Influence Analysis of Real Exchange Rate Fluctuations on Trade Balance Data Using Feature Important Evaluation Methods

Abstract

:1. Introduction

- Advanced Methodology: The study pioneers the use of the MDI, PIM, and SHAP value measurement methods within an artificial intelligence framework. This innovative approach allows for detailed and nuanced quantification of the impact of real exchange rates on the trade balance, providing a more comprehensive understanding compared to traditional linear or non-linear approaches.

- Detailed Empirical Insight: Unlike previous studies that often categorize the impact of exchange rates as negative or positive, our research delves into the nuanced impact of real exchange rates on the trade balance. By offering a more granular examination, we contribute a fresh perspective to the existing literature.

- Methodological and Empirical Synthesis: The study seamlessly integrates methodological innovation with empirical evidence, providing a holistic analysis of the intricate relationship between exchange rates and trade balances. This synthesis enhances the robustness of our findings and contributes to a more comprehensive understanding of the subject.

2. Literature

2.1. Real Exchange Rate Fluctuations and Trade Balance

2.2. Feature Importance Evaluation Methods in Economic Analysis

2.3. Gaps in the Literature and Rationale for the Current Study

3. Materials and Methods

3.1. Feature Importance Evaluation Methods

- Random Forest Training: First, a random forest model, which consists of multiple decision trees, is trained on the dataset. Each tree is trained on a bootstrapped sample of the data with a random subset of features () considered at each node split.

- Impurity Measure: The impurity measure, often referred to as Gini impurity or entropy, is calculated for each node during the tree-building process. The reduction in impurity due to a feature (e.g., ) is measured as follows:(1) Impurity: The Gini impurity for a node is calculated as follows:where is the proportion of instances of class i in the node.(2) Impurity Reduction: To measure the impurity reduction due to a feature (e.g., ), we calculate a weighted average of impurity reductions over all the nodes where the feature is used for splitting. It is defined aswhere j iterates over all nodes where the feature () is used for splitting. is the weighted fraction of data points in . and are the weighted fractions of data points in the left and right child nodes after splitting, respectively. Impurity(), Impurity(), and Impurity () are the Gini impurity values for , the left child, and the right child.

- Ranking Features: Finally, the features () are ranked based on the total impurity reduction they provide. The higher the MDI value, the more important the feature is in making decisions within the random forest model for predicting the output ().

- Model Training: To use the Permutation Importance method, first, we need to train your machine learning model on your dataset with features () to predict the output ().

- Initial Accuracy: Measure the initial accuracy or performance metric of our model (e.g., accuracy, mean squared error, etc.) using the test dataset. This initial performance serves as a baseline for feature importance evaluation.

- Feature Shuffling: For each feature (), we randomly shuffle the values of that feature while keeping all other features and the output constant.

- Performance Evaluation: After shuffling the feature, re-evaluate the model’s performance using the same performance metric as in step 2. The drop in performance (accuracy or other metrics) is indicative of the importance of that feature. The idea is that if the feature were important for predictions, shuffling it would lead to a significant drop in performance.

- Repeat for All Features: Repeat steps 3 and 4 for each feature individually. This will provide a measure of importance for each feature based on the reduction in model performance.

- Rank Features: Rank the features based on the drop in model performance. Features that, when shuffled, cause the largest drop in performance are considered more important for prediction.

- Model Training: To use the SHAP value measurement method, we first need to train our machine learning model on our dataset with the features () to predict the output ().

- SHAP Values’ Calculation: Calculate the SHAP values for each data point in our test dataset. SHAP values explain the difference between the model prediction and the expected value of the prediction for each feature.

- Summary Statistics: Calculate the summary statistics (e.g., mean or absolute mean) of the SHAP values for each feature. These summary statistics provide a measure of the average contribution of each feature across the entire dataset.

- Bar Plot Visualization: Create a bar plot where each bar represents a feature, and the height of the bar corresponds to the summary statistic of the SHAP values for that feature. Positive values indicate features that push predictions higher, while negative values suggest features that push predictions lower.

- Calculate the model’s output (prediction) for a specific data point: , where x is a data point.

- Calculate the expected value of the model’s output across all data points: .

- The SHAP value for feature for a specific data point x can be represented as

- To compute the summary statistic (e.g., mean or absolute mean) for the SHAP values of , we would calculate this statistic across all data points.

3.2. Dataset Description

- Real Exchange Rates: Capturing the relative value of a country’s currency against a basket of other currencies, thereby providing a measure of competitiveness in international trade.

- Trade Balance: Reflecting the difference between a country’s exports and imports, a key indicator of its economic relationship with the rest of the world.

3.3. Data Collection and Preprocessing

4. Experimental Results

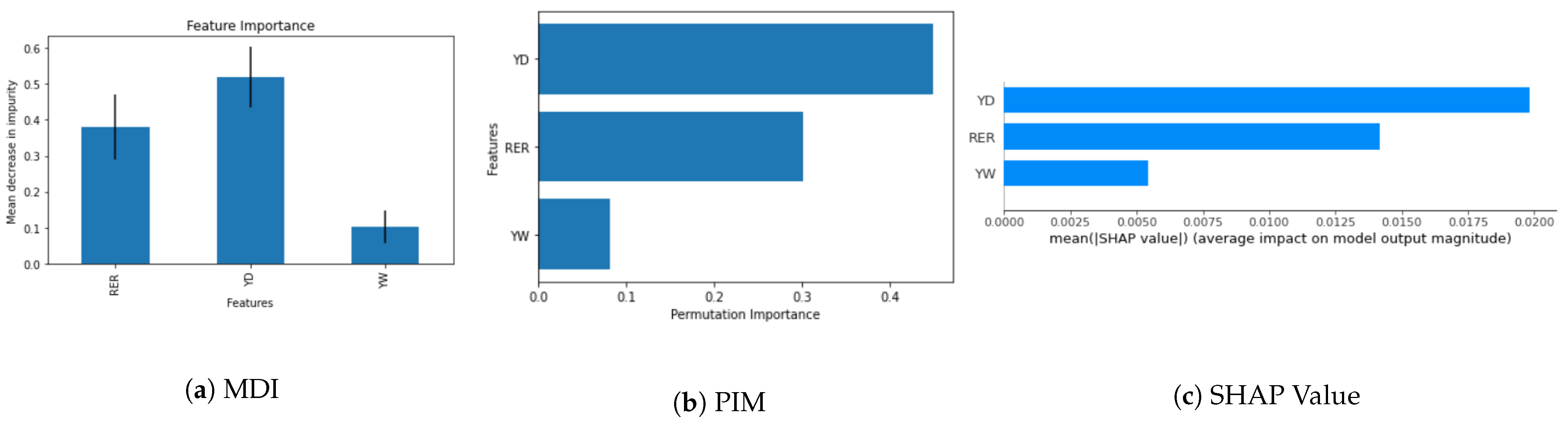

4.1. The Effectiveness of the Proposed Method on Single Country and Group Country Data

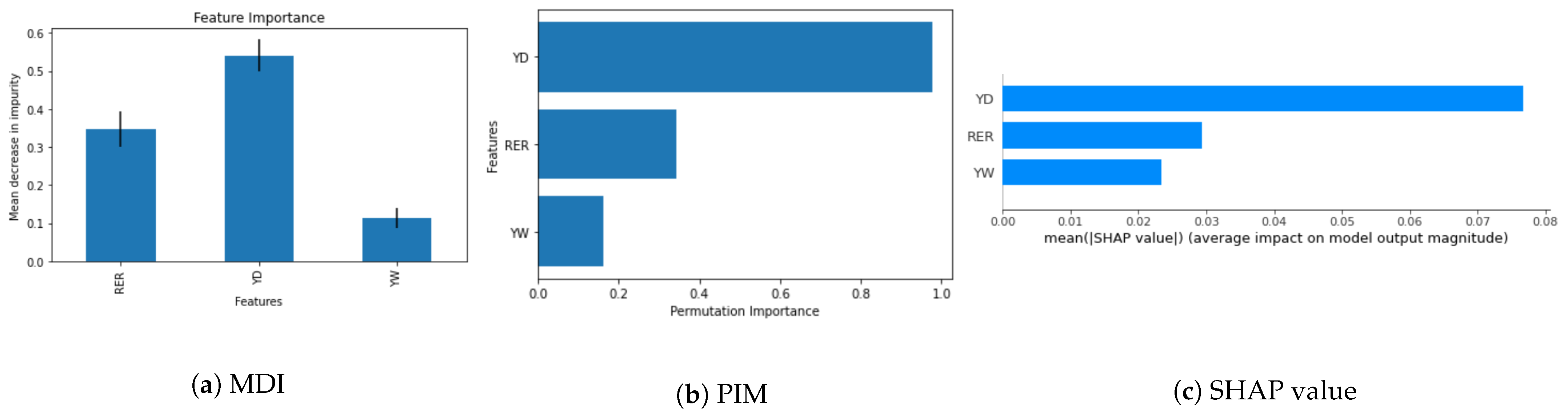

4.2. The Effectiveness of the Proposed Method on Panel Countries Data

- (Domestic Real Income): Evidently, consistently emerges as the most influential feature affecting across all three methods, underscoring its considerable impact on trade balance outcomes.

- (Real Exchange Rate): follows closely, identified as a substantial factor affecting , albeit with slightly less of an impact than .

- (Foreign Real Income): Conversely, exhibits a relatively minor influence on as per the results obtained from the three methods.

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| YD | Domestic Real Income |

| TB | Trade Balance |

| RER | Real Exchange Rate |

| YW | Foreign Real Income |

| WB | World Bank |

| IMF | International Momentary Fund |

| CE | Country Economy |

| MDI | Mean Decrease Impurity |

| PIM | Permutation Importance Measurement |

| SHAP | SHapley Additive exPlanation |

References

- Edwards, S.; Cabezas, L. Exchange Rate Pass-through, Monetary Policy, and Real Exchange Rates: Iceland and the 2008 Crisis. Open Econ. Rev. 2022, 33, 197–230. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Aftab, M. Asymmetric effects of exchange rate changes on the Malaysia-EU trade: Evidence from industry data. Empirica 2016, 2, 339–365. [Google Scholar] [CrossRef]

- Alshubiri, F. The impact of the real interest rate, the exchange rate and political stability on foreign direct investment inflows: A comparative analysis of G7 and GCC Countries. Asia-Pac. Financ. Mark. 2022, 29, 569–603. [Google Scholar] [CrossRef]

- Hall, S.G.; Hondroyiannis, G.; Kenjegaliev, A.; Swamy, P.; Tavlas, G.S. Is the relationship between prices and exchange rates homogeneous? J. Int. Money Financ. 2013, 37, 411–438. [Google Scholar] [CrossRef]

- Liu, T.Y.; Lee, C.C. Exchange rate fluctuations and interest rate policy. Int. J. Financ. Econ. 2022, 27, 3531–3549. [Google Scholar] [CrossRef]

- Lim, W.M.; Mandrinos, S. A general theory of de-internationalization. Glob. Bus. Organ. Excell. 2023, 42, 9–15. [Google Scholar] [CrossRef]

- Mandrinos, S.; Lim, W.M. De-internationalization: An organizational institutionalism perspective. Glob. Bus. Organ. Excell. 2023, 42, 58–73. [Google Scholar] [CrossRef]

- Mandrinos, S.; Lim, W.M.; Liew, C.S.L. De-internationalization through the lens of intellectual property rights. Thunderbird Int. Bus. Rev. 2022, 64, 13–24. [Google Scholar] [CrossRef]

- Lal, M.; Kumar, S.; Pandey, D.K.; Rai, V.K.; Lim, W.M. Exchange rate volatility and international trade. J. Bus. Res. 2023, 167, 114156. [Google Scholar] [CrossRef]

- Asseery, A.; Peel, D.A. The effects of exchange rate volatility on exports: Some new estimates. Econ. Lett. 1991, 37, 173–177. [Google Scholar] [CrossRef]

- Arize, A.C. The long-run relationship between import flows and real exchange-rate volatility: The experience of eight European economies. Int. Rev. Econ. Financ. 1998, 7, 417–435. [Google Scholar] [CrossRef]

- Arora, S.; Bahmani-Oskooee, M.; Goswami, G. Bilateral J-curve between India and her trading partners. Appl. Econ. 2003, 35, 1037–1041. [Google Scholar] [CrossRef]

- Hall, S.; Hondroyiannis, G.; Swamy, P.; Tavlas, G.; Ulan, M. Exchange-rate volatility and export performance: Do emerging market economies resemble industrial countries or other developing countries? Econ. Model. 2010, 27, 1514–1521. [Google Scholar] [CrossRef]

- Rose, A.K.; Yellen, J.L. Is there a J-curve? J. Monet. Econ. 1989, 24, 53–68. [Google Scholar] [CrossRef]

- Rahman, M.; Mustafa, M.; Burckel, D.V. Dynamics of the yen-dollar real exchange rate and the US-Japan real trade balance. Appl. Econ. 1997, 29, 661–664. [Google Scholar] [CrossRef]

- Nyeadi, J.D.; Atiga, O.; Atogenzoya, C.A. The impact of exchange rate movement on export: Empirical evidence from Ghana. Int. J. Acad. Res. Account. Financ. Manag. Sci. 2014, 4, 41–48. [Google Scholar] [CrossRef] [PubMed]

- Asteriou, D.; Masatci, K.; Pılbeam, K. Exchange rate volatility and international trade: International evidence from the MINT countries. Econ. Model. 2016, 58, 133–140. [Google Scholar] [CrossRef]

- Khachatryan, G.A.; Grigoryan, A. Export growth dynamics and real exchange rate: Evidence from Armenia. Int. Econ. J. 2020, 34, 493–509. [Google Scholar] [CrossRef]

- Nguyen, H.M.; Quan, B.Q.M.; Le, H.V.; Tran, T.V. Determinants of intra-industry trade between vietnam and countries in tpp. J. Asian Financ. Econ. Bus. 2020, 7, 123–129. [Google Scholar] [CrossRef]

- Rose, A.K. The role of exchange rates in a popular model of international trade. J. Int. Econ. 1991, 30, 301–316. [Google Scholar] [CrossRef]

- Cheung, Y.-W.; Chinn, M.D.; Qian, X. Are Chinese trade flows different? J. Int. Money Financ. 2012, 31, 2127–2146. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Aftab, M. On the asymmetric effects of exchange rate volatility on trade flows: New evidence from US-Malaysia trade at the industry level. Econ. Model. 2017, 63, 86–103. [Google Scholar] [CrossRef]

- Bampi, R.E.; Colombo, J.A. Heterogeneous effects of foreign exchange appreciation on industrial output: Evidence from disaggregated manufacturing data. Q. Rev. Econ. Financ. 2021, 80, 431–451. [Google Scholar] [CrossRef]

- Marquez, J.; Schindler, J. Exchange-rate effects on China’s trade. Rev. Int. Econ. 2007, 15, 837–853. [Google Scholar] [CrossRef]

- Baek, J.; Nam, S. The South Korea–China trade and the bilateral real exchange rate: Asymmetric evidence from 33 industries. Econ. Anal. Policy 2021, 71, 463–475. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Harvey, H. Exchange rate volatility and commodity trade between United States and Australia: An asymmetric analysis. World Econ. 2021, 44, 1509–1700. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Karamelikli, H. Exchange rate volatility and commodity trade between UK and China: An asymmetric analysis. Chin. Econ. 2022, 55, 41–65. [Google Scholar] [CrossRef]

- Hashmi, S.M.; Chang, B.H.; Shahbaz, M. Asymmetric effect of exchange rate volatility on India’s cross-border trade: Evidence from global financial crisis and multiple threshold nonlinear autoregressive distributed lag model. Aust. Econ. Pap. 2021, 60, 64–97. [Google Scholar] [CrossRef]

- Senadza, B.; Diaba, D.D. Effect of exchange rate volatility on trade in Sub-Saharan Africa. J. Afr. Trade 2017, 4, 20–36. [Google Scholar] [CrossRef]

- Yazgan, M.E.; Ozturk, S.S. Real exchange rates and the balance of trade: Does the J-curve effect really hold? Open Econ. Rev. 2019, 30, 343–373. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Kara, O. Income and price elasticities of trade: Some new estimates. Int. Trade J. 2005, 19, 165–178. [Google Scholar] [CrossRef]

- Ky Chang, B. Changes in Effects of Exchange Rate on Trade Balance according to Industrial Structure Change. J. Korea Trade (JKT) 2005, 9, 5–23. [Google Scholar]

- Bahmani-Oskooee, M.; Ardalani, Z. Exchange rate sensitivity of US trade flows: Evidence from industry data. South. Econ. J. 2006, 72, 542–559. [Google Scholar]

- Baek, J.; Koo, W.W. How sensitive is US agricultural trade to the bilateral exchange rate? Evidence from bulk, intermediate, and consumer-oriented products. Agric. Econ. 2011, 42, 387–403. [Google Scholar] [CrossRef]

- Baek, J. Exchange rate sensitivity of Korea-US bilateral trade: Evidence from industrial trade data. J. Korea Trade 2012, 16, 1–21. [Google Scholar]

- Baek, J. Does the exchange rate matter to bilateral trade between Korea and Japan? Evidence from commodity trade data. Econ. Model. 2013, 30, 856–862. [Google Scholar] [CrossRef]

- Baek, J. Exchange rate effects on Korea–US bilateral trade: A new look. Res. Econ. 2014, 68, 214–221. [Google Scholar] [CrossRef]

- Jiranyakul, K.; Brahmasrene, T. An analysis of the determinants of Thailand’s exports and imports with major trading partners. Southwest. Econ. Rev. 2002, 29, 111–121. [Google Scholar]

- Thorbecke, W.; Zhang, H. The effect of exchange rate changes on China’s labour-intensive manufacturing exports. Pac. Econ. Rev. 2009, 14, 398–409. [Google Scholar] [CrossRef]

- Hatemi-J, A.; Irandoust, M. Bilateral trade elasticities: Sweden versus her major trading partners. Am. Rev. Political Econ. 2005, 3, 38–50. [Google Scholar] [CrossRef]

- Irandoust, M.; Ekblad, K.; Parmler, J. Bilateral trade flows and exchange rate sensitivity: Evidence from likelihood-based panel cointegration. Econ. Syst. 2006, 30, 170–183. [Google Scholar] [CrossRef]

- Mohsen, B.-O.; Brooks, T.J. Cointegration approach to estimating bilateral trade elasticities between US and her trading partners. Int. Econ. J. 1999, 13, 119–128. [Google Scholar] [CrossRef]

- Kim, A. An empirical analysis of Korea’s trade imbalances with the US and Japan. J. Asia Pac. Econ. 2009, 14, 211–226. [Google Scholar] [CrossRef]

- Chang, B.-K. Korean bilateral trade balances and exchange rate sensitivity: Evidence from the panel approach. J. Korea Trade (JKT) 2009, 13, 1–19. [Google Scholar]

- Bahmani-Oskooee, M.; Fariditavana, H. Nonlinear ARDL approach and the J-curve phenomenon. Open Econ. Rev. 2016, 27, 51–70. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Harvey, H. Do inpayments and outpayments respond to exchange rate changes asymmetrically: Evidence from Malaysia. Int. Trade J. 2018, 32, 317–342. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Fariditavana, H. How sensitive are the US inpayments and outpayments to real exchange rate changes: An asymmetry analysis. Int. Econ. Econ. Policy 2019, 16, 619–647. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Kanitpong, T. Thailand-China commodity trade and exchange rate uncertainty: Asymmetric evidence from 45 industries. J. Econ. Asymmetries 2019, 20, e00130. [Google Scholar] [CrossRef]

- Phan, T.H.; Jeong, J.Y. Vietnam trade balance and exchange rate: Evidence from panel data analysis. J. Appl. Econ. Bus. Res. 2015, 5, 220–232. [Google Scholar]

- Kofoworade, A. Effect of Real Exchange Rate on Trade Balance and Economic Growth in Nigeria. 2018. Available online: https://doi.org/10.2139/ssrn.4560722 (accessed on 13 February 2024).

- Phong, L.H.; Bao, H.H.G.; Van, D.T.B. Application of nonlinear autoregressive distributed lag (NARDL) model for analysis of the asymmetric effects of real exchange rate volatility on Vietnam’s trade balance. J. Eng. Appl. Sci. 2019, 14, 4317–4322. [Google Scholar] [CrossRef]

- Durmaz, N. Industry level J-curve in Turkey. J. Econ. Stud. 2015, 42, 689–706. [Google Scholar] [CrossRef]

- Akbostanci, E. Dynamics of the trade balance: The Turkish J-curve. Emerg. Mark. Financ. Trade 2004, 40, 57–73. [Google Scholar] [CrossRef]

- Iyke, B.N.; Ho, S.-Y. The real exchange rate, the Ghanaian trade balance, and the J-curve. J. Afr. Bus. 2017, 18, 380–392. [Google Scholar] [CrossRef]

- Iyke, B.N.; Ho, S.-Y. Nonlinear effects of exchange rate changes on the South African bilateral trade balance. J. Int. Trade Econ. Dev. 2018, 27, 350–363. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Usman, A.; Ullah, S. Asymmetric J-curve in the commodity trade between Pakistan and United States: Evidence from 41 industries. Eurasian Econ. Rev. 2020, 10, 163–188. [Google Scholar] [CrossRef]

- Kyophilavong, P.; Shahbaz, M.; Uddin, G.S. Does J-curve phenomenon exist in case of Laos? An ARDL approach. Econ. Model. 2013, 35, 833–839. [Google Scholar] [CrossRef]

- Baek, J.; Yoon, J.H. The Korea-Vietnam trade and the bilateral exchange rate: Asymmetric evidence from commodity trade data. Aust. Econ. Pap. 2023, 62, 124–148. [Google Scholar] [CrossRef]

- Strobl, C.; Boulesteix, A.L.; Kneib, T.; Augustin, T.; Zeileis, A. Conditional variable importance for random forests. BMC Bioinform. 2008, 9, 307. [Google Scholar] [CrossRef]

- McKenzie, M.D. The impact of exchange rate volatility on international trade flows. J. Econ. Surv. 1999, 13, 71–106. [Google Scholar] [CrossRef]

- Nicita, A. Exchange rates, international trade and trade policies. Int. Econ. 2013, 135, 47–61. [Google Scholar] [CrossRef]

- Barkoulas, J.T.; Baum, C.F.; Caglayan, M. Exchange rate effects on the volume and variability of trade flows. J. Int. Money Financ. 2002, 21, 481–496. [Google Scholar] [CrossRef]

- Auboin, M.; Ruta, M. The relationship between exchange rates and international trade: A literature review. World Trade Rev. 2013, 12, 577–605. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Case Study | Number of Countries | Country Name |

|---|---|---|---|

| 1 | Single country | 2 | Bulgaria and Australia are randomly selected |

| for visualization results | |||

| 2 | OECD group | 17 | Australia, Canada, Switzerland, Chile, Colombia, Costa Rica, |

| Czech Republic, Denmark, United Kingdom, Hungary, Iceland, | |||

| Japan, Korea, Rep., Mexico, Norway, New Zealand, Sweden | |||

| 3 | Non-OECD group | 61 | Albania, Armenia, Azerbaijan, Benin, Bangladesh, Bulgaria, |

| Belarus, Bolivia, Brazil, Brunei Darussalam, Botswana, China, | |||

| Cote d’Ivoire, Cameroon, Congo, Rep., Dominican Republic, | |||

| Algeria, Egypt, Arab Rep., Fiji, Ghana, Gambia, The, Guatemala, | |||

| Hong Kong SAR, China, Honduras, Haiti, Indonesia, India, | |||

| Jamaica, Kazakhstan, Kenya, Macao SAR, China, Morocco, | |||

| Madagascar, Mali, Mongolia, Mauritius, Malaysia, Niger, | |||

| Nigeria, Pakistan, Peru, Philippines, Paraguay, Romania, | |||

| Russian Federation, Sudan, Singapore, Solomon Islands, | |||

| Eswatini, Seychelles, Togo, Thailand, Tonga, Tunisia, Turkiye, | |||

| Tanzania, Uganda, Ukraine, Uruguay, Vanuatu, South Africa | |||

| 4 | Panel country data | 78 | Albania; Armenia; Australia; Azerbaijan; Benin; Bangladesh; |

| Bulgaria; Belarus; Bolivia; Brazil; Brunei Darussalam; Botswana; | |||

| Canada; Switzerland; Chile; China; Cote d’Ivoire; Cameroon; | |||

| Congo, Rep.; Colombia; Costa Rica; Czechia; Denmark; | |||

| Dominican Republic; Algeria; Egypt; Arab Rep.; Fiji; | |||

| United Kingdom; Ghana; Gambia, The; Guatemala; | |||

| Hong Kong SAR China; Honduras; Haiti; Hungary; Indonesia; | |||

| India; Iceland; Jamaica; Japan; Kazakhstan; Kenya; | |||

| Korea, Rep.; Macao SAR, China; Morocco; Madagascar; Mexico; | |||

| Mali; Mongolia; Mauritius; Malaysia; Niger; Nigeria; Norway; | |||

| New Zealand; Pakistan; Peru; Philippines; Paraguay; Romania; | |||

| Russian Federation; Sudan; Singapore; Solomon Islands; Sweden; | |||

| Eswatini; Seychelles; Togo; Thailand; Tonga; Tunisia; Turkiye; | |||

| Tanzania; Uganda; Ukraine; Uruguay; Vanuatu; South Africa |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kim, M.-J.; Le, T.-T.-H. Influence Analysis of Real Exchange Rate Fluctuations on Trade Balance Data Using Feature Important Evaluation Methods. Information 2024, 15, 156. https://doi.org/10.3390/info15030156

Kim M-J, Le T-T-H. Influence Analysis of Real Exchange Rate Fluctuations on Trade Balance Data Using Feature Important Evaluation Methods. Information. 2024; 15(3):156. https://doi.org/10.3390/info15030156

Chicago/Turabian StyleKim, Min-Joon, and Thi-Thu-Huong Le. 2024. "Influence Analysis of Real Exchange Rate Fluctuations on Trade Balance Data Using Feature Important Evaluation Methods" Information 15, no. 3: 156. https://doi.org/10.3390/info15030156

APA StyleKim, M.-J., & Le, T.-T.-H. (2024). Influence Analysis of Real Exchange Rate Fluctuations on Trade Balance Data Using Feature Important Evaluation Methods. Information, 15(3), 156. https://doi.org/10.3390/info15030156