Impact of the COVID-19 Pandemic on Agri-Food Companies in the Region of Extremadura (Spain)

Abstract

:1. Introduction

2. The Dynamics of Responses to the “New Reality”

3. Methodology and Data

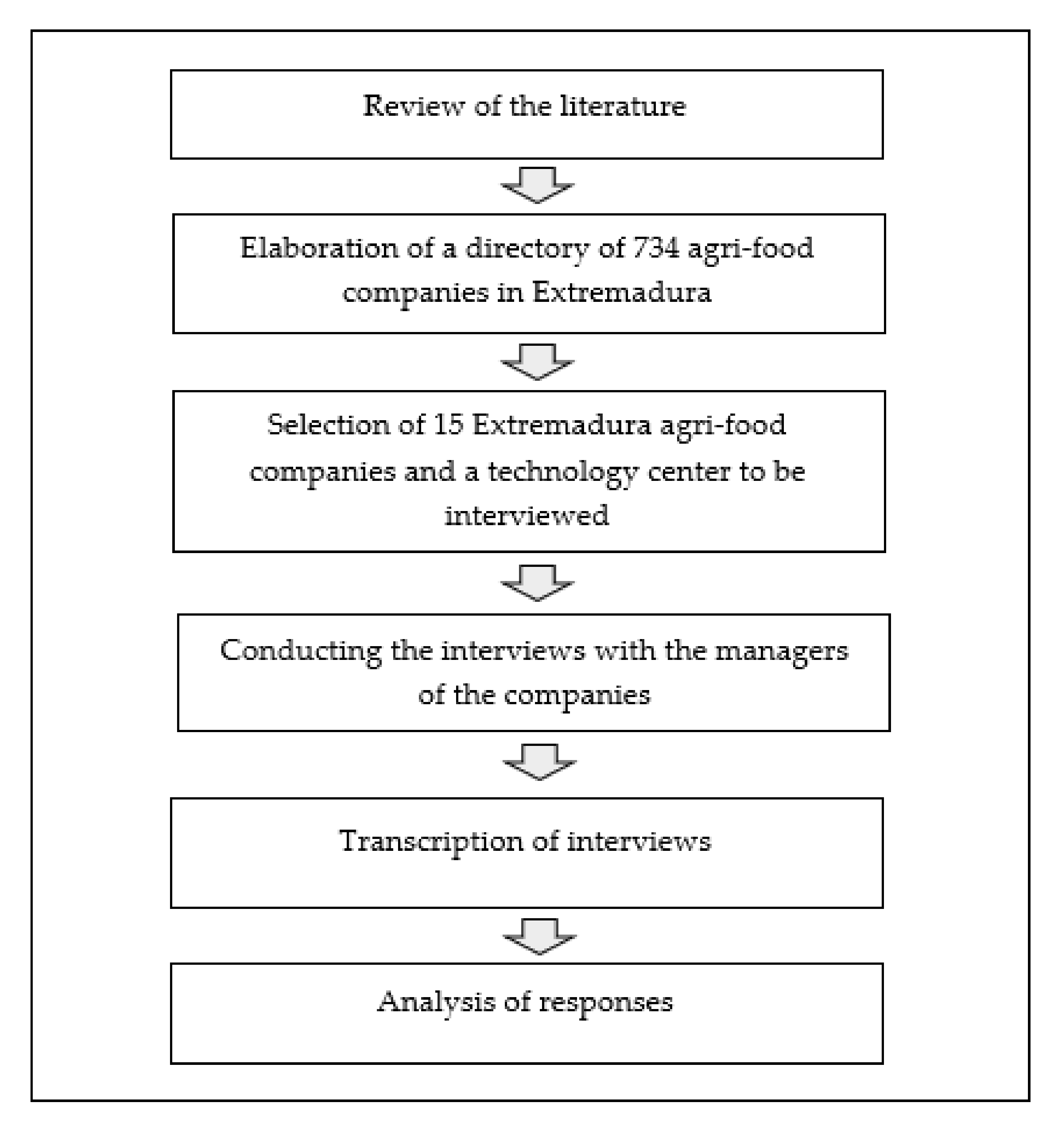

3.1. Research Design

3.2. Characteristics of the Companies

4. Findings

4.1. Negative Impacts

4.1.1. Decrease in Sales/Turnover

Director of Operations (Company 11): “COVID-19 has had a negative impact and has resulted in a drop in sales. Last year we had a turnover of about 18 million euros. At present, the loss of turnover is about 3 million euros. In other words, we are going to have a 61% drop in our sales. And also where we are most noticing this drop in sales is in hams, which is the product that contributes volume and margin to the business”.

CEO (Company 14): “In the HORECA channel, sales have fallen by 17%, because the school canteens closed, the restaurants… So we thought that the gains in retail were going to offset these losses, but it has not been the case”.

CEO (Company 9): “[…] taking into account the situation of many citizens, some are in ERTE, others are unemployed, people are afraid and all this leads to a decline in consumption”.

CEO (Company 4): “The wine that has suffered the most from the coronavirus crisis is sparkling wine. Unfortunately there were no reasons to celebrate…”.

4.1.2. Displacement in the Demand for Products

Head of department (Company 12): “COVID-19 has affected us. In the restaurant area, there has been a lull. Unfortunately, this has been the case and nothing else can be done. On the other hand, we have had an increase in sales in the other area, in filleting and processing. Because in the end, when people were at home, what they consumed were ready meals and they no longer went to restaurants. This has created a very strong demand, which, in fact, in March was a bit overwhelming, because we were waiting for another packing machine to arrive, which fortunately arrived on time because we had to double staff, lines…. In the end, we were all the same, shopping in supermarkets and trying to spend as little time as possible there and people did not stop at the butchers, but preferred ready meals and, in the shortest possible time, to get back home”.

CEO (Company 15): “In principle, we almost benefited from the coronavirus situation, since in part the demand for our products is shifting. For example, we have 3 product lines: fresh garlic, peeled garlic clove and garlic paste. In the case of the peeled garlic clove, the final consumer does not use it because it is aimed at hospitality and industry, and the hospitality industry has closed, so its consumption has decreased. It is also true that if consumption in the hospitality industry decreases, household consumption increases, although not in the same proportion, but now the demand for fresh garlic has grown and that of peeled cloves has decreased”.

CEO (Company 13): “[…] in berries, we have redcurrant. We have very little of this product. It is commonly consumed and used in desserts; We have had clients who habitually sold it directly to the hospitality industry and this year they have not sold anything”.

Operations Director (Company 11): “[…] consumers, in fear of the situation of economic uncertainty, will always go to those products that have a lower value and this always affects those with higher value…”. “[…] When there is a crisis situation, like the one we find ourselves in now and the consumer is sensitive to price, the most affected sector will be precisely the one that opts for Iberian and traditional products”.

4.1.3. Difficulty in Marketing Activities

CFO (Company 5): “I had already done a market study to start carrying out marketing activities in Madrid, Seville… but after the pandemic started in March we have been inactive. Now at the beginning of May we have started again […] For now the expectations are good, they are positive, but there is still some uncertainty”.

Department manager (Company 10): “We have been affected by the coronavirus, especially in terms of visiting our clients. In the end, our sales method in vegetable production is mostly commercial visits to clients”. “[…] in April, which is when visits are made to close deals with clients, in the end, up to 70 or 80% of the visits have been lost”.

CEO (Company 2): “With the coronavirus we have problems. For example, now in April I was going to Japan and in June to the United States. In June we were going to the Summer Fancy Food in New York, which we have been attending for 3 years, this would be the 4th year. We have also been to Japan in other years, this would also be the 4th year”.

4.1.4. Slow Down and Budget Reduction in R&D Projects

CEO (Company 8): “For more than 10 years, R&D projects have been developed which have allowed new references to be drawn annually. However, during 2020 the number of projects has reduced and all those that were already underway have slowed down”.

CEO (Company 11): “Before the pandemic, we had an investment and development budget of approximately 1,000,000 € intangible assets and we had an investment and development protocol to invest 500,000 € in research and development every year. In fact, in 2019 we invested 800,000 €, which was an exceptional investment year. And this year, the pandemic has forced us to cut that budget because the benefits have dropped”.

4.1.5. Lack of Staff (Quarantine)

Operations Director (Company 7): “At the manufacturing and sales level, the truth is that it has not affected us. What we have had are other typical problems. If there was someone who for whatever reason had to carry out the PCR test, then you could not count on that person until they did the test and it was negative twice. So maybe we have lost 2, 3 or 4 people for about 4 weeks, without any being positive in the end”.

4.1.6. Stoppage or Decrease in Company Activity

CFO (Company 1): “It has affected us, because we have a factory in China and the output of products from China is stopped at the ports. The market in general is stopped in China”.

CEO (Company 13): “Now, according to our protocols, each line has to enter half an hour after the previous one”. This is fine to ensure safety, but it is also causing us to reduce production and activity”.

4.1.7. Supply Problems

CEO (Company 8: transformer and marketer of olive oil-based products): “[…] Much of the packaging that we use to manufacture our products comes from China. When China closed, they radically stopped manufacturing and an incredible backlog was formed. We had to go to European manufacturers, where an important hold-up also occurred due to the great demand, and to which was added the large shortage of containers produced by the hydroalcoholic gel…”.

4.2. Positive Impacts

Increase in Production and Sales

CEO (Company 6: production of cereals, mainly for the production of animal feed): “The agricultural sector did not stop […] People have continued sowing and harvesting with all security measures […] In the case of rice we had a significant increase in cereal production”.

CEO (Company 15: production, transformation and commercialization of garlic): “We also have to say that prices have remained high and demand has increased for our product, dried whole garlic. So, in general, we can say that it has almost benefited us”.

Department head (Company 12: leading company in the transformation of beef products and their commercialization in the Horeca and retail channels): “[…] we have certainly had an increase in sales in the other area, in filleting and manufacture. Because in the end, since people were staying at home, they consumed ready meals and they didn’t go to restaurants. This has resulted in a strong demand…”.

4.3. Other Actions Induced by the Changes

4.3.1. Search and Diversification of Clients and Suppliers in Other Markets

Commercial Director (Company 3: wine-growing company that enhances all phases of the product value chain): “With the whole issue of the pandemic… the only ones who have been selling are the supermarkets. People have been consuming a lot of wine, so you have to look for other alternatives. This is how the idea of doing the largest online tasting service so far came about […] “When the lockdown happened… I was forced to stop, although my mind did not stop at home […] I had scheduled tastings with clients in restaurants. They were worried, because they had closed. So, I started preparing for an online tasting. But since there were already people doing online tastings, I decided to do the largest online tasting in the world […] In the end 150 people attended the tasting […] You have to be very active and know all the tools”.

CEO (Company 8: transformer and marketer of olive oil-based products): “The closing of the borders caused us supply problems. Much of the packaging that we use to manufacture our products comes from China. So we had problems when that country closed. In fact, in China they suddenly stopped manufacturing. We acted fast and we had to go to European manufacturers”.

4.3.2. Increased Use of Technology in Communication and Marketing Activities

CEO (Company 6: cooperative leader in the production of cereals and vegetables for sale to other processing industries and end customer at its facilities): “What has come to stay with COVID-19 is […] having a meeting by video-conference without having to travel. I, who belong to many companies, wasted a lot of time going, coming, apart from the contamination generated by the transfer […] I already have all the platforms that allow working through video-conference installed. In addition, the meetings are much more participatory, more practical and less time is wasted”.

CEO (Company 15: cooperative that produces, transforms and markets garlic): “Digitization is being encouraged. We continue working through WhatsApp, which is a very useful tool for making video calls, sending photos… also, everyone knows it and uses it”.

CEO (Technological center): “The coronavirus has also obliged us to get used to this type of meeting and that is in part an organizational change that has come to stay”.

CEO (Company 13): “With the situation of the pandemic, Zoom has made it much easier. For example, now we are going to hold a meeting of the Board of all the Governing Boards online. This will allow the rest of the cooperatives to know what the end of the campaign report is and we will allow all the members to connect and not just the administrator of each of the 15 cooperatives as happened before”.

CEO (Company 6: vegetable products): “Internet sales have also been greatly boosted, and they have come to stay. We sold oil online previously, but we had a rather obsolete payment platform; now we have updated our website and orders can be made on the same page. The coronavirus has forced us to update ourselves […] In another of the cooperatives in which we have participation, we have created a web page, so the sale of the cheeses is also carried out through the internet”.

CEO (Company 11: Iberian pork meat products): “Now we are working a lot on online marketing because we think it is part of the future, especially now with the pandemic”.

4.3.3. Reorganization of Personnel and Activities

Department manager (Company 12): “[…] in the catering area, we had a stoppage. […] However, we have had an increase in sales in the other area, in filleting and processing. […] This has caused a very strong demand… […] So, all the staff that we had in the hotel industry have been put on the lines to lend a hand since there has been a lot of demand in that area”.

CEO (Company 13): “Perhaps where this situation has affected us the most is at the level of costs at the plant. We have had to invest a lot of money to adapt and implement action protocols for our workers. […] For example, before we had 5 lines and the workers were entering at the same time. Now according to our protocols, each line has to enter half an hour after the previous one”.

CEO (Technological center): “Precisely one of the things that we did and that has allowed us to differentiate ourselves from our competitors was to put forward all our public projects and to implement an action plan for high-value services that are independent of financing by public entities, because we knew that everything was stopping”.

4.3.4. Implementation of New Health Protocols

CEO (Company 13): produces, transforms and markets large volumes of fruit and vegetables): “[…] We have had to invest a lot of money to adapt and implement action protocols for our workers. Take into account that in the campaign, we can reach 1000 workers and in this situation of health risk we have had to provide many material means such as hydroalcoholic gels, masks, changes of tables in the dining rooms, new temperature controls, spacing the entrance areas of the plant”.

CEO (Company 14: producer that carries out the first transformation of vegetables): “In our plant we have had only one positive case and we have protocols that ensure the safety of all our workers. With the positive person in coronavirus we acted fast. In fact, and using the services of an external company, we carried out up to 48 PCRs on all staff members who could have been in contact with that worker […] In short, as soon as the state of alarm was decreed here, the protocol crisis was activated and implemented right from the beginning”.

4.3.5. Development of New Products

CEO (Company 8): “In cosmetics, seeing the opportunity to make hydroalcoholic gel and sanitizers, we developed a number of products and formats. In November of last year, one of our clients, the franchisee that we have in Barcelona, who receives many Asian, Chinese and Korean clients mainly, noticed that many of those clients were ordering hydroalcoholic gel from him. We have never had this product before and this franchisee requested it form us and now in his 4 stores we sell a lot, because we developed it for him. In the end it has been great for us, because in the last few months we have been selling a lot of hydroalcoholic gel, just because we listened to that customer. And as a result of that, we have developed this same product, but in other formats and even a surface sanitizer, also a sanitizing bath gel…”.

5. Discussion

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| COMPANY 1: Processing and preserving of fruits and vegetables |

| Company 1 is a second-generation family business. It was founded in 1976. It currently ranks second in the production of tomato powder worldwide. It is a primary producer, whose main clients are multinational food processors. Since 2014, it has begun a process of expansion which involves direct investment and location in countries with important markets, such as China and the United States (California). In Spain, it has also multiplied its production infrastructures, to achieve proximity to its suppliers and to have greater stability in the supplies of raw materials, since they are sometimes affected by climatic changes. The group resulting from the expansion has an average of 600 workers, but at the height of the season they can reach 1600. It produces a total of 300 million kilos of tomatoes, which is equivalent to 25% of the tomatoes of the Iberian Peninsula and 3.5% of the world production. |

| COMPANY 2: Manufacture of vegetable and animal oils and fats |

| Company 2 is a small company with five workers that was founded in 2015 and belongs to the subsector of the manufacture of extra olive oil, its subsequent packaging, and marketing. Its facilities are modern and they have their own olive groves. In addition, its product portfolio also includes sherry vinegar, fragrant cooking wine, as well as aceiterol (an active ingredient in cosmetics), and olive leaf tea. They are oil exporters, with a presence of their brand in Japan, Mexico, the United States and Germany, among other countries. |

| COMPANY 3: Manufacture of beverages |

| Company 3 is a family winery that was born in 2003 as a consequence of continuing with the family trajectory of winemakers. The goal is to make a high quality own brand of bottled wines. It has a limited range of products, among which are red and white organic wines. They invest in an R&D project. In addition, the company has recently started exporting to clients in the United Kingdom, Belgium and Portugal. |

| COMPANY 4: Manufacture of beverages |

| Company 4 is an agrarian transformation society (SAT in Spanish). It was founded in 1982, and it is located in Almendralejo (Badajoz). It is a family business, with a tradition of more than five generations in the cultivation and production of wines. Ten employees work in the winery. The wines they make are red, white and semi-sweet. In recent years, they have begun to make sparkling wine (cava in Spanish), and for this, they built a second winery in 2019. The organization has also diversified its activities and has a restaurant within the winery’s facilities, they offer tastings, pairings, events and guided tours. They market their products nationally and internationally to markets such as the United States or Japan. |

| COMPANY 5: Manufacture of other food products |

| Company 5 is a young organization that was founded in 2019 with its headquarters in Los Santos de Maimona (Badajoz). It was established by an individual entrepreneur and its industrial activity is the production of organic and vegan patés. For the elaboration of its products, it subcontracts production to another regional company which is a leader in the manufacture of conventional patés. The company has only one employee, the owner. It markets its products through online sales, distributors, in gourmet stores and other specialized stores. The turnover is less than EUR 500,000. |

| COMPANY 6: Manufacture of products for animal feed |

| Company 6 is an agrarian transformation society (SAT), located in Don Benito (Badajoz). It was founded in 1985 and its main activity is the manufacture of products for animal feed, although in recent years it has diversified its activity, working with products such as tomato, oil, rice, compound feed, seeds, fertilizers and phytosanitary products. They have five production centers and are also shareholders of several agri-livestock companies in the region. They market their products regionally and nationally, and also in Italy and Portugal. It is a benchmark company within the agrarian cooperatives in Extremadura and Spain. The Spanish Business Confederation of the Social Economy (CEPES in Spanish), in its annual report, ranks it no. 67 out of the total of 722 national agri-food cooperatives, with EUR 68,000,000 in turnover and 70 employees. |

| COMPANY 7: Processing and preserving of fruits and vegetables |

| Company 7 is the subsidiary of a Portuguese multinational leader in the production and commercialization of vegetable oils, biofuels, soaps and olives. It began its activity in 2008, when the Portuguese group to which it belongs bought an old olive processing factory in Plasencia (Cáceres). It currently has 60 employees who work in the dressing of green and black table olives. They market their products in a wide variety of countries through their own brands and distribution, providing them with a turnover of more than EUR 30,000,000 per year. |

| COMPANY 8: Manufacture of vegetable and animal oils and fats |

| The origins of Company 8 date back to 1932, although it was not until 1996 when the company was established as a limited company for the fourth generation of the family. They manufacture and market products made with extra virgin olive oil that is divided into: olive oil, gourmet products and cosmetics. The headquarters and activity center are located in Plasencia, where they have 35 workers and where the central offices, industrial warehouses and an oil library are located. The organization also has two of its own stores and a franchise network made up of more than 39 stores spread across Spain and other European and international countries. They market their products to individuals, gourmet shops, other delicatessens and businessmen belonging to the Horeca channel. They do not sell in large stores or do private labels for any supermarkets. Their turnover amounts to EUR 18,000,000, they pack more than 6,000,000 L of olive oil a year and they export to more than 35 countries. Company 8 is considered one of the 10 most important Spanish companies in this market segment. |

| COMPANY 9: Processing and preserving of meat and elaboration of meat products |

| Company 9 is a limited company of family origin located in Fregenal de la Sierra (Badajoz), made up of three founding partners and a total of nine employees. Created in 2012 after the dissolution of another company in 2008 that fell into bankruptcy, it is a producer, processor and marketer of Iberian cattle and pigs raised in extensive systems. They work the entire value chain of their products, with the exception of slaughter. They carry out national and international commercial activity in different markets, such as Europe and Latin America or Asia. Its clients are final consumers, other companies and the hospitality sector, which provide it with a turnover of close to EUR 1,000,000. |

| COMPANY 10: Manufacture of products for animal feed |

| Company 10 is a limited company created in 2013 and of family origin that is located in Badajoz. They function mainly as distributors of agricultural products that have been developed and patented together with their “partners” in France. Its main objective is to advise and commercialize agricultural products nationally and in Portugal. In 2020, they reached a turnover of more than EUR 6,000,000 and have a total of 10 employees. |

| COMPANY 11: Processing and preserving of meat and elaboration of meat products |

| Company 11 is a limited company established in 1995 that manufactures meat products from acorn-fed Iberian pigs and controls the entire value chain. It is made up of 75 livestock partners from Extremadura and Andalusia and another 16 collaborators in the Portuguese Alentejo. The company is a leader in the production of pure Iberian hams in Extremadura. Currently, they market their products in more than 25 countries, in particular, Canada, Japan, the United Kingdom and France. |

| COMPANY 12: Processing and preserving of meat and elaboration of meat products |

| Company 12 was established in 1998 as a public limited company by two partners with extensive professional and family careers in the meat sector. The company is the leader in Spain in the production of meat and beef products. It is currently made up of 400 employees distributed in two locations, one in Madrid and the other in Almaraz (Cáceres), made up of 200 workers. This company has strategically located the slaughterhouse and cutting plants in Extremadura, since Extremadura is the second Community in the census of cattle breeders. The company has clients in large distribution, export, retail and wholesale markets. They invoice more than EUR 200,000,000 annually. In addition, they sell their products nationally (70%) and the rest is exported, mainly to Europe, although they have also worked in Africa and Asia. |

| COMPANY 13: Processing and preserving of fruits and vegetables |

| Company 13 is a second-degree cooperative that integrates 16 other first-degree cooperatives from the northern area of Extremadura. This company markets products from its member cooperatives (cherries, chestnuts, dried figs, plums and berries), it markets other processed products in which it subcontracts its production and it carries out transformation in the distillery and oil mill activities. It was established in 1986 in Valdeastillas (Cáceres) and currently produces more than 20,000 tons of products; The company works with 3500 farmers and has 110 permanent employees 900, more of which are added during the high seasons. This company is a leader in the retail channel, especially with its flagship product, the cherry. Its clients are large hypermarket and supermarket chains. They also carry out foreign trade, exporting 50–60% of their production, mainly to Europe, although they also work with non-European countries, such as the United Arab Emirates and Hong Kong. |

| COMPANY 14: Processing and preserving of fruits and vegetables |

| Company 14 is a limited company located in Badajoz that has a total of 55 permanent workers, reaching 120 with discontinued workers. This joint venture was established in 2010 by two Belgian multinational groups with a 50% stake each. It is dedicated to the first and second transformation of vegetable products that are finally deep-frozen (peppers, courgettes, aubergines, potatoes, sweet potatoes, etc.). They work with more than 170 references that are packed in bulk and in different quantities, although the final part of production, mixing and packaging is carried out in other production plants of multinational groups. They market their products in the Horeca, retail and large industrial channels, billing more than EUR 32,000,000 per year. |

| COMPANY 15: Processing and preserving of fruits and vegetables |

| Company 15 is an Extremaduran cooperative company that integrates 45 partners and is dedicated to the transformation and commercialization of fresh whole garlic, paste and peeled garlic cloves. It was established in 2003 and is located in Aceuchal (Badajoz), where six permanent employees and 74 temporary employees work. It is a leading company in the marketing of garlic nationally and internationally. It produces more than 5000 tons of garlic per year and invoices between EUR 6,000,000 and EUR 10,000,0000 per year. Since 2012, they have marketed their products in Brazil, North America, Canada and European countries. As a result, they have experienced continuous growth reaching 10% in 2020. |

| TECHNOLOGICAL CENTER |

| This is a leading private agri-food technology center in terms of innovation located in Badajoz and established in 2001. Its business activity is based on supporting companies in the agri-food sector by offering research, development, innovation and training services to contribute to the competitive development of regional, national and international companies. Its technological center is very innovative, in fact, it has several pilot plants, experimental farms, laboratories, kitchens, tasting rooms and other facilities for process control, where a total of 49 employees are working. |

Appendix B

| COMPANY 1 |

| CFO: “It has affected us. Because we have a factory in China and the output of products from China is stopped at the ports. The market in general has stopped in China”. |

| CFO: “Luckily we have a very residual business there. To give you an idea, this factory in Villafranco del Guadiana makes 300 million kilos, we remember that, in total, we have 11 production centers and our factory in China makes 50 million. And well, in China now everything is stopped and now in Europe we need to wait to see what happens”. |

| COMPANY 2 |

| CEO: “Until the coronavirus happened, we exported to Taiwan, Japan, Canada, the United States and then in Europe, in countries like Germany”. |

| CEO: “With the coronavirus we have problems. For example, now in April I was going to Japan and in June to the United States. In June we were going to the Summer Fancy Food in New York, which we have been attending for 3 years, this would be the 4th year. We have also been to Japan in other years, this would also be the 4th year”. |

| COMPANY 3 |

| Commercial Director: “With the whole issue of the pandemic… the only ones who have been selling are the supermarkets. People have been consuming a lot of wine, so you have to look for other alternatives. This is how the idea of doing the largest online tasting service so far came about”. |

| Commercial Director: “When the lockdown happened… I was forced to stop, although my mind did not stop at home […] I had scheduled tastings with clients in restaurants. They were worried, because they had closed. So, I started preparing for an online tasting. But since there were already people doing online tastings, I decided to do the largest online tasting in the world […] In the end 150 people attended the tasting […] You have to be very active and know all the tools”. |

| COMPANY 4 |

| CEO: “The wine that has suffered the most from this coronavirus crisis is sparkling wine. Unfortunately, there are no reasons to celebrate… I have a meeting this afternoon with the governing board and one of the topics that we are going to discuss is the harvest, to see how we are going to organize it and it is not clear how prices will evolve. Farmers are concerned about prices”. |

| COMPANY 5 |

| CEO: “I had already done a market study to start entering Madrid, Seville… but then what happened happened and the truth is that during COVID-19 we have been inactive. Now at the beginning of May we have started again […] For now the expectations are good, they are positive, but there is still some uncertainty”. |

| COMPANY 6 |

| CEO: “The agricultural sector did not stop […] People have continued sowing and harvesting with all security measures […] In the case of rice we had a significant increase in cereal production”. |

| CEO: “What has come to stay with COVID-19 is […] having a meeting by video-conference without having to travel. I, who belong to many companies, wasted a lot of time going, coming, apart from the contamination generated by the transfer […] I already have all the platforms that allow working through video-conference installed. In addition, the meetings are much more participatory, more practical and less time is wasted”. |

| CEO: “Internet sales have also been greatly boosted, and they have come to stay. We sold oil online previously, but we had a rather obsolete payment platform; now we have updated our website and orders can be made on the same page. The coronavirus has forced us to update ourselves […] In another of the cooperatives in which we have participation, we have created a web page, so the sale of the cheeses is also carried out through the internet”. |

| CEO: “COVID-19 has led us to do things that we already did, but we did them in a half-hearted way; well, now we do them 100% and as I said, they have come to stay, such as virtual meetings and Internet sales”. |

| CEO: “With the coronavirus, I believe that the most important thing is yet to come, that is, the economic recession that comes with the fall of the economy will mean that there is less consumption. In our case, as a primary sector it will be one of the things that will decrease the least […]”. |

| CEO: “The situation we have experienced has to open the eyes of governments, because certain sectors cannot depend on third countries […] We cannot hope that food will be provided by the United States or Brazil, but rather that governments have to have a series of issues that as a society are essential. In food we cannot dismantle our livestock and agriculture because there are others that also do so, because at some point they may stop serving you or set prices, and sectors as strategic as the primary sector cannot be dismantled”. |

| COMPANY 7 |

| Director of operations: “It has forced us to adjust our protocols […] because being a food company, the hygienic protocols are high and we have had to increase them even more and try not to have so much contact between the employees”. |

| Director of operations: “At the manufacturing and sales level, the truth is that it has not affected us. What we have had are other typical problems. If there was someone who for whatever reason had to carry out the PCR test, then you could not count on that person until they did the test and it was negative twice. So maybe we have lost 2, 3 or 4 people for about 4 weeks, without any being positive in the end”. |

| COMPANY 8 |

| CEO: “Export has not affected us too much. When the Spanish market stopped… well, we sell a lot in Asia, it is one of our main markets with countries like Korea and China, especially in cosmetics. So both Korea and China were inactive in January or February, then they began to recover and in March we were already taking orders for those countries. And after these two markets, we also sell a lot in Europe, especially the central and northern part, which has not been affected as much as in Spain, France and Italy. So, we have continued to function”. |

| CEO: “The stores, our franchises, in the Spanish market have been closed for a while”. |

| CEO: “Where the virus situation has affected us is in the development of new products”. |

| CEO: “[…] Much of the packaging that we use to manufacture our products comes from China. When China closed, they radically stopped manufacturing and an incredible backlog was formed. We had to go to European manufacturers, where an important hold-up also occurred due to the great demand, and to which was added the large shortage of containers produced by the hydroalcoholic gel….”. |

| CEO: “The closing of the borders caused us supply problems. Much of the packaging that we use to manufacture our products comes from China. So, we had problems when that country closed. In fact, in China they suddenly stopped manufacturing. We acted fast and we had to go to European manufacturers”. |

| CEO: “They have been a difficult few months and they have slowed us down a lot for the development of new products”. |

| CEO: “Sales have also dropped a lot”. |

| CEO: “In cosmetics, seeing the opportunity to make hydroalcoholic gel and sanitizers, we developed a number of products and formats. In November of last year, one of our clients, the franchisee that we have in Barcelona, who receives many Asian, Chinese and Korean clients mainly, noticed that many of those clients were ordering hydroalcoholic gel from him. We have never had this product before and this franchisee requested it form us and now in his 4 stores we sell a lot, because we developed it for him. In the end it has been great for us, because in the last few months we have been selling a lot of hydroalcoholic gel, just because we listened to that customer. And as a result of that, we have developed this same product, but in other formats and even a surface sanitizer, also a sanitizing bath gel…”. |

| CEO: “With the coronavirus we have stopped doing some things, but we have started to develop others”. |

| COMPANY 9 |

| CEO: “The coronavirus has affected us negatively and significantly. It has affected us more because now it has also been the bubble that has existed in the pork sector worldwide, in countries like China, Vietnam or Japan, which have been depending a lot on Spanish products, German products, Chilean products; American products… because they have had barriers with tariffs and boycotts that have been made between capitalist countries worldwide… So, well, what we have seen is that there has been an important bubble and right now you can say that there is an excess of production and that has affected”. |

| CEO: “With the current situation, there are companies that are not from the primary sector like us, for example, slaughter companies and they have been able to do an ERTE. On the other hand, we have not been able to do any ERTEs because we are cataloged within the primary sector and they have not let us do it. So, we have had to work things in other ways”. |

| CEO: “Our turnover does not reach a million euros, although it is true that it is increasing, although COVID-19 has slowed down”. |

| CEO: “We have end customers, we have companies that consume us, we have the e-commerce page, so of course, we have several market outlets for the same product. But if a company focuses a lot or is very strong in the Horeca channel, then in times of COVID it will have a terrible time”. |

| COMPANY 10 |

| Department manager: “We have been affected by the coronavirus, especially in terms of visiting our clients. In the end, our sales method in vegetable production is mostly commercial visits to clients”. “[…] in April, which is when visits are made to close deals with clients, in the end, up to 70 or 80% of the visits have been lost”. |

| Department manager: “The most important campaign for us has passed, which is the tomato campaign and also the corn campaign; in April, which is when the visits are made to close the deal with the clients; in the end, up to 70 or 80% of the visits have been lost”. |

| Department manager: “In addition, in the agricultural sector, what we are doing now, that is, meeting someone in a video-conference, is very difficult, but we try”. |

| Department manager: “In the same way, in the area of animal production, sales have also dropped a lot. They also have the crisis of the Iberian pig”. |

| COMPANY 11 |

| CEO: “Before the pandemic, we had an investment and development budget of approximately 1,000,000 € intangible assets and we had an investment and development protocol to invest 500,000 € in research and development every year. In fact, in 2019 we invested 800,000 €, which was an exceptional investment year. And this year, the pandemic has forced us to cut that budget because the benefits have dropped”. |

| CEO: “Right now with the consumer crisis that we have in Spain, relatively speaking, we are doing a little better. We sell a lot abroad. Now, two of our main markets, England and France, are also hit by the pandemic and although the consumption of Iberian products there has also decreased, it has not done so in the same way as in Spain. Bear in mind that our products are typical for meetings, celebrations, events, get-togethers and if they are not available, the situation becomes complicated”. |

| CEO: “Now we are working a lot on online marketing because we think it is part of the future, especially now with the pandemic”. |

| Operations Director: “COVID-19 has had a negative impact and has resulted in a drop in sales. Last year we had a turnover of about 18 million euros. At present the loss of turnover is about 3 million euros. In other words, we are going to have a 61% drop in our sales. And also where we are most noticing this drop in sales is in hams, which is the product that contributes volume and margin to the business”. |

| Operations Director: “There is a drop in sales because the HORECA channel has collapsed, and because consumers, faced with fear of the situation of economic uncertainty, will always go to those products that have a lower value and perhaps have a position in the market is very similar, so they always affect the one with the highest value…”. |

| Operations Director: “In the current situation there is a drop in sales”. |

| Director of operations: “[…] When there is a crisis situation, like the one we find ourselves in now and the consumer is sensitive to price, the most affected sector will be precisely the one that opts for Iberian and traditional products”. |

| COMPANY 12 |

| Department manager: “COVID-19 has affected us positively and negatively. In the restaurant area, there has been a lull. Unfortunately, this has been the case and nothing else can be done. On the other hand, we have had an increase in sales in the other area, in filleting and processing. Because in the end, when people were at home, what they consumed were ready meals and they no longer went to restaurants. This has created a very strong demand, which, in fact, in March was a bit overwhelming, because we were waiting for another packing machine to arrive, which fortunately arrived on time because we had to double staff, lines… So, all the staff that we had in the hospitality industry got on those lines to lend a hand since there was a lot of demand in that area. In the end, we were all the same, shopping in supermarkets and trying to spend as little time as possible there and people did not stop at the butchers, but preferred ready meals and, in the shortest possible time, to get back home”. |

| Department manager: “In the part of Madrid we also have hospitality, although now with this situation, it is a bit in the doldrums”. |

| COMPANY 13 |

| CEO: “It is difficult to determine because precisely this year has been disastrous because of the weather. We have only obtained 50% of the usual production […] It has not affected us directly as it has happened to the hotel industry. Although we believe that we have not noticed it so much in the market due to the misfortune of the weather year that has reduced production by half. One wonders whether the markets would have acted the same if this fact had not happened”. |

| CEO: “Perhaps where this situation has affected us the most has been at the level of costs at the plant. We have had to invest a lot of money to adapt and implement action protocols for our workers. Take into account that in the campaign, we can reach 1000 workers and in this situation of health risk we have had to provide many material means such as hydroalcoholic gels, masks, changes of tables in the dining rooms, new temperature controls, spacing the entrance areas of the plant. For example, before we had 5 lines and the workers were entering at the same time. Now according to our protocols, each line has to enter half an hour after from the previous one”. This is fine to ensure safety, but it is also causing us to reduce production, because we are delaying it. Therefore, it has been noticed more at the cost and investment level to adapt our plant than at the market level”. |

| CEO: “With the situation of the pandemic, Zoom has made it much easier. For example, now we are going to hold a meeting of the Board of all the Governing Boards online. This will allow the rest of the cooperatives to know what the end of the campaign report is and we will allow all the members to connect and not just the administrator of each of the 15 cooperatives as happened before”. |

| CEO: “[…] in berries, we have currants. We have very little of this product. It is very oriented to consume it and use it in desserts; We have had a client who sold it directly to the hospitality industry and this year they have not sold anything”. |

| COMPANY 14 |

| CEO: “From an operational point of view, for the moment, being a company that produces basic necessities, lockdown has not affected us because our campaign in Extremadura runs from the beginning of June to the end of March. During March, April and May we stopped and dedicated ourselves to making projects, modifying lines, doing maintenance… among other things; As the confinement began in March, we were caught when fewer people were working in the company since the campaigns had ended. Therefore, we never stop producing”. |

| CEO: “In our plant we have had only one positive case and we have protocols that ensure the safety all our workers. With the positive person in coronavirus we acted fast. In fact, and using the services of an external company, we carried out up to 48 PCRs on all staff members who could have been in contact with that worker […] In short, as soon as the state of alarm was decreed here, the protocol crisis was activated and implemented right from the beginning”. |

| CEO: “Other actions we carried out were to reduce capacity and provide protective equipment to all our employees”. |

| CEO: “In the HORECA channel, sales have fallen by 17%, because the school canteens closed, the restaurants… So we thought that the gains in retail were going to offset these losses, but it has not been like that. Yes, it is true that part of it has been compensated, but taking into account the situation of many citizens, some are in ERTE, others without work, people are afraid and that leads to a decline in consumption”. |

| COMPANY 15 |

| CEO: “In principle, we almost benefited from the coronavirus situation since in part the demand for our products is shifting. For example, we have 3 product lines: fresh garlic, peeled garlic clove and garlic paste. In the case of the peeled garlic clove, the final consumer does not use it because it is aimed at the hospitality and industry, and the hospitality industry has closed, so its consumption decreased. It is also true that if consumption in the hospitality industry decreases, household consumption increases, although not in the same proportion, but now the demand for fresh garlic has grown and that of peeled cloves has decreased”. |

| CEO: “We made a significant investment in the machinery to produce our garlic cloves. However, on reducing the demand for this product because it has shifted towards fresh garlic, it means we are not getting the expected performance, therefore, this is an inconvenience”. |

| CEO: “We also have to say that prices have remained high and demand has increased for our product, dried whole garlic. So in general we can say that it has almost benefited us”. |

| CEO: “Digitization is being encouraged. We continue working through WhatsApp, which is a very useful tool for making video calls, sending photos… also, everyone knows it and uses it”. |

| TECHNOLOGICAL CENTER |

| CEO: “I think that the Administration in this situation of COVID-19, is showing the least capacity for reaction”. |

| CEO: “We made an emergency action plan. The coronavirus has not interrupted us at all, but we have provided the same services. We started services that are independent from the Administration, which is a big bottleneck”. |

| CEO: “Precisely one of the things that we did and that has allowed us to differentiate ourselves from our competitors was to put forward all our public projects and to implement an action plan for high-value services that are independent of financing by public entities, because we knew that everything was stopping”. |

| CEO: “Of course, all this has involved a great effort on the part of the entire team.” |

| CEO: “A celebration is going to be held at our facilities and we are going to put up a tent, as we need more space due to the coronavirus situation. We are going to hold a public event to expose this and gain visibility”. |

| CEO:”The coronavirus has also obliged us to get used to this type of meeting and that is in part an organizational change that has come to stay”. |

Appendix C

| Word | Repetition/Frequency | Number of Letters |

|---|---|---|

| Company | 59 | 7 |

| COVID-19 | 25 | 8 |

| Coronavirus | 25 | 11 |

| Affected | 13 | 8 |

| Sales | 12 | 5 |

| Market | 8 | 6 |

| Customers | 8 | 9 |

| Sector | 8 | 6 |

| Hostelry | 8 | 9 |

| Production | 7 | 10 |

| Consumption | 7 | 10 |

| Demand | 7 | 6 |

| Online | 6 | 6 |

| Trend | 6 | 5 |

| Actions | 6 | 7- |

| Development | 6 | 11 |

| Crisis | 5 | 6 |

| Prices | 5 | 6 |

| Drop | 5 | 4 |

| Protocols | 5 | 9 |

Appendix D

| Negative Impacts |

| Decrease in sales and turnover in the Horeca channel, high-value products and celebration products. |

| Displacement in the demand for products towards household consumer products and lower-priced substitute products. |

| Difficulty in marketing activities; temporary stoppage of promotion, marketing and attendance at fairs and events. |

| Slowdown and budget reduction in R&D projects |

| Lack of staff (quarantine) |

| Stoppage or decrease in some company activities |

| Supply problems |

| Positive Impacts |

| Increase in production and sales in certain activities |

| Actions carried out by the companies |

| Search and diversification of clients and suppliers in other markets |

| Increased use of technology in communication and marketing activities |

| Reorganization of personnel and activities |

| Implementation of new health protocols |

| Development of new products |

References

- Gjaja, M.; Faeste, L.; Hansell, G.; Hohner, D. COVID 19: Win the Fight, Win the Future. 2020. Available online: https://www.bcg.com/publications/2020/covid-scenario-planning-winning-the-future-series (accessed on 11 January 2021).

- CaixaBank Research. Informe Sectorial Agroalimentario 2020. Resiliencia y Desarrollo del Sector Durante la Pandemia, 2020. Available online: https://www.caixabankresearch.com/es/informes-sectoriales/octubre-2020/agroalimentario (accessed on 11 December 2020).

- FIAB. Informe Económico 2019. Spanish Federation of Food and Beverage Industries, 2020. Available online: https://fiab.es/es/archivos/documentos/INFECO_2019.pdf (accessed on 20 December 2020).

- Bank of Spain. Evolución Reciente y Perspectivas Para el Sector Turístico Español e Implicaciones Para el Conjunto de la Economía; Informe Annual: 2019. Available online: https://repositorio.bde.es/bitstream/123456789/13053/1/InfAnual_2019-Rec4.1.pdf (accessed on 11 April 2021).

- State Tax Administration Agency (AEAT). Estadísticas de Comercio Exterior. Principales resultados. 2020. Available online: https://www.agenciatributaria.es/AEAT.internet/datosabiertos/catalogo/hacienda/comercio_exterior/datos_estadisticos/principales_resultados.shtml (accessed on 11 April 2021).

- National Institute of Statistics (NSI). Population Figures. Available online: https://www.ine.es/jaxiT3/Datos.htm?t=9681 (accessed on 10 April 2021).

- National Institute of Statistics (NSI). Central Business Directory. Available online: https://www.ine.es/jaxiT3/Datos.htm?t=39372 (accessed on 11 April 2021).

- Grupo Alba Internacional. Contexto de la Comunidad Autónoma de Extremadura; Programa de Desarrollo Rural 2014-2020; Grupo Alba Internacional: 2014. Available online: http://www.juntaex.es//filescms/ddgg002/uploaded_files/fondos_europeos/FondosEuropeos2014_2020/BORRADOR_CONTEXTO_EXTREMADURA_FEADER_2014_2020.pdf (accessed on 11 April 2021).

- Corchuelo, B.; Mesías, F.J. Disposición a innovar y competitividad en la agroindustria extremeña. Inf. Téc. Econ. Agrar. 2017, 113, 176–191. [Google Scholar]

- Carrasco, M.; Chandran, P.; Chin, V.; Hayden, P.; Hoteit, L.; Subudhi, S.; Werfel, D. Strat Remaining Government Now: Beyond the Curve, 2020. Available online: https://www.bcg.com/publications/2020/start-reimagining-government-now (accessed on 27 November 2020).

- BDO. COVID-19 Is Accelerating the Rise of the Digital Economy. Digital Transformation in the Pandemic and Post-Pandemic Era. Available online: https://www.bdo.com/insights/business-financial-advisory/strategy,-technology-transformation/covid-19-is-accelerating-the-rise-of-the-digital-e (accessed on 28 April 2021).

- UNCTAD. COVID-19 and e-Commerce. A Global Review; United Nations Conference on Trade and Development: 2021. Available online: https://unctad.org/es/node/32378 (accessed on 11 April 2021).

- Tarcisio, D.M.; Allison, C. Rethinking tax for the digital economy after COVID-19. HBLR 2021. [Google Scholar] [CrossRef]

- Grigorescu, A.; Pelinescu, A.; Ion, A.E.; Dutcas, M.F. Human capital in digital economy: An empirical analysis of central and eastern European countries from the European Union. Sustainability 2021, 13, 2020. [Google Scholar] [CrossRef]

- Sigala, M. Tourism and COVID-19: Impacts and implications for advancing and resetting industry and research. J. Bus. Res. 2020, 117, 312–321. [Google Scholar] [CrossRef] [PubMed]

- Makhiboroda, M.; Ananyeva, E.; Doucek, P. Changes in transport activity regulation in the context of the coronavirus pandemic. In E3S Web of Conferences (Vol. 222). EDP Sci. 2020. [Google Scholar] [CrossRef]

- OECD. The Territorial Impact of COVID-19: Managing the Crisis across Levels of Government; Organization for Economic Cooperation and Development: 2020. Available online: https://www.oecd.org/coronavirus/policy-responses/theterritorial-impact-of-covid-19-managing-the-crisis-across-levels-ofgovernment-d3e314e1/ (accessed on 11 April 2021).

- Lazarus, J.V.; Ratzan, S.; Palayew, A.; Billari, F.B.; Binagwaho, A.; Kimball, S.; Larson, H.; Melegaro, A.; Rabin, K.; White, T.M.; et al. COVID-SCORE: A global survey to assess public perceptions of government responses to COVID-19 (COVID-SCORE-10). PLoS ONE 2020. [Google Scholar] [CrossRef] [PubMed]

- Bol, D.; Giani, M.; Blais, A.; Loewen, P.J. The effect of COVID-19 lockdowns on political support: Some good news for democracy? Eur. J. Political Res. 2021, 60, 497–505. [Google Scholar] [CrossRef]

- Al-Hasn, A.; Yim, D.; Khunti, J. Citizens’ adherence to COVID-19 mitigation recommendations by the government: A 3-country comparative evaluation using web-based cross-sectional survey data. J. Med. Internet Res. 2020, 22, e20634. [Google Scholar] [CrossRef] [PubMed]

- Roos, A.; Satange, S.; Tucker, J.; Grabowski, J.; Uebber, B. COVID-19 CFO Pulse Check 2. 2020. Available online: https://www.bcg.com/publications/2020/covid-cfo-pulse-check-2 (accessed on 27 November 2020).

- Carlsson-Szlezak, P.; Swartz, P.; Reeves, M. Why the global economy is recovery faster than expected? 2020. Available online: https://hbr.org/2020/11/why-the-global-economy-is-recovering-faster-than-expected (accessed on 27 November 2020).

- Bharadwaj, A.; Sanghi, K.; Witschi, P.; Balaji, N.; Chen, C. Edition 3: Who Is the Emerging-Market Consumer in the Post Pandemic Era? 2020. Available online: https://www.bcg.com/publications/2020/covid-19-impact-emerging-market-consumers-third-edition (accessed on 27 November 2020).

- Russo, M.; Feng, T. Contact Tracing Accelerates a Lot of Opportunities and Risks: The Economy of IoT Data Sharing. 2020. Available online: https://www.bcg.com/publications/2020/contact-tracing-accelerates-iot-opportunities-and-risks-2 (accessed on 27 November 2020).

- Chan, T.; Lang, N.; Modi, S.; Tang, T.; von Szcepanski, K. How Chinese Digital Ecosystem Battle COVID 19. 2020. Available online: https://www.bcg.com/publications/2020/how-chinese-digital-ecosystems-battled-covid-19 (accessed on 27 November 2020).

- Kropp, M.; Andersen, P. How to Price-and-Sell in a Pandemic. 2020. Available online: https://www.bcg.com/capabilities/marketing-sales/best-practices-for-sales-managers-covid-19 (accessed on 27 November 2020).

- McKinsey & Company. COVID-19 and the Great Reset: Briefing Note #31, November 2020. Available online: https://www.mckinsey.de/business-functions/risk/our-insights/covid-19-implications-for-business (accessed on 27 November 2020).

- Bona, C.; Koslow, L.; Frantz, R.; Nadres, B.; Ratacjczak, D. How Marketers Can Win with the Gen Z and Millenials Post-COVID. 2020. Available online: https://www.bcg.com/publications/2020/how-marketers-can-win-with-gen-z-millennials-post-covid (accessed on 27 November 2020).

- Lesser, R.; Reeves, M. Leading out Adversity. 2020. Available online: https://www.bcg.com/publications/2020/business-resilience-lessons-covid-19 (accessed on 27 November 2020).

- Barcaccia, G.; D’Agostino, V.; Zotti, A.; Cozzi, B. Impact of the SARS-CoV-2 on the Italian Agri-food Sector: An Analysis of the Quarter of Pandemic Lockdown and Clues for a Socio-Economic and Territorial Restart. Sustainability 2020, 12, 5651. [Google Scholar] [CrossRef]

- Hossain, S.T. Impacts of COVID-19 on the agri-food sector: Food security policies of asian productivity organization members. J. Agric. Sci. 2020, 15, 116–132. [Google Scholar] [CrossRef]

- Patterson, G.T.; Thomas, L.F.; Coyne, L.A.; Rushton, J. Moving health to the heart of agri-food policies; mitigating risk from our food systems. Glob. Food Sec. 2020, 26, 100424. [Google Scholar] [CrossRef] [PubMed]

- UNIDO. Agri-Food and COVID-19 in Egypt: Adaptation, Recovery and Transformation; United Nations Industrial Development organization: 2020. Available online: https://www.unido.org/sites/default/files/files/2020-09/IGGE_Agrifood_and_COVID19.pdf (accessed on 17 April 2021).

- FAO. Adjusting Business Models to Sustain Agri-Food Enterprises during COVID-19. 2020. Rome. Available online: https://doi.org/10.4060/ca8996en (accessed on 12 December 2020).

- Stephens, E.C.; Martin, G.; van Wijk, M.; Timsina, J.; Snow, V. Impacts of COVID-19 on Agricultural and food systems worldwide and on progress to the sustainable development goals. Agric. Syst. 2020, 183, 102873. [Google Scholar] [CrossRef] [PubMed]

- Torero, M. Without food, there can be no exit from the pandemic. Countries must join forces to avert a global food crisis from COVID-19. Nature 2020, 580, 588–589. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Mukhamedjanova, K. The impact of the Covid-19 pandemic on the supply chain of agricultural products. Asian J. Technol. Manag. Res. 2020, 10, 49–52. [Google Scholar]

- Caldart, A.; Gifra, J.; Akhmedova, A.; La Crisis de la COVID-19 en el Sector de Alimentación y Bebidas. Impacto y Futuro. 2021. IESE Business School. University of Navarra 2021, 17. Available online: https://media.iese.edu/research/pdfs/ST-0608 (accessed on 10 April 2021).

- FIAB. Impacto de la Crisis del COVID-19 en la Industria de Alimentación y Bebidas Española; Spanish Federation of Food and Beverage Industries: 2020. Available online: https://fiab.es/producto/impacto-covid-19-industria-alimentacion-y-bebidas/ (accessed on 11 April 2021).

- Ruiz, J.I. Metodología de la Investigación Cualitativa, 4th ed.; Universidad Deusto: Bilbao, Spain, 2007. [Google Scholar]

- Yin, R.K. Case Study Research: Design and Methods (Applied Social Research Methods); Sage: Newbury Park, CA, USA, 1989. [Google Scholar]

- Tell, J.; Hoveskog, M.; Ulvenblad, P.; Ulvenblad, P.-O.; Barth, H.; Ståhl, J. Business model innovation in the agri-food sector: A literature review. Brit. Food J. 2016, 118, 1462–1476. [Google Scholar] [CrossRef]

- MAPA. Informe del consumo alimentario en España 2018; Ministerio de Agricultura, Pesca y Alimentación: 2019. Available online: https://www.mapa.gob.es/images/es/20190807_informedeconsumo2018pdf_tcm30-512256.pdf (accessed on 10 April 2021).

- EIT Food. Impact of COVID-19 on the Food Sector in Southern Europe. Madrid. 2020. Available online: https://www.eitfood.eu/projects/food-foresight (accessed on 10 January 2021).

- Zhang, Y.; Diao, X.; Chen, K.Z.; Robinson, S.; Fan, S. Impact of COVID-19 on China’s macroeconomy and agri-food system—An economy-wide multiplier model analysis. China Agric. Econ. Rev. 2020, 12, 387–407. [Google Scholar] [CrossRef]

- United Nations. Sustainable Development Goals. United Nations. 2019. Available online: https://sdgs.un.org/goals (accessed on 17 April 2021).

| Company | Interviewed | Gender | Modality | Date | Length |

|---|---|---|---|---|---|

| Company 1 | CFO | Female | On-site | 28 February 2020 | 1 h 50 m |

| Company 2 | CEO 1 | Male | On-site | 13 March 2020 | 1 h 15 m |

| Company 3 | Commercial Director | Female | Video-conference | 8 June 2020 | 2 h |

| Company 4 | CEO | Male | Video-conference | 18 June 2020 | 1 h |

| Company 5 | CEO | Male | Video-conference | 25 June 2020 | 1 h 15 m |

| Company 6 | CEO | Male | Video-conference | 6 July 2020 | 1 h 15 m |

| Company 7 | Operations Director | Male | Video-conference | 7 July 2020 | 1 h |

| Company 8 | CEO | Male | Video-conference | 8 July 2020 | 1 h |

| Company 9 | CEO | Male | Video-conference | 18 July 2020 | 1 h 30 m |

| Company 10 | Department Manager | Male | Video-conference | 20 July 2020 | 50 m |

| Company 11 | Operations Director | Male | Video-conference | 28 September 2020 | 1 h |

| CEO | Male | Video-conference | 6 October 2020 | 1 h | |

| Company 12 | Department Manager | Female | Video-conference | 5 October 2020 | 45 m |

| Company 13 | CEO | Female | Video-conference | 15 October 2020 | 55 m |

| Company 14 | CEO | Male | Video-conference | 30 October 2020 | 1 h 30 m |

| Company 15 | CEO | Male | Video-conference | 12 January 2021 | 1 h 15 m |

| Technology center | CEO | Male | Video-conference | 7 October 2020 | 35 m |

| Company | NCEA 2009 1 | Number of Employees | Turnover | Export | Position in Value Chain | Destination Channels |

|---|---|---|---|---|---|---|

| Company 1 | 103 | 600 | >EUR 10,000,000 | Yes | Transformation | Other processing industry |

| Company 2 | 104 | 3 | EUR 1,000,001–2,000,000 | Yes | Transformation Commercialization | Retail market |

| Company 3 | 110 | 3 | EUR 0–500,000 | Yes | Production Transformation Commercialization | Retail market |

| Company 4 | 110 | 10 | EUR 1,000,001–2,000,000 | Yes | Production Transformation Commercialization | Horeca channel |

| Company 5 | 108 | 1 | EUR 0–500,000 | No | Commercialization | Retail market |

| Company 6 | 109 | 70 | >EUR 10,000,000 | Yes | Production Transformation Commercialization | Other processing industry Final consumer |

| Company 7 | 103 | 60 | >EUR 10,000,000 | Yes | Transformation Commercialization | Horeca channel Retail market |

| Company 8 | 104 | 35 | >EUR 10,000,000 | Yes | Transformation Commercialization | Horeca channel Retail market |

| Company 9 | 101 | 9 | EUR 500,001–1,000,000 | Yes | Commercialization | Horeca channel Final consumer |

| Company 10 | 109 | 10 | EUR 6,000,001–10,000,000 | Yes | Commercialization | Final consumer |

| Company 11 | 101 | 66 | >EUR 10,000,000 | Yes | Production Transformation Commercialization | Horeca channel Final consumer Retail market |

| Company 12 | 101 | 200 | >EUR 10,000,000 | Yes | Transformation Commercialization | Horeca channel Retail consumer |

| Company 13 | 103 | 110 | >EUR 10,000,000 | Yes | Production Transformation Commercialization | Horeca channel Retail market |

| Company 14 | 103 | 55 | >EUR 10,000,000 | Yes | Production Transformation | Other processing industry |

| Company 15 | 103 | 6 | EUR 6,000,001–10,000,000 | Yes | Production Transformation Commercialization | Horeca channel Retail market |

| Technology center | 721 | 49 | >EUR 2,000,000 | Yes | Production Transformation Commercialization | Final customer |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Corchuelo Martínez-Azúa, B.; López-Salazar, P.E.; Sama-Berrocal, C. Impact of the COVID-19 Pandemic on Agri-Food Companies in the Region of Extremadura (Spain). Agronomy 2021, 11, 971. https://doi.org/10.3390/agronomy11050971

Corchuelo Martínez-Azúa B, López-Salazar PE, Sama-Berrocal C. Impact of the COVID-19 Pandemic on Agri-Food Companies in the Region of Extremadura (Spain). Agronomy. 2021; 11(5):971. https://doi.org/10.3390/agronomy11050971

Chicago/Turabian StyleCorchuelo Martínez-Azúa, Beatriz, Pedro Eugenio López-Salazar, and Celia Sama-Berrocal. 2021. "Impact of the COVID-19 Pandemic on Agri-Food Companies in the Region of Extremadura (Spain)" Agronomy 11, no. 5: 971. https://doi.org/10.3390/agronomy11050971

APA StyleCorchuelo Martínez-Azúa, B., López-Salazar, P. E., & Sama-Berrocal, C. (2021). Impact of the COVID-19 Pandemic on Agri-Food Companies in the Region of Extremadura (Spain). Agronomy, 11(5), 971. https://doi.org/10.3390/agronomy11050971