1. Introduction

The institutional changes that have taken place in the Russian economy over the past thirty years demonstrate a sharp breakdown of agricultural development trends. The article elaborates the four-staged history of transformations of socio-economic relations in rural areas. The first stage is characterized by collective, state ownership of land and means of production and a minimal amount of micro-ownership. At the second stage, the basic laws were adopted, which allowed a new class of landowners to appear, but did not offer common and understandable “rules of the game”. At the third stage, a mixed agriculture, combining state and private property, was shaped, and many diverse actors began to develop rural lands, which consequently led to various conflicts and problems. Among these problems are social stratification and incomplete social legitimacy. The fourth stage is characterized by the strengthening of the government role, the rapid enlargement of the owners’ class and the further increase in social stratification. However, a positive effect was also very noticeable, since from a country of food shortages and imports, Russia became an exporter of a number of agricultural products. The Russian case is very instructive on a global scale, since no country in the world has experienced such a long withdrawal from private property and market principles, which required dramatic efforts by all participants of production chains and property relations. Institutional gaps in agriculture are particularly significant, since the issue of private ownership of land remains open, and institutions for supporting agriculture have not settled down. The experience of post-Soviet market transformations in Russia is important for studying due to the caused negative effects that require careful and consistent attention.

The article aims to study the impact of institutional reforms on the structure and dynamics of market agents in rural areas of Russia from 1990 to 2020. Methodologically, the work is carried out in the traditions of modern critical institutional economics. We relied on new approaches of institutional analysis in the subject areas of economics and the sociology of agriculture. We based on the study of statistical and sociological data on the development of agriculture and rural areas of Russia. The research topic is the behavioral characteristics of economic agents (small, medium and large), as well as economic and social processes associated with the creation of new and the destruction of old institutions in rural areas of post-Soviet Russia. It seems to us that a more complete understanding of specifics and prospects of rural development in a country that encompasses more than one-eighth of Earth’s inhabited land area is impossible without immersion in a more general institutional context.

The object of the study is institutions that facilitate post-Soviet (market) transformations in Russian rural areas. The main institutions are the land reform; the state policy of supporting agriculture; the principles and results of the development of the agricultural products market; social relations and behavior of the main market actors. In this article, the role of governmental, social and economic institutions is considered. We note the relativity of this classification, since each considered category comprises the characteristics of the other two. Governmental institutions provide the legal framework, regulatory documents, structures, and other forms that facilitate transformations in rural areas. Social institutions designate the relationships and activities of the main actors. Economic institutions determine the ways and forms of economic activities. Such a threefold nature determines the complexity of the analysis and understanding of emerging processes. In this article, the main focus is on the issue of ownership of land and the form of economic activities on this land.

A statistical analysis of agricultural production is carried out, and the effects of “holdingization” and the main problems associated with the policy of state support are shown. When analyzing Russian statistical data, it is necessary to note that the operation of Russian agricultural businesses needs to be «decoded», since the principles of transparency and openness have only recently begun to be applicable to agricultural holdings (mandatory publication of budgets and reports, full information on state support). Small businesses and peasant farms report on their operation very poorly and fragmentally. Therefore, our analysis involved in-depth interviews with economic and social actors of rural territories. The interview narrative reflects historical and social perceptions, as well as features and motives of the actors’ behavior.

The limitations are determined, in the first, by the institutional approach itself, as it relies on the analysis of subjective data. In this article, we used the opinions and assessments of expert groups—“civil society activists” and “entrepreneurs”, who live and work in rural territories. In the second, statistics on the operation of market actors are very distorted. In the third, we mainly used the data on large and small (including individual) actors, since the data on medium-sized businesses is fragmentary and requires additional study. We agree that medium businesses ensure the basis for the sustainable development of the territory, since they involve bigger masses of local residents in modern entrepreneurship. However, the current situation has inalienable features, such as excessive reliance on the government, consolidation of land and capital and “holdingization”, which determine a partial withdrawal of medium-sized businesses from the territories and weakens their market positions. However, these conclusions need to be tested on other data using other methods.

2. Materials and Literature Review

Human communities traditionally consisted mainly of the rural population, which was engaged in agricultural activities. Resource transfer systems along supply chains from source to producer and consumer were localized, and supply chains were short. In the twenty-first century, it changed significantly. As shown by W. Myers and T. Johnson, the role of agriculture in the evolution and historical development of countries is significant. In turn, evolution cannot be understood without recognizing the role of public policy in changing the agricultural sector. Agricultural and rural policy is shaped by the processes of collective choice within the institutional and socio-economic contexts [

1]. Currently, production and consumption in agriculture are viewed as an institutionalized, socio-economic and psychologically self-determining practice that is run and promoted by both corporations and governments.

Our research continues the tradition of critical institutional economics, which analyses conventions, norms, practices, rules and regulations used by humans to coordinate socio-economic interaction [

2] (p. 13). We proceed from the assumption that institutions are not only formal and informal rules of the game and social norms, but also symbolic systems, cognitive scenarios and classifications that make the actions possible and impart importance to interactions and situations. Institutions provide expectations, stability and meaning necessary for human existence and behavior coordination, as well as support values, create and protect interests [

3] (p. 31). In our research, we rely on institutional approaches to explain how fundamentally new institutions were built in a historically short period of time, which successfully replaced the traditional ones.

In the context of normative aspect, it is important to note that human actions may be largely regulated by rules and patterns of behavior. These rules are followed because people consider it natural, legitimate and expected. Socially embedded actors strive to fulfill obligations associated with their role, identity, community or group membership [

4,

5,

6] and therefore adjust their actions to situations. In this regard, the sociological school of institutional studies continues the ideas of E. Durkheim, T. Parsons and R. Merton as theorists of institutional systems. The works of these authors emphasize the normative dimension of institutions. R. Merton wrote that identification and habituation are fundamental mechanisms of individual and group behavior [

7]. Within the sociological framework, the main definitions important for the intention of this article are introduced: institutional requirements; institutional procedures; deinstitutionalization; institutionalized means [

7] (pp. 177–204). It is also emphasized that the level of motivational analysis is mistaken for the level of institutional analysis [

7] (p. 587). A. Giddens, when developing a concept of institutionalization, focused on the structuring and organization of institutions [

8].

R. Scott distinguishes three key components of these processes: regulatory, normative and cultural-cognitive. The different perceptions of institutions in connection with the mentioned components are examined in his works. He develops institutional logic, identifies institutional carriers, emphasizes the complexity of the analysis of hierarchical levels and explores the processes of institutionalization and deinstitutionalization [

9].

We reveal behavioral aspect of this dynamics through the study of real practices of representatives of business and authorities in rural territories of Russia. Open data of accounting and economic reporting of agricultural companies are involved. Based on the conclusions of P. A. Hall and R. C. Taylor on the new institutionalism [

10], we identify the key points of the state institutional organization that structure collective behavior and lead to distinctive outcomes. The state is considered not as a neutral mediator between competing interests of economic agents but as a complex of institutions capable of structuring the nature and results of any group conflicts. Institutions vary according to the rules of the constitutional system, bureaucratic procedures and conventions that govern behavior. The ideas of the addressed scientific schools allowed us to explore social and political institutions; to analyze the structure of interactions at the macro-, meso- and micro-levels; to reveal nation-specific development trajectories; to emphasize the influence of national political institutions on the structure and forms of relations between legislators, officials and the electorate.

Proponents of sociological institutionalism define institutions much more broadly than political scientists and economists do. They take into account not only formal rules, procedures, norms, but also symbol systems, cognitive scenarios and moral patterns, since they are believed to provide the key “semantic frameworks” of human actions. In this frame “culture” is redefined as “institutions”, which reflects the “cognitive turn” in sociology itself. This approach focuses on how semantic frameworks, scenarios and symbols arise from processes of interpretation and disagreement [

10] (pp. 937–947).

Mass urbanization, new social division of labor and expansion of economic markets have required approaches to be more functional. For the analysis in this article, the concept of territorial institutions is important, since it represents contexts of territorial policy as social and political structures for the governments of any country. The study of features and changes of territorial institutions composes own research area, where approaches that organize knowledge about the relationships between center and periphery dominate. Reflecting either a federal-centered or a pluralist perspective, the object of territorial policy is often intergovernmental relations. In centralized national states under the influence of Roman law, it is rather a relationship between the center and local authorities [

11] (p. 281).

The institutional conditions for the development of agricultural production are understood as the current norms and rules within which the agents of production and distribution in agriculture operate. Within the framework of institutional theory, governance depends not only on administration and officials, but also on changing identities and solidarities, as well as social competition. Rural spaces determine their own specifics for studying the constructive nature of institutions. In this sense, government institutions have power and legitimacy, while the participation of other actors is structured institutionally in one way or another. Differentiated localities eventually merge into a single national and regional reproduction system in rural areas. Functional and economic division of labor replaces their territorial roots and identities.

The institutional development of the European Union has opened new horizons of knowledge about the development of institutions [

12] (pp. 285–286). S. Tarrow and D. Ashford in their study of France, Great Britain, Italy and Sweden showed how institutions were built to support industries and how market regulation rules were constructed in conflicts between the “center” and the “periphery” of the European Union [

13,

14,

15,

16]. It turned out that the open borders do not always stimulate the development of production, as farmers and business executives resisted changes if their usual way of life was violated [

17]. Territorial policy and territorial institutions as scientific fields embraced many research approaches and interpretations, which sometimes leads to opposite conclusions. The lack of consensus was reinforced by ideological competition over the choice of a model of good government [

18,

19,

20]. It appeared that even with the preservation of market principles, traditional state management is gaining more power [

21]. It was assumed that historical evolution explains how the periphery is integrated and how national resources are distributed across localities. In this regard, interviews with local elected officials, administrators, representatives of communities, become an important source of data [

13]. In this article, we considered competing modes of production, institutional order and rules, based on qualitative and quantitative data that demonstrate the legitimacy of market development of agriculture. The transfer from full state regulation to a market-based arrangement is shown. Post-Soviet transformations are peculiar in their initial vector, which is opposite to the institutional transfer in Europe and the USA, as it moves from market to state or supra-state regulation [

21]. However, the lack of legitimacy and incompleteness of the transition led to an actual reversal to the dominance of large forms of management and the priority of state regulation.

In rural areas, the traditional (peripheral) way of life conflicts with global practices since innovative approaches to the organization of production and management of the territory compete with the usual ones [

22]. For example, due to the small number and low population density in peripheral territories, access to new technologies is limited [

23]. Cross-country analysis showed the significant role of the state in the development of rural areas and agriculture [

24]. Most countries are rapidly urbanizing. Rural-urban migration is often seen as a way to improve economic opportunities. It is particularly difficult to retain young people in rural areas, as they often move to urban areas for social and cultural reasons. The institutions that shape and regulate demographic processes also directly affect agriculture. However, in this paper, we will not consider such a wide range of influencing factors.

State policy has become the main institution for supporting (or resisting) land reform in Russia. But this country is no exception. For example, the Food and Agricultural Policy Research Institute conducted a study of global agricultural markets and showed the evolution of US and EU food policy [

25] (p. 60).

In the context of the stated problem field, the results of research on agriculture as a dynamic system are of interest, since these results point out that the development if influenced by temporal and spatial factors as well as induced effects between the system’s elements. The example of China’s economy is indicative. The country has adopted a new model of open agriculture, when the development of the domestic cycle is recognized as a priority, which subsequently contributes to the development of the international cycle. Wang D. et al. emphasize that local regional characteristics and capabilities are important, and this experience is especially significant for geographically large countries such as China, Canada, USA and Russia [

26]. The openness of agriculture contributes to the creation of new institutional formations in international markets—global trade networks of agricultural products. The analysis of one of these networks is presented in the works of Gutierrez-Moya E., Lozano S., Adenso-Diaz B. [

27].

Data on global trade networks and agricultural trade volume can be used to quantify the transfer of virtual land between countries. The study [

28] evaluates virtual land trade (VLT) related to world agricultural trade based on yield indicators in exporting countries. Institutional ties and players are being formed within national, geographical and economic groups that have a strong impact on society, the economy and the environment.

Emerging global land systems are increasingly dependent on international agricultural trade. More and more studies [

29,

30] are quantifying the diverse impacts that agricultural trade has on the sustainability of the land system.

It should be noted that the research of rural areas and territories is not limited only to zones favorable for agriculture, therefore we considered the results of other studies. The possibilities of building vertical farms in the Russian Arctic and new economic models of sustainable development are described in [

31]; the peculiarities of nutrition and health status of residents of the northern regions of the world and Russia are considered in [

32]; the problems of food security in the Russian Arctic are discussed in [

33]. In the related food products topic, the advantages and limitations of environmental efficiency measures are evaluated on the example of the Polish food industry [

34]. The analysis of consumer trust in quality and safety of food products in Western Siberia is presented in [

35]. The article [

36] examines and evaluates the impact of intellectual capital on the profitability of Russian agricultural firms. A theoretical study of the urban and rural territorial and social spaces in different countries is presented in the generalizing article [

37].

3. Data and Methods

The analysis involved documents and laws regulating agriculture in Russia for the period from 1990 to 2020. On the basis of open data of the Federal State Statistics Service, a database was formed for the period 1990–2020 (average annual) for the following variables (in total and for certain types of agricultural products): acreage (thousand hectares), production volume (gross harvest and livestock in physical and monetary terms), production indices, exports and imports, the number of people employed in agriculture [

38,

39,

40,

41]. According to the data of the Federal Service for State Registration, Cadastre and Cartography, information on the land fund and its use for the period from 1990 to 2020 was analyzed [

42]. The authors accumulated data from the Ministry of Agriculture of the Russian Federation, monitoring of the consulting company BEFL, research results published in Forbes magazine, reports of the largest Russian agricultural companies, which made it possible to characterize the activities of leading Russian agricultural holdings (Miratorg [Миратoрг], Agrocomplex [Агрoкoмплекс], Steppe Agroholding [Степь Аргoхoлдинг], EkoNivaAgro [ЭкoНиваАгрo], Prodimex [Прoдимекс], Rusagro [Русагрo]) [

43,

44,

45].

During the period 2020–2021, our research team conducted 59 expert interviews (

Appendix A Table A1). The informants were those individuals who are actively involved in the development of rural settlements and agricultural business. Interviews were conducted with experts in three categorical groups: executive managers and (or) owners of enterprises in agriculture (21 interviews), representatives of public organizations (19 interviews), representatives of regional (8 interviews) and local authorities (11 interviews). We used the snowball method to find informants. Informants from the categories “public” and “business” were selected based on a preliminary study of data on socio-economic development, industrial and socio-cultural potential of the territory; we also used information about operating agricultural enterprises and other open information.

The key criteria for the selection of respondents were: (1) type of settlement (“big” more than 5 thousand inhabitants—29; “small” up to 5 thousand inhabitants—30); (2) type of agricultural enterprise (“large and medium-sized”—10; “small”—11 interviews); (3) the level of economic development of an enterprise (“strong”, “medium”, “weak”). When searching informants for the “public” group, we conversed with the heads of rural settlements, local activists, representatives of veteran and youth organizations, and appealed to common residents of the countryside. The sample structure of the expert study is presented in

Appendix A. The interviews were face-to-face and semi-formalized; they were audio-recorded and subsequently transcribed. The interview guide contains four blocks of questions for discussion: (1) assessment of the agro-industrial complex institutional dynamics (company development stages; factors of advancement of agricultural territories; «growth points» of business and territory; social initiatives; social entrepreneurship); (2) assessment of economic behavior (socio-cultural, institutional and power bases of economic behavior; economic motivation; rational and irrational economic behavior; support for initiatives of entrepreneurs and citizens); (3) the main problems of rural territories (problems and necessary changes to solve them; the role of authorities, business, and community in providing problem-solving decisions); (4) image of the future of the countryside. Informants outlined the most important problems and commented on them in more detail. The analysis of our data in this article is given from the point of view of informal institutions—in the narratives of in–depth interviews in the triangle: government—business—local communities. The analysis of our data in this article is given from the point of view of informal institutions, presented through narratives of in-depth interviews in the triangle “government-business-local communities”.

4. Results

This section includes 4 subsections. The agrarian reform is described as the main manifestation of institutional changes that allowed the formation of a class of landowners in Russia, which was important for improving private land use and strengthening agricultural entrepreneurship. The main stages of the agrarian reform are outlined in

Section 4.1.

Section 4.2 examines the socio-economic aspects of transformations and presents the structural features of rural production. It is important to note that, declaratively, the goal of reforming Russian agriculture was to establish market relations and increase commodity production in the agro-industrial complex. However, an unexpected and socially contradictory result of the reforms was the creation of new actors—agricultural holdings. Agroholdings, despite their growing strength, are not represented in Russian legislation as a form of entrepreneurial activity. In official statistics on their operation, results of their structural units are presented separately, which distorts the picture of the real industry structure (

Section 4.3). Nevertheless, the positive dynamics of agricultural production can be considered the main result of institutional changes (

Section 4.4).

4.1. The Main Stages of Agrarian Reform

For almost the entire XX century, Russian economy existed in the paradigm of collective (public) or state property. Anything that did not fit into this idea was either discouraged (the so-called household plots or personal subsidiary farms) or prosecuted by law (the use of public property for individualistic purposes). The population held on to their tiny pieces of land as the last island of personal well-being, but this was despite the prevailing institutional order. By national standards, the share of production in household plots was negligible, the used technologies were backward and primitive, and the labor costs were enormous. However, in some segments, for example potato growing, personal subsidiary farms played a strong role of social damping, partly social protection and provided insurance in conditions of general deficit. There were so-called «food trains», when people came to Moscow and took away the necessary food products, because in their regions (including agrarian ones) they simply could not buy them. By the early 1990s, the Russian government recognized that the country was on the brink of famine. Incredibly, these events took place in a country that had some of the most extensive farmland in the world. Society wanted change, there was a consensus on the «transition to the market». But few people understood how and at what speed these changes should have taken place. One of the most painful areas to transform was agrarian reform.

The reforms began at a time when agricultural producers were forced to sell products at purchase prices below market prices, which led to a sharp decline in production volumes. The regulatory authorities acted in a fork between two equally unfavorable scenarios. On the one hand, a huge number of agricultural producers could not function without state support; the peculiarity of Russia is that many territories are unsuitable for agriculture (such as Siberia, the Far East and the Northern territories of Central Russia). On the other hand, the budget burden became unbearable and hindered other sectors of the economy. Since the federal budget could not compensate for the increasing difference between domestic purchase prices and world food prices and could not pay «tied loans», the government comprehended the possible threat of famine and decided to initiate an institutional reform in agriculture.

Agrarian reform had three main stages. The first stage is associated with the adoption of the Land Code of the RSFSR No. 1103-1 of 25 April 1991, which allowed the formal ownership of land for individuals and associations. The second stage (period of 1993–2000) is characterized by mass privatization of agricultural land, reorganization of collective farms (kolkhozes) and state farms (sovkhozes), according to the Decree of the President of the Russian Federation of 27 October 1993, No. 1767. The key point of the third stage, which began in 2001, was the adoption of the new Land Code of the Russian Federation on 25 October 2001, when the Federal Law No. 137 established private ownership of land. Formerly collectively owned land was excluded from public and federal ownership and became available for free purchase and sale. Eleven million of private landowners appeared in Russia, a class of recipients of agrarian reform was formed. To some extent, this stimulated the development of small and medium-sized businesses in the countryside. Many rural entrepreneurs were forced to rebuild their businesses due to the difficulties of the perestroika period. Illustrative quotes from the interview:

There was an economic situation… I was not paid a salary. I came up with the idea to start my own business. It worked. (Owner of bakery);

It did not depend on our desire, but time and situation demanded it. We enlarged, en-larged, and this leapfrog continued… (Owner of a dairy enterprise).

This period was accompanied by significant in dispersion and direction institutional changes in the Russian countryside, namely decollectivization, denationalization, concentration and subsequent centralization of land and other types of capital, the creation of new organizational forms of business—private farms and agricultural holdings.

The nature of these transformations can be judged by the change in the main indicators of the agricultural sector. At the beginning of the reforms, in 1990, the total area of sown crops was 117,705 thousand hectares. Over the next twenty years, this area steadily declined, and reached the value of 74,861 thousand hectares in 2010 (the acreage decreased by 36%). After that, the total area of crops increased, but at a much slower pace. In 2020, the acreage of Russia amounted to 79,948 thousand hectares (only 68% of the value at the beginning of the reforms) [

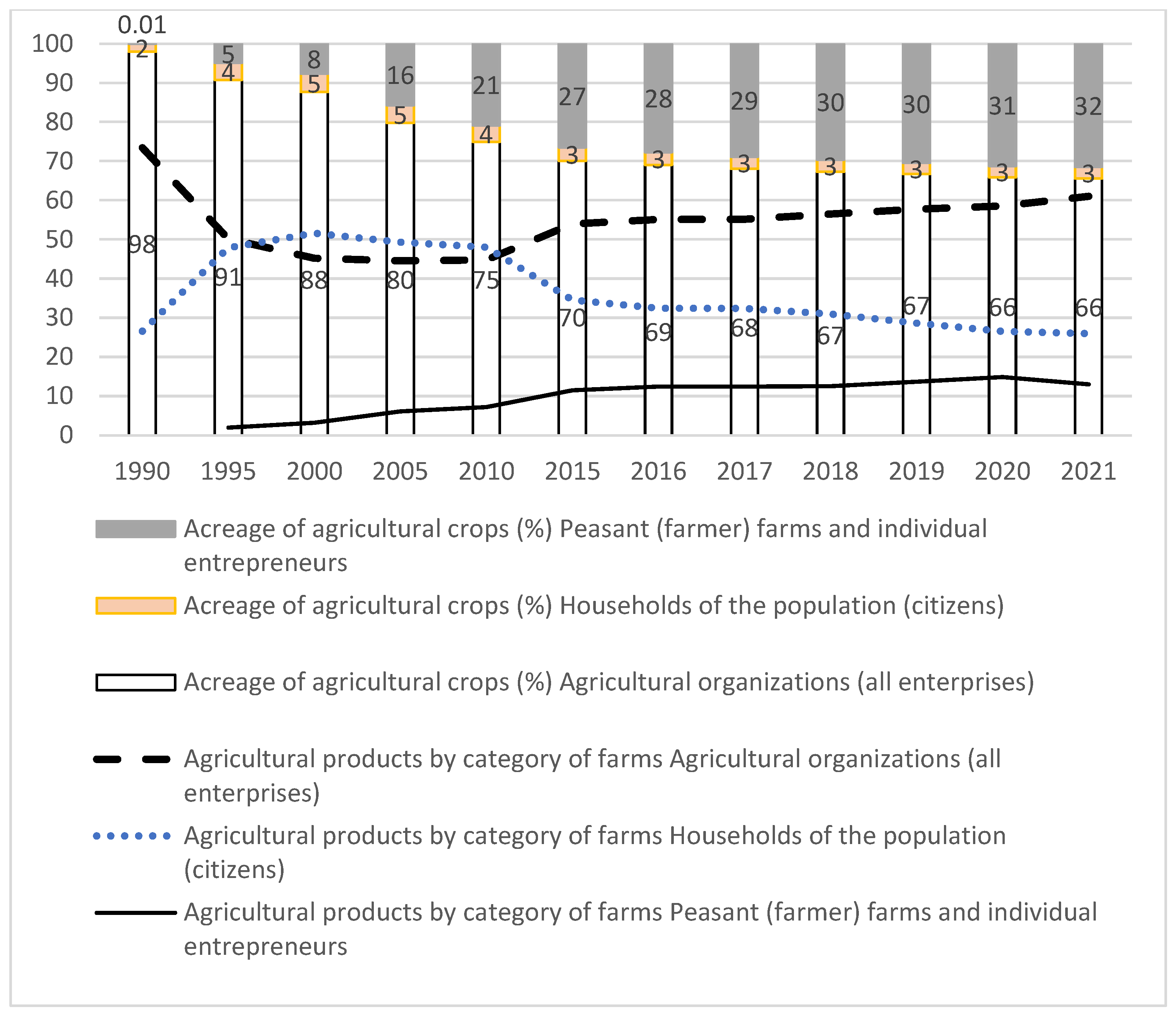

40]. The distribution of areas between entities of different types also changed between 1990 and 2020: the share of agricultural organizations decreased from 98% to 66%; the share of farms and individual entrepreneurs grew to 32%. This share is significantly lower than in countries with a long-standing farming culture, but it is very high for Russia. The share of private land of citizens is negligible and ranges from 2% to 5% in 2000–2005.

It is important to note that the share of production of different types of entities is incommensurable with their land shares. If household plots accounted for 27% of the total agricultural output in 1990, then during the destruction of kolkhozes and sovkhozes in 1995 they provided up to 52%. With the development of farming business, the share of household plots has decreased to 26% in the current period (

Figure 1).

The productivity of household plots differs significantly from agricultural organizations. According to the roughest estimates, the relative efficiency of one hectare in household plots is 20 times higher than the efficiency of farms, and 10 times higher than the efficiency of agricultural organizations. The household plots have always been characterized by an extremely low level of technology and were actually self-exploitation. Russian rural residents were used to the fact that working on kolkhozes and sovkhozes did not bring them sufficient income, and tried to create a “safety cushion” using personal subsidiary farms, which allowed providing themselves with sufficient amount of crop and livestock products.

As a result of reforms and institutional transformations in agriculture, Russia managed to rise in the world agricultural ranking from 21st place in 2000 to 9th place in 2020. The volume of production in Russian agriculture in 2020 amounted to 54.9 billion dollars at current prices (

Table 1). This indicator is comparable to the level of Pakistan (

$58.5 billion) and Japan (

$54.0 billion). The share of Russian agriculture in the world is equal to 1.5%.

Despite a significant increase in gross agricultural indicators, Russia ranked only 97th in the world per capita in 2020 (

$376.2), which is 26% less than the global average (

$474.4). Comparing the performance of agriculture in Russia with the industry leaders, it should be noted that the country lags behind Iran by 75.3% (

$1523.8 per capita), China by 53.9% (

$816.6 per capita), Indonesia by 29.1% (

$530.3 per capita), the United States by 28.6% (

$527.2 per capita) [

47].

Simultaneously with the land reform and changes in the structure of production, there were transformations of socio-economic, demographic, territorial and socio-cultural relations in rural areas. These changes are associated with an increase in social inequalities, which will be shown below.

4.2. Socio-Economic Aspects of Transformations

Socio-economic aspects of transformations in rural areas of Russia for the period 1990–2021 can be summarized in the following theses: (1) the goals of multi-structurization of rural economy on the basis of land privatization, reorganization of collective farms and state farms have been solved; (2) transition from directive-planning relations to market relations; (3) ensuring the turnover of land and means of production, maintaining control over the quality of agricultural products, replenishing state reserves; (4) conditions have been created for conducting agro-industrial business at the so-called “socially acceptable prices”, which allowed to saturate the domestic market with food and agricultural raw materials; (5) the Russian state has organized subsidies, subventions, grants, social benefits and other forms of support for agricultural producers in the rural areas; (6) agribusinesses were exempted from obligations to finance the construction and maintenance of social facilities and engineering infrastructure; these duties were assigned to municipal authorities; (7) a market for land shares and land plots has emerged, which has established a clear institutional framework for the mobility of land resources; for the first time in the rural territories, «commodity lending» is employed. But the general goal of the social revival of the countryside was not achieved. This is one of the main problems and contradictions of the modern development of rural areas in Russia. Examples of quotes from expert interviews:

What good can there be in the village? It’s miserable, forgotten. At least the roads were slightly repaired, a couple of streets were paved with gravel, we won’t live to see asphalt concrete here. (Head of collective farm);

The whole problem… is largely in the infrastructure. Because people should be convinced that they will receive normal primary healthcare… and their children will get a normal education and will be able to develop culturally, too. (Owner of plant growing business);

People are moving to centers (cities or bigger towns). So, one way or another, the process is going on, and it will continue… (Representative of regional authorities).

Nevertheless, the most important incentives for the modernization of Russian agriculture have been provided, namely: elite seed production and animal husbandry; new equipment (through the system of preferential agricultural leasing); opened access to subsidized investment loans; debts restructuring; Federal Law established criteria for classifying a business entity as a micro, small, medium, and large (Federal Law No. 209 of 24.07.2007). Examples of quotes from expert interviews.

…You can’t stand still, you need to move, develop, go forward. If you just stop, others will immediately trample you and forget tomorrow. For success, you also need a team and must educate its members. (Owner of the enterprise, plant growing);

Our company has always needed to develop. We started working on the old equipment. To grow, we took a risk, got a loan, and purchased a building, made reconstruction works, bought new equipment, increased production facilities, bought new equipment again. (Owner of the production of bread products).

New problems are identified in determining the effectiveness of agricultural organizations: if earlier the «income» included means of state support (subsidies, subventions, grants, social benefits), now a relatively new indicator—revenue—has become key. If total income integrates state support, it may characterize a business entity not in a positive sense of labor efficiency, but rather in a “negative” sense of ability to build institutional relations with decision-makers on the allocation of subsidies, subventions, grants in conditions of limited rare resources and unequal access to them. Examples of quotes from expert interviews:

We are actively working with the heads of villages. They do not deny us anything. (Head of collective farm);

We are working with the regional department of agriculture today… They hear us. That’s why they subsidize these programs, and we need to show up and let them see us. To avoid any difficulties later. First, if something needs to be agreed, we go to the head of the district to enlist his support. It opens doors. Say, a letter from me is one thing, a letter from him is, of course, another (Dairy farm executive manager);

After we talked with the governor on this topic, he immediately came to us. We have been working with the Agricultural Academy since then. (Owner of an agricultural enterprise);

The authorities turn to business for support on a regular basis. I help as much as possible, sometimes I have to refuse. (Owner of the enterprise, plant growing).

It should be noted that questions on environmental aspects of agriculture are not articulated and moreover are directly rejected by respondents during the interview. Most small farms use natural ingredients in their work and do not resort to chemicals and pesticides. While large producers claim that the further development of eco-oriented forms of agriculture has a doubtful potential for profitability and may even be an unbearable burden. The promotion of eco-products to regional markets is associated with problems: prices are often excessively high; people do not distinguish between eco and usual products; unwillingness to change consumer habits. According to expert statements, sufficient demand for eco-products arises only in large cities:

Our farmers do not use any harmful additives… It’s all environmentally friendly… Small business always has cleaner foods. (Owner of a small business);

We do not have so many people who buy up such a volume of ecological product… We do not use growth hormones and graze cattle in meadows that are not treated with chemicals. In winter, cows eat grain that we have grown. (Owner of a small business);

Natural products like lettuce grown on the ground naturally, are in demand today in cities with a population of more than 1 million: St. Petersburg, Moscow. (Representative of the authorities);

Many people understand that this is a very difficult path, because if you want to meet certain standards, it will be necessary to change equipment, and sometimes fundamentally rebuild production… In order to go beyond one’s own locality to new markets, additional resources are needed… The main limitation is the economic factor. (Representative of the authorities).

However, the Russian segment of eco-products has great resource potential, due to the vast territory with a favorable ecological situation (areas remote from industrial centers suitable for harvesting wild berries and herbs, as well as a significant area of productive agricultural land).

4.3. Agricultural Holdings as a New Actor of Changes

A wide variety of organizational forms of business entities in agriculture and their relationships with government bodies cause problems when assessing business effectiveness. In this context, the definition of agroholding matters. In general, an agricultural holding (agroholding) is understood as a company that owns controlling stakes in other agricultural firms, which gives the opportunity to manage their operation.

We agree with the standpoint that agricultural holding interprets not as a form of vertical integration, but as a form of concentration of land ownership. This is a possession of a fund of a land bank, estimated by the area (in hectares) and the market value. W. Myers and K. Scheder drew attention to this very important point when comparing the new rural development programs of different countries of the European Union. They note significant differences in direct payments between countries, ranging from 100 euros per hectare in Latvia to 466 euros in the Netherlands [

25] (p. 67). These features are economically determined, since they reflect the quality of the land, its commodity composition, the intensity of land use, the cost of production, regional payment models. At the same time, a sense of injustice persists. The Common Agricultural Policy for Rural Development of the European Union also faces such problems.

Using the ideas of the «land bank fund» and land valuation, the authors approach the issue of identifying the forms of agricultural organizations in Russia according to four priorities: land bank (area of agricultural land), «value» (market price of agricultural land), revenue and net profit. If these quantitative and qualitative data are presented in matrix form, we will get a fairly convincing picture of the dynamics of the largest land holdings in Russia over the past few years (

Table 2).

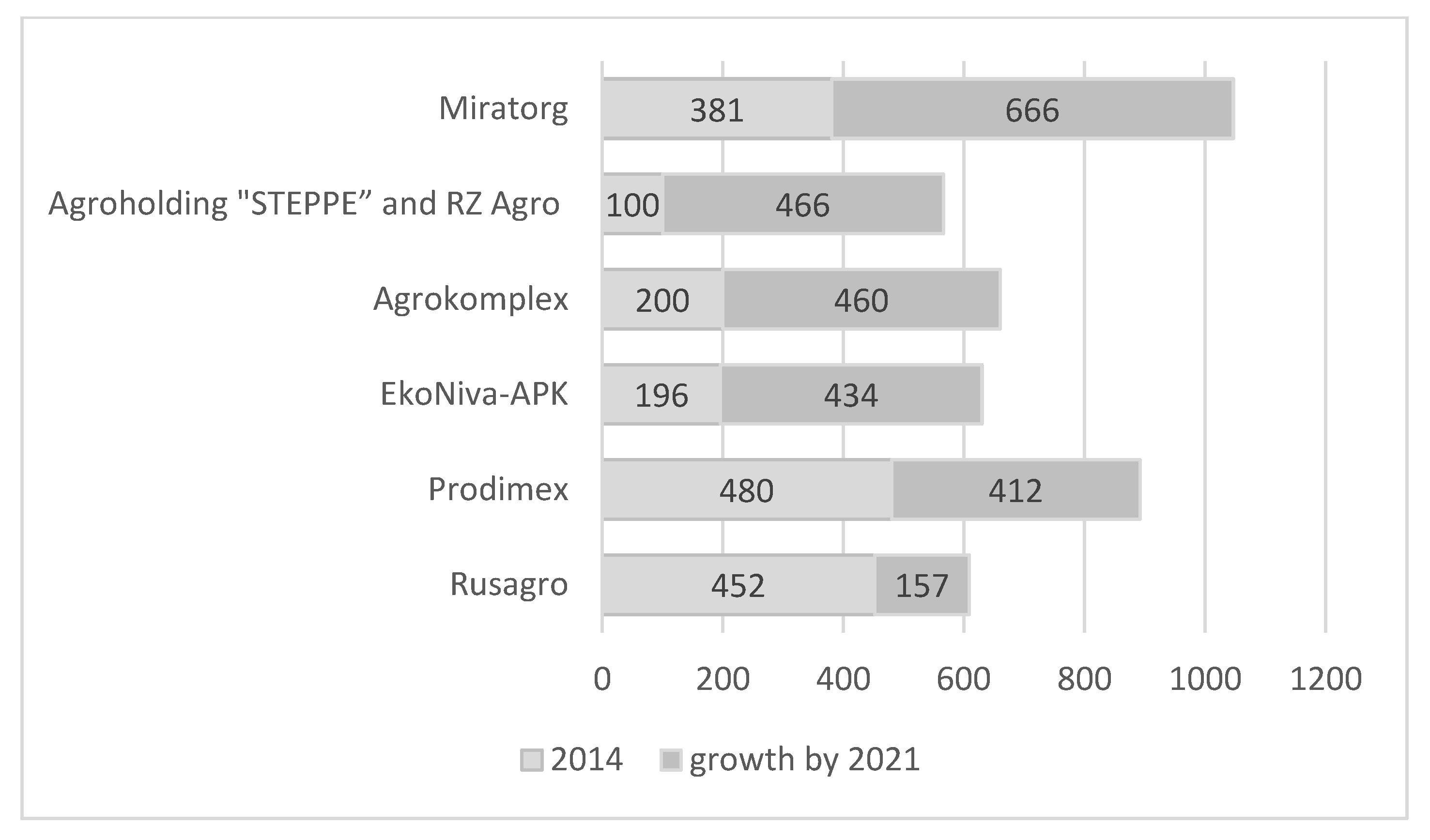

According to consulting company BEFL, which regularly ranks the largest owners of agricultural land in Russia, over the period of 2014–2021 the number of such owners increased from 30 to 66, and the total land bank of these companies increased from 7.2 million hectares to 15.4 million hectares [

44]. The cost of total agricultural land in 2020 was 617.3 billion rubles (in market prices) [

45]. In Russia, there is an increase in the land bank of the largest agricultural holdings, especially in the last three years. The total land bank in 2012 was 3828 thousand hectares, in 2017–5198 thousand hectares, in 2021–6135 thousand hectares. This trend is due to the currently high profitability of crop production, since there is a significant increase in commodity prices on world markets. As a result, excess profits are actively invested in the further expansion of the land bank, and investors from other industries appear on the market. In 2019, several large mergers and acquisitions of agricultural assets with significant land banks were publicly announced. The leaders of Russian agribusiness demonstrate a general trend of increasing land assets over the past decade and especially since 2019. However, the growth of the land bank is much faster for companies from the top ten of the rating than for other players [

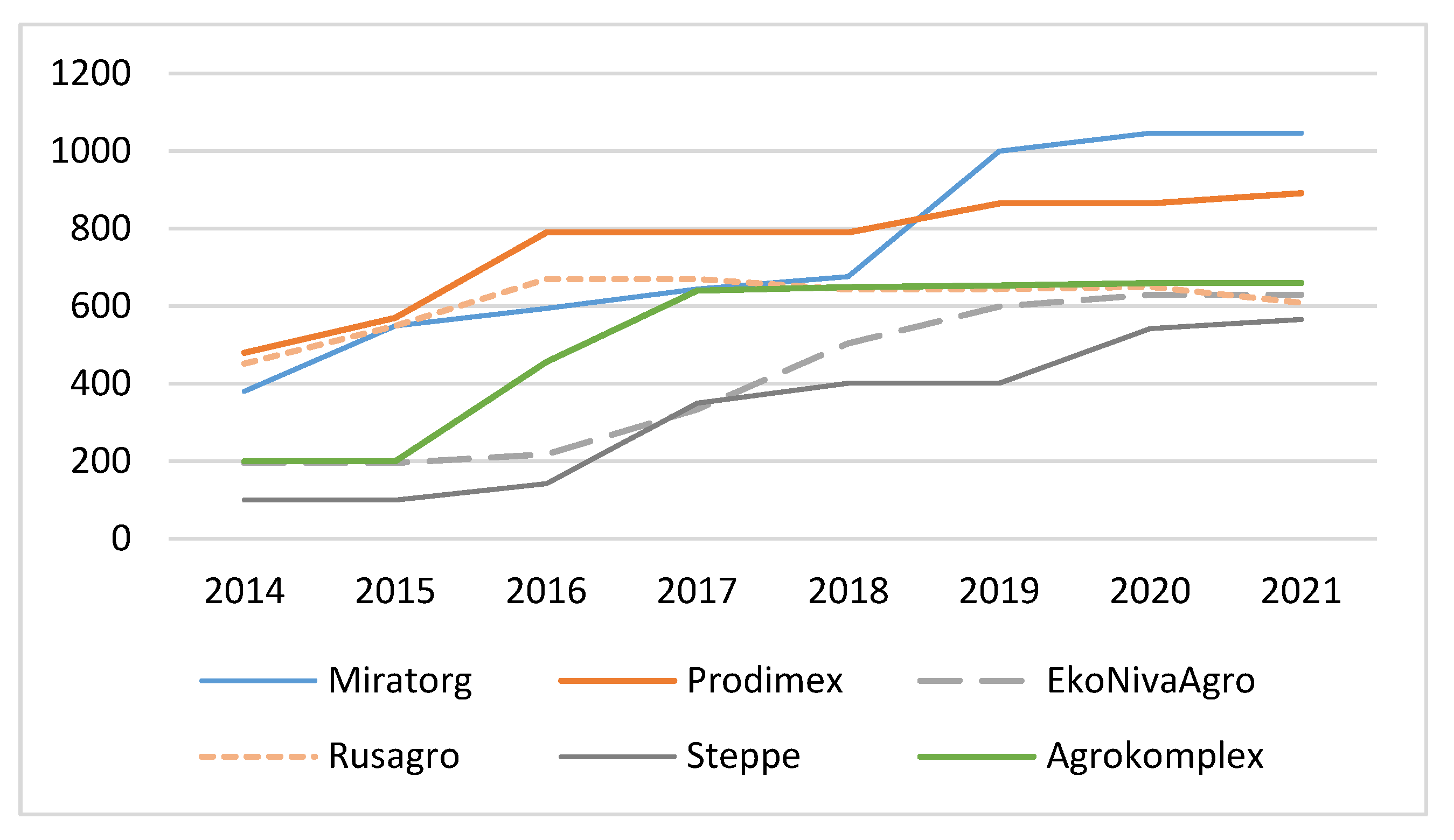

43]. This trend is illustrated in

Figure 2.

Miratorg is in first place in terms of land fund growth (+ 666 thousand hectares over seven years), followed by Agrocomplex (+460 thousand hectares), Steppe (+466 thousand hectares), EkoNivaAgro (+434 thousand hectares), Prodimex (+412 thousand hectares), Rusagro (+157 thousand hectares) completes the rating, despite a slight decrease in the land bank in recent years (

Figure 3).

The share of agricultural holdings in the total revenue of crop production is 31% (data for 2020). A similar situation is observed in another key branch of agriculture—livestock, where the share of agricultural holdings is estimated at 37%. The revenue of the largest meat producers in 2020 increased by 1% compared to the previous year. More than a third of all meat in Russia is produced in 10 leading agricultural holdings (the leaders are Miratorg [Миратoрг], Cherkizovo Group [Черкизoвo], The Resource Group of Companies [Группа кoмпаний Ресурс]). Meat production increased from 10.9 million tons in 2019 to 11.2 million tons in 2020. The consolidation of agricultural holdings is also taking place in the oil and fat sector, as their share in the revenue reached 61% in 2020, compared to 60% in 2019 [

43]. This is also confirmed by experts.

The following are examples of quotes from expert interviews:

If we talk about Federal support without embellishment, then the most serious support is provided to holdings today. Well, that’s all clear. Whoever belongs to this holding develops, and smaller ones are absorbed or dissolved… (Regional power);

Until 2012, there was super support in general, and the budget apparently had money. Until 2014, we purchased equipment for subsidies… we were paid more than a billion rubles for equipment alone. Then things got more complicated. (Senior manager of the company that belongs to agroholding);

The support is incoherent… small businesses receive it on one scheme, large ones on another. Second question is whether this is enough or not enough… Now there is also the issue of lending, which also does not seem to depend entirely on us. Today, in general, bankers do not really want to work with small proprietors… Why would they work with 20 small farms if they can give someone a large 50-million loan? (Owner of a small business);

It turns out that we do not have state support, but some kind of maintenance or allowance. For example, my company was originally built in such a way that there were no unnecessary costs, it was built with an understanding of future operation and service. Many other enterprises in our district were built on state support simply in order to take it more and more later. In general, the fact is that many enterprises were thoughtlessly organized. (Owner of a small business).

Thus, a new actor has appeared in the modern Russian agro-industrial complex—agroholding. Even though Russian legislation does not give a clear interpretation of agroholdings as an organizational form of entrepreneurial activity, they are gaining strength and increasingly determine the trend of consolidation of agricultural business. It is quite difficult to have an objective picture of the scale of their development, since official statistics take into account their business results separately by structural units.

4.4. Dynamics of Agricultural Products Market Development

If we consider Russia’s agro-industrial production in a global context, it is important to emphasize that the country ranks third in terms of arable land area after the USA and India [

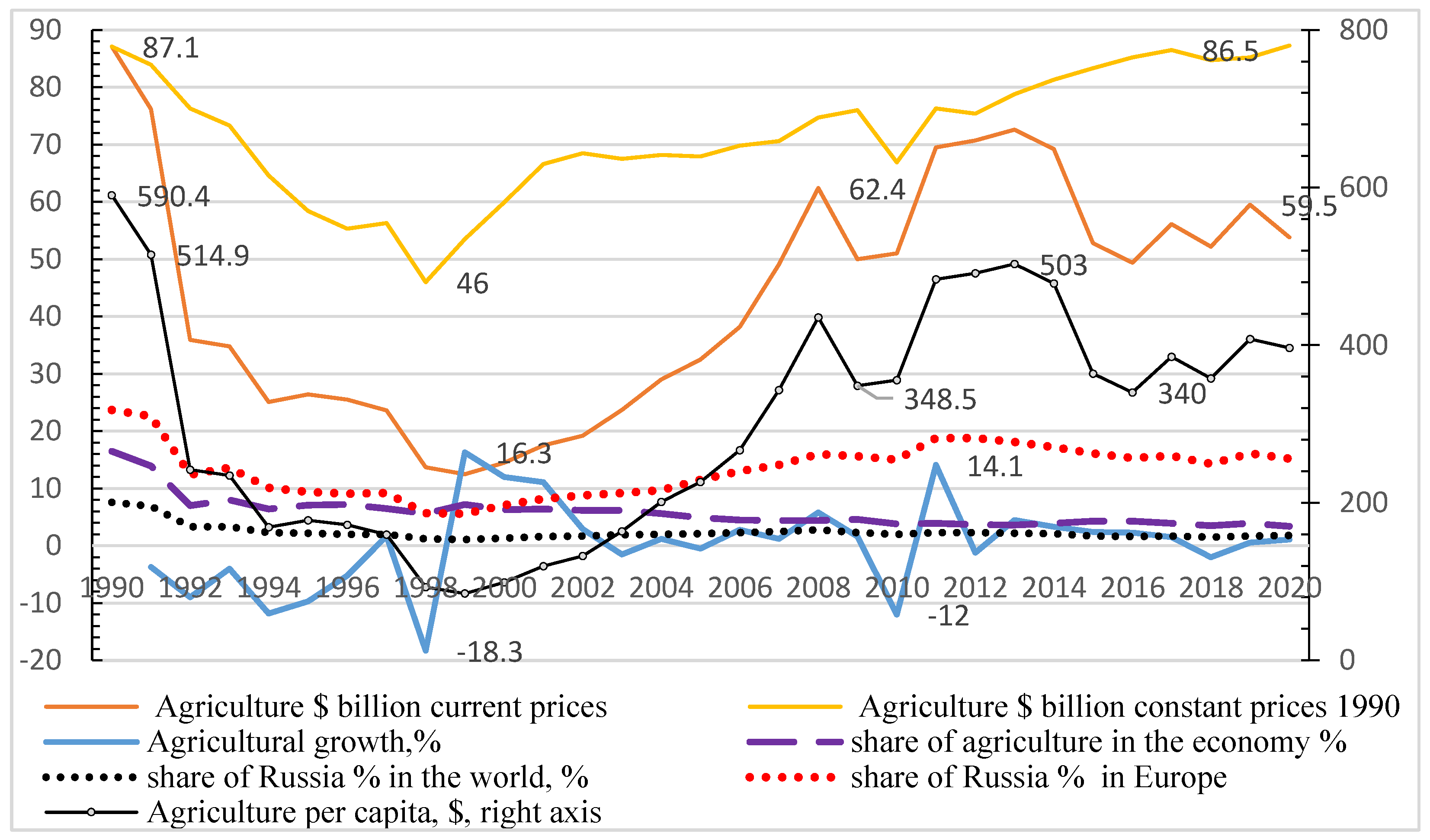

48]. In a number of countries, the total area of agricultural land is growing. For example, the increase in arable land for the period 2000–2019 in Brazil was 23%, in Argentina 18%, in Australia 30%. However, the main global trend is the reduction of this area. After 1990, the total area of agricultural land in Russia has significantly decreased. This was particularly significant in 2006, when the land area decreased to 75,277 thousand hectares. Later, there was a slow recovery, but today this area still does not exceed the level of 2002. The main part of the land is traditionally occupied by grain crops, technical and fodder crops. Since 1990, we have seen an explosive growth in the share of land for industrial crops, primarily due to fodder crops. This trend is quite consistent with the global one and indicates the intensification of agriculture, the transition to new technologies in the production of feed and other products. Nevertheless, even in the most prosperous years, the agriculture of the Russian Federation lags significantly in productivity not only from developed countries, but also from a number of developing ones. The agricultural sector of the Russian economy practically «fell» during the post-Soviet transformations of 1992–2000. However, it would be a misapprehension to explain everything by post-Soviet transformations, since even a cursory glance at the dynamics shows a series of strong crises: two V-crises of 1998–1999 and 2009–2011 and two long L-crises in the period 1999–2009 and from 2011 to the present day (

Figure 4).

In 1998, due to the default, Russia’s agriculture experienced a catastrophic drop (by 18.3%), but the following year it almost recovered (+16.3%); hence, the crisis had a V-form. The positive dynamics gradually turned into stagnation in 2000–2013, which ended for the reasons discussed above. In 2010–2011, agriculture again experienced the V-crisis, which later turned into the long wave of the L-crisis. Russia is one of the largest suppliers of oil and gas in the world, but the land remains the main national wealth. Nevertheless, due to very unfavorable external and internal factors, the share of agriculture in the economy has steadily declined throughout the period of transformation. In 1990, the share of agriculture in the economy was 16.5%; it was only 3.4% in 2020. When considered at current prices, the volume of agriculture was

$87.1 billion in 1990 and

$53.8 billion in 2020. In 1990 prices, the volume of agriculture in Russia was

$87.3 billion in 2020, which amounted to

$396.4 per capita, 1.8% of the global volume of the industry and 15.2% of the European [

38].

It should be noted that by 2021 the volume of agricultural production in Russia (in 1990 prices) has returned to the level of 1990. This is shown by the top line of the diagram (

Figure 4). Agriculture was among those industries that eventually benefited from the so-called war of “sanctions—counter-sanctions”. The Russian authorities announced a food embargo in response to sanctions imposed against Russia by a number of countries, which were aimed to affect both high-tech exports and direct deliveries of some “dual-use” goods. The Decree of the President of the Russian Federation on special economic measures to ensure the security of the country banned the import of a number of products from the EU and the USA (in particular milk, cheese, vegetables, fruits, fish and meat) [

37]. This regulatory act has been prolonged several times, and the latest updates preserve restrictions until the end of 2022. The food embargo (countersanctions) was introduced in three stages: from 2014—in relation to the EU countries, the USA, Australia, Canada and Norway; from 2015—in relation to Iceland, Liechtenstein, Albania and Montenegro; from 2016—in relation to Ukraine. The food embargo had a number of consequences for Russia.

The following are examples of quotes from expert interviews.

Then, when all these sanctions began… the owners made another decision that they needed an airbag and decided to intensify building… The first important point was when we brought high-quality livestock of Danish breeding. (Director of an enterprise that belongs to agroholding).

The Russian embargo on food imports [

49] as a response to economic sanctions has become one of the factors of increasing production in the sector and positively affected the food industry. In this sense, agriculture has effectively responded to the deterioration in the Russian economy. From 2010–2012, production in the industry increased by 12%, and the number of employees in the industry decreased by 20%. If the level of profitability of the country’s economy as a whole decreased from 18.9% to 9.4% from 2000 to 2020, then in agriculture this indicator increased from 6.3% to 20.3% [

50]. This positive dynamic was ensured by the record harvest of 2016. The growth of agriculture in 2015–2016 led to a short-term growth of the labor force; however, this trend stopped due to unfavorable weather in 2017. After 2016, technological modernization of the industry accelerated. Governmental support programs, tax incentives and subsidized loans supported the growth of high-performance jobs, which consequently led to the displacement of some low-skilled workers and an increase in labor productivity, the index of which exceeded 100% from 2016 to 2019. In 2020, the impulse of labor productivity growth was exhausted, and the share of industry products in the economy decreased for the first time since 2014. According to the World Bank, “counter-sanctions” were among the factors contributing to the growth of agricultural production in Russia and the expansion of access to the domestic market for Russian enterprises [

51].

Here are quotes from expert interviews:

We did not make any updates of equipment and livestock until 2005. And if this continued, we would have become impoverished. But nothing much has changed since 2005: we took loans, we take them now, we were in debt, we are in debt now. And speaking about efficiency, our path shows that technical updating does not solve the most important problem. Yes, we just reached the level where 20 tractors are used instead of 50, 20 tractor drivers are needed instead of 50. (Owner of a small business.).

The decline in the number of agricultural and industrial workers is a global trend, and Russia is also moving in this direction at a slow pace. These changes led to the separation of agricultural production from rural life.

Below are quotes from expert interviews:

What is the agricultural sector in Russia? Previously, there were up to 100 heads of cattle in each village, everyone had cattle, people fed themselves… It made substantial assistance to state and corporate agriculture. Now people stand in line at the village store for milk. (Owner of a small business);

Some people, about 30 percent, work on a shift basis, they leave and come each month. (Representative of local authorities.);

… I have to commute every day to work in the city. (Leader of a public organization.).

According to experts, food embargo and import substitution affected about 10% of the total consumption of population. At the same time, the embargo and import substitution have many negative consequences, such as the significant increase in food prices and the expansion of replacing natural products with surrogates (powdered milk, palm oil). Some European importers managed to initiate supply by a roundabout route through Serbia and Belarus, which made products more expensive, while domestic businesses increased prices due to a reduction in supply. Moreover, many entrepreneurs were forced to take loans at high interest rates. Thus, the food embargo was beneficial for selected companies.

However, the main obstacle to the evolution of Russian agriculture and rural territories is the insufficient level of small and medium-sized agribusinesses development. At the initial stage of the reforms, the creation of a class of landowners was characterized by an increasing role of small business structures (microenterprises, personal subsidiary farms, peasant farms, etc.) in the total volume of agricultural production. At the beginning of the reform path, small businesses and household plots provided little more than a quarter of food production, but by 2006 their share had doubled, reaching 55%. The change in the structure of agricultural production by categories of producers in the Russian Federation for the period 1990–2020 is shown in

Figure 1 [

38]. At the next stage, the reform path has changed. Over the past two decades, there has been a significant reduction in the share of household plots (52% in 2000, 27% in 2020). Part of them is being transformed into peasant farms, the share of which increased fivefold over the specified period. But the overall contribution of small business in Russian agriculture has decreased by 23% against the background of an increase in the contribution of large business.

Here are quotes from expert interviews:

By supporting only megafarms, our government missed the development of medium and small companies. But small production forms are less vulnerable, more resistant to cata-clysms. They need support, too. (Owner of a small business);

Small-scale farming cannot afford new technologies. Therefore, it seems to me that their number will still slowly decrease. (Representative of regional authorities);

Today, without state support, small forms of economic activity simply cannot survive, there is no attraction in doing this. (Representative of regional authorities).

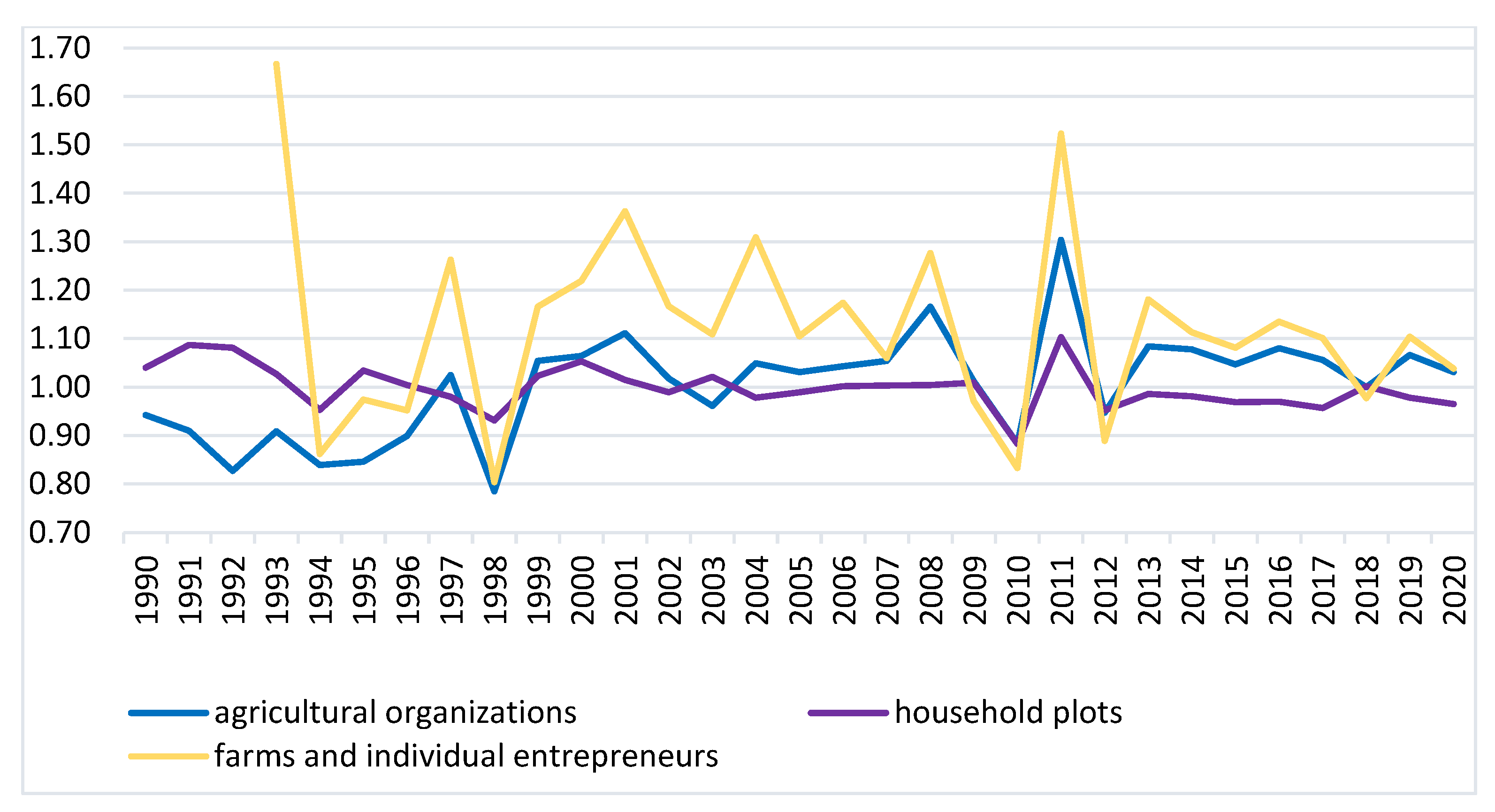

Today, there is a realization of the need to create attractive conditions for peasant farms, as well as to expand and diversify the types of farms [

50]. Even though the share of small and medium-sized businesses is rather insignificant in terms of the gross product, they demonstrate sufficiently high performance. Peasant farms and individual entrepreneurs demonstrate higher growth rates than large-scale agricultural organizations, even in difficult years for the industry (

Figure 5).

Thus, external and internal factors have expanded opportunities for domestic producers. Due to government support tools, a foundation has been created for the development of hundreds of investment projects in many regions of the federation. Investors are interested in greenhouse vegetable growing, orchards and vineyards establishment, animal husbandry. The national agroindustry has significantly strengthened. In several product categories, Russia has indeed achieved import substitution.

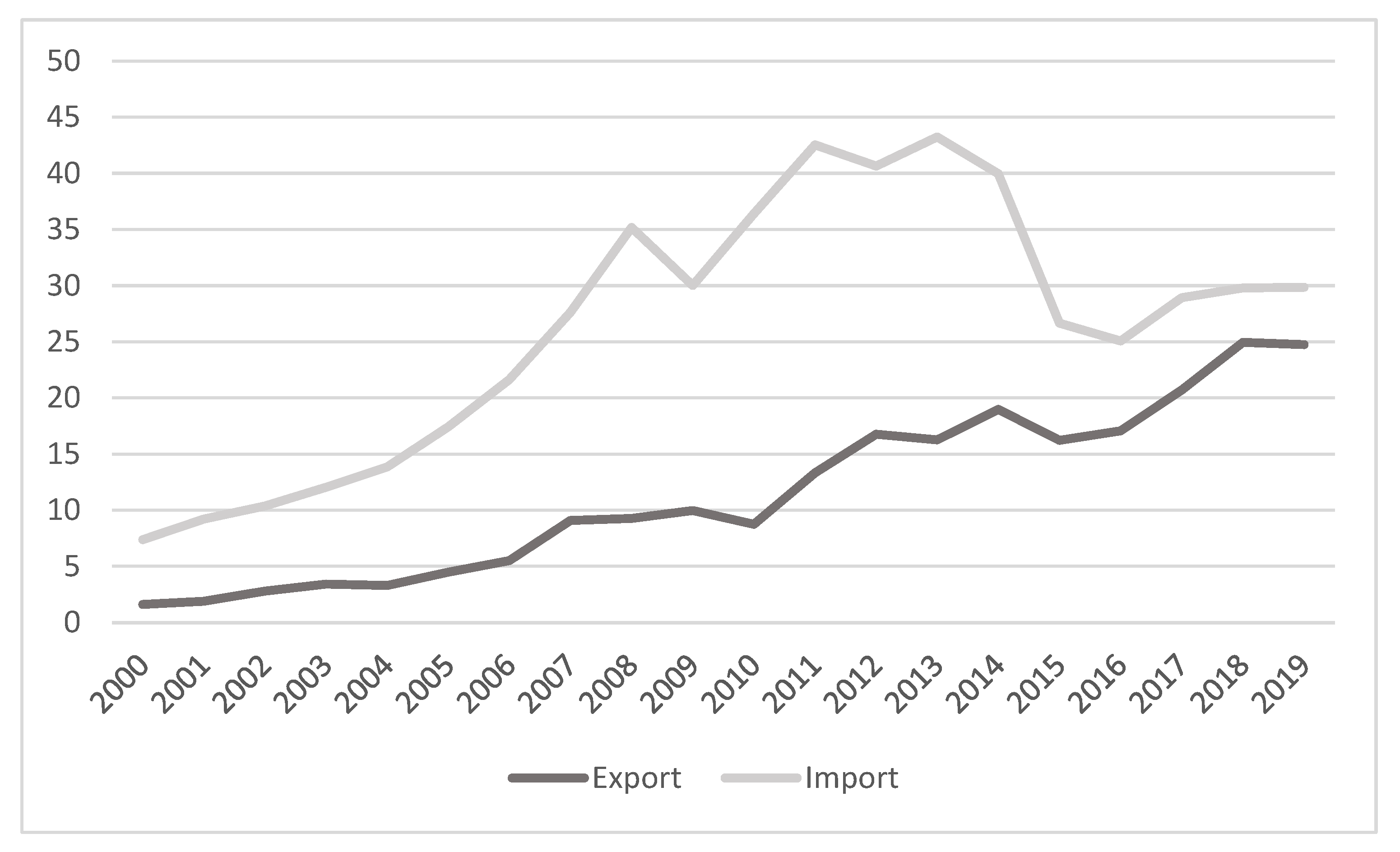

Figure 6 shows the Russian dynamics of exports and imports of food and agricultural feedstock (except textile) for the period of 2000–2019 [

41].

By 2018, domestic agricultural producers almost fully provided the country with grain (by 99%), meat and meat products (by 93%), sugar (by 95%) and milk (by 84%) [

51]. Having secured its own production of goods that were traditionally imported, Russia became one of the world’s largest wheat suppliers.

5. Discussion

A review of the dynamics of agriculture in Russia over the past 20 years has shown that the accelerated introduction of market relations has indeed solved the problem of food supply. Despite the fact that Russia is a northern country, shelves in grocery stores remain filled. The situation of the 1990s, when there was a deficit in range and quality of food products, did not repeat, even in the pandemic years of 2020–2021. Government support policies have led to the transition from the small-scale production in agriculture to the large-scale production, to the so-called agroholdings. There was a significant increase in the profitability of agriculture, which exceeds the average Russian values. This is also one of the results of increasing industrial production in rural areas.

At the same time, it should be noted that the share of small-scale farms in the total volume of agricultural production remains very significant at the expense of household plots. Analysts and experts note that these farms are very poorly technological, but they continue to carry a huge social function in the countryside. This tradition has remained since Soviet times, when villagers did not seek to make excessive efforts when working on state land, preferring to strain themselves on their tiny household plots.

The policy of sanctions–counter-sanctions has led to certain difficulties in the structure of food supplies. Consumers felt a shortage of certain high-quality foods mainly in the form of a sharp decline in choice. However, agricultural producers evaluate this policy rather positively. Closed markets proved to be more resilient during the pandemic restrictions. Therefore, consumers in Russia felt a shortage of only high-quality products (cheeses, meat). However, the leading agricultural holdings managed to replace these products. As a result, in 2020, Russia ranked 9th in the world in terms of gross agricultural production and 1st in Europe: Russia—

$54.9 billion; France—

$42 billion; Spain—

$40.3 billion; Italy—

$27.5 billion; Germany—

$28.3 billion. The share of Russian agriculture is 15% of the European and 1.5% of the world [

47].

The characteristic features of Russian agroholdings are that they operate in several regions of the country, in product segments dominant for a particular region and have several auxiliary production facilities. The advantages of Russian agroholdings are that they provide a key role in ensuring Russia’s food security. The high concentration of capital, technology, labor and innovation allows for the use of economies of scale, reduces costs and increases competitiveness. Technological breakthrough opportunities are provided due to the update of the material and technical part of fixed assets, the introduction of advanced tillage technologies, the use of mineral fertilizers, and the implementation of digital management. New jobs opportunities are being created, which supports the economic growth of the home regions. There are large volumes of attractive investments in agriculture in the regions of the country. The quality control of products and the application of international ISO standards is provided. The possibility of combining narrow specialization and diversification of production has been achieved. There are resources for a full cycle of reproduction, starting from agricultural raw materials, processing, production and marketing. Agricultural markets, including export supplies, have been expanded. There are opportunities for close cooperation with regional and municipal authorities to safeguard mutual interests.

The disadvantages of agroholdings are a continuation of their advantages and consist in monopolization of agricultural markets, which leads to the squeezing out of small and medium-sized enterprises. The increase in lobbying potential is to the detriment of small players, primarily peasant farms. The lack of competition between structural divisions within one agroholding hinders the growth of profitability and economic efficiency. Excessive bureaucratization is enlarging, which increases the complexity of multilevel systems of hierarchical management structure. The internal political system does not have adequate mechanisms for the regulation of agroholdings operation. There is a shortage of qualified workers, especially in high-tech sectors of agriculture. There are no real incentives for the active participation of representatives of agricultural holdings in the construction of social infrastructure facilities in the host territories. Agricultural lands are depleted, their ecological condition is deteriorating due to the high intensification.

The positive trends described above have affected the dynamics of foreign trade in agricultural products. Throughout modern history, imports of food products and agricultural raw materials exceeded exports. A particularly noticeable gap was observed in the period 2007–2013. Currently, the gap between imports and exports of food products and agricultural raw materials has been reduced. In modern Russian history, 2020 is a record year, as Russian producers exported 79 million tons of agricultural products and food worth

$30.7 billion; imports of the respective products overtook exports by

$1 billion [

52].

State support for agricultural business creates certain incentives for the development of small and medium-sized business structures, but their absolute volume of production remains incomparable with the examples of European countries. The negative effects of such distortions in institutional forms of regulation and support should include poor technological efficiency and low level of marketability of small and medium-sized business structures in rural areas. This distortion is characterized by the fact that most villagers have an image of the countryside as abandoned and poor, since they can receive income necessary and sufficient for life only as a result of extremely hard and non-technological work, or temporary jobs at large enterprises.

Based on the analysis of expert interviews, the main social institutions that played an important role in post-Soviet transformations in rural areas are identified. In the first, the incomplete legitimacy of these changes has led to growth of distrust in the market and the government. There is evidence that rural residents could not or did not want to take advantage of the range of opportunities for state support. A whole class of “fake” entrepreneurs appeared; the informants called them “dependents”, drawing attention to the excessive state support of their economic activity. In the second, the significant involvement of the state has led to the consolidation of the land fund and the concentration of capital. In the third, the sanctions policies have affected the economic relations in rural areas. Agricultural enterprises saw new opportunities in the policy of “sanctions-anti-sanctions” due to weakness and lack of competitiveness at the first stages of changes. As a result, the choice of market actors led to the creation of a flexible mixed economic structure, which was relatively effective for the internal market, but not for the external market. In the fourth, the transformation of the production and ownership structure has led to a change in the forms of employment and living conditions (e.g., work on a rotational basis, which is new for rural Russia). Since the interests of the residents of rural areas mainly belong to urban life, they wean themselves from the peasant farms. Due to this, vast territories in modern Russia are maintained by temporarily attracted labor force, while local residents either cannot or do not want to work there.

6. Conclusions

According to the new institutional economics, individuals opt for institutions in the process of economic and social interactions. Therefore, institutions do not determine individual preferences and behavioral patterns, but are the result of choice. This is the key feature of the influence of institutions on the post-Soviet transformations of Russian rural territories. The main institution and the start of transformations was agrarian reform, which was virtually indisputably necessary. However, the actions of the reformers were contradictory, many of the important institutions to support the reform appeared with a delay and some were never fully established.

Despite the contradictions and inconsistency, the agrarian reform in Russia has achieved its main goals. A substantial class of landowners was created, the threat of famine and shortage of food was overcome, a body of institutions for the support and development of agricultural production and rural areas was formed.

During the period of agrarian reforms in Russia, important incentives for the advancement of rural entrepreneurship have been provided. The privatization of land and the institutionalization of small-scale forms of business have ensured the diversity of the rural economy. Business consolidation has accelerated the transition to new technologies in crop production and animal husbandry. However, these innovations apply mainly to large agricultural organizations. The formation of agroholdings, a new phenomenon for the market, has shown a trend towards the consolidation of agricultural production. The Russian phenomenon of agroholding accelerated institutional changes after 2010. It is quite true that agricultural holdings have played the predominant role when “feeding the country” with grain, sugar and meat. However, in the production volume of other food products, their share is about the same as the share of other agricultural producers. Furthermore, strong distortions in the structure have given ambiguous socio-economic consequences. On the one hand, within the framework of state support, huge financial resources were directed to agricultural holdings, which led to a growth in the income of owners and the concentration of capital in a very narrow circle of owners. Accumulated wealth is poorly distributed among employees, and productivity does not affect salaries. On the other hand, the state-supported consolidation and vertical integration made possible technological renewal and modernization in a very short time and increased efficiency and product quality in agriculture. As a result, modern Russia is radically different from the Russia of the 1990s, primarily in terms of the quality and quantity of food produced and consumed.

As a result, modern Russia is radically different from the Russia of the 1990s, primarily in terms of the quality and quantity of food produced and consumed. By the beginning of 2021, the volume of agricultural production reached the level of the pre-reform period. Through organizational, economic, financial and legal transformations, the domestic market was saturated with food and agricultural feedstock.

The role of state support for agriculture is important, both in Russia and in other countries. Additionally, it is objectively necessary, since competent budget planning provides ample opportunities for the development of rural areas. However, the dominance of direct forms of cost-based support does not stimulate cost-effective and innovative activities, although it is precisely these conditions that could bring various branches of agricultural production to a competitive level in the future. Governmental incentives do not ensure the development of small and medium-sized businesses at a level sufficient to make their contribution to production significant and visible to consumers. There is very little and irregular support for local communities, farming and other types of agricultural entrepreneurship in the countryside. The volatility of the regulatory framework and legislation endangers strategic projects. Mainly less costly and short-term forms of economic activities are becoming appealing.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}