Impact of Information Sharing and Forecast Combination on Fast-Moving-Consumer-Goods Demand Forecast Accuracy

Abstract

:1. Introduction

2. Literature Review

2.1. On Information Sharing

2.2. On Forecast Reconciliation

2.3. On Forecast Combination

2.4. On FMCG Forecasting

2.5. Section Summary

- Various information-sharing strategies in hierarchical FMCG demand forecasting. Four cases are elaborated, based on different levels of information sharing. Forecasting models are selected based on the available information in each case. More specifically, Case I (see below) considers univariate forecasting models (ARIMA and ETS); Case II considers a reduced ADL model; the forecasting models for Case III utilizes hierarchical reconciliation; and Case IV again uses the ADL model, but with more predictors.

- Hierarchical reconciliation procedure. It has three main steps: (1) arrange the data into a hierarchical structure, (2) generate base forecasts, and (3) reconcile the base forecasts. Two methods, namely, the bottom-up approach and the optimal reconciliation are used.

- Effect of combining forecasts. After the forecast accuracies under different levels of information sharing are compared, all models are subsequently treated as component models to investigate the effect of combining forecasts. A total of seven forecast combination methods are considered in this paper.

3. Cases of Different Levels of Information Sharing and Hierarchical Reconciliation

3.1. Case I

3.2. Case II

3.3. Case III

3.4. Case IV

4. Forecast Combination Methods

4.1. Simple Averaging

4.2. Trimmed Simple Averaging

4.3. Combination through Variance

4.4. Combination through Ordinary Least Squares

4.5. Combination through Least Absolute Deviations

4.6. Combination through Lasso

4.7. Combination through Complete Subset Regression

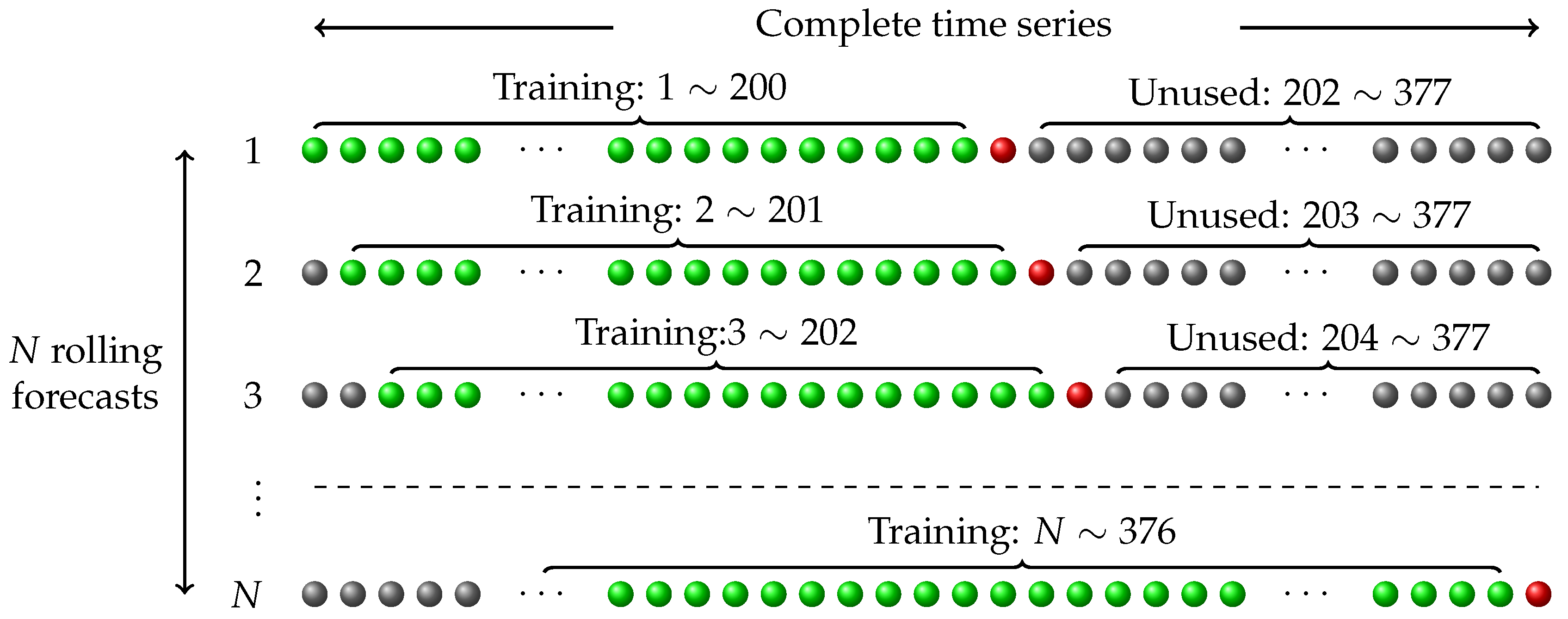

5. Empirical Study

5.1. Forecast Accuracies under Different Levels of Information Sharing

5.2. Forecast Accuracies of the Combined Forecasts

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| ACV | all commodity volume |

| ADL | autoregressive distributed lag |

| ARIMA | autoregressive integrated moving average |

| BJC | bottle juice category |

| DFF | Dominick’s Finer Food |

| ETS | exponential smoothing |

| FMCG | fast moving consumer goods |

| LAD | least absolute deviations |

| MAPE | mean absolute percentage error |

| OLS | ordinary least squares |

| UPC | universal product code |

| WLS | weighted least squares |

References

- Niranjan, T.T.; Wagner, S.M.; Aggarwal, V. Measuring information distortion in real-world supply chains. Int. J. Prod. Res. 2011, 49, 3343–3362. [Google Scholar] [CrossRef]

- Ramanathan, U. Performance of supply chain collaboration—A simulation study. Expert Syst. Appl. 2014, 41, 210–220. [Google Scholar] [CrossRef]

- Wong, K.K.; Song, H.; Witt, S.F.; Wu, D.C. Tourism forecasting: To combine or not to combine? Tour. Manag. 2007, 28, 1068–1078. [Google Scholar] [CrossRef] [Green Version]

- Hibon, M.; Evgeniou, T. To combine or not to combine: selecting among forecasts and their combinations. Int. J. Forecast. 2005, 21, 15–24. [Google Scholar] [CrossRef]

- Palm, F.C.; Zellner, A. To combine or not to combine? Issues of combining forecasts. J. Forecast. 1992, 11, 687–701. [Google Scholar] [CrossRef]

- Bates, J.M.; Granger, C.W.J. The Combination of Forecasts. J. Oper. Res. Soc. 1969, 20, 451–468. [Google Scholar] [CrossRef]

- Gaur, V.; Giloni, A.; Seshadri, S. Information Sharing in a Supply Chain Under ARMA Demand. Manag. Sci. 2005, 51, 961–969. [Google Scholar] [CrossRef] [Green Version]

- Giloni, A.; Hurvich, C.; Seshadri, S. Forecasting and information sharing in supply chains under ARMA demand. IIE Trans. 2014, 46, 35–54. [Google Scholar] [CrossRef]

- Ali, M.M.; Boylan, J.E. Feasibility principles for Downstream Demand Inference in supply chains. J. Oper. Res. Soc. 2011, 62, 474–482. [Google Scholar] [CrossRef]

- Cui, R.; Allon, G.; Bassamboo, A.; Mieghem, J.A.V. Information Sharing in Supply Chains: An Empirical and Theoretical Valuation. Manag. Sci. 2015, 61, 2803–2824. [Google Scholar] [CrossRef] [Green Version]

- Ali, M.M.; Boylan, J.E. On the value of sharing demand information in supply chains. In Proceedings of the OR56 Annual Conference, London, UK, 9–11 September 2014; pp. 44–56. [Google Scholar]

- Gümüş, M. With or Without Forecast Sharing: Competition and Credibility under Information Asymmetry. Prod. Oper. Manag. 2014, 23, 1732–1747. [Google Scholar] [CrossRef]

- Özer, O.; Zheng, Y.; Ren, Y. Trust, Trustworthiness, and Information Sharing in Supply Chains Bridging China and the United States. Manag. Sci. 2014, 60, 2435–2460. [Google Scholar] [CrossRef] [Green Version]

- Özer, O.; Zheng, Y.; Chen, K.Y. Trust in Forecast Information Sharing. Manag. Sci. 2011, 57, 1111–1137. [Google Scholar] [CrossRef] [Green Version]

- Cachon, G.P.; Lariviere, M.A. Contracting to Assure Supply: How to Share Demand Forecasts in a Supply Chain. Manag. Sci. 2001, 47, 629–646. [Google Scholar] [CrossRef] [Green Version]

- Friedman, J.W. A Non-cooperative Equilibrium for Supergames. Rev. Econ. Stud. 1971, 38, 1–12. [Google Scholar] [CrossRef]

- Yagli, G.M.; Yang, D.; Srinivasan, D. Reconciling solar forecasts: Sequential reconciliation. Sol. Energy 2019, 179, 391–397. [Google Scholar] [CrossRef]

- Yang, D.; Quan, H.; Disfani, V.R.; Rodríguez-Gallegos, C.D. Reconciling solar forecasts: Temporal hierarchy. Sol. Energy 2017, 158, 332–346. [Google Scholar] [CrossRef]

- Yang, D.; Quan, H.; Disfani, V.R.; Liu, L. Reconciling solar forecasts: Geographical hierarchy. Sol. Energy 2017, 146, 276–286. [Google Scholar] [CrossRef]

- Hong, T.; Xie, J.; Black, J. Global energy forecasting competition 2017: Hierarchical probabilistic load forecasting. Int. J. Forecast. 2019. [Google Scholar] [CrossRef]

- Athanasopoulos, G.; Ahmed, R.A.; Hyndman, R.J. Hierarchical forecasts for Australian domestic tourism. Int. J. Forecast. 2009, 25, 146–166. [Google Scholar] [CrossRef] [Green Version]

- Yang, D.; Goh, G.S.W.; Jiang, S.; Zhang, A.N.; Akcan, O. Forecast UPC-level FMCG demand, Part II: Hierarchical reconciliation. In Proceedings of the IEEE International Conference on Big Data (Big Data), Santa Clara, CA, USA, 29 October–1 November 2015; pp. 2113–2121. [Google Scholar] [CrossRef]

- Bray, R.L.; Mendelson, H. Information Transmission and the Bullwhip Effect: An Empirical Investigation. Manag. Sci. 2012, 58, 860–875. [Google Scholar] [CrossRef] [Green Version]

- Chen, F.; Drezner, Z.; Ryan, J.K.; Simchi-Levi, D. Quantifying the Bullwhip Effect in a Simple Supply Chain: The Impact of Forecasting, Lead Times, and Information. Manag. Sci. 2000, 46, 436–443. [Google Scholar] [CrossRef] [Green Version]

- Hyndman, R.J.; Ahmed, R.A.; Athanasopoulos, G.; Shang, H.L. Optimal combination forecasts for hierarchical time series. Comput. Stat. Data Anal. 2011, 55, 2579–2589. [Google Scholar] [CrossRef] [Green Version]

- Hyndman, R.J.; Lee, A.J.; Wang, E. Fast computation of reconciled forecasts for hierarchical and grouped time series. Comput. Stat. Data Anal. 2016, 97, 16–32. [Google Scholar] [CrossRef] [Green Version]

- Wickramasuriya, S.L.; Athanasopoulos, G.; Hyndman, R.J. Forecasting Hierarchical and Grouped Time Series through Trace Minimization; Working Paper 15/15; Department of Econometrics & Business Statistics, Monash University: Melbourne, Australia, 2015. [Google Scholar]

- Granger, C.W.J. Invited review combining forecasts—Twenty years later. J. Forecast. 1989, 8, 167–173. [Google Scholar] [CrossRef]

- Yang, D.; Dong, Z. Operational photovoltaics power forecasting using seasonal time series ensemble. Sol. Energy 2018, 166, 529–541. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, N.; Tan, Y.; Hong, T.; Kirschen, D.S.; Kang, C. Combining Probabilistic Load Forecasts. IEEE Trans. Smart Grid 2019, 10, 3664–3674. [Google Scholar] [CrossRef]

- Baran, S.; Lerch, S. Combining predictive distributions for the statistical post-processing of ensemble forecasts. Int. J. Forecast. 2018, 34, 477–496. [Google Scholar] [CrossRef] [Green Version]

- De Menezes, L.M.; Bunn, D.W.; Taylor, J.W. Review of guidelines for the use of combined forecasts. Eur. J. Oper. Res. 2000, 120, 190–204. [Google Scholar] [CrossRef]

- Berry, S.; Levinsohn, J.; Pakes, A. Automobile Prices in Market Equilibrium. Econometrica 1995, 63, 841–890. [Google Scholar] [CrossRef]

- Nevo, A. Measuring Market Power in the Ready-to-Eat Cereal Industry. Econometrica 2001, 69, 307–342. [Google Scholar] [CrossRef] [Green Version]

- Muller-Navarra, M.; Lessmann, S.; Voss, S. Sales Forecasting with Partial Recurrent Neural Networks: Empirical Insights and Benchmarking Results. In Proceedings of the 48th Hawaii International Conference on System Sciences (HICSS), Kauai, HI, USA, 5–8 January 2015; pp. 1108–1116. [Google Scholar] [CrossRef]

- Fildes, R.; Nikolopoulos, K.; Crone, S.F.; Syntetos, A.A. Forecasting and operational research: A review. J. Oper. Res. Soc. 2008, 59, 1150–1172. [Google Scholar] [CrossRef]

- Fildes, R.; Goodwin, P.; Lawrence, M.; Nikolopoulos, K. Effective forecasting and judgmental adjustments: an empirical evaluation and strategies for improvement in supply-chain planning. Int. J. Forecast. 2009, 25, 3–23. [Google Scholar] [CrossRef]

- Ali, O.G.; Sayin, S.; van Woensel, T.; Fransoo, J. SKU demand forecasting in the presence of promotions. Expert Syst. Appl. 2009, 36, 12340–12348. [Google Scholar] [CrossRef]

- Huang, T.; Fildes, R.; Soopramanien, D. The value of competitive information in forecasting FMCG retail product sales and the variable selection problem. Eur. J. Oper. Res. 2014, 237, 738–748. [Google Scholar] [CrossRef]

- Tibshirani, R. Regression Shrinkage and Selection via the Lasso. J. R. Stat. Soc. Ser. B (Methodol.) 1996, 58, 267–288. [Google Scholar] [CrossRef]

- Toro-González, D.; McCluskey, J.J.; Mittelhammer, R.C. Beer Snobs do Exist: Estimation of Beer Demand by Type. J. Agric. Resour. Econ. 2014, 39, 174–187. [Google Scholar]

- Jami, A.; Mishra, H. Downsizing and Supersizing: How Changes in Product Attributes Influence Consumer Preferences. J. Behav. Decis. Mak. 2014, 27, 301–315. [Google Scholar] [CrossRef]

- Chahrour, R.A. Sales and price spikes in retail scanner data. Econ. Lett. 2011, 110, 143–146. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Component Models | Combined Forecasts | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| UPC | C1ets | C1arima | C2adl | C3bu | C3opt | C4adl | Avg | Trim | Var | Ols | Lad | Lasso | Subset | |

| 7045011402 | 55 | 10.97 | 10.88 | 9.44 | 7.48 | 6.97 | 7.77 | 7.35 | 7.23 | 7.19 | 6.73 | 8.13 | 6.87 | 6.85 |

| 5300015154 | 61 | 9.58 | 9.51 | 9.49 | 9.24 | 9.06 | 9.33 | 8.76 | 8.74 | 8.77 | 9.46 | 8.94 | 9.12 | 9.08 |

| 5300015108 | 64 | 13.10 | 14.02 | 11.83 | 10.39 | 10.41 | 11.71 | 11.40 | 11.02 | 11.35 | 11.85 | 10.57 | 11.61 | 12.08 |

| 3828103123 | 61 | 17.06 | 17.33 | 16.53 | 20.13 | 19.42 | 17.15 | 15.36 | 15.43 | 15.68 | 12.37 | 11.85 | 12.32 | 13.51 |

| 3828103091 | 66 | 38.12 | 40.32 | 34.03 | 22.21 | 22.20 | 27.46 | 27.78 | 26.96 | 26.42 | 29.16 | 18.85 | 26.48 | 27.77 |

| 3828103025 | 52 | 57.05 | 52.18 | 24.51 | 18.13 | 17.72 | 17.10 | 24.59 | 20.54 | 22.23 | 48.04 | 16.13 | 46.25 | 30.65 |

| 3828103021 | 63 | 113.02 | 211.64 | 53.78 | 35.91 | 35.62 | 37.02 | 72.00 | 47.21 | 50.81 | 47.75 | 40.71 | 52.98 | 44.78 |

| 3120027407 | 42 | 29.46 | 36.50 | 28.61 | 17.94 | 18.09 | 12.47 | 21.27 | 20.07 | 17.25 | 13.23 | 10.61 | 13.23 | 13.61 |

| 3120027007 | 53 | 26.89 | 32.80 | 29.31 | 12.35 | 12.48 | 13.24 | 18.35 | 17.24 | 13.66 | 13.98 | 12.22 | 17.15 | 14.20 |

| 3120026134 | 52 | 26.42 | 24.26 | 24.79 | 11.33 | 11.49 | 12.68 | 16.42 | 15.45 | 13.09 | 11.94 | 11.91 | 12.09 | 11.81 |

| 3120021007 | 62 | 26.42 | 29.21 | 21.93 | 12.08 | 12.05 | 10.62 | 15.12 | 14.10 | 11.56 | 12.25 | 11.01 | 23.78 | 12.74 |

| 3120020035 | 63 | 22.45 | 22.91 | 19.61 | 8.99 | 8.94 | 9.01 | 12.91 | 11.99 | 9.88 | 9.16 | 9.60 | 14.28 | 9.14 |

| 3120020007 | 65 | 32.73 | 28.84 | 21.33 | 10.56 | 10.43 | 9.56 | 14.66 | 12.73 | 10.52 | 17.65 | 15.78 | 18.26 | 15.64 |

| 3120020005 | 66 | 54.05 | 52.50 | 32.74 | 11.26 | 11.36 | 11.92 | 26.33 | 23.57 | 16.96 | 15.55 | 14.36 | 39.36 | 12.18 |

| 1480031656 | 65 | 75.89 | 58.68 | 33.14 | 22.87 | 22.90 | 22.76 | 30.83 | 25.69 | 27.78 | 30.98 | 28.83 | 27.16 | 28.71 |

| 1480000034 | 67 | 84.17 | 73.04 | 39.76 | 27.50 | 27.96 | 28.71 | 38.12 | 34.39 | 30.93 | 36.07 | 24.96 | 33.80 | 38.29 |

| 7045011328 | 61 | 10.81 | 11.59 | 12.45 | 11.20 | 10.77 | 8.31 | 9.54 | 9.26 | 9.24 | 9.04 | 8.76 | 8.36 | 8.66 |

| 5300015132 | 66 | 15.13 | 16.72 | 15.47 | 17.82 | 16.73 | 18.55 | 14.85 | 14.40 | 14.99 | 14.33 | 14.15 | 14.76 | 14.39 |

| 4850000193 | 34 | 29.11 | 29.52 | 25.98 | 13.01 | 13.06 | 13.46 | 18.34 | 17.28 | 15.70 | 14.90 | 12.03 | 12.26 | 13.61 |

| 4180022700 | 54 | 10.46 | 10.91 | 10.06 | 16.01 | 14.86 | 9.65 | 10.59 | 10.36 | 9.98 | 9.92 | 9.68 | 10.16 | 10.31 |

| 4180020750 | 65 | 11.26 | 11.80 | 10.28 | 14.71 | 14.00 | 9.42 | 10.37 | 10.29 | 10.17 | 9.71 | 9.81 | 18.25 | 9.83 |

| 4176000394 | 64 | 261.68 | 279.95 | 51.56 | 35.86 | 34.19 | 33.35 | 108.79 | 89.05 | 46.47 | 59.35 | 32.44 | 49.71 | 54.45 |

| 3828103017 | 67 | 71.01 | 75.98 | 47.17 | 25.85 | 25.59 | 27.98 | 39.33 | 36.35 | 31.07 | 36.36 | 28.24 | 32.84 | 29.60 |

| 3828103009 | 40 | 15.77 | 14.25 | 13.96 | 12.13 | 11.51 | 11.34 | 12.11 | 12.09 | 12.02 | 11.85 | 11.57 | 12.23 | 11.99 |

| 3120027005 | 39 | 34.41 | 33.18 | 33.07 | 17.49 | 17.69 | 18.63 | 23.79 | 22.11 | 20.09 | 17.09 | 17.58 | 17.83 | 18.42 |

| 3120026107 | 56 | 33.09 | 32.66 | 23.02 | 11.28 | 11.22 | 11.09 | 17.07 | 15.97 | 12.00 | 17.98 | 13.20 | 16.03 | 14.73 |

| 3120026105 | 45 | 67.83 | 72.35 | 48.22 | 19.81 | 22.30 | 22.51 | 39.21 | 35.34 | 28.42 | 24.59 | 20.01 | 27.16 | 26.31 |

| 3120021005 | 41 | 52.78 | 52.54 | 40.44 | 16.69 | 17.04 | 17.65 | 30.48 | 27.86 | 22.73 | 18.07 | 13.97 | 15.98 | 17.31 |

| 3828103115 | 7 | 34.80 | 36.58 | 38.50 | 28.60 | 29.94 | 31.73 | 31.94 | 31.40 | 31.48 | 30.37 | 31.63 | 38.95 | 33.69 |

| 3828103033 | 61 | 24.86 | 23.09 | 20.71 | 19.39 | 19.28 | 18.55 | 18.44 | 18.54 | 18.10 | 18.95 | 19.38 | 23.70 | 18.68 |

| 3828103005 | 41 | 16.05 | 14.29 | 15.51 | 15.15 | 14.01 | 13.14 | 13.14 | 13.07 | 13.15 | 13.46 | 13.51 | 13.30 | 13.41 |

| 3120027405 | 26 | 39.52 | 37.32 | 34.64 | 19.68 | 20.17 | 19.39 | 26.39 | 24.16 | 22.59 | 16.01 | 16.80 | 17.35 | 17.90 |

| 1480000032 | 62 | 9.12 | 9.43 | 9.10 | 11.67 | 10.87 | 9.31 | 9.23 | 9.10 | 9.14 | 9.14 | 8.94 | 9.31 | 8.61 |

| 5300015407 | 7 | 25.03 | 25.06 | 24.26 | 24.61 | 23.96 | 24.58 | 24.02 | 23.90 | 24.06 | 24.63 | 25.03 | 25.25 | 24.84 |

| 7045011401 | 58 | 14.79 | 12.15 | 11.68 | 10.56 | 10.04 | 9.68 | 9.72 | 9.82 | 9.50 | 9.37 | 9.07 | 9.28 | 9.04 |

| 3120020000 | 59 | 10.71 | 10.74 | 10.79 | 11.26 | 11.08 | 10.61 | 10.31 | 10.42 | 10.31 | 10.62 | 10.08 | 10.54 | 10.67 |

| 1480051324 | 61 | 10.44 | 11.94 | 11.21 | 14.62 | 13.91 | 11.49 | 10.89 | 10.87 | 10.91 | 12.66 | 10.52 | 12.18 | 11.96 |

| Overall | 1971 | 40.50 | 43.63 | 24.29 | 16.60 | 16.36 | 16.06 | 23.10 | 20.54 | 17.94 | 19.36 | 15.63 | 20.57 | 18.18 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, D.; Zhang, A.N. Impact of Information Sharing and Forecast Combination on Fast-Moving-Consumer-Goods Demand Forecast Accuracy. Information 2019, 10, 260. https://doi.org/10.3390/info10080260

Yang D, Zhang AN. Impact of Information Sharing and Forecast Combination on Fast-Moving-Consumer-Goods Demand Forecast Accuracy. Information. 2019; 10(8):260. https://doi.org/10.3390/info10080260

Chicago/Turabian StyleYang, Dazhi, and Allan N. Zhang. 2019. "Impact of Information Sharing and Forecast Combination on Fast-Moving-Consumer-Goods Demand Forecast Accuracy" Information 10, no. 8: 260. https://doi.org/10.3390/info10080260

APA StyleYang, D., & Zhang, A. N. (2019). Impact of Information Sharing and Forecast Combination on Fast-Moving-Consumer-Goods Demand Forecast Accuracy. Information, 10(8), 260. https://doi.org/10.3390/info10080260