Fintech Services and the Drivers of Their Implementation in Small and Medium Enterprises

Abstract

:1. Introduction

2. Literature Review

2.1. Definition of Fintech

2.2. COVID-19 Impact

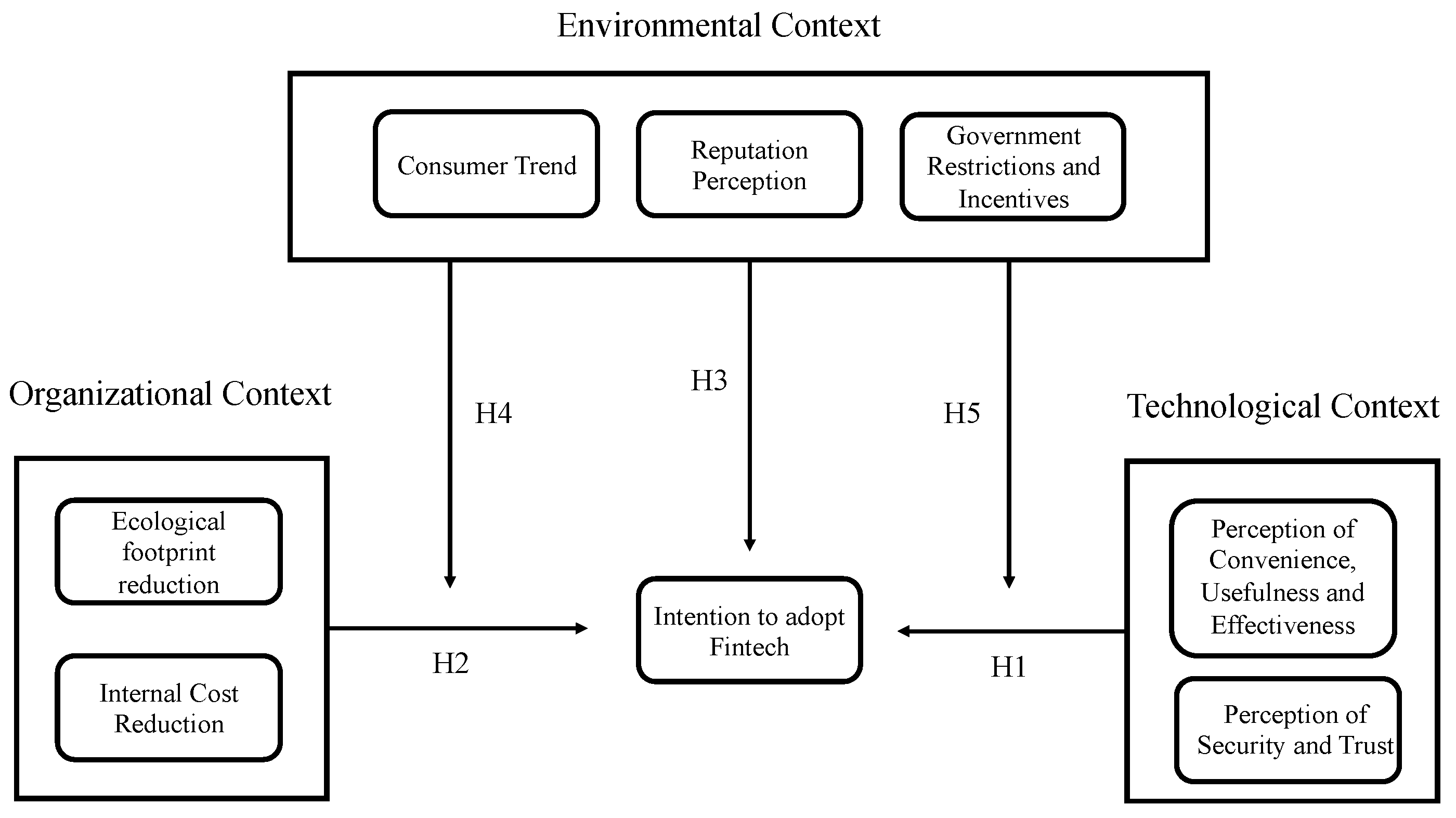

2.3. Presentation of the Conceptual Model and Research Hypotheses

2.3.1. TOE Framework

2.3.2. Technological Context—Convenience, Utility, and Effectiveness

Perception of Safety and Trust

2.3.3. Organizational Context

Internal Cost Reduction

Ecological Footprint Reduction

2.3.4. Environmental Context

Reputation and Branding Perception

Government Restrictions and Incentives

Consumer Trends

“Klarna acts as a search engine for local brands, which now have access to an ecosystem of 90 million customers. “(…) in Portugal, it will be fundamental to attract SMEs. The e-Commerce market comprises a percentage of large Portuguese companies, another percentage of international brands, and then there is a huge “long tail” of small national brands that together represent a very significant cake for this economy.”(p. 89)

3. Materials and Methods

3.1. Data Collection Procedure

3.2. Participants

3.3. Data Analysis Procedure

3.4. Instruments

4. Results

4.1. Descriptive Statistics of the Variables under Study

4.2. Descriptive Statistics of the Variables under Study

4.3. Hypothesis Testing

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ryu, H.-S. What Makes Users Willing or Hesitant to Use Fintech? The Moderating Effect of User Type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Sebastiani, S.; Kazi, M.S. The Local FinTech Opportunity in a Post COVID-19 World. 2020. Available online: https://www.google.com.hk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwiHyMvv5uv5AhU1gMYKHURVAAUQFnoECAsQAQ&url=https%3A%2F%2Fwww.pwc.com%2Fm1%2Fen%2Fpublications%2Fdocuments%2Flocal-fintech-opportunity-post-covid-19-world.pdf&usg=AOvVaw0hLdi_k7Kh5K0g9kaVmQ3y (accessed on 27 April 2022).

- Arslanian, H.; Fischer, F. The Rise of Fintech. In The Future of Finance; Springer International Publishing: Cham, Switzerland, 2019. [Google Scholar]

- Gu, S.; Ślusarczyk, B.; Hajizada, S.; Kovalyova, I.; Sakhbieva, A. Impact of the COVID-19 Pandemic on Online Consumer Purchasing Behavior. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 2263–2281. [Google Scholar] [CrossRef]

- Schindler, J. FinTech and Financial Innovation: Drivers and Depth. Financ. Econ. Discuss. Ser. 2017. [Google Scholar] [CrossRef]

- Gonçalves, R.; Martins, J.; Pereira, J.; Cota, M.; Branco, F. Promoting E-Commerce Software Platforms Adoption as a Means to Overcome Domestic Crises: The Cases of Portugal and Spain Approached from a Focus-Group Perspective. In Trends and Applications in Software Engineering; Mejia, J., Munoz, M., Rocha, Á., Calvo-Manzano, J., Eds.; Springer International Publishing: Cham, Switzerland, 2016; pp. 259–269. ISBN 978-3-319-26285-7. [Google Scholar]

- Priyatingsih, K.; Triantono, H.B. Fintech Accelerates Economic Recovery Solutions from COVID-19. In Proceedings of the 6th International ACM In-Cooperation HCI and UX Conference (CHIuXID), Jakarta & Bandung, Indonesia, 21–23 October 2020; pp. 25–28. [Google Scholar]

- Fu, J.; Mishra, M. The Global Impact of COVID-19 on Fintech Adoption; Swiss Finance Institute: Zürich, Switzerland, 2020. [Google Scholar]

- Sinha, S.; Huraimel, K.A. Reimagining Businesses with AI; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2020. [Google Scholar]

- Mekinjić, B.; Grujić, M.; Vujičić-Stefanović, D. Influence of Digitalisation and Technological Innovations in the Financial Market on the Development of the Financial Market. Ekon. Preduz. 2020, 68, 270. [Google Scholar] [CrossRef]

- Lexis Nexis LexisNexis® Risk Solutions 2019 True Cost of Fraud™ Study. 2019. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwj4iN34mOr5AhUQ-4UKHaxgCIAQFnoECAsQAQ&url=https%3A%2F%2Frisk.lexisnexis.com%2F-%2Fmedia%2Ffiles%2Ffinancial%2520services%2Fresearch%2Flnrs-2019-true-cost-of-fraud-financial-report-services-and-lending-nxr14106-00-1019-en-us.pdf&usg=AOvVaw0jNYicEEeUsdpDptmjcpu3 (accessed on 27 April 2022).

- Spínola, C.; Orgeira, J.; Moreira, M. FinTech Report; Nova School of Business & Economics: Lisbon, Portugal, 2020. [Google Scholar]

- Leong, K.; Sung, A. FinTech (Financial Technology): What Is It and How to Use Technologies to Create Business Value in Fintech Way? Int. J. Innov. Manag. Technol. 2018, 9, 74–78. [Google Scholar] [CrossRef]

- Arner, D.; Barberis, J.; Buckley, R. The Evolution of Fintech: A New Post-Crisis Paradigm? 2015. Available online: https://ssrn.com/abstract=2676553 (accessed on 27 April 2022).

- Lee, T.H.; Kim, H.W. An Exploratory Study on Fintech Industry in Korea: Crowdfunding Case. In Proceedings of the International Conference on Innovative Engineering Technologies, Bangkok, Thailand, 7 August 2015. [Google Scholar]

- Quirk, E. The Intersection of ERP and Fintech. Available online: https://solutionsreview.com/enterprise-resource-planning/the-intersection-of-erp-and-fintech/ (accessed on 24 July 2022).

- Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and Financial Inclusion. Eur. Bus. Organ. Law Rev. 2020, 21, 7–35. [Google Scholar] [CrossRef]

- Zveryakov, M.; Kovalenko, V.; Sheludko, S.; Sharah, E. FinTech Sector and Banking Business: Competition or Symbiosis? Econ. Ann.-XXI 2019, 175, 53–57. [Google Scholar] [CrossRef]

- Moreira, M.D.N. Fintech Report—An Overview of The Iberian Fintech Market. 2020. Available online: https://run.unl.pt/bitstream/10362/106855/1/2019-20_S1-24155-36-Mariana_Moreira.pdf (accessed on 27 April 2022).

- Gabor, D.; Brooks, S. The Digital Revolution in Financial Inclusion: International Development in the Fintech Era. New Political Econ. 2017, 22, 423–436. [Google Scholar] [CrossRef]

- Swartz, K.L. Stored Value Facilities: Changing the Fintech Landscape in Hong Kong. J. Investig. Compliance 2017, 18, 107–110. [Google Scholar] [CrossRef]

- Hasan, R.; Ashfaq, M.; Shao, L. Evaluating Drivers of Fintech Adoption in The Netherlands. Glob. Bus. Rev. 2021, 1–14. [Google Scholar] [CrossRef]

- Arner, D.W.; Barberis, J.N.; Walker, J.; Buckley, R.P.; Zetzsche, D.A. Digital Finance & the COVID-19 Crisis. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Kergroach, S. SMEs Going Digital: Policy Challenges and Recommendations, Going Digital Toolkit Note, No. 15. 2021. Available online: https://goingdigital.oecd.org/data/notes/No15_ToolkitNote_DigitalSMEs.pdf (accessed on 27 April 2022).

- Saunders, M.N.K.; Lewis, P.; Adrian, T. Research Methods for Business Students, 8th ed.; Pearson: Harlow, UK, 2019. [Google Scholar]

- Baker, J. The Technology–Organization–Environment Framework. In Information Systems Theory; Dwivedi, Y., Wade, M., Schneberger, S., Eds.; Springer: New York, NY, USA, 2012; Volume 28, pp. 231–245. [Google Scholar] [CrossRef]

- Bijker, M.; Hart, M. Factors Influencing Pervasiveness of Organisational Business Intelligence. In Proceedings of the Third International Conference on Business Intelligence and Technology (BUSTECH), Valencia, Spain, 27 May–1 June 2013; pp. 21–26. [Google Scholar]

- Oliveira, T.; Martins, M.F. Literature Review of Information Technology Adoption Models at Firm Level. Electron. J. Inf. Syst. Eval. 2011, 14, 110–121. [Google Scholar]

- Kowtha, N.R.; Choon, T.W.I. Determinants of Website Development: A Study of Electronic Commerce in Singapore. Inf. Manag. 2001, 39, 227–242. [Google Scholar] [CrossRef]

- Wang, Y.-M.; Wang, Y.-S.; Yang, Y.-F. Understanding the Determinants of RFID Adoption in the Manufacturing Industry. Technol. Forecast. Soc. Chang. 2010, 77, 803–815. [Google Scholar] [CrossRef]

- Zhu, K.; Kraemer, K.L.; Dedrick, J. Information Technology Payoff in E-Business Environments: An International Perspective on Value Creation of E-Business in the Financial Services Industry. J. Manag. Inf. Syst. 2004, 21, 17–54. [Google Scholar] [CrossRef]

- Collins, P.D.; Hage, J.; Hull, F.M. Organizational and Technological Predictors of Change in Automaticity. Acad. Manag. J. 1988, 31, 512–543. [Google Scholar]

- Okazaki, S.; Mendez, F. Exploring Convenience in Mobile Commerce: Moderating Effects of Gender. Comput. Hum. Behav. 2013, 29, 1234–1242. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An Empirical Examination of Factors Influencing the Intention to Use Mobile Payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Kuo-Chuen, D.L.; Teo, E.G. Emergence of FinTech and the LASIC Principles. J. Financ. Perspect. 2015, 3, 24–36. [Google Scholar]

- Haddad, C.; Hornuf, L. The Emergence of the Global Fintech Market: Economic and Technological Determinants. Small Bus. Econ. 2019, 53, 81–105. [Google Scholar] [CrossRef]

- Pokorná, M.; Sponer, M. Social Lending and Its Risks. Procedia Soc. Behav. Sci. 2016, 220, 330–337. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Hille, E.; Nasir, M.A. Diversification in the Age of the 4th Industrial Revolution: The Role of Artificial Intelligence, Green Bonds and Cryptocurrencies. Technol. Forecast. Soc. Chang. 2020, 159, 120188. [Google Scholar] [CrossRef]

- Lashitew, A.A.; van Tulder, R.; Liasse, Y. Mobile Phones for Financial Inclusion: What Explains the Diffusion of Mobile Money Innovations? Res. Policy 2019, 48, 1201–1215. [Google Scholar] [CrossRef]

- Najib, M.; Ermawati, W.J.; Fahma, F.; Endri, E.; Suhartanto, D. FinTech in the Small Food Business and Its Relation with Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 88. [Google Scholar] [CrossRef]

- Mills, K.; McCarthy, B. How banks can compete against an army of fintech start-ups. Harv. Bus. Rev. 2017, 13, 1–5. [Google Scholar]

- Sanchiz, C. How Fintech Is Helping Small Businesses Grow-Sage Advice US. Available online: https://www.sage.com/en-us/blog/the-small-business-owners-guide-to-fintech/ (accessed on 13 June 2022).

- Lwin, M.; Wirtz, J.; Williams, J.D. Consumer Online Privacy Concerns and Responses: A Power–Responsibility Equilibrium Perspective. J. Acad. Mark. Sci. 2007, 35, 572–585. [Google Scholar] [CrossRef]

- Ernst & Young. Ernst & Young Global FinTech Adoption Index 2019, pp. 1–44. Available online: https://assets.ey.com/content/dam/ey-sites/ey-com/en_gl/topics/banking-and-capital-markets/ey-global-fintech-adoption-index.pdf (accessed on 27 April 2022).

- Statista Number of Fintech Startups Globally by Region 2021|Statista. Available online: https://www.statista.com/statistics/893954/number-fintech-startups-by-region/ (accessed on 13 June 2022).

- Lee, E.-Y.; Lee, S.-B.; Jeon, Y.J.J. Factors Influencing the Behavioral Intention to Use Food Delivery Apps. Soc. Behav. Personal. Int. J. 2017, 45, 1461–1473. [Google Scholar] [CrossRef]

- Morosan, C. Theoretical and Empirical Considerations of Guests’ Perceptions of Biometric Systems in Hotels. J. Hosp. Tour. Res. 2012, 36, 52–84. [Google Scholar] [CrossRef]

- Lam, S.Y.; Shankar, V. Asymmetries in the Effects of Drivers of Brand Loyalty Between Early and Late Adopters and Across Technology Generations. J. Interact. Mark. 2014, 28, 26–42. [Google Scholar] [CrossRef]

- Shin, D.-H. Modeling the Interaction of Users and Mobile Payment System: Conceptual Framework. Int. J. Hum. Comput. Interact. 2010, 26, 917–940. [Google Scholar] [CrossRef]

- Schuermann, P.; Schuermann, T. How a Cyber Attack Could Cause the Next Financial Crisis. Harv. Bus. Rev. 2018, 8, 1–6. [Google Scholar]

- Bull, T. How FinTechs Are a World of Choice for Small and Medium-Sized Enterprises; EY: 2019; pp. 1–9. Available online: https://www.ey.com/en_gl/banking-capital-markets/how-fintechs-are-a-world-of-choice-for-small-and-medium-sized-enterprises (accessed on 27 April 2022).

- Chau, P.Y.K.; Tam, K.Y. Factors Affecting the Adoption of Open Systems: An Exploratory Study. MIS Q. 1997, 21, 1–24. [Google Scholar] [CrossRef]

- OECD. OECD SME and Entrepreneurship Outlook 2019; OECD Publishing: Paris, France, 2019; ISBN 9789264374805. [Google Scholar]

- OECD. The Missing Entrepreneurs 2017: Policies for Inclusive Entrepreneurship; OECD Publishing: Paris, France, 2017; ISBN 9789264283596. [Google Scholar]

- Kabulova, J.; Stankevičienė, J. Valuation of FinTech Innovation Based on Patent Applications. Sustainability 2020, 12, 10158. [Google Scholar] [CrossRef]

- Moro-Visconti, R.; Cruz Rambaud, S.; López Pascual, J. Sustainability in FinTechs: An Explanation through Business Model Scalability and Market Valuation. Sustainability 2020, 12, 10316. [Google Scholar] [CrossRef]

- Macchiavello, E.; Siri, M. Sustainable Finance and Fintech: Can Technology Contribute to Achieving Environmental Goals? A Preliminary Assessment of ‘Green FinTech’. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- High Level Expert Group on Sustainable Finance-Secretariat Provided by the European Commission, Financing a Sustainable European Economy. Final Report 2018 by the High-Level Expert Group on Sustainable Finance. Secretariat Provided by the European Commission. 2018. Available online: https://ec.europa.eu/info/sites/default/files/180131-sustainable-finance-final-report_en.pdf (accessed on 27 April 2022).

- Busch, D. Sustainability Disclosure in the EU Financial Sector. In Sustainable Finance in Europe; Springer: Cham, Switzerland, 2021. [Google Scholar]

- Siri, M.; Zhu, S. Will the EU Commission Successfully Integrate Sustainability Risks and Factors in the Investor Protection Regime? A Research Agenda. Sustainability 2019, 11, 6292. [Google Scholar] [CrossRef]

- Jiang, X.; Shen, J.H.; Lee, C.-C.; Chen, C. Supply-Side Structural Reform and Dynamic Capital Structure Adjustment: Evidence from Chinese-Listed Firms. Pac. Basin Financ. J. 2021, 65, 101482. [Google Scholar] [CrossRef]

- Mayor, T. Fintech, Explained|MIT Sloan. Available online: https://mitsloan.mit.edu/ideas-made-to-matter/fintech-explained (accessed on 27 April 2022).

- Awa, H.O.; Ukoha, O.; Emecheta, B.C. Using T-O-E Theoretical Framework to Study the Adoption of ERP Solution. Cogent Bus. Manag. 2016, 3, 1196571. [Google Scholar] [CrossRef]

- Mansfield, E. Industrial Research and Technological Innovation. Econ. J. 1968, 78, 676–679. [Google Scholar] [CrossRef]

- Mansfield, E.; Rapoport, J.; Romeo, A.; Villani, E.; Wagner, S.; Husic, F. The Production and Application of New Industrial Technology. Acad. Manag. Rev. 1977. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model. Symmetry 2019, 11, 340. [Google Scholar] [CrossRef]

- Park, E.; Kim, H.; Ohm, J.Y. Understanding Driver Adoption of Car Navigation Systems Using the Extended Technology Acceptance Model. Behav. Inf. Technol. 2015, 34, 741–751. [Google Scholar] [CrossRef]

- Riyadh, A.N.; Bunker, D.; Rabhi, F. Barriers to E-Finance Adoption in Small and Medium Sized Enterprises (Smes) in Bangladesh. In Proceedings of the 5th Conference on Qualitative Research in IT, Brisbane, Australia, 17 November 2010. [Google Scholar]

- Shapiro, S.L.; Reams, L.; So, K.K.F. Is It Worth the Price? The Role of Perceived Financial Risk, Identification, and Perceived Value in Purchasing Pay-per-View Broadcasts of Combat Sports. Sport Manag. Rev. 2019, 22, 235–246. [Google Scholar] [CrossRef]

- Chandra, S.; Srivastava, S.C.; Theng, Y.-L. Evaluating the Role of Trust in Consumer Adoption of Mobile Payment Systems: An Empirical Analysis. Commun. Assoc. Inf. Syst. 2010, 27. [Google Scholar] [CrossRef] [Green Version]

- OECD Coronavirus (COVID-19): SME Policy Responses-OECD. Available online: https://read.oecd-ilibrary.org/view/?ref=119_119680-di6h3qgi4x&title=Covid-19_SME_Policy_Responses (accessed on 27 April 2022).

- European Commission Payment Services Directive and Interchange Regulation: Frequently Asked Questions. Available online: https://ec.europa.eu/commission/presscorner/detail/pt/MEMO_13_719 (accessed on 14 February 2022).

- Recuperar Portugal Investimento RE-C01-I01-Recuperar Portugal. Available online: https://recuperarportugal.gov.pt/2021/06/13/investimento-td-c16-i03/ (accessed on 14 February 2022).

- Chatzoglou, P.; Chatzoudes, D. Factors Affecting E-Business Adoption in SMEs: An Empirical Research. J. Enterp. Inf. Manag. 2016, 29, 327–358. [Google Scholar] [CrossRef]

- Kumar, D.; Fenn, C.J.; Normala, S.G. Technology Disruption and Business Performance in SMEs. Relig. Rev. Cienc. Soc. Humanid. 2019, 4, 130–138. [Google Scholar]

- Maduku, D.K.; Mpinganjira, M.; Duh, H. Understanding Mobile Marketing Adoption Intention by South African SMEs: A Multi-Perspective Framework. Int. J. Inf. Manag. 2016, 36, 711–723. [Google Scholar] [CrossRef]

- Nugroho, M.A.; Susilo, A.Z.; Fajar, M.A.; Rahmawati, D. Exploratory Study of SMEs Technology Adoption Readiness Factors. Procedia Comput. Sci. 2017, 124, 329–336. [Google Scholar] [CrossRef]

- Norrestad, F. Consumer Fintech Adoption Rates Globally from 2015 to 2019, by Category. Available online: https://www.statista.com/statistics/1055356/fintech-adoption-rates-globally-selected-countries-by-category/ (accessed on 27 April 2022).

- Gross, I.; Kriffy Perez, K.; Quah, B.-L. Why Hasn′t Apple Pay Replicated Alipay′s Success? Available online: https://hbr.org/2020/09/why-hasnt-apple-pay-replicated-alipays-success (accessed on 11 April 2022).

- Almeida, D. Lisboa Queremos romper com a banca tradicional. Marketeer 2022, 86–89. [Google Scholar]

- Zhang-Zhang, Y.; Rohlfer, S.; Rajasekera, J. An Eco-Systematic View of Cross-Sector Fintech: The Case of Alibaba and Tencent. Sustainability 2020, 12, 8907. [Google Scholar] [CrossRef]

- Anagnostopoulos, I. Fintech and Regtech: Impact on Regulators and Banks. J. Econ. Bus. 2018, 100, 7–25. [Google Scholar] [CrossRef]

- Hommel, K.; Bican, P.M. Digital Entrepreneurship in Finance: Fintechs and Funding Decision Criteria. Sustainability 2020, 12, 8035. [Google Scholar] [CrossRef]

- Newman, D. Accounting for Change: Why Finance Should Lead Technology Adoption. Available online: https://www.sage.com/en-us/blog/why-finance-should-lead-technology-adoption/ (accessed on 13 June 2022).

- Vilelas, J. Investigação-O Processo de Construção Do Conhecimento; Edições Sílabo.: Lisboa, Portugal, 2020; ISBN 9789895610976. [Google Scholar]

- Marôco, J. Análise Estatística Com o SPSS Statistics, 8th ed.; ReportNumber, Lda: Pêro Pinheiro, Portugal, 2021; ISBN 9789899676374. [Google Scholar]

- Leite, P. Working Like You Mean It: Contribuição Para A Tradução E Validação De Uma Escala De Meaningful Work; ISPA–Instituto Universitário Ciências Psicológicas, Sociais e da Vida: Lisboa, Portugal, 2018. [Google Scholar]

- Le, M.T.H. Examining Factors That Boost Intention and Loyalty to Use Fintech Post-COVID-19 Lockdown as a New Normal Behavior. Heliyon 2021, 7, e07821. [Google Scholar] [CrossRef] [PubMed]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, Business Models, Investment Decisions, and Challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- República Portuguesa Certificação de Maturidade Digital-Portugal Digital. Available online: https://portugaldigital.gov.pt/avaliar-a-maturidade-digital-e-certificar-a-sua-empresa/certificacao-de-maturidade-digital/ (accessed on 28 May 2022).

- Comissão Europeia. Proposta de Regulamento do Parlamento Europeu e do Conselho relativo às obrigações verdes europeias. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:e77212e8-df07-11eb-895a-01aa75ed71a1.0017.02/DOC_1&format=PDF (accessed on 28 May 2022).

- Aiken, L.S.; West, S.G. Multiple Regression: Testing and Interpreting Interactions; SAGE Publications, Inc.: Newbury Park, CA, USA, 1991. [Google Scholar]

- Smith, A. The Theory of Moral Sentiments; Penguin Classics: London, UK, 2010; ISBN 9780143105923. [Google Scholar]

- Smith, A. An Inquiry into the Nature and Causes of the Wealth of Nations; Liberty Fund: Carmel, IN, USA, 2003; ISBN 978-0865970069. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | t | p | Mean | Standard Deviation |

|---|---|---|---|---|

| Intention | 2.31 ** | 0.013 | 3.36 | 1.08 |

| Effectiveness | 4.92 *** | <0.001 | 3.44 | 0.63 |

| Utility | 5.32 *** | <0.001 | 3.41 | 0.54 |

| Trust | 5.33 *** | <0.001 | 3.44 | 0.57 |

| Safety | 3.68 *** | <0.001 | 3.30 | 0.56 |

| Cost Reduction | 5.01 *** | <0.001 | 3.39 | 0.55 |

| Importance | 6.83 *** | <0.001 | 3.69 | 0.71 |

| Image | 8.85 *** | <0.001 | 3.65 | 0.51 |

| Reputation | 4.83 *** | <0.001 | 3.23 | 0.34 |

| Governmental Restrictions | 3.25 *** | 0.001 | 3.32 | 0.68 |

| Reduction of the Ecological Footprint | 5.67 *** | <0.001 | 4.90 | 1.11 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| -- | ||||||||||

| 0.37 *** | -- | |||||||||

| 0.39 *** | 0.23 | -- | ||||||||

| 0.53 *** | 0.54 *** | 0.26 * | -- | |||||||

| 0.22 | 0.08 | 0.50 *** | −0.06 | -- | ||||||

| 0.43 *** | 0.55 *** | 0.16 | 0.63 *** | −0.11 | -- | |||||

| 0.40 *** | 0.36 * | 0.18 | 0.15 | 0.31 ** | 0.27 * | -- | ||||

| 0.40 *** | 0.32 * | 0.17 | 0.30 * | 0.03 | 0.33 *** | 0.47 *** | -- | |||

| 0.35 ** | 0.28 ** | 0.32 ** | 0.32 ** | 0.36 ** | 0.18 | 0.31 ** | 0.13 | -- | ||

| 0.10 | 0.13 | −0.25 | −0.02 | −0.31 * | 0.28 | 0.14 | 0.34 * | 0.17 | -- | |

| 0.32 ** | 0.30 ** | 0.01 | 0.23 | −0.13 | 0.36 ** | 0.15 | 0.43 ** | 0.08 | 0.66 *** | -- |

| Predictor Variable | Dependent Variable | F | p | R2a | β | t | p |

|---|---|---|---|---|---|---|---|

| Effectiveness | Intention | 7.09 *** | 0.002 | 0.20 | 0.30 ** | 2.28 ** | 0.027 |

| Utility | 0.32 ** | 2.40 ** | 0.021 | ||||

| Trust | 12.09 *** | <0.001 | 0.32 | 0.55 *** | 4.55 *** | <0.001 | |

| Safety | 0.26 ** | 2.14 ** | 0.038 |

| Predictor Variable | Dependent Variable | F | p | R2a | β | t | p |

|---|---|---|---|---|---|---|---|

| Reduction of the Ecological Footprint | Intention | 5.19 ** | 0.027 | 0.10 | 0.32 ** | 2.28 ** | 0.027 |

| Internal Cost Reduction | 10.68 *** | 0.002 | 0.19 | 0.43 *** | 3.27 *** | 0.002 |

| Predictor Variable | Dependent Variable | F | p | R2a | β | t | p |

|---|---|---|---|---|---|---|---|

| Image | Intention | 5.72 *** | 0.005 | 0.22 | 0.36 *** | 2.80 *** | 0.007 |

| Reputation | 0.30 ** | 2.34 ** | 0.024 | ||||

| Importance | 9.04 *** | 0.004 | 0.14 | 0.40 *** | 3.01 *** | 0.004 | |

| Governmental Restrictions | 0.052 | 0.474 | 0.01 | 0.11 | 0.72 | 0.474 |

| Independents Variables | Intention to Adopt Fintech | |

|---|---|---|

| β Step 1 | β Step 2 | |

| Ecological Footprint | 0.26 | 0.27 |

| Importance | 0.22 | 0.14 |

| Image | 0.20 | 0.22 |

| Reputation | 0.21 | 0.21 |

| Governmental Restrictions | −0.13 | −0.09 |

| Footprint × Importance | −0.17 | |

| Footprint × Image | 0.01 | |

| Footprint × Reputation | −0.06 | |

| Footprint × Governmental Restrictions | −0.05 | |

| Overall F | 3.86 ** | 2.20 * |

| R2 | 0.31 | 0.34 |

| Δ | 0.03 | |

| Independents Variables | Intention to Adopt Fintech | |

|---|---|---|

| β Step 1 | β Step 2 | |

| Cost Reduction | 0.29 | 0.32 |

| Importance | 0.16 | 0.12 |

| Image | 0.21 | 0.21 |

| Reputation | 0.21 | 0.22 |

| Governmental Restrictions | −0.03 | −0.01 |

| Cost Reduction × Importance | 0.04 | |

| Cost Reduction × Image | −0.08 | |

| Cost Reduction × Reputation | −0.11 | |

| Cost Reduction × Governmental Restrictions | −0.01 | |

| Overall F | 4.51 *** | 2.43 ** |

| R2 | 0.34 | 0.36 |

| Δ | 0.02 | |

| Independents Variables | Intention to Adopt Fintech | |

|---|---|---|

| β Step 1 | β Step 2 | |

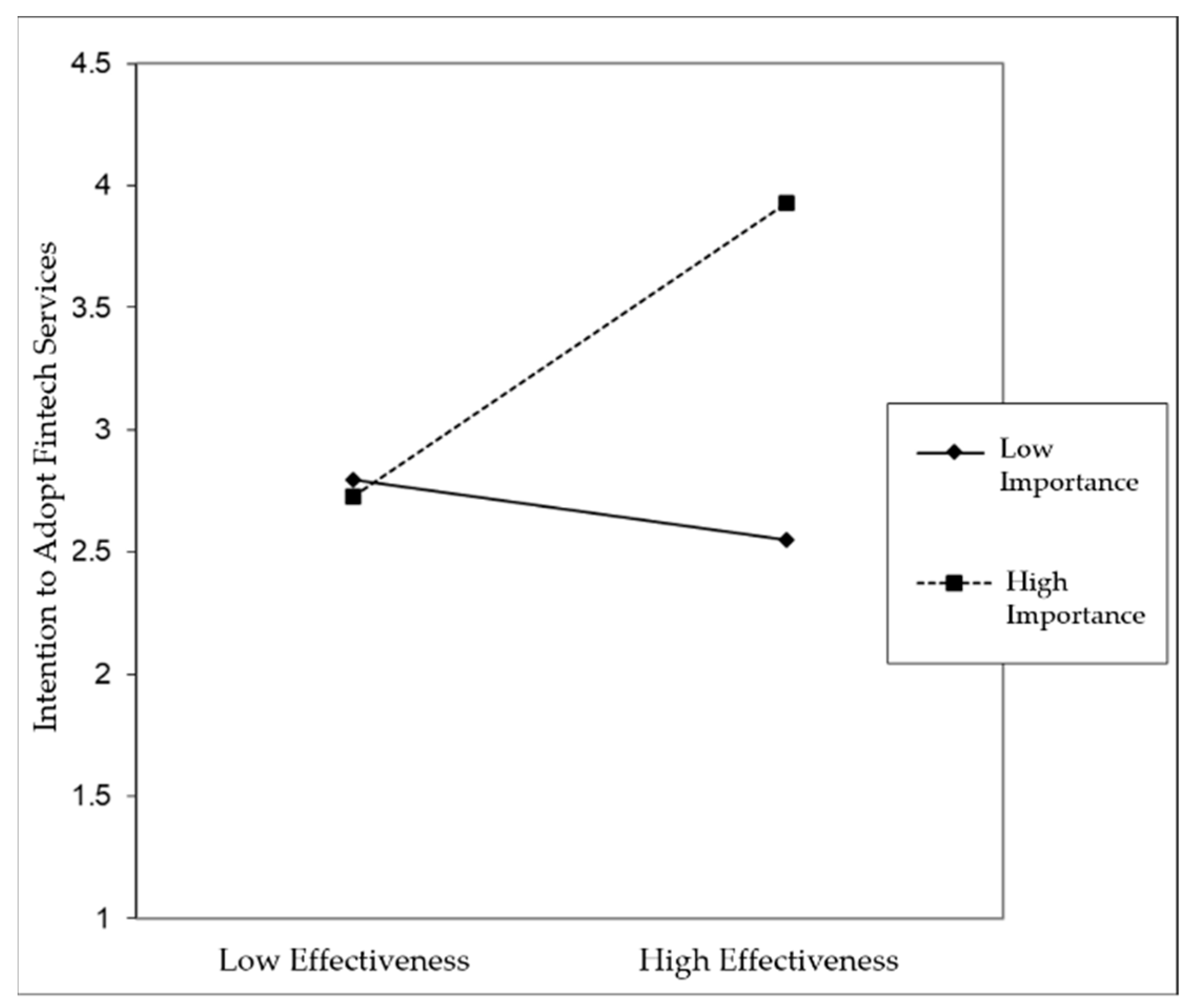

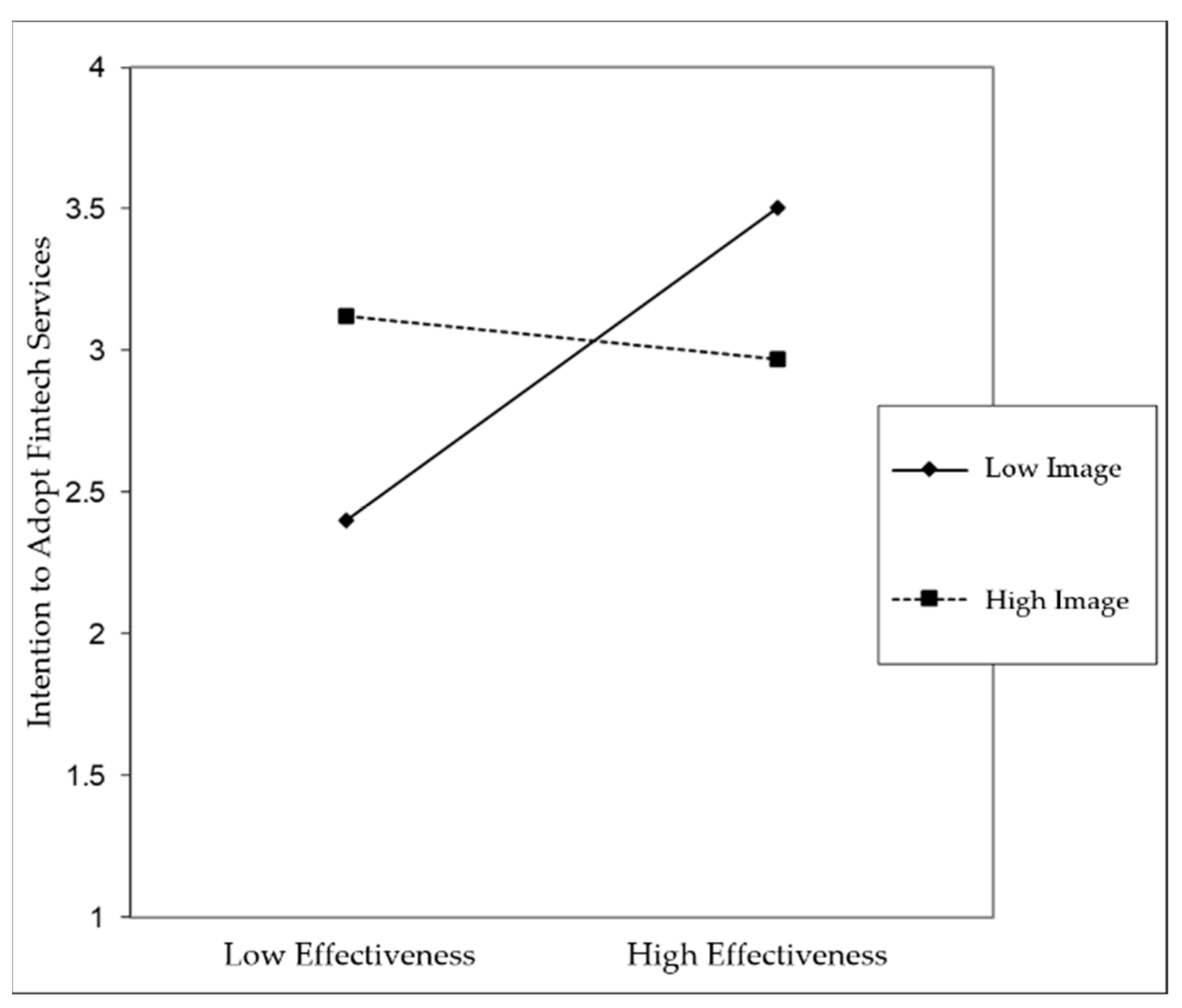

| Effectiveness | 0.18 | 0.22 |

| Importance | 0.16 | 0.30 * |

| Image | 0.23 | 0.04 |

| Reputation | 0.23 | 0.09 |

| Governmental Restrictions | 0.03 | 0.15 |

| Effectiveness × Importance | 0.31 * | |

| Effectiveness × Image | −0.31 * | |

| Effectiveness × Reputation | −0.22 | |

| Effectiveness × Governmental Restrictions | 0.07 | |

| Overall F | 3.72 *** | 3.01 *** |

| R2 | 0.30 | 0.41 |

| Δ | 0.11 | |

| Independents Variables | Intention to Adopt Fintech | |

|---|---|---|

| β Step 1 | β Step 2 | |

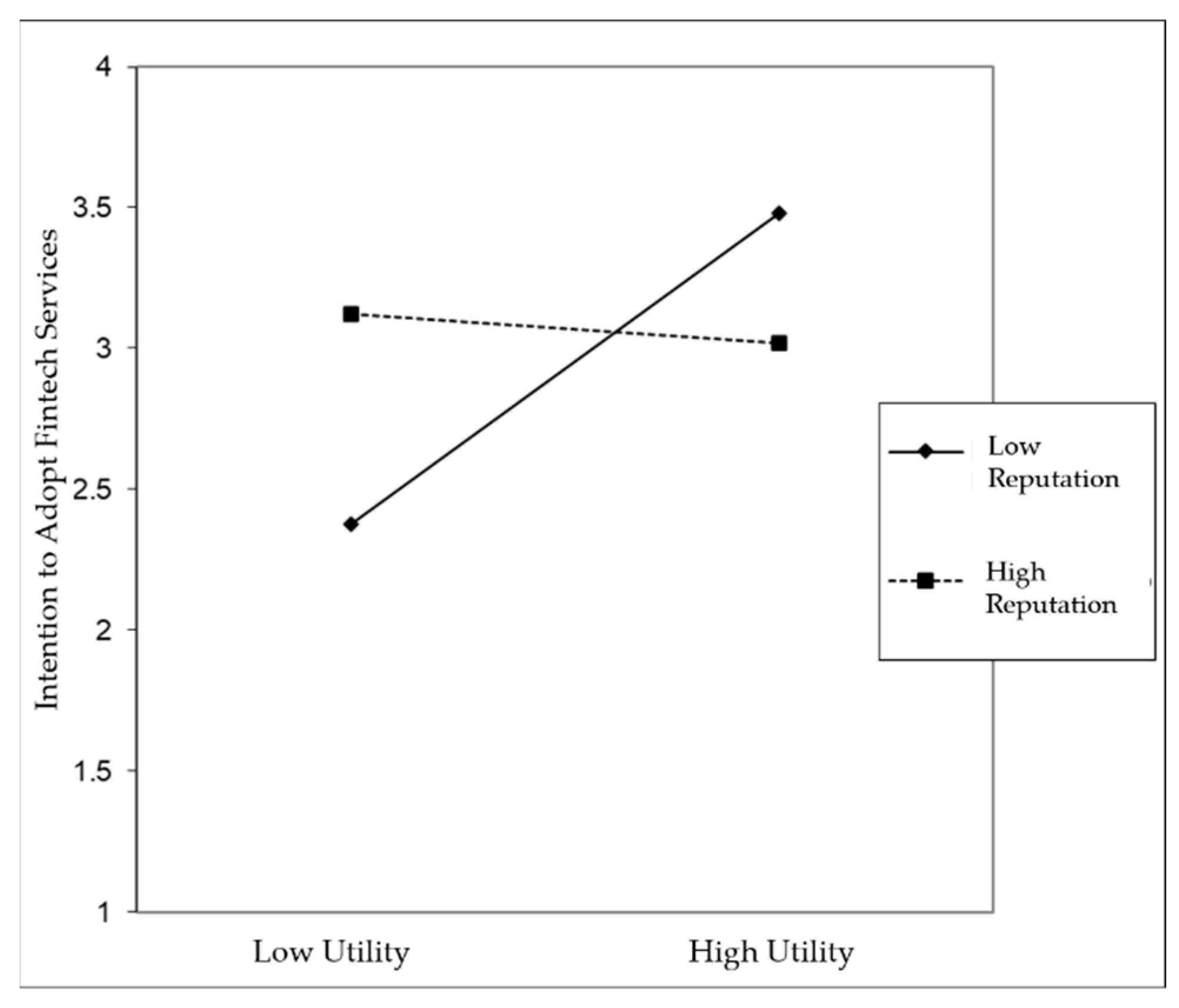

| Usefulness | 0.29 ** | 0.23 |

| Importance | 0.18 | 0.28 * |

| Image | 0.20 | 0.01 |

| Reputation | 0.20 | 0.07 |

| Governmental Restrictions | 0.12 | 0.20 |

| Utility × Importance | 0.24 | |

| Utility × Image | −0.25 | |

| Utility × Reputation | −0.25 * | |

| Utility × Governmental Restrictions | 0.20 | |

| Overall F | 4.50 *** | 3.54 *** |

| R2 | 0.34 | 0.45 |

| Δ | 0.11 | |

| Independent Variables | Intention to Adopt Fintech | |

|---|---|---|

| β Step 1 | β Step 2 | |

| Trust | 0.41 *** | 0.55 *** |

| Importance | 0.23 | 0.22 |

| Image | 0.13 | 0.06 |

| Reputation | 0.14 | 0.14 |

| Governmental Restrictions | 0.07 | 0.01 |

| Trust × Importance | −0.21 | |

| Trust × Image | −0.02 | |

| Trust × Reputation | −0.05 | |

| Trust × Governmental Restrictions | 0.03 | |

| Overall F | 6.15 *** | 3.37 *** |

| R2 | 0.42 | 0.44 |

| Δ | 0.02 | |

| Independent Variables | Intention to Adopt Fintech | |

|---|---|---|

| β Step 1 | β Step 2 | |

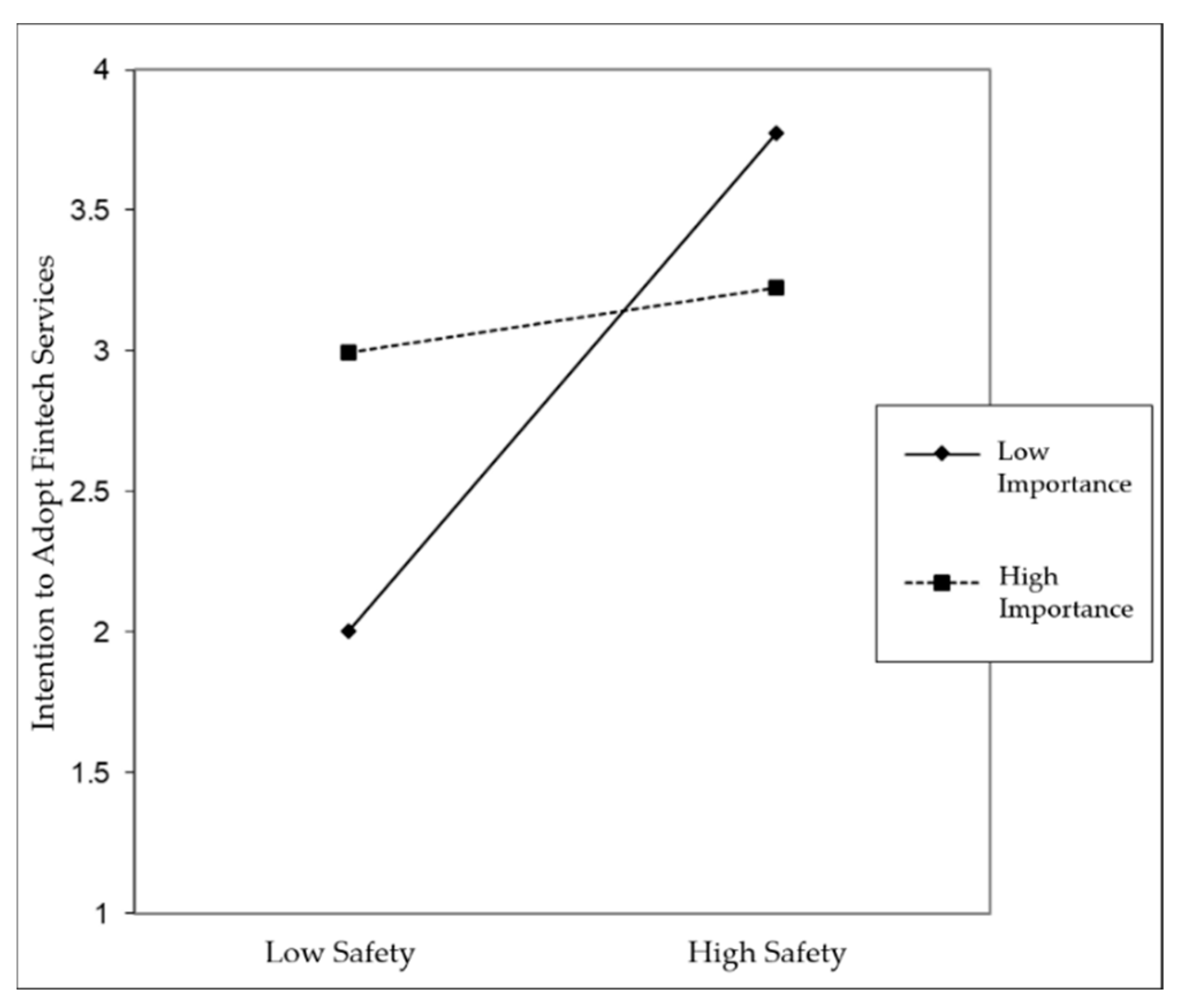

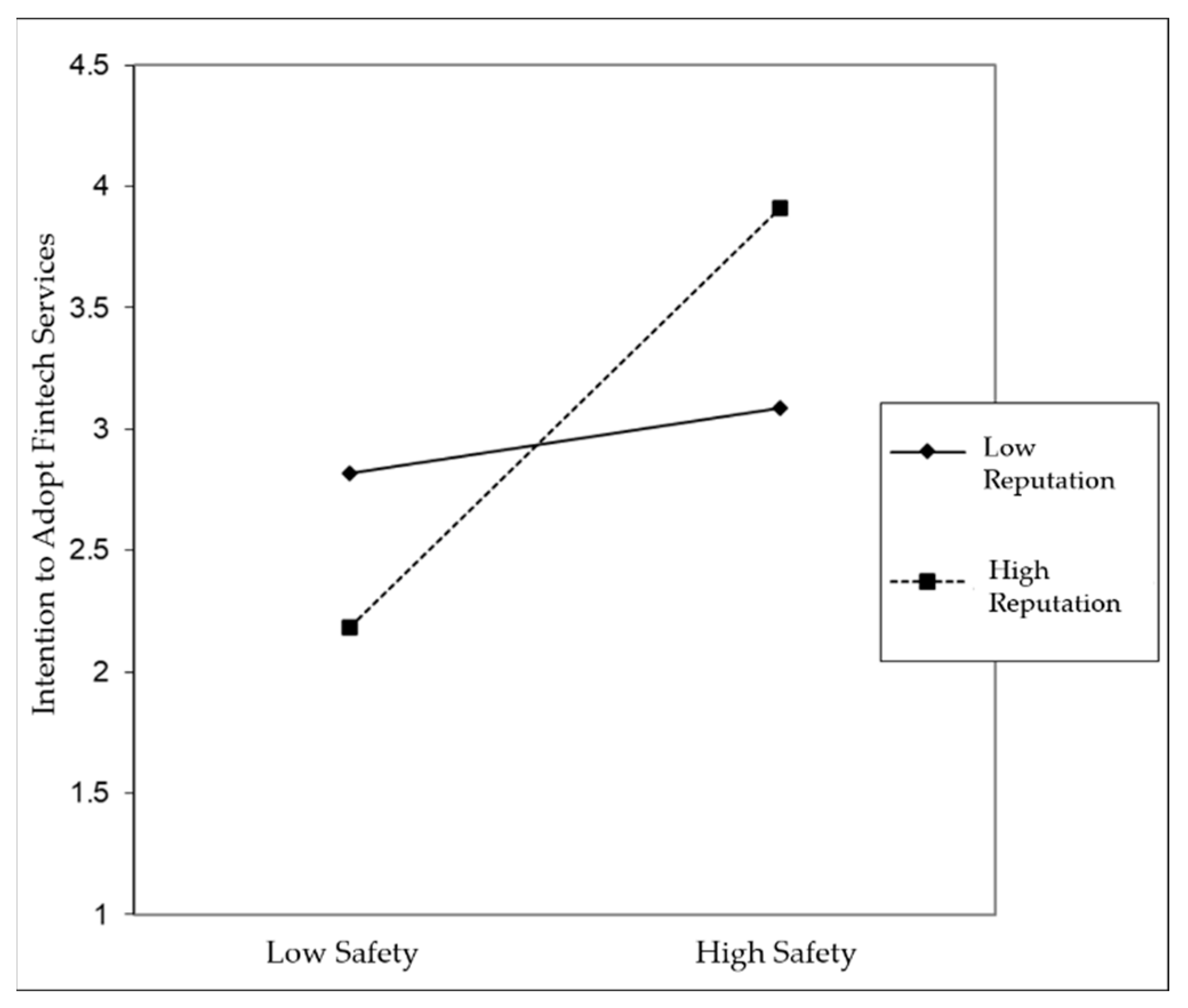

| Safety | 0.10 | 0.46 ** |

| Importance | 0.16 | 0.10 |

| Image | 0.27 * | 0.23 |

| Reputation | 0.24 * | 0.04 |

| Governmental Restrictions | 0.07 | 0.13 |

| Safety × Importance | −0.30 ** | |

| Safety y × Image | −0.26 | |

| Safety × Reputation | 0.27 * | |

| Safety × Governmental Restrictions | −0.08 | |

| Overall F | 3.41 ** | 3.76 *** |

| R2 | 0.28 | 0.47 |

| Δ | 0.19 ** | |

| Hypotheses | Result |

|---|---|

| H1: The Technological context ((a) perceived convenience, usefulness and effectiveness and (b) perceived safety and trust) has a positive and significant effect on Fintech service adoption intention. | Confirmed |

| H2: The organizational context ((a) ecological footprint reduction and (b) internal cost reduction) has a positive and significant effect on SMEs’ intention to adopt Fintech. | Confirmed |

| H3: The environmental context ((a) consumer trends, (b) reputation perception and (c) government restrictions and incentives) has a positive and significant effect on and the intention to adopt Fintech by SMEs. | Partially Confirmed |

| H4: The environmental context ((a) consumer trends, (b) reputation perception and (c) government restrictions and incentives) has a moderating effect on the relationship between the organizational context ((a) ecological footprint reduction and (b) internal cost reduction) and the intention to adopt Fintech by SMEs. | Rejected |

| H5: The environmental context ((a) consumer trends, (b) reputation perception and (c) government restrictions and incentives) has a moderating effect on the relationship between the technological context ((a) perceived convenience, usefulness and effectiveness and (b) perceived safety and trust) and the intention to adopt Fintech by SMEs. | Partially Confirmed |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Moreira-Santos, D.; Au-Yong-Oliveira, M.; Palma-Moreira, A. Fintech Services and the Drivers of Their Implementation in Small and Medium Enterprises. Information 2022, 13, 409. https://doi.org/10.3390/info13090409

Moreira-Santos D, Au-Yong-Oliveira M, Palma-Moreira A. Fintech Services and the Drivers of Their Implementation in Small and Medium Enterprises. Information. 2022; 13(9):409. https://doi.org/10.3390/info13090409

Chicago/Turabian StyleMoreira-Santos, Diana, Manuel Au-Yong-Oliveira, and Ana Palma-Moreira. 2022. "Fintech Services and the Drivers of Their Implementation in Small and Medium Enterprises" Information 13, no. 9: 409. https://doi.org/10.3390/info13090409

APA StyleMoreira-Santos, D., Au-Yong-Oliveira, M., & Palma-Moreira, A. (2022). Fintech Services and the Drivers of Their Implementation in Small and Medium Enterprises. Information, 13(9), 409. https://doi.org/10.3390/info13090409