An Empirical Research of FDI Spillovers and Financial Development Threshold Effects in Different Regions of China

Abstract

:1. Introduction

2. Literature Review

3. Model and Data

3.1. Framework and Model

3.2. The Principle of Estimating and Testing the Thresholds

3.3. Data and Variables

4. Empirical Analyses

4.1. Test and Estimate Threshold Values

4.2. Regression Results

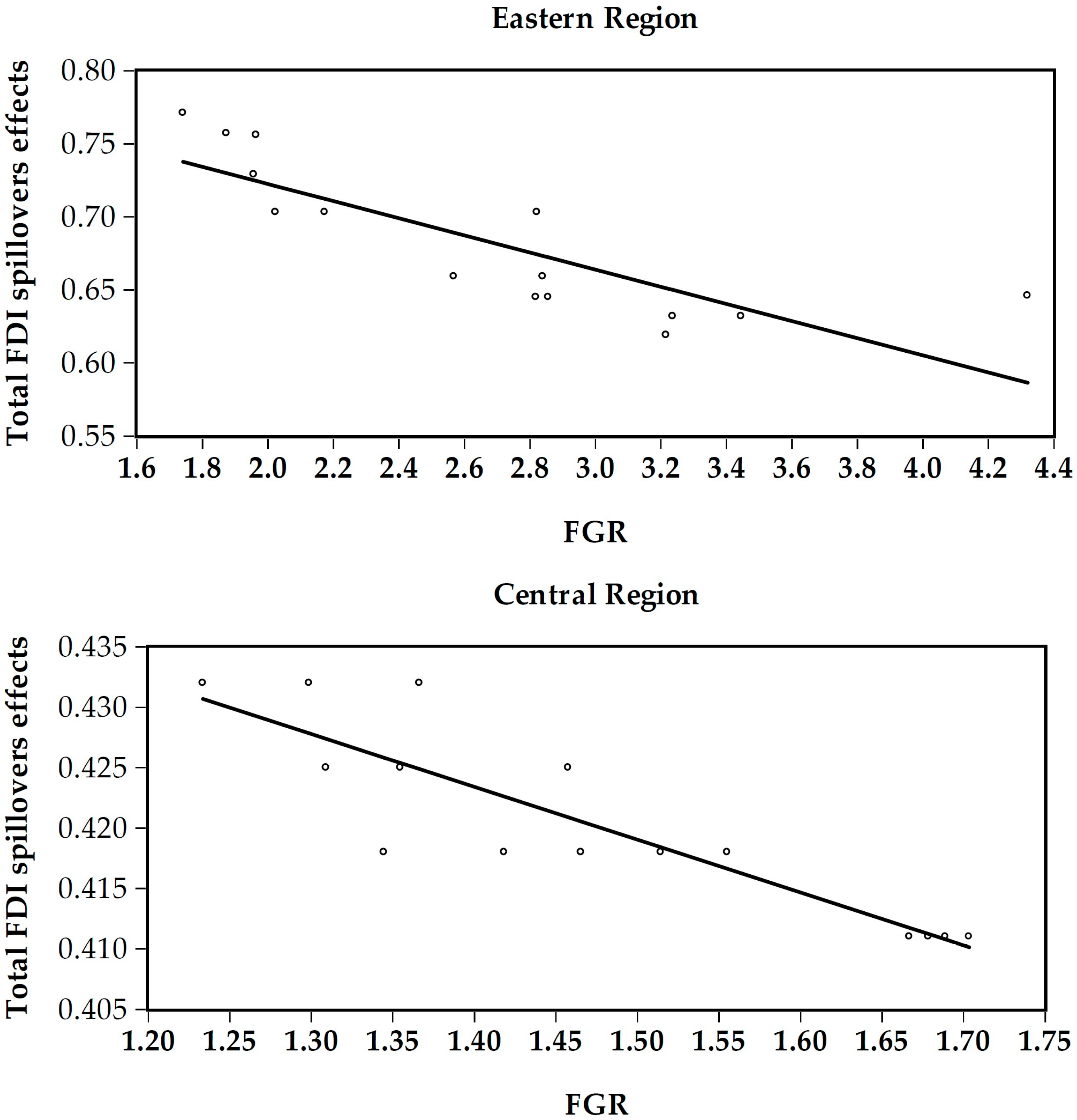

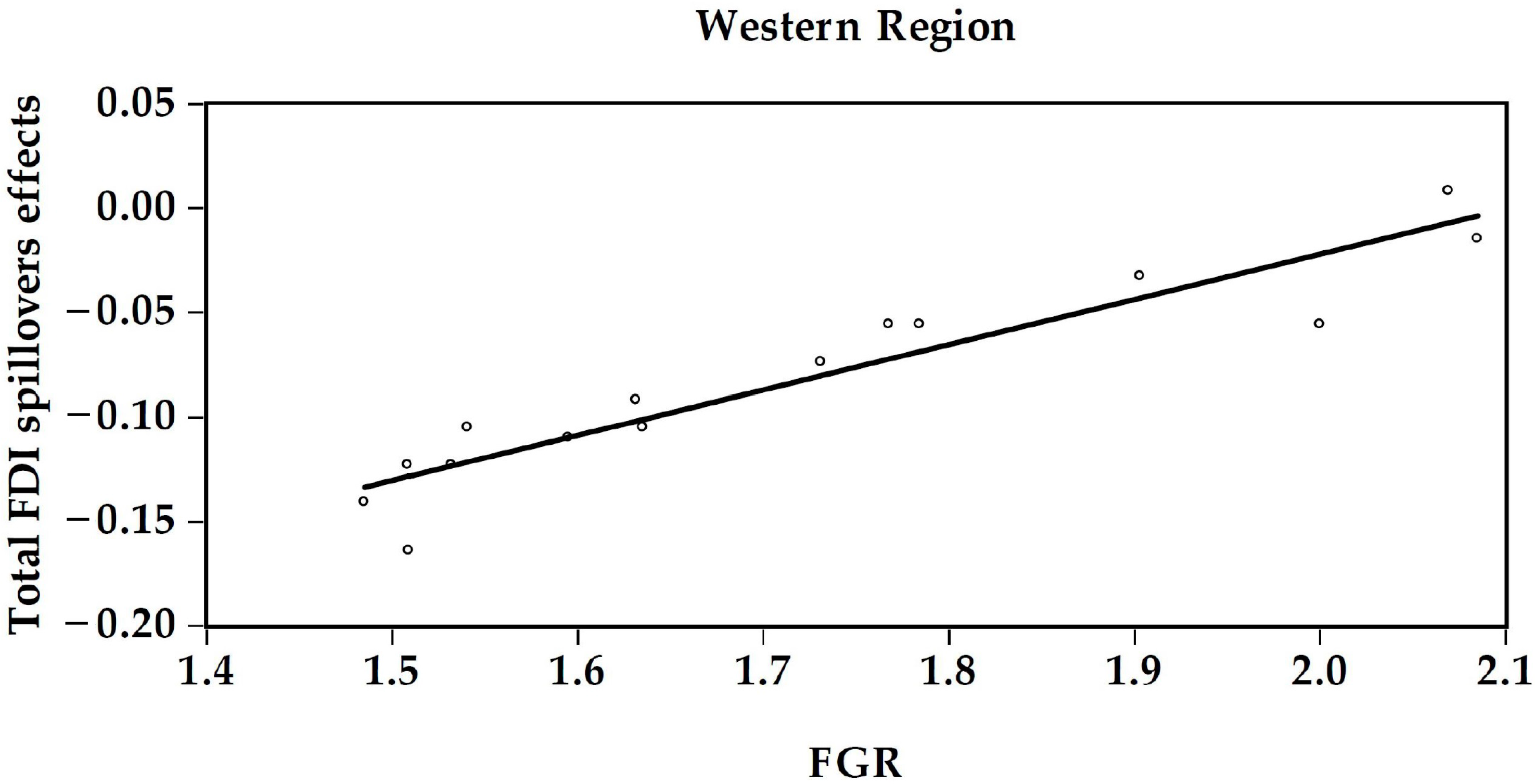

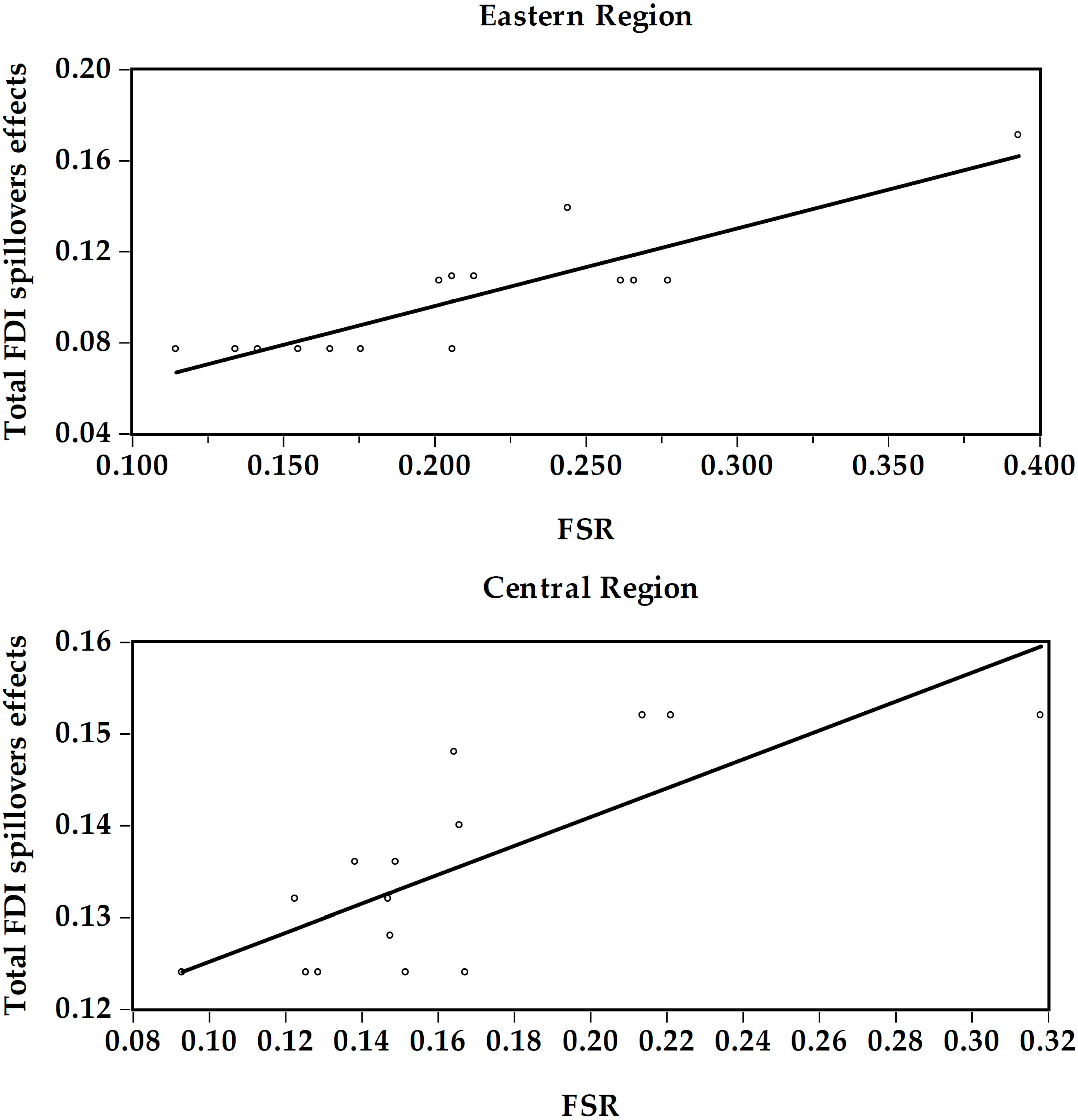

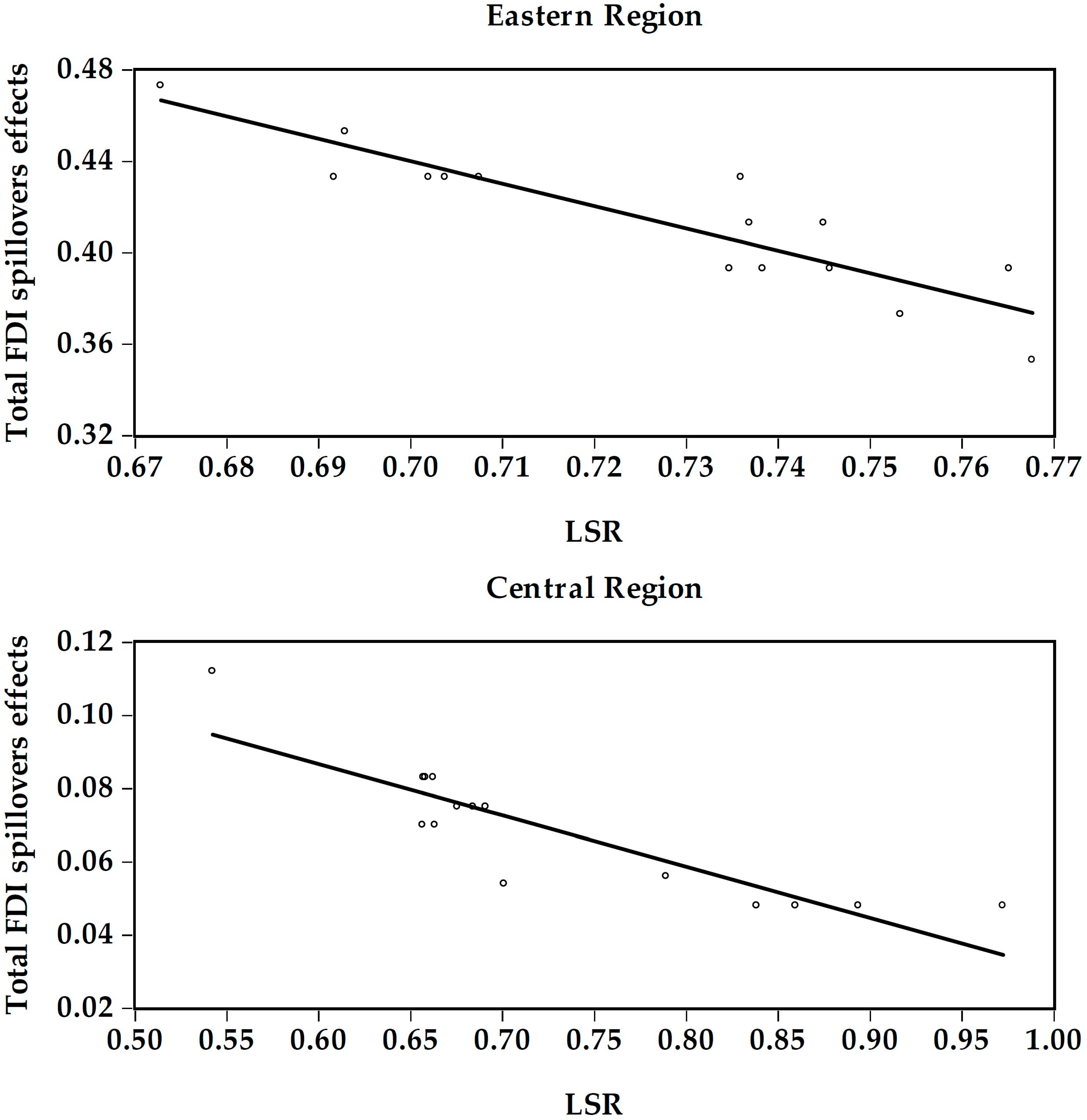

4.3. Discussion of the Results

5. Conclusions and Policy Recommendations

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

References

- United Nations Conference on Trade and Development. Available online: http://unctad.org/en/Pages/MeetingDetails.aspx?meetingid=743 (accessed on 24 June 2015).

- National Bureau of Statistics of the People’s Republic of China. Available online: http://www.stats.gov.cn/tjsj/ndsj/2015/indexch.htm (accessed on 17 October 2015). (In Chinese)

- Zhang, J.H.; Ouyang, Y.W. Foreign direct investment, the spillover effect and economic growth—A case of Guangdong province. China Econ. 2003, 2, 647–666. (In Chinese) [Google Scholar]

- Findlay, R. Relative backwardness, direct foreign investment, and the transfer of technology: A simple dynamic model. Q. J. Econ. 1978, 92, 1–16. [Google Scholar] [CrossRef]

- Koizumi, T.; Kopecky, K.J. Foreign direct investment, technology transfer and domestic employment effects. J. Int. Econ. 1980, 10, 1–20. [Google Scholar] [CrossRef]

- Kokko, A. Technology, market characteristics, and spillovers. J. Dev. Econ. 1994, 43, 279–293. [Google Scholar] [CrossRef]

- Colombo, M.G.; Mosconi, R. Complementarity and cumulative learning effects in the early diffusion of multiple technologies. J. Ind. Econ. 1995, 43, 13–48. [Google Scholar] [CrossRef]

- Caves, R.E. International corporations: The industrial economics of foreign investment. Economica 1971, 38, 1–27. [Google Scholar] [CrossRef]

- Wang, J.Y.; Blomström, M. Foreign investment and technology transfer: A simple model. Eur. Econ. Rev. 1992, 36, 137–155. [Google Scholar] [CrossRef]

- Dasb, S. Externalities and technology transfer through multinational corporations: A theoretical analysis. J. Int. Econ. 1987, 22, 171–182. [Google Scholar]

- Görg, H.; Strobl, E. Multinational companies and productivity spillovers: A meta-analysis. Econ. J. 2001, 111, 723–739. [Google Scholar] [CrossRef]

- Jiang, D.C.; Xia, L.K. The Empirical Study of the Function of FDI on Innovation in China’s High-Tech Industries. World Econ. 2005, 8, 3–10. (In Chinese) [Google Scholar]

- Savvides, A.; Zachariadis, M. International technology diffusion and the growth of TFP in the manufacturing sector of developing economies. Rev. Dev. Econ. 2005, 9, 482–501. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive Capacity: A New Perspective on Learning and Innovation. Adm. Sci. Q. 1990, 35, 39–67. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Innovation and Learning: The Two Faces of R&D. Econ. J. 1989, 99, 569–596. [Google Scholar]

- Borensztein, E.; Gregorio, J.D.; Lee, J.W. How does foreign direct investment affect economic growth? Nber Work. Pap. 1995, 45, 115–135. [Google Scholar] [CrossRef]

- Haskel, J.E.; Slaughter, M.J. Does Inward Foreign Direct Investment Boost the Productivity of Domestic Firms? Rev. Econ. Stat. 2007, 89, 482–496. [Google Scholar] [CrossRef]

- Qi, J.H.; Wei, Q.G.; Ju, L. FDI, Financial Market and Economic Growth: Regional Differences and threshold Effect. Rev. Ind. Econ. 2009, 8, 91–106. (In Chinese) [Google Scholar]

- Li, M.; Liu, S.C. The regional differences and the threshold effect of the OFDI: The regression analysis based on the threshold of the Chinese provincial panel data. Manag. World 2012, 1, 21–32. (In Chinese) [Google Scholar]

- Yong, K.L.; Liu, Y. The Contribution of Inward FDI to Chinese Regional Innovation: The Moderating Effect of Absorptive Capacity on Knowledge Spillover. Eur. J. Int. Manag. 2016, 3, 284–313. [Google Scholar]

- Alfaro, L.; Chanda, A.; Kalemli-Ozcan, S.; Sayek, S. FDI and economic growth: The role of local financial markets. SSRN Electron. J. 2003, 64, 89–112. [Google Scholar]

- Zhang, L.; Ran, G.H.; Chen, Q. Regional financial strength, FDI spillover and the real economy Growth: A research based on the panel threshold model. Econ. Sci. 2014, 6, 76–89. (In Chinese) [Google Scholar]

- Macodougall, G.D.A. The benefits and costs and costs of private investment from abroad: A theoretical approach. Oxf. Bull. Econ. Stat. 1960, 36, 13–35. [Google Scholar] [CrossRef]

- Caves, R.E. Multinational firms, competition, and productivity in host-country markets. Economic 1974, 41, 176–193. [Google Scholar] [CrossRef]

- Blomström, M.; Persson, H. Foreign investment and spillover efficiency in an underdeveloped economy: Evidence from the Mexican manufacturing industry. World Dev. 1983, 11, 493–501. [Google Scholar] [CrossRef]

- Hu, X.J.; Wen, L.Q. Empirical research on technology spillover effects of FDI to domestic firms of auto industry in China. J. Hunan Univ. 2009, 3, 60–64. (In Chinese) [Google Scholar]

- Du, L.; Harrison, A.; Jefferson, G.H. Testing for horizontal and vertical foreign investment spillovers in China, 1998–2007. J. Asian Econ. 2012, 23, 234–243. [Google Scholar] [CrossRef]

- Mao, Z.X.; Yang, Y. FDI spillovers in the Chines hotel industry: The role of geographic regions, star-rating classifications, ownership types, and foreign capital origins. Tour. Manag. 2016, 54, 1–12. [Google Scholar] [CrossRef]

- Liu, W.S.; Agbola, F.W.; Dzator, J.A. The impact of FDI spillover effects on total factor productivity in the Chinese electronic industry: A panel data analysis. J. Asia Pac. Econ. 2016, 2, 217–234. [Google Scholar] [CrossRef]

- Aitken, B.J.; Harrison, A.E. Do domestic firms benefit from direct foreign investment? Evidence from Venezuela. Am. Econ. Rev. 1999, 89, 605–618. [Google Scholar] [CrossRef]

- Javorcik, B.S. Does foreign direct investment increase the productivity of domestic firms? In search of spillovers through backward linkages. Am. Econ. Rev. 2004, 94, 605–627. [Google Scholar] [CrossRef]

- Pattnayak, S.S.; Thangavelu, S.M. Linkages and technology spillovers in the presence of foreign firms. J. Econ. Stud. 2011, 38, 275–286. [Google Scholar] [CrossRef]

- Suyanto; Ruhul, S. Foreign direct investment spillovers and technical efficiency in the Indonesian pharmaceutical sector: Firm level evidence. Appl. Econ. 2013, 45, 383–395. [Google Scholar]

- Lichtenberg, F.R. International R&D spillovers: A re-examination. Anal. Chem. 1996, 55, 245–246. [Google Scholar]

- Djankov, S.; Hoekman, B. Foreign investment and productivity growth in Czech enterprises. World Bank Econ. Rev. 2000, 14, 49–64. [Google Scholar] [CrossRef]

- Driffield, N. The impact on domestic productivity of inward investment in the UK. Manch. Sch. 2001, 69, 103–119. [Google Scholar] [CrossRef]

- Goldsmith, R.W. Financial structure and development. Stud. Comp. Econ. 1969, 70, 31–45. [Google Scholar]

- Beck, T.H.L.; Levine, R.; Loayza, N.V. Financial intermediary development and growth: Causes and causality. J. Monet. Econ. 2000, 46. [Google Scholar] [CrossRef]

- Aghion, P.; Howitt, P.; Mayerfoulkes, D. The effect of financial development on convergence: Theory and evidence. Q. J. Econ. 2004, 120, 173–222. [Google Scholar]

- Vlachos, J.; Waldenström, D. International financial liberalization and industry growth. Int. J. Financ. Econ. 2005, 10, 263–284. [Google Scholar] [CrossRef]

- Habibullah, M.S.; Eng, Y.K. Does financial development cause economic growth? A panel data dynamic analysis for the Asian developing countries. J. Asia Pac. Econ. 2006, 11, 377–393. [Google Scholar] [CrossRef]

- Christopoulos, D.K.; Tsionas, E.G. Financial development and economic growth: Evidence from panel unit root and cointegration tests. Res. Financ. Econ. Issues 2007, 73, 55–74. [Google Scholar] [CrossRef]

- Hasan, R.; Barua, S. Financial development and economic growth: Evidence from a panel study on south Asian countries. Asian Econ. Financ. Rev. 2015, 10, 1159–1173. [Google Scholar]

- Valickova, P.; Havranek, T.; Horvath, R. Financial development and economic growth: A meta-analysis. J. Econ. Surv. 2015, 3, 506–526. [Google Scholar] [CrossRef]

- Boulila, G.; Trabelsi, M. Financial development and long-run growth: Evidence from Tunisia: 1962–1997. Sav. Dev. 2004, 28, 289–314. [Google Scholar]

- Kim, Y.C. Does financial development precede growth? Robinson and Lucas might be right. Appl. Econ. Lett. 2007, 14, 15–19. [Google Scholar]

- Chakraborty, I. Does financial development cause economic growth? The case of India. South Asia Econ. J. 2008, 9, 109–139. [Google Scholar] [CrossRef]

- Shan, J.Z.; Morris, A.G.; Fiona, S. Financial development and economic growth: An egg-and-chicken problem? Rev. Int. Econ. 2001, 5, 514. [Google Scholar] [CrossRef]

- Calderón, C.; Liu, L. The direction of causality between financial development and economic growth. J. Dev. Econ. 2003, 72, 321–334. [Google Scholar] [CrossRef]

- Caporale, G.M.; Rault, C.; Sova, A.D.; Sova, R. Financial development and economic growth: Evidence from 10 new European Union members. Int. J. Financ. Econ. 2015, 1, 48–60. [Google Scholar] [CrossRef]

- Aghion, P.; Bacchetta, P.; Banerjee, A. Financial development and the instability of open economies. J. Monet. Econ. 2004, 51, 1077–1106. [Google Scholar] [CrossRef]

- Li, J.W. Foreign direct investment and economic growth: The role of the financial markets. Contemp. Financ. Econ. 2007, 1, 27–30. (In Chinese) [Google Scholar]

- Liu, S.J. FDI and economic growth: Research based on the financial market absorption capacity. Shanghai Financ. 2007, 5, 9–12. (In Chinese) [Google Scholar]

- Sun, L.J. Financial Development, FDI and Economic Growth. J. Quant. Tech. Econ. 2008, 25, 3–14. (In Chinese) [Google Scholar]

- Alfaro, L.; Chanda, A.; Kalemli-Ozcan, S.; Sayek, S. Does foreign direct investment promote growth? Exploring the role of financial markets on linkages. J. Dev. Econ. 2006, 91, 242–256. [Google Scholar] [CrossRef]

- Chen, Y.; Feng, D. The association among the regional level of financial development, the spillover effects of FDI and economic growth in the Pearl River. J. Reg. Financ. Res. 2015, 1, 17–21. (In Chinese) [Google Scholar]

- Li, X.Y. Study on the relationship between financial development and FDI. Sci. Econ. Soc. 2016, 1, 55–59. (In Chinese) [Google Scholar]

- Ang, J.B. Financial development and the FDI growth nexus: The Malaysian experience. Appl. Econ. 2009, 41, 1595–1601. [Google Scholar] [CrossRef]

- Gungor, H.; Katircioglu, S.T. Financial development, FDI and real income growth in Turkey: An empirical investigation from bounds tests and causality analysis. Actual Probl. Econ. 2010, 12, 215–225. [Google Scholar]

- Cheng, L.W.; Yuan, M.C. Study of Nonlinear Effects of Institutional Quality and Financial Development on Transnational Capital. In Proceedings of the 7th International Conference on Financial Risk and Corporate Finance Management, Las Vegas, NV, USA, 18–20 August 2015. [Google Scholar]

- Rahman, M.M.; Shahbaz, M. Foreign Direct Investment-Economic Growth Link: The Role of Domestic Financial Sector Development in Bangladesh. Acad. Taiwan Bus. Manag. Rev. 2011, 7, 104–112. [Google Scholar]

- Anwar, S.; Cooray, A. Financial development, political rights, civil liberties and economic growth: Evidence from South Asia. Econ. Model. 2012, 29, 974–981. [Google Scholar] [CrossRef]

- Güngör, H.; Katircioglu, S.T.; Mercan, M. Revisiting the nexus between financial development, FDI, and growth: New evidence from second generation econometric procedures in the Turkish context. Acta Oecon. 2014, 64, 73–89. [Google Scholar] [CrossRef]

- Choong, C.K. Does domestic financial development enhance the linkages between foreign direct investment and economic growth? Empir. Econ. 2012, 42, 819–834. [Google Scholar] [CrossRef]

- Niels, H.; Lensink, R. Foreign direct investment, financial development and economic growth. J. Dev. Stud. 2003, 40, 142–163. [Google Scholar]

- Choong, C.K.; Yusop, Z.; Soo, S.C. Foreign Direct Investment, Economic Growth, and Financial Sector Development. J. Southeast Asian Econ. 2004, 21, 278–289. [Google Scholar]

- Li, J.C.; Zeng, H. The Relationship between FDI Spillover and Economic Growth: A Study Based on the Financial Market Development with Panel Data of Chinese Provinces. Stat. Res. 2009, 26, 30–37. [Google Scholar]

- Su, N.; Song, L.S. The influence of financial development on FDI technology spillover effect. J. Zhongnan Univ. Econ. Law 2012, 4, 54–61. (In Chinese) [Google Scholar]

- Luo, J. Threshold of financial development, FDI and regional economic growth. World Econ. Study 2016, 4, 107–118. (In Chinese) [Google Scholar]

- Jiang, X.L.; Wang, Y. The impact of financial development on FDI spillovers—Analysis based on the perspective of human capital flow. Financ. Trade Econ. 2011, 5, 65–70. (In Chinese) [Google Scholar]

- Li, B.; Li, Q.; Qi, Y. An Analysis of the Threshold Effects of the FDI Technology Spillover on the Technological Progress in the High-tech Industry. Int. Bus. 2016, 3, 74–84. (In Chinese) [Google Scholar]

- Choong, C.K.; Yusop, Z.; Law, S.H. Private Capital flows to developing countries: The role of the domestic financial sector. J. Asia Pac. Econ. 2010, 15, 509–529. [Google Scholar] [CrossRef]

- Wang, M.; Wong, M.C.S. Foreign Direct Investment and Economic Growth: The Growth Accounting Perspective. Econ. Inq. 2009, 47, 701–710. [Google Scholar] [CrossRef]

- Azman-Saini, W.N.W.; Law, S.H.; Ahmad, A.H. FDI and economic growth: New evidence on the role of financial markets. Econ. Lett. 2010, 107, 211–213. [Google Scholar] [CrossRef]

- Yao, Y.J.; Shi, W.L. FDI and TFP growth: The test of financial development threshold effect. J. Financ. Dev. Res. 2013, 2, 16–20. (In Chinese) [Google Scholar]

- Tan, L.Z.; Luo, L. Financial development and the FDI technology spillover effect: Linear or nonlinear? Jilin Univ. J. Soc. Sci. Ed. 2013, 3, 49–57. (In Chinese) [Google Scholar]

- Wu, C.; Wang, D.X.; Li, C. Financial Deepening, FDI Spillovers and Regional TFP—Empirical Analysis Based on Provincial Panel Threshold Model. J. Shanghai Financ. Univ. 2013, 4, 10–22. (In Chinese) [Google Scholar]

- Hansen, B.E. Sample Splitting and Threshold Estimation. Econometrica 2000, 68, 575–603. [Google Scholar] [CrossRef]

- Hansen, B.E. Threshold effects in non-dynamic panels: Estimation, testing, and inference. J. Econ. 1999, 93, 345–368. [Google Scholar] [CrossRef]

- Huang, L.Y.; Liu, X.M.; Xu, L. Regional innovation and spillover effects of foreign direct investment in China: A threshold approach. Reg. Stud. 2012, 5, 583–596. [Google Scholar] [CrossRef]

- Anwar, S.; Lan, P.N. Is foreign direct investment productive? A case study of the regions of Vietnam. J. Bus. Res. 2014, 67, 1376–1387. [Google Scholar] [CrossRef]

- Nowak-Lehmann, F.; Dreher, A.; Herzer, D.; Klasen, S.; Martínez-Zarzoso, I. Does foreign aid really raise per capita income? A time series perspective. Can. J. Econ. Rev. Can. D'écon. 2012, 45, 288–313. [Google Scholar] [CrossRef]

- Ubeda, F.; Pérez-Hernández, F. Absorptive capacity and geographical distance two mediating factors of FDI spillovers: A threshold regression analysis for Spanish firms. J. Ind. Compet. Trade 2017, 17, 1–28. [Google Scholar] [CrossRef]

- Girma, S. Absorptive capacity and productivity spillovers from FDI: A threshold regression analysis. Oxf. Bull. Econ. Stat. 2005, 67, 281–306. [Google Scholar] [CrossRef]

- Zhang, J.; Wu, G.Y.; Zhang, J.P. The Estimation of China’s provincial capital stock: 1952–2000. Econ. Res. J. 2004, 10, 35–44. [Google Scholar]

- Wang, H.; Liu, H.F.; Cao, Z.Y.; Wang, B.W. FDI technology spillover and threshold effect of the technology gap: Regional differences in the Chinese industrial sector. SpringerPlus 2016, 1, 323–334. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Unit | Variable Expression | Explanation |

|---|---|---|---|

| Yit | 0.1 Billion Yuan | Gross Domestic Product (GDP) | The GDP represents the total output in regions or countries. |

| FDIit | 0.1 Billion Yuan | The actual utilized foreign direct investment | 1. FDI is a stock variable; |

| 2. We take the perpetual inventory method to estimate FDI stock. The formula of FDI stock is FDIit = (1 − δ) FDIi,t-1 + fdiit, where FDIit represents the stock, fdiit represents the flow, δ represents the economic depreciation rate of stock. The economic depreciation rate is usually 9.6% which was pointed out by Zhang [85]; We use the formula of FDIi0 = fdii0/(g + δ) to estimate FDI stock in the base period. The g represents the average growth rate of FDI from 2000 to 2014; | |||

| 3. The original data are measured in dollars, so we converted it to Chinese Yuan at the average central parity rate. | |||

| Kit | 0.1 Billion Yuan | The total amount of investment in fixed assets | Capital is a stock variable and its estimation method is the same as the FDI estimation method. |

| Lit | 10,000 employees | The average annual number of employees | The total value is calculated by the sum of the average annual number of employees of the first, second, and third industries. |

| R&Dit | 0.1 Billion Yuan | Research and development expenses | R&D is a stock variable and its estimation method is the same as the FDI estimation method. |

| FGRit | percentage | The ratio of total financial assets to the amount of corresponding GDP | 1. The ratio represents the degree of scale expansion; |

| 2. The financial development scale usually refers to total financial assets, including deposit balances of all financial institutions, stock prices, bond balances and premium income. Since the bond market is relatively small, and the statistical data of bond balances are not complete in some provinces, we do not consider the impact of the bond market in the empirical process. | |||

| FSRit | percentage | The ratio of the sum of stock price and premium income to the amount of corresponding total financial assets | The ratio can represent the changes in the financial development structure to some degree. |

| LSRit | percentage | The ratio of loan balance to deposit balance of all financial institutions | There are many indicators to measure financial development efficiency. The deposit balance of all financial institutions occupies a large proportion of the total financial assets. Therefore, we use the savings and loans ratio to measure the efficiency of savings translating indirectly into investment. The ratio can represent the financial development efficiency to some degree. |

| Variables | Regions | Mean | Std. Dev. | Min | Max | Observations |

|---|---|---|---|---|---|---|

| Yit | Eastern Region | 6349.65 | 3710.44 | 526.82 | 14,652.85 | 165 |

| Central Region | 3762.23 | 1466.13 | 1843.35 | 7670.93 | 120 | |

| Western Region | 2005.27 | 1228.91 | 263.68 | 5749.71 | 165 | |

| Kit | Eastern Region | 28,791.16 | 26,951.56 | 700.45 | 131,164.3 | 165 |

| Central Region | 18,597.73 | 17,226.58 | 1523.56 | 89,010.58 | 120 | |

| Western Region | 11,302.46 | 12,246.23 | 510.1 | 66,872.13 | 165 | |

| Lit | Eastern Region | 2742.71 | 1913.39 | 335.17 | 6606.5 | 165 |

| Central Region | 3021.8 | 1467.63 | 1164.02 | 6520.03 | 120 | |

| Western Region | 1787.43 | 1219.24 | 275.5 | 4833 | 165 | |

| FDIit | Eastern Region | 3732.66 | 3195.31 | 178.02 | 13,983.34 | 165 |

| Central Region | 837.99 | 778.57 | 38.06 | 3721.59 | 120 | |

| Western Region | 296.31 | 459 | 3.35 | 2923.03 | 165 | |

| R&Dit | Eastern Region | 1286.22 | 1523.3 | 2.12 | 7088.2 | 165 |

| Central Region | 407.91 | 418.79 | 23.77 | 2104.62 | 120 | |

| Western Region | 231.07 | 353.27 | 3.99 | 2016.8 | 165 | |

| FGRit | Eastern Region | 2.66 | 2.88 | 0.39 | 24.6 | 165 |

| Central Region | 1.47 | 0.38 | 0.92 | 2.99 | 120 | |

| Western Region | 1.72 | 0.44 | 0.86 | 3.81 | 165 | |

| FSRit | Eastern Region | 0.21 | 0.15 | 0.06 | 0.84 | 165 |

| Central Region | 0.16 | 0.06 | 0.07 | 0.43 | 120 | |

| Western Region | 0.17 | 0.1 | 0.05 | 0.64 | 165 | |

| LSRit | Eastern Region | 0.76 | 0.41 | 0.51 | 5.76 | 165 |

| Central Region | 0.73 | 0.14 | 0.08 | 1.19 | 120 | |

| Western Region | 0.81 | 0.2 | 0.54 | 2.33 | 165 |

| LnY | LnK | LnL | LnR&D | LnFDI | LnFGR | LnFSR | LnLSR | |

| LnY | 1.0000 | |||||||

| LnK | 0.7856 | 1.0000 | ||||||

| LnL | 0.5875 | 0.4127 | 1.0000 | |||||

| LnR&D | 0.8104 | 0.1324 | 0.3383 | 1.0000 | ||||

| LnFDI | 0.7795 | 0.2046 | 0.2807 | 0.3036 | 1.0000 | |||

| LnFGR | −0.0380 | 0.0918 | −0.3874 | 0.2764 | 0.1500 | 1.0000 | ||

| LnFSR | −0.0748 | 0.0784 | −0.2823 | 0.1122 | 0.129 | 0.5696 | 1.0000 | |

| LnLSR | −0.2367 | −0.2466 | −0.0567 | −0.2876 | −0.2146 | −0.3625 | −0.0112 | 1.0000 |

| Variables | Testing Method | Statistic Value | Prob. | Results |

|---|---|---|---|---|

| LnY | Levin, Lin & Chu t | −1.82611 ** | 0.0339 | Stationary |

| LnK | Levin, Lin & Chu t | −4.15009 *** | 0.0000 | Stationary |

| LnL | Levin, Lin & Chu t | −3.83709 *** | 0.0001 | Stationary |

| LnR&D | Levin, Lin & Chu t | −9.76045 *** | 0.0000 | Stationary |

| LnFDI | Levin, Lin & Chu t | −14.0164 *** | 0.0000 | Stationary |

| LnFGR | Levin, Lin & Chu t | −8.79669 *** | 0.0000 | Stationary |

| LnFSR | Levin, Lin & Chu t | −10.8390 *** | 0.0000 | Stationary |

| LnLSR | Levin, Lin & Chu t | −7.61093 *** | 0.0000 | Stationary |

| Regions | Thresholds | Threshold Variable (FGR) | Threshold Variable (FSR) | Threshold Variable (LSR) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| F-Value | p-Value | Critical Value | F-Value | p-Value | Critical Value | F-Value | p-Value | Critical Value | ||||||||

| 1% | 5% | 10% | 1% | 5% | 10% | 1% | 5% | 10% | ||||||||

| Eastern Region | Single Threshold | 25.052 *** | 0.017 | 25.475 | 23.894 | 21.514 | 7.092 | 0.163 | 13.819 | 9.428 | 8.005 | 35.089 * | 0.083 | 41.319 | 37.184 | 34.472 |

| Double Threshold | 35.575 *** | 0.000 | 4.558 | −2.720 | 35.575 *** | 6.979 *** | 0.000 | 3.496 | 2.093 | 1.600 | 22.257 *** | 0.000 | −8.661 | −10.895 | −11.967 | |

| Tripe Threshold | 0.000 | 0.603 | 0.000 | 0.000 | 0.000 | 0.000 | 0.440 | 0.000 | 0.000 | 0.000 | 0.000 | 0.723 | 0.000 | 0.000 | 0.000 | |

| Central Region | Single Threshold | 25.196 | 0.133 | 42.164 | 35.419 | 32.657 | 4.931 * | 0.057 | 6.779 | 5.09 | 4.055 | 24.513 | 0.163 | 33.126 | 29.830 | 26.852 |

| Double Threshold | 5.164 *** | 0.000 | −4.017 | −10.132 | −13.241 | 1.976 *** | 0.003 | 0.692 | −0.984 | −1.542 | 32.267 *** | 0.000 | 4.137 | −8.691 | −12.159 | |

| Tripe Threshold | 0.000 | 0.623 | 0.000 | 0.000 | 0.000 | −5.402 | 0.843 | 4.713 | 3.752 | 2.873 | 8.476 | 0.850 | 37.050 | 31.558 | 27.401 | |

| Western Region | Single Threshold | 7.919 | 0.467 | 43.823 | 29.176 | 23.006 | 6.022 | 0.383 | 14.439 | 11.512 | 9.996 | 21.095 | 0.177 | 45.214 | 28.969 | 25.05 |

| Double Threshold | 29.632 *** | 0.003 | 19.84 | 7.930 | 4.646 | 11.976 *** | 0.000 | 2.426 | 0.052 | −1.477 | 31.603 *** | 0.000 | −7.240 | −11.574 | −14.502 | |

| Tripe Threshold | 8.706 | 0.15 | 29.934 | 18.499 | 12.272 | 0.000 | 0.490 | 0.000 | 0.000 | 0.000 | 0.000 | 0.493 | 0.000 | 0.000 | 0.000 | |

| Threshold Variables | Threshold Variable (FGR) | Threshold Variable (FSR) | Threshold Variable (LSR) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Regions | Threshold | Estimate | 95% Confidence Interval | Threshold | Estimate | 95% Confidence Interval | Threshold | Estimate | 95% Confidence Interval |

| Eastern Region | λ1 | 1.155 | [1.155, 5.735] | λ1 | 0.517 | [0.067, 0.607] | λ1 | 0.584 | [0.571, 0.590] |

| λ2 | 1.755 | [1.565, 4.669] | λ2 | 0.607 | [0.064, 0.724] | λ2 | 0.749 | [0.744, 0.753] | |

| Central Region | λ1 | 1.247 | [1.093, 2.962] | λ1 | 0.132 | [0.076, 0.387] | λ1 | 0.704 | [0.692, 0.710] |

| λ2 | 1.637 | [1.093, 1.712] | λ2 | 0.137 | [0.135, 0.147] | λ2 | 0.731 | [0.722, 0.877] | |

| Western Region | λ1 | 1.206 | [1.165, 1.740] | λ1 | 0.130 | [0.071, 0.336] | λ1 | 0.774 | [0.751, 1.486] |

| λ2 | 1.671 | [1.653, 1.740] | λ2 | 0.213 | [0.071, 0.519] | λ2 | 1.187 | [0.963,1.187] | |

| LnY | Eastern Region | Central Region | Western Region | ||||||

|---|---|---|---|---|---|---|---|---|---|

| LnK | 0.068 (0.062) | 0.170 (0.057) | 0.052 *** (0.018) | 0.152 *** (0.042) | 0.090 ** (0.035) | 0.043 (0.049) | 0.325 *** (0.040) | 0.479 *** (0.038) | 0.048 (0.036) |

| LnL | 0.067 *** (0.011) | 0.076 *** (0.036) | 0.030 *** (0.007) | 0.889 *** (0.029) | 0.909 *** (0.026) | 0.845 *** (0.037) | 0.839 *** (0.038) | 0.809 *** (0.035) | 0.420 *** (0.033) |

| LnR&D | 0.086 ** (0.044) | 0.273 *** (0.046) | 0.251 *** (0.263) | −0.053 (0.036) | 0.102 *** (0.038) | 0.038 (0.045) | 0.056 * (0.034) | 0.030 (0.036) | 0.241 *** (0.025) |

| LnFGR | 0.199 *** (0.022) | −0.076 (0.085) | −0.249 *** (0.056) | ||||||

| LnFSR | −0.105 *** (0.040) | −0.007 (0.025) | −0.034 (0.042) | ||||||

| LnLSR | 0.110 * (0.073) | 0.026 (0.030) | −0.595 *** (0.114) | ||||||

| LnFDI·I(FGR < λ1) | 0.085 *** (0.020) | 0.054 *** (0.019) | −0.037 *** (0.012) | ||||||

| LnFDI·I(λ1≤FGR < λ2) | 0.071 *** (0.019) | 0.047 *** (0.018) | −0.014 (0.012) | ||||||

| LnFDI·I(FGR ≥ λ2) | 0.058 *** (0.019) | 0.040 ** (0.019) | 0.004 * (0.012) | ||||||

| LnFDI·I(FSR < λ1) | 0.007 (0.047) | 0.015 ** (0.015) | −0.149 *** (0.018) | ||||||

| LnFDI·I(λ1≤FSR<λ2) | 0.039 ** (0.049) | 0.007 (0.016) | −0.131 *** (0.018) | ||||||

| LnFDI·I(FSR ≥ λ2) | 0.037 ** (0.048) | 0.019 ** (0.016) | −0.110 *** (0.018) | ||||||

| LnFDI·I(LSR < λ1) | 0.083 * (0.049) | 0.014 ** (0.018) | −0.027 (0.022) | ||||||

| LnFDI·I(λ1≤LSR < λ2) | 0.043 ** (0.046) | -0.007 (0.019) | −0.001 (0.022) | ||||||

| LnFDI·I(LSR ≥ λ2) | 0.023 ** (0.047) | 0.006 * (0.020) | 0.072 *** (0.024) | ||||||

| C | 6.541 *** (0.299) | 7.231 *** (0.224) | 7.991 *** (0.187) | −0.036 (0.264) | 0.467 * (0.262) | 0.604 (0.365) | −0.935 *** (0.317) | −1.315 *** (0.272) | 3.804 *** (0.296) |

| within R-sq | 0.7164 | 0.644 | 0.8844 | 0.9524 | 0.9624 | 0.945 | 0.9212 | 0.9255 | 0.9247 |

| F-statistics | 54.5 | 39.03 | 163.96 | 311.31 | 349.91 | 267.47 | 252.1 | 267.9 | 256 |

| (Prob > F) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| F test for No Fixed Effects | 159.48 | 122.28 | 525.69 | 91.4 | 109.28 | 65.95 | 57.93 | 64.66 | 135.27 |

| (Prob > F) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Durbin-Wu-Hausman(p-value) | 0.1271 | 0.4448 | 0.4125 | 0.237 | 0.5893 | 0.3507 | 0.3684 | 0.7791 | 0.332 |

| N | 165 | 165 | 165 | 120 | 120 | 120 | 165 | 165 | 165 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, H.; Liu, H. An Empirical Research of FDI Spillovers and Financial Development Threshold Effects in Different Regions of China. Sustainability 2017, 9, 933. https://doi.org/10.3390/su9060933

Wang H, Liu H. An Empirical Research of FDI Spillovers and Financial Development Threshold Effects in Different Regions of China. Sustainability. 2017; 9(6):933. https://doi.org/10.3390/su9060933

Chicago/Turabian StyleWang, Hui, and Huifang Liu. 2017. "An Empirical Research of FDI Spillovers and Financial Development Threshold Effects in Different Regions of China" Sustainability 9, no. 6: 933. https://doi.org/10.3390/su9060933

APA StyleWang, H., & Liu, H. (2017). An Empirical Research of FDI Spillovers and Financial Development Threshold Effects in Different Regions of China. Sustainability, 9(6), 933. https://doi.org/10.3390/su9060933