2.1. Business Performance of the Winery

In the modern literature, “successful organizations” have positive financial results, successfully adapt to changes in the environment, possess a managerial focus on social opportunities and innovation, having positive business performance. Market-oriented behavior implies different activities/strategies and results in improved business performance of the company, whether we are talking about company resources or additional variables (innovation or marketing capabilities, and brand management capabilities). The diversity and mobility of resources is significant and it is difficult to determine which resources or activities are more valuable. Managing the business performance of wineries firstly implies the identification of critical factors, adequate measurement and final improvement, i.e., successful management of risk parameters. As far as the brand performance of wineries is concerned, the key questions are: how the value is built, how it is improved and maintained.

Reid et al. [

14], Albert and Merunka [

15], Gumparthi and Patra [

16] pointed out that building a wine brand requires modern precise marketing tools, the marketing communication and the communication through social networks [

17,

18,

19,

20,

21], the internet advertising, and the web design [

22]. Szolnoki et al. [

17] pointed out that membership in the groups on the social networks [

23] or the wine groups [

24] has a positive effect on the wine purchase, and contribute to the strengthening and to the brand recognition [

25,

26]. Efficient marketing communication [

27] leads to company profiles with a desired image and creates an appropriate position in the consciousness of consumers and the general public [

28] contributing to an increased awareness on sustainability. Muñoz et al. [

29] pointed to the importance of the brand in the prevention of wine counterfeiting. They concluded that proactivity and differentiation of wine, the development of loyalty of wine consumers [

30], the improvement and the guarantee of the wine quality, the geographical indication [

31,

32,

33,

34] contribute to the purchase and the brand recognition [

35] and the overall performance of the wineries. Peattie [

36] and Barber and Taylor [

37] pointed to the existence of a link between the purchase and willingness to pay a premium for environmentally friendly products or wines with guaranteed quality/origin [

38,

39,

40,

41,

42]. The business performance of wineries largely depends on supply chain management, although managers are not yet aware of this [

43]. There is a lack of marketing studies on the impact of distribution systems and logistics [

44].

Buying wine when visiting a winery is a form of distribution and affects customer satisfaction and brand and image development [

45]. Mitchell and Hall [

46] pointed out that visits to wineries contribute to strengthening loyalty and influence subsequent consumer behavior, as well as that a loyalty, buying wine after a visit and repeating visits, is more pronounced among domestic visitors. Wineries attract visitors with their ambience [

47]. Consumer activities in a winery or wine club [

48] are crucial for developing and strengthening loyalty to certain brands. Wine tourists plan their visits based on certain information (size of winery, length of stay in the wine region), including various motivating factors [

46,

49,

50,

51,

52,

53,

54]. Educating visitors and other potential consumers is important in building brand loyalty and improving the winery’s business performance [

55,

56]. Tours, product tastings and production presentations are activities for the education of visitors and consumers, wine tourism is connected with the past and tradition, in the global context of tourism (landscape, cultural activities, and catering systems). As Bruwer and Rueger-Muck [

57] stated, visits to wineries present a multitude of different sensations: ambiance, atmosphere, environment, regional culture and cuisine, local wine styles and varieties. Revenues from winery visits contribute to rural development, along with the sustainability of rural life and agricultural landscapes [

5,

58]. In this way, tourists get acquainted with wine culture, creating synergy between localities, gastronomy and visitor experiences [

59]. Wine becomes a traditional resource that forms the authenticity of the destination to the stage of forming and branding the tourist region [

60].

A study by Santos et al. [

61] showed that wine entrepreneurs need a long-term investment horizon because the recovery of initial investments in winery start-up projects takes many years. The authors pointed out that the startup projects of wineries are greatly influenced by prices and costs. High land prices are economically justified for investors and entrepreneurs with the possibility of risk diversification, but can be a critical obstacle for individual entrepreneurs who lack capital. Some authors have dealt with the relationship between climate change, i.e., temperature rise, and the quality and price of wine [

62,

63]. Ashenfelter and Storchmann [

64] and Ashenfelter [

65] presented the economic implications between climate change and wine. Gergaud and Ginsburgh [

66] showed that the technology applied in vineyards and wineries explains the price differences between wines, while Cross et al. [

67] revealed that vineyard sales prices are strongly determined by names but not by specific location attributes, such as slope, aspect, altitude, and soil types. Price is a variable category and manufacturers usually use it to influence consumers’ choices, along with other parameters: bottle style, label design, advertising campaigns (for example, champagne). In addition, the importance of expert assessments and the role of experts is very controversial. Several papers emphasize the assessments of experts as important. Cardebat et al. [

68] confirmed that the price variations can be better explained by weather conditions than by differences in expert estimates. Many studies reveal that the size of the manufacturer, or the size of the production, can be a significant price factor. However, there is a surprising lack of marketing studies on the impact of distribution systems and logistics [

69]. Outreville [

69] summarized the determinant factors: geography/viticulture; time horizon; public information; production costs and quantity supplied. Wine prices are not only affected by the quantity demanded, but also by the set of attributes that the consumers consider. Wine prices are usually studied using a hedonistic pricing model based on the Lancaster approach, which links the price of goods with different objective attributes (color, vintage, alcohol content, and grape variety) [

70,

71], sensory attributes (aroma, finish or harmony), information that usually comes from expert opinions (ratings) or medals awarded [

62,

72,

73,

74]; the influence of reputation, both individual and collective, of wines and producers amongst consumers. Ecologically oriented consumers show a greater willingness to buy organic wine [

37,

75]; and pay a higher price [

76,

77,

78]. The consumers who had the largest share of organic wine expenditure showed strong environmental attitudes, propensity for sustainable products, and ethical concern [

79]. Pomarici et al. [

80] indicated that some wine consumers are interested in environmentally-friendly wine, environmental protection, and water footprint [

81]. However, some research has shown [

42,

82] that environmental concerns are not a decisive factor in buying organic wine, linking it to a lack of trust in organic labeling or a lack of information regarding organic certification [

83]. On the other hand, some authors consider the price to be the only important attribute when making a purchase decision, i.e., they believe that the eco-label is not a strong element of wine differentiation [

84,

85].

Innovative winery models pay attention to new technologies, and it often represents a platform for developing completely new business models in the long term [

86,

87]. Small and medium-sized enterprises (SMEs) usually lack the resources to implement new technologies and digital transformation. Dressler and Paunović [

86] pointed out that the wineries often expand their range to include grape juice, vermouth, gin, and similar drinks. Social media are an essential element of the online platform and facilitate the communication process [

88]. The wineries are often focused on making a profit, while social and environmental benefits are often marginalized [

89]. Annunziata et al. [

90] pointed out that the sustainability-oriented capabilities of wineries are rooted in strategic orientation and proactive socio-environmental practices, and the sustainability orientation is expected to have a positive impact on business growth and transformation.

2.2. Environmental Behaviour and Business Performance

Barba-Sánchez and Atienza-Sahuquillo [

91] addressed the question of the relationship between the degree of proactivity of a firm’s environmental strategies and its business performance. They concluded that environmental proactivity [

92] improves business performance, and has a greater impact on reducing environmental impact and improving environmental efficiency. Banerjee et al. [

93] concluded that there is an internal and external environmental orientation and an environmental corporate and marketing strategy. Connection with various environmental issues is important for the integration of environmental proactivity into corporate strategy [

94,

95]. Environmental proactivity is a segment of sustainable competitive advantage, and should ultimately contribute to improving economic performance and reducing companies’ environmental impact by improving their environmental performance.

Some studies point out to the economic viability, i.e., the impact of environmental behavior and business results [

96], while other authors show that a large number of factors influence positive business results. Knight et al. [

97] analyzed the impact of the wine industry on the society and the environment and point out that sustainable business has become an integral part of modern corporate governance [

98]. Therefore, wine production should be sustainable, and management of resources and production process is one of the most important activities. The authors pointed out the ecological dimension of land and water resources, chemical fertilizers, and the ecological behavior in the wine industry has been and will continue to be the subject of research. Thus, the responsible behavior towards the environment can be a result, but also a precondition of financial effects, it can be related to the wealth and/or specificity of resources. Some authors pointed out a negative relationship between financial performance and environmental activities [

99], while Ko and Liu [

100] showed that the development of this relationship is influenced by the level of development of marketing and R&D performance of the company. Research by Barber et al. [

101] showed that the high prices that consumers are willing to pay are related to the qualitative and quantitative characteristics of the wine, and not to the ecological dimension of the winery’s business. Ginon et al. [

102] investigated consumers’ perception of environmentally friendly logos in wine production and concluded that there is a need for improving communication on environmentally sustainable wines. Barber [

101] pointed to the importance of eco-friendly packaging for wine [

21].

In the wine industry, resources can be scarce, interconnected, i.e., in correlation. So, the question arises: is any of these individual resources related to behavior and environmental discovery, and what is the nature and intensity of the relationship? The assumption is that wineries that own and exploit rare resources behave responsibly, i.e., have pro-environmental management and business strategies. Previous research on the ecological perspective of the agri-food sector in Serbia, especially winemaking, has been dedicated to very specific issues, e.g., technological production processes, pollution, emissions of air pollutants, legislation [

103,

104], organic agriculture [

105,

106] etc. However, there is a lack of a study dealing with corporate environmental responsibility [

107]. The relationship between environmental behavior and company performance, as well as impact of certain business factors on environmental behavior in the Serbian agri-food industry, especially wine sector, has been insufficiently investigated. Winemakers are aware of the existence of the impact of production on the environment [

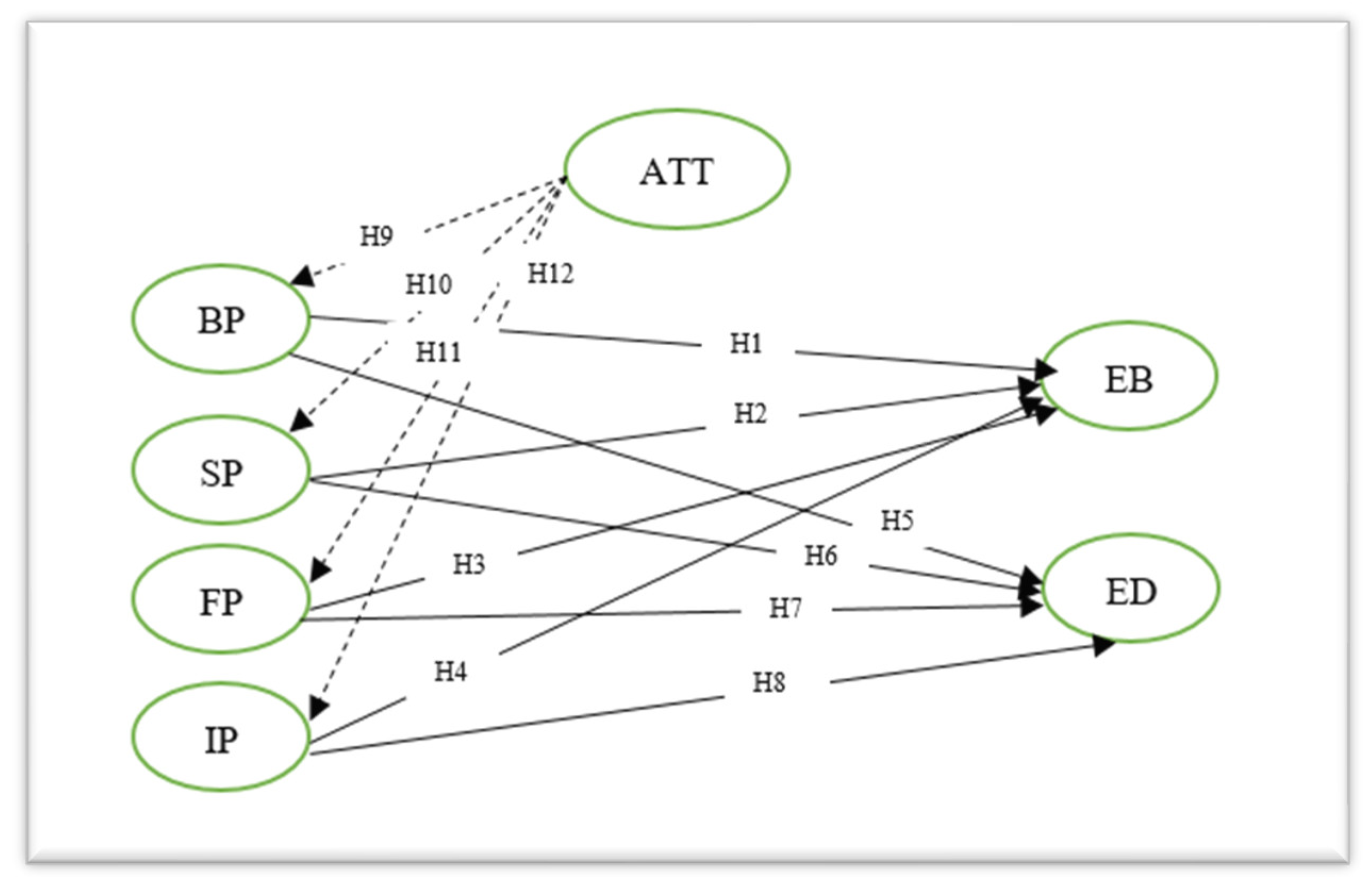

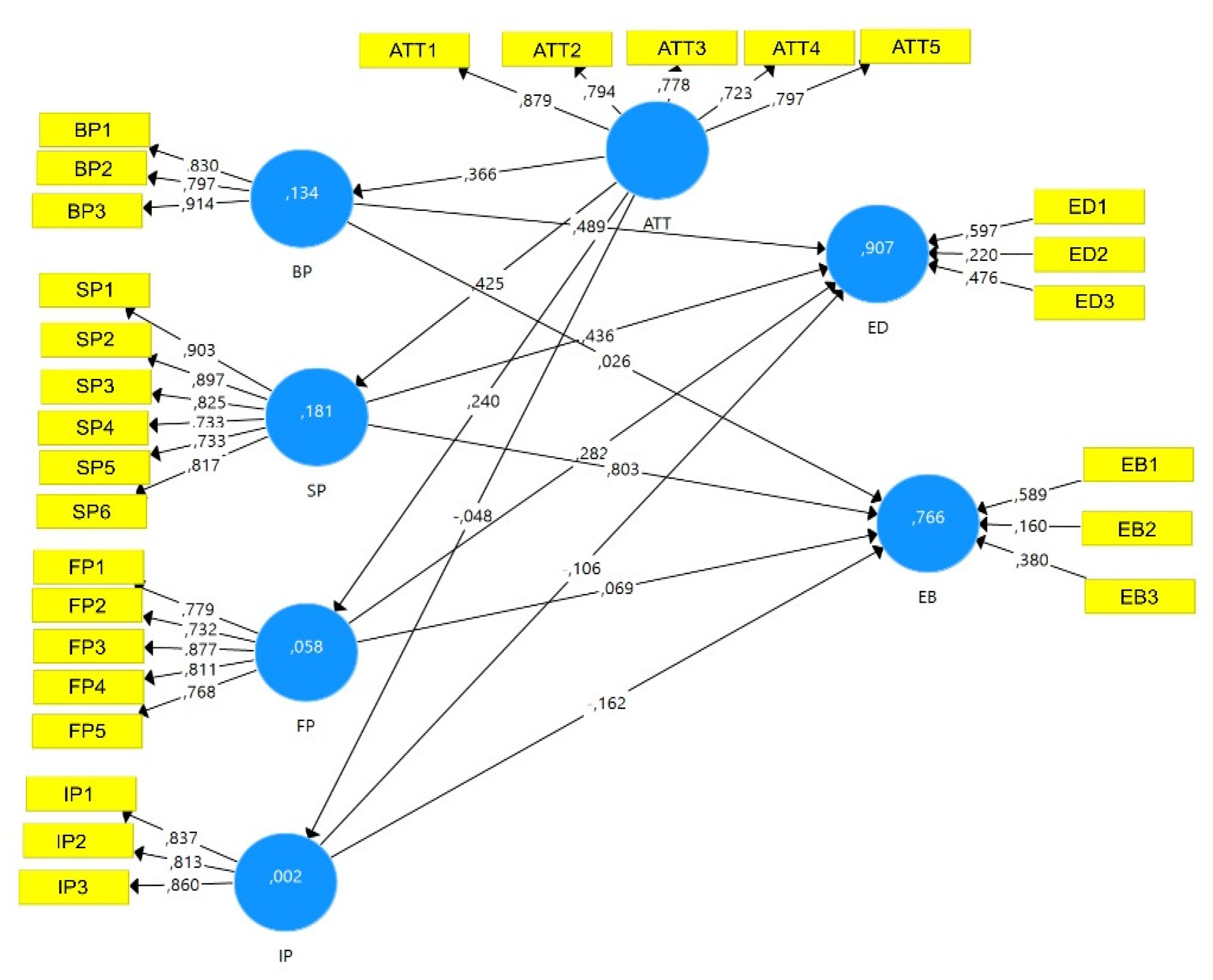

2], and their environmental activities, but they do not sufficiently articulate their own responsibility in relation to sustainable development. Such an attitude can be related to the volume of production, i.e., share in the total wine industry. This research should fill this gap, i.e., explain the importance of knowing the performance of wineries and their impact on environmental behavior for agro-managers and other actors. The purpose of the research is to examine the performance of small wineries in Serbia in relation to environmental behavior. Since the business performance of wineries includes several segments, the following research is aimed at examining the conditionality and the degree of impact and significance of these performances on environmental behavior. The following are hypotheses that show the connection (

Figure 1) between the business performance of wineries and environmental behavior (EB):

Hypothesis 1 (H1): There is a positive connection between brand performance (BP) and environmental behavior (EB).

Hypothesis 2 (H2): There is a positive connection between service performance (SP) and environmental behavior (EB).

Hypothesis 3 (H3): There is a positive connection between innovative performance (IP) and environmental behavior (EB).

Hypothesis 4 (H4): There is a positive connection between financial performance (FP) and environmental behavior (EB).

2.3. Environmental Disclosure and Business Peformance

As Malarvizhi and Matta [

108] stated, sustainability reporting is the reporting of credible and relevant corporate environmental, social and economic performance [

109]. Campbell [

110] defined environmental disclosure as the presentation of data on activities affected by organizational processes or operations to the natural environment. Environmental disclosure provides a comprehensive picture of the company’s capabilities in the long run. It portrays the company’s social responsibility, its sustainable development, corporate governance and the company’s impact on the environment and society. The economic effects of companies’ operations on society and the environment are the subject of sustainability reports, whether they are an integral part of annual reports or as separate sustainability reports [

111]. In the process of managing companies, managers make decisions about the environment. Such sustainable business and commitment to the environment is a segment of strategic management [

112,

113]. It is logical that companies do not want to publish reports of violations of environmental laws and want to avoid the risk of paying fines [

108]. In order for companies to present positive information about the environment, they must work on improving their environmental impact, i.e., business performance. Stevanović and Petrović-Randjelović [

114] pointed out that environmental issues are critical success factors in creating a positive image of the company [

108] in modern business conditions.

The size of the company is most often directly related to the publication of environmental data and, as Gray et al. [

115] stated, the level of environmental disclosures differs between firms, the whole industry, and states [

116]. As Knight et al. [

97] stated, large companies are focused on reporting on long-term environmental policies and use publicly available documents (annual reports, environmental reports). Small companies dealing with environmental issues often do not publish such information when needed. Even, small wineries choose not to publish data on environmental activities. The reasons and justification for that are found in the reservations of consumers, the fear that activities may be misinterpreted, or that they may harm the brand.

On the other hand, environmental disclosure can be related to the so-called reputational risk, so it is important to pay attention and act preventively. Research by Singh and Joshi [

117] indicated a positive relationship between profitability [

115,

117,

118], company size and environmental disclosures, while Molina-Azorín et al. [

112] pointed to a positive relationship between environmental disclosures and firm financial performance [

119]. Malarvizhi and Matta [

108] linked environmental disclosure to greater business opportunities, extra sales, due to the demand for cleaner products. They pointed out that environmentally responsible companies will have a better relationship with customers, investors and employees. On the other hand, the findings of Abdul-Rahman et al. [

120] showed no significant association between firm performance and environmental disclosure.

Most of the previous studies refer to developed countries, developed companies or sectors. They do not raise the question of the need and importance of environmental disclosure, but analyze its impacts and effects. This topic has been researched in Serbia on the example of the textile industry [

9], banking sector [

121], multinational companies and service company [

122]. This study should fill the research gap and explain the relationship between business performance and the disclosure of environmental information on the example of wineries. Finally, in this research, we start from the existence of a positive relationship between (

Figure 1) winery performance and environmental disclosure.

Hypothesis 5 (H5): There is a positive connection between brand performance (BP) and environmental disclosure (ED).

Hypothesis 6 (H6): There is a positive connection between service performance (SP) and environmental disclosure (ED).

Hypothesis 7 (H7): There is a positive connection between innovative performance (IP) and environmental disclosure (ED).

Hypothesis 8 (H8): There is a positive connection between financial performance (FP) and environmental disclosure (ED).

2.4. Attitudes and Business Performance

The environmental attitudes determine the behavior of individuals in the environment. They are often associated with moral norms, customs and lead to the improvement of human behavior, i.e., the establishment of positive interaction with the environment [

123]. Environmental attitudes of managers and their intentions towards the environment [

124] depend on personal values [

125] and influence environmental decisions and define specific practices [

126]. Managers’ personal values influence environmental behavior, enable managers to distinguish between important and unimportant issues, influence other members of organizations, and can change the way they do business [

127,

128]. As Sharma [

129] pointed out, environmental strategies range from compliance with regulations and standard industry practices to voluntary actions to protect the environment. Managerial interpretation of environmental issues differs, problems are perceived as threats or opportunities depending on personal attitudes, personality traits [

130], but also organizational factors, company performance. Managers are ready to change the way the company operates depending on the beliefs on the human–environment relationship, through the selection of information. Papagiannakis and Lioukas [

131] went a step further and identified two types of personal values that are expected to shape managers’ environmental attitudes and impact on business and environmental behavior.

The implementation of the environmental behavior in wineries is strongly influenced by the managers and their attitudes [

132,

133], especially in small wineries where they are the owners and the managers and where they make all decisions, and logically, on the sustainable production [

134]. The managers’ environmental actions are a response to individual attitudes on the environment, as well as on the environmental disclosure. Gabadylova et al. [

135] concluded that the satisfaction of individuals and personal attitude towards the environment were decisive in the decision-making and sustainable wine production. The study of Singh et al. [

136] introduced the notion of green governance and green innovation and the impact on enterprise environmental performance. The authors concluded that a firm’s business performance depends on the quality of environmentally friendly products, green processes and product innovation, and the involvement of sustainable policies [

137,

138]. Moreover, not only can employee attitudes influence green product innovation and reduce the negative impact of business on the environment, but they can also increase the company’s financial and social performance. Šarković et al. [

139] identified the attitudes, behavior and willingness of farmers in Serbia to participate in solving environmental problems. Authors such as Aminrad [

140] concluded that formal education influences farmers’ decisions on key environmental and agricultural production issues. Thus, the attitudes of employees should not be perceived as pressure, but as organizational intentions and practices for increasing the performance and competitiveness of companies. Our study contributes to spreading knowledge on wineries managers/owners’ environmental attitudes and business performance. Second, our research should fill a gap on the key role of employees in a firm’s environmental ethics, its environmental performance, and its competitive advantage. Last but not least, our study should offer managers and practitioners the knowledge and information they need to use and manage business performance to increase environmental performance and sustainable economic success. The following are hypotheses that show the connection (

Figure 1) between ethical environmental attitudes and attitudes of wineries with the business performance of wineries:

Hypothesis 9 (H9): There is a positive connection between environmental attitudes (ATT) and brand performance (BP).

Hypothesis 10 (H10): There is a positive connection between environmental attitudes (ATT) and financial performance (FP).

Hypothesis 11 (H11): There is a positive connection between environmental attitudes (ATT) and service performance (SP).

Hypothesis 12 (H12): There is a positive connection between environmental attitudes (ATT) and innovative performance (IP).

,

,

{kind=link}

{kind=link}