Impact of MiFID II on the Market Volatility—Analysis on Some Developed and Emerging European Stock Markets

Abstract

:1. Introduction

2. Theoretical Background

3. Methodological Approach

3.1. Data and Methodology

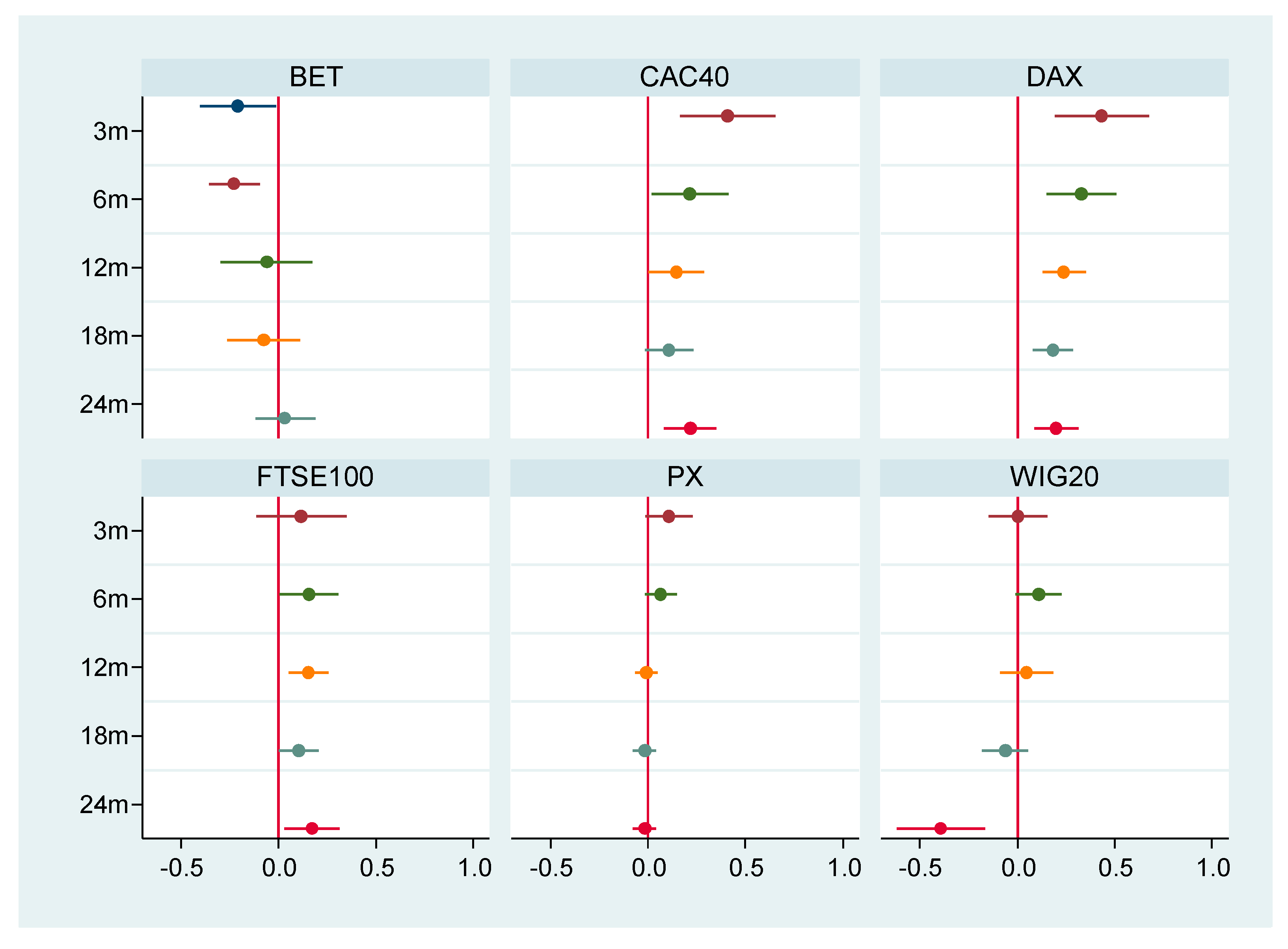

3.2. Results and Interpretation

4. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| BET | CAC40 | DAX | FTSE100 | PX | WIG20 | |

|---|---|---|---|---|---|---|

| −4.4428 *** | −4.443 *** | −4.0937 *** | −4.109 *** | −3.5605 ** | −1.3538 | |

| (0.0019) | (0.0019) | (0.0064) | (0.0061) | (0.0333) | (0.874) | |

| −2.8729 | −2.4511 | −1.8789 | −2.4979 | −2.2412 | −0.9305 | |

| (0.1715) | (0.3528) | (0.6655) | (0.329) | (0.4667) | (0.9528) | |

| −6.8858 *** | −8.2455 *** | −8.0313 *** | −7.4196 *** | −10.8376 *** | −6.8573 *** | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |

| −9.6168 *** | −8.335 *** | −8.6793 *** | −9.8804 *** | −6.374 *** | −7.4217 *** | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) |

References

- Ackert, Lucy F., Bryan K. Church, and Narayanan Jayaraman. 2005. Circuit breakers with uncertainty about the presence of informed agents: I know what you know…I think. Financial Markets, Institutions & Instruments 14: 135–68. [Google Scholar]

- Aghanya, Daniel, Vineet Agarwal, and Sunil Poshakwale. 2020. Market in financial instruments directive (MiFID), stock price informativeness and liquidity. Journal of Banking and Finance 113: 105730. [Google Scholar] [CrossRef]

- Andersen, Torben G. 1996. Return volatility and trading volume: An information flow of stochastic volatility. The Journal of Finance 51: 169–204. [Google Scholar] [CrossRef]

- Anselmi, Giulio, and Giovanni Petrella. 2020. Regulation and Stock Market Quality: The Impact of MiFID II on Liquidity and Efficiency on European Stocks. Working Paper. Available online: https://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2020-Dublin/papers/EFMA%202020_stage-1301_question-Full%20Paper_id-428.pdf (accessed on 25 June 2021).

- Anselmi, Giulio, and Giovanni Petrella. 2021. Regulation and stock market quality: The impact of MiFID II provision on research unbundling. International Review of Financial Analysis 76: 101788. [Google Scholar] [CrossRef]

- Anshuman, Ravi V. 2003. Regulatory measures to curb stock price volatility. Money, Banking and Finance 38: 677–79. [Google Scholar]

- Bloomfield, Robert, and Maureen O’Hara. 1999. Market transparency: Who wins and who loses? The Review of Financial Studies 12: 5–35. [Google Scholar] [CrossRef]

- Boehmer, Ekkehart, Gideon Sarr, and Lei Yu. 2005. Lifting the veil: An analysis of pre-trade transparency at the NYSE. The Journal of Finance 60: 783–815. [Google Scholar] [CrossRef] [Green Version]

- Bollerslev, Tim, Julia Litvinova, and George Tauchen. 2006. Leverage and volatility feedback effects in high-frequency data. Journal of Financial Econometrics 4: 353–84. [Google Scholar] [CrossRef] [Green Version]

- Brogaard, Jonathan, and Corey Garriott. 2019. High-frequency trading competition. Journal of Financial and Quantitative Analysis 54: 1469–97. [Google Scholar] [CrossRef] [Green Version]

- Buss, Adrian, Bernard Dumas, Raman Uppal, and Grigory Vilkov. 2013. Comparing Different Regulatory Measures to Control Stock Market Volatility: A General Equilibrium Analysis. Available online: https://www.erim.eur.nl/fileadmin/erim_content/documents/Uppal_May7.pdf (accessed on 12 December 2020).

- Chiang, Thomas C., Zhuo Qiao, and Wing-Keung Wong. 2010. New evidence on the relation between return volatility and trading volume. Journal of Forecasting 29: 502–15. [Google Scholar]

- Chlistalla, Michael. 2011. High-Frequency Trading. Better Than Its Reputation? Deutsche Bank Research. Available online: https://secure.fia.org/ptg-downloads/dbonhft2-11.pdf (accessed on 12 December 2020).

- Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam. 2002. Order imbalance, liquidity and market returns. Journal of Financial Economics 65: 3–28. [Google Scholar] [CrossRef] [Green Version]

- Copeland, Thomas E. 1976. A model of asset trading under the assumption of sequential information arrival. Journal of Finance 31: 1149–68. [Google Scholar] [CrossRef]

- Corrado, Charles, and Cameron Truong. 2007. Forecasting stock index volatility: Comparing implied volatility and the intraday high–low price range. Journal of Financial Research 30: 201–15. [Google Scholar] [CrossRef]

- Darrat, Ali F., Shafiqur Rahman, and M. Maosen Zhang. 2003. Intraday trading volume and return volatility of the DJIA stocks: A note. Journal of Banking and Finance 27: 2035–43. [Google Scholar] [CrossRef]

- Dufour, Jean-Marie, René Garcia, and Abderrahim Taamouti. 2012. Measuring High-Frequency Causality Between Returns, Realised Volatility, and Implied Volatility. Journal of Financial Econometrics 10: 124–63. [Google Scholar] [CrossRef]

- Dumitrescu, Ariadna. 2010. Liquidity and Optimal Market Transparency. European Financial Management 16: 599–623. [Google Scholar] [CrossRef]

- ESMA. 2014. High-Frequency Trading Activity in EU Equity Markets. Economic Report, No.1. Available online: https://www.esma.europa.eu/sites/default/files/library/2015/11/esma20141_-_hft_activity_in_eu_equity_markets.pdf (accessed on 12 December 2020).

- ESMA. 2020. Market Impacts of Circuit Breakers—Evidence from EU Trading Venues, Working Paper, No.1. Available online: https://www.esma.europa.eu/sites/default/files/library/esmawp-2020-1_market_impacts_of_circuit_breakers.pdf (accessed on 12 December 2020).

- Fama, Eugene F. 1991. Efficient capital markets: II. The Journal of Finance 46: 1575–617. [Google Scholar] [CrossRef]

- Fang, Bingxu, Ole Kristian Hope, Zhongwei Huang, and Rucsandra Moldovan. 2020. The Effects of MiFID II on Sell- Side Analysts, Buy-Side Analysts, and Firms. Review of Accounting Studies 25: 855–902. [Google Scholar] [CrossRef]

- Hagströmer, Björn, and Lars Norden. 2013. The diversity of high-frequency traders. Journal of Financial Markets 16: 741–70. [Google Scholar] [CrossRef]

- Harris, Lawrence. 1987. Transaction data test of the mixture of distributions hypothesis. Journal of Financial and Quantitative Analysis 22: 127–41. [Google Scholar] [CrossRef]

- Hasbrouck, Joel, and Gideon Saar. 2013. Low latency trading. Journal of Financial Markets 16: 646–79. [Google Scholar] [CrossRef]

- Hassan, Gazi M., and Eliza Wu. 2015. Sovereign credit ratings, growth volatility and the global financial crisis. Applied Economics 47: 1–16. [Google Scholar] [CrossRef] [Green Version]

- Hendershot, Terrence, Charles M. Jones, and Albert J. Menkveld. 2011. Does algorithmic trading improve liquidity? The Journal of Finance LXVI: 1–33. [Google Scholar] [CrossRef] [Green Version]

- Hibbert, Ann M., Robert T. Daigler, and Brice Dupoyet. 2008. A behavioural explanation for the negative asymmetric return-volatility relation. Journal of Banking and Finance 32: 2254–66. [Google Scholar] [CrossRef]

- Jennings, Robert H., Laura T. Starks, and John C. Fellingham. 1981. An equilibrium model of asset trading with sequential information arrival. Journal of Finance 36: 143–61. [Google Scholar] [CrossRef]

- Lamdin, Douglas J. 2001. Implementing and interpreting event studies of regulatory changes. Journal of Economics and Business 53: 171–83. [Google Scholar] [CrossRef]

- Lee, Jen-Sin, Kuan-Ling Lai, and Yu-Ko Huang. 2015. Information transparency and idiosyncratic risk. Applied Economics Letters 22: 934–37. [Google Scholar] [CrossRef]

- Madhavan, Ananth, David Porter, and Daniel Weaver. 2005. Should securities markets be transparent? Journal of Financial Markets 8: 265–87. [Google Scholar] [CrossRef]

- Madhavan, Ananth. 1996. Security prices and market transparency. Journal of Financial Intermediation 5: 255–83. [Google Scholar] [CrossRef]

- Meijers, Julian. 2018. The Effect of the MiFID I and MiFID II/MiFIR Transparency Requirements on the Volatility: Evidence from European Equity Markets. Available online: https://scripties.uba.uva.nl (accessed on 12 December 2020).

- Oxera. 2019. The Design of Equity Trading Markets in Europe. An Economic Analysis of Price Formation and Market Data Services, Prepared for Federation of European Securities Exchanges. Available online: https://www.oxera.com/wp-content/uploads/2019/03/design-of-equity-trading-markets-1.pdf (accessed on 12 December 2020).

- Pástor, Ľuboš, and Robert F. Stambaugh. 2003. Liquidity risk and expected stock returns. Journal of Political Economy 111: 642–85. [Google Scholar] [CrossRef] [Green Version]

- Utkilen, Henriette, and Synne Wakeford-Wesmann. 2019. Liquidity Following MiFID II. Estimating the Effect of Research Unbundling on Norwegian Small- and Mid-Cap Stocks. Master’s thesis, Norwegian School of Economics, Bergen, Norway. Available online: https://openaccess.nhh.no/nhh-xmlui/bitstream/handle/11250/2609729/masterthesis.PDF?sequence=1&isAllowed=y (accessed on 12 December 2020).

| 1 | The “sequential information” hypothesis e.g., Copeland (1976), Jennings et al. (1981) assumes that not all traders receive the information simultaneously, but rather sequentially and randomly, revising their expectations accordingly, with a new equilibrium being reestablished when all fully react to new information. |

| Stock Market Index | Number of Companies Included in the Stock Market Index |

|---|---|

| BET | 17 most traded companies on the Bucharest Stock Exchange (Romania) |

| WIG-20 | 20 most traded companies on the Warsaw Stock Exchange (Poland) |

| PX | 12 most traded companies on the Prague Stock Exchange (Czech Republic) |

| FTSE100 | 100 largest companies traded on the London Stock Exchange (UK) |

| DAX30 | 30 largest companies traded on Deutsche Börse (Germany) |

| CAC40 | 40 largest companies traded on Bourse de Paris (France) |

| Country | National Regulation That Transposes MiFID II Directive | Date of Enforcement |

|---|---|---|

| Romania | Law no.126/2018 regarding financial instruments market | 6 July 2018 |

| Poland | Act of 21 March 2018, amending the Financial Instruments Trading Act from 29 July 2005 | 21 April 2018 |

| Czech Republic | Act no. 204/2017 Coll. from 14th July 2017, for amending Act no. 256/2004 Coll. Capital Market Undertakings Act | 3 January 2018 |

| UK | Financial Services and Markets Act 2000 (Regulated Activities) (Amendment) Order 2017 Financial Services and Markets Act 2000 (Markets in Financial Instruments) Regulations 2017 Data Reporting Services Regulations 2017 | 3 January 2018 |

| Germany | Second Financial Markets Amendment Act (Zweites Finanzmarktnovellierungsgesetz—2nd FiMaNoG, from 24 June 2017 | 3 January 2018 |

| France | Ordinance no. 827 of 23 June 2016 (Ordonnance n° 2016-827 du 23 June 2016 relative aux marchés d’instruments financiers) the Monetary and Financial Code (Code monétaire et financier, CMF) General Regulation of the Financial Markets Authority (Règlement général de l’Autorité des marchés financiers, RGAMF) | 3 January 2018 |

| Variables | BET-3 Months | BET-6 Months | BET-12 Months | BET-18 Months | BET-24 Months |

|---|---|---|---|---|---|

| Post MIFID-II | −0.210 ** | −0.226 *** | −0.0620 | −0.0743 | 0.0347 |

| (0.0984) | (0.0670) | (0.120) | (0.0953) | (0.0779) | |

| High-Low Spread | 0.000696 | 0.000927 *** | 0.000932 ** | 0.00138 *** | 0.00156 *** |

| (0.000537) | (0.000270) | (0.000377) | (0.000315) | (0.000288) | |

| MIFID II * Spread | 0.000247 | 0.00260 *** | 0.00372 *** | 0.00321 ** | 0.00321 *** |

| (0.000714) | (0.000584) | (0.00131) | (0.00126) | (0.000756) | |

| Log(Trade Volume) | −0.0455 * | −0.0424 ** | 0.00902 | 0.0155 | 0.0296 |

| (0.0239) | (0.0214) | (0.0321) | (0.0234) | (0.0245) | |

| Log(Price Index) | 1.960 | 4.750 * | 5.739 | 4.037 | 8.975 *** |

| (1.815) | (2.758) | (3.876) | (3.530) | (2.810) | |

| Constant | 1.505 *** | 1.393 *** | 0.498 | 0.310 | 0.0460 |

| (0.411) | (0.360) | (0.523) | (0.382) | (0.395) | |

| 0.4158 | 0.3666 | 0.2956 | 0.2805 | 0.3858 | |

| Observations | 124 | 246 | 491 | 738 | 981 |

| 3 months | |||||

| (1) | (2) | (3) | (4) | (5) | |

| VARIABLES | CAC40_3 | DAX_3 | FTSE100_3 | PX_3 | WIG20_3 |

| Post MIFID-II | 0.407 *** | 0.434 *** | 0.117 | 0.109 * | 0.00457 |

| (0.124) | (0.123) | (0.117) | (0.0608) | (0.0753) | |

| High-Low Spread | 0.00329 ** | 0.00186 *** | 0.000516 | 0.00767 *** | 0.00109 |

| (0.00132) | (0.000440) | (0.000540) | (0.00292) | (0.00113) | |

| MIFID II * Spread | −0.000944 | −0.000664 | 0.00198 * | 0.00190 | 0.000449 |

| (0.00167) | (0.000579) | (0.00113) | (0.00537) | (0.00148) | |

| Log(Trade Volume) | −0.0541 | −0.0874 | −0.0917 * | −0.00663 | 0.00234 |

| (0.105) | (0.0831) | (0.0508) | (0.0216) | (0.0326) | |

| Log(Price Index) | 3.176 | 2.739 | 6.266 ** | 0.522 | 1.309 |

| (2.392) | (1.790) | (2.499) | (1.498) | (0.913) | |

| Constant | 1.318 | 1.965 | 2.306 ** | 0.498 | 1.045 * |

| (1.902) | (1.530) | (1.033) | (0.306) | (0.543) | |

| 0.6038 | 0.6340 | 0.4437 | 0.3937 | 0.0354 | |

| Observations | 124 | 123 | 124 | 123 | 125 |

| 6 months | |||||

| (1) | (2) | (3) | (4) | (5) | |

| VARIABLES | CAC40_3 | DAX_3 | FTSE100_3 | PX_3 | WIG20_3 |

| Post MIFID-II | 0.215 ** | 0.327 *** | 0.156 ** | 0.0670 | 0.109 * |

| (0.0994) | (0.0909) | (0.0758) | (0.0411) | (0.0601) | |

| High-Low Spread | 0.00365 *** | 0.00127 *** | 0.00128 *** | 0.00218 | 0.00133 |

| (0.00110) | (0.000358) | (0.000441) | (0.00343) | (0.000940) | |

| MIFID_II * Spread | −0.00144 | −0.000361 | 0.000389 | 0.00323 | 0.000369 |

| (0.00155) | (0.000459) | (0.000691) | (0.00412) | (0.00119) | |

| Log(Trade Volume) | −0.0527 | −0.117 ** | −0.127 *** | −0.00190 | 0.0206 |

| (0.0593) | (0.0469) | (0.0426) | (0.0193) | (0.0236) | |

| Log(Price Index) | 1.996 | 1.318 | 2.093 | −0.408 | 0.548 |

| (1.736) | (1.182) | (1.401) | (0.911) | (0.737) | |

| Constant | 1.389 | 2.648 *** | 3.045 *** | 0.507 * | 0.628 |

| (1.079) | (0.858) | (0.862) | (0.270) | (0.395) | |

| 0.2252 | 0.5116 | 0.3547 | 0.2535 | 0.1914 | |

| Observations | 251 | 248 | 249 | 248 | 248 |

| 12 months | |||||

| (1) | (2) | (3) | (4) | (5) | |

| VARIABLES | CAC40_3 | DAX_3 | FTSE100_3 | PX_3 | WIG20_3 |

| Post MIFID-II | 0.147 ** | 0.241 *** | 0.154 *** | −0.00862 | 0.0488 |

| (0.0722) | (0.0563) | (0.0522) | (0.0297) | (0.0698) | |

| High-Low Spread | 0.00137 | 0.000683 *** | 0.00112 *** | 0.000720 * | 0.00323 *** |

| (0.000946) | (0.000220) | (0.000305) | (0.000392) | (0.000893) | |

| MIFID_II * Spread | 0.000259 | 0.000112 | 0.000569 | 0.00625 *** | 0.00332 ** |

| (0.00110) | (0.000300) | (0.000501) | (0.00237) | (0.00153) | |

| Log(Trade Volume) | 0.116 | −0.0199 | −0.0923 ** | 0.00142 | 0.0512 * |

| (0.0710) | (0.0349) | (0.0357) | (0.0150) | (0.0280) | |

| Log(Price Index) | 2.043 * | 1.641 ** | 2.292 ** | 0.242 | 1.078 |

| (1.146) | (0.830) | (0.930) | (0.778) | (0.770) | |

| Constant | −1.553 | 0.948 | 2.356 *** | 0.474 ** | 0.000794 |

| (1.271) | (0.639) | (0.721) | (0.215) | (0.468) | |

| 0.2075 | 0.4669 | 0.4122 | 0.0799 | 0.2689 | |

| Observations | 504 | 498 | 500 | 445 | 493 |

| 18 months | |||||

| (1) | (2) | (3) | (4) | (5) | |

| VARIABLES | CAC40_3 | DAX_3 | FTSE100_3 | PX_3 | WIG20_3 |

| Post MIFID-II | 0.109 * | 0.183 *** | 0.104 ** | −0.0159 | −0.0622 |

| (0.0636) | (0.0518) | (0.0517) | (0.0307) | (0.0608) | |

| High-Low Spread | 0.00282 *** | 0.00116 *** | 0.00176 *** | 0.00168 | 0.00262 *** |

| (0.00106) | (0.000289) | (0.000369) | (0.00148) | (0.000849) | |

| MIFID_II * Spread | −0.000846 | −0.000257 | −1.05 × 10−5 | 0.00356 | 0.00404 *** |

| (0.00116) | (0.000327) | (0.000482) | (0.00277) | (0.00141) | |

| Log(Trade Volume) | 0.0623 | −0.0853 ** | −0.0680 | 0.0422 ** | 0.0423 |

| (0.0558) | (0.0383) | (0.0469) | (0.0184) | (0.0285) | |

| Log(Price Index) | 3.193 *** | 2.502 *** | 2.199 *** | 0.0460 | 1.901 *** |

| (1.194) | (0.930) | (0.827) | (0.933) | (0.728) | |

| Constant | −0.530 | 2.196 *** | 1.901 ** | −0.0883 | 0.205 |

| (1.002) | (0.699) | (0.944) | (0.262) | (0.477) | |

| 0.0721 | 0.1593 | 0.1516 | 0.0686 | 0.1358 | |

| Observations | 757 | 748 | 749 | 536 | 737 |

| 24 months | |||||

| (1) | (2) | (3) | (4) | (5) | |

| VARIABLES | CAC40_3 | DAX_3 | FTSE100_3 | PX_3 | WIG20_3 |

| Post MIFID-II | 0.216 *** | 0.200 *** | 0.171 ** | −0.0159 | −0.391 *** |

| (0.0686) | (0.0584) | (0.0716) | (0.0307) | (0.115) | |

| High-Low Spread | 0.00722 *** | 0.00298 *** | 0.00459 *** | 0.00168 | 0.00125 |

| (0.00118) | (0.000375) | (0.000959) | (0.00148) | (0.00136) | |

| MIFID_II * Spread | −0.00562 *** | −0.00207 *** | −0.00286 *** | 0.00356 | 0.0180 *** |

| (0.00126) | (0.000418) | (0.000995) | (0.00277) | (0.00441) | |

| Log(Trade Volume) | 0.227 *** | 0.0277 | −0.0469 | 0.0422 ** | 0.339 *** |

| (0.0662) | (0.0518) | (0.0485) | (0.0184) | (0.129) | |

| Log(Price Index) | 4.443 *** | 3.601 *** | 3.954 *** | 0.0460 | 4.667 ** |

| (1.414) | (1.249) | (1.287) | (0.933) | (2.067) | |

| Constant | −3.612 *** | 0.0789 | 1.399 | −0.0883 | −4.751 ** |

| (1.197) | (0.946) | (0.975) | (0.262) | (2.160) | |

| 0.2384 | 0.1796 | 0.2181 | 0.0686 | 0.3324 | |

| Observations | 1011 | 999 | 1000 | 536 | 984 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miloș, M.C. Impact of MiFID II on the Market Volatility—Analysis on Some Developed and Emerging European Stock Markets. Laws 2021, 10, 55. https://doi.org/10.3390/laws10030055

Miloș MC. Impact of MiFID II on the Market Volatility—Analysis on Some Developed and Emerging European Stock Markets. Laws. 2021; 10(3):55. https://doi.org/10.3390/laws10030055

Chicago/Turabian StyleMiloș, Marius Cristian. 2021. "Impact of MiFID II on the Market Volatility—Analysis on Some Developed and Emerging European Stock Markets" Laws 10, no. 3: 55. https://doi.org/10.3390/laws10030055

APA StyleMiloș, M. C. (2021). Impact of MiFID II on the Market Volatility—Analysis on Some Developed and Emerging European Stock Markets. Laws, 10(3), 55. https://doi.org/10.3390/laws10030055