First, this paper looks at how all three organizations developed their overall goals and strategies, and how this has been implemented in structures, values, and practices. Second, it explores how people in the corporations could respond to these goals and strategies and to what extent there was room for dissent and adaptation. Third, it analyses the extent to which there was illegal behavior and whether this behavior was condoned or disciplined internally. Fourth, it recounts what the companies did after the illegal behavior was discovered and made public, and to what extent they took responsibility or tried to deflect blame. And finally, it looks at how the companies’ messages over the years have compared to their practices in order to find out whether there was cognitive dissonance. After discussing these aspects separately, the final section examines the broader patterns of toxic cultural elements and explores what these patterns mean for attempts at cultural change.

3.1. Goals and Strategies

BP, VW, and Wells Fargo all started as underdogs with high ambitions. In the early 1990s, BP was struggling as oil prices had declined, many oil reserves in the Middle East had been nationalized by local countries, and the production costs of onshore drilling had hampered profits (

Lustgarten 2012;

Steffy 2010). At that time, Volkswagen had major difficulties in the U.S. market, where it had been unable to find a successor to the counterculture successes of the Beetle and the Transporter Van in the 1960s. Further, it struggled with the image of being unreliable and requiring frequent repair, had high labor and production costs, and barely broke even financially in 1992 (

Ewing 2017). Wells Fargo was a local bank operating largely in California (

Colvin 2017).

Yet, all three developed grand ambitions as new CEOs came to power. When John Browne became CEO of BP in 1995, he saw that BP could close its gap with the largest petroleum giants by rigorously focusing on divesting on-shore operations with low profits, by cutting costs, and by doing new oil exploration for major off-shore fields (so-called “Elephants”) in areas with higher risk but also higher profits (

Lustgarten 2012). When Ferdinand Piëch, grandson of Ferdinand Porsche who had designed the original Beetle for Hitler, took over as CEO of VW, he soon declared that by 2018 the German carmaker should become the largest in the world (

Ewing 2017). And when Richard Kovacevich became CEO of Wells Fargo, after it had been acquired by Minneapolis-based Norwest in 1998 that opted to drop its old name, he adopted the “Go for Gr-Eight” motto, seeking to guide the bank to the national and global top by outselling competitors and selling eight products per customer—four times the average rate for banks (

Colvin 2017).

In each of these cases, high ambitions focused on growth and profit increase, and with risk-prone means to achieve the goals. Wells Fargo had to go where no bank had gone before—to achieve fast growth, and reach the highly ambitious sales target, it had to somehow convince its clients not to buy two of its products (e.g., credit cards, insurance, special accounts), but eight.

At BP, the risk came as the new strategy required two opposed interventions: cutting costs and laying off a large part of the engineering expertise on the one hand, and developing new oil exploration in high risk areas that required extra engineering resources (

Steffy 2010). At VW, the mission to become number one could only be achieved by becoming competitive in the number one car market, the U.S. When Martin Winterkorn became CEO, he wanted to increase car production from six million to ten million in the next ten years, surpassing both GM and Toyota, which would mean that VW would finally have to succeed in the difficult U.S. car market.

To do so, Winterkorn bet on clean diesel and a new diesel engine: the EA 189. The problem was that the company had been unable to develop an engine that was actually economical, practical, and clean and could compete in the U.S. market. VW’s option—to cut the toxic NOx emissions that the higher temperature burning diesel engines produce—came with its own problems of higher price, occupying precious storage space, and requiring more frequent maintenance, which would all prohibit a successful strategy (

Ewing 2017). Thus, VW set itself a target that may well have been impossible to achieve.

It was not long before the new ambitions and values they represented turned into practices and structures that produced risks of wrongdoing and damages. At BP, this was most evident in cost-saving reforms. After John Browne took the helm, he started to cut costs aggressively, with across-the-board cuts of 25%, first in 1999 and then again in 2004. This affected not just material costs, but also personnel, resulting in forced lay-offs, thus shrinking BP’s pool of engineering talent (

Steffy 2010). It was not long until these general cuts started to affect the safety at BP operations. In the years prior to the 2005 Texas City explosion, BP had decided not to replace outdated equipment that later caused the massive accident. BP simply wanted to save on the

$150,000 investment that was needed. One employee, as reported by PBS, wrote: “We need to decide if we want to invest

$150,000 now to save money later on” (

PBS 2010). And a senior manager wrote “that capital expenditure is ‘very tight. Bank the

$150,000 in savings right now’” (

PBS 2010). It is no wonder that former Secretary of State James Baker, who headed one of the two investigations into the Texas City explosion, concluded that “BP has not adequately embraced safety as a core value” (

Baker et al. 2007). In the 2006 Alaskan spill, the leak occurred in a corroded pipe, “which hadn’t been cleaned in over a decade” (

PBS 2010). In Alaska, BP had for years, as a subsequent investigation found, sacrificed proper maintenance for profit. Investigators found that “‘unacceptable’ maintenance backlogs ballooned as BP tried to sustain profits…even though production was declining” (

Lustgarten and Knutson 2010). The investigation clearly concluded that these issues are at the heart of BP’s value system: “There is a disconnect between…management’s stated commitment to safety and the perception of that commitment” (

Lustgarten and Knutson 2010). And preceding the Gulf spill in 2010, BP managers “were shaving maintenance costs with the practice of ‘run to failure,’ under which aging equipment was used as long as possible” (

Lustgarten and Knutson 2010). In sum, BP in its day-to-day operations valued profits over anything else, even at the repeated sacrifice of safety and the environment.

The overall targets of cost reduction played a crucial role in BP safety issues, as the Chemical Safety and Hazard Investigation Board (CSB) concluded in its 341 page report after the 2005 report in response to the Texas explosion that had killed 15 (

U.S. Chemical Safety and Hazard Investigation Board 2007). As a supervisor told lower-level managers who had questioned the 2004 budget cuts and their implications for ensuring operations: “Which bit of 25 percent do you not understand?” (

Steffy 2010, p. 117). Another manager explained how this forced them towards risky and illegal practices: “The focus on controlling costs was acute at BP, to the point it became a distraction. They just go after it with a ferocity that’s mind-numbing and terrifying. No one’s ever asked to cut corners or take a risk, but often it ends up like that” (

Steffy 2010, p. 58).

At VW, Winterkorn’s ambitious target, to sell ten million cars and focus on clean diesel, put engineers in a bind. They could develop a clean diesel engine. To do so, they could use technology from Daimler, called BlueTec, that sprayed a chemical substance called urea into the exhaust to help breakdown NOx emissions (

Ewing 2017). However, it came with an extra cost of about

$350 dollars for each car, and also required installing an extra tank that would take up cargo space and require owners to do frequent refills.

The other option was a so-called “lean NOx trap” that separated nitrogen oxide molecules into harmless oxygen and diatomic nitrogen. This technique was cheaper and did not need an extra tank, but it required an exhaust gas recirculation system that produced more carcinogenic fine particle emissions, and also caused the soot filter to wear out faster (

Ewing 2017). Considering U.S. law obliged car makers to have emissions control systems effective for the entire lifespan of the vehicle, the soot filter wear was a core problem.

Nonetheless, VW’s highly ambitious targets played such a strong role that by late 2007, engine specialists had never seriously considered adjusting them to the engineering realties they faced. Rather than give up on the targets, VW engineers were forced to look for alternative solutions. They not only adopted the lean NOx trap, but also installed the software “defeat device” that would only switch on the emissions control system during emissions testing, so that during normal driving the soot filter would remain intact longer (

Ewing 2017). Because of VW’s cost reduction efforts to make as many models as possible share the same parts, the decision to install cheating devices on the EA 189 engine came to affect over ten million cars VW produced and sold.

At Wells Fargo, the push for growth through the extremely high sales targets was to be achieved through bank employee incentive systems. The bank’s branches started to set product sales goals for employees to meet. This put tremendous pressure on Wells Fargo bankers to sell more products to their clients. Employees would be under constant scrutiny with daily and monthly “Motivator” reports tracking their sales volumes (

Frost 2017). If they failed to meet targets, employees would undergo “coaching sessions.” One employee explained later to National Public Radio (NPR) journalists that these sessions were not there to support the workers but just to pressure them to sell more (

Arnold 2016). Another employee explained how, when she failed to meet her target, two managers would lecture her at her desk and then perp-walk her while colleagues were watching. As she explained: “It’s like being called into the principal’s office. Sit down at the large conference table, no windows in this room, they shut the door, lock the door” (

Arnold 2016). After that she was forced to sign a “formal warning” and was warned: “If you don’t meet your solutions you’re not a team player. If you’re bringing down the team then you will be fired and it will be on your permanent record” (

Arnold 2016). She was simply afraid to lose her job and fearful not to get another one with the bad state of the economy. This employee said that things got so bad that she vomited under her desk.

Another employee compared his Wells Fargo job to “being in an abusive relationship” (

Arnold 2016). Things were worst during special sales campaigns, such as the “Jump into January” campaign that sought to start the year with strong sales. During such campaigns, employees were to reach even higher targets than usual, sometimes even up to twenty per customer. In one local branch office, employees were forced to “run the gauntlet” by running past costumed district managers to write their sales numbers on a white board (

Frost 2017). It became increasingly clear that employees had started to resort to creating unauthorized or fake accounts in response to these extreme pressures to boost their sales targets and achieve the overall goals set in the company. Yet, for a long time no change was made to the targets themselves or the pressures through which they were implemented. As one report found, Wells Fargo “was hesitant to end the program because (Carrie) Tolstedt (the head of community banking at the time) was ‘scared to death’ that it could hurt sales figures for the entire year” (

Frost 2017).

And the strategy worked. In 1999, BP, after cutting costs and taking over several competitors, quadrupled in value, and finally caught up with the top oil companies. Its stocks soared, and its CEO, Browne, was dubbed “Sun King” in British newspapers. VW finally became successful in the U.S. market with its clean diesel, and eventually even after the emission scandal was discovered became the largest car company in the world in 2015, three years ahead of the planned schedule (

Ewing 2017, p. 187). And Wells Fargo jumped from the ninth most valuable bank in America, to the most valuable one in the world in 2015. Wells Fargo achieved 18 consecutive quarters of over

$5 billion in profits—a feat it shares only with Apple (

Colvin 2017).

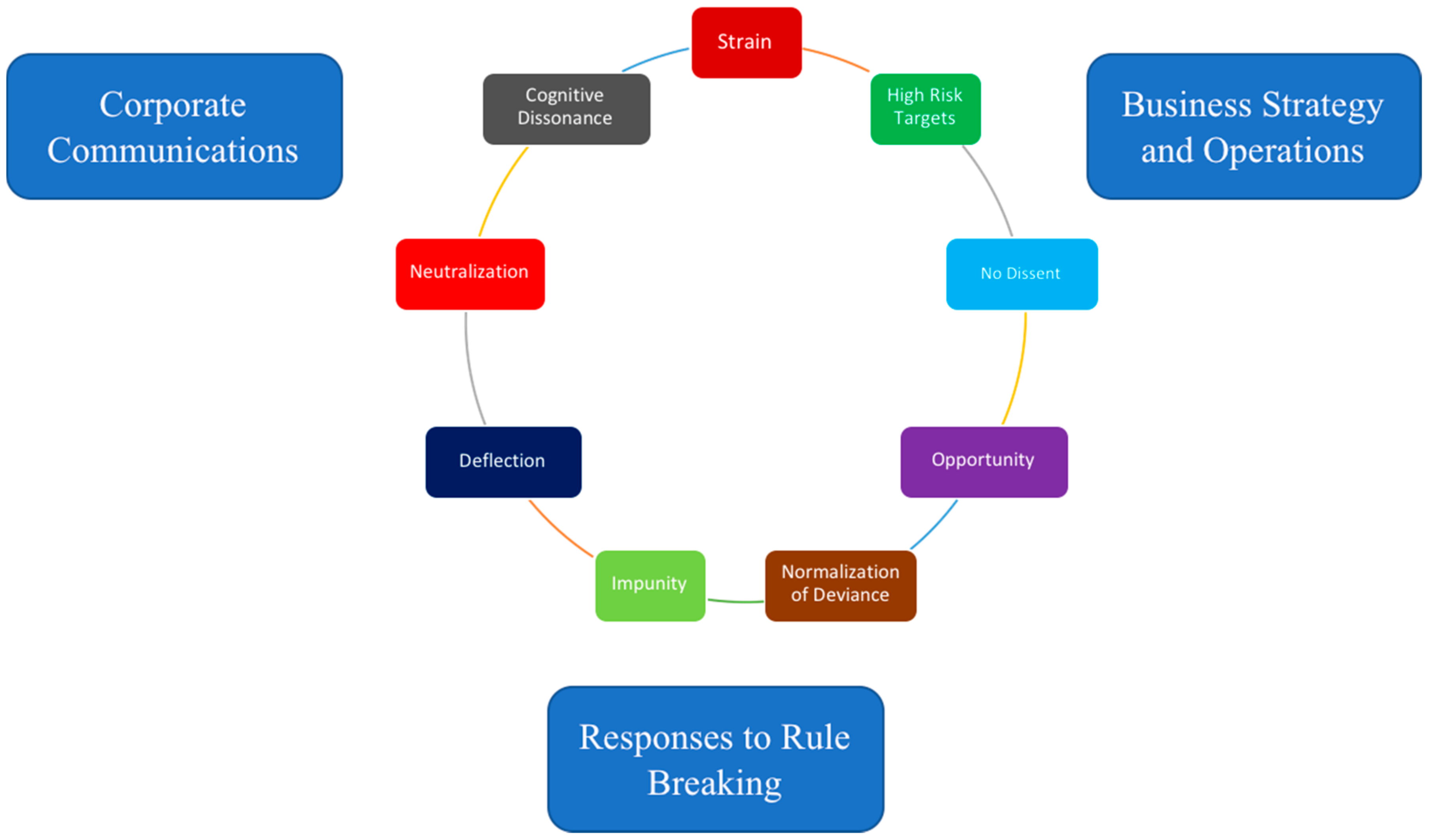

In sum, this analysis of how these companies set their targets and responded to challenges in the business environment demonstrates how toxic elements came to exist in these three cases. The most important type of toxic norm, from those discussed in

Table 2 earlier, is strain (

Agnew 1992,

2001;

Agnew et al. 2009;

Simpson and Koper 1997). What we see here is that the companies themselves were under strain of the shareholder’s expectations of growth and revenue formation. New leaders responded to these pressures by setting highly ambitious goals that because of their high risk and low feasibility nature brought the external strain into the company’s operations and ultimately to the employees, which in crucial instances forced them to make or go along with decisions that were damaging, and at worst illegal. These negative responses to strain and its resultant negative influences came at the cultural level of structures (see

Table 1), as it was laid down in targets and incentives (cf.

Schein 2010), but soon moved deeper into explicit shared values and visible common behavior (see

Table 1).

3.2. Management and Employee Responses to Goals and Strategies

So why did BP employees, VW employees, and Wells Fargo employees go along with these goals? Why did they not successfully resist or change these goals or the practices they produced, even though they must have seen they were not realistic or risk free? To answer these questions, we must look at the corporate structures in the companies and how they shaped internal communication as well as the way responsibility for targets and work was shared.

BP and Wells Fargo have hierarchies that are strikingly different from Volkswagen. VW had a highly centralized structure with strong power vested in the CEO at the top. There was a centralized authority in decision-making that forced decisions to go up the chain of command. As one former manager trainee described it: “VW was like North Korea without the labor camps. You have to obey everyone” (

Ewing 2017, p. 93). VW’s CEO played a central and direct role in day-to-day decisions, with first Piëch, and later his successor Winterkorn, as engineers who micro-managed engineering decisions all the way to the interior color of cars promoted at auto shows.

By contrast, Wells Fargo and BP had highly decentralized structures. Under Browne’s leadership, BP established business units that were to operate at autonomous companies within the overall BP structure. Each had its own targets, its own profit reporting, and its own leadership. At some point BP had over 300 such decentralized units. As Steffy argues, this created an unwieldy structure, with each unit leader caring for his own goals without focusing on how these affected the whole (

Steffy 2010). BP also often used sub-contractors and outsourced key aspects of its work, further delegating responsibilities, but now outside of its own employees (

Bozeman 2011). Wells Fargo was very similar to BP in that its operation was split amongst business units. Wells Fargo’s CEO Kovacevich nicely illustrated the structure when he called himself a “CEO of CEOs” (

Colvin 2017).

While the three companies had such different hierarchical structures, in all three there was limited possibility to resist top-down targets and have effective dissent. Comparing the cases reveals that the overall hierarchy itself was not the core issue here, but rather how information flowed across the structure from bottom to top and top to bottom. Clearly, VW’s highly centralized hierarchy meant lower level employees had trouble getting their information heard at higher levels. Thus, at VW it was hard for lower level employees to correct faulty central level decision making and targets.

However, BP and Wells Fargo’s decentralized structures did not allow for much better information flow that might have corrected unrealistic budget cuts and sales targets. At BP for instance, in 1999, a group of 77 workers at the Alaskan operations—where later a major spill would occur—wrote a desperate letter to CEO John Browne trying to sway him from the intended cuts as they feared it would further undermine the already appalling safety conditions (

Lustgarten 2012). The letter points to the difficulty of communicating critical information upwards: “Anything we say either stays at this level or gets filtered on the way up to a version of ‘can do sir’…Our feedback is ignored because it doesn’t support the preordained agenda…Your frontline management and supervision will continue to cut as long as you direct and sanction it, right up to the precipice of disaster and over” (

Lustgarten 2012). John Browne did not reply and instead, a month later, announced another

$4 billion budget cut.

Five years later, in 2004, the new BP Texas City Refinery Plant manager also tried to get attention from higher executives at the London office. He presented a detailed report entitled “Texas City is Not a Safe Place to Work,” about the horrible safety record at the plant, where over three decades 23 workers had died—one of the worst records in the industry. He also conducted a survey amongst workers that unearthed widespread safety concerns that had long gone unheard and unaddressed. The new manager used the report to ask for a budget increase to upgrade the safety at the plant. The main office denied his request and asked him to focus on the 25% budget cuts he had to meet for 2004, all the while the refinery was making

$100 million a month for BP (

Steffy 2010, p. 67).

Similarly, Wells Fargo senior executives refused to respond to challenges by regional leaders of the bank who had come forward to complain that the sales goals were too high and had become “increasingly untenable” (

Frost 2017). What was at play here was not so much the structure itself, but the failure of higher level employees to adequately allow lower level employees to provide input and be heard. Targets were formulated in a top-down fashion and implemented while disregarding critique, regardless of the decentralized structure at Wells Fargo and VW.

In all three companies, the composition of the labor force and executive management practices made dissent difficult. At Wells Fargo the high strain of the job resulted in massive staff turnover, reaching up to 41% in one year (

Colvin 2017). This left the bank with highly inexperienced employees, less likely to successfully raise concerns over the targets they had to meet. Through its mass lay-offs, BP similarly got rid of a large swatch of its senior engineers, who would have been in the best position to speak out against the safety hazards that were becoming increasingly apparent (

Steffy 2010). BP CEO John Browne wanted a bench of followers, which he dubbed his “turtles,” referring to the Ninja Turtle cartoon (

Steffy 2010, p. 58). And at VW, CEOs Piëch and later Winterkorn often fired executives they did not like, keeping only those who would agree with them and support their positions (

Ewing 2017). At BP, meanwhile, frequent executive job rotations, which were a standard management practice, incentivized these lower level leaders to focus on short term targets while disregarding the longer term consequences, and thus made them more concerned with meeting the targets set by the company headquarters than enhancing long term safety (

Lyall 2010).

Dissenting opinions were also suppressed through intimidating management practices. An investigative report following the 2010 Deep Water Horizon Spill found at BP “a pattern of intimidating workers who raised safety or environmental concerns” (

Lustgarten and Knutson 2010). At Wells Fargo, as discussed above, daily intimidation practices were used to cajole and publicly shame employees to keep focused on their targets and the overall growth of the bank. Employees at all levels worked on the pressure of constant, sometimes hourly ranking of their sales rates in comparison with peers. When found to be lagging, they risked demotion or dismissal. As one employee recalled: “We were constantly told we would end up working for McDonald’s if we did not make the sales quotas…we had to stay for what felt like after-school detention, or report to a call session on Saturdays” (

Reckard 2013). This clearly did not produce an atmosphere conducive to voicing critical opinions.

At VW, intimidation occurred at the highest levels. CEO Winterkorn was known for his Tuesday top executive meetings that included the highest-level officials in charge of major brands like Audi or Seat. At the meetings, with all present, Winterkorn would mercilessly criticize any executive that had failed to meet set targets. Ewing explains the humiliating tactics that Winterkorn used: “Managers who were favorites one week could suddenly fall from grace the next. Sometimes they learned they had been demoted or dismissed not from Winterkorn or a colleague but from reading about it in a German business publication, like

Manager Magazine, that had somehow been tipped off” (

Ewing 2017, p. 157). Similarly, at Wells Fargo the head of community banking, Tolstedt, an internal board review found, was “insular and defensive and did not like to be challenged or hear negative information. Even senior leaders within the Community Bank were frequently afraid of or discouraged from airing contrary views” (

Colvin 2017).

Let us here also look at what we can draw out from these three cases about how toxic cultures form.

The most important insight here is that in all three cases a strong social norm (injunctive but also in the form of visible common (and probably unaware common) behavior) developed that dissent was not appreciated and that targets had to be met. A strong norm developed in all three companies not to resist or disagree with higher level targets and commands. This norm in and of itself is not directly opposed to the legal norms at play here. It does not support breaking safety standards, creating defeat devices, or fraudulently opening false or unauthorized bank accounts. This social norm here rather obstructs behavior that supports compliance. It makes it harder for employees or executives to come to speak out and resist practices that break the law. As such, it also undermines checks and balances within the company, especially over policies and practices of higher level leaders that come to break the law. In turn, this creates a larger opportunity to break the law (

Belknap 1987;

Cohen and Felson 1979;

Felson 1987;

Osgood et al. 1996), and when such rule breaking is allowed to occur without critique, it thus becomes condoned and even normalized (

Vaughan 1989,

1997). As such employees here operated in an inactive moral climate, where there may have been recognition of unethical and immoral problems, but a very limited space to act on them (cf.

Moore and Gino 2013;

Scholten and Ellemers 2016).

In this context, the social norm against critique and dissent can work in tandem with generating further strain (

Agnew 1992,

2001;

Agnew et al. 2009;

Simpson and Koper 1997). Specifically, employees and managers were under pressure due to the strong coercive processes as well as the fierce competition and job insecurity some had. As such, in light of

Table 2’s framework to understand toxic organizational norms and processes, our analysis of employee and management participation in goals and targets shows that four toxic processes were at play in the organizational culture: obstruct behavior that supports compliance, strain away from compliance, normalization of deviancy, and creating opportunity to violate the law. Here, in light of

Table 1’s outline of the levels and aspects of organizational cultural analysis, we see that these toxic processes developed first at the level of values, they became reinforced by the structures of hierarchy and incentives, and became deeply embedded as they developed into common practices (cf.

Schein 2010).

3.3. Illegal Behavior and Internal Responses

By the time the scandals became public, all three companies had already engaged in the damaging and rule breaking behavior for years or even decades. BP had, from the 1990s onwards, developed an appalling safety record at its operations. Its operations were so bad that it had one of the worst safety records in the industry, paying one multimillion dollar fine and settlement after another to the EPA and OSHA, only to be found breaking the same safety standards again (

Lustgarten 2012;

Mattera 2016;

Steffy 2010). Even after the major 2005 Texas Refinery explosion that had killed 15 workers and wounded 170, BP’s major safety problems continued. In the three years following the explosion, and after paying

$20 million in fines to OSHA, and after being forced to do a

$1 billion upgrade to the facilities, another four people were killed at the refinery. And another two were killed in another BP refinery in Washington State. BP thus had five fatalities in two facilities, while there had been a total of nine fatalities in all other 146 non-BP refineries in the U.S. (

Steffy 2010, p. 139).

For comparison purposes, consider how BP had had 700 OSHA safety violations in three years, whereas Exxon, which after the Valdez disaster completely improved its safety record, had only one (

Steffy 2010, p. 150). BP never seriously responded to the concerns of its employees, its lower level managers, or even regulators. Each time, BP would negotiate a settlement or simply pay the fine, and do what was demanded in paying for upgrades or installing safety management. But it would not end its relentless pursuit for higher profits by cutting costs and pursuing high risk high reward exploration and refinery. The norm in BP thus became that safety hazards were part of the job, that deviating from safety norms was normal, and that redress rather than prevention was the way to address them (

Lustgarten 2012;

Steffy 2010).

Volkswagen and Wells Fargo had similarly normalized deviancy. As we saw already, Volkswagen had used defeat devices all the way back to 1973, when it was first caught and ordered to pay a

$120,000 fine to the EPA. Then, in 2005, VW had to pay a

$1.1 million fine to the EPA for emissions cheating in Mexico. And starting in 1999, the company had installed a device in the software controlling the highly polluting noise control system in its Audi engines that would switch off this system and reduce pollution when it recognized the car was being tested (

Ewing 2017). So, when engineers frantically sought to find a solution to make the new VW diesel clean, but also economical and practical, they had models to turn to. In fact, the Audi device served as a direct example for the much more widespread cheating that VW would do with the EA 189 engine. During a meeting where 15 engineers, including the head of VW engine development, met to discuss how to create an economical engine that would pass stringent U.S. emissions tests, the idea of this defeat device was presented and debated. While some pointed out of the risks breaking the law by adopting this device, others stated that this was normal and that many carmakers did so and VW had to do so as well if it were to keep up with competition (

Ewing 2017, p. 122). According to Ewing’s analysis of the meeting, most engineers would not see this as “a grave violation of Volkswagen standards. There was plenty of precedent for using shortcuts to cope with inconvenient regulations” (

Ewing 2017, p. 123). In all the earlier instances of cheating, VW as a company had turned a blind eye and condoned the behavior that had occurred, paying the fines should they come, without creating clear boundaries that this was unacceptable behavior. And once they had started using the cheat in their diesel engine there was no more stopping. As Ewing explains, “defeat devices which may have begun as a stopgap had become a habit” (

Ewing 2017, p. 178).

Since adopting the ambitious Going for Gr-eight targets, Wells Fargo learned about more and more instances where its employees had opened fake and unauthorized accounts, from 63 in 2000, to 680 in 2004, to 288 in a single quarter in 2007, to 1469 in a single quarter in 2013 (

Colvin 2017). In 2002, it was discovered that a whole Colorado branch had been opening unauthorized and fake accounts simply to reach their sales targets. The bank responded simply by firing individual employees involved, but not by addressing this as a systemic problem caused by their own targets. Bank leaders were actually positive about the numbers, as it showed them that only 1% of the work force had to be fired for cheating, while they assumed the other 99% were in compliance. As then CEO Stumpf said in an email to another bank leader: “Do you know only around 1% of our people lose their jobs [for] gaming the system, and about 2/3 of those are for gaming the monitoring of the system, i.e., changing phone numbers, etc. Nothing could be further from the truth on forcing products on customers. In any case, right will win and we are right. Did some do things wrong—you bet and that is called life. This is not systemic” (

Colvin 2017).

While the company would fire employees caught red-handed in defrauding clients or the bank, it turned a blind eye to ongoing practices, never seeking to proactively find out how widespread they were and end them. Neither did Wells Fargo fully make clear that reaching sales targets was less important than compliance. As increasingly more employees started to cheat, a norm developed. As Colvin explains: “The message was clear to everyone in the retail bank: Everyone knew the goals were sheer fantasy for many branches and employees. At some branches not enough customers walked in the door, or area residents were too poor to need more than a few banking products. Bank leaders called overall quotas ‘50/50 plans’ because they figured only half the regions could meet them. Yet no excuses were tolerated. You met the quotas or paid a price” (

Colvin 2017).

In all three companies, norms thus developed that normalized risky, rule breaking, and damaging practices that would come to shape the values and assumptions of corporate employees and executives. This was not merely a passive process in which the corporations allowed the practices to develop in response to the structures of budget cuts and highly ambitious targets. At times corporations would directly condone these practices. Volkswagen never strongly responded to any of the earlier cases where its engineers had installed defeat devices. At BP for instance, an independent investigation found that the oil company allowed “pencil whipping” and the fabrication of inspection data. One employee said that “BP workers felt pressure to skip key diagnostics, including pressure testing, cleaning of pipelines, and checking for corrosion, in order to cut costs” (

Lustgarten and Knutson 2010). A former Wells Fargo assistant vice president and regional private banker has sued the bank claiming that she was fired when she refused “to participate in a scheme to manipulate accounts and sell products that weren’t in customers’ best interest.” She alleged that her superiors were running the scheme (

Associated Press 2017). Other employees have come forth complaining that they were fired after trying to report the illegal practices to the ethic’s hotline (

Egan 2017). In another case, a former branch manager had found out that bankers had swayed a homeless person to open six bank accounts getting her to pay

$39 per month. She explained: “It’s all manipulation. We are taught exactly how to sell multiple accounts” (

Reckard 2013). She reported the situation to higher executives but never received any answer (

Reckard 2013). Or as another former employee explained: “Training in questionable sales practices was required or you were to be fired” (

Colvin 2017). Clearly, at Wells Fargo this was not simply a matter of lower employees breaking Wells Fargo rules. And it was not simply a common practice: It had become something that was endorsed and for which no internal complaints were accepted, let alone seriously acted upon to change the root causes that sustained it.

The ongoing illegal behavior and internal responses to it in all three cases offer us further insight into toxic elements in their culture. Again, we will first discuss the types of toxic norms and their processes (drawing on

Table 2 above) and then look at what level of culture we find these in (drawing on

Table 1). A first clear toxic process was that in all three cases the existence of illegal practices formed visible common behavior (a descriptive social norm (cf.

Cialdini et al. 2006)) that was directly against the law and thus came to compete and resist with the law (cf.

Moore 1973;

Heimer 1999). The lack of company responses to such illegal behavior spurred two further negative cultural processes. As illegal behavior could continue unaddressed, the companies normalized deviance (

Vaughan 1989,

1997) and failed to foster learning processes that could prevent future misconduct (

Homsma et al. 2009). As the companies turned a blind eye to the ongoing illegal practices, and never sought to proactively detect and stop them, they also created an opportunity for employees to cut corners at very little risk. As long as it did not create a major scandal with outside complaints or regulatory investigations, the companies were not proactively seeking to find violators or hold them accountable. And thus, the companies left the henhouse open to the foxes. Or in the terms of the Routine Activities Theory, “committed offenders” had access to “suitable targets” as there were no “capable guardians” (

Cohen and Felson 1979). The negative cultural processes here started at the practice level, with visible common behavior, that probably became unaware common behavior, and then moved into the values, especially the injunctive social norms and hidden assumptions, as what people saw converged with what they came to think.

3.4. Responses to Exposure of Scandals

So, what happened when the three companies came to face strong public and legal scrutiny when each had its scandals exposed? Organizational responses to crisis offer a clear window into what values a company communicates both outwards and inwards to its own employees at the most critical moments. Crucially, responses to scandals are major organizational moments that can have a strong impact on the organizational culture and the extent to which it is toxic. In all three, the companies deflected blame, defended themselves from liability, and some, most notably VW, even tried to downplay the damages of their actions. By doing so, the companies neutralized their own culpability, thus enabling further rule breaking.

The Wells Fargo response to over a decade of fraudulent practices was to blame the individual employees, and not the unrealistic sales targets, lack of response to complaints, and threatening practices that had stimulated these lower level bankers to start cheating. As Frost explains: “It was convenient instead to blame the problem of low quality and unauthorized accounts and other employee misconduct on individual wrongdoers” (

Frost 2017). At Wells Fargo, the fragmented corporate structure enabled blame shifting and obstructed taking responsibility for malpractice elsewhere in the company. As Colvin analyses: “For example, the corporate chief risk officer had no authority over the retail bank’s risk officer, who reported only to Tolstedt (who headed community banking). The HR department regarded employee misbehavior as an issue of training, incentive compensation, and performance management. The law department’s employment section focused mainly on litigation risks from firing employees. Each concerned itself with its assigned slice of the issue; no one looked for the root cause or envisioned big-picture consequences” (

Colvin 2017).

Wells Fargo tried to persist in this strategy even in 2016, after the true scale of the fraudulent behavior became public and the company had to respond to news that it had defrauded millions of U.S. customers. Its first response was to blame individual employees and fire 5300 lower level bankers, without taking responsibility at the top. In a hearing before the Senate Banking Committee on 20 September 2016, CEO Stumpf apologized for not ending the illegal practices earlier and promised that the bank would undergo reform (

Corkery 2016). Senators were angry that he did not offer any concrete steps against executives, including himself, and had just shifted blame and punishment to those at the bank’s lower levels. As Senator Elizabeth Warren asked him: “Have you returned one nickel of the money that you earned while this scandal was going on? Have you fired any senior management, the people who actually oversaw this fraud?” After Mr. Stumpf, answered that he had not, Warren retorted: “Your definition of accountability is to push this on your low-level employees. This is gutless leadership.” But Mr. Stumpf persisted stating: “The 5300 (fired employees) were dishonest, and that is not part of our culture. That is not scapegoating” (

Corkery 2016). In a statement to National Public Radio inquiries following the hearings, Mr. Stumpf said: “Although the vast majority of our team members do the right thing, every day, on behalf of our customers, these allegations and accusations are very serious. And if any of these things transpired, it's distressing and it’s not who Wells Fargo is” (

Arnold 2016).

Senators also pushed the CEO about whether the bank would seek to claw back the millions of compensations of top executives who had failed to fulfil their duty to stop the scandal. Here they especially focused on Carrie Tolstedt, who had been in charge of community banking where all the issues had happened. She retired at age 56 with a package of tens of millions of dollars, just three months before the hearing. Mr. Stumpf explained that although Ms. Tolstedt had let the illegal practices go on for three years after they were first discovered in 2013, he did not want to fire her because she performed so well in her other duties (

Corkery 2016).

BP’s first response to major scandals was to deflect blame. One tactic was to try to place on blame on individual workers, at worst the ones who had been directly hurt in accidents. These were the same workers who had been concerned over the safety of the operations, as years and years of budget cuts had created a very hazardous working environment. And when things then did go wrong, as was likely to happen with the budget cuts, their company would blame them. Workers at the Texas Refinery, which was the site of the deadly 2005 explosion, had been interviewed previously about safety issues. One explained: “Yes I have been hurt and had management punish me and made a fool out of me. Need I say more?” (

Steffy 2010, p. 66). Another, who had been hurt because of a mechanical failure: “I was blamed in the end. I was not the root cause” (

Steffy 2010, p. 66).

And after the 2005 explosion at the Texas refinery facility BP followed a strategy of stonewalling and blame shifting (

Smithson and Venette 2013). It first put the refinery on lockdown for eight days, not letting anybody in, claiming that it was too hazardous. Then two months later, it issued its internal investigation report and placed blame squarely on the low level employees who were alleged to have overfilled and overheated the raffinate splitter (

Steffy 2010, p. 89). Steffy summarized BP’s response: “Human error-or workers not following rules-meant that BP itself wasn’t to blame” (

Steffy 2010, pp. 89–90). Ironically enough, a BP executive had chaired the development of safety guidelines by the Center for Chemical Process Safety that concluded that “errant employees aren’t the root cause of an accident but rather its symptom” (

Steffy 2010, p. 90).

Five years later, following the Deepwater Horizon spill, BP also sought to deflect blame. Its first tactic was to try to steer out of the scandal, when media during the initial 12 days focused on Transocean, the owner of the rig. Transocean could act as a good shield (

Steffy 2010, p. 182). In one of the early statements BP CEO Hayward stated: “We are responsible, not for the accident, but we are responsible for the oil” (

Smithson and Venette 2013, p. 402). He said this in spite of Transocean’s reliance for most of its business on BP for most of its business and the big oil company’s major influence in day-to-day operational decisions—decisions that enhanced risks and neglected industry standards, all to expedite the drilling and save costs (

Smithson and Venette 2013, p. 402). Therefore at first, BP tried to use its decentralized structure with sub-contractors to defect blame. It had done so earlier. In the 1990s for instance, BP had blamed a sub-contractor, Doyon, when it was found that BP Alaska had been illegally injecting its toxic waste into the ground, even though BP was again directly in charge and Doyon relied for 80% of its income on BP (

Lustgarten 2012, p. 61).

BP leadership also tried to downplay the role they themselves played in all this. This was most apparent in CEO Hayward’s testimony during the U.S. congressional hearings. He kept on deflecting critical questions about how BP had managed risk. Hayward instead focused on how much money the company had spent on safety (

Smithson and Venette 2013, p. 402). Whenever he was pressed about problems, Hayward would insist that the investigation was ongoing and no firm conclusions about the role BP had played in all this could be made yet. When Representative Bart Stupak asked him, “Are you trying to tell me you have not reached a conclusion that BP really cut corners here?” Hayward answered simply: “I think it’s too early to reach conclusions, with respect, Mister Chairman. The investigations are ongoing” (

Smithson and Venette 2013, p. 403). When Hayward was asked about BP’s decisions about particular aspects of the operation that had caused the risk, he would explain that he was not involved in the decision making. When pressed on details, he would claim ignorance. For instance, when Representative Michael Burges asked a question about why BP had installed fewer than the recommended number of centralizers that were to ensure the proper flow of cement, Hayward said: “I can’t answer that question, I’m not a cement engineer I’m afraid” (

Smithson and Venette 2013, p. 404). But Hayward does have a PhD in geology, 28 years of experience in oil and gas exploration, and had been CEO of BP America for the three years prior. As Smithson and Venette conclude: “The suggestion that someone with Hayward’s experience and knowledge had insufficient information to determine whether BP made risky decisions was ridiculous” (

Smithson and Venette 2013, p. 404).

BP did not stop there. It even tried to downplay the damage of the spill. At first, BP had stated that that oil was leaking at 1000 barrels a day, a relatively modest spill. That would indicate that the spill would only reach Exxon Valdez levels after one year. A little later, BP raised that figure from 1000 to 5000 barrels a day (

Steffy 2010, p. 184). In fact, oceanographers from Florida had used satellite imaging data and found that the size of the leak was much larger at 30,000 barrels a day, meaning the leak could surpass the Valdez spill in only two weeks. CEO Hayward dismissed these findings saying that their own information was the most accurate: “A guestimate is a guestimate and the guestimate remains at 5000 barrels a day” (

Steffy 2010, p. 184). When BP was forced to release its live video feed from the wellhead or face a congressional subpoena, experts found that the leak was even larger—about 60,000–70,000 barrels per day (

Steffy 2010, p. 185). Hayward later even went as far as to deny that such a massive spill caused much damage. In an interview with the Guardian he stated: “The Gulf of Mexico is a very big ocean…the amount of oil and dispersant we are putting into [it] is tiny in relation to the total water volume” (

Kollewe 2010).

But no one tried to deflect blame like Volkswagen. Soon after Volkswagen learned about the West Virginia University study that had demonstrated that the on-road emissions were many times higher than lab tested emissions, the head of product safety, Bern Gottweis, sent a memo to CEO Winterkorn. The memo concluded that “A thorough explanation for the dramatic increase in NOx emissions cannot be given to the authorities” (

Ewing 2017, p. 177). He concluded that in further testing, the authorities would find out that there was a cheat device. And VW could revise the software to decrease emissions during road testing, but not to a compliant level (

Ewing 2017). So very early on in the development of the scandal, the highest level executives at VW knew that regulators would find the defeat device and there was no way to salvage the situation. But rather than coming clean with the Californian and federal environmental regulators, VW opted to stall, to cheat even more, to deflect blame, and even to try to argue that the harm was limited. Soon after VW learned of the tests, there was a presentation that discussed the costs and benefits of different response options: refuse to acknowledge the problem and continue to stonewall and lie, offer an update to the engine software that would decrease emissions but not to the compliant level, or admit to the problem and buy back diesel cars in the US. The last option, Ewing concludes, “does not appear to have been seriously discussed at the time” (

Ewing 2017, p. 179).

By this time, in May 2014, Volkswagen came to adopt a new NOx control system by installing urea tanks that catalyzed NOx into harmless oxygen and nitrogen. However, Volkswagen never installed a tank big enough to truly control the emissions at a sufficient level. So, the cars continued to have cheat devices that would only allow a sufficient level of urea to be used during lab testing, and not during road driving so that owners would not have to fill up their tanks with an extra chemical (

Ewing 2017). In light of the investigation, Volkswagen tweaked its EPA application, indicating that owners would have to fill their tank “approximately” every ten thousand miles. This was a major change, as Ewing explains Volkswagen thus no longer promised that the system could work long enough through the full circle between regular oil changes. Volkswagen also updated the software so that the cars would use more urea to better catalyze NOx, and reduce the difference between road emissions and laboratory emissions, which would still not bring the true road emissions within the standards. In this way, Volkswagen tinkered and improved its cheating device, even when they already knew that in time it would be discovered. It continued to sell large volumes of cars that were not as clean as they claimed (

Ewing 2017, p. 181).

Meanwhile, Volkswagen stalled and obstructed the CARB investigation into why there was a difference between the lab and road emissions. CARB at that time did not expect deliberate wrongdoing; they simply just tried to understand the cause and fix it. Volkswagen, however, was not really cooperative. As Ewing details: “The Volkswagen executives responsible for dealing with regulators gave answers that the regulators regarded as evasive, non-sensical, or dismissive. CARB’s testing was wrong, Volkswagen complained. The outside air temperature threw off the results. The routes followed [during the road tests] were inconsistent” (

Ewing 2017, p. 182). As this process went on and started to consume more and more CARB time, Volkswagen informed the regulators that they would do a recall to update the software and “optimize” the emission control equipment in all clean diesels it had sold (

Ewing 2017, p. 182). This was no admission of what actually had been happening, and instead gave the false promise that this would bring emissions within standards. Volkswagen also lied about the recall to customers and dealers, claiming that the recall was necessary to deal with a malfunction light defect (

Ewing 2017, p. 183).

Most shocking, Volkswagen in fact used the recall to improve the effectiveness of the cheating software. It improved the car’s ability to detect when it was being tested in the lab, switching on its fully effective emissions controls only when the steering wheel was stationary for a longer time while driving, as it would only be at the lab (

Ewing 2017, p. 183). The regulators responded with further and more stringent tests, and asked questions about other models with larger engines, which by then had also had defeat devices. And Volkswagen, even though by then it knew for sure that the game would soon be up, just continued its stonewalling and deceit.

Volkswagen executives became especially worried when they learned CARB was going to test an older clean diesel model. One internal email stated: “If the Gen I goes on to the roller at CARB then we’ll have nothing to laugh about” (

Ewing 2017, p. 193). CARB also demanded that Volkswagen show them the software that controlled the urea injections in the new 2016 cars.

Volkswagen continued its cover-up all the way until it could no longer do so. It was forced to come clean and admit the existence of the defeat device only after CARB threatened that if Volkswagen failed to show them the software, it would refuse to approve the 2016 models onto the Californian market, which would keep them from the whole U.S. market (

Ewing 2017, pp. 192–93). At first Volkswagen still would not admit to using the cheating software. A legal memo had estimated that the risk Volkswagen was running was still manageable. By now, Volkswagen had stalled and obstructed the CARB investigation for over a year. The company provided CARB a thick binder with the latest technical information, which seemed to indicate that VW had finally solved the problem. When CARB looked deeper into the information provided it found it was “all nonsense” (

Ewing 2017, p. 197). The only explanation, CARB also now saw was that VW had been using a defeat device all along. It was August 2015, and CARB had still not approved the 2016 VW models, which were waiting in port to enter the market. And CARB was still waiting for the software information it had requested, and further it asked VW for a 2016 model car for new testing. This proved to be the final straw, as Volkswagen eager to get its cars on the US market ready for 2016, finally confessed that its cars had had defeat devices (

Ewing 2017, pp. 197–98).

Volkswagen later claimed that it had failed to disclose the issue earlier because executives had not known about this. According to VW, it was only a small group of technicians who knew about the device. Top executives, Volkswagen claimed, had only learned about “conclusive proof” for the defeat device just before its confession to CARB (

Ewing 2017, p. 200). And thus, Volkswagen moved from stonewalling, deceit and denial, to shifting blame downwards in the company. VW’s new CEO, Müller, has maintained this discourse since then. Stating, in an interview with a German newspaper: “Based on what I know today only a few employees were involved.” Defending his former CEO Winterkorn, he said: “Do you really think that a chief executive had time for the inner functioning of engine software?” (

Ewing 2017, p. 216). Volkswagen leadership maintained this line, even when former CEO and grand architect of the Volkswagen growth strategy in the 1990s and early 2000s, Piëch came forward to claim that he had learned of the emissions problems in February 2015 while still chairing the board and that at the time Winterkorn had told them that there was nothing to worry about (

Ewing 2017, p. 271).

Volkswagen ended up suspending several dozens of its midlevel engineers and executives, including the head of quality control and a member of the Audi management board (

Ewing 2017, pp. 223, 256). Yet VW never addressed the more than a year period VW had tried to stall, obstruct, and deceive the ongoing investigations. Nor did VW seriously explore that the scandal involved a larger plot involving the highest level executives (

Ewing 2017, p. 223). The company’s supervisory board never took any disciplinary action against the company’s top level executives who served on the management board (

Ewing 2017, p. 256). And the car maker still paid out

$33.9 million dollar in top executive bonuses, even when it reported a record

$1.6 billion loss. This meant that even Winterkorn, who had been CEO during most of the saga, received a total compensation package of

$8 million in 2015, and that was for ten months only, as he had retired in October (

Ewing 2017, pp. 242–43). Volkswagen employees ended up paying the brunt of the costs, as in November 2016 the company announced it would cut 14,000 jobs (

Ewing 2017, p. 258).

Volkswagen also tried to downplay that it had broken the law. VW CEO Müller tried to paint what had happened in a much more positive light. In an interview, he stated: “It was a technical problem…An ethical problem? I cannot understand why you [the reporter] say that.” As he explained, they did not have: “the right interpretation of the American law…We didn’t lie. We didn’t understand the question first. And then we worked since 2014 to solve the problem” (

Glinton 2016). Meanwhile in Europe, Volkswagen took a directly confrontational legal approach, claiming that what had happened was not against the law there. A Volkswagen representative called to share the company’s response to the scandal to the UK House of Commons Transport Select Committee, called the software a “drive trace” and said that it “was not defined as a defeat device in Europe.” When members pressed that this was incorrect, the company’s representative simply stated that “in the understanding of the Volkswagen Group it is not a defeat device” (

Ewing 2017, pp. 232–33).

The crassest deflection attempt of all was when Volkswagen tried to deny that it had damaged public health. It simply tried to refute that NOx was harmful. In a statement issued in late 2016 VW said: “A reliable determination of morbidity or even fatalities for certain demographic groups based on our level of knowledge is not possible from a scientific point of view” (

Reuters 2016). In 2018, a German newspaper reported that Volkswagen had tried to back up its claims by exposing monkeys for hours to exhausts from the “clean diesel” engine of a 2016 Beetle, and compare them with monkeys exposed to the fumes from a 1997 heavy duty gasoline Ford F250 pick-up truck. Volkswagen had kept the study quiet, not in the least because the results had shown that the old Ford was less damaging to the monkeys than the state of the art Beetle. Several studies have now proven that the health effects are real. One of the most recent studies by MIT scientists, published in Environmental Research Letters, estimates that the extra NOx emissions emitted because of VW’s cheating will cost 1200 premature deaths in Europe, each dying a decade early (

Chossière et al. 2017).

In conclusion, all three companies clearly tried to deflect blame, doing so each time they had a scandal and when the most major scandals erupted over the last years. Blame deflection had become a regular practice in all three companies, and with it came values that were harmful for compliance. The blame deflection resulted in several toxic cultural norms and processes. Again, we shall discuss these here referring back to

Table 2 for the norms and processes and

Table 1 for the levels these played out in within the cultures.

The first toxic process we see here is neutralization. By shifting away blame from the company and its executives to sub-contractors and lower level workers, the company neutralized the culpability of the corporation and its leaders, and it failed to take responsibility itself that could foster organizational learning from the wrongdoing that would help to prevent it (

Homsma et al. 2009). This “denial of responsibility” can enable further rule breaking, as corporate executives rationalize and legitimize illegal practices in their firm as they reiterate time and again that it was not the corporation, that this is not who we are, or that it was just a few bad apples (cf.

Maruna and Copes 2005;

Minor 1981;

Sykes and Matza 1957). This mentality prevents the corporation from developing normative values, from taking responsibility for mistakes, and from acknowledging that what happened was unacceptable and must be prevented at all cost. BP and Volkswagen also denied the damaging impact of the rule violations, claiming that the oil spill was but a drop in the ocean and that the NOx emissions were not damaging to health. This “denial of injury” is another classic neutralization technique that directly enables continued offending behavior, as it allows future rule breakers to tell themselves that this is not as bad as what people make it out to be (

Maruna and Copes 2005;

Minor 1981;

Sykes and Matza 1957). In VW’s case, a different neutralization technique not discussed in the original criminological literature can be identified—a legal neutralization that occurred when the company claimed that its actions were not against the law. Again, this claim enabled offending and damaging behavior by appealing to the letter of the law to justify behavior was so clearly against its spirit.

The deflection of blame further strengthened the normalization of deviancy (cf.

Vaughan 1989,

1997). As blame is pushed downward and outward, discipline for higher level leaders remains lagging. In all three cases, stronger internal action, to the extent that it did happen, only came after outside pressure. Wells Fargo, for instance, sought to claw back bonuses after relentless critique that it had not done so. And through this, the deflection of blame practices further enabled rule breaking and normalized deviancy, as it failed to establish a clear norm that offending behavior is not tolerated.

The deflection of blame does not play out in a vacuum, but exists as a response to the broader economic and legal forces companies operate in and thus interacts with the responses to strain these companies are under (

Agnew 1992,

2001;

Agnew et al. 2009;

Simpson and Koper 1997). Blame deflection is not just part of the toxic culture at these three companies, but a much more common practice for firms that are trying to repair their image in the aftermath of scandals (

Benoit 2014). Blame deflection is also a direct response against legal forms of strain that come with criminal and civil liability. With the push for punishment and compensation—that is highly justified and also necessary to end impunity—also comes the risk of steering companies towards blame deflection. Blame deflection undermines the value of taking true responsibility and setting true internal norms and, as is evident in all three cases, acknowledging that such behavior is not acceptable. And, in turn, the push to punish the highest levels of corporate leadership may instead lead to a shifting of blame onto those individual leaders, without truly addressing the toxic corporate culture.

Here we see that these toxic processes started most clearly at the level of values in the form of explicit shared values that came with statements from the companies. But when companies respond to a longer series of scandals, as BP so clearly did, employees will begin to expect that their company deflects blame and does not take responsibility, and at some point this is can become a hidden assumption, and thus become more deeply embedded in the corporate culture, reaching the levels of hidden assumptions.

3.5. Mixed Messages and Corporate Dissonance

None of the companies openly claimed that their actions of defrauding customers, cheating on emissions, or chafing of safety standards were good or intentional. All three companies ostensibly had ethical standards, positive corporate messages, and even branding and commercials that were highly aligned with compliance and the goals of the law. The expressed values all three companies promoted formally, however, were in stark contrast with their actual practices and the values the public observed through these practices. As New York Federal Reserve President William Dudley said about Wells Fargo: “There was a serious mismatch between the values Wells Fargo espoused and the incentives that Wells Fargo employed” (

Puzzanghera 2017).

BP and Volkswagen provide the most detailed information about such “corporate dissonance” between preached values and practiced norms (

Ewing 2017). During the 1990s, both companies had made environmental protection part of their core image. Volkswagen started with the development of the turbo charged direct injection diesel engine. The new technology that VW brought to market in 1989 made the fuel-efficient diesel cleaner and less noisy, thus making diesel a palatable option for small and midsized cars. The company dubbed this technology—associated with power and fuel efficiency—“TDI”, and made it a core part of its brand (

Ewing 2017). In the 2000s, VW went a step further and developed “clean diesel,” which was promoted as an equally clean, fuel efficient, but more powerful and economical alternative to the hybrid models Toyota and other companies started to advertise. To promote the new technology, VW commissioned several new commercials. One series of commercial featured three old ladies driving in a VW clean diesel car and discussing “old wives tales” about diesel. Each commercial ended by suggesting that Volkswagen’s new clean diesel led to less noise, more power, and, most importantly, clean exhaust emissions . In one commercial, one of the elderly women placed her white handkerchief behind the exhaust just to show how clean the diesel was (

Ewing 2017, p. 147). Another commercial, played during the break of the American Super Bowl, depicted environmental police busting people for minor issues, from not separating their trash to using the wrong lightbulbs. In the final scene, a police checkpoint verified if cars were environmentally friendly enough. A man driving a Volkswagen is waved through by a friendly cop who says: “Volkswagen Clean Diesel. Sir, you are good to go.”

4Volkswagen’s green branding and advertising stood in stark contrast to its actual practices, which were anything but clean. For those who had been in some way involved in the defeat device, the contrast between the public image of Volkswagen as environmentally friendly and the practice they knew was absolute.

This corporate dissonance between what was stated and what was practiced became even larger the moment the California regulators began to look into the discrepancy in VW lab and road test results. For over a year, VW’s official stance was that the testing had problems and that it was not accurate, but not that the company had been cheating. As the pressure escalated, VW executives must have come to know of the defeat device, and the more they strategized how to continue to deflect blame, the more the discrepancy grew between what VW said and what happened in the company. This is especially clear with the recall VW organized, formally letting regulators know it was to fix the emissions problem, and telling dealers that it was to fix a safety light, while in fact it was a deliberate attempt to make the cheating even better (

Ewing 2017, pp. 182–83). What employees and executives learned at VW was that what the company said, whether in advertisements, against regulators, and against the public, had little to no relation to what it practiced. This continued after even VW admitted it had a defeat device, as it tried to argue that it had not broken EU law, that the emissions were not toxic, that leadership had not been involved, and that this was not a problem in the culture, but just the work of a small group of bad apples. All public statements, and all statements VW executives knew or came to know, were not true.

BP had a similar disconnect between its corporate communication and its actual practices. While BP cut costs and focused on risky exploration—resulting in a long stream of spills, hazards, and accidents—it sought to be seen as an environmentally responsible company. In 1997, BP CEO Browne announced that the link between greenhouse gases and global climate change was real and could no longer be ignored. He announced that BP would invest in alternative energy operations and research. A few years after, the company dropped its longer name, “British Petroleum”, and simply became BP, but with a new slogan “Beyond Petrol.” Also it launched a new shield logo of an upbeat yellow sun, signifying solar energy, surrounded by “what looked like leaves” (

Steffy 2010). In the following years, and even after the Gulf disaster, the company repeatedly issued statements proclaiming that it was strongly committed to the environment. Yet this was in stark contrast not only to the company’s continued exploration operations, which were trying to get as much fossil fuels as possible out of the ground and sold to consumers to burn into the air (

Frey 2002), but also to its appalling disregard for safety and the oil spills it could, and indeed would, cause. BP’s new imagine was not welcomed everywhere. Greenpeace said that a more fitting logo for the company would be “a miserable polar bear on an icecap shrinking because of global warming” (

Frey 2002). And the environmental NGO honored CEO John Browne for the “Best Impression of an Environmentalist” (

Frey 2002).

BP also claimed that it cared about safety—especially at times following major incidents. In 2000, for instance, BP’s Grangemouth refinery in Scotland had three separate accidents, all in one week. As a result, BP received a criminal fine of £750,000. The investigation found that BP’s quest for cost reductions had created the safety hazards, and that its fractured management structure had undermined a safety prevention strategy (

Steffy 2010, p. 62). BP’s response was to state that it had gotten the message and that it had “shared the lessons it learned with its 11 other refineries in the world” (

Steffy 2010, p. 62). While in fact, BP did not change its practices of cost cutting, ignoring safety concerns, and deflecting blame, even on those who had been hurt themselves in accidents BP had caused. With each new incident, BP claimed improvement and change, yet real change did not happen. Instead, BP’s internal communication on safety focused on minor, low-cost matters. As one former exploration engineer recalls, the company and its executives “focused so heavily on the easy part of safety, holding the hand rails, spending hours discussing the merits of reverse parking and the dangers of not having a lid on a coffee cup, but were less enthusiastic about the hard stuff, investing in and maintaining their complex facilities” (

Steffy 2010, p. 57).

Real change did not even come when BP’s new CEO, Hayward, took over from Browne. Hayward promised to make safety a priority; he promised a “new BP.” Hayward promised a less complex organization with more transparency and accountability. He promised to hire 1000 engineers and improve safety in all of BP’s global operations (

Steffy 2010, p. 151). However, Hayward never took full accountability for how BP’s cost cutting had led to the major accidents that had occurred before his tenure. He even resumed cost reductions, cutting

$4 billion in 2009 in response to the 2008 crisis (

Steffy 2010, p. 162). He was also unable to convince his executives that safety should become the priority, in part because English executives saw this as an American problem, and in part because he was not as popular as his predecessor Browne (

Steffy 2010, p. 152).

Under Hayward’s tenure, BP would not change its core safety problems. As Steffy summarizes: “Its management structure was still convoluted, accountability was hard to find, decisions were made by committee, and cost cutting and financial performance continued to overshadow operations” (

Steffy 2010, p. 160). A good illustration of this is a 2009 OSHA inspection at the Texas City refinery. The inspection resulted in one of the highest fines in OSHA history—

$87 million. OSHA fined BP especially for hazards that had been identified before, but that BP had failed to fix. During another inspection in the BP refinery in Toledo, Ohio, OSHA found that BP had only done the repairs it had specifically mentioned, while leaving similar problems in other part of its operation unaddressed. As Steffy summarizes: “Hayward’s ‘laser’ was so precise that it was able to separate the letter of the rules from the intent” (

Steffy 2010, p. 162). The more Hayward promised, as new CEO in the aftermath of the Texas refinery, to change BP, the more he undermined his own credibility and thus his ability to institute reform when practices on the ground did not actually change.

Here, again, we can analyze what this means for the corporate culture. Drawing on

Table 2, we see that the most important type of toxic norm at play here is the disconnect between what the companies express as their values and what their actual day to day practice has been. A disconnect between the expressed values in support of compliance (safety, environmental protection, consumer protection) and practices that run directly counter to it will damage corporate compliance. When employees and executives hear one thing in corporate messaging, but see the complete opposite in everyday practices, they will not be convinced that their company and leaders are truly committed. This will either undermine the authority and credibility of corporate leadership within the company, or it will mean that lower level executives and employees learn that these messages are just for show, just to demonstrate commitment, but that what is truly expected is the opposite. This is very similar to findings in psychology that placing prohibition signs in environments where they are clearly being violated will create more offending (

Keizer et al. 2011).

The damage in this case, however, can get worse. Once corporate employees and executives begin to doubt their leaders, achieving reform in corporate values and practices becomes very difficult. When CEOs preach improvement and preach that what has happened is not in line with the corporate culture year after year (or incident after incident), how will employees know when they truly mean it and when they should truly change what they do and think is right? Consequently, the corporate cognitive dissonance derived from conflicting corporate messages and practices can be viewed as the ultimate toxic element in a corporate culture—one that can obstruct any attempt to detoxify the culture.

{kind=link}