The Effect of Financial Market Factors on House Prices: An Expected Utility Three-Asset Approach

Abstract

:1. Introduction

2. Theory

2.1. The Expected Utility Three-Asset Housing Life-Cycle Model

2.2. Special Solutions under the Specific Utility Functions

2.3. Portfolios between Housing and Risky Financial Assets

3. Empirical Section

3.1. Data and Testing

3.2. Regression Analysis

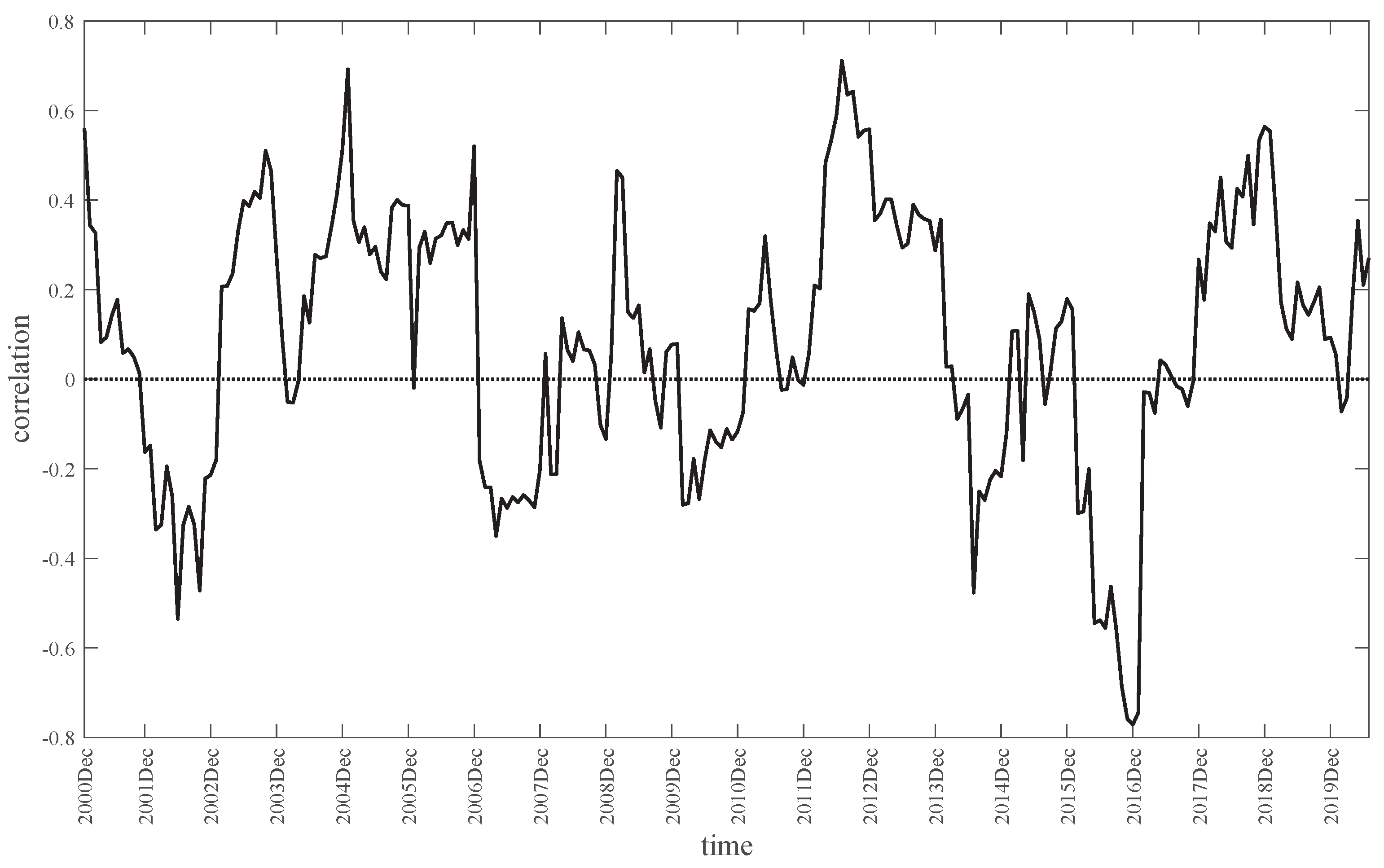

3.3. Historical Correlation between Housing and Financial Market Returns

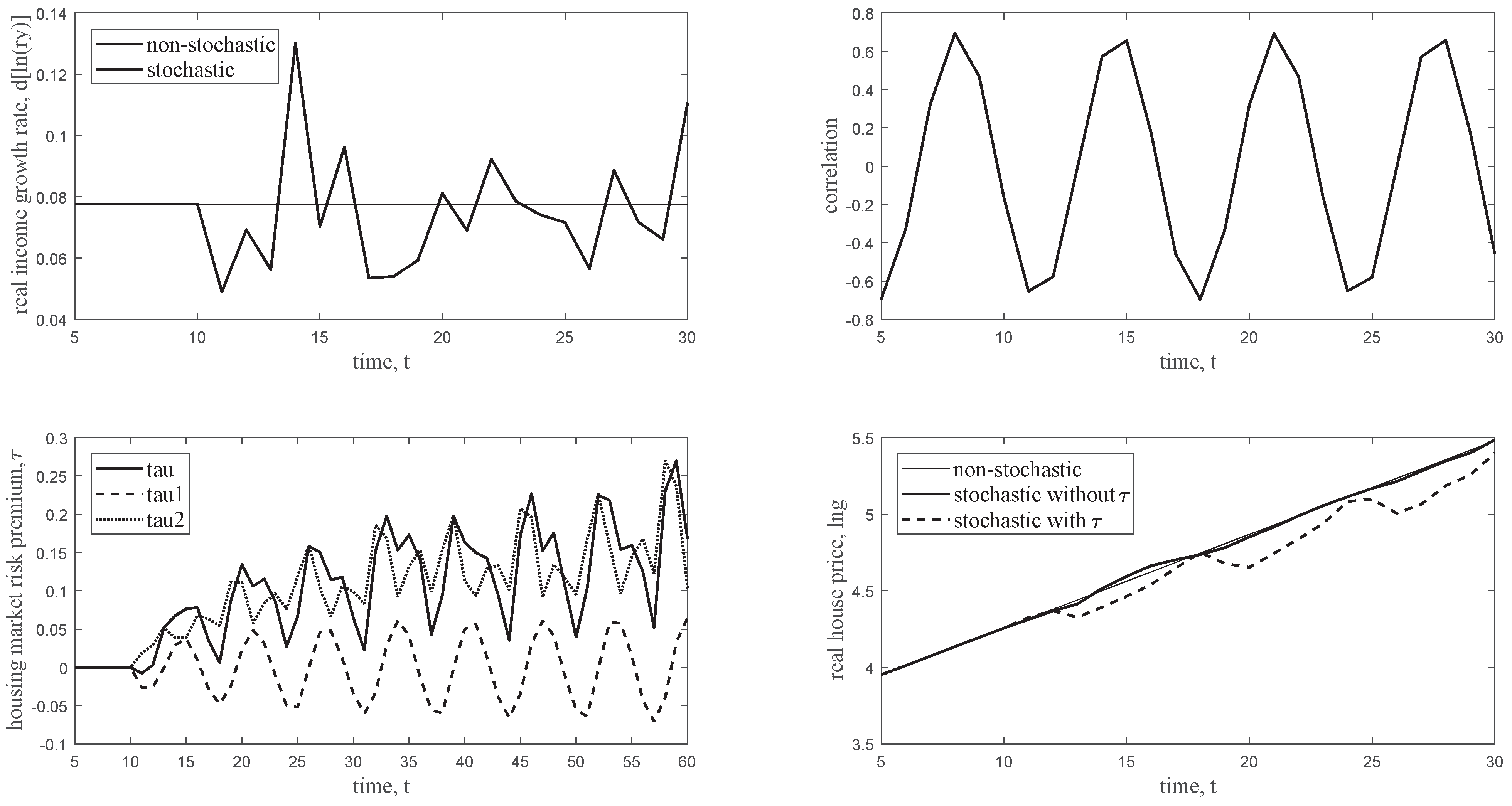

4. Simulation Analysis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Mathematical Derivations

Appendix A.1. The Expected Utility Three-Asset Housing Life-Cycle Model, Part I

Appendix A.2. The Expected Utility Three-Asset Housing Life-Cycle Model, Part II

Appendix A.3. The Three-Asset Expected Utility Housing Life-Cycle Model under CARA Utility

Appendix A.4. The Three-Asset Expected Utility Housing Life-Cycle Model under CRRA Utility

Appendix A.5. Derivation of the Optimal Ratio of Risk Financial Assets to Housing Assets from Our Three-Asset Model

Appendix A.6. Derivation of the Optimal Ratio of Risky Financial Assets to Housing Assets from the Mean-Variance Model

Appendix B. Values Used in the Simulations

{kind=link}

{kind=link}

| Parameter | Interpretation | Value | Rationale |

|---|---|---|---|

| g_initial | Initial real house price | 40.74 | national level in 2010 |

| ry_initial | Initial real income | 152.03 | national level in 2010 |

| HEtoC | 0.203 | national level in 2010 | |

| rry_cons | Growth rate of real income | 0.0776 | Sample average |

| std_rry_cons | Standard deviation of rry | 0.0807 | Sample average |

| interest_cons | Nominal interest rate | 0.053 | Sample average (Table 1) |

| inf_cons | Inflation rate | 0.0248 | Sample average |

| dep_cons | Housing depreciation rate | 0.01 | See text |

| theta_cons | CRRA parameter | 5 | See text |

| ra_cons | SSEC growth rate | 0.0577 | sample average |

| std_ra_cons | Standard deviation of ra | 0.0655 | sample average |

References

- Wang, Y.; Liu, J.; Tang, Y.; Sriboonchitta, S. Housing Risk and Its Influence on House Price: An Expected Utility Approach. Math. Probl. Eng. 2020, 2020, 16. [Google Scholar] [CrossRef]

- Muellbauer, J.; Murphy, A. Booms and Busts in the UK Housing Market. Econ. J. 1997, 107, 1701–1727. [Google Scholar] [CrossRef]

- Green, R. Stock prices and house prices in California: New evidence of a wealth effect? Reg. Sci. Urban Econ. 2002, 32, 775–783. [Google Scholar] [CrossRef]

- Lee, M.; Lee, C.; Lee, M.; Liao, C. Price linkages between Australian housing and stock markets. Int. J. Hous. Mark. Anal. 2017, 10, 305–323. [Google Scholar] [CrossRef]

- Kakes, J.; Van Den End, J. Do stock prices affect house prices? Evidence for the Netherlands. Appl. Econ. Lett. 2004, 11, 741–744. [Google Scholar] [CrossRef]

- Takala, K.; Pere, P. Testing the cointegration of house and stock prices in Finland. Finn. Econ. Pap. 1991, 4, 33–51. [Google Scholar]

- Ibrahim, M. House price-stock price relations in Thailand: An empirical analysis. Int. J. Hous. Mark. Anal. 2010, 3, 69–82. [Google Scholar] [CrossRef]

- Meen, G. Modelling Spatial Housing Markets: Theory, Analysis, and Policy, 2nd ed.; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2001; pp. 42–76. [Google Scholar]

- Dougherty, A.; Van Order, R. Inflation, Housing Costs, and the Consumer Price Index. Am. Econ. Rev. 1982, 72, 154–164. [Google Scholar] [CrossRef]

- Case, K.; Cotter, J.; Gabriel, S. Housing Risk and Return: Evidence from a Housing Asset-Pricing Model. J. Portf. Manag. 2011, 37, 89–109. [Google Scholar] [CrossRef] [Green Version]

- Hu, J.; Sui, Y.; Ma, F. The Measurement Method of Investor Sentiment and Its Relationship with Stock Market. Comput. Intell. Neurosci. 2021, 2021, 1–11. [Google Scholar] [CrossRef]

- Wang, J.; Wang, J.; Fang, W.; Niu, H. Financial time series prediction using elman recurrent random neural networks. Comput. Intell. Neurosci. 2016, 105, 214–224. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Lucas, R., Jr. Asset Pricing in an Exchange Economy. Econometrica 1978, 46, 1429–1445. [Google Scholar] [CrossRef]

- Grossman, S.; Laroque, G. Asset Pricing and Optimal Portfolio Choice in the Presence of Illiquid Durable Consumption Goods. Econometrica 1990, 58, 25–51. [Google Scholar] [CrossRef]

- Flavin, M.; Nakagawa, S. A Model of Housing in the Presence of Adjustment Costs: A Structural Interpretation of Habit Persistence. Am. Econ. Rev. 2008, 98, 474–495. [Google Scholar] [CrossRef] [Green Version]

- Piazzesi, M.; Schneider, M.; Tuzel, S. Housing, Consumption and Asset Pricing. J. Financ. Econ. 2007, 83, 531–569. [Google Scholar] [CrossRef] [Green Version]

- Chen, N. Asset price fluctuations in Taiwan: Evidence from stock and real estate prices 1973 to 1992. J. Asian Econ. 2001, 12, 215–232. [Google Scholar] [CrossRef]

- Aliev, R.; Mraiziq, D.; Huseynov, O. Expected Utility Based Decision Making under Z-Information and Its Application. Comput. Intell. Neurosci. 2015, 2015. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Y.; Wang, Y. Price dynamics of China’s housing market and government intervention. Appl. Econ. 2021, 53, 1212–1224. [Google Scholar] [CrossRef]

- Zhi, T.; Li, Z.; Jiang, Z.; Wei, L.; Sornette, D. Is there a housing bubble in China? Emerg. Mark. Rev. 2019, 39, 120–132. [Google Scholar] [CrossRef] [Green Version]

- Poterba, J. Tax Subsidies to Owner-occupied Housing: An Asset-market Approach. Q. J. Econ. 1984, 99, 729–752. [Google Scholar] [CrossRef] [Green Version]

- Poterba, J. House Price Dynamics: The Role of Tax Policy and Demography. Brookings Pap. Econ. Act. 1991, 1991, 143–203. [Google Scholar] [CrossRef]

- Andrew, M.; Meen, G. House price appreciation, transactions and structural change in the British housing market: A macroeconomic perspective. Real Estate Econ. 2003, 31, 99–116. [Google Scholar] [CrossRef]

- Yamashita, T. House price appreciation, liquidity constraints, and second mortgages. J. Urban Econ. 2007, 62, 424–440. [Google Scholar] [CrossRef]

- Meen, G. The removal of mortgage market constraints and the implications for econometric modelling of UK house prices. Oxf. Bull. Econ. Stat. 1990, 52, 1–23. [Google Scholar] [CrossRef]

- Dynan, K. How Prudent Are Consumers? J. Political Econ. 1993, 101, 1104–1113. [Google Scholar] [CrossRef]

- Sharpe, W. Mutual Fund Performance. J. Bus. 1966, 39, 119–138. [Google Scholar] [CrossRef]

- Markowitz, H. Portfolio Selection. J. Financ. 1952, 7, 77–91. [Google Scholar] [CrossRef]

- Babcock, B.; Choi, E.; Feinerman, E. Risk and probability premiums for CARA utility functions. J. Agric. Resour. Econ. 1993, 18, 17–24. [Google Scholar]

| Name | Variable | Label/Measurement | Mean | S.D. |

|---|---|---|---|---|

| Monthly: | ||||

| monthly | 100 million yuan | |||

| monthly | 10 thousand m | |||

| monthly | ||||

| SSEC | – | |||

| monthly growth | ||||

| monthly growth | ||||

| Annual: | ||||

| housing expenditure | 100 million yuan | 1592.1 | 2194.1 | |

| housing space sold | 10 thousand m | 2862.4 | 2765.5 | |

| house price (yuan/m) | 4566.0 | 3730.9 | ||

| Y | disposable income | yuan/person | 18,218.8 | 10,332.2 |

| consumer price index | 2000 = 100 | 123.1 | 17.72 | |

| final consumption | 100 million yuan | 6136.5 | 6342.3 | |

| G | real house price | 35.953 | 27.701 | |

| logarithm form | ||||

| real income | 142.028 | 68.680 | ||

| logarithm form | ||||

| i | (loan) interest rate | – | 0.053 | 0.0056 |

| nominal return | 0.095 | 0.093 | ||

| Equation (20) | −0.0036 | 0.084 | ||

| Equation (21) | 0.035 | 0.100 | ||

| expected housing yield | ||||

| expected financial yield | ||||

| S.D. of | ||||

| S.D. of | ||||

| correlation | ||||

| Test | ||

|---|---|---|

| Levin-Lin-Chu (LLC) test | <0.001 | <0.001 |

| Im-Pesaran-Shin (IPS) test | <0.001 | <0.001 |

| ADF-Fisher unit-root test (lag = 2) | <0.001 | <0.001 |

| Hadri LM stationary test | 0.680 | 0.726 |

| Coefficient | Equation (26), DFE | Equation (27), MG | Equation (28), PMG |

|---|---|---|---|

| (or ) | 0.772 *** (4.4) | 0.785 *** (3.3) | 1.007 *** (5.3) |

| (or ) | −0.383 *** (10.8) | −0.644 *** (10.0) | −0.499 *** (9.7) |

| (or ) | 0.830 *** (25.7) | 0.906 *** (7.4) | 0.853 *** (55.5) |

| (or ) | −7.401 *** (3.9) | −4.173 (0.6) | −5.806 *** (6.8) |

| (or ) | 0.381 *** (3.3) | 0.607 *** (4.0) | 0.168 ** (2.4) |

| (or ) | −0.367 ** (2.1) | −0.987 * (1.7) | −0.319 *** (3.3) |

| (or ) | −0.303 ** (2.1) | −0.982 (0.5) | 0.077 (0.9) |

| constant | −0.079 (0.9) | −0.283 * (1.7) | −0.224 *** (5.0) |

| Coefficient | Equation (31), UCC by (29) | Equation (31), UCC by (30) |

|---|---|---|

| 0.798 *** (4.5) | 0.815 *** (4.7) | |

| −0.396 *** (11.0) | −0.380 *** (10.7) | |

| 0.812 *** (24.1) | 0.807 *** (23.2) | |

| −0.345 *** (3.6) | −0.410 *** (4.5) | |

| constant | −0.583 *** (4.3) | −0.619 *** (5.2) |

| (within) | 0.296 | 0.315 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, Y.; Liu, J.; Qiu, Z.; Sriboonchitta, S. The Effect of Financial Market Factors on House Prices: An Expected Utility Three-Asset Approach. Axioms 2022, 11, 145. https://doi.org/10.3390/axioms11040145

Wang Y, Liu J, Qiu Z, Sriboonchitta S. The Effect of Financial Market Factors on House Prices: An Expected Utility Three-Asset Approach. Axioms. 2022; 11(4):145. https://doi.org/10.3390/axioms11040145

Chicago/Turabian StyleWang, Yehui, Jianxu Liu, Zhaolin Qiu, and Songsak Sriboonchitta. 2022. "The Effect of Financial Market Factors on House Prices: An Expected Utility Three-Asset Approach" Axioms 11, no. 4: 145. https://doi.org/10.3390/axioms11040145

APA StyleWang, Y., Liu, J., Qiu, Z., & Sriboonchitta, S. (2022). The Effect of Financial Market Factors on House Prices: An Expected Utility Three-Asset Approach. Axioms, 11(4), 145. https://doi.org/10.3390/axioms11040145