Scenario-Based Analysis of IT Enterprises Servitization as a Part of Digital Transformation of Modern Economy

Abstract

:1. Introduction

1.1. Goods and Products

- Physical objects for which a demand exists;

- Their physical attributes are preserved over time;

- Ownership rights can be established;

- They exist independently of their owner;

- They are exchangeable;

- Unit ownership rights can be exchanged between institutions;

- They can be traded on markets;

- They embody specialized knowledge in a method that is highly advantageous for promoting the division of labor.

1.2. Services

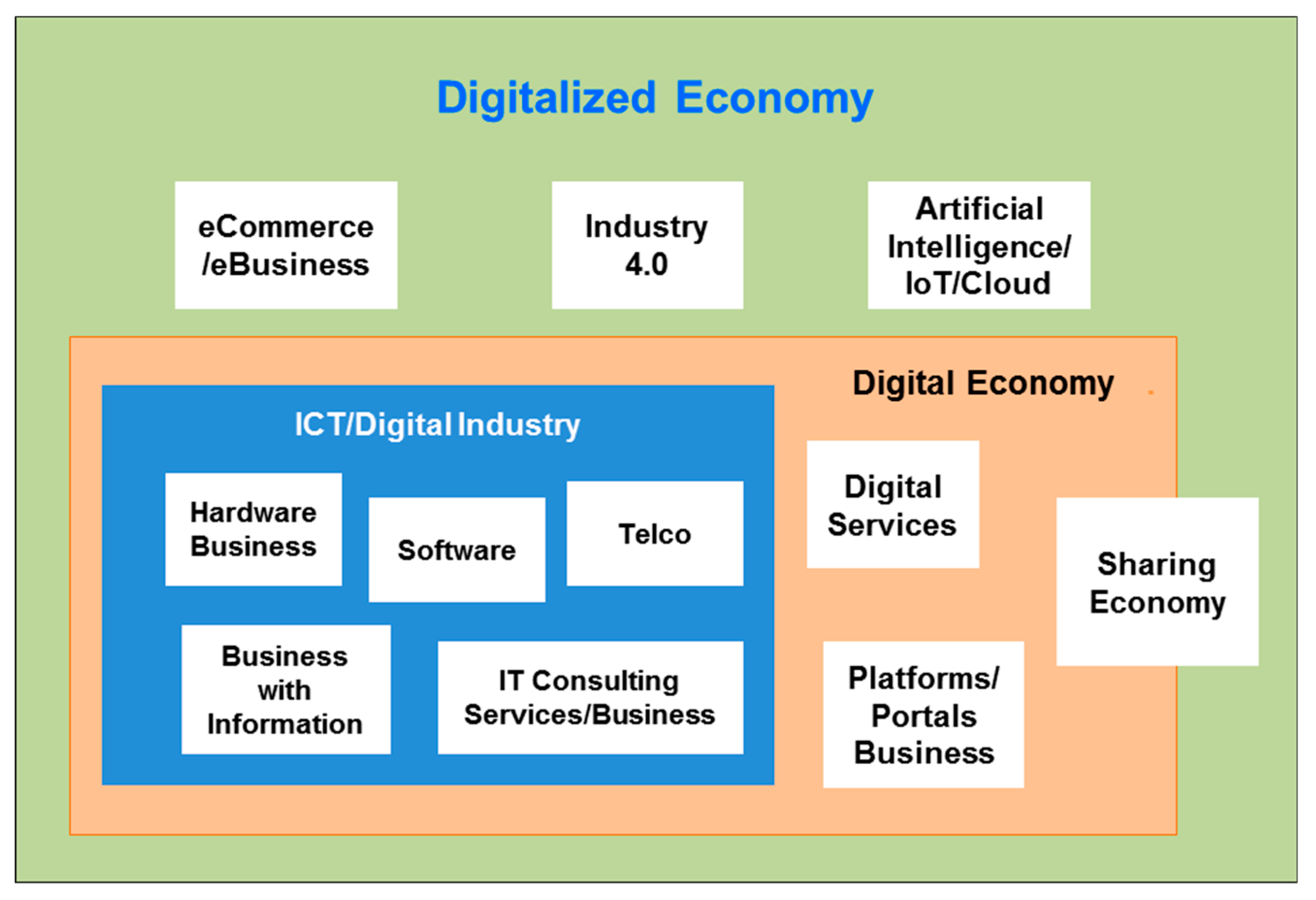

1.3. Digital Goods and Digital Products

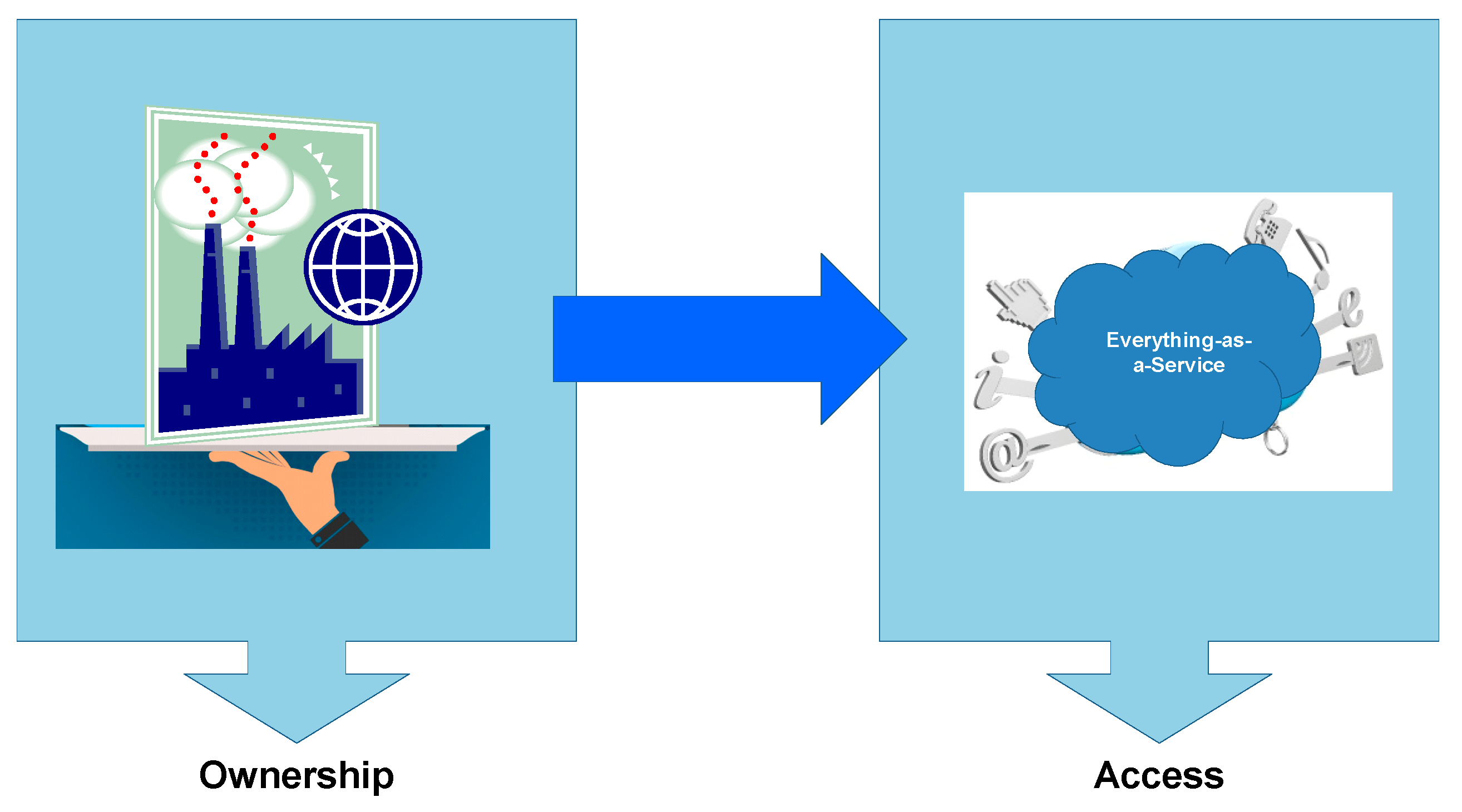

2. Servitization

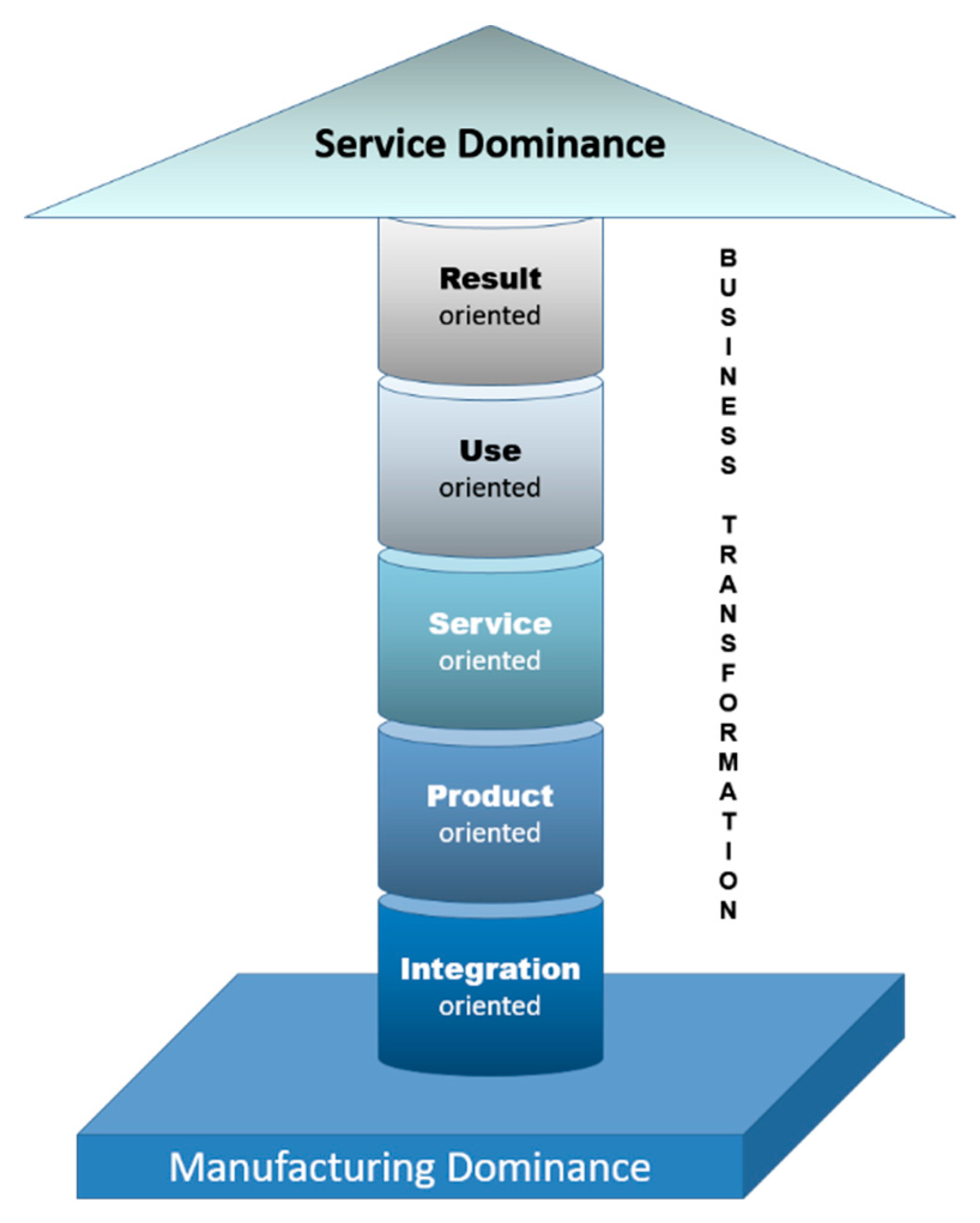

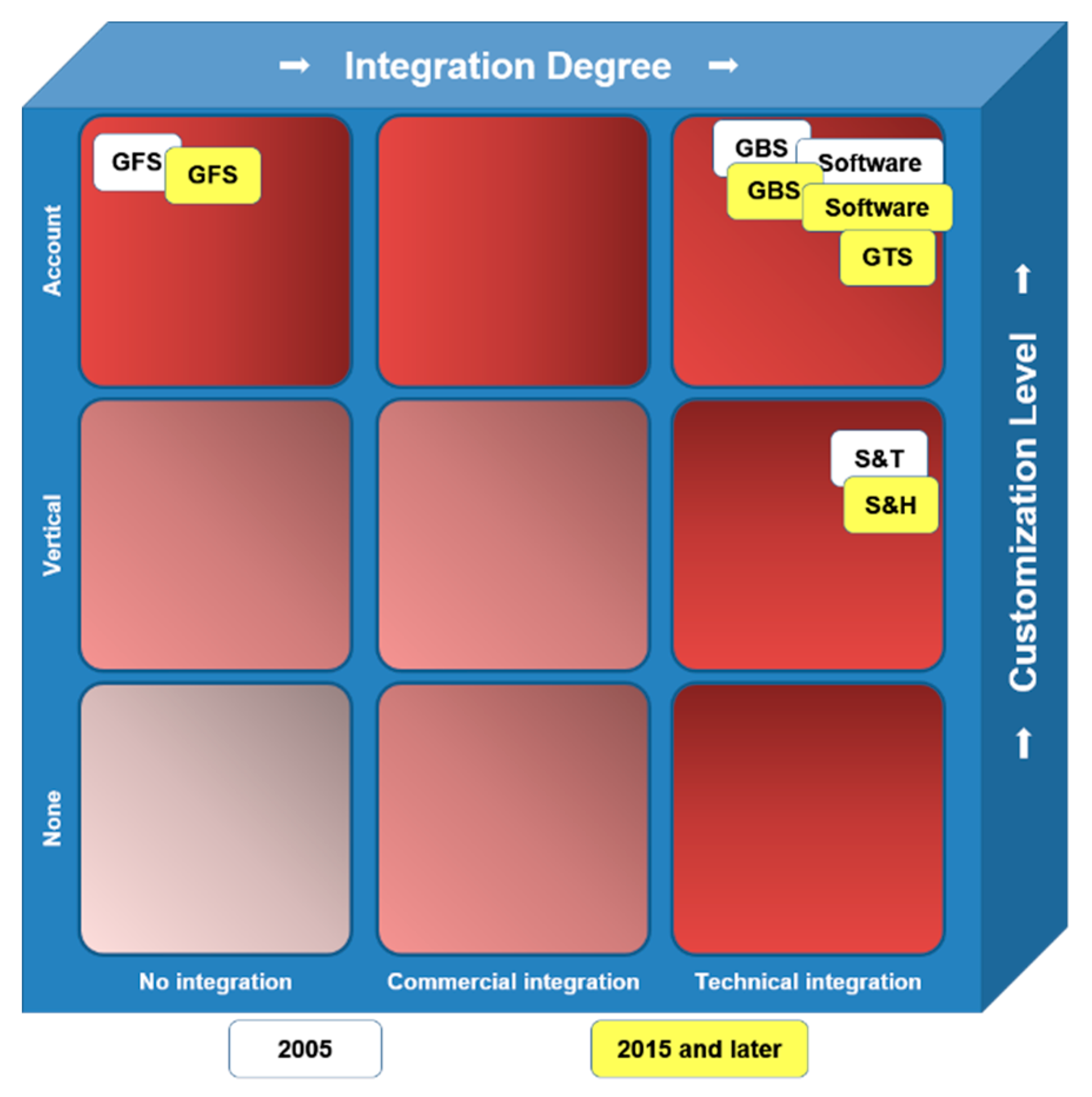

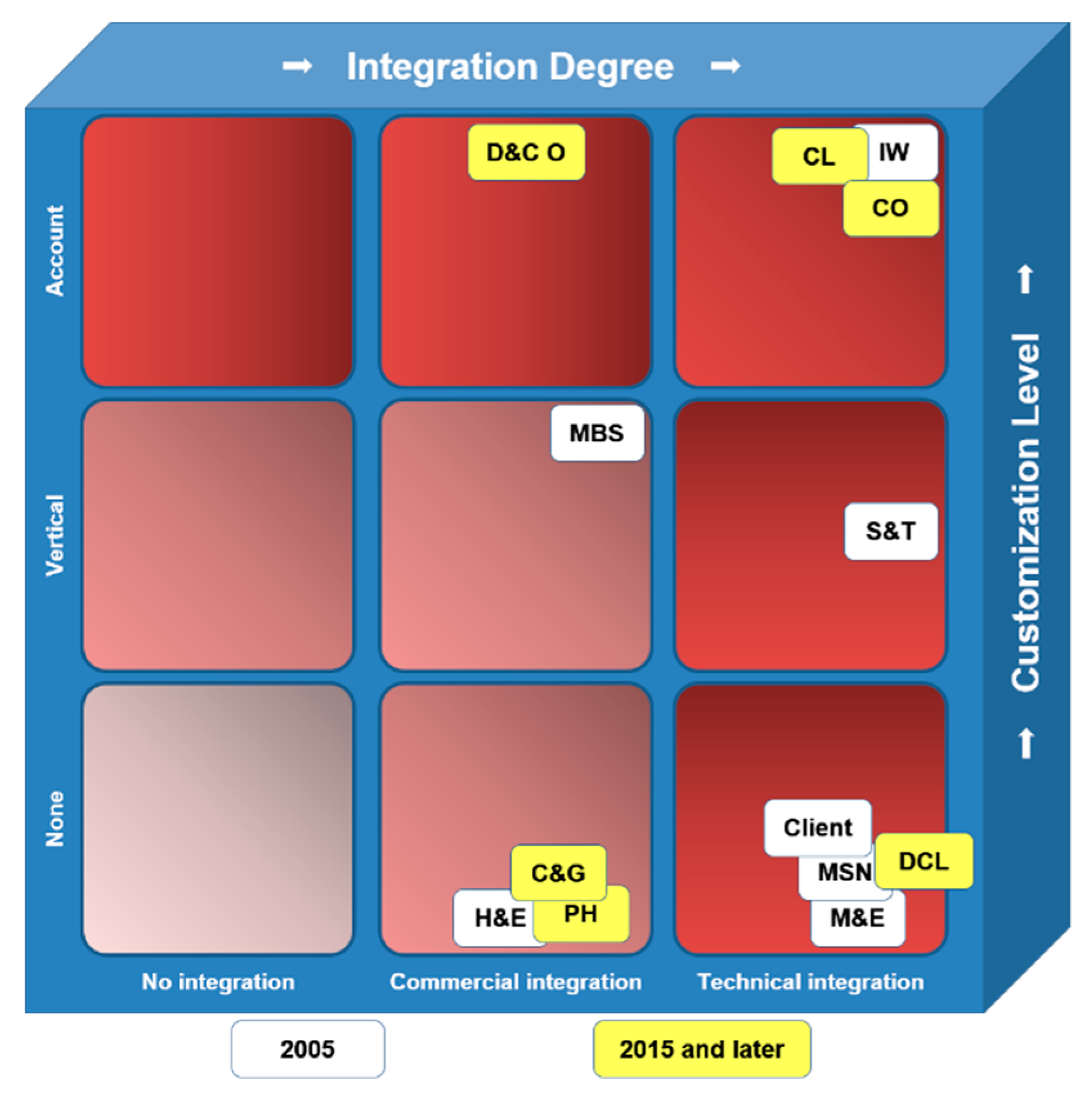

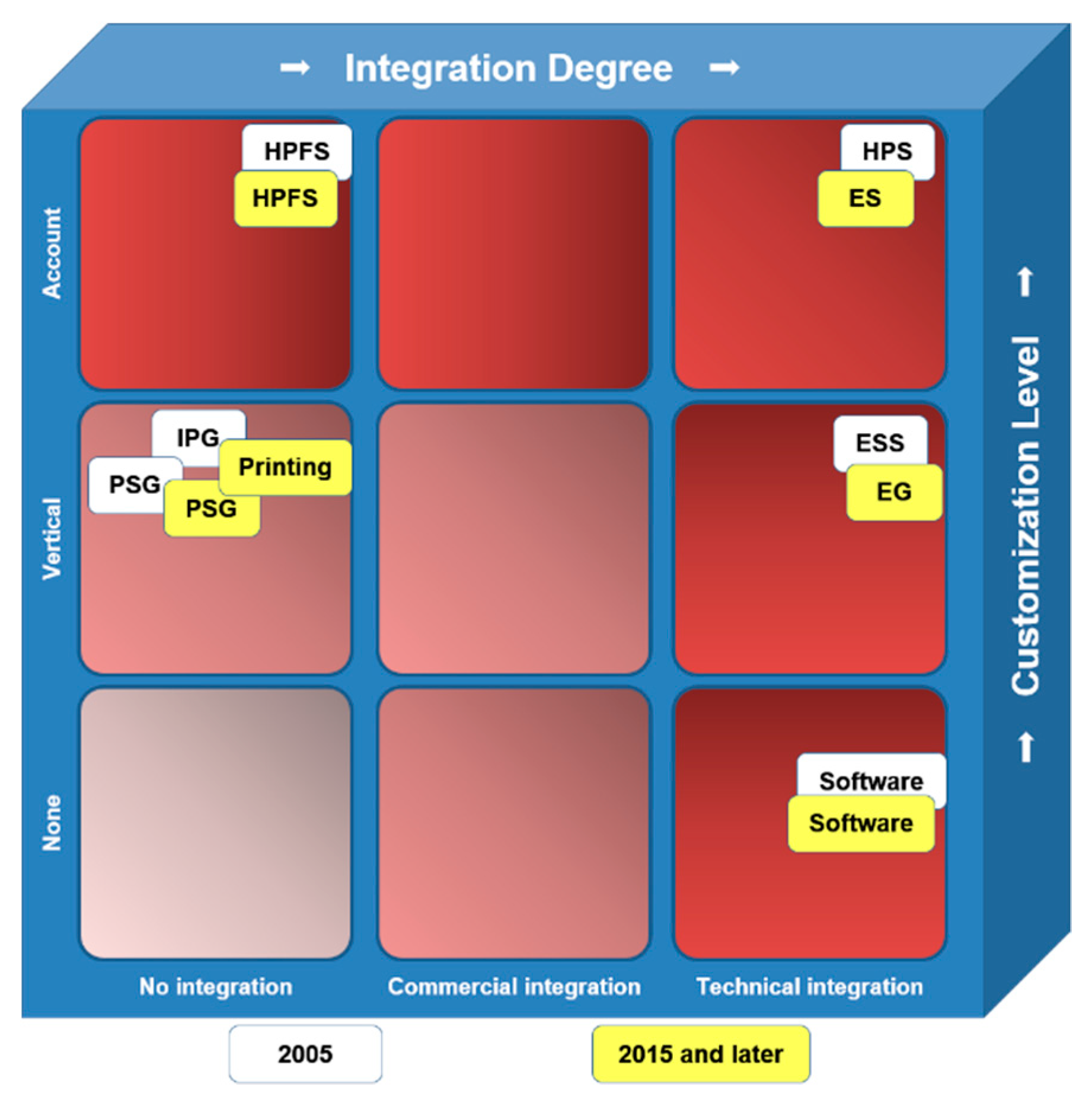

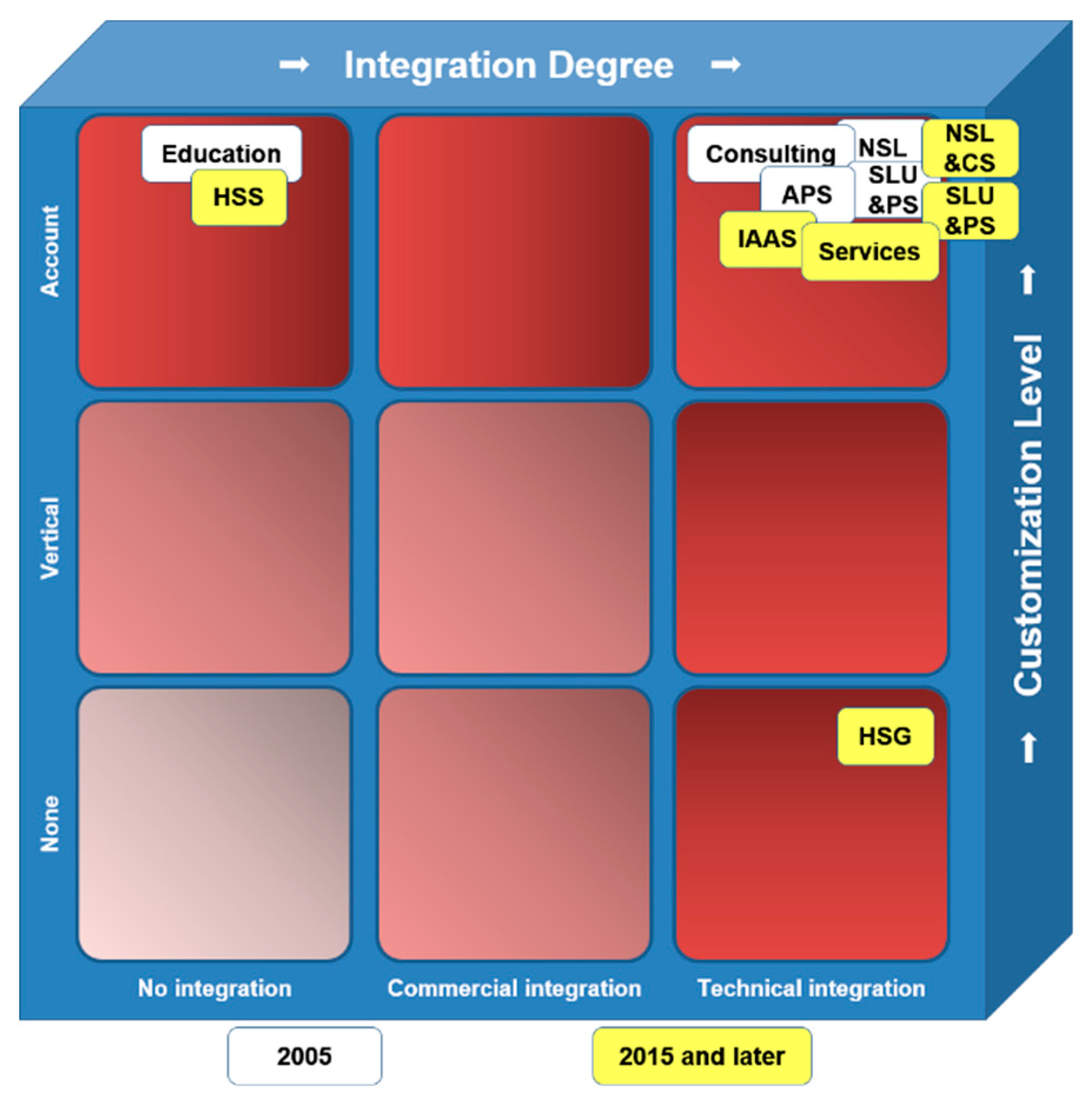

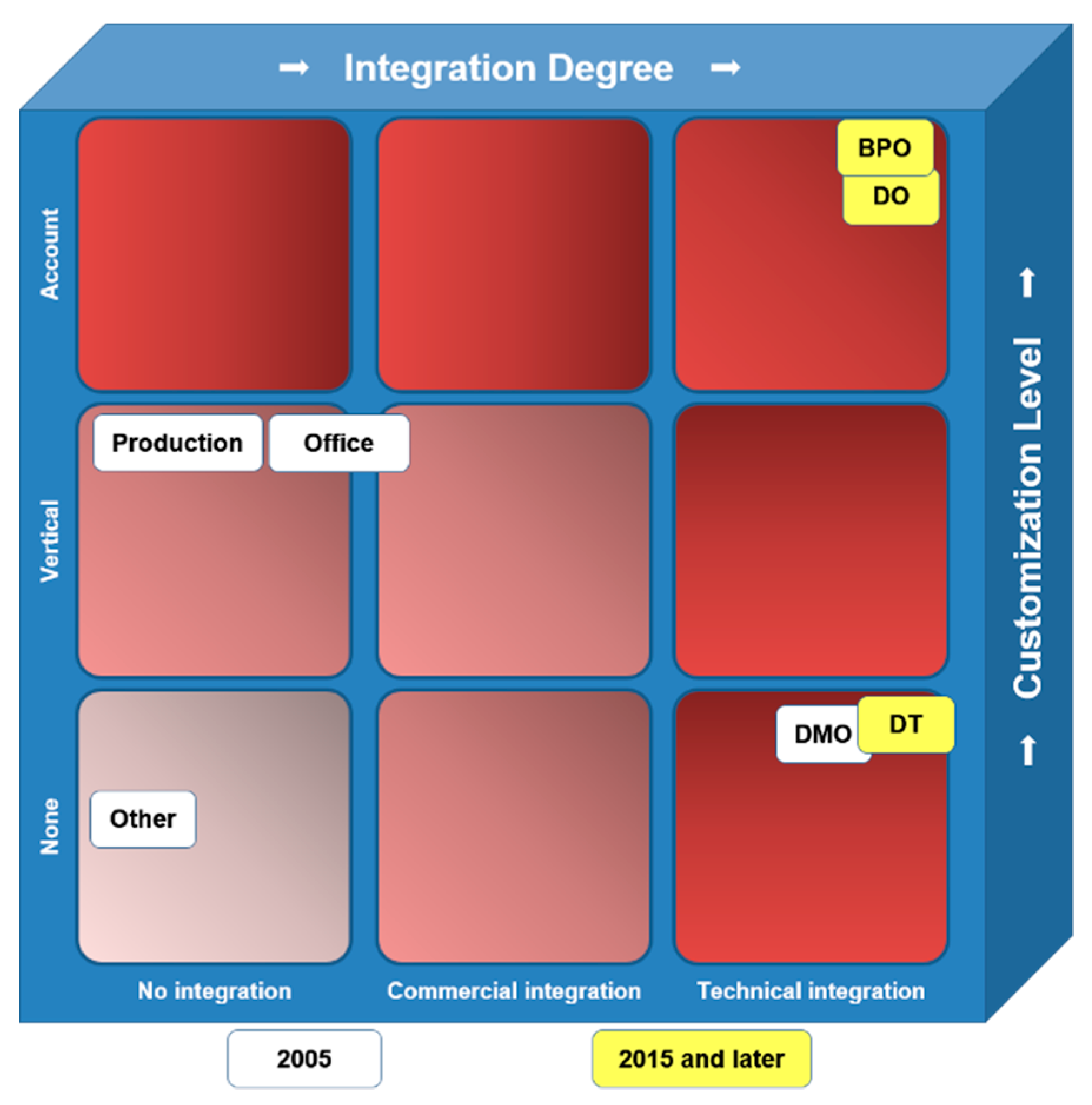

2.1. Phases Analysis

- On the first level there is no customization added to the basic product/service. These products/services are usually standardized and have the same marketing strategies;

- On the second level, several adoptions and modifications, geared towards industries or customer segments, are implemented. This primarily varies in the technical specifications or the marketing of the product/service;

- On the first level no interrelation is occurring and only a single product or service is sold;

- On the second level commercial integration is happening, where multiple products/services are put into a single offer. In this phase, there are various types of product or price bundles;

- At the highest degree of integration, commercial integration and technical integration occur simultaneously. This degree of integration requires the interoperability of the components and occurs in offers where an option is offered from beginning to end. In this case, the offerings are interlinked for customer satisfaction and support [39,41].

2.2. Transaction Analysis

3. Servitization Scenarios of Top 5 IT Enterprises

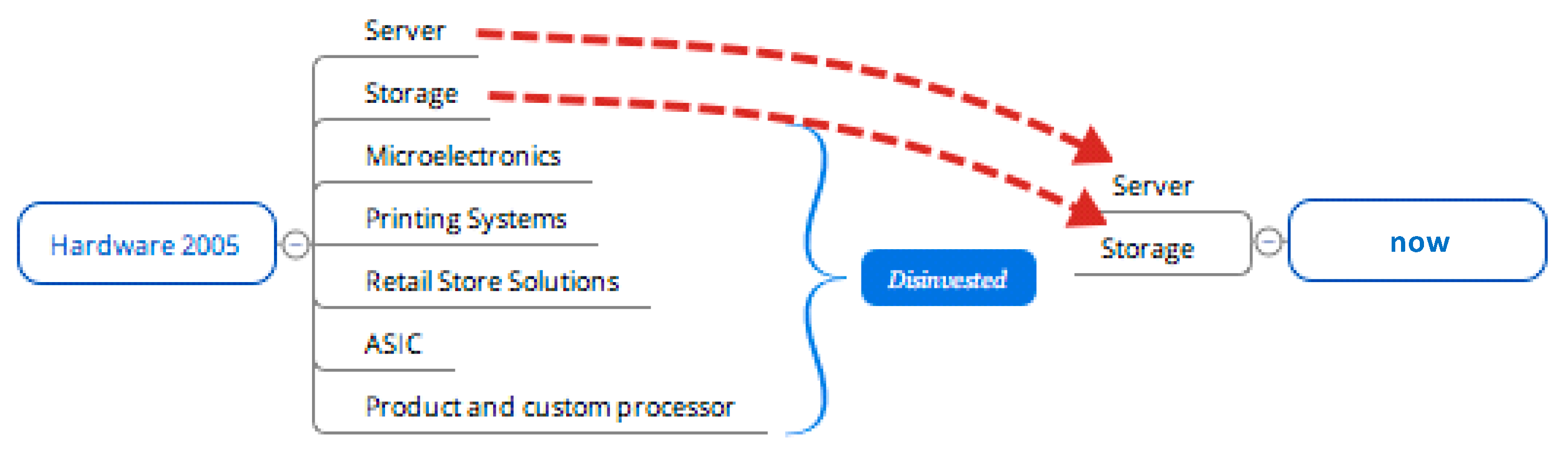

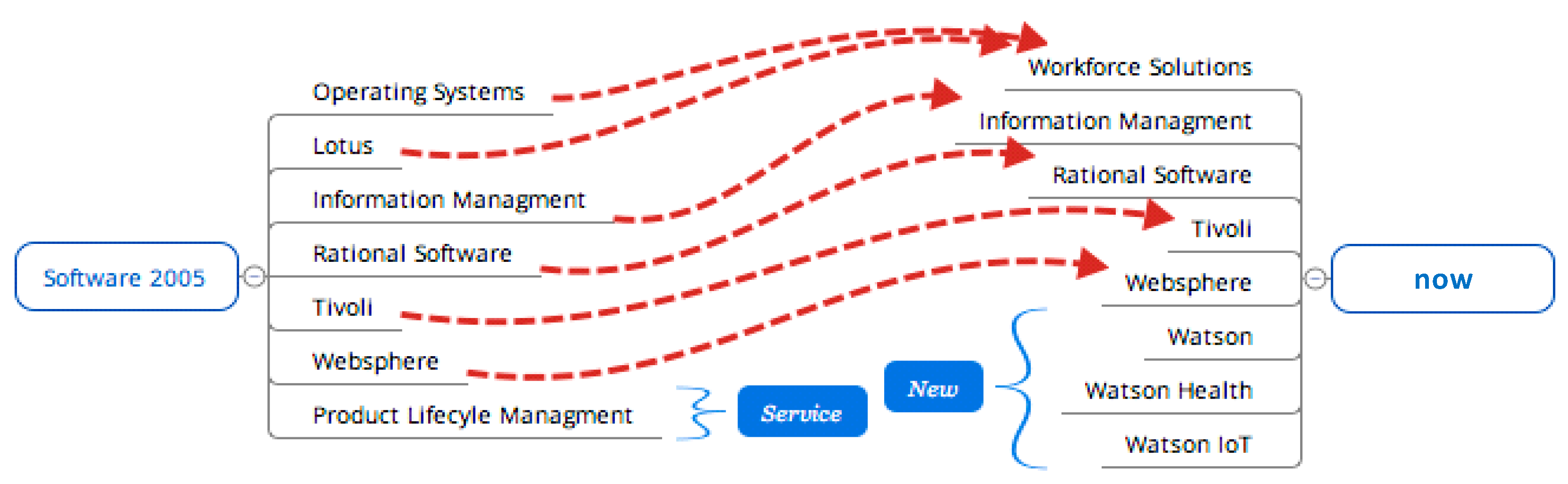

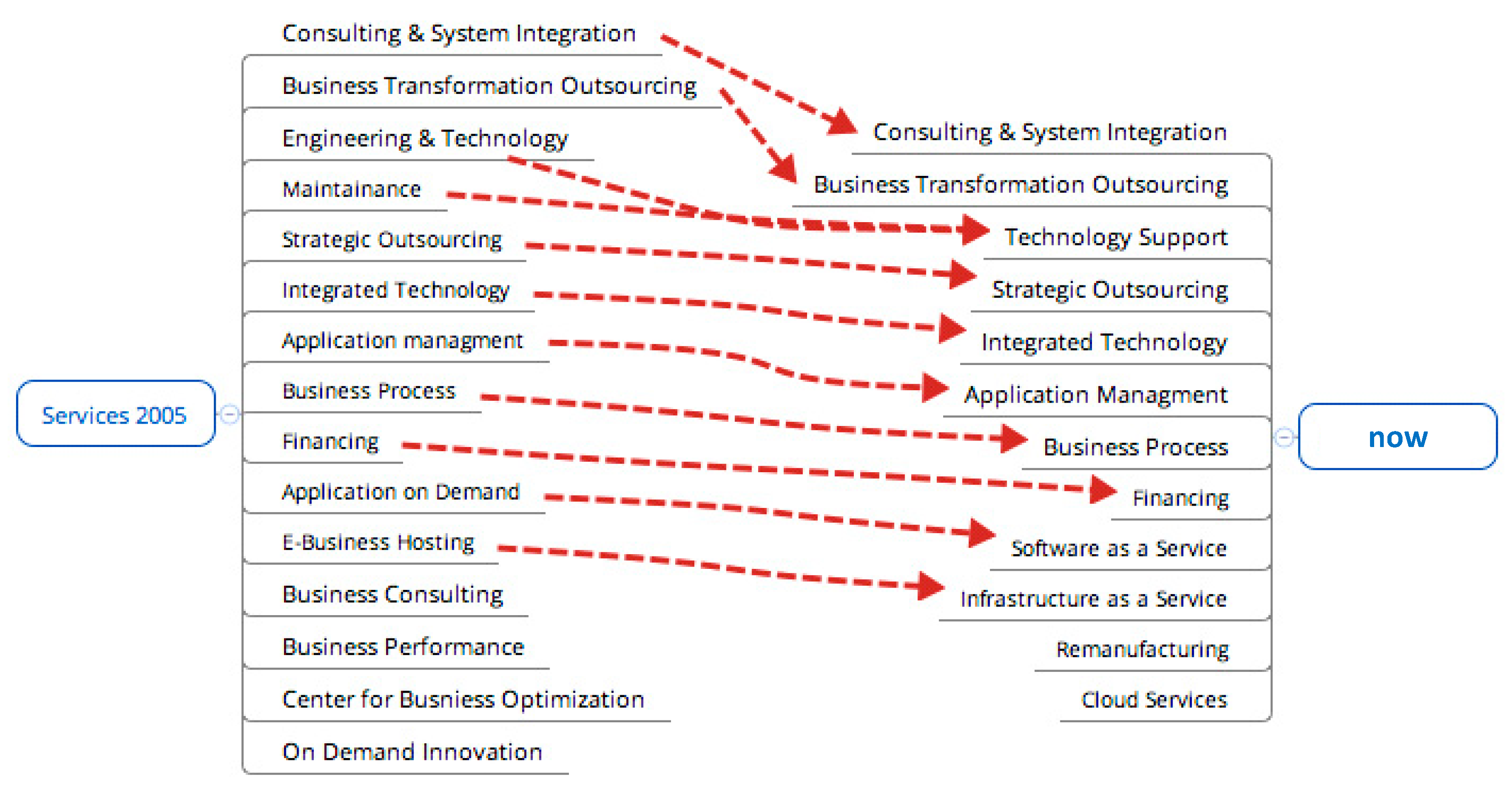

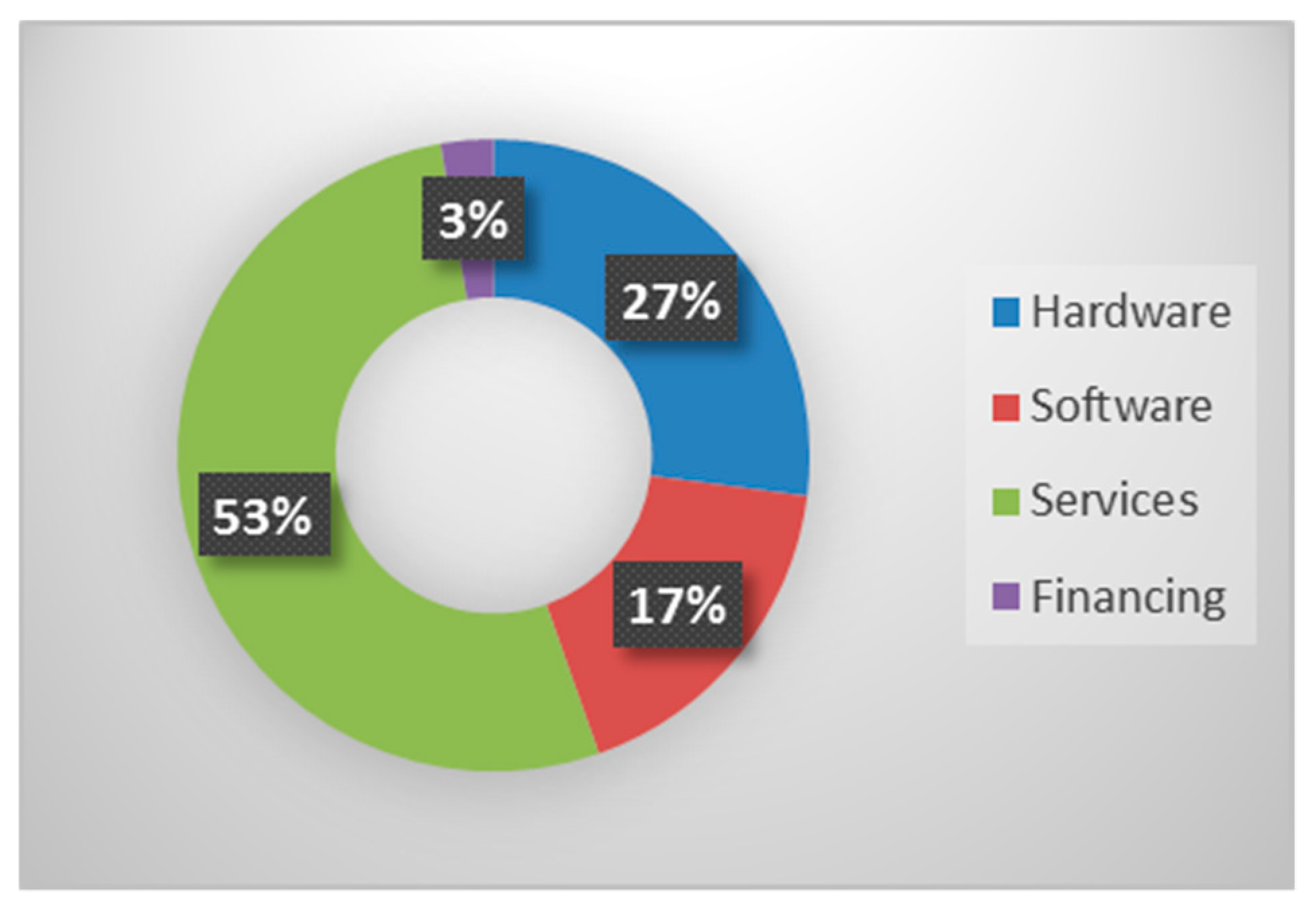

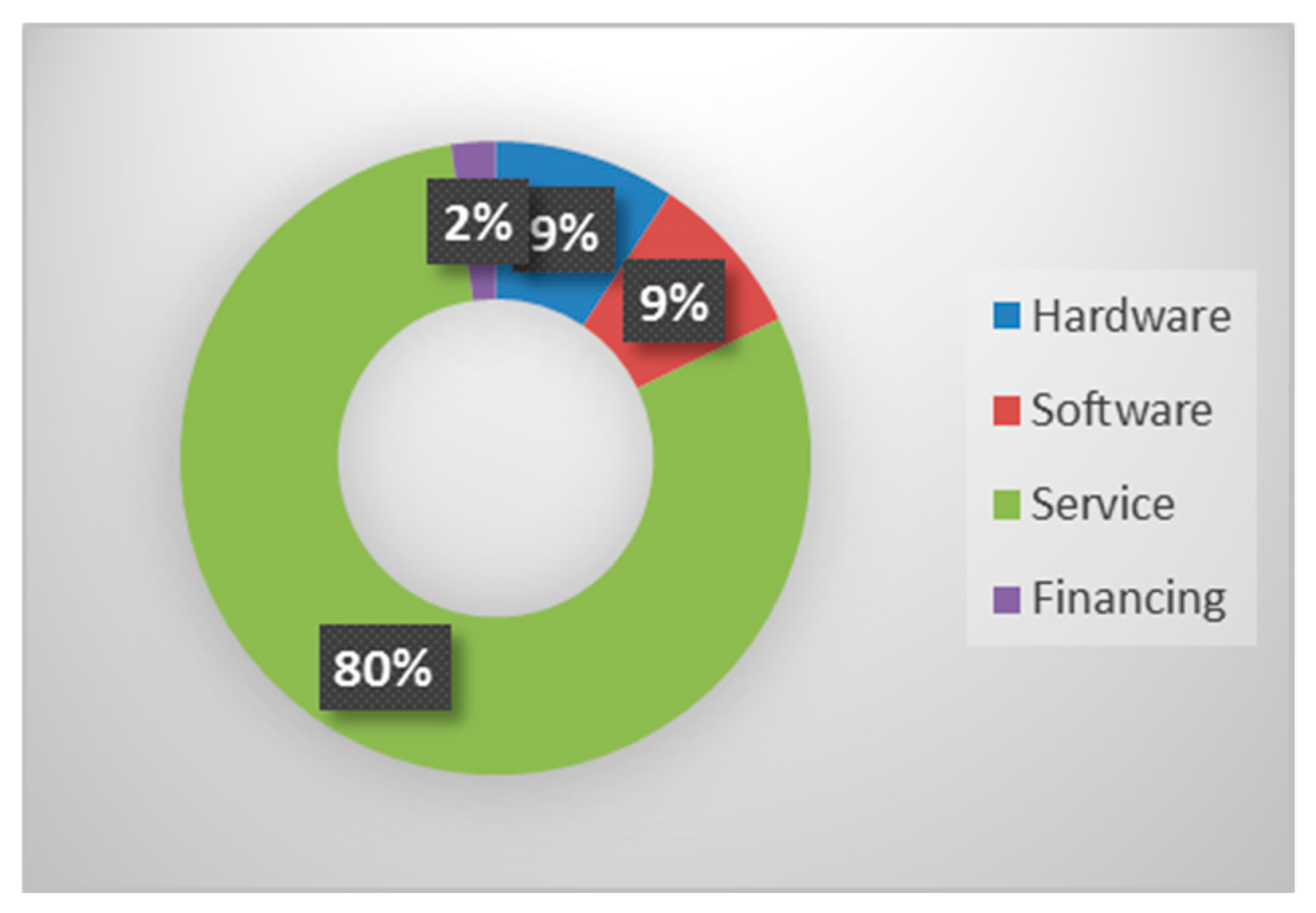

3.1. IBM Servitization Scenario

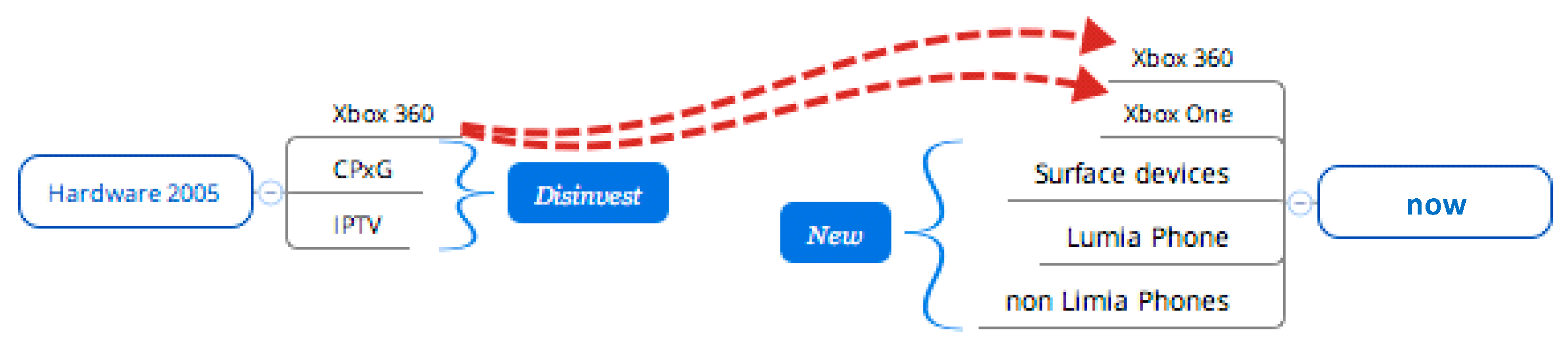

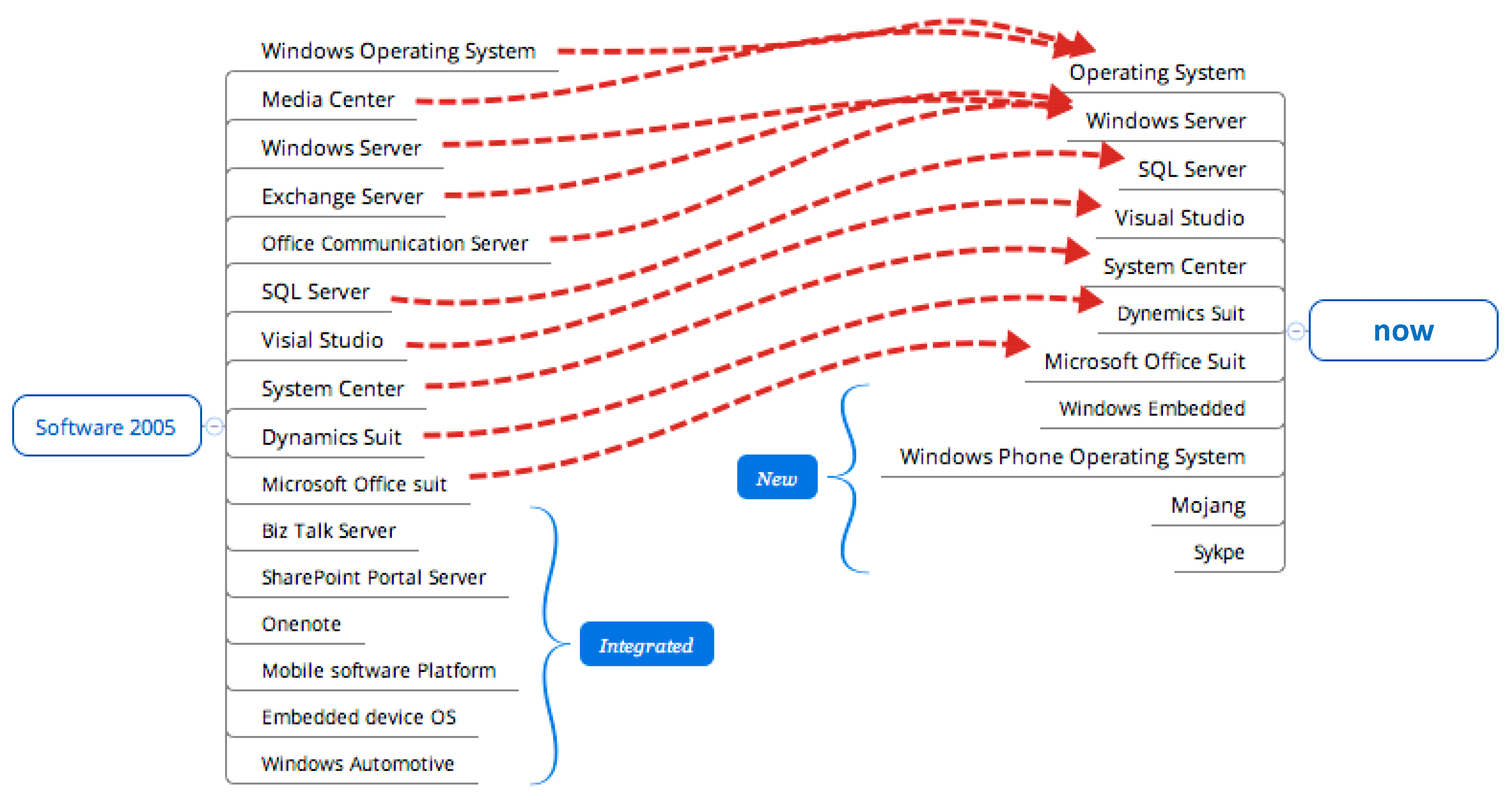

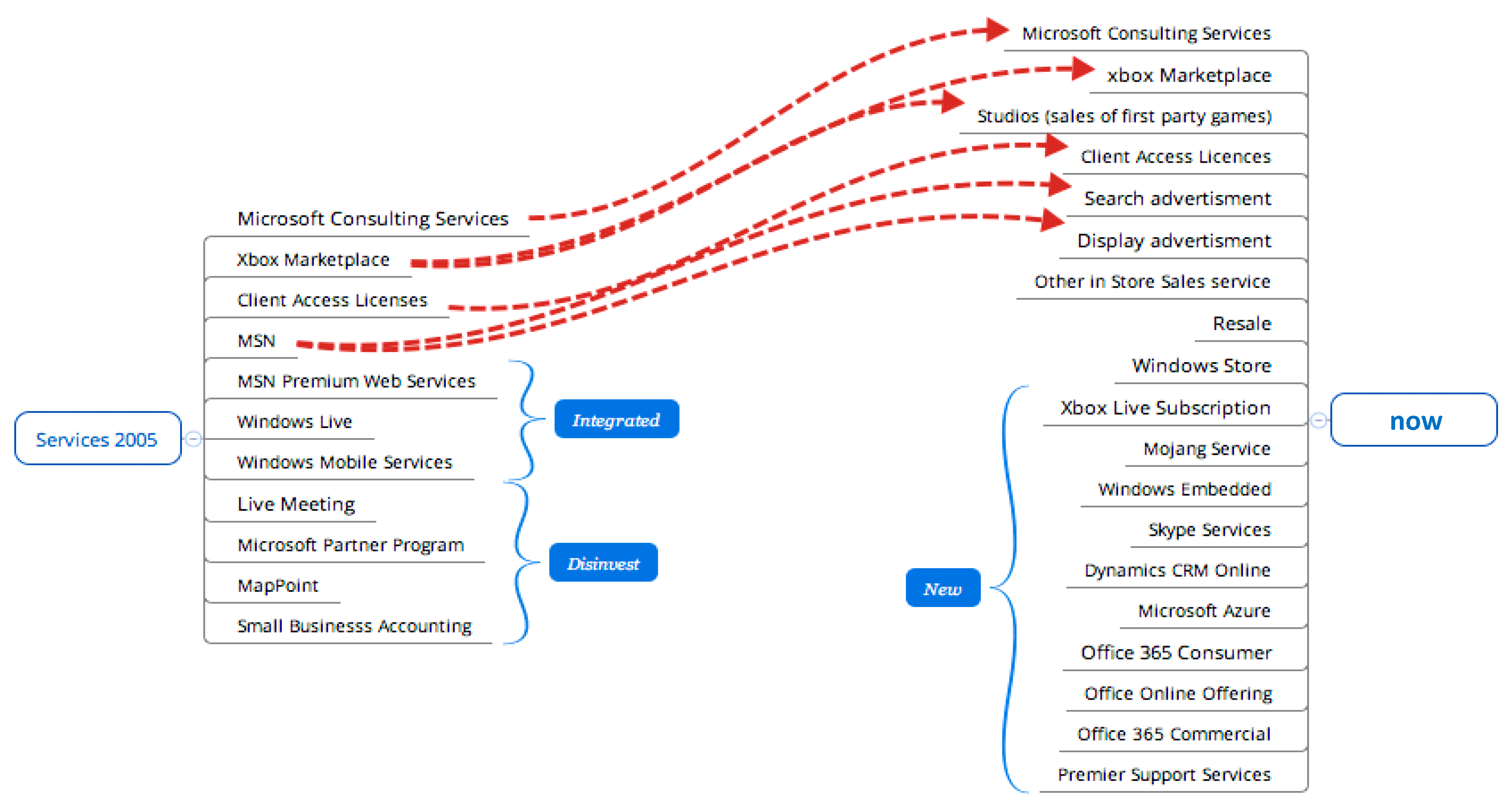

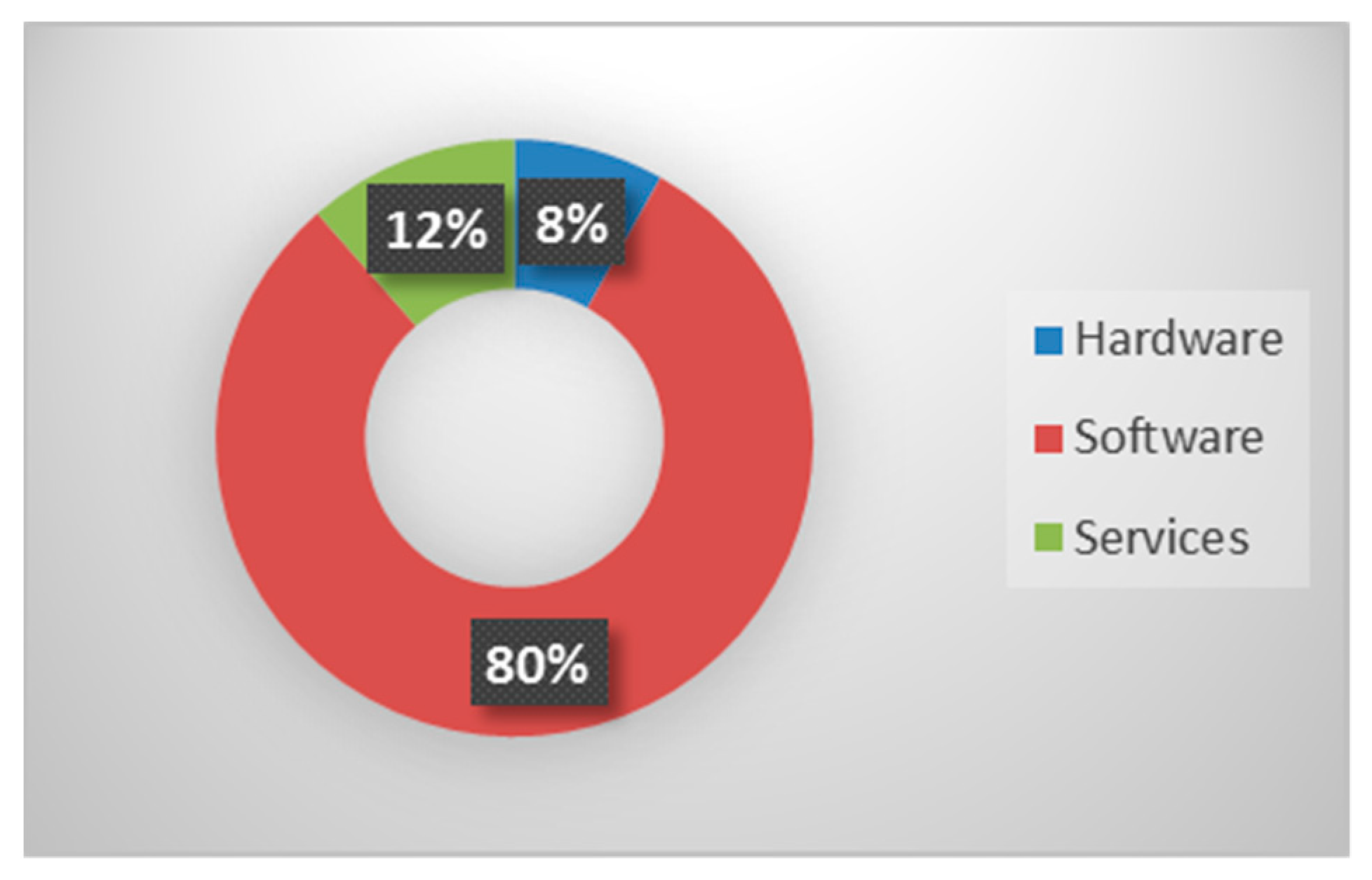

3.2. Microsoft Servitization Scenario

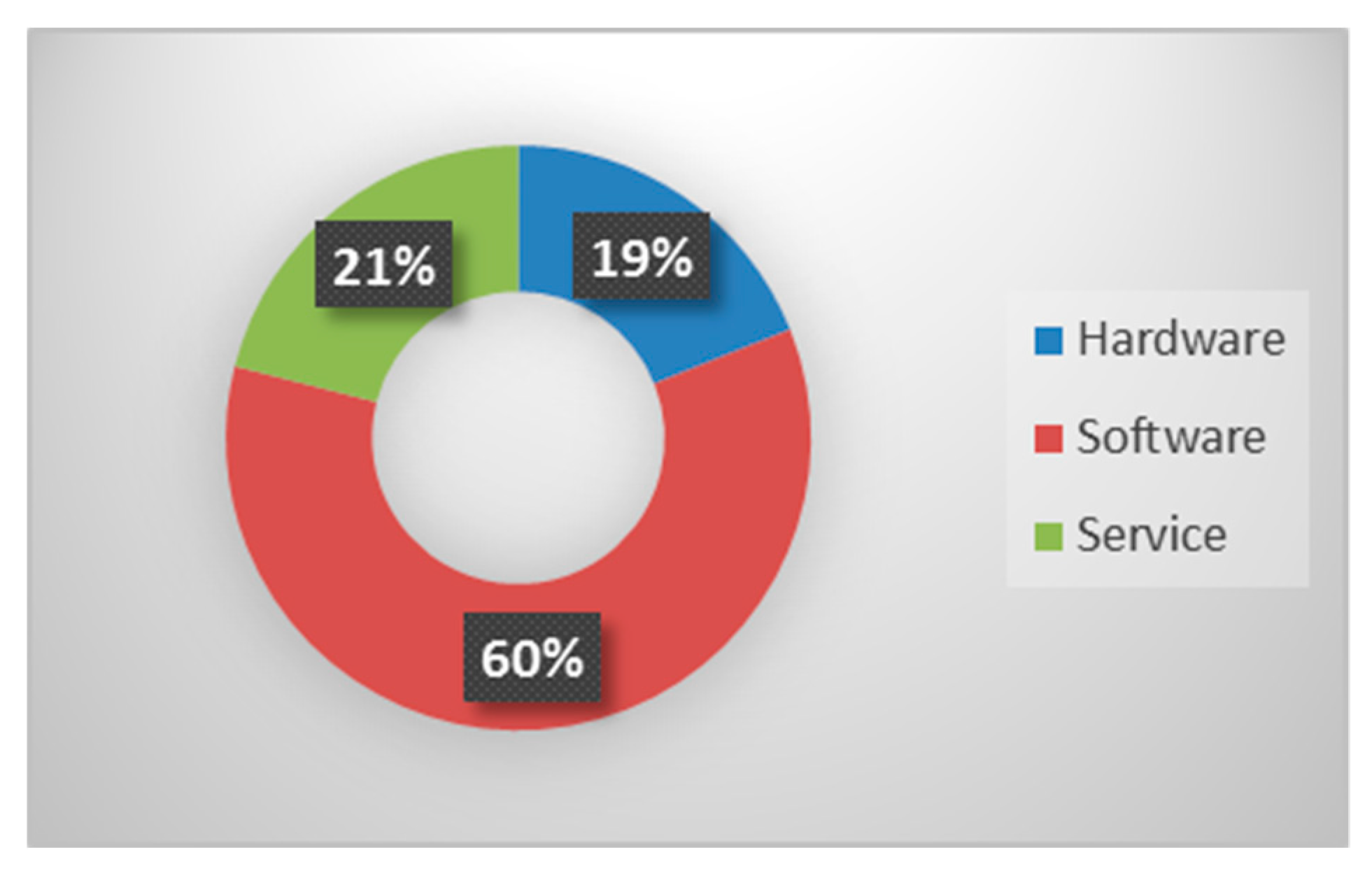

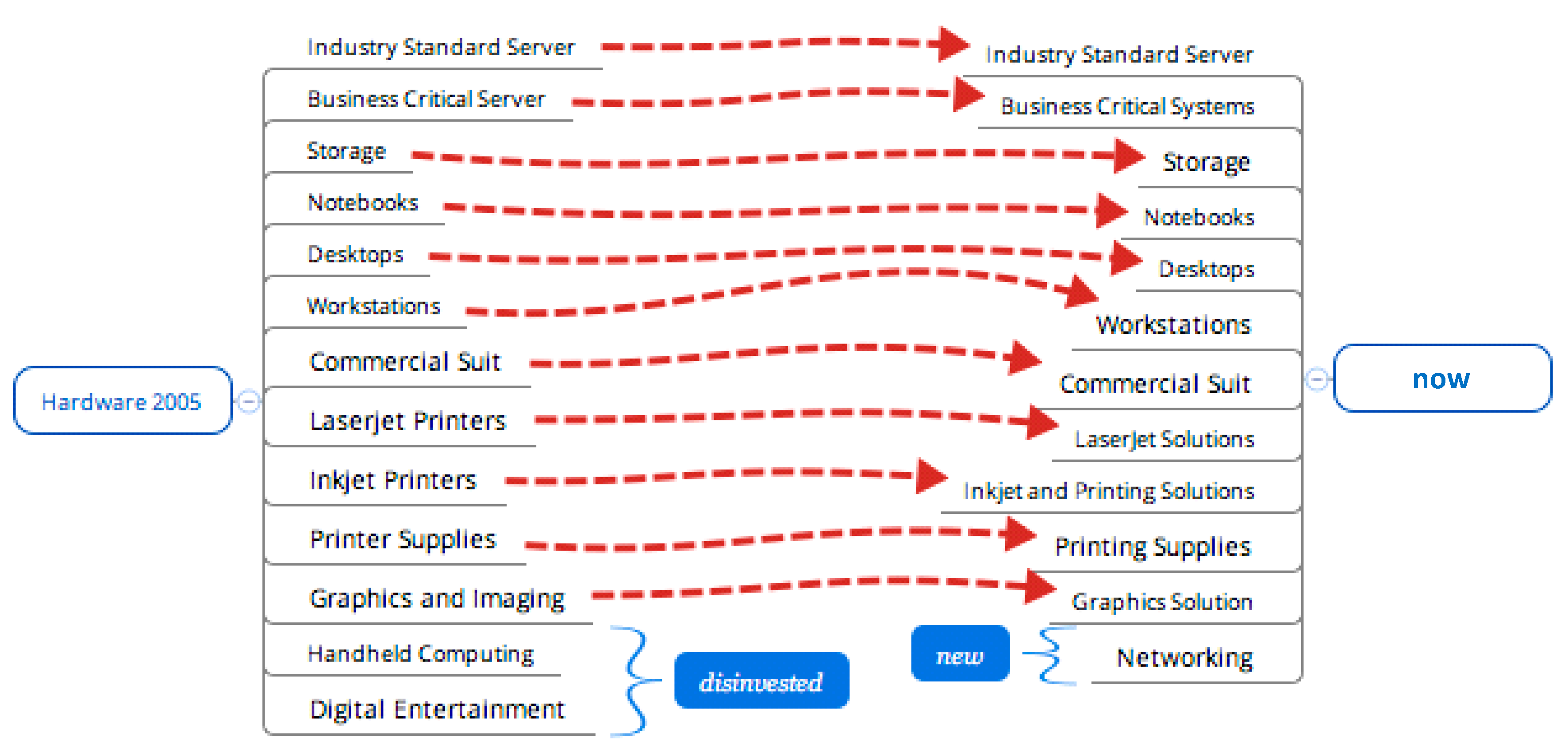

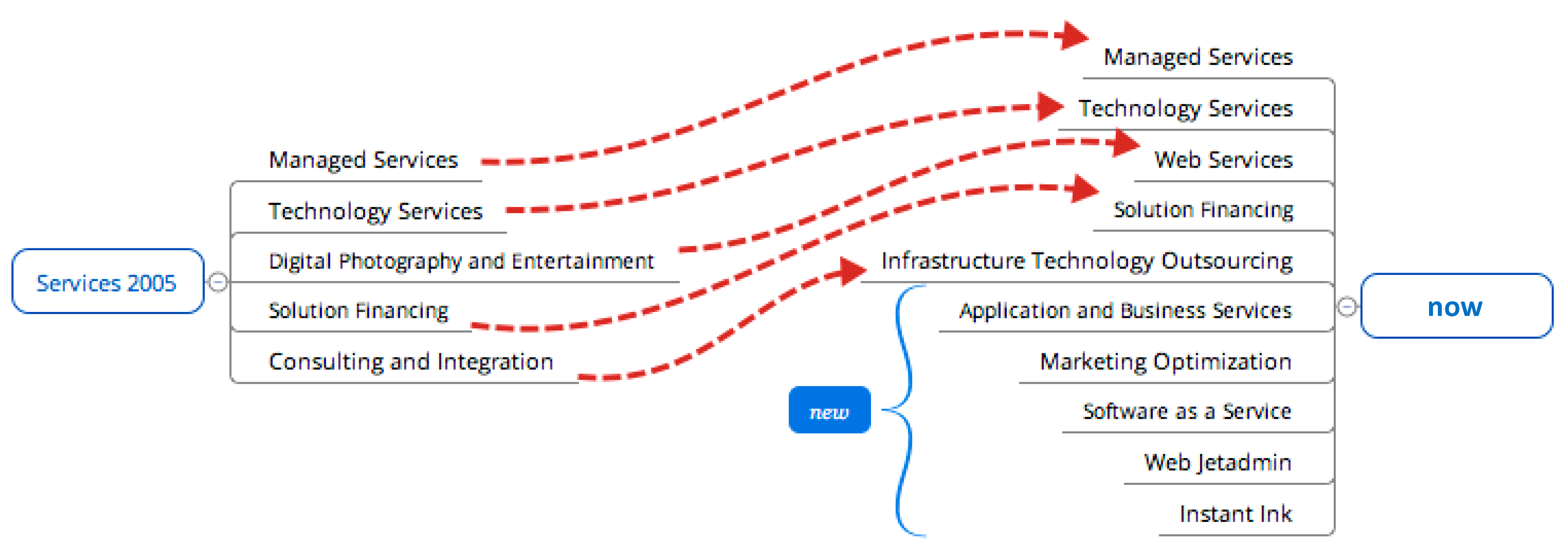

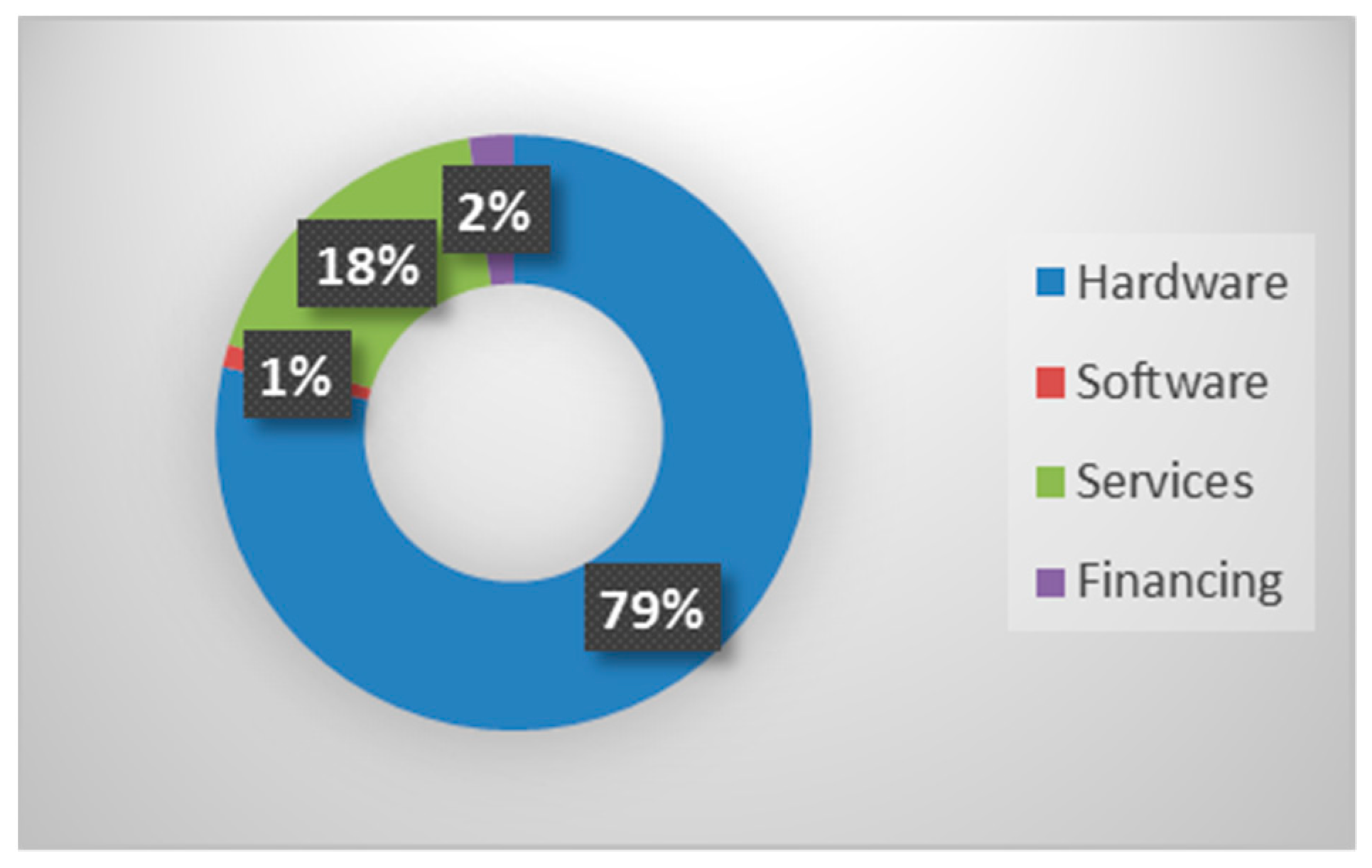

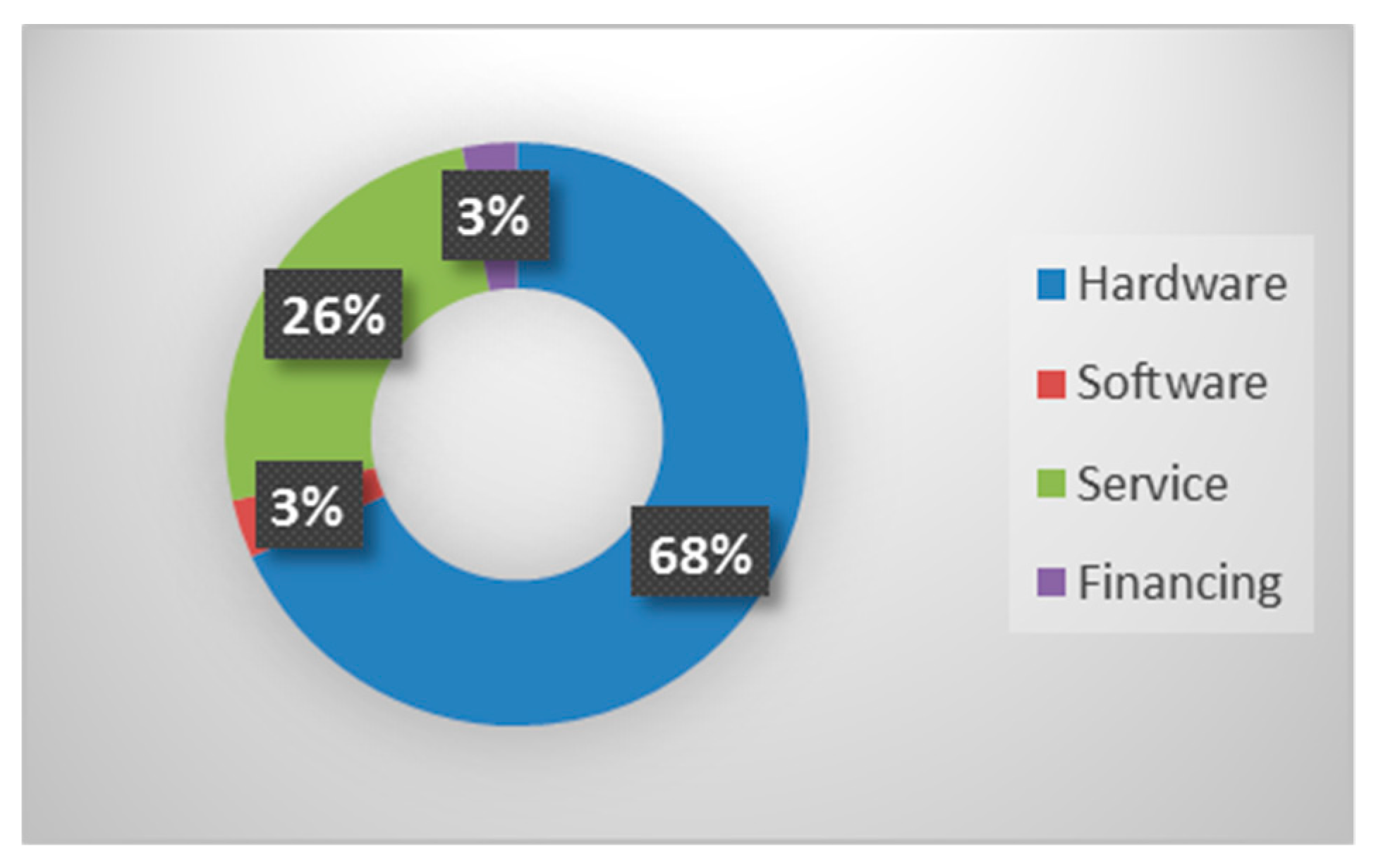

3.3. HP Servitization Scenario

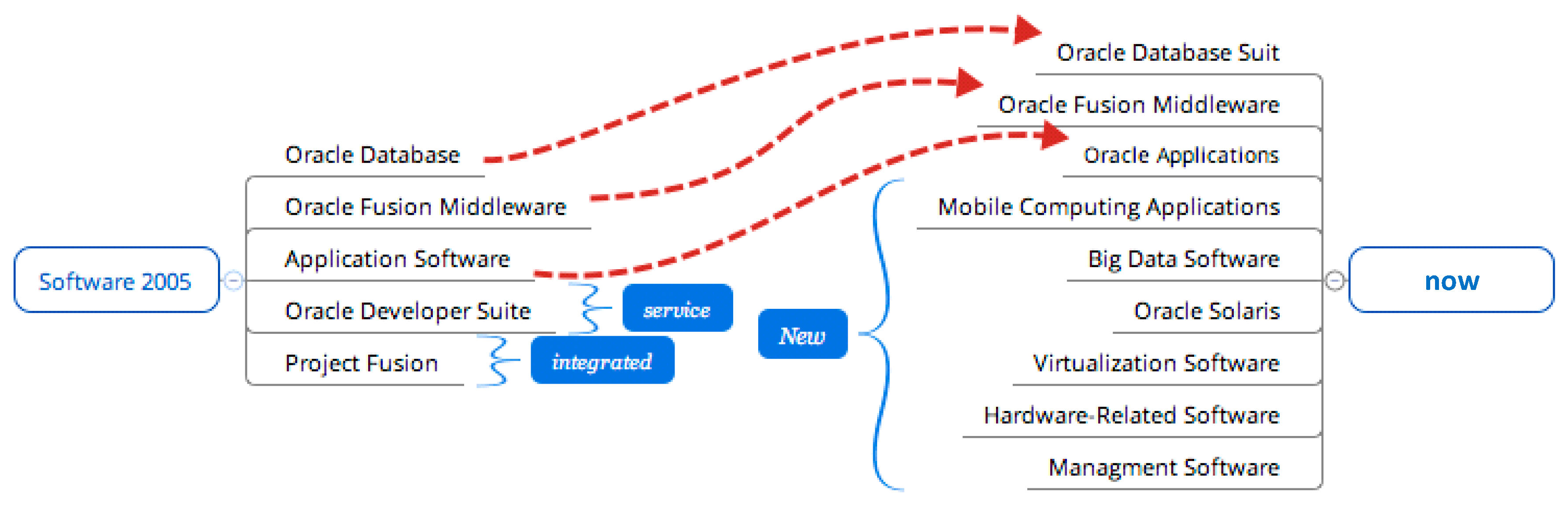

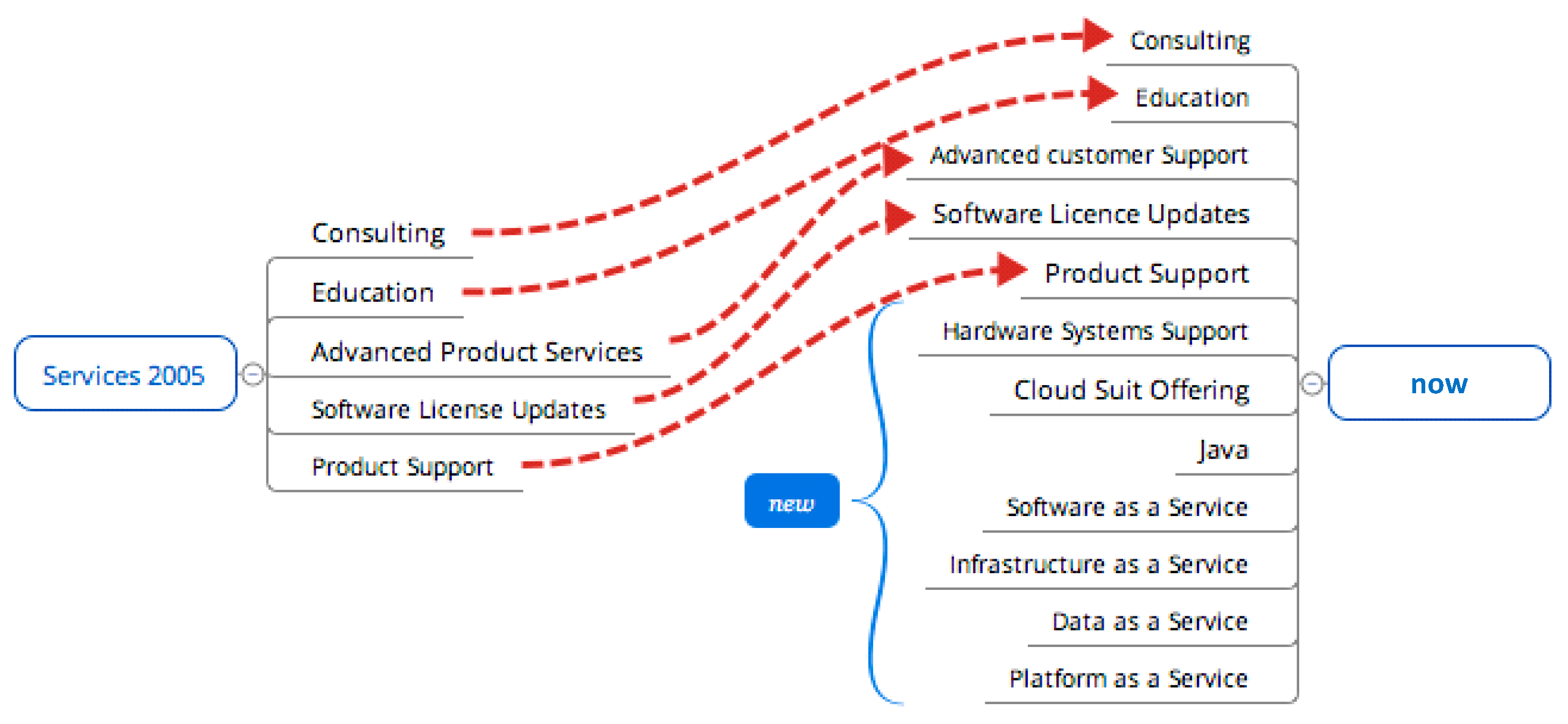

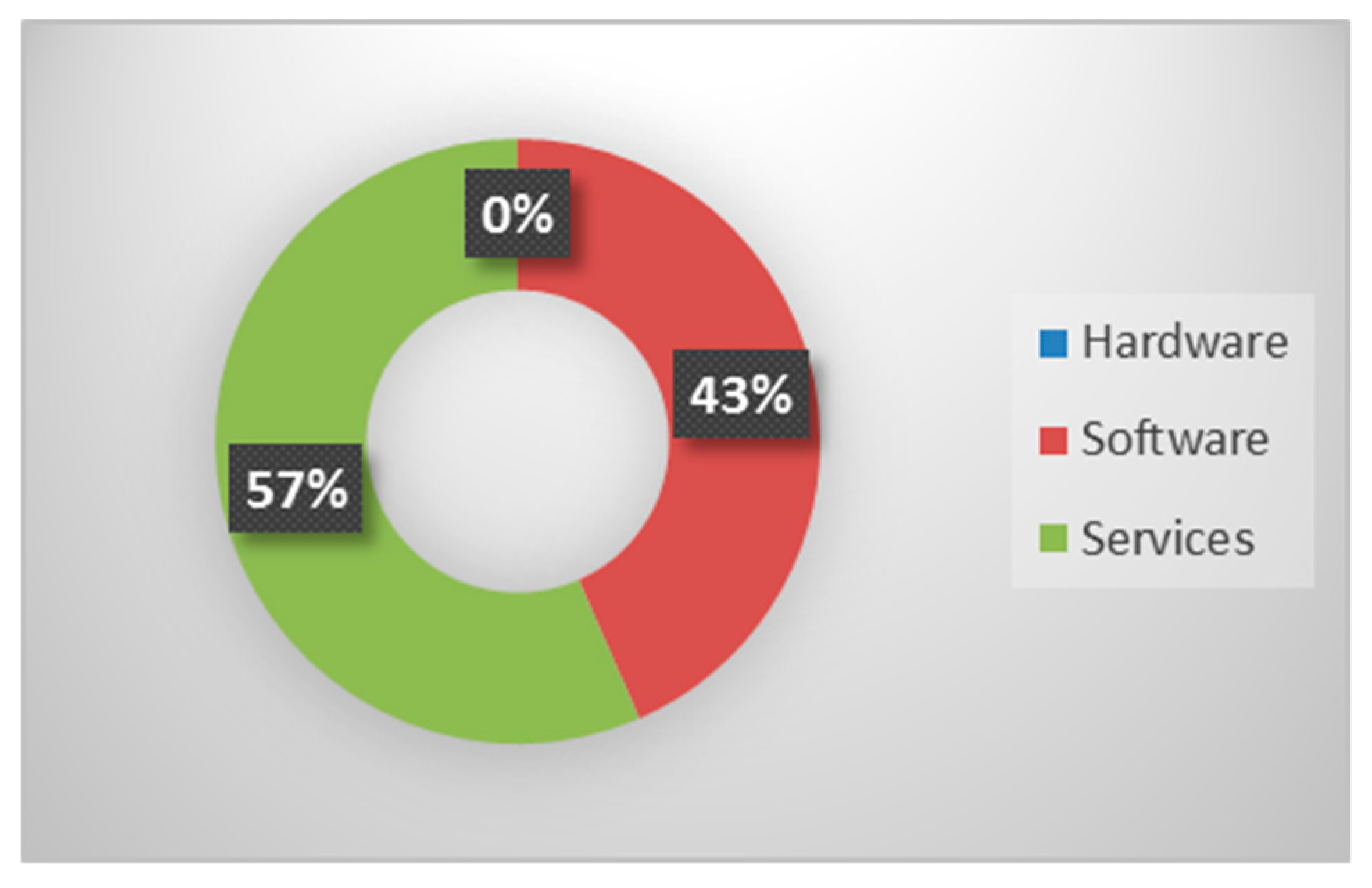

3.4. Oracle Servitization Scenario

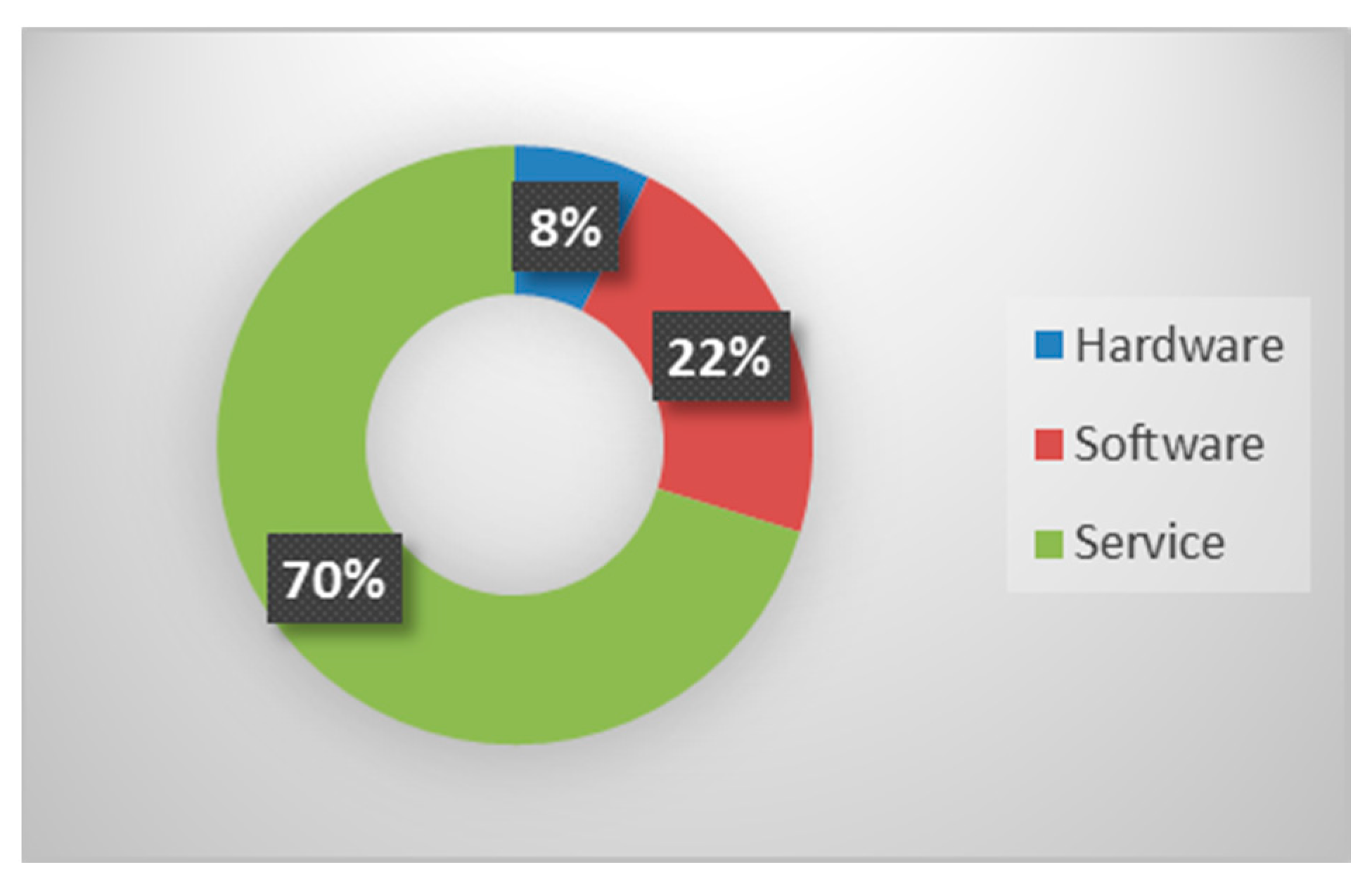

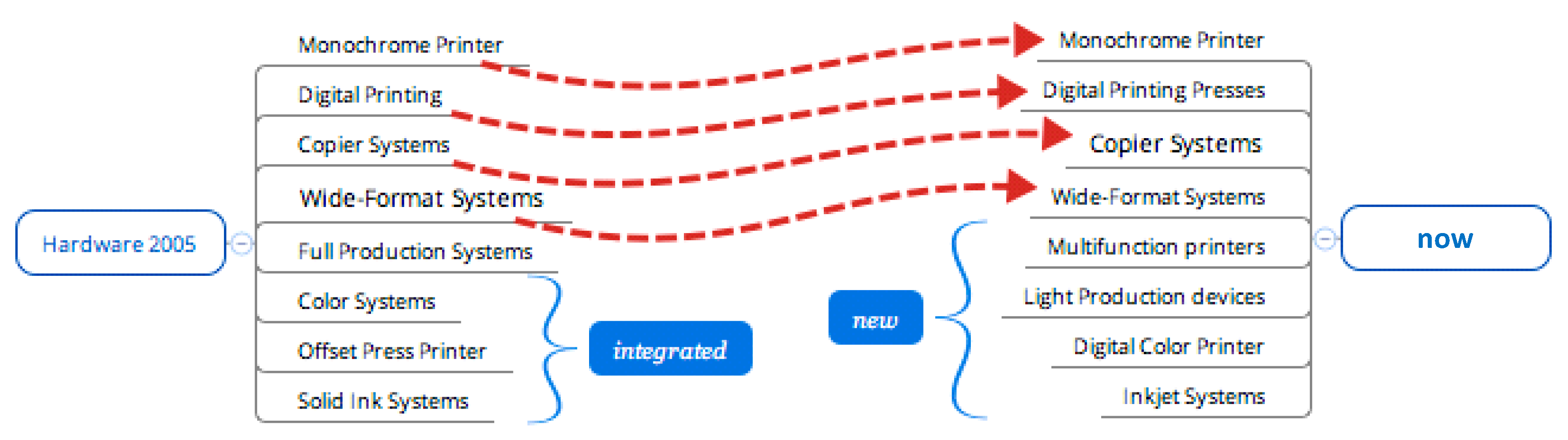

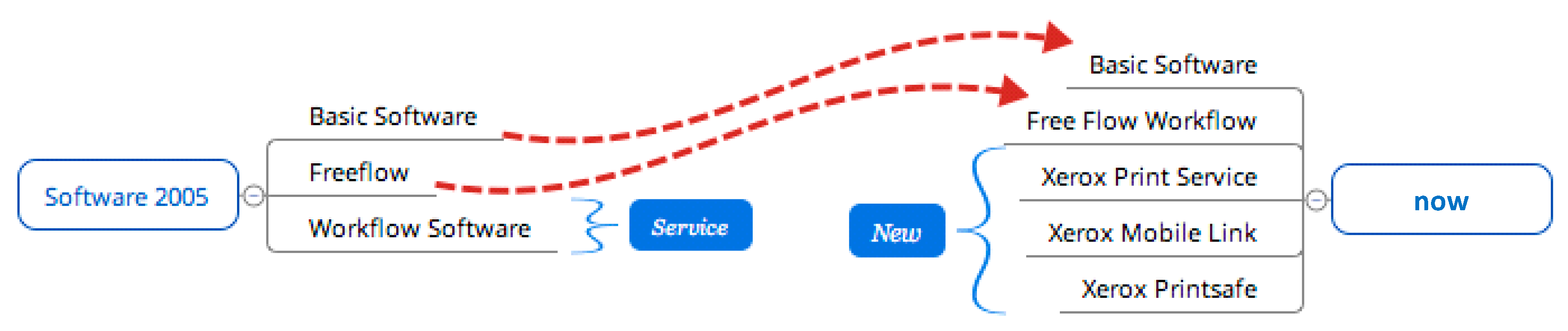

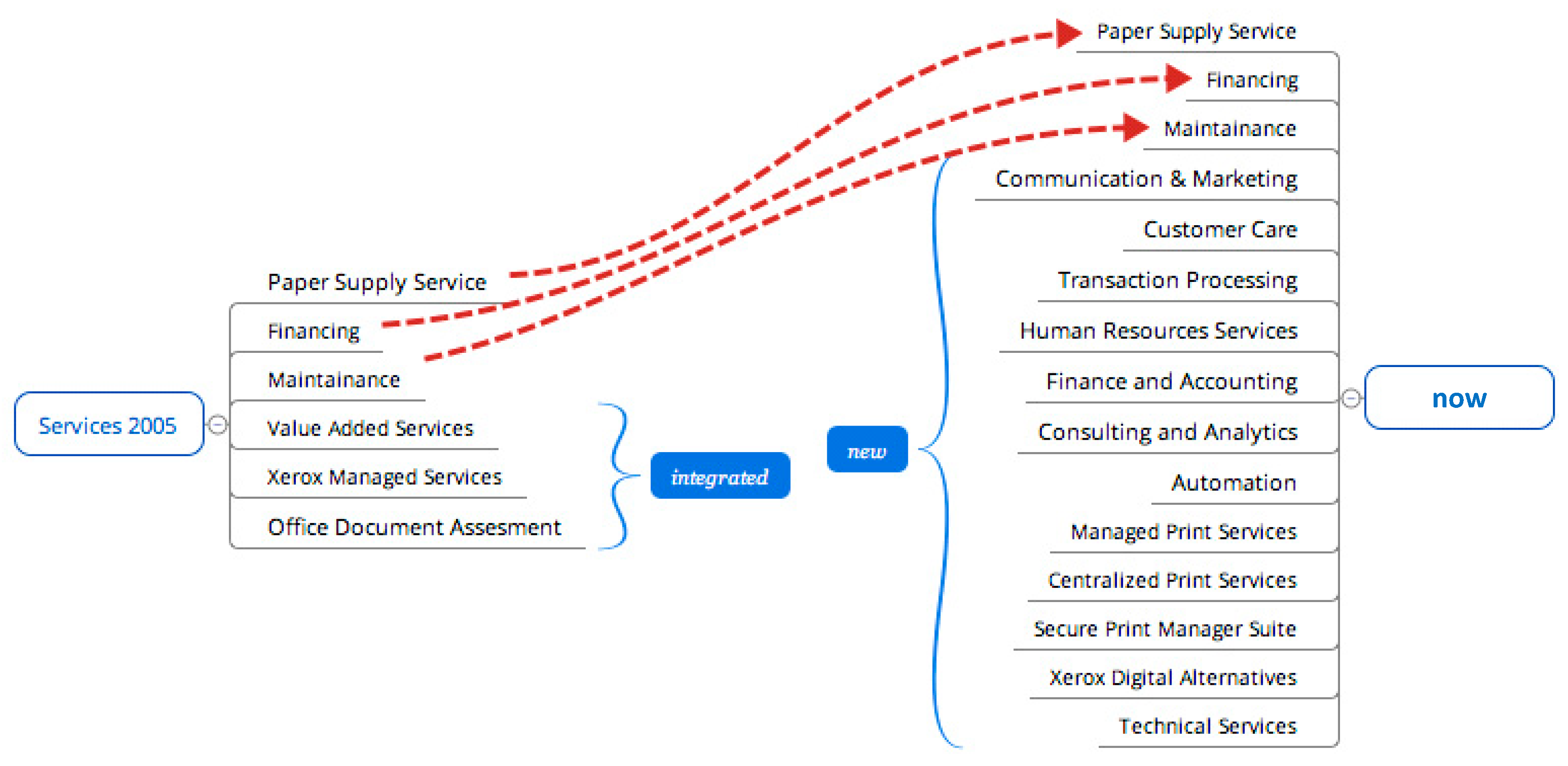

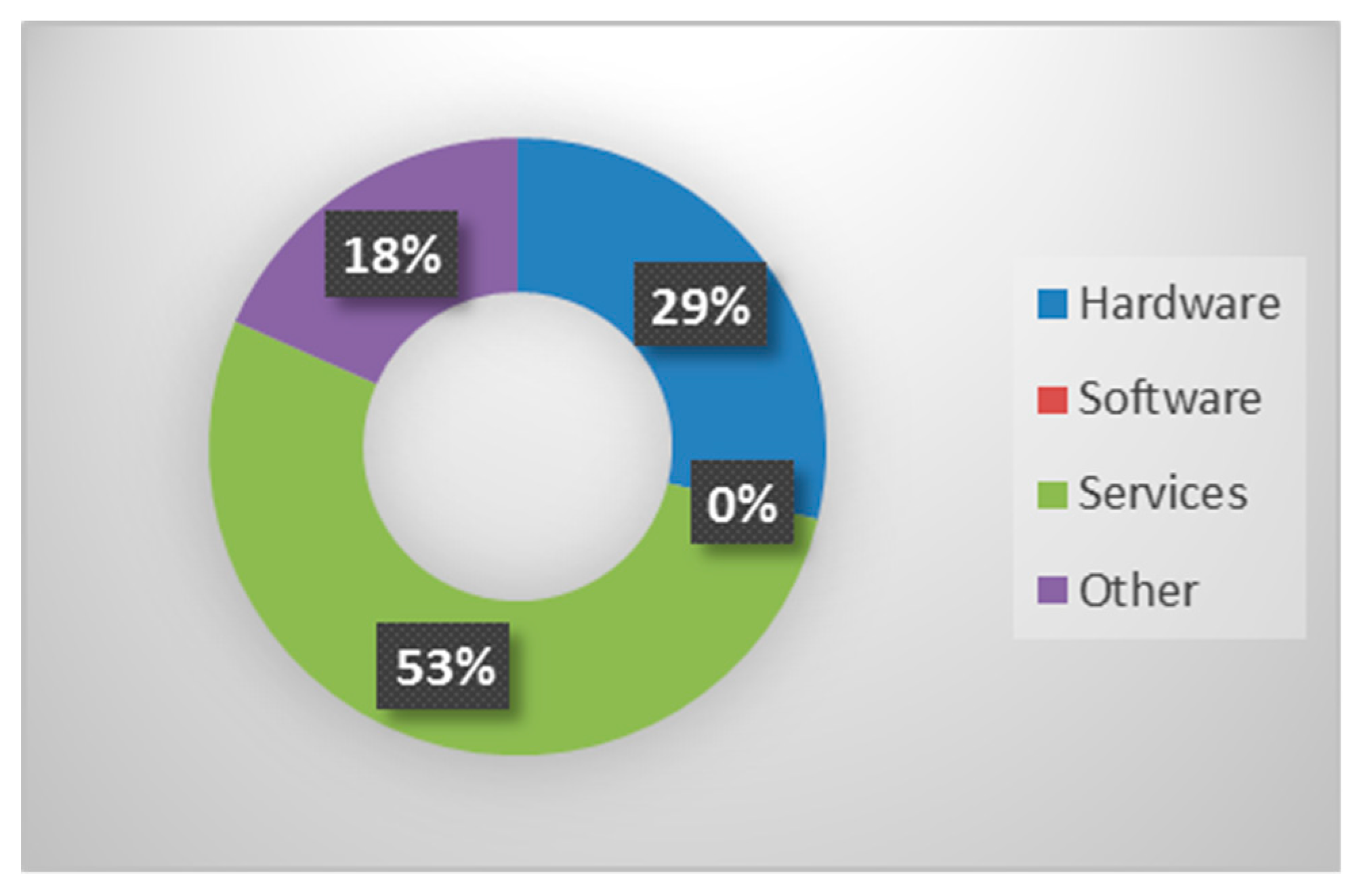

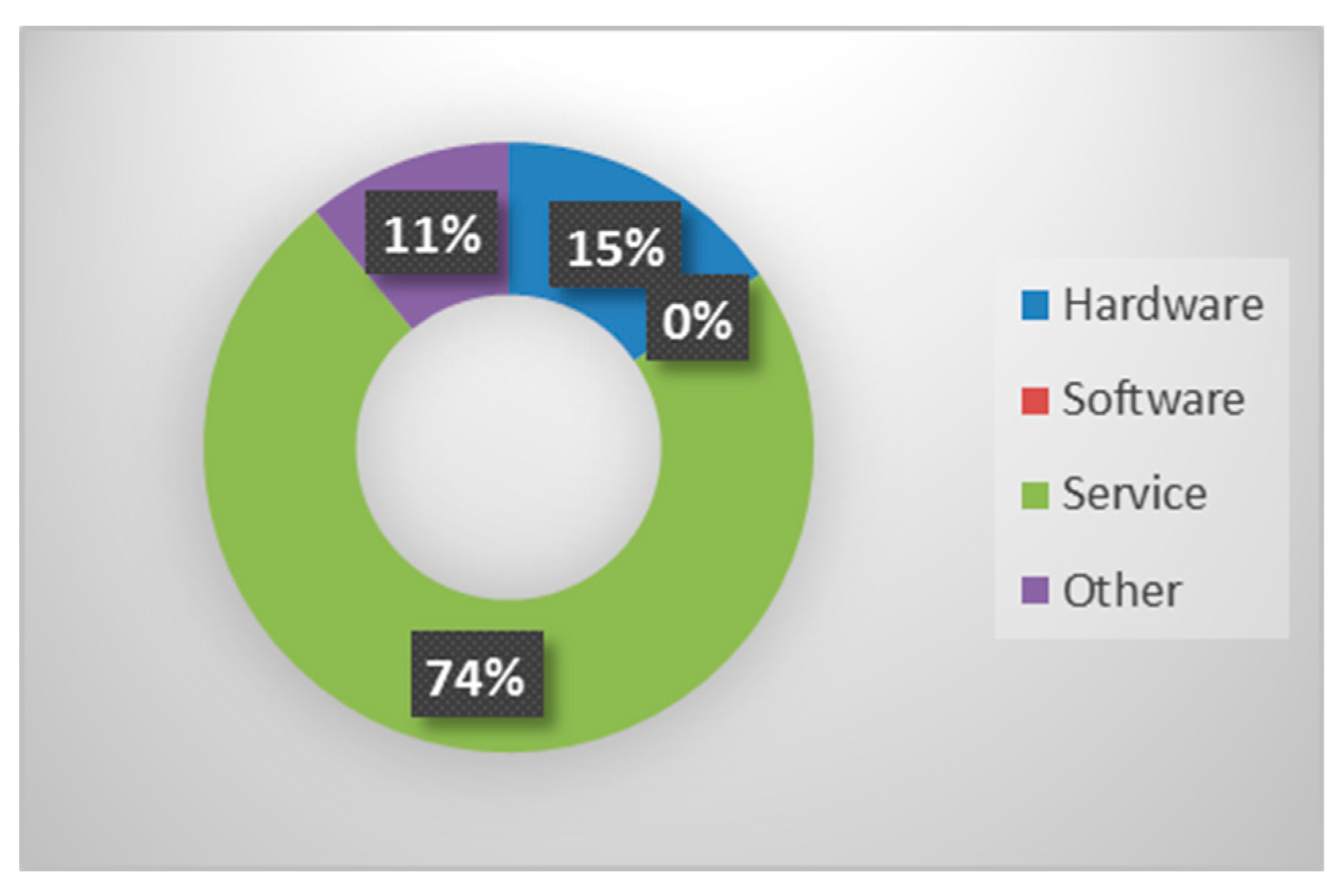

3.5. Xerox Servitization Scenario

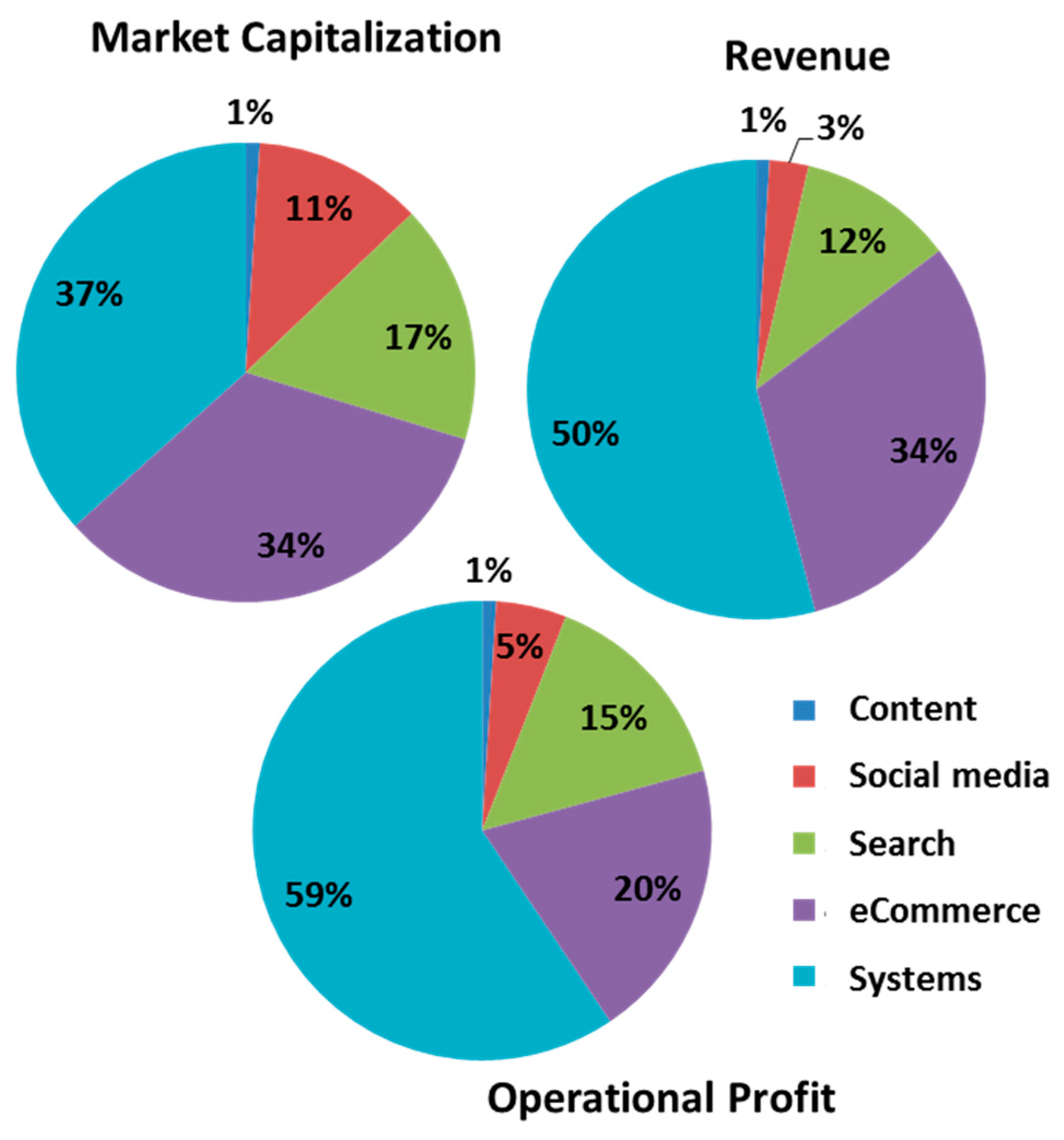

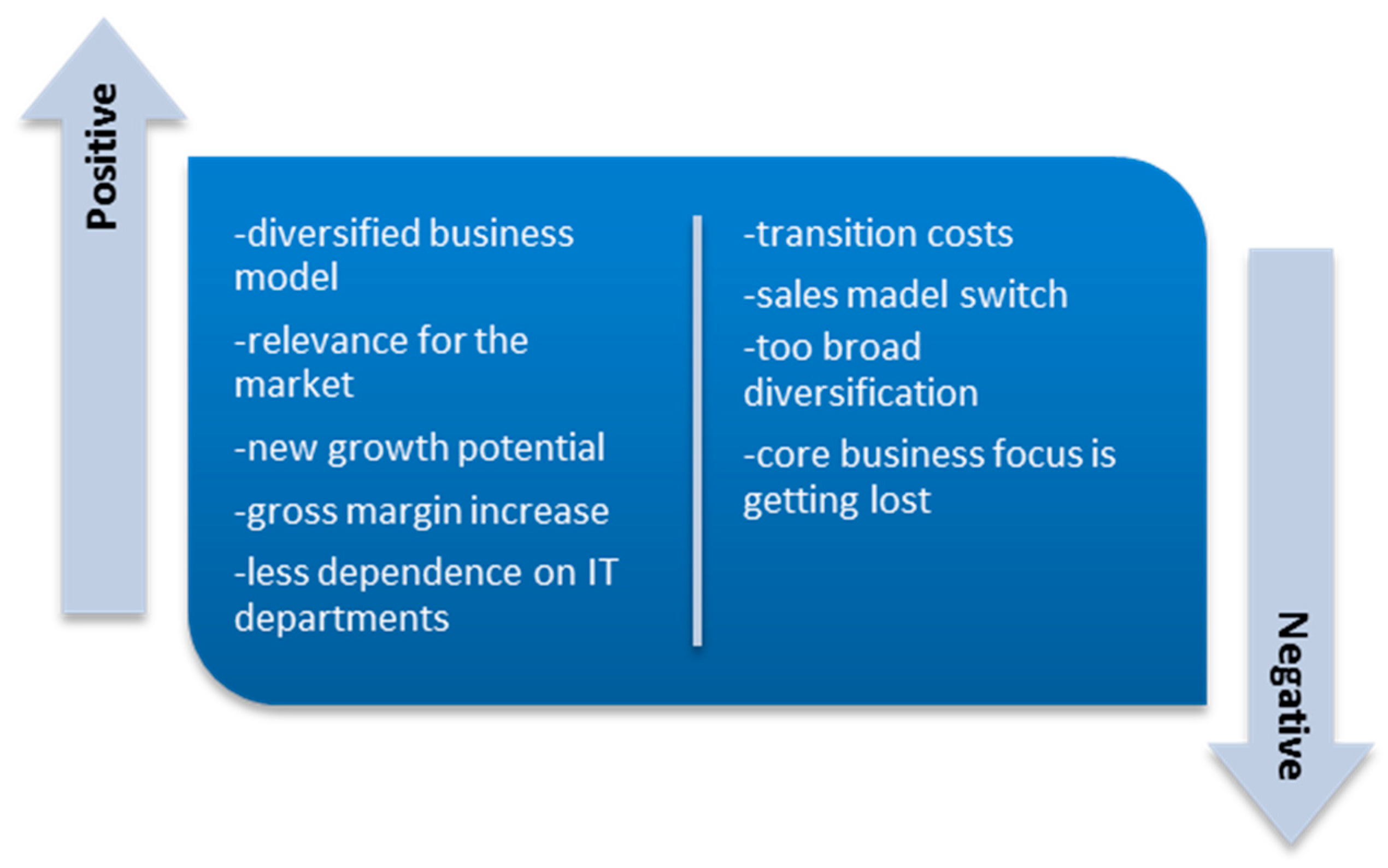

3.6. General Evaluation of Servitization Similarities and Differences by Five Players

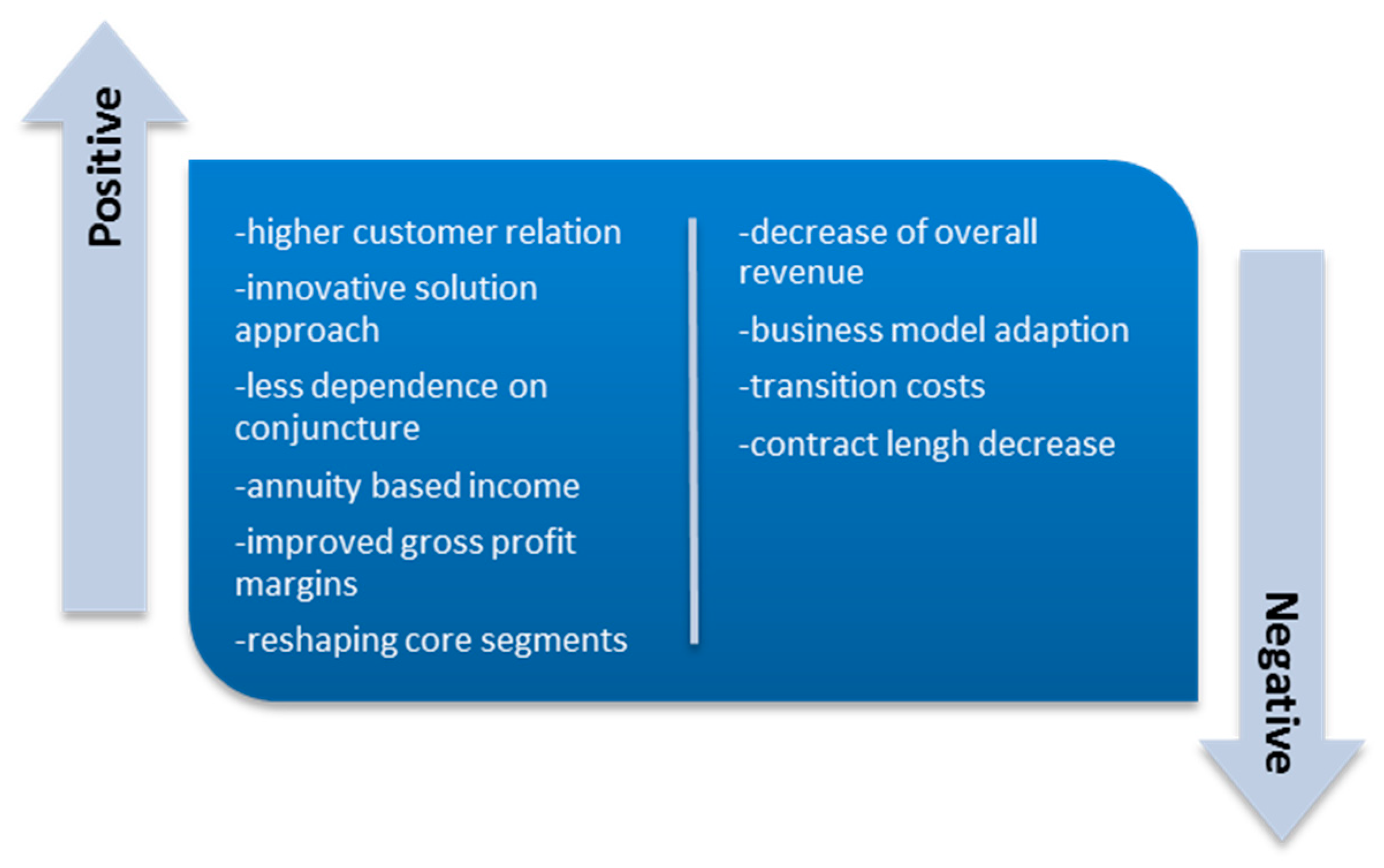

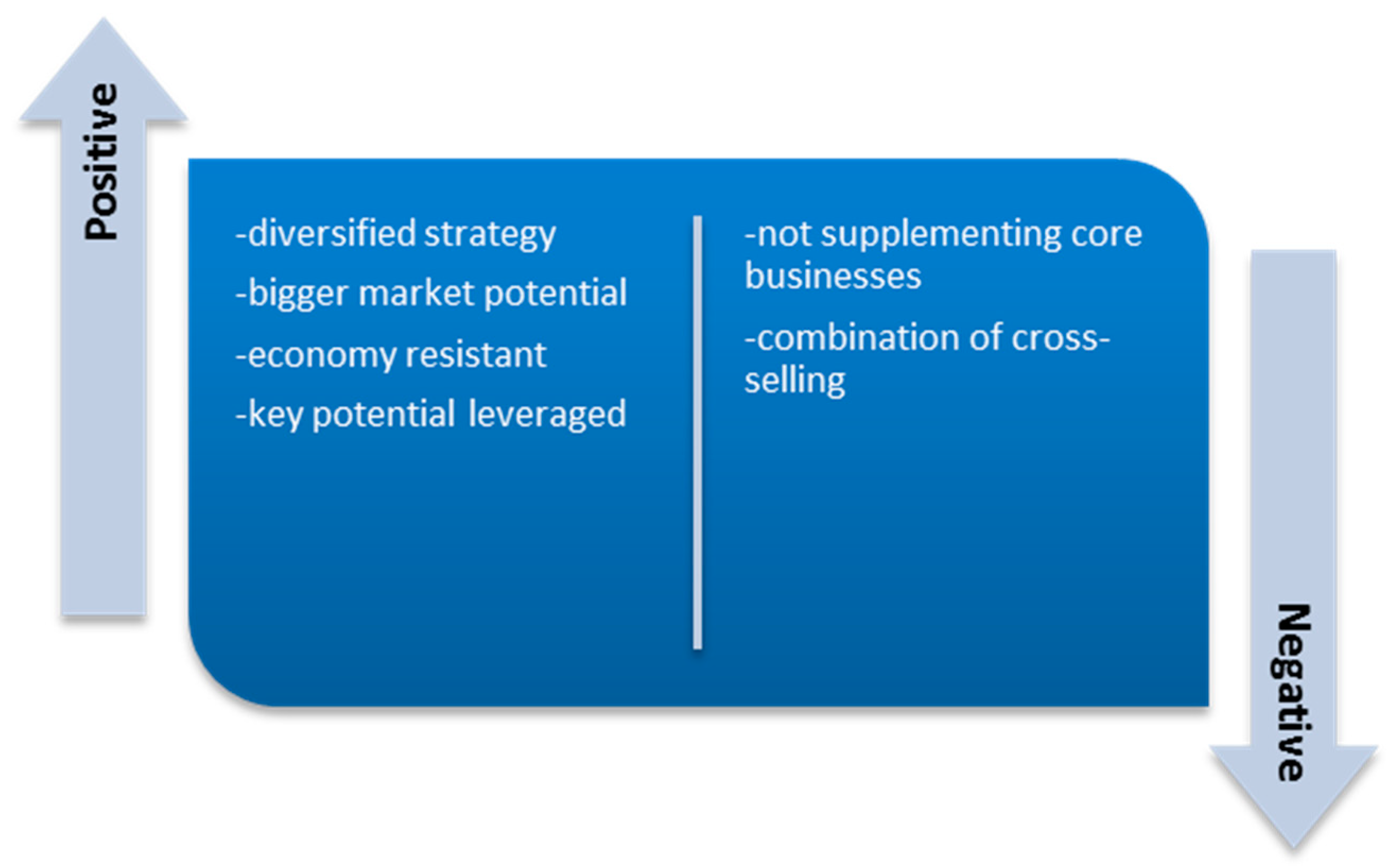

- Market Expansion—All analyzed companies attempted to enter new markets with higher growth potential or higher profit margins by adding services to their portfolios. The approach taken and the market entered depended on the fundamentals of their original core business;

- Transformation of core business—In the last decade, aside from HP, all companies transformed their core businesses, which were either hardware sales or software sales, towards a combination of sales and service delivery. The choice to add services to their core business or increase the importance of the service core business is evidence that Servitization is occurring in the IT industry. Additional evidence is that the growth rate of services has been increasing rapidly;

- Product as a Service—The major players started to offer their customers a new way to interact with them. Instead of buying the products and taking ownership of them, this new method consisted of, depending on the fundamentals of the business, either the rental of the products, as in the cases of IBM, HP and Xerox, or the licensing of/subscribing to the products, as in the cases of Microsoft and Oracle;

- Key Knowledge consulting—Four of the five cases created a new revenue stream, which was generated by offering their accumulated business knowledge to their business model. IBM and HP offered their knowledge of IT infrastructure and helped optimize costs for their customers. Oracle started consultations based on their vast knowledge of data management and the increase in big data analytics;

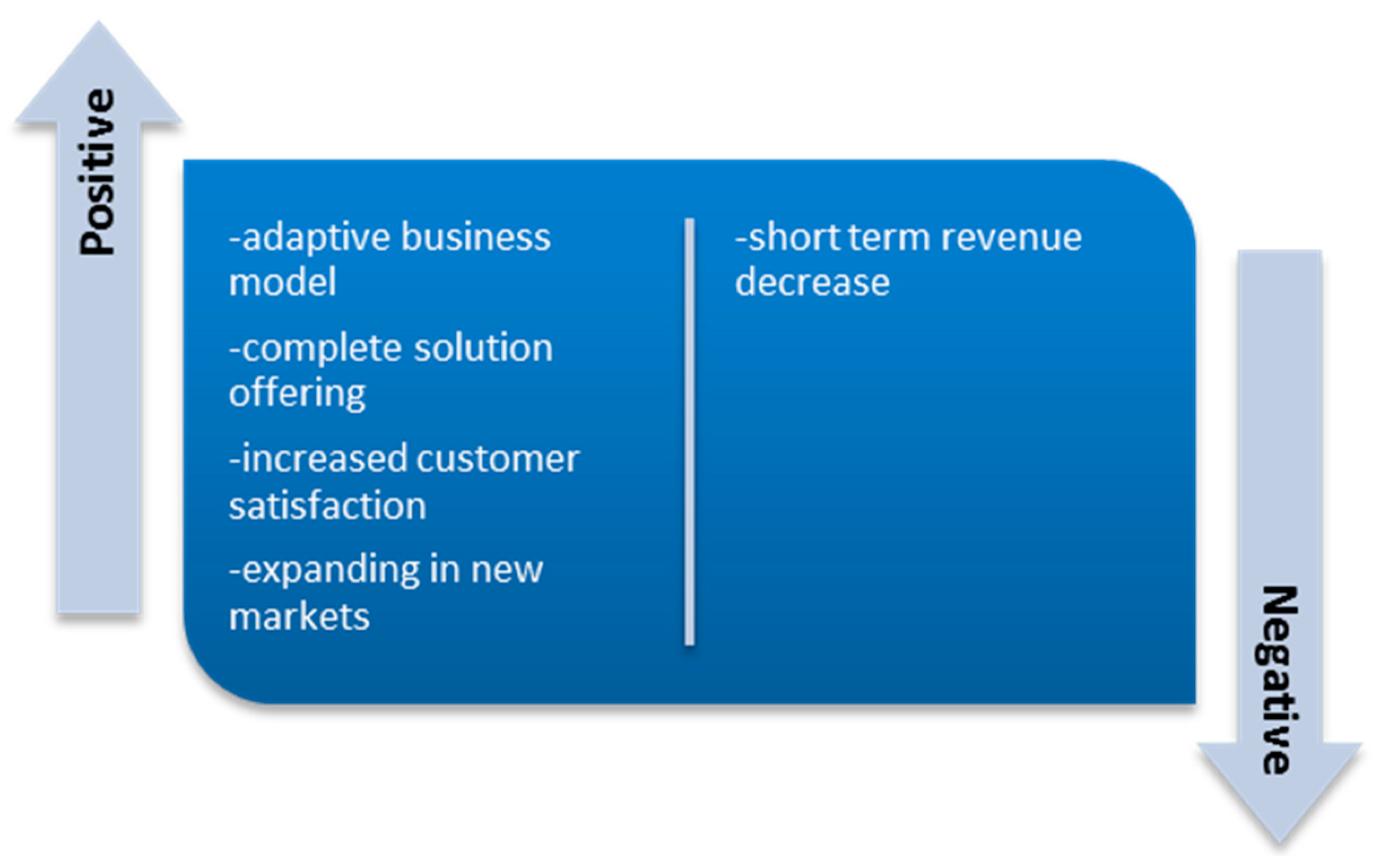

- Acquisition Integration Challenge—Major switches in business segments were usually triggered by large acquisitions by the companies analyzed. These acquisitions often required a rethinking of the business models of the companies and a long internal integration processes to improve customer satisfaction and return profits.

- Change of PSS—Invariably there was a visible change in their orientation towards a more service dominant PSS. Most companies started with a product-oriented PSS and switched to a use-oriented PSS. In several cases, they took it a step further, to a results-oriented PSS, which is mostly performed by the companies whose foundation was in hardware.

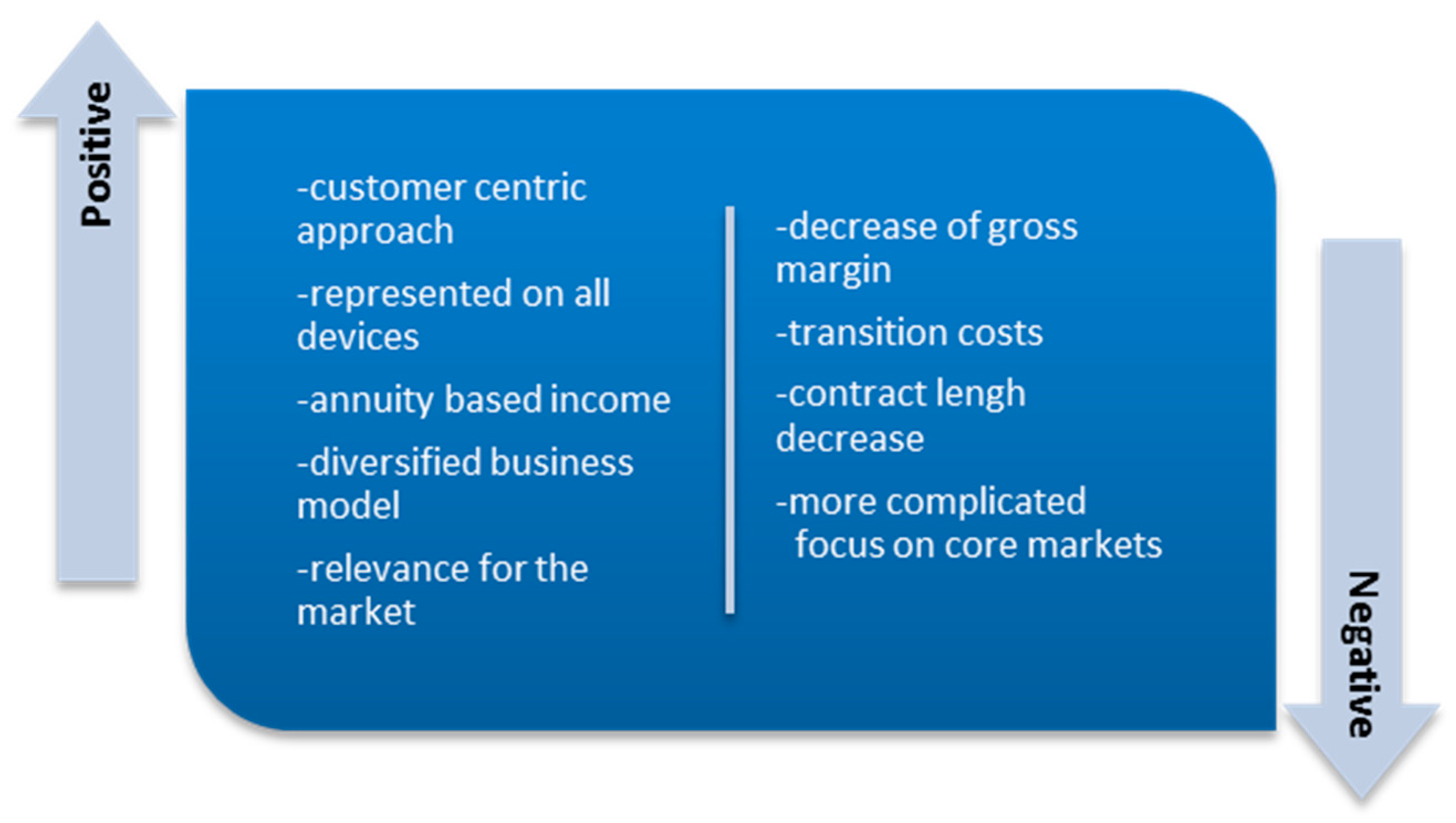

- Separation and Integration—One of the key differences is in the approach companies took towards Servitization. Hardware IT companies first diversified their portfolio with services and then started to separate or disinvest certain product lines to strengthen their new core businesses. Software IT companies previously had a strong mix of software and services and diversified their businesses to include some hardware, to increase their interaction with customers and the synergies of their all-round solutions;

- Cloud Services—Another difference was in the approach to cloud services. Three of the five companies included cloud services as a major segment with growth potential. Notably, Microsoft and Oracle integrated cloud services as the future of their business strategy. IBM integrated cloud services as support and a possible future trend to aid their customers in going digital.

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Digitalization will Transform the Global Economy-Policy Briefs-IIASA. Available online: http://www.iiasa.ac.at/web/home/resources/publications/IIASAPolicyBriefs/pb20.html (accessed on 26 January 2019).

- Gada, K. The Digital Economy In 5 Minutes. Forbes. Available online: https://www.forbes.com/sites/koshagada/2016/06/16/what-is-the-digital-economy/ (accessed on 26 January 2019).

- The MIT Initiative on the Digital Economy (IDE), MIT Sloan School of Management. A Year of Impact—2018 in Review. Available online: http://ide.mit.edu/sites/default/files/MIT2018report-final-digital_0.pdf (accessed on 26 January 2019).

- Bukht, R.; Heeks, R. Defining, Conceptualising and Measuring the Digital Economy. Working Paper Series Development Informatics, Developed as Part of DIODE: The Development Implications of Digital Economies Strategic Research Network; UK’s Economic and Social Research Council: Swindon, UK, 2017. [Google Scholar]

- Kryvinska, N.; Kaczor, S.; Strauss, C.; Gregus, M. Servitization Strategies and Product-Service-Systems. In Proceedings of the 2014 IEEE World Congress on Services, Anchorage, AK, USA, 27 June–2 July 2014; pp. 254–260. [Google Scholar]

- Bickel, L.; Kryvinska, N. Comparative Analysis of Two Operational Developments within IT Companies’ Servitization—Microsoft and HP. In Proceedings of the 2017 IEEE 5th International Conference on Future 751 Internet of Things and Cloud (FiCloud), Prague, Czech Republic, 21–23 August 2017; pp. 249–256. [Google Scholar]

- Bickel, L.; Kryvinska, N. IBM Case Analysis by Servitization in IT Industry. In Advances in Intelligent Networking and Collaborative Systems (INCoS); Springer: Berlin/Heidelberg, Germany, 2017; pp. 380–388. [Google Scholar]

- Bickel, L.; Kryvinska, N. Servitization Transition in IT Industry—An IBM Scenario Analysis. In Proceedings of the 5th International Conference on Serviceology (ICServ2017), Vienna, Austria, 12–14 July 2017; pp. 295–298. [Google Scholar]

- Kaczor, S.; Kryvinska, N. It is all about Services-Fundamentals, Drivers, and Business Models. Soc. Serv. Sci. J. Serv. Sci. Res. 2013, 5, 125–154. [Google Scholar] [CrossRef]

- Kaczor, S.; Kryvinska, N.; Strauss, C. Pitfalls in Servitization and Managerial Implications. In Proceedings of the Global Conference on Services Management (GLOSERV 2017), Volterra, Tuscany, Italy, 3–7 October 2017; pp. 115–119. [Google Scholar]

- Kryvinska, N.; Kaczor, S.; Strauss, C.; Greguš, M. Servitization-Transition from Manufacturer to Service Provider In the Service Dominant Logic, Network and Systems Theory and Service Science: Integrating three Perspectives for a New Service Agenda. In Proceedings of the Naples Forum on Service 2015, Naples, Italy, 9–12 June 2015. [Google Scholar]

- Kryvinska, N.; Strauss, C.; Kaczor, S. A Scientometric Analysis of Back-end and Front-end Solutions for the Challenges on Enterprises’ Servitization in Digital Era. Comput. Ind. Eng. under review.

- Avlonitis, V.; Frandsen, T.; Hsuan, J.; Karlsson, C. Driving Competitiveness Through Servitization—A Guide for Practitioners. In The CBS Competitiveness Platform, 1st ed.; Copenhagen Business School: Frederiksberg, Denmark, 2014; ISBN 978-87-93226-03-6. [Google Scholar]

- Marks, F.; Ramselaar, L.; Mulder, J.; Muller, H.; Langkamp, S.; Boymans, C. Seeing Things Differently-Servitization in product companies, Creating business value beyond products. In White Paper; Atos Consulting: Bezon, France, 2011. [Google Scholar]

- RapidBI. Critical Success Factors CSF—Analysis. 12 May 2016. Available online: https://rapidbi.com/criticalsuccessfactors/ (accessed on 26 January 2019).

- Rockart, J.F. Chief executives define their own data needs. Harv. Bus. Rev. 1979, 57, 81–93. [Google Scholar] [PubMed]

- Daniel, D.R. Management Information Crisis. Harv. Bus. Rev. 1961, 39, 111–121. [Google Scholar]

- Le Breton, P.P. The Case Study Method and the Establishment of Standards of Efficiency. Acad. Manag. Proc. 1956, 103–104. [Google Scholar] [CrossRef]

- Kreye, M.E.; Jensen, P.L. Key variables of organisation design in servitization. In Proceedings of the 21st International EurOMA Conference European Operations Management Association, Palermo, Italy, 20–25 June 2014. [Google Scholar]

- Martinez, V.; Neely, A.; Urmetzer, F. Seven Critical Success Factors in the Shift to Services. p. 16. Available online: https://www.ifm.eng.cam.ac.uk/insights/servitization/619454seven-critical-success-factors-in-the-shift-to-services/ (accessed on 26 January 2019).

- Servadio, L.; Nordin, F. Critical issues during servitization: An in-depth case study. In Proceedings of the AMA Servsig, International Service Research Conference, Hanken School of Economics, Helsinki, Finland, 7–9 June 2012. [Google Scholar]

- Oláh, J.; Popp, J.; Máté, D. An Examination of Servitization as a Breakthrough Success Factor Along The Supply Chain. SEA-Pract. Appl. Sci. 2017, 15, 373–379. [Google Scholar]

- Smith, A. Wealth of Nations; Library of Economics and Liberty: Indianapolis, IN, USA, 1766; Available online: http://www.econlib.org/library/Smith/smWN.html (accessed on 18 January 2019).

- Parry, G.; Newnes, L.; Huang, X. Goods, Products and Services. In Service Design and Delivery; Springer: Boston, MA, USA, 2011; pp. 19–29. [Google Scholar]

- Gronroos, C. Service Management and Marketing: Customer Management in Service Competition, 3rd ed.; Wiley: Hoboken, NJ, USA, 2007. [Google Scholar]

- Moeller, S. Characteristics of services—A new approach uncovers their value. J. Serv. Mark. 2010, 24, 359–368. [Google Scholar] [CrossRef]

- Shostack, G.L. Breaking Free from Product Marketing. J. Mark. 1977, 41, 73–80. [Google Scholar] [CrossRef]

- Lovelock, C.; Gummesson, E. Whither Services Marketing? In Search of a New Paradigm and Fresh Perspectives. J. Serv. Res. 2004, 7, 20–41. [Google Scholar] [CrossRef] [Green Version]

- Edvardsson, B. Service quality: Beyond cognitive assessment. Manag. Serv. Qual. Int. J. 2005, 15, 127–131. [Google Scholar] [CrossRef]

- Pernul, G. Trust for Digital Products. In Computer Vision—ECCV 2012; Springer: Berlin/Heidelberg, Germany, 2003; pp. 1–5. [Google Scholar]

- Hill, P. Tangibles, Intangibles and Services: A New Taxonomy for the Classification of Output. Can. J. Econ. Rev. Can. Econ. 1999, 32, 426–446. [Google Scholar] [CrossRef]

- Vandermerwe, S.; Rada, J. Servitization of business: Adding value by adding services. Eur. Manag. J. 1988, 6, 314–324. [Google Scholar] [CrossRef]

- Vandermerwe, S.; Matthews, W.; Rada, J. European Manufacturers Shape Up for Services. J. Bus. Strategy 1989, 10, 42–46. [Google Scholar] [CrossRef]

- Wise, R.; Baumgartner, P. Go Downstream: The New Profit Imperative in Manufacturing. Harvard Bus. Rev. 1999. Available online: https://hbr.org/1999/09/go-downstream-the-new-profit-imperative-in-manufacturing (accessed on 21 January 2019).

- Lay, G. Servitization in Industry; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar]

- Baines, T.S.; Lightfoot, H.W.; Benedettini, O.; Kay, J.M. The servitization of manufacturing: A review of literature and reflection on future challenges. J. Manuf. Technol. Manag. 2009, 20, 547–567. [Google Scholar] [CrossRef] [Green Version]

- Vandermerwe, S. The market power is in the services: Because the value is in the results. Eur. Manag. J. 1990, 8, 464–473. [Google Scholar] [CrossRef]

- Festo Corp. Customer Specific Solutions; Festo: Esslingen, Germany, 2008; Available online: https://www.festo.com/rep/en-ca_ca/assets/Customer_Solutions_Brochure.pdf (accessed on 10 January 2019).

- McKinsey. Solution Selling—Is the Pain wort the Gain? McKinsey & Company: New York, NY, USA, 2003; Volume 4. [Google Scholar]

- Stremersch, S.; Tellis, G.J. Strategic Bundling of Products and Prices: A New Synthesis for Marketing. J. Mark. 2002, 66, 55–72. [Google Scholar] [CrossRef] [Green Version]

- Davies, A.; Brady, T.; Hobday, M. Organizing for solutions: Systems seller vs. systems integrator. Ind. Mark. Manag. 2007, 36, 183–193. [Google Scholar] [CrossRef] [Green Version]

- Tukker, A. Eight types of product–service system: Eight ways to sustainability? Experiences from SusProNet. Bus. Strategy Environ. 2004, 13, 246–260. [Google Scholar] [CrossRef]

- Neely, A. Exploring the financial consequences of the servitization of manufacturing. Oper. Manag. Res. 2008, 1, 103–118. [Google Scholar] [CrossRef] [Green Version]

- Baines, T.; Lightfoot, H. (Eds.) Made to Serve: How Manufacturers Can Compete Through Servitization and Product-Service Systems; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2012. [Google Scholar]

- Britchfield, G. State-of-the-Art in Product-Service Systems. 2013. Available online: https://uldamienobrien.wordpress.com/2013/10/12/state-of-the-art-in-product-service-systems/ (accessed on 17 January 2019).

- Kazman, R.; Carrière, S.J.; Woods, S.G. Toward a discipline of scenario-based architectural engineering. Ann. Softw. Eng. 2000, 9, 5–33. [Google Scholar] [CrossRef]

- Sutcliffe, A. Scenario-based requirements analysis. Requir. Eng. 1998, 3, 48–65. [Google Scholar] [CrossRef]

- Kazman, R.; Abowd, G.; Bass, L.; Clements, P. Scenario-based analysis of software architecture. IEEE Softw. 1996, 13, 47–55. [Google Scholar] [CrossRef] [Green Version]

- Bonilla, S.H.; Silva, H.R.O.; Terra da Silva, M.; Franco Gonçalves, R.; Sacomano, J.B. Industry 4.0 and Sustainability Implications: A Scenario-Based Analysis of the Impacts and Challenges. Sustainability 2018, 10, 3740. [Google Scholar] [CrossRef] [Green Version]

- Carrol, J.M. Five reasons for scenario-based design. In Proceedings of the 32nd Annual Hawaii International Conference on Systems Sciences. 1999. HICSS-32. Abstracts and CD-ROM of Full Papers, Maui, HI, USA, 5–8 January 1999. [Google Scholar]

- Vrakopoulou, M.; Li, B.; Mathieu, J.L. Chance Constrained Reserve Scheduling Using Uncertain Controllable Loads Part I: Formulation and Scenario-Based Analysis. IEEE Trans. Smart Grid 2019, 10, 1608–1617. [Google Scholar] [CrossRef]

- Goeke, L.; Pousttchi, K. A Scenario-Based Analysis of Mobile Payment Acceptance. In Proceedings of the 2010 Ninth International Conference on Mobile Business and 2010 Ninth Global Mobility Roundtable (ICMB-GMR), Athens, Greece, 13–15 June 2010; pp. 371–378. [Google Scholar]

- IBM Corp. 2005 Annual Report. Available online: Ftp://public.dhe.ibm.com/annualreport/2005/2005_ibm_annual.pdf (accessed on 7 January 2019).

- IBM Corp. 2006 Annual Report. Available online: Ftp://public.dhe.ibm.com/annualreport/2006/2006_ibm_annual.pdf (accessed on 7 January 2019).

- IBM Corp. 2007 Annual Report. Available online: Ftp://public.dhe.ibm.com/annualreport/2007/2007_ibm_annual.pdf (accessed on 7 January 2019).

- IBM Corp. 2008 Annual Report. Available online: Ftp://public.dhe.ibm.com/annualreport/2008/2008_ibm_annual.pdf (accessed on 7 January 2019).

- IBM Corp. 2009 Annual Report. Available online: https://www.ibm.com/annualreport/2009/2009_ibm_annual.pdf (accessed on 7 January 2019).

- IBM Corp. 2010 Annual Report. Available online: Ftp://public.dhe.ibm.com/annualreport/2010/2010_ibm_annual.pdf (accessed on 7 January 2019).

- IBM Corp. 2011 Annual Report. Available online: https://www.ibm.com/annualreport/2011/bin/assets/2011_ibm_annual.pdf (accessed on 7 January 2019).

- IBM Corp. 2012 Annual Report. Available online: https://www.ibm.com/annualreport/2012/bin/assets/2012_ibm_annual.pdf (accessed on 8 January 2019).

- IBM Corp. 2013 Annual Report. Available online: https://www.ibm.com/annualreport/2013/bin/assets/2013_ibm_annual.pdf (accessed on 5 January 2019).

- IBM Corp. 2014 Annual Report. Available online: https://www.ibm.com/annualreport/2014/bin/assets/IBM-Annual-Report-2014.pdf (accessed on 7 January 2019).

- IBM Corp. 2015 Annual Report. Available online: https://www.ibm.com/annualreport/2015/assets/img/2016/02/IBM-Annual-Report-2015.pdf (accessed on 5 January 2019).

- IBM Corp. Available online: http://www.ibm.com/us-en/ (accessed on 5 January 2019).

- Microsoft Corp. 2005 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar05/staticversion/10k_dl_dow.html (accessed on 11 January 2019).

- Microsoft Corp. 2006 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar06/staticversion/10k_dl_dow.html (accessed on 11 January 2019).

- Microsoft Corp. 2007 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar07/staticversion/10k_dl_dow.html (accessed on 11 January 2019).

- Microsoft Corp. 2008 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar08/10k_dl_dow.html (accessed on 11 January 2019).

- Microsoft Corp. 2009 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar09/10k_dl_dow.html (accessed on 11 January 2019).

- Microsoft Corp. 2010 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar10/10k_dl_dow.html (accessed on 11 January 2019).

- Microsoft Corp. 2011 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar11/download_center.html (accessed on 11 January 2019).

- Microsoft Corp. 2012 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar12/download-center/index.html (accessed on 11 January 2019).

- Microsoft Corp. 2013 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar13/download-center/index.html (accessed on 11 January 2019).

- Microsoft Corp. 2014 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar14/download-center.html (accessed on 11 January 2019).

- Microsoft Corp. 2015 Annual Report. Available online: https://www.microsoft.com/investor/reports/ar15/download-center/index.html (accessed on 11 January 2019).

- Microsoft Corp. Available online: https://www.microsoft.com/en-us (accessed on 11 January 2019).

- HP Inc. 2005 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2006/05ar-graphics.pdf (accessed on 5 January 2019).

- HP Inc. 2006 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2007/hp-2006ar.pdf (accessed on 5 January 2019).

- HP Inc. 2007 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2008/hp-annual-report-2007.pdf (accessed on 5 January 2019).

- HP Inc. 2008 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2009/hewlettpackard-2008-ar.pdf (accessed on 5 January 2019).

- HP Inc. 2009 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2010/hewlett-packardannualreport2009.pdf (accessed on 5 January 2019).

- HP Inc. 2010 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2011/hewlett-packard-annual-report-final-pdf.pdf (accessed on 4 January 2019).

- HP Inc. 2011 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2012/2011-annual-report.pdf (accessed on 4 January 2019).

- HP Inc. 2012 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2013/hp-10-kar-searchable.pdf (accessed on 4 January 2019).

- HP Inc. 2013 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2014/hpq-annual-report-2013.pdf (accessed on 4 January 2019).

- HP Inc. 2014 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2015/hpq-annual-report-2014.pdf (accessed on 5 January 2019).

- HP Inc. 2015 Annual Report. Available online: http://h30261.www3.hp.com/~/media/Files/H/HP-IR/documents/reports/2016/2015-form-10k.pdf (accessed on 5 January 2019).

- HP Inc. Available online: http://www.hp.com/country/us/en/welcome.html (accessed on 2 January 2019).

- HP Enterprise Company. Available online: https://www.hpe.com/us/en/home.html (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/8f89365c-f24d-4318-a4eb-76f4369afe8c.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/13409113-9264-4cc2-880b-0608458080ab.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/cc70d156-4a8f-4110-a423-b1908f6af43f.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/73e4159f-767e-4a02-9ced-f38420fb3fe0.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/5890e138-346b-456e-9a0f-0ef3693e9d45.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/fef751b6-6c47-46e6-b96c-cebdba155d6f.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/5ba3ac88-481f-4ef0-98e1-278fc99ac7a5.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/dfeeb28c-b033-4299-88d8-0e58524dfdff.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/34075018-f2c1-4907-9c92-dd96f56f49fa.pdf (accessed on 2 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/495da947-b778-4d53-89be-fa66ffb9c3a9.pdf (accessed on 3 January 2019).

- Oracle Corp. Annual Report. Available online: http://d1lge852tjjqow.cloudfront.net/CIK-0001341439/ee127b2b-13a7-4bdb-a384-d27bb7c5bddb.pdf (accessed on 3 January 2019).

- Oracle Corp. Available online: https://www.oracle.com/index.html (accessed on 3 January 2019).

- Xerox Corp. 2005 Annual Report. Available online: http://www.xerox.com/annualreport/2005/Xerox_Annual_Report_05.pdf (accessed on 8 January 2019).

- Xerox Corp. 2006 Annual Report. Available online: http://www.xerox.com/annualreport/2006/Xerox_Annual_Report_06.pdf (accessed on 8 January 2019).

- Xerox Corp. 2007 Annual Report. Available online: http://www.xerox.com/annualreport/2007/Xerox_Annual_Report_07.pdf (accessed on 8 January 2019).

- Xerox Corp. 2008 Annual Report. Available online: http://www.xerox.com/annualreport/2008/2008_annual_report.pdf (accessed on 8 January 2019).

- Xerox Corp. 2009 Annual Report. Available online: http://www.xerox.com/annual-report-2009/pdfs/2009_Annual_Report.pdf (accessed on 8 January 2019).

- Xerox Corp. 2010 Annual Report. Available online: http://www.xerox.com/annual-report-2010/pdfs/2010_Annual_Report.pdf (accessed on 8 January 2019).

- Xerox Corp. 2011 Annual Report. Available online: https://www.xerox.com/assets/pdf/2011_Annual_Report.pdf (accessed on 8 January 2019).

- Xerox Corp. 2012 Annual Report. Available online: https://www.xerox.com/assets/pdf/partners/studiocom/annual/2012_Xerox_Annual_Report.pdf (accessed on 8 January 2019).

- Xerox Corp. 2013 Annual Report. Available online: http://www.xerox.com/annual-report-2013/assets/xerox-oar-2013-full.pdf (accessed on 8 January 2019).

- Xerox Corp. 2014 Annual Report. Available online: http://www.xerox.com/annual-report-2014/assets/Xerox2014AnnualReport.pdf (accessed on 8 January 2019).

- Xerox Corp. 2015 Annual Report. Available online: http://www.xerox.com/annual-report-2015/pdfs/Xerox-2015-Annual-Report.pdf (accessed on 8 January 2019).

- Xerox Corp. Available online: http://www.xerox.com (accessed on 8 January 2019).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Transmutable | slight changes create new goods with different features |

| Non-rival | the use of one person does not decrease its usefulness to others |

| Indestructible | using it will not wear off the product |

| Infinitely reproducible | it can be easily reproduced, and every copy is the same as the original |

| Indivisible | there can only be an entire product because the code would be broken if you split it in half |

| Virtual | they are only accessible over a network |

| Invaluable | difficult to put a monetary value on them as duplication is unlimitedly possible |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kryvinska, N.; Bickel, L. Scenario-Based Analysis of IT Enterprises Servitization as a Part of Digital Transformation of Modern Economy. Appl. Sci. 2020, 10, 1076. https://doi.org/10.3390/app10031076

Kryvinska N, Bickel L. Scenario-Based Analysis of IT Enterprises Servitization as a Part of Digital Transformation of Modern Economy. Applied Sciences. 2020; 10(3):1076. https://doi.org/10.3390/app10031076

Chicago/Turabian StyleKryvinska, Natalia, and Lukas Bickel. 2020. "Scenario-Based Analysis of IT Enterprises Servitization as a Part of Digital Transformation of Modern Economy" Applied Sciences 10, no. 3: 1076. https://doi.org/10.3390/app10031076

APA StyleKryvinska, N., & Bickel, L. (2020). Scenario-Based Analysis of IT Enterprises Servitization as a Part of Digital Transformation of Modern Economy. Applied Sciences, 10(3), 1076. https://doi.org/10.3390/app10031076