]

- Hillman, A.J.; Cannella, J.A.A.; Paetzold, R.L. The resource dependence role of corporate directors: Strategic adaptation of board composition in response to environmental change. J. Manag. Stud. 2000, 37, 235–255. [Google Scholar] [CrossRef]

- Haynes, K.T.; Hillman, A. The effect of board capital and ceo power on strategic change. Strat. Manag. J. 2010, 31, 1145–1163. [Google Scholar] [CrossRef]

- Claes, C.; Van Hove, G.; van Loon, J.; Vandevelde, S.; Schalock, R.L. Quality of life measurement in the field of intellectual disabilities: Eight principles for assessing quality of life-related personal outcomes. Soc. Indic. Res. 2010, 98, 61–72. [Google Scholar] [CrossRef]

- KLD. Kld Ratings Data: Inclusive Social Rating Criteria; KLD Research & Analytics, Inc.: Boston, Masachusetts, USA, 2003. [Google Scholar]

- DJSI. The Dow Jones Sustainability World Index Guide; S&P Dow Jones Indices LLC: New York, USA, 2012. [Google Scholar]

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons by Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Crucke, S.; Decramer, A. The Development of a Measurement Instrument for the Organizational Performance of Social Enterprises. Sustainability 2016, 8, 161. https://doi.org/10.3390/su8020161

Crucke S, Decramer A. The Development of a Measurement Instrument for the Organizational Performance of Social Enterprises. Sustainability. 2016; 8(2):161. https://doi.org/10.3390/su8020161

Chicago/Turabian StyleCrucke, Saskia, and Adelien Decramer. 2016. "The Development of a Measurement Instrument for the Organizational Performance of Social Enterprises" Sustainability 8, no. 2: 161. https://doi.org/10.3390/su8020161

APA StyleCrucke, S., & Decramer, A. (2016). The Development of a Measurement Instrument for the Organizational Performance of Social Enterprises. Sustainability, 8(2), 161. https://doi.org/10.3390/su8020161