1. Introduction

Controlling, in its modern understanding, has been and still is considered by both scientists and practitioners in the field of management as an extremely dynamic method of supporting management [

1,

2,

3]. Confirmation of the dynamic nature of controlling should first of all be found in its history-on a macro scale. It is worth noting that at the stage of creating the concept of controlling at the end of the 19th century in the USA [

4] —when the position of a comptroller was created in one of the American railway companies around 1880 (Atchinson, Topeka and Santa Fe Railroad Company)—it was a person responsible only for financial matters related mainly to profitability of production [

5,

6]. However, in the 1920s, new challenges emerged before organizations (and controlling implemented in them) as a result of the great world crisis [

7]. This management method has therefore evolved and thanks to the use of a wide range of management accounting tools and the improvement of planning in the organization, it allowed not only to answer questions about the profitability of production, but also supported “clear setting of goals and quick verification of the areas of the organization’s deficiencies” [

8] (pp. 168–169). Controllers in USA became a combination of managerial experience and the knowledge of accounting [

9]. A significant change in the perception of controlling should also be noted in the post-war period, when controlling reached the Old Continent as a result of establishing branches of American organizations in Europe, which was rebuilding after World War II [

10]. In Germany, controlling solutions have been adapted to the operating conditions of European organizations and have been successfully implemented in them. In 1970, at the Controller Akademie, founded in Germany, researchers developed a comprehensive set of new assumptions related to controlling, significantly different from the American ones [

11]. It should be emphasized that the “German” controlling differed from the “American” controlling, which is definitely underlined by e.g., Horvath [

10,

12], Weber [

11], Portz and Lere [

13], Chenhall [

14], Wagenhofer [

15], Schäffer and colleagues [

16].

In the above context, it can be stated that controlling changes over time, because organizations and their environment evolve over time. It is also true for micro scale, i.e., changes in controlling during its operation in a specific organization. As Skrzyniarz [

1], (p. 10) notes, “a dynamic approach is a prerequisite for the effective implementation and functioning of the controlling system”. As a result of changes in the environment, changes take place inside the organization, which means that “the managers of organizations find that the previously adopted solutions do not take into account new needs and again face the necessity to change on the scale of reorganization. Controlling is therefore dynamic and is constantly changing, hence the difficulty of describing it with static concepts, language and way of thinking” [

1], (pp. 10–11). Weber [

17] confirms that by combining changes in controlling with factors shaping controlling solutions that change in time. The perspective of situational conditions reveals the dynamic nature of controlling. Bender [

18] and Erben [

19] confirm that controlling is “a living organism, which must absolutely keep up with all changes and evolutions in the enterprise.” Bender [

18] simply excludes the functioning of controlling, once implemented in the organization, in a rigid, unchanged form. Hence—as it would seem—in this dynamic nature lies the basic source of controlling’s success.

In this context, dynamic capabilities of controlling, understood in general terms as the ability to adapt to changes taking place both inside the organization and in its environment, are of particular importance. As a new construct, the dynamic capabilities of controlling are based on a concept of organizational dynamic capabilities by Teece, Pisano and Shuen [

20] as well as Eisenhardt and Martin [

21], who noticed the role of dynamic capabilities in shaping the competitive advantage of an organization. However, Teece, Pisano and Shuen [

20] (p. 516) stated that DC concerns “the firm’s ability to integrate, build, and reconfigure internal and external competencies to address rapidly changing environment”, and Eisenhardt and Martin [

21] (p. 1107) underlined also that DC can be understood as “the firm’s processes that use resources—specifically the processes to integrate, reconfigure, gain and release resources—to match and even create market change”.

However, as the controlling is contemporary one of the management methods most heavily relying on IT support [

22], it seems crucial to consider what is the role of that support in case of dynamic capabilities of controlling. Nowadays, both the functioning of controlling in an organization and changes within it must be supported by IT, which—as research shows—plays an important role in the process of its functioning and builds the effectiveness of the discussed method of supporting management. Hence, it seems that various characteristics of IT may exhibit an influence, which enables organization to obtain more benefits from controlling use, especially considering its dynamic capabilities. Due to the fact that IT capabilities have the ability to support any dynamic capabilities which may be present in the organization [

23,

24,

25], it would be logical to assume that their role in supporting controlling dynamic capabilities should be verified. However, it seems that in order to gain a full set of benefits from the high-quality products of controlling, the IT used in the organization to support it must be reliable, in order for the employees to rely on its use [

22]. Hence, it seems that also IT reliability role in supporting dynamic capabilities of controlling should be examined.

In this context, the aim of the article is to examine the impact of controlling dynamic capabilities on organizational performance through quality of controlling and verify the role of IT support for the obtainment of benefits for the organization as a whole. It would potentially allow to fulfill the research gap concerning the need for underlining the mechanism of influence of dynamic capabilities of controlling on both quality of controlling, and performance of organization as a whole (to reveal the level of benefits gained by organization due to use of such controlling). Moreover, it would allow to indicate which aspects of IT support are most crucial in order to enable or magnify the benefits obtained by the organization as a whole through the proper utilization of dynamic capabilities of controlling. Such research aim will be accomplished by development of theoretical model explaining the mechanism of dynamic capabilities of controlling influence on organizational performance and describing the role of IT support in this mechanism, which will be presented in second chapter. Next, empirical research will be performed in order to verify those theoretical assumptions (through multiple regression analysis with mediator and moderators) and the findings will be presented in third chapter. Finally, the fourth chapter will contain discussion concerning the findings and will establish a contribution for given field of study.

2. The Role of Dynamic Capabilities of Controlling in Shaping Organizational Performance

Dynamic capabilities are a type of organizational capabilities, which are in general understood as a collection of routines [

26], which are divided into two main groups: operational capabilities and dynamic capabilities. As the operational capabilities concern the ability to “make a daily living”, the dynamic capabilities concern the ability to “make a living” [

26] in changing environment, which seems to be especially important in the world, in which dynamics of environment is constantly rising. Teece [

27] (p. 40) states that dynamic capabilities are “a unique and valuable general-purpose resource” and shows that dynamic capabilities can be treated by the contemporary organizations as the foundation for obtaining and maintaining sustainable competitive advantage. Because of that, the dynamic capabilities attracted a huge attention among the research community [

21,

27,

28,

29] not only in its native domain, which is strategic management, but also in much narrower ones. Therefore, it is reasonable to assume that such a broad literature coverage caused multiple dynamic capabilities models to rise and it is a valid research subject to analyze them in the context of controlling, which is a management method enabling swifter operations of organization in, among others, dynamic environment.

The perception of controlling varies in modern organizations, however regardless of the perception it is very often considered as a key for economic growth of contemporary organizations [

3]. This term includes both “managerial/ management control and accounting” [

30], and also subsystem of organization’s management support (Horvath, 2009), support for planning and coordinating [

12,

31,

32], coordination of the management or supporting of decisions making [

33]. Without going into terminological details, undoubtedly connected with the multi-threaded history of controlling, in this study it is assumed to understand controlling as “a method of management support used mainly in the areas of planning, control and steering—for the implementation of functions such as information supply, coordination, supervision, monitoring or participation in management; enabling managers—through its measurable and economical overtone—for making rational (and apt) decisions, and thus aimed at achieving the goals of the organization as a whole” [

34] (p. 38). In such understanding, controlling is considered as a management method, which is one of the most often used in contemporary organization [

22,

35].

Controlling is characterized by a dynamic nature. The cause of controlling′s dynamic nature should be most definitely sought precisely throughout its existence, during which controlling has been and still is connected and dependent on practice. The dynamic character of controlling is related to its maturity and excellence, which are discussed in the literature [

36,

37]. As indicated by Bieńkowska and collegues [

37] “controlling cannot freeze after implementation, but according to contextual changes, it will start to change in an evolutionary (or if necessary even in revolutionary) way”.

It should be noted that not all organizations cope with the improvement of controlling solutions adequately to the needs of the organization and the environment in which the organization operates. Hence, it is reasonable to define a new construct, i.e., dynamic capabilities of controlling, which by definition will relate to the controlling’s ability to effectively adapt to changes inside the organization and in its environment, thus ensuring its development and improvement. Dynamic capabilities of controlling should be understood as the abilities of controllers (with the support of managers) to integrate, build, and reconfigure controlling solutions to address rapidly changing environment, which is influencing the quality of controlling and—as a consequence—organizational performance. The dynamic capabilities of controlling are connected to the following assumptions:

Controllers are able to identify the needs and expectations formulated by managers and employees regarding controlling.

Controllers are flexible and can adapt to the changing needs and expectations of internal controlling clients.

Controllers are able to develop new controlling solutions that will meet the needs and expectations of managers and employees towards controlling to a greater extent.

As in the case of organizational dynamic capabilities, controllers should be sensitive to identifying changes in the needs and expectations of internal controlling customers, assuming that these in turn result from changes inside the organization and in its environment. Then, assuming that controllers also show flexibility and openness to adapt to the changing needs and expectations, the very change of needs and expectations is the basis for developing new controlling solutions and, for example, adapting the management accounting system or budgeting to new operating conditions.

It is also worth noting that dynamic capabilities of controlling is relativized directly to the changing needs and expectations formulated by managers and employees. These, in turn, are a derivative of changes taking place in the organization itself and in its environment, which often cause vast changes within the organization, sometimes connected even to business model change [

38]. For example, Bieńkowska and collegues [

39] emphasize that controlling solutions should be dedicated to particular phases of the organization’s growth-according to particular phases of e.g., the organizational growth model proposed by L. Greiner.

Dynamic capabilities of controlling understood in this way are part of the dynamic capabilities of organization, so naturally, as such, they will contribute to the organization′s competitive advantage. This is due to the fact that controllers are able to provide managers and employees with the desired information necessary in decision-making processes, or effectively participate in coordination processes in the organization only with solutions (including tools) tailored to their needs. This means a direct increase in the quality of controlling in the organization—where the quality of controlling should be understood as “the degree to which the set of inherent properties of controlling products (services, benefits) meets the requirements of primarily recipients of these products (managers and/or other recipients in the organization), but also controllers—as implementers of the idea of controlling” [

34] (p. 221). The quality of controlling understood in this way is therefore a relative category and the key issue here is emphasized by e.g., Webera and Nevriesa [

17], who claim that controlling should be oriented towards the internal customer. The focus on the recipient is also emphasized by Roehl-Anderson and Bragg [

40]. Thus, the quality of controlling products i.e., primarily the quality of: information generated by the controlling information system, including all kinds of reports, controlling reports and analyzes, plans or budgets, as well as controlling services such as: decision-making support, participation in planning, supervising the control system or coordination of planning processes in the organization, etc. [

34], it must be correlated with the needs of people who use these products/services.

It confirms some literature reports stating that dynamic perspective is crucial driver of successful controlling [

2,

41]. Pasch [

42] is underlining that dynamic capabilities are especially needed in high competition environment and it is a well-known fact that almost all contemporary organizations are forces to operate in such environment. Hence, it seems that dynamic capabilities of controlling will indeed have a potential to influence its quality, allowing to include a dynamic perspective in its implementation and use. In view of the above, the following hypothesis can be proposed:

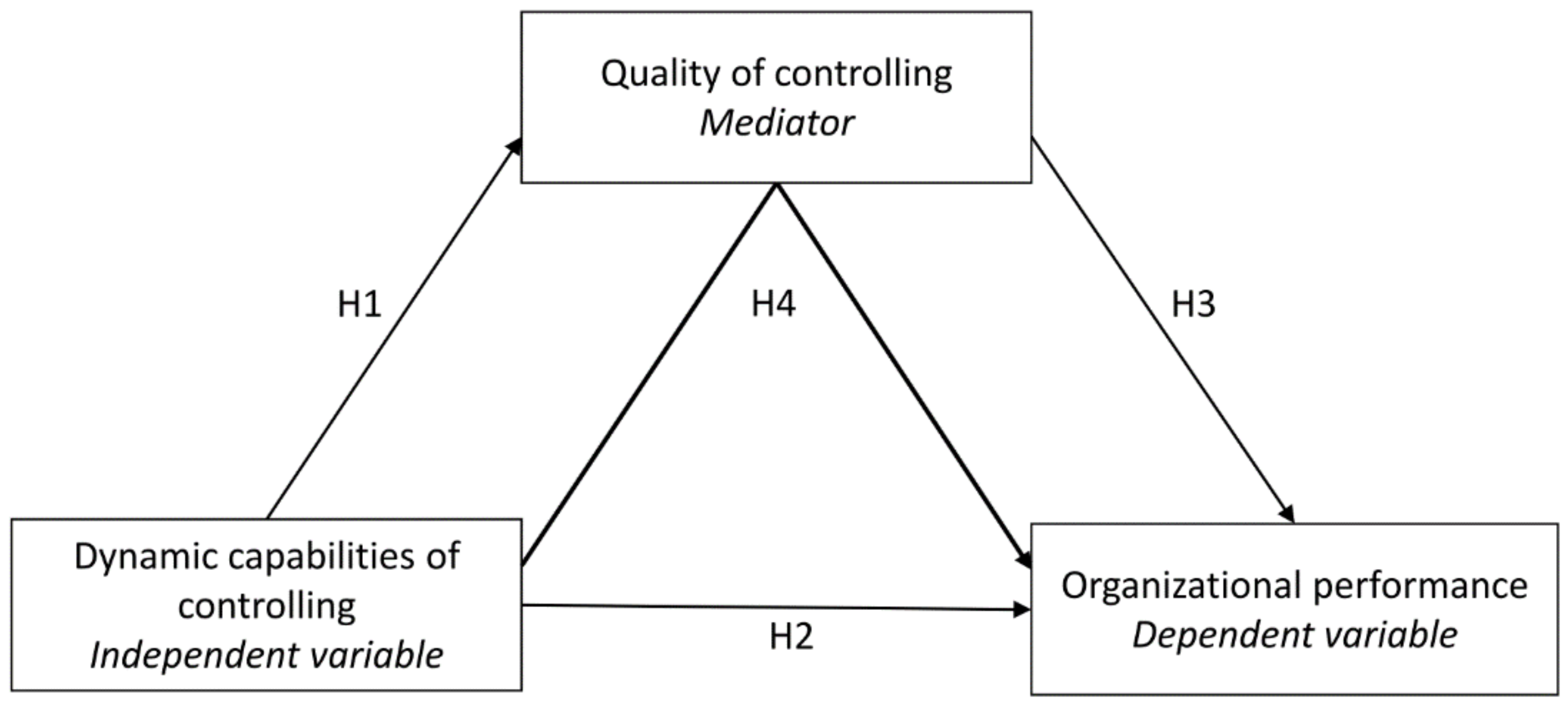

Hypothesis 1 (H1). There is a relation between dynamic capabilities of controlling and quality of controlling.

What′s more, it is known that the longer controlling is implemented in the organization, the stronger it influences the results obtained due to its implementation related to the functioning of the organization as a whole. Controlling time of use is strongly positively related with all results obtained due to controlling implementation [

37]. Therefore, assuming that the time of controlling use in an organization may, in simple terms, be a measure of its excellence (because it is assumed that both controlling solutions and, consequently, the products (services) it offers are of higher quality—as a result of undertaken improvement activities), it can be assumed that controlling has the ability for the very fast reaction to the changes occurring in economic reality. It allows for constant development of new solutions and facilitating business management increasingly well. Hence, it gives possibilities to ensure continued existence of organization. Therefore, the following hypothesis can be formulated:

Hypothesis 2 (H2). There is a relation between dynamic capabilities of controlling and organizational performance.

It is also natural that the quality of controlling influences organizational performance. The hypothesis relating to the above statement is formulated in the study to analyze the mediation model of controlling dynamic capabilities influence on organizational performance and has already been de facto repeatedly confirmed in the previous studies of the authors [

24,

37,

43,

44]. It will be also verified in this research:

Hypothesis 3 (H3). There is a relation between quality of controlling and organizational performance.

In the context of the relations described above, it seems that there is a need to comprehensively explain the mechanism of the impact of controlling dynamic capabilities on organizational performance, while analyzing the mediating role of quality of controlling. It will allow to verify and more comprehensively explain the mechanism of controlling dynamic capabilities influence on organizational performance. It seems that controllers, using their controlling solutions and providing managers with high-quality products (services), affect the job performance of employees and managers [

45], which ultimately and indirectly affects organizational performance [

45]. Therefore, in the light of the above, the main hypothesis should be formulated:

Hypothesis 4 (H4). Dynamic capabilities of controlling influence organizational performance through quality of controlling.

The diagram illustrating the adopted research hypotheses is presented in

Figure 1.

4. Research Methodology

The empirical research based on the questionnaire technique was conducted in order to verify the formulated hypothesis. The main survey was preceded by the pilot survey conducted in the middle of 2019 among the group of 25 managers (acting as competent judges). According to obtained results, some ambiguous questions were rewritten and it was established that proposed questions are understood by respondents as it was intended by researchers (which is a prerequisite for establishing a questionnaire as a valid measurement method [

60]). The main research conducted with CAWI method among 229 organization from Poland was implemented in October 2019. The country of operation was the only condition limiting the sample (organizations were surveyed regardless of size, industry or type of business etc.). It is possible to form the overall conclusions as the sample is sufficiently diversified (considering diversity of organizational characteristics). Sample characteristics are presented in

Table 1, which presents that the sample is covering diverse group of organizations. Among those organizations, 188 have declared implementation of controlling.

4.1. Variables Overview

The hypotheses verification was based on four key variables (their description is given in

Table 2):

controlling dynamic capabilities, controlling quality, IT dynamic capabilities, IT reliability and organizational performance.

IT dynamic capabilities (ITDC) was measured based on 7 items covering activities (gathering information about the environment, predicting changes in the environment, recognizing opportunities in the environment, defending against threats from the environment, designing or reshaping business process, reconfiguring resources, realignment to changing needs) automatically supported by IT DC. The scale was based on a 5-point Likert scale (from I strongly disagree, to I strongly agree with a middle point: I have no opinion).

IT reliability (ITrel) was measured based on 4 items covering the reliability of four components: system, usage, information and support services. The scale was based on a 5-point Likert scale (from I strongly disagree, to I strongly agree with a middle point: I have no opinion).

Organizational performance (OP) was measured based on Balances Scorecard concept (Kaplan & Norton, 1996), being the framework that allows to draw together multiple measures aimed at financial performance, internal business processes, customer perspectives, and innovation and learning. Within these 4 perspectives, ensuring consistency between the strategic objectives and the projects implemented by the organization, 8 measures of the organizational performance were indicated. They were rated on the 5-points’ Likert scale (from well below expectations to well above expectations with the middle point: as expected).

Controlling quality (CQ) was measured based on 8 items referring to the elements which are directly affected by controlling—budgeting and information provided to managers for the purposes of decision making (including reports and analyzes). The scale was based on a 5-point Likert scale (from I strongly disagree, to I strongly agree with a middle point: I have no opinion).

Controlling dynamic capabilities (CDC) was measured based on the list of 3 items concerning controllers ability to identify the needs and expectations formulated by managers and employees regarding controlling, controllers flexibility and ability to adaptation to the changing needs and expectations of internal controlling clients, as well as controllers ability to develop new controlling solutions that will meet the needs and expectations of managers and employees towards controlling to a greater extent. The scale was based on a 5-point Likert scale (from I strongly disagree, to I strongly agree with a middle point: I have no opinion).

To ensure that the given scale can be used, the Cronbach′s α, as well as Factor Analysis were analyzed for

controlling dynamic capabilities, controlling quality, IT dynamic capabilities, IT reliability and organizational performance. The obtained results indicate the high internal reliability of the scales (Cronbach′s α > 0.8 in almost all cases, it is equal 0.754 in one case but it is supported by high values for factors analysis). The results confirmed that there were no collinearity issues and the model could be built based on the given set of data (see

Table 2).

4.2. Research Results

In order to verify the research hypothesis, multiple linear regression with mediator and moderators was performed using SPSS Macro Process by Hayes.

As a first step, a regression model with mediator was calculated. There are three conditions, which must be fulfilled to establish mediation model. First of all, there must be a relation between independent variables and the mediator. Second of all, there must be a relation between dependent variables and the mediator. Third of all, while controlling for the given mediator, there should be a reduction (partial mediation) or disappearance (full mediation) of a significant relations between the independent variables and dependent variables.

First, the linear regression analysis using control variables was performed in order to verify whether dynamic capabilities of controlling indeed have statistically significant influence on organizational performance. The sample was controlled for variables connected to all elements of organization, to show that the influence of controlling dynamic capabilities is statistically significant and stronger than anyone of them. It is worth noting that the regression model without dynamic capabilities of controlling variable shows that all control variables are significant. The results of the obtained model with dynamic capabilities of controlling are given in

Table 3 and they show that it is indeed a statistically significant element of the model and its influence is so substantial that most of control variables was tested as insignificant in this case. Hence, the results allow for the analysis to go forward.

Next, the r-Pearson correlation analysis was performed in order to satisfy those conditions and the results are given in

Table 4. The correlation is considered as high in social sciences when r coefficient is above 0.6 [

61], which is the case for all relations.

The obtained results of correlation analysis show that there is a statistically significant and high correlation between all analyzed variables, which satisfies the conditions for mediation analysis. Hence, the next step of the verification of the mediation model can be performed. In order to do that, regression model with mediator is built for controlling dynamic capabilities as independent variable, and organizational performance as dependent variable. The controlling quality is tested as the mediator in the model. The results of the analysis are included in

Table 5.

The obtained regression model with mediator is statistically significant (F (2224) = 139,073 and corrected R2 = 0.553), as the obtained coefficient satisfy the rule of thumb for research in social sciences (Hair et al., 2010). Moreover, controlling quality is a statistically significant mediator of the model (

p < 0.001, coeff. = 0.348, se = 0.069). Those results confirm that the mediating effect is statistically significant, as can be observed in

Table 4 (indirect effect occurs,

p < 0.001). The obtained model shows

that controlling quality is indeed a mediator of the relation between controlling dynamic capabilities and organizational performance. Therefore, those results together with the results of correlation analysis allow for accepting hypothesis H1–H4.

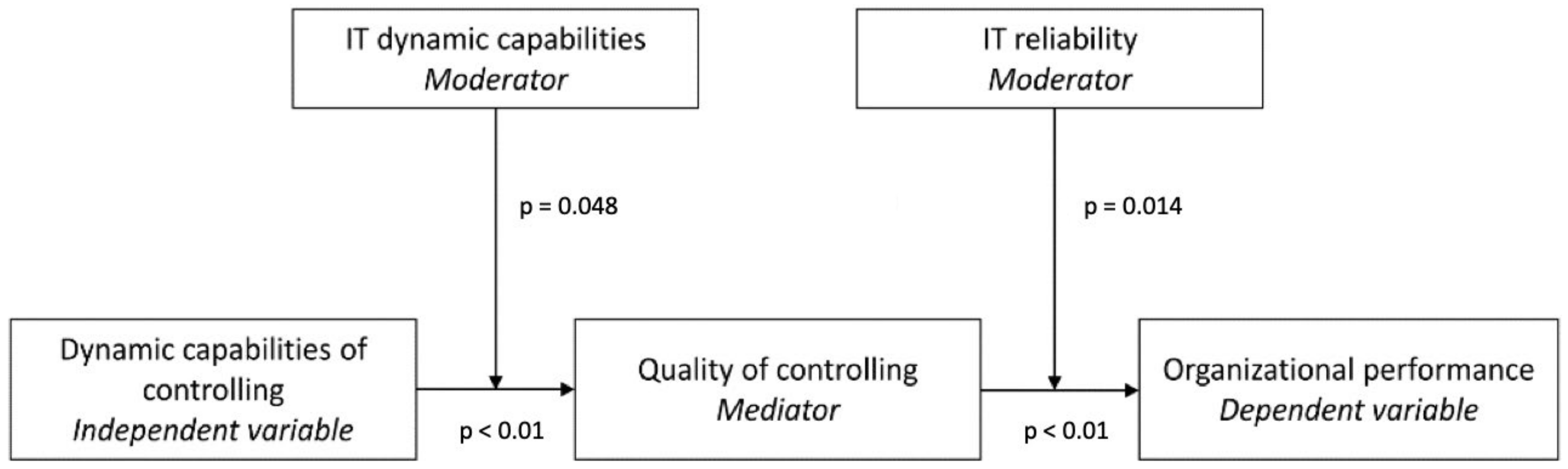

The obtained mediation model was analyzed in the context of IT influence to verify the statistical significance of IT dynamic capabilities and IT reliability it as moderators of the relations given in the model. The hypotheses were tested using multiple mediated regression analysis with moderator for every relation. Using the Process Macro (models 7 and 14), the moderated regression analysis procedure was performed to verify the proposed hypotheses. The moderator was introduced into the mediated linear regression model as a new variable for every case. Mediator is a product of two standardized independent variables. For every case, three linear regression models were built. The first model, where only independent variables were added as predictors, is a base one for comparison. The second model, where not only independent variables, but also the moderator is added as predictors, is compared with it. It allows to verify if there is a moderating influence in the entire sample. The third model is built for confirmation, where only moderator and one independent variable are introduced. The results of the analysis are presented in

Table 6.

The performed mediated linear regression analysis with moderators confirmed the hypotheses. The obtained results clearly show that IT dynamic capabilities is a statistically significant moderator in case of the relation between controlling dynamic capabilities and controlling quality in a given mediated regression model (F (3216) = 183,130,

p < 0.001). The IT reliability is in turn a statistically significant moderator in case of the relation between controlling quality and organizational performance in a given mediated regression model (F (3216) = 137,171,

p < 0.001). In both cases, the model fit and F-Snedecor statistics were sufficient and statistically significant, hence the model could be used for statistical reasoning. Therefore, as shown in

Table 6, obtained results are the basis for the acceptance of hypothesis H5 and H6.

5. Discussion

The performed empirical research was based on the mediated linear regression analysis with moderators. It revealed, most of all (see

Figure 3), that dynamic capabilities of controlling have the influence on organizational performance through quality of controlling.

The obtained results first of all confirmed the significant role of dynamic capabilities of controlling in the process of shaping organizational performance. It remains in line with the literature considering organizational capabilities (understood as the collection of routines [

26] describing the efficiency of those routines) as a source of competitive advantage. It is all the more true for dynamic capabilities, as the entire dynamic capabilities view (DCV) emerged in the literature as the way to untangle issues concerning sustaining competitive advantage in dynamic environment and translate the capabilities into performance [

20,

21]. Hence, the obtained results remain especially important since so far, the beneficial influence of the implementation of controlling itself on the functioning of the organization was shown [

22,

43,

44,

62], but the necessity to change controlling over time was not emphasized. This study proves that the quality of controllers to identify the needs and expectations formulated by managers and employees regarding controlling, as well as their flexible response in the form of adapting solutions of controlling to these needs and expectations, determines the quality of products and services offered by controlling. It is worth emphasizing here that the needs and expectations of managers and employees result from changes both in the environment and in the organization itself. The results also show that dynamic capabilities of controlling affect organizational performance, but the impact is indirect. The quality of controlling, which is relating to controlling products and services, is a mediator of this relation. Hence, the existing state of knowledge was expanded to include empirical verification of the significance of the dynamic nature of controlling, thus extending the conclusions of Skrzyniarz [

1] and Weber [

2].

Moreover, the obtained results show that the influence of IT on the use of controlling dynamic capabilities for the benefit of the organization is diverse and based on various different characteristics. Hence, it seems that it is not enough to conclude that IT indeed enables organization to benefit from controlling use, especially supporting its dynamic capabilities. It must be underlined that first of all, dynamic capabilities of IT are needed for that in order to properly support controlling in such changing conditions and facilitate its fast adaptation and second of all, IT must be reliable in order to allow organization to gain full range of benefits from high quality controlling products. Therefore, the obtained results allowed to confirm that dynamic capabilities of IT indeed act as a factor, which has the potential to strengthen the relation between controlling dynamic capabilities and controlling quality. It confirms views found in the literature, as e.g., Granlund and Taipeleenmaki [

41] assumed that dynamic nature of solutions used for controlling in organization will have the ability to enhance its quality by enabling quick adaptation of controlling to changes in the organization’ needs. It also confirms some collateral views that dynamic capabilities are now essential for obtaining proper organizational performance while managing vast amount of data (which is characteristic for controlling) [

52]. Moreover, such results furthermore confirm those, which are already existing in the literature, in which it is underlined that dynamic capabilities of IT allow to gain a competitive advantage in currently growing dynamics of environment because not only directly but through their support for other dynamic capabilities existing in organization [

51,

52]. It allows to confirm more general assumptions concerning dynamic capabilities and the IT support for them made for different countries [

25].

However, there is a need to underline that IT is crucial for supporting dynamic capabilities of controlling on two levels. First of all, from the perspective of supporting the indication of changes, which are needs. As stated before, controllers should be able to identify changes in the needs and expectations of internal controlling customers and shape controlling solutions in order to meet them. The obtained results clearly underline that in order to do it in a way, which will allow organization to gain higher level of benefits, the support of reliable IT is crucial, especially including the use of dynamic capabilities of such IT. It remains in line with Second of all, from the perspective of supporting changes within controlling solutions, which are needed in order to align the changed needs and expectations to those solutions, as dynamic capabilities of IT allow for quicker and smoother changes within IT solutions in the organization.

6. Conclusions

The aim of the article was to examine the impact of controlling dynamic capabilities on organizational performance through quality of controlling and verify the role of IT support for the obtainment of benefits for the organization as a whole. The performed empirical research allow to fulfil this aim and partially close the indicated scientific research gap. It was pointed out that the phenomenon of dynamic capabilities should not be related only to the organization as a whole. It is also worth noting the possibilities of adaptation, learning or problem-solving in relation to its individual elements, such as employees, IT, or, as in this study, management methods. Moreover, the research results confirmed that IT support is crucial for obtaining benefits from controlling use in the organization and this support is especially needed in case of seeking benefits coming from dynamic capabilities of controlling [

62].

From the utilitarian point of view both confirmations are crucial. It has been confirmed that not only the quality of controlling, but also its dynamic nature, are the source of the success of this management support method. Dynamic capabilities of controlling allow to react very quickly to all changes taking place in the economic reality and to propose new solutions aimed at improving management in the organization. In this way, they significantly influence organizational performance. Organizations should therefore pay special attention to the constant adjustment of controlling products/services to the needs and expectations of managers in the organization. The dynamic nature of controlling, which is “marked by the practical activity of enterprises” [

2] implies objective difficulties related to the interpretation, analysis or description of this method, but-as confirmed by the research results-this dynamic nature and practical pedigree are the primary basis for the development of controlling for all. In this way, the obtained results have a significant value for managers responsible for controlling in contemporary organizations.

Moreover, controllers and managers should also consider the shape of IT solutions in order to maximize the benefits coming from controlling dynamic capabilities. To obtained results clearly confirmed that dynamic capabilities of IT are crucial for boosting the benefits obtained by the organization from dynamic capabilities of controlling, as they allow for a quick adaptation of IT solutions supporting controlling to the changed needs of organization. Moreover, the results also underlined the fact, that all those benefits are even higher among organizations, in which IT is reliable. Therefore, there is a clear need for tending to those characteristics of IT.

Moreover, it is important to underline that the year 2020 will be remembered in the history of management as a time when practically every organization in the world was affected by the extreme crisis caused by the COVID-19 pandemic, having all the characteristics of the so-called Black Swan. It caused extremely dynamic changes in the environment and research focused on enabling organizations to function in such conditions is especially important. Therefore, the obtained results seem to be important not only from the point of view of broadening the theory concerning controlling as a management method but also from the point of view of establishing mechanisms for organizations to gain more benefits from controlling use in contemporary conditions.

Of course, the performed research has certain limitations: only organizations operating in Poland participated in the research, and therefore the analyzes take into account the specificity of controlling implemented in these organizations, so in future it is worth to consider the verification of formulated hypotheses in organizations operating in other countries, especially in USA and Germany-a countries with a long tradition of controlling. It can be a guide to future research. The current situation also calls for the replication of the study in more turbulent environment, which may further confirm the obtained views but will have limitations concerning the “after-Black Swan event” conditions. It is also worth noting that the research sample was not representative, so the conclusions may not be generalizable for all companies operating in Poland. Of course, it was varied enough to allow generalized conclusions to be drawn but it further confirms the possibility for further studies in this area.

{kind=link}

{kind=link}

{kind=link}