On Barrier Binary Options in the Telegraph-like Financial Market Model

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Market Model and Measure Transform

- (a)

- The jump-telegraph process and its stochastic exponent are martingale if and only ifHere, and are the average amplitudes of the jumps associated with states 0 and 1, respectively,

- (b)

- For models (3)–(4), there is an equivalent martingale measure if and only if there exists a pair of positive measurable functions such thatUnder the new measure the Poisson rates are changed toand the jump amplitudes are distributed as

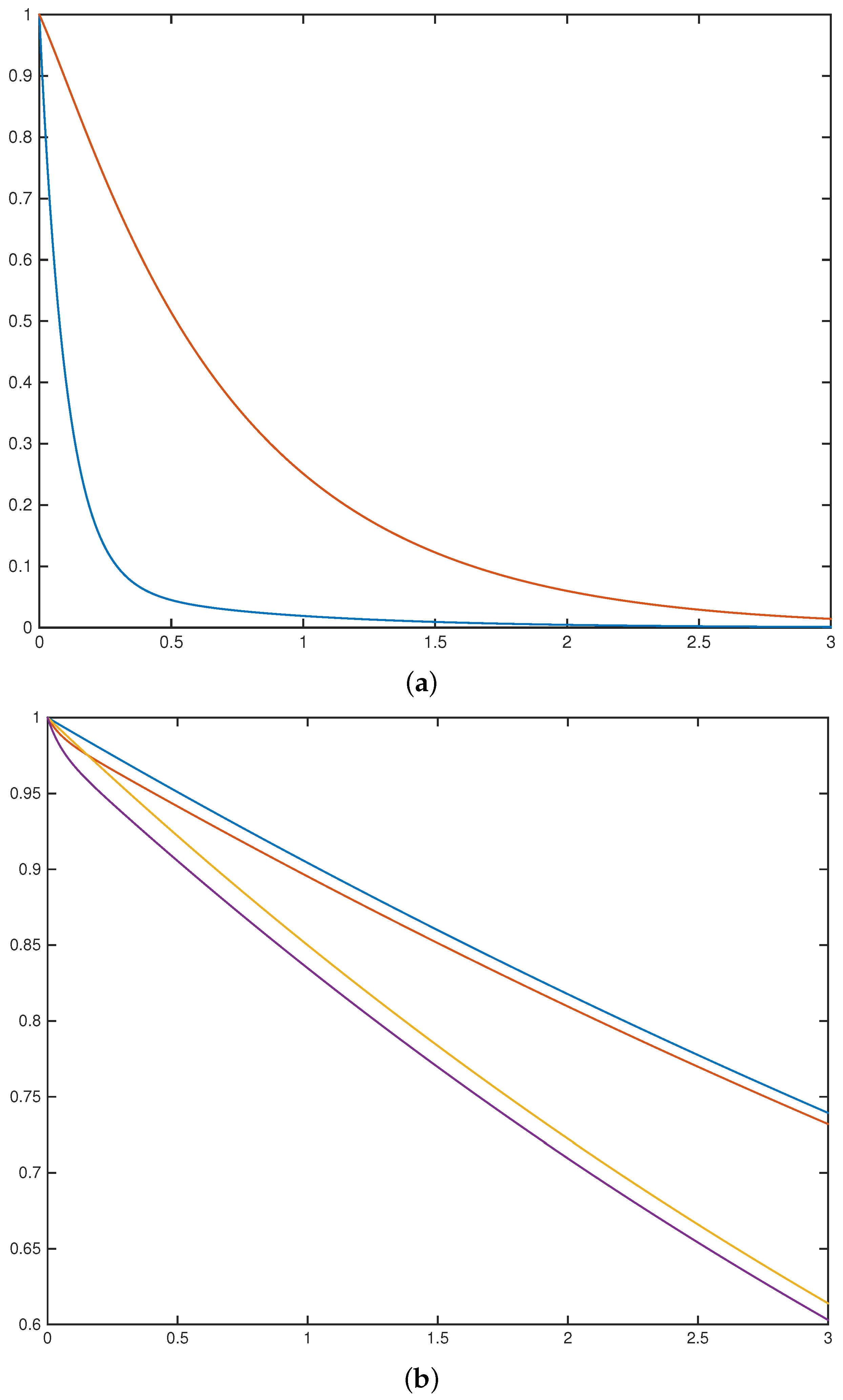

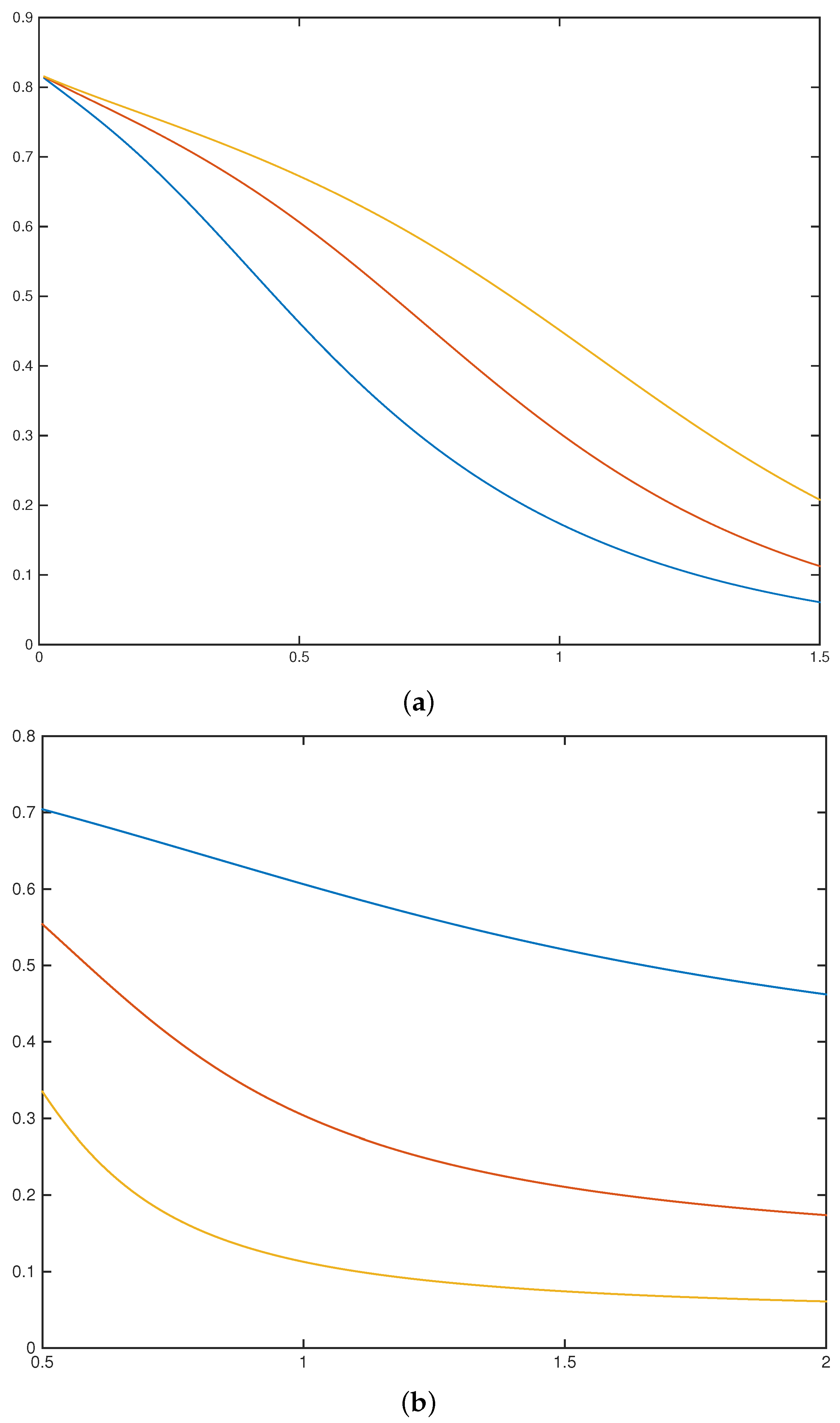

3. Pricing “Cash-(At Hit)-or-Nothing Barrier Binary Option”

3.1. “Bull Market” and Positive Threshold

3.2. “Bull Market” and Negative Threshold

3.3. “Bear Market” and the Cram ér–Lundberg Ruin Model

4. Appendix: How to Choose a Martingale Measure

- Jump risk is not priced. Note that the telegraph process and the accompanying Markov process can be considered as a source of systematic risk, while jump amplitudes can be classified as unsystematic. Under such assumptions, it is reasonable to assume that a change of the measure does not affect the distribution of jump amplitudes. This idea resembles the approach proposed by R.C.Merton [14].This corresponds to a constant solution of the Equation (6), which coincides with the new switching intensities, i.e., and .To choose a risk-neutral measure, we apply the measure transformation determined by the Radon–Nikodym derivative,where with deterministic constants and satisfying the martingale condition (5), i.e.,For the measure specified in this way, the distribution of jump amplitudes does not change, but the market regimes switch with changed rates which are determined byBy virtue of (31), it is clear that transformation (30) leads to a risk-neutral measure for this market model if and only ifWith this martingale measure, the switching rates and are given by

- Jump risk is insured. To choose another risk-neutral measure, we supply the market with an additional security, which magnifies its value by a fixed rate every time there is a change of the market state, i.e., letHere, the process is governed by the same Poisson process and it has deterministic jump values . This security can be considered as insurance that compensates losses and gains provoked by state changes and helps to hedge the option with a general payoff function . A market formed by three assets is still incomplete, but now we can use the following approach to make a reasonable choice of risk-neutral measure. First, we change the measure with respect to the switching intensities. Assume the magnification coefficients alter according to alternating market states, Applying the Radon–Nikodym derivative (30) to the asset we define the equivalent measure with switching intensities . We then make one more change of measure, conserving the form of the distribution of the jump values .

Funding

Acknowledgments

Conflicts of Interest

References

- Goldstein, S. On diffusion by discontinuous movements and on the telegraph equation. Q. J. Mech. Appl. Math. 1951, 4, 129–156. [Google Scholar] [CrossRef]

- Kac, M. A stochastic model related to the telegrapher’s equation. Rocky Mt. J. Math. 1974, 4, 497–509, reprinted in Kac, M. Some Stochastic Problems in Physics and Mathematics; Colloquium lectures in the pure and applied sciences, No. 2, hectographed; Field Research Laboratory, Socony Mobil Oil Company: Dallas, TX, USA, 1956; pp. 102–122.. [Google Scholar] [CrossRef]

- Ratanov, N. A jump telegraph model for option pricing. Quant. Financ. 2007, 7, 575–583. [Google Scholar] [CrossRef]

- López, O.; Ratanov, N. Option pricing driven by a telegraph process with random jumps. J. Appl. Probab. 2012, 49, 838–849. [Google Scholar] [CrossRef]

- Ratanov, N.; Kolesnik, A.D. Telegraph Processes and Option Pricing, 2nd ed.; Springer: Heidelberg, Germany; New York, NY, USA; Dordrecht, The Netherlands; London, UK, 2022. [Google Scholar]

- Ratanov, N. Telegraph Processes and Option Pricing; 2nd Nordic-Russian Symposium on Stochastic Analysis; Springer: Beitostolen, Norway, 1999. [Google Scholar]

- Di Crescenzo, A.; Pellerey, F. On prices’ evolutions based on geometric telegrapher’s process. Appl. Stoch. Model. Bus. Ind. 2002, 18, 171–184. [Google Scholar] [CrossRef]

- Dalang, R.C.; Hongler, M.-O. The right time to sell a stock whose price is driven by Markovian noise. Ann. Appl. Probab. 2004, 14, 2176–2201. [Google Scholar] [CrossRef]

- Jeanblanc, M.; Yor, M.; Chesney, M. Mathematical Methods for Financial Markets; Springer: Dordrecht, The Netherlands; Heidelberg, Germany; London, UK; New York, NY, USA, 2009. [Google Scholar]

- Rubinstein, M.; Reiner, E. Unscrambling the binary code. Risk Mag. 1991, 4, 75–83. [Google Scholar]

- Linz, P. Analytical and Numerical Methods for Volterra Equations; SIAM: Philadelphia, PN, USA, 1985. [Google Scholar]

- Rolski, T.; Schmidli, H.; Schmidt, V.; Teugels, J. Stochastic Processes for Insurance and Finance; John Wiley & Sons: Hoboken, NJ, USA, 1999. [Google Scholar]

- Prudnikov, A.P.; Brychkov, Y.A.; Marichev, O.I. Integrals and Series, Vol. 5. Inverse Laplace Transforms; Gordon and Breach Science Publishers: Langhorne, PA, USA, 1992. [Google Scholar]

- Merton, R.C. Option pricing when underlying stock returns are discontinuous. J. Financ. Econom. 1976, 3, 125–144. [Google Scholar] [CrossRef] [Green Version]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ratanov, N. On Barrier Binary Options in the Telegraph-like Financial Market Model. Computation 2022, 10, 163. https://doi.org/10.3390/computation10090163

Ratanov N. On Barrier Binary Options in the Telegraph-like Financial Market Model. Computation. 2022; 10(9):163. https://doi.org/10.3390/computation10090163

Chicago/Turabian StyleRatanov, Nikita. 2022. "On Barrier Binary Options in the Telegraph-like Financial Market Model" Computation 10, no. 9: 163. https://doi.org/10.3390/computation10090163

APA StyleRatanov, N. (2022). On Barrier Binary Options in the Telegraph-like Financial Market Model. Computation, 10(9), 163. https://doi.org/10.3390/computation10090163