Quantifying a Financially Sustainable Strategy of Public Transport: Private Capital Investment Considering Passenger Value

Abstract

:1. Introduction

2. Private Capital Investment Models in the Transportation Industry

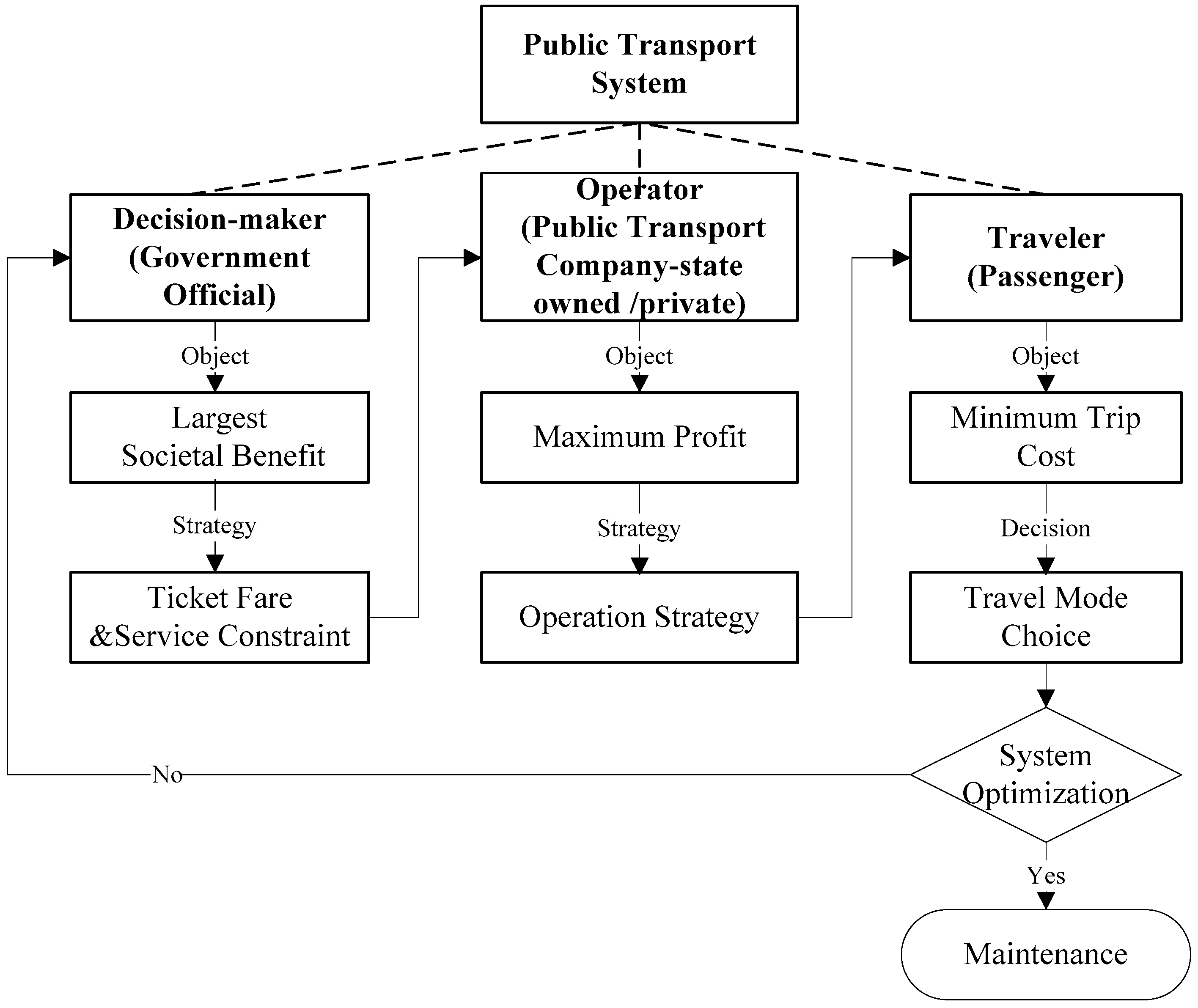

3. The Investment Model in Public Transport Considering Passenger Value

4. BLPM of Private Capital Investment in Public Transport

- public transport operator’s surplus;

- ticket price of route i;

- passenger flow of route i;

- total passenger flow of public transport;

- subsidy of route i;

- other benefit of route i;

- the operation cost without private capital investment under departure frequency F;

- surplus of travelers, equal to the cost bus travelers are willing to pay for the service minus the actual cost, minus the travel cost of car users. This means the fewer car users the better, although it is not compulsory for travelers to drop private cars.

- public transport travel demand under O-D (origin-destination) pair s and t, which is a function of ticket price and bus service;

- the inverse function of public transport demand, reflects the corresponding price and service corresponding to demand D;

- returns to passengers ‘Q’ by the private capital enterprise;

- the travel cost of private car from origination s to destination t;

- the travel flow of private car from origination s to destination t;

- m: the number of total public transit lines;

- n: the number of state-owned lines, n ≤ m;

- trip cost of travelers under private capital investment type S (in the paper S means lease);

- volume of route i;

- volume of private car from origination s to destination t;

- generalized travel cost of route i;

- generalized travel cost of private car from origination s to destination t;

- travel time value of the bus (yuan/hour);

- travel time by bus;

- wait time value of the bus (yuan/hour);

- wait time of the bus;

- walk time value of the bus (yuan/hour);

- walk time of the bus;

- travel time value of the BRT (yuan/hour);

- travel time of the BRT;

- wait time value of the BRT (yuan/hour);

- wait time of the BRT

- walk time value of the BRT (yuan/hour);

- walk time of the BRT;

- travel time value of the subway (yuan/hour);

- travel time of the subway;

- wait time value of the subway (yuan/hour);

- wait time of the subway;

- walk time value of the subway;

- walk time of the subway;

- travel time value of private car users;

- travel time of private car from s to t.

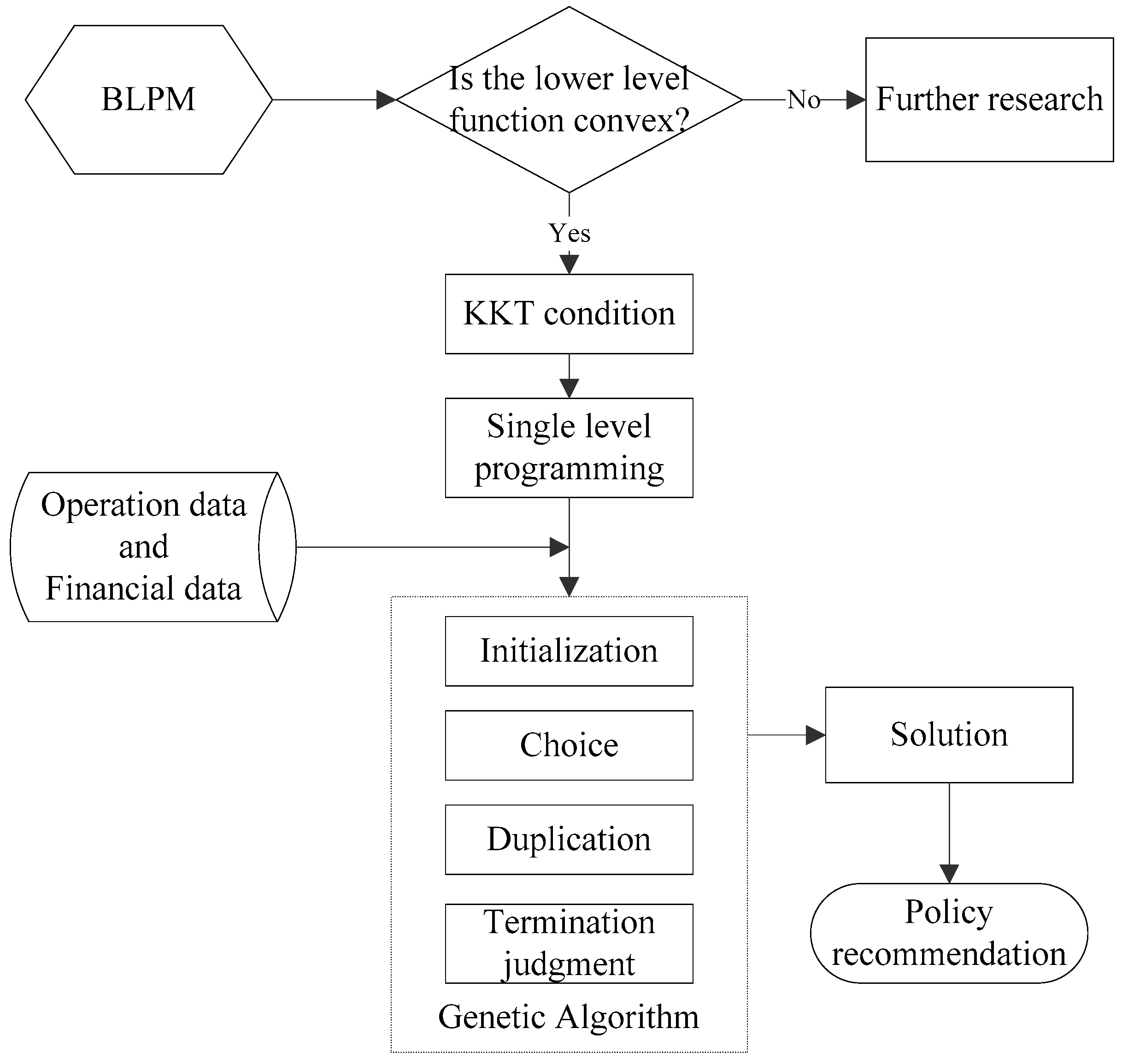

5. Solution Algorithm

6. Case Study

7. Discussion and Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Malandraki, G.; Papamichail, L.; Papageorgiou, M.; Dinopoulou, V. Simulation and Evaluation of a Public Transport Priority Methodology. Trans. Res. Procedia 2015, 6, 402–410. [Google Scholar] [CrossRef]

- Jara, D.; Gschwender, A.; Ortega, M. The impact of a financial constraint on the spatial structure of public transport services. Transportation 2014, 41, 21–36. [Google Scholar] [CrossRef]

- Xue, Y.; Guan, H.; Corey, J.; Qin, H.; Han, Y.; Ma, J. Bi-level Programming Model of Private Capital Investment in Urban Public Transportation: Case Study of Jinan City. Math. Probl. Eng. 2015, 2015, 1–12. [Google Scholar] [CrossRef]

- Chan, A.; Lam, P.; Chan, D.; Cheung, E.; Ke, Y. Privileges and attractions for private sector involvement in PPP projects. Chall. Oppor. Solut. Struct. Eng. Constr. 2010, 2010, 751–755. [Google Scholar]

- Cox, W. Competitive Participation in U.S. Public Transport: Special Interests versus the Public Interest. In Proceedings of the 8th International Conference on Competition and Ownership in Land Passenger Transport, Rio de Janeiro, Brazil, 15–18 September 2003.

- Daube, D.; Vollrath, S.; Alfen, H. A Comparison of Project Finance and the Forfeiting Model as financing forms for PPP projects in Germany. Int. J. Proj. Manag. 2008, 26, 376–387. [Google Scholar] [CrossRef]

- Costa, A.; Fernandes, R. Urban public transport in Europe: Technology diffusion and market organisation. Transp. Res. A 2012, 46, 269–284. [Google Scholar] [CrossRef]

- Matsunaka, R.; Tetsuharu, O.; Nakagawa, D.; Nagao, M.; Nawrocki, J. International comparison of the relationship between urban structure and the service level of urban public transportation—A comprehensive analysis in local cities in Japan, France and Germany. Transp. Policy 2013, 30, 26–39. [Google Scholar] [CrossRef] [Green Version]

- Medda, F.R.; Carbonaro, G.; Davis, S.L. Public private partnerships in transportation: Some insights from the European experience. IATSS Res. 2013, 36, 83–87. [Google Scholar] [CrossRef]

- Lu, Y. Research on the Reform of Marketization in Urban Public Transport Industry; Economy & Management Publishing House: Beijing, China, 2014. [Google Scholar]

- Rossi, M.; Civitillo, R. Public Private Partnerships: A general overview in Italy, in 2nd World Conference on Business, Economics and Management. WCBEM 2013, 2014, 1–10. [Google Scholar]

- Osei-Kyei, R.; Chan, A.P.C. Review of studies on the Critical Success Factors for Public-Private Partnership (PPP) projects from 1990 to 2013. Int. J. Proj. Manag. 2015, 33, 1335–1346. [Google Scholar] [CrossRef]

- English, L.M. Public Private Partnerships in Australia: An Overview of Their Nature, Purpose, Incidence and Oversight. UMSW Law J. 2006, 29, 250–263. [Google Scholar]

- World Bank; Asian Development Bank; Inter-American Development Bank. Public-Private Partnerships Reference Guide—Version 2.0; World Bank Group: Washington, DC, USA, 2014. [Google Scholar]

- De Los Rios-Carmenado, I.; Ortuno, M.; Rivera, M. Private-Public Partnership as a Tool to Promote Entrepreneurship for Sustainable Development: WWP Torrearte Experience. Sustainability 2016, 8, 199. [Google Scholar] [CrossRef]

- Bidne, D.; Kirby, A.; Luvela, L.J.; Shattuck, B.; Standley, S.; Welker, S. The Value for Money Analysis: A Guide for More Effective PSC and PPP Evaluation; American University: Washington, DC, USA, 2013; pp. 1–60. [Google Scholar]

- Ho, P.H.K. Development of Public Private Partnerships (PPPs) in China. Surv. Times 2006, 15, 1–5. [Google Scholar]

- Takim, R.; Ismail, K.; Nawawi, A.; Jaafar, A. The Malaysian Private Finance Initiative and Value for Money. Asian Soc. Sci. 2009, 5, 103–111. [Google Scholar] [CrossRef]

- Jung, S.; Huynh, D.; Rowe, P.G. The pattern of foreign property investment in Vietnam: The apartment market in Ho Chi Minh City. Habitat Int. 2013, 39, 105–113. [Google Scholar] [CrossRef] [Green Version]

- Fox, E.M. An Anti-Monopoly Law for China-Scaling the Walls of Protectionist Administrative Restraints. Antitrust Law J. 2007, 74, 1–31. [Google Scholar]

- Mu, R.; de Jong, M.; Koppenjan, J. The rise and fall of Public-Private Partnerships in China: A path-dependent approach. J. Transp. Geogr. 2011, 19, 794–806. [Google Scholar] [CrossRef]

- Zhang, S.; Gao, Y.; Feng, Z.; Sun, W. PPP application in infrastructure development in China: Institutional analysis and implications. Int. J. Proj. Manag. 2015, 33, 497–509. [Google Scholar] [CrossRef]

- Chang, Z. Financing new metros-The Beijing metro financing sustainability study. Transp. Policy 2014, 32, 148–155. [Google Scholar] [CrossRef]

- Soomro, M.A.; Zhang, X. An Analytical Review on Transportation Public Private Partnerships Failures. Int. J. Sustain. Constr. Eng. Technol. 2011, 2, 62–80. [Google Scholar]

- Soomro, M.A.; Zhang, X. Failure Links between Public and Private Sector Partners in Transportation Public Private Partnerships Failures. J. Traffic Logist. Eng. 2013, 1, 116–121. [Google Scholar] [CrossRef]

- Soomro, M.A.; Zhang, X. Evaluation of the Functions of Public Sector Partners in Transportation Public-Private Partnerships Failures. J. Manag. Eng. 2015, 32, 1–11. [Google Scholar] [CrossRef]

- Zhang, X.; Soomro, M.A. Failure Path Analysis with Respect to Private Sector Partners in Transportation Public-Private Partnerships. J. Manag. Eng. 2015, 32, 1–10. [Google Scholar] [CrossRef]

- Winston, C. Government Failure in Urban Transportation. Fiscal Stud. 2000, 21, 403–425. [Google Scholar] [CrossRef]

- Murthi, M.; Orszag, J.M.; Orszag, P.R. The Value for Money of Annuities in the UK: Theory, Experience and Policy; World Bank: Washington DC, USA, 1994. [Google Scholar]

- Nisar, T.M. Value for money drivers in public private partnership schemes. Int. J. Public Sect. Manag. 2007, 20, 147–156. [Google Scholar] [CrossRef]

- Soomro, M.A.; Zhang, X. Value for Money Drivers in Transportation Public Private Partnerships. In Proceedings of the 24th International Project Management Association (IPMA) World Congress, Istanbul, Turkey, 1–3 November 2010; pp. 1–6.

- Berger, P.; Hawkesworth, I. How To Attain Value for Money: Comparing PPP and Traditional Infrastructure Public Procurement. OECD J. Budg. 2011, 1, 1–56. [Google Scholar] [CrossRef]

- European PPP Expertise Centre (EPEC). Value for Money Assessment; European PPP Expertise Centre: Luxembourg, 2015. [Google Scholar]

- Mounter, N.; Annema, J.A.; van Wee, B. Managing the insolvable limitations of cost-benefit analysis: Results of an interview based study. Transportation 2015, 42, 277–302. [Google Scholar] [CrossRef]

- Proost, S.; Dunkerley, F.; van der Loo, S.; Adler, N.; Brocker, J.; Korzhenevych, A. Do the selected Trans European transport investments pass the cost benefit test? Transportation 2014, 41, 107–132. [Google Scholar] [CrossRef]

- Macario, R. Future challenges for transport infrastructure pricing in PPP arrangements. Res. Transp. Econ. 2010, 30, 145–154. [Google Scholar] [CrossRef]

- Morallos, D.; Amekudzi, A. A Review of Value-for-Money Analysis for Comparing Public-Private Partnerships with Traditional Procurements. In Proceedings of the Transportation Research Board 87th Annnual Meeting, Washington, DC, USA, 13–17 January 2008; pp. 1–13.

- Peng, W. Achieving Value for Money: An Analytic Review of Studies on Public Private Partnerships. Constr. Res. Congr. 2014, 2014, 1–10. [Google Scholar]

- Yang, H.; Kong, H.Y.; Meng, Q. Value-of-time distributions and competitive bus services. Transp. Res. E 2001, 37, 411–424. [Google Scholar] [CrossRef]

- Pedro, A.L.A. The economic value of bus subsidy. Transp. Res. Procedia 2013, 8, 247–258. [Google Scholar]

- Wan, X.; Chen, J.; Wang, W. Travel Characteristics and Mode Choice Behavior of Public Transport in China. Int. Conf. Transp. Eng. 2009, 2009, 1–6. [Google Scholar]

- Tang, R.; Sun, H. Discussion on involvement modes and fields of private capital introducted into transportation industry. Financ. Acc. Commun. 2012, 8, 10–16. [Google Scholar]

- Cruz, C.O.; Marques, R.C. Infrastructure Public-Private Partnerships: Decision, Management and Development; Springer: Berlin, Germany, 2013. [Google Scholar]

- Xu, S. Applying Pubic-Private-Partnership to Chinese Subway Infrastructure; Delft University of Technology: Delft, The Netherlands, 2008. [Google Scholar]

- Percoco, M. Quality of institutions and private participation in transport infrastructure investment: Evidence from developing countries. Transp. Res. A 2014, 70, 50–58. [Google Scholar] [CrossRef]

- Seybold, P.B. The Customer Revolution: How to Thrive When Customers Are in Control; Crown Business: New York, NY, USA, 2001. [Google Scholar]

- Verhoef, P.C.; Lemon, K.N. Successful customer value management: Key lessons and emerging trends. Eur. Manag. J. 2013, 31, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Kahreh, M.; Tive, M.; Babania, A.; Hesan, M. Analyzing the applications of customer lifetime value (CLV) based on benefit segmentation for the banking sector. Procedia Soc. Behabioral Sci. 2014, 109, 590–594. [Google Scholar] [CrossRef]

- Ulaga, W.; Chacour, S. Measuring customer-perceived value in business markets: A prerequisite for marketing strategy development and implementation. Ind. Mark. Mana. 2001, 30, 525–540. [Google Scholar] [CrossRef]

- Brown, S.A. Customer Relationship Management: A Strategy Imperative in the World of E-Business; John Wiley & Sons: New York, NY, USA, 2000. [Google Scholar]

- Gerpott, T.J.; Rams, W.; Schindler, A. Customer retention, loyalty, and satisfaction in the German mobile cellular telecommunication market. Telecommun. Policy 2001, 25, 249–269. [Google Scholar] [CrossRef]

- Chou, J.S.; Yeh, C.P. Influential constructs, mediating effects, and moderating effects on operations performance of high speed rail from passenger perspective. Transp. Policy 2013, 30, 207–219. [Google Scholar] [CrossRef]

- Wong, W.G.; Han, B.M.; Ferreira, L.; Zhu, X.N.; Sun, Q. Evaluation of management strategies for the operation of high-speed railways in China. Transp. Res. A Policy Pract. 2002, 36, 277–289. [Google Scholar] [CrossRef] [Green Version]

- Xue, X. White Book of Jinan Public Traffic Development in Year 2011; Jinan Urban Transport Research Center: Jinan, China, 2012. [Google Scholar]

- Wei, M.; Sun, B.; Jin, W. A Bi-level Programming Model for Uncertain Regional Bus Scheduling Problems. J. Transp. Syst. Eng. Inf. Technol. 2013, 13, 106–113. [Google Scholar] [CrossRef]

- Zhao, X.; Yang, J. Research on the Bi-level Programming Model for Ticket fare pricing of Urban Rail Transit Based on Particle Swarm Optimization Algorithm. In Proceedings of the 13th COTA International Conference of Transportation Professionals, Shenzhen, China, 13–16 August 2013; pp. 633–642.

- Moshe, B.-A.; Bierlaire, M. Discrete Choice Analysis: The Theory and Application on Travel Demand; MIT Press: Cambridge, MA, USA, 2010. [Google Scholar]

- Train, K.E. Discrete Choice Methods with Simulation, 2nd ed.; Cambridge University Press: Cambridge, UK, 2009. [Google Scholar]

- Li, J.; Lai, X.; Yu, Z. A paired combinatorial logit route choice model with probit-based equivalent i mpedance. J. Transp. Syst. Eng. Inf. Technol. 2013, 13, 100–105. [Google Scholar]

- Zhang, G. Enhanced traffic information dissemination to facilitate toll road utilizaiton: A nested logit model of a stated preference survey in Texas. Transportation 2014, 41, 231–249. [Google Scholar] [CrossRef]

- Paulssen, M. Values, attitudes and travel behavior: A hierarchical latent variable mixed logit model of travel mode choice. Transportation 2014, 41, 873–888. [Google Scholar] [CrossRef]

- Colson, B. Mathematical Programs with Equilibrium Constraints and Nonlinear Bi-Level Programming Problems; University of Namur: Namur, Belgium, 1999. [Google Scholar]

- Colson, B.; Marcotte, P.; Savard, G. A trust-region method for nonlinear programming: Algorithm and computational experience. Cumput. Optim. Appl. 2005, 30, 211–227. [Google Scholar] [CrossRef]

- Colson, B.; Marcotte, P.; Savard, G. An overview of bilevel optimization. Ann. Oper. Res. 2007, 153, 235–256. [Google Scholar] [CrossRef]

- Yokota, T.; Gen, M.; Li, Y.; Kim, C.E. A genetic algorithm for interval nonlinear integer programming problem. Comput. Ind. Eng. 1996, 31, 913–917. [Google Scholar] [CrossRef]

- Demps, S. Foundation of Bi-Level Programming; Kluwer Academic Publishers: Dordrecht, The Netherlands, 2003. [Google Scholar]

- Baky, I.A. Solving multi-level multi-objective linear programming problems through fuzzy goal programming approach. Appl. Math. Model. 2010, 34, 2377–2387. [Google Scholar] [CrossRef]

- Tang, J.; Zhang, G.; Wang, Y.; Wang, H.; Liu, F. A hybrid approach to integrate fuzzy C-means based imputation method with genetic algorithm for missing traffic volume data estimation. Transp. Res. C 2015, 51, 29–40. [Google Scholar] [CrossRef]

- Yang, H.; Bell, M.G. Transport bi-level programming problems: Recent methodological advances. Transp. Res. B Methodol. 2001, 35, 1–4. [Google Scholar] [CrossRef]

- Jinan, B.O.S. Jinan Statistical Year Book 2015; China Statistic Press: Beijing, China, 2016. [Google Scholar]

- Xue, Y.; Guan, H.; Qin, H.; Liu, T.; Gong, L. The study on key factors influencing public transport share rate based on disaggregate model-Jinan as an example. In Proceedings of the 14th COTA International Conference of Transportation Professionals, Changsha, China, 4–7 July 2014; pp. 1–13.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| PPP Category | PPP Contract | Description |

|---|---|---|

| Management and lease contracts | Management contract | The government pays a private operator to manage the facility. The operational risk remains with the government |

| Lease contract | The government leases the assets to a private operator for a fee. The private operator takes on the operational risk | |

| Concessions | Rehabilitate, operate, and transfer (ROT) | A private sponsor rehabilitates an existing facility, then operates and maintains the facility at its own risk for the contract period |

| Rehabilitate, lease or rent, and transfer (RLT) | A private sponsor rehabilitates an existing facility at its own risk, leases or rents the facility from the government owner, then operates and maintains the facility at its own risk for the contract period | |

| Build, lease, and transfer (BROT) | A period developer builds an add-on to an existing facility or completes a partially built facility and rehabilitates existing assets, then operates and maintains the facility at its own risk for the contract period | |

| Greenfield projects | Build, lease, and transfer (BLT) | A private sponsor builds a new facility largely at its own risk, transfers ownership to the government, leases the facility from the government and operates it at its own risk until expiry of the lease. The government usually provides revenue guarantees through long-term take-or-pay contracts for bulk supply facilities or minimum traffic revenue guarantees |

| Build, operate, and transfer (BOT) | A private sponsor builds a new facility at its own risk, operates the facility at its own risk, and then transfers the facility to the government at the end of the contract period. The private sponsor may or may not have ownership of the assets during the contract period. The government usually provides revenue guarantees through long-term take-or-pay contracts for bulk supply facilities or minimum traffic revenue guarantees | |

| Build, own, and operate (BOO) | A private sponsor builds a new facility at its own risk, then owns and operates the facility at its own risk. The government usually provides revenue guarantees through long-term take-or-pay contracts for bulk supply facilities or minimum traffic revenue guarantees | |

| Merchant | A private sponsor builds a new facilities in a liberalized market in which the government provides no revenue guarantees. The private developer assumes construction, operating, and market risk for the project (for example, a merchant power plant) | |

| Rental | Electricity utilities or governments rent mobile power plants from private sponsors for periods ranging from one year to 15 years. A private sponsor builds a new facility at its own risk, owns and operates the facility at its own risk during the contract period. The government usually provides revenue guarantees through short-term purchase agreements such as a power purchase agreement for bulk supply facilities | |

| Divestitures | Full | The government transfer 100% of the equity in the state-owned company to private entities (operator, institutional investors, and the like) |

| Partial | The government transfers part of the equity in the state-owned company to private entities (operator, institutional investors, and the like). The private stake may or may not imply private management of the facility |

| Not Considering Passenger Value | Considering Passenger Value | |

|---|---|---|

| Benefits of private capital company | Ticket fares | Ticket fares |

| Profits of cash flow in accounts (bank interest) | Profits of cash flow in accounts (investment profit) | |

| Advertisement profits (bus body and platform ads) | Advertisement profits (bus body and platform ads, e-commerce ads) | |

| Government subsidies | Government subsidies | |

| Costs of private capital company | Fixed cost (including the involvement fees) | Fixed cost (including the involvement fees) |

| Variable cost | Variable cost, returns to passengers |

| Parameter | Value | Parameter | Value | Parameter | Value | Parameter 1 | Value |

|---|---|---|---|---|---|---|---|

| 1 yuan | 15 vehicles | 30 yuan/hour | –0.1 | ||||

| 3 yuan | 20 vehicles | 35 yuan/hour | –0.08 | ||||

| 2 yuan | 15 km/hour | 1 yuan/trip | –0.06 | ||||

| 5 yuan | 25 km/hour | 3 yuan/vehicle·km | –0.15 | ||||

| 1 yuan/km | 4 km/hour | 5 yuan/vehicle·km | –0.1 | ||||

| 4 buses/hour | 35 km/hour | 20 yuan | –0.2 | ||||

| 15 buses/hour | 20 yuan/hour | 100 yuan/day | –0.15 | ||||

| 6 buses/hour | 25 yuan/hour | 0.5 | –0.12 | ||||

| 20 buses/hour | 25 yuan/hour | 6% | –0.1 | ||||

| 50 people/vehicle | 25 yuan/hour | 10% | –0.08 | ||||

| 70 people/vehicle | 30 yuan/hour | Q | 1500 trip | Qcar | 500 |

| Car Competition | Situation of Private Capital Investment | Bus Ticket Price (Yuan) | BRT Ticket Price (Yuan) | Bus Departure Frequency (Bus/Hour) | BRT Departure Frequency (BRT/Hour) | Objective Value (Yuan) |

|---|---|---|---|---|---|---|

| Without car competition | Without private capital | 1 | 2 | 15 | 20 | 2737 |

| Traditional investment | 1 | 2 | 15 | 20 | 3457 | |

| Investment with returns | 1 | 2 | 15 | 20 | 3488 | |

| Consider car competition | Without private capital | 1 | 2 | 15 | 20 | 2271 |

| Traditional investment | 1 | 2 | 15 | 20 | 2371 | |

| Investment with returns | 1 | 2 | 15 | 20 | 2396 |

| Passenger Flow | Bus Ticket Price (Yuan) | BRT Ticket Price (Yuan) | Bus Departure Frequency (Bus/Hour) | BRT Departure Frequency (BRT/Hour) | Objective Value (Yuan) |

|---|---|---|---|---|---|

| 200 | 1 | 2 | 15 | 20 | Not satisfied |

| 300 | 1 | 2 | 15 | 20 | 428 |

| 1000 | 1 | 2 | 15 | 20 | 1358 |

| Return Ratio of Account Benefits | Bus Ticket Price (Yuan) | BRT Ticket Price (Yuan) | Bus Departure Frequency (Bus/Hour) | BRT Departure Frequency (BRT/Hour) | Objective Value (Yuan) |

|---|---|---|---|---|---|

| 0.0 | 1 | 2 | 15 | 20 | 2371.6 |

| 0.2 | 1 | 2 | 15 | 20 | 2381.7 |

| 0.4 | 1 | 2 | 15 | 20 | 2391.7 |

| 0.9 | 1 | 2 | 15 | 20 | 2416.9 |

| 1.0 | 1 | 2 | 15 | 20 | Not satisfied |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xue, Y.; Guan, H.; Corey, J.; Wei, H.; Yan, H. Quantifying a Financially Sustainable Strategy of Public Transport: Private Capital Investment Considering Passenger Value. Sustainability 2017, 9, 269. https://doi.org/10.3390/su9020269

Xue Y, Guan H, Corey J, Wei H, Yan H. Quantifying a Financially Sustainable Strategy of Public Transport: Private Capital Investment Considering Passenger Value. Sustainability. 2017; 9(2):269. https://doi.org/10.3390/su9020269

Chicago/Turabian StyleXue, Yunqiang, Hongzhi Guan, Jonathan Corey, Heng Wei, and Hai Yan. 2017. "Quantifying a Financially Sustainable Strategy of Public Transport: Private Capital Investment Considering Passenger Value" Sustainability 9, no. 2: 269. https://doi.org/10.3390/su9020269

APA StyleXue, Y., Guan, H., Corey, J., Wei, H., & Yan, H. (2017). Quantifying a Financially Sustainable Strategy of Public Transport: Private Capital Investment Considering Passenger Value. Sustainability, 9(2), 269. https://doi.org/10.3390/su9020269