Women’s Role in the Accounting Profession: A Comparative Study between Italy and Romania

Abstract

:1. Introduction

2. Theoretical Framework

2.1. Gender Stratification Theory

2.2. Institutional Theory

2.3. Gendered Nature of the Accounting Profession

3. Methodology

3.1. Country Selection

3.2. Method Selection

3.3. Data Selection

- data from the literature and accountancy national bodies archives concerning the historiography of the accounting profession in both countries

- data on cultural factors, using Hofstede six dimensions (Hofstede et al. 2010)

- data on gender diversity useful to introduce the context of comparative gender analysis, have been extracted from the Report on equality between women and men in Europe (EU 2017), relative to the following features: gender segregation in occupations (all economic sectors), the proportion of women on boards of the largest publicly listed companies; the percentage of women in the single/lower houses of the national/federal parliaments and federal governments. The index “gender segregation” in occupations and economic sectors reflects the proportion of the employed population that would need to change occupation/sector to bring about an even distribution of men and women across occupations or sectors. The index varies between 0 (no segregation) and 50 (complete segregation).

- the AFECA’s (Association des Formations Européennes a la Comptabilité et l’Audit) survey. AFECA represent a European benchmark on valorising women’s capital in the accountancy profession. The study conducted by AFECA aimed to obtain an overview of progress within the 24 institutes from 22 countries concerning the valorisation of women capital and provoke exchanges and the sharing of best practices (AFECA and FEE 2016). This benchmark, useful for the assessment and comparison of the respective situations, was intended to generate dynamic movement (without stigmatisation and making value-based judgments) and allow each institute member (FEE or EFAA) to learn some lessons for their strategies in the field of the development and balance of human capital. Moreover, the key findings of the survey contribute to the reinforcement of collective action for parity and professional balance. Both countries were included in the international AFECA’s survey, thus allowing a comparison based on a similar dataset.

3.4. Research Design

4. Results

4.1. Accounting Profession and Women Accountants in Italy and Romania: The Historical and Institutional Framework

4.1.1. Women in the Accounting Profession in Italy between Past and Present Times

4.1.2. The Accounting Profession from Romania—Key Highlights

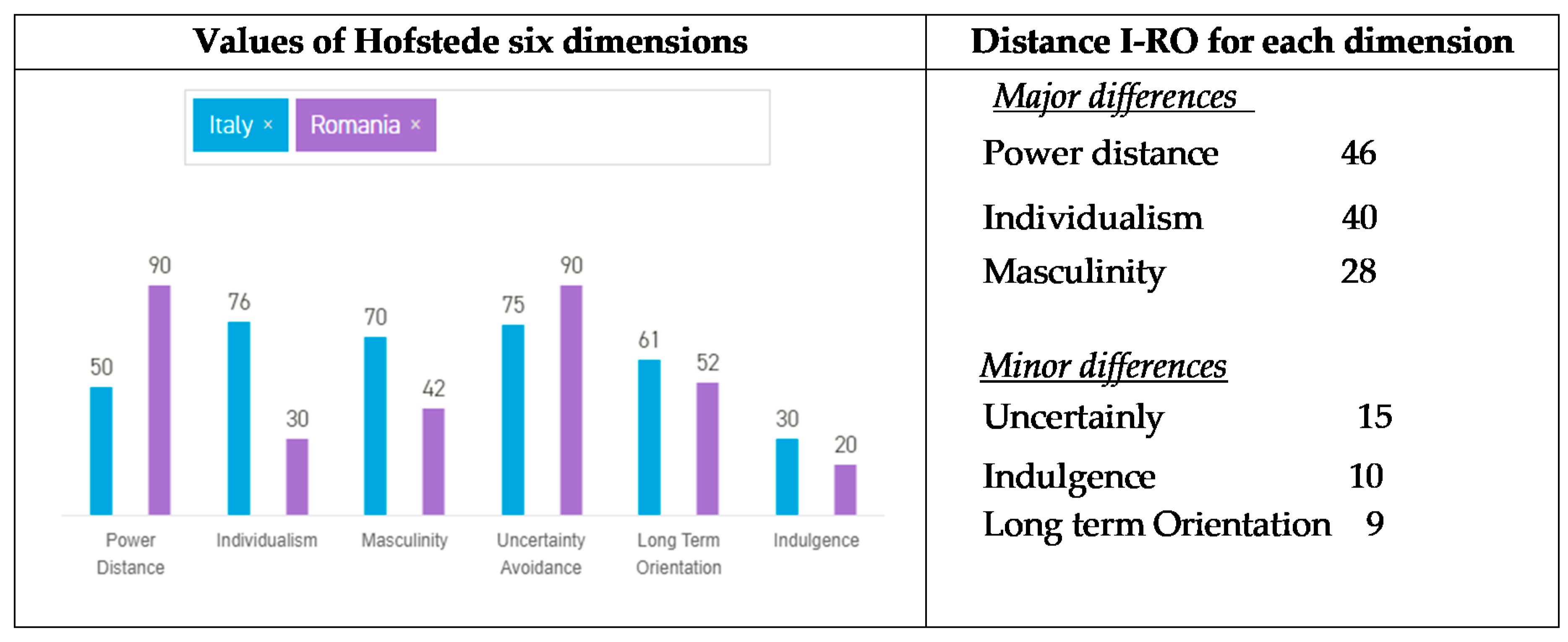

4.2. Comparative Results Concerning Cultural Factors in Italy and Romania

4.3. General Context of the Gender Comparative Study

4.4. Romania–Italy Country Level Comparison Based on AFECA Study

5. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Adapa, Sujana, Alison Sheridan, and Jennifer Rindfleish. 2015. Career enablers for women in regional and metropolitan accounting SMEs. Australasian Journal of Regional Studies 21: 178–201. Available online: http://www.anzrsai.org/publications/ajrs/ (accessed on 20 December 2018).

- Adler, Paul S., Seok-Woo Kwon, and Charles Heckscher. 2008. Professional Work: The Emergence of Collaborative Community. Organization Science 19: 359–76. [Google Scholar] [CrossRef]

- Association des Femmes diplômées d’Expertise Comptable Administrateurs Gender (AAECA), and Fédération des Experts Comptables Européens (FEE). 2016. Diversity in the European Accountancy Profession. An AFECA Study with the Support of FEE. Paris: AFECA. [Google Scholar]

- Albu, Nadia, Catalin Albu, Maria Gĭrbină, and Maria Sandu. 2011. The Implications of Corporate Social Responsibility on the Accounting Profession: The Case of Romania. Amfiteatru Economic Journal, The Bucharest University of Economic Studies, Bucharest 13: 221–34. [Google Scholar]

- Anderson, John C., Eric N. Johnson, and Philip MJ Reckers. 1994. Perceived effects of gender, family structure and physical appearence on carreer progression in public accounting: A research note. Accounting, Organization and Society 19: 483–91. [Google Scholar] [CrossRef]

- Anderson-Gough, Fiona, Christopher Grey, and Keith Robson. 2002. Accounting Professionals and the Accounting Profession: Linking Conduct and Context. Accounting and Business Research 32: 41–56. [Google Scholar] [CrossRef]

- Anderson-Gough, Fiona, Christopher Grey, and Keith Robson. 2005. “Helping them to forget”: The organizational embedding of gender relations in public audit firms. Accounting Organizations and Society 30: 469–90. [Google Scholar] [CrossRef]

- Bailey, Sarah Frances, Elora C. Voyles, Lisa Finkelstein, and Kristina Matarazzo. 2016. Who is your ideal mentor? An exploratory study of mentor prototypes. Career Development International 21: 160–75. [Google Scholar] [CrossRef]

- Baldarelli, Maria Gabriella, Mara Del Baldo, and Stefania Vignini. 2016. Pink accounting in Italy: Cultural perspectives over discrimination and/or lack of interest. Meditari Accountancy Research 24: 269–92. [Google Scholar] [CrossRef]

- Barbu, Elena, Nicoleta Farcane, and Adina Popa. 2010. Looking for an Accounting Identity: The Case of Romania during the 20th Century. Available online: http://hal. archives-ouvertes.fr/docs/00/53/47/41/PDF/cr_2010_03_E2.pdf (accessed on 6 November 2018).

- Baxter, Janeen, and Erik Olin Wright. 2000. The glass Ceiling Hypothesis: A Comparative Study of the United States, Sweden, and Australia. Gender and Society 14: 275–94. [Google Scholar] [CrossRef]

- Bell, Myrtle P., Mary E. McLaughlin, and Jennifer M. Sequeira. 2002. Discrimination, harassment, and the glass ceiling: Women executives as change agents. Journal of Business Ethics 37: 65–76. [Google Scholar] [CrossRef]

- Biographical Dictionary of Chartered Accountants. 1967. Dizionario Biografico dei dottori commercialisti. Roma: CNDCEC. [Google Scholar]

- Blackburn, Robert M., Jude Browne, Bradley Brooks, and Jennifer Jarman. 2002. Explaining gender segregation. British Journal of Sociology 53: 513–36. [Google Scholar] [CrossRef] [PubMed]

- Bloom, Robert, and M. Ahmed Naciri. 1989. Accounting standard setting and culture: A comparative analysis of the United States, Canada, England, West Germany, Australia, New Zealand, Sweden, Japan, and Switzerland. The International Journal of Accounting 24: 70–97. [Google Scholar]

- Blumberg, Rae Lesser. 1984. A general theory of gender stratification. Sociological Theory 2: 23–101. [Google Scholar] [CrossRef]

- Boxenbaum, Eva. 2006. Lost in translation? The making of Danish diversity management. American Behavioral Scientist 49: 939–48. [Google Scholar] [CrossRef]

- Branciforte, Laura, and Rossana Tazzioli. 2001. La presenza delle donne nella matematica e nel suo insegnamento. Catania: Società di storia patria per la Sicilia Orientale. [Google Scholar]

- Brinton, Mary C. 1998. The Social-Institutional Bases of Gender Stratification: Japan as an Illustrative Case. American Journal of Sociology 94: 300–34. [Google Scholar] [CrossRef]

- Broadbent, Jane. 1998. The gendered nature of ‘accounting logic’: Pointers to an accounting that encompasses multiple values. Critical Perspectives on Accounting 9: 267–97. [Google Scholar] [CrossRef]

- Broadbent, Jane. 2016. A gender agenda. Meditari Accountancy Research 24: 169–81. [Google Scholar] [CrossRef]

- Broadbent, Jane, and Linda Kirkham. 2008. Glass ceilings, glass cliffs or new worlds?: Revisiting gender and accounting. Accounting and Accountability Journal 21: 465–73. [Google Scholar] [CrossRef]

- Bryant, Lydia L. 2010. What role does the ‘Glass ceiling’ play for women in the accounting? The York Scholar 1: 2–13. [Google Scholar]

- Bunget, Ovidiu-Constantin, Nicoleta Farcane, Alin-Constantin Dumitrescu, and Adina Popa. 2009. The Accounting Profession and Professions in Romania. Available online: https://mpra.ub.uni-muenchen.de/id/eprint/18408 (accessed on 25 January 2018).

- Burke, Ronald J., and Carol A. McKeen. 1990. Mentoring in organizations: Implications for women. Journal of Business Ethics 9: 317–32. [Google Scholar] [CrossRef]

- Burrell, Gibson. 1987. No Accounting for Sexuality. Accounting, Organizations and Society 12: 89–101. [Google Scholar] [CrossRef]

- Cantagalli, Alessandra. 1996. La professione del dottore commercialista. In Storia d’Italia. Annali, 10: I professionisti. Edited by Maria Malatesta. Torino: Einaudi, pp. 225–58. [Google Scholar]

- Cantagalli, A. 2006. Il Ragioniere Commercialista: Una storia lunga un secolo (1906–2006). I ragionieri commercialisti in Italia. 100 anni della nostra storia.Summa 23: 223. [Google Scholar]

- Carnegie, Garry D., and Christopher J. Napier. 2010. Traditional accountants and business professionals: Portraying the accounting profession after Enron. Accounting, Organization and Society 35: 360–76. [Google Scholar] [CrossRef]

- Christensen, Hans B., Edward Lee, Martin Walker, and Cheng Zeng. 2015. Incentives or Standards: What Determines Accounting Quality Changes around IFRS Adoption? European Accounting Review 24: 31–61. [Google Scholar] [CrossRef] [Green Version]

- Ciancanelli, Penelope, Sonja Gallhofer, Christopher Humphrey, and Linda M. Kirkham. 1990. Gender and Accountancy: Some Evidence from the UK. Critical Perspectives on Accounting 1: 117–44. [Google Scholar] [CrossRef]

- Consiglio Nazionale dei Dottori Commercialisti e degli Esperti Contabili (CNDCEC). 2016. Gender Report, CNDCEC Bilancio di genere del Consiglio Nazionale dei Dottori Commercialisti e degli Esperti Contabili, Marzo 2016. A cura della Commissione Parità di Genere—Area Parità di Genere. Rome: CNDCEC. [Google Scholar]

- Collins, Randall. 1990. Conflict theory and the advance of macro-historical sociology. In Frontiers of Social Theory. Edited by George Ritzer. New York: Columbia University Press, pp. 68–87. [Google Scholar]

- Collins, Randall, Janet Saltzman Chafetz, Rae Lesser Blumberg, Scott Coltrane, and Jonathan H. Turner. 1993. Toward an integrated theory of gender stratification. Sociological Perspectives 36: 185–216. [Google Scholar] [CrossRef]

- Cooper, David J., and Keith Robson. 2006. Accounting, professions and regulation: Locating the site of professionalization. Accounting, Organizations and Society 31: 415–44. [Google Scholar] [CrossRef]

- Coronella, Stefano, ed. 2014. L’ingresso delle donne nel mondo professionale. In Storia della Ragioneria Italiana. Epoche, uomini e idee. Milano: F. Angeli, pp. 349–51. [Google Scholar]

- Cotter, David A., Joan M. Hermsen, Seth Ovadia, and Reeve Vanneman. 2001. The glass ceiling effect. Social Forces 80: 655–81. [Google Scholar] [CrossRef]

- Dambrin, Claire, and Caroline Lambert. 2006. La Question du Genre en Compatibilité. Analyses Theoriques et Metodologiques. Les Cahiers de Recherche 862. Paris: HEC, pp. 1–26. [Google Scholar]

- Dambrin, Claire, and Caroline Lambert. 2008. Mothering or auditing? The case of two Big four in France. Accounting, Auditing & Accountability Journal 21: 474–506. [Google Scholar]

- Dambrin, Claire, and Caroline Lambert. 2012. Who is she and who are we? A reflexive journey in research into the rarity of women in the highest ranks of accountancy. Critical Perspectives on Accounting 23: 1–16. [Google Scholar] [CrossRef]

- De Rossi, Roberta. 2007. Le donne di Cà Foscari, Percorsi di emancipazione, Materiali di studi. Venezia: Università Cà Foscari. [Google Scholar]

- De Vivo, Francesco, and Giovanni Genovesi, eds. 1986. Cento anni di Università l’istruzione superiore in Italia dall’Unità ai nostri giorni. Napoli: Esi, Collana CIRSE, Frontiere dell’Educazione. [Google Scholar]

- Dreher, George F., and Ronald A. Ash. 1990. A comparative study of mentoring among men and women in managerial, professional, and technical positions. Journal of Applied Psychology 75: 539–46. [Google Scholar] [CrossRef]

- Dubose, Renalia. 2017. Compliance Requires Inspection: The Failure of Gender Equal Pay Efforts in the United States. Mercer Law Review 68: 445–60. [Google Scholar]

- European Commission (EC). 2014. Gender Equality in Horizon 2020, 2014, Luxembourg. Available online: https://ec.europa.eu/research/swafs/pdf/pub_gender_equality/she_figures_2015-final.pdf (accessed on 8 November 2018).

- European Commission (EC). 2015a. European Commission and the European External Action Service (EEAS) Joint Staff Working Document on “Gender Equality and Women’s Empowerment: Transforming the lives of Girls and Women through EU External Relations 2016–2020 Brussels, 21.9.2015 SWD (2015) 182 Final. Available online: https://ec.europa.eu/europeaid/joint-staff-working-document-gender-equality-andwomens-empowerment-transforming-lives-girls-and_en (accessed on 2 February 2018).

- European Commission (EC). 2015b. European Commission: Fact Sheet—Sustainable Development Goals and the Agenda 2030, Brussels, 25 September 2015. Available online: http://europa.eu/rapid/press-release_MEMO-15-5709_en.htm (accessed on 2 February 2018).

- European Commission (EC). 2016. She Figures 2015, Publication Office of the European Union. Luxembourg: European Union. [Google Scholar]

- Grigsby, Ellen. 2008. Analyzing Politics. Belmont: Cengage Learning, pp. 108–9, 112, 347. ISBN 978-0-495-50112-1. [Google Scholar]

- European Union. 2017. European Commission Report on Equality between Women and Men in the EU Justice and Consumers. Belgium: European Union, p. 68. ISSN 2443-5228. [Google Scholar] [CrossRef]

- European Economic and Social Committee. 2014. The State of Liberal Professions Concerning Their Functions and Relevance to European Civil Society. Available online: https://publications.europa.eu/fr/publication-detail/-/publication/f106f20b-36f7-4425-8e07-33db339da6e6 (accessed on 10 November 2018).

- Farcas, Teodora Viorica, and Adriana Tiron-Tudor. 2016. An overlook into the Accounting History Evolution from a Romanian point of view. A Literature Review. Economia Aziendale Online 7: 71–84. [Google Scholar]

- FNC (Fondazione Nazionale dei Commercialisti). 2015. The Profession of Commercialista in Italy, July 2015 ed. Rome: FNC. [Google Scholar]

- FNC (Fondazione Nazionale dei Commercialisti). 2016. Report on the Register of Chartered Accountants and Accounting Experts from the National Accountants Foundation. Rome: FNC. [Google Scholar]

- FNC (Fondazione Nazionale dei Commercialisti), ed. 2017. Consiglio Nazionale dei Dottori Commercialisti e degli Esperti Contabili, Rapporto 2017 sull’Albo dei Dottori Commercialisti e degli Esperti Contabili, a cura di Di Nardo, T., Giugno 2017. Roma: FNC. [Google Scholar]

- Fondazione Nazionale dei Commercialisti (FNC), ed. 2018. Rapporto 2018 Sull’albo dei DottoriCommercialisti e degli Esperti Contabili. Sintesi dei dati, a cura di Di Nardo, T., Giugno 2018. Roma: FNC. [Google Scholar]

- Fogarty, Timothy J., Larry M. Parker, and Thomas Robinson. 1998. Where the rubber meets the road: Performance evaluation and gender in large public accounting organizations. Women in Management Review 13: 299–311. [Google Scholar] [CrossRef]

- Frattini, Romana. 2011. Le donne all’Università di Cà Foscari un percorso tormentato: Dati e problemi. In Nominare per esistere: Nomi e cognomi. Edited by Giuliana Glusti. Venezia: Libreria Editrice Cafoscarina, pp. 171–82. [Google Scholar]

- Gallhofer, Sonja. 1998. The silence of mainstream feminist accounting research. Critical Perspectives on Accounting 9: 355–75. [Google Scholar] [CrossRef]

- Gambusera, E. 1908. Le donne possono essere iscritti nei Collegi legali della Ragioneria? Rivista dei Ragionieri 1: 93. [Google Scholar]

- Gammie, Bob, and Elizabeth Gammie. 1997. Career progression in accountancy. The role of personal and situational factors. Women in Management Review 12: 167–73. [Google Scholar] [CrossRef]

- Gauthier, Lane Roy. 2000. The role of questioning: Beyond comprehension’s front door. Reading Horizons: A Journal of Literacy and Language Arts 40: 239–52. [Google Scholar]

- Goedegebuure, Leo, and Frans van Vught. 1996. Comparative higher education studies: The perspective from the policy sciences. Higher Education 32: 371–94. [Google Scholar] [CrossRef]

- Goodman, Jodi S., Dail L. Fields, and Terry C. Blum. 2003. Cracks in the Glass Ceiling. In What Kinds of Organizations do Women Make it to the Top? Group and Organization Management 28: 475–501. [Google Scholar] [CrossRef]

- Grey, Christopher. 1998. On being a professional in a ‘Big Six’ firm. Accounting, Organizations and Society 23: 569–87. [Google Scholar] [CrossRef]

- Hlaciuc, Elena, and Veronica Deac. 2014. An Overview of Past and Present Romanian Accounting. Procedia Economics and Finance 15: 909–15. [Google Scholar] [CrossRef]

- Hans, Joas, and Wolfgang Knöbl, eds. 2011. Conflict sociology and conflict theory. In Social Theory: Twenty Introductory Lectures. Cambridge: Cambridge University Press, pp. 174–98. [Google Scholar]

- Haynes, Kathryn. 2008a. (Re)figuring accounting and maternal bodies: The gendered embodiment of accounting professionals. Accounting, Organizations and Society 33: 328–48. [Google Scholar] [CrossRef]

- Haynes, Kathryn. 2008b. Moving the gender agenda or stirring chicken’s entrails? Where next for feminist methodologies in accounting? Accounting, Auditing and Accountability Journal 21: 539–55. [Google Scholar] [CrossRef]

- Haynes, Kathryn. 2017. Accounting as gendering and gendered: A review of 25 years of critical accounting research on gender. Critical Perspectives on Accounting 43: 110–24. [Google Scholar] [CrossRef]

- Hines, Ruth D. 1992. Accounting: Filling the negative space. Accounting Organizations and Society 18: 313–41. [Google Scholar] [CrossRef]

- Hofstede, Geert, G. J. Hofstede, and M. Minkov. 2010. Cultures and Organizations: Software of the Mind: Intercultural Cooperation and Its Importance for Survival, 3rd ed. New York and London: McGraw-Hill. [Google Scholar]

- Hopwood, Anthony G. 1987. Accounting and Gender: An Introduction. Accounting Organization and Society 12: 65–69. [Google Scholar] [CrossRef]

- Irvine, Helen, Lee Moerman, and Kathy Rudkin. 2010. A green drought: The challenge of mentoring for Australian accounting academics. Accounting Research Journal 23: 146–71. [Google Scholar] [CrossRef]

- Istrate, Costel. 2012. Gender issues in romanian accounting profession. Review of Economics Business Studies 5: 21–45. [Google Scholar]

- Italian Ministry of Public Education—Ministero della Pubblica Istruzione. 1878. Programmi, osservazioni e memorie sullo insegnamento della Ragioneria e Computisteria negli Istituti tecnici del Regno con l’aggiunta di un elenco bibliografico di Computisteria e Ragioneria. Roma: Tipografia Eredi Botta. [Google Scholar]

- Jianu, Iulia, and Ionel Jianu. 2012. The told and retold story of Romanian accounting. Accounting and Management Information Systems 11: 391–423. [Google Scholar]

- Kabeer, Naila. 2005. Gender equality and women’s empowerment: A critical analysis of the third Millennium Development Goal. Gender and Development 13: 13–24. [Google Scholar] [CrossRef]

- Kanter, Rosabeth Moss. 1977. Men and Women of the Corporation. New York: Basic Books. [Google Scholar]

- Keiran, Sarah Elizabeth. 2017. Gender Roles in Public Accounting and the Absence of Women in Upper Level Management. Honors Theses and Capstones, University of New Hampshire Scholars’ Repository, Durham, NH, USA. Available online: https://scholars.unh.edu/honors/358 (accessed on 2 September 2018).

- Keister, Lisa A., and Darby E. Southgate. 2012. Inequality: A Contemporary Approach to Race, Class, and Gender. Cambridge: Cambridge University Press. [Google Scholar]

- Kirkham, Linda M., and Anne Loft. 1993. Gender and the construction of the professional accountant. Accounting, Organizations and Society 18: 507–58. [Google Scholar] [CrossRef]

- Kirkpatrick, Ian, and Daniel Muzio. 2011. Introduction: Professions and organizations—A conceptual framework. Current Sociology 59: 389–405. [Google Scholar] [CrossRef]

- Komori, Naoko. 1998. In Search of Feminine Accounting Practice: The Experience of Women Accountants in Japan. The Second Asia Pacific Interdisciplinary Research in Accounting Conference. Available online: http://www.apira2013.org/past/apira1998/archives/pdfs/50.pdf (accessed on 7 July 2017).

- Komori, Naoko. 2007. The “hidden” history of accounting in Japan: A historical examination of the relationship between Japanese women and Accounting. Accounting History 12: 329–58. [Google Scholar] [CrossRef]

- Komori, Naoko. 2008. Towards the feminization of accounting practice: Lessons from the experiences of Japanese women in the accounting profession. Accounting, Auditing and Accountability Journal 21: 507–38. [Google Scholar] [CrossRef]

- Komori, Naoko. 2012. Visualizing the Negative Space: Making Feminine Accounting Practices Visible by Reference to Japanese Women’s Household Accounting Practices. Critical Perspectives on Accounting 26: 451–67. Available online: https://elsevier.conference-services.net/resources/247/2182/pdf/CPAC2011_0039_paper.pdf (accessed on 7 July 2017). [CrossRef]

- Kornberger, Martin, Chris Carter, and Anne Ross-Smith. 2010. Changing gender domination in a Big Four accounting firm: Flexibility, performance and client service in practice. Accounting, Organizations and Society 35: 775–91. [Google Scholar] [CrossRef]

- Kyriakidou, Olivia, Orthodoxia Kyriacou, Mustafa Özbilgin, and Emmanouil Dedoulis. 2013. Equality, diversity and inclusion in accounting. Critical Perspective on Accounting, Special Issue 35: 1–12. [Google Scholar]

- Laughlin, Richard. 2011. Accounting research policy and practice: Worlds together or worlds apart? In Bridging the Gap between Academic Research and Professional Practice. Edited by Elaine Evans, Roger Burritt and James Guthrie. Sidney: Centre for Accounting, Governance and Sustainability, University of South Australia and Institute of Chartered Accountants of Australian, pp. 22–30. [Google Scholar]

- Lehman, Cheryl R. 1992. Herstory in accounting: The first eighty years. Accounting Organizations and Accounting 17: 261–85. [Google Scholar] [CrossRef]

- Liparini, Francesca. 2005. Genere e professioni contabili. Fondazione dei Dottori Commercialisti di Bologna. Zola Predosa: Tipolitografia Labor. [Google Scholar]

- Llewellyn, Sue. 1996. Theories for theorists or theories for practice? Liberating academic accounting research? Accounting, Auditing & Accountability Journal 9: 112–18. [Google Scholar]

- Loft, Anne. 1992. Accountancy and the gendered division of labour: A review essay. Accounting, Organisation and Society 17: 367–78. [Google Scholar] [CrossRef]

- Lupu, Ioana. 2010. Women in the French Accountancy Profession: The Test of Labyrinth, GREG-CRC, Conservatoire National des Artes et Métieres (Paris), Académie d’Etudes Economiques, Bucares Working Paper. pp. 1–26. Available online: https://docplayer.net/38197254-Women-in-the-french-accountancy-profession-the-test-of-the-labyrinth.html (accessed on 3 June 2017).

- Marlow, Susan, and Sara Carter. 2003. Accounting for change: Professional status, gender disadvantage and self-employment. Women in Management Review 19: 5–17. [Google Scholar] [CrossRef]

- Marquis, Christopher, and András Tilcsik. 2016. Institutional Equivalence: How Industry and Community Peers Influence Corporate Philanthropy. Organization Science 27: 1325–41. [Google Scholar] [CrossRef]

- Merriam, Sharan. 1983. Mentors and protégés: A critical review of the literature. Adult Education Quarterly 33: 161–73. [Google Scholar] [CrossRef]

- Milburn Report. 2009. Unleashing Aspiration; The Final Report of the Panel on Fair Access to the Professions. Available online: http: //www.cabinetoffice.gov.uk/accessprofessions (accessed on 10 November 2018).

- Muller, Jerry Z. 1997. Conservatism: An Anthology of Social and Political Thought from David Hume to the Present. Princeton: Princeton University Press, p. 26. ISBN 0691037116. [Google Scholar]

- Mustata, Razvan V., Szilveszter Fekete, and Dumitru Matis. 2010. Motivating accounting professionals in Romania. Analysis after five decades of communist ideology and two decades of accounting harmonization. Accounting and Management Information Systems 10: 169–201. [Google Scholar]

- Napier, Christopher J. 2001. Accounting history and accounting progress. Accounting History 6: 7–31. [Google Scholar] [CrossRef]

- OhOgartaigh, Ciaran O. 2000. Accounting for feminisation and the feminisation of accounting in Ireland: Gender and self-evaluation in the context of uncertain accounting information. IBAR, Irish Business and Administrative Research 21: 10–29. [Google Scholar]

- Paisey, Catriona, and Nicholas J. Paisey. 2010. Comparative research: An opportunity for accounting researchers to learn from other professions. Journal of Accounting & Organizational Change 6: 180–99. [Google Scholar]

- Paris, Dubravka. 2016. History of accounting and accountancy profession in Great Britain. Journal of Accounting and Management 6: 33–44. [Google Scholar]

- Patel, Chris. 2004. Some theoretical and methodological suggestions for cross-cultural accounting studies. International Journal of Accounting, Auditing and Performance Evaluation 1: 61–84. [Google Scholar] [CrossRef]

- Patel, Christopher. 2006. A Comparative Study of Professional Accountants’ Judgments—Studies in Managerial and Financial Accounting. Amsterdam and Oxford: Elsevier. [Google Scholar]

- Patel, Chris, and Jim Psaros. 2000. Perceptions of external auditors’ independence: Some cross-cultural evidence. The British Accounting Review 32: 311–38. [Google Scholar] [CrossRef]

- Pistoni, Anna, and Laura Zoni. 2000. Comparative management accounting education in Europe: An undergraduate education perspective. The European Accounting Review 9: 285–319. [Google Scholar] [CrossRef]

- Ried, Glenda E., Brenda T. Acken, and Elise G. Jancura. 1987. A Historical perspective on women in Accounting. Journal of Accountancy 163: 338–55. [Google Scholar]

- Rhoades, Gary. 2001. Introduction to special section: Perspectives on comparative higher education. Higher Education 41: 345–52. [Google Scholar] [CrossRef]

- Roberts, Diane H. 2013. Women in accounting occupations in the 1880 US Census. Accounting History Review 23: 141–60. [Google Scholar] [CrossRef]

- Rodrigues, Lúcia Lima, Delfina Gomes, and Russell Craig. 2003. Corporatism, Liberalism and the Accounting Profession in Portugal Since. Accounting Historians Journal 30: 95–128. [Google Scholar] [CrossRef]

- Samkin, Grant, and Annika Schneider. 2014. The Accounting Academic. Meditari Accountancy Research 22: 2–19. [Google Scholar] [CrossRef]

- Scott, Joan Wallach. 1986. Gender: A Useful Category for Historical Analysis. The American Historical Review 5: 1053–75. [Google Scholar] [CrossRef]

- Scott, W. Richard. 2004. Institutional theory. In Encyclopedia of Social Theory. Edited by George Ritzer. Thousand Oaks: Sage, pp. 408–14. [Google Scholar]

- Shearer, Teri L., and C. Edward Arrington. 1989. Accounting in other worlds: A feminism without reserve. Accounting, Organizations and Society 18: 253–72. [Google Scholar] [CrossRef]

- Treas, Judith, and Tsuio Tai. 2016. Gender inequality in housework across 20 European Nations: Lessons from Gender Stratification Theories. Sex Roles 74: 495–511. [Google Scholar] [CrossRef]

- Tremblay, Marie-Soleil, Bertrand Malsch, and Yves Gendron. 2016. Gender on board: Deconstructing the legitimate female director. Accounting, Auditing & Accountability Journal 29: 165–90. [Google Scholar]

- Tudor, Adriana Tiron, and Alexandra Mutiu. 2007. Important stages in the development of Romanian accounting profession (from 1800 up to now). Spanish Journal of Accounting History 6: 183–99. [Google Scholar]

- Ulivieri, Simonetta. 1986. La donna e gli studi universitari nell’Italia postunitaria. In Cento anni di università—L’istruzione superiore in Italia dall’unità ai nostri giorni. Edited by Francesco De Vivo and Giovanni Genovesi. Napoli: Edizioni Scientifiche Italiane, pp. 219–28. [Google Scholar]

- Virtanen, Aila. 2009. Accounting, gender and history: The life of Minna Canth. Accounting History 14: 79–100. [Google Scholar] [CrossRef]

- Waldmann, Erwin. 2000. Teaching ethics in accounting: A discussion of cross-cultural factors with a focus on Confucian and Western philosophy. Accounting Education: An International Journal 9: 23–35. [Google Scholar] [CrossRef]

- Walker, Stephen P. 2008. Accounting histories of women: Beyond recovery? Accounting, Auditing & Accountability Journal 21: 580–610. [Google Scholar]

- Wermuth, Laurie, and Miriam Ma’at-Ka-Re Monges. 2002. Gender stratification. A Structural Model for Examining Case Examples of Women in Less-Developed Countries. Frontiers: A Journal of Women Studies 23: 1–22. [Google Scholar] [CrossRef]

- Whiting, Rosalind H., Elizabeth Gammie, and Kathleen Herbohn. 2015. Women and the prospects for partnership in professional accountancy firms. Accounting and Finance 55: 575–605. [Google Scholar] [CrossRef]

- Whitten, Donna L. 2016. Mentoring and Work Engagement for Female Accounting, Faculty Members in Higher Education. Mentoring & Tutorship: Partnership in Learning 24: 365–82. [Google Scholar]

- Windsor, Carolyn, and Pak Auyeung. 2006. The Effect of Gender and Dependent Children on Professional Accountants’ Career Progression. Critical Perspectives on Accounting 17: 828–44. [Google Scholar] [CrossRef]

- Wootton, Charles W., and Barbara E. Kemmerer. 2000. The changing genderization of the accounting workforce in the US, 1930–1990. Accounting, Business & Financial History 10: 169–90. [Google Scholar]

- Wright, Cheryl A., and Scott D. Wright. 1987. The role of mentors in the career development of young professionals. Family Relations 36: 204–8. [Google Scholar] [CrossRef]

- Yin, Robert K. 2003. Case Study Research. Design and Methods, 3rd ed. London: Sage Publications. [Google Scholar]

{kind=link}

| Gender Segregation in Occupations | Gender Segregation in Sectors | |||||

|---|---|---|---|---|---|---|

| 2005 | 2010 | 2015 | 2005 | 2010 | 2015 | |

| EU 27 | 24.8 | 24.9 | 24.3 | 17.8 | 19.1 | 18.9 |

| EU 28 | 24.9 | 24.3 | 19.1 | 18.9 | ||

| Italy | 23.6 | 24.7 | 24.8 | 17.8 | 19.7 | 19.5 |

| Romania | 19.3 | 22 | 23 | 14.9 | 16.7 | 18.1 |

| Proportion of Women in Boards of the Largest Publicly Listed Companies (%) | Proportion of Women in the Single/Lower Houses of the National/Federal Parliaments (%) | Proportion of Women among Senior Ministers in National/FEDERAL Governments (%) | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2013 | 2016 | 2010 | 2013 | 2016 | 2010 | 2013 | 2016 | |

| EU28 | 11.9% | 17.8% | 23.9% | 24.4% | 27.4% | 28.7% | 26.2% | 26.6% | 27.9% |

| Italy | 4.5% | 15.0% | 32.3% | 21.1% | 31.3% | 31.0% | 21.7% | 28.6% | 29.4% |

| Romania | 21.3% | 7.8% | 10.1% | 11.4% | 13.5% | 14.2% | 11.8% | 21.4% | 36.4% |

| Key Areas | Italy | Romania |

|---|---|---|

| Equal economic independence (2016) Source: Eurostat, LFS | Men 72.2% Women 51.7% | Men 76.8 Women 58.5 |

| Women and men’s employment rate in full-time equivalent (20–64 years old, 2015) Source: Eurostat, LFS | Italy Women 43.7 Men 68.3 Gender gap (men-women) 24.6 | Romania Women 55.4 Men 73 Gender gap (men-women) 17.6 |

| 2015 | 2016 | |

|---|---|---|

| Presidents | 7.1% | 7.0% |

| CEOs | 3.6% | 5.1% |

| Non-executive directors: | 22.5% | 26.1% |

| Senior executives: | 13.7% | 14.9% |

| Gender Diversity Dimensions/Countries | Italy (CNDCEC—Consiglio Nazionale dei Dottori Commercialisti e degli Esperti Contabili) | Romania (CECCAR—Body of Expert and Licensed Accountants of Romania) |

|---|---|---|

| Law on gender equality | Establishes a gender quota for companies listed in the Stock Exchange—noncompliance results in a warning followed by financial sanctions and in the case of noncompliance the exclusion from the board YES | Law No 202/2002 on equal opportunities and treatment for women and men in labour market, education and the elimination of gender roles and stereotypes YES |

| Quotas on Boards | Mandatory 33.3% | NO |

| % Women on Boards | 31% | 12% |

| % Women in accountancy | 31.60% | 77.90% |

| Actions | working committees dedicated for gender equality; databases collecting resumes of women that are interested in being appointed to boards; collection of signs of discrimination in order to implement actions that promote gender equality YES | NO |

| Good Practices | NO | NO |

| Work from home | NO | NO |

| Flexible work hours | NO | NO |

| Part-time work | NO | NO |

| Internal quotas | NO | NO |

| Promotion rules | NO | NO |

| Services allowing workers to achieve a better balance between work and family life | NO | NO |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Del Baldo, M.; Tiron-Tudor, A.; Faragalla, W.A. Women’s Role in the Accounting Profession: A Comparative Study between Italy and Romania. Adm. Sci. 2019, 9, 2. https://doi.org/10.3390/admsci9010002

Del Baldo M, Tiron-Tudor A, Faragalla WA. Women’s Role in the Accounting Profession: A Comparative Study between Italy and Romania. Administrative Sciences. 2019; 9(1):2. https://doi.org/10.3390/admsci9010002

Chicago/Turabian StyleDel Baldo, Mara, Adriana Tiron-Tudor, and Widad Atena Faragalla. 2019. "Women’s Role in the Accounting Profession: A Comparative Study between Italy and Romania" Administrative Sciences 9, no. 1: 2. https://doi.org/10.3390/admsci9010002

APA StyleDel Baldo, M., Tiron-Tudor, A., & Faragalla, W. A. (2019). Women’s Role in the Accounting Profession: A Comparative Study between Italy and Romania. Administrative Sciences, 9(1), 2. https://doi.org/10.3390/admsci9010002