Developing a Numerical Method of Risk Management Taking into Account the Decision-Maker’s Subjective Attitude towards Multifactorial Risks

,

,  ,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

3. Methodology

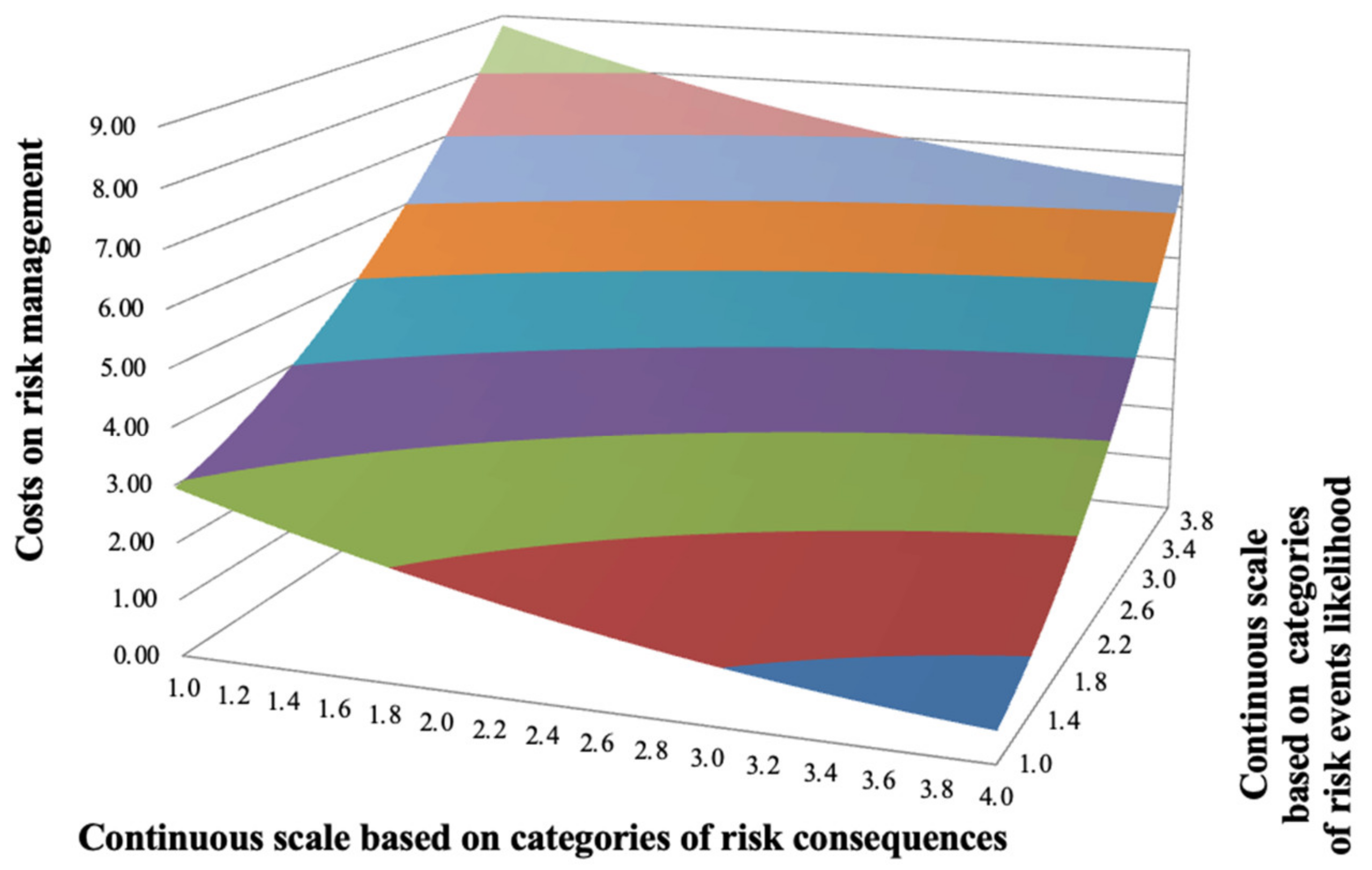

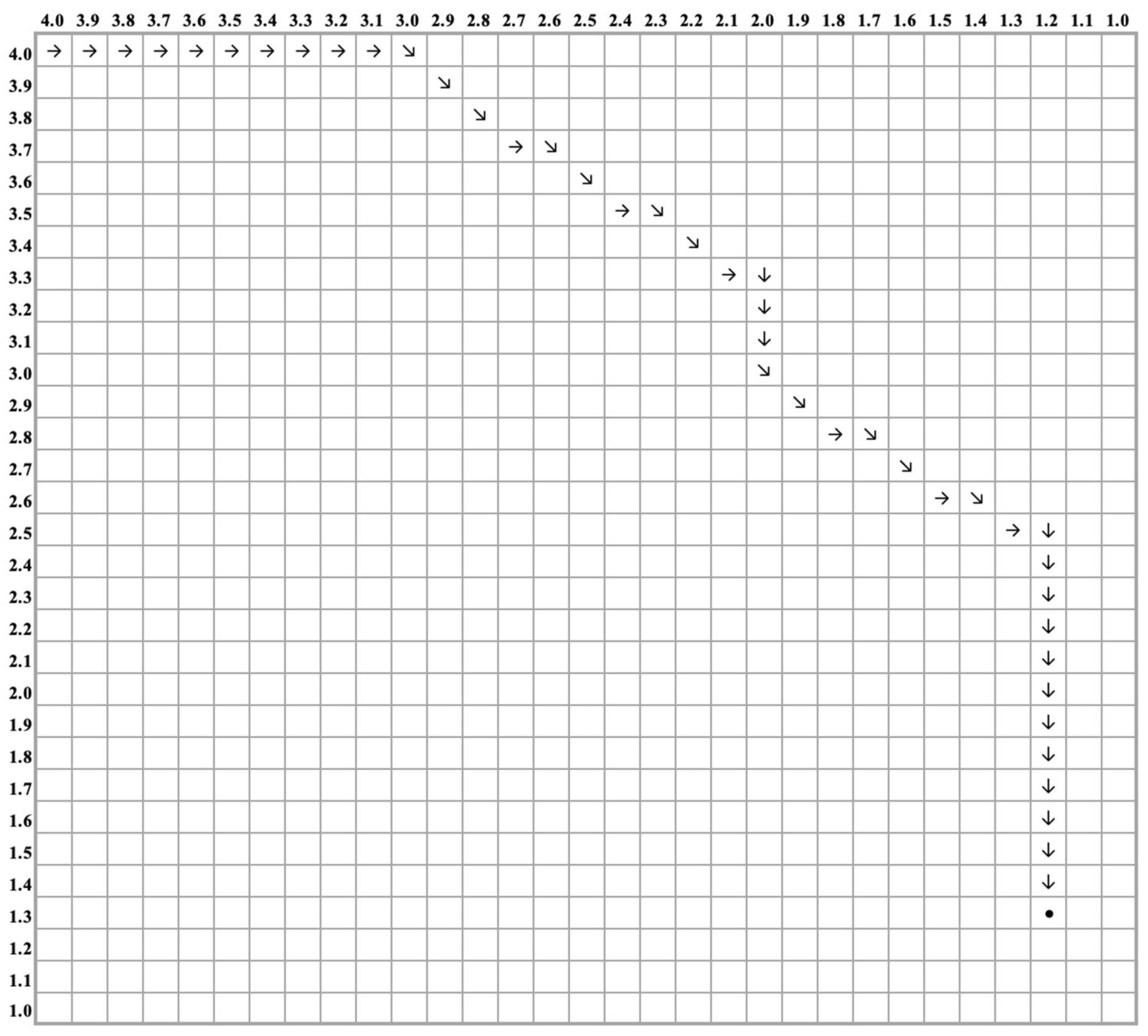

3.1. Applied Terminology and Definitions

3.2. Approximate Method

3.3. Statement of the Risk Management Problem

3.4. Applied Programs

- -

- prototyping is carried out in order to create a sample information system to demonstrate the principles of operation and perform preliminary tests;

- -

- the resulting prototype is easy to use as an element of the technical task for programmers to create an information system;

- -

- Microsoft Excel spreadsheets are quite common; hence, the prototype can be demonstrated on almost any computer and users do not need to take special advanced training courses; and

- -

- work in Microsoft Excel does not require advanced programming skills, which will allow users to modify the prototype of the information system on their own.

4. Results

5. Conclusions and Discussion

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Brandenburg, M.; Rebs, T. Sustainable supply chain management: A modeling perspective. Ann. Oper. Res. 2015, 229, 213–252. [Google Scholar] [CrossRef]

- Lin, T.T.; Yen, H.-T.; Hsu, S.-Y. A Synergy Value Analysis of Sustainable Management Projects: Illustrated by the Example of the Aesthetic Medicine Industry. J. Risk Financ. Manag. 2022, 15, 348. [Google Scholar] [CrossRef]

- Willett, A.H. The Economic Theory of Risk and Insurance; P.S. King & Son: London, UK, 1901; 142p. [Google Scholar]

- Nosratabadi, S.; Mosavi, A.; Shamshirband, S.; Zavadskas, E.K.; Rakotonirainy, A.; Chau, K.W. Sustainable business models: A review. Sustainability 2019, 11, 1663. [Google Scholar] [CrossRef] [Green Version]

- Haimes, Y.Y. Risk Modeling, Assessment, and Management, 2nd ed.; First published 1998; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2004; p. 837. [Google Scholar]

- Gracheva, M.V.; Sekerin, A.B.; Afanasyev, A.M.; Babaskin, S.Y.; Bykova, A.G.; Volkov, I.M.; Kopytin, K.V.; Nikitin, S.A.; Pervushin, V.A.; Svetlov, N.M.; et al. Risk-Management of Investment Project; Unity-Dana: Moscow, Russia, 2012; p. 544. [Google Scholar]

- Mazumder, M.; Hossain, D.M. Research on corporate risk reporting: Current trends and future avenues. J. Asian Financ. Econ. Bus. 2018, 5, 29–41. [Google Scholar] [CrossRef]

- Yang, S.; Ishtiaq, M.; Anwar, M. Enterprise risk management practices and firm performance, the mediating role of competitive advantage and the moderating role of financial literacy. J. Risk Financ. Manag. 2018, 11, 35. [Google Scholar] [CrossRef] [Green Version]

- Hsu, M.-F.; Hsin, Y.-S.; Shiue, F.-J. Business analytics for corporate risk management and performance improvement. Ann. Oper. Res. 2021, 315, 629–669. [Google Scholar] [CrossRef]

- Villanueva, E.; Nuñez, M.A.; Martins, I. Impact of Risk Governance, Associated Practices and Tools on Enterprise Risk Management: Some Evidence from Colombia. Rev. Finanz. Política Económica 2022, 14, 187–206. [Google Scholar] [CrossRef]

- Dragomir, V.D. Theoretical aspects of environmental strategy. In Corporate Environmental Strategy; Springer: Cham, Switzerland, 2020; pp. 1–31. [Google Scholar] [CrossRef]

- Chaudhuri, A.; Boer, H.; Taran, Y. Supply chain integration, risk management and manufacturing flexibility. Int. J. Oper. Prod. Manag. 2018, 38, 690–712. [Google Scholar] [CrossRef] [Green Version]

- Fan, Y.; Stevenson, M. A review of supply chain risk management: Definition, theory, and research agenda. Int. J. Phys. Distrib. Logist. Manag. 2018, 48, 205–230. [Google Scholar] [CrossRef] [Green Version]

- Singh, N.P. Managing environmental uncertainty for improved firm financial performance: The moderating role of supply chain risk management practices on managerial decision making. Int. J. Logist. Res. Appl. 2020, 23, 270–290. [Google Scholar] [CrossRef]

- El Baz, J.; Ruel, S. Can supply chain risk management practices mitigate the disruption impacts on supply chains’ resilience and robustness? Evidence from an empirical survey in a COVID-19 outbreak era. Int. J. Prod. Econ. 2021, 233, 107972. [Google Scholar] [CrossRef]

- Elmsalmi, M.; Hachicha, W.; Aljuaid, A.M. Prioritization of the Best Sustainable Supply Chain Risk Management Practices Using a Structural Analysis Based-Approach. Sustainability 2021, 13, 4608. [Google Scholar] [CrossRef]

- Mingaleva, Z.; Deputatova, L.; Starkov, Y. Management of Organizational Knowledge as a Basis for the Competitiveness of Enterprises in the Digital Economy. Lect. Notes Netw. Syst. 2020, 78, 203–212. [Google Scholar] [CrossRef]

- Lee, J.; Lee, D.K. Application of industrial risk management practices to control natural hazards, facilitating risk communication. Int. J. Geo-Inf. 2018, 7, 377. [Google Scholar] [CrossRef] [Green Version]

- Krause, T.A.; Tse, Y. Risk management and firm value: Recent theory and evidence. Int. J. Account. Inf. Manag. 2016, 24, 56–81. [Google Scholar] [CrossRef]

- Eriandani, R.; Wijaya, L.I. Corporate Social Responsibility and Firm Risk: Controversial Versus Noncontroversial Industries. J. Asian Financ. Econ. Bus. 2021, 8, 953–965. [Google Scholar] [CrossRef]

- Kim, S.; Lee, G.; Kang, H.-G. Risk management and corporate social responsibility. Strateg. Manag. J. 2021, 42, 202–230. [Google Scholar] [CrossRef]

- Kuo, Y.-F.; Lin, Y.-M.; Chien, H.-F. Corporate social responsibility, enterprise risk management, and real earnings management: Evidence from managerial confidence. Financ. Res. Lett. 2021, 41, 101805. [Google Scholar] [CrossRef]

- Renault, B.; Agumba, J.; Ansary, N. An exploratory factor analysis of risk management practices: A study among small and medium contractors in Gauteng. Acta Structilia 2018, 25, 1–39. [Google Scholar] [CrossRef] [Green Version]

- Joshi, H. Corporate risk management, firms’ characteristics and capital structure: Evidence from Bombay Stock Exchange (BSE) Sensex Companies. Vision 2018, 22, 395–404. [Google Scholar] [CrossRef]

- Busru, S.A.; Shanmugasundaram, G.; Bhat, S.A. Corporate governance an imperative for stakeholders protection: Evidence from risk management of Indian listed firms. Bus. Perspect. Res. 2020, 8, 89–116. [Google Scholar] [CrossRef]

- Girangwa, K.G.; Rono, L.; Mose, J. The influence of enterprise risk management practices on organizational performance: Evidence from Kenyan State Corporations. J. Account. Bus. Financ. Res. 2020, 8, 11–20. [Google Scholar] [CrossRef] [Green Version]

- Avdiysky, V.I.; Bezdenezhnykh, V.M.; Katayeva, E.G. Risk management as a key element of ensuring the implementation of the risk-oriented approach in the activities of business entities. Econ. Taxes Right 2017, 10, 6–15. [Google Scholar]

- Akatov, N.; Mingaleva, Z.; Klačková, I.; Galieva, G.; Shaidurova, N. Expert Technology for Risk Management in the Implementation of QRM in a High-Tech Industrial Enterprise. Manag. Syst. Prod. Eng. 2019, 27, 250–254. [Google Scholar] [CrossRef] [Green Version]

- DuHadway, S.; Carnovale, S.; Hazen, B. Understanding risk management for intentional supply chain disruptions: Risk detection, risk mitigation, and risk recovery. Ann. Oper. Res. 2019, 283, 179–198. [Google Scholar] [CrossRef]

- Vincent, N.E.; Higgs, J.L.; Pinsker, R.E. Board and management-level factors affecting the maturity of IT risk management practices. J. Inf. Syst. 2019, 33, 117–135. [Google Scholar] [CrossRef]

- Liu, B.; Niu, Y.; Zhang, Y. Corporate liquidity and risk management with time-inconsistent preferences. Econ. Model. 2019, 81, 295–307. [Google Scholar] [CrossRef]

- Hao, J.P.; Kang, F. Corporate environmental responsibilities and executive compensation: A risk management perspective. Bus. Soc. Rev. 2019, 124, 145–179. [Google Scholar] [CrossRef] [Green Version]

- Tai, V.W.; Lai, Y.-H.; Yang, T.-H. The role of the board and the audit committee in corporate risk management. N. Am. J. Econ. Financ. 2020, 54, 100879. [Google Scholar] [CrossRef]

- Cassano, R. Corporate global responsibility and reputation risk management. Symphonya Emerg. Issues Manag. 2019, 1, 129–142. [Google Scholar] [CrossRef] [Green Version]

- Catanzaro, A.; Teyssier, C. Export promotion programs, export capabilities, and risk management practices of internationalized SMEs. Small Bus. Econ. 2021, 57, 1479–1503. [Google Scholar] [CrossRef]

- Christopher, J.; Sarens, G. Diffusion of Corporate Risk-Management Characteristics: Perspectives of Chief Audit Executives through a Survey Approach. Aust. J. Public Adm. 2018, 77, 427–441. [Google Scholar] [CrossRef]

- Wahlström, B. Models, modelling and modellers: An application to risk analysis. Eur. J. Oper. Res. 1994, 75, 477–487. [Google Scholar] [CrossRef]

- Alekseev, A. Stability analysis of the rating and control mechanism to agent’s strategic behavior (on example of the risk management policy coordination). Appl. Math. Control Sci. 2019, 4, 136–154. [Google Scholar] [CrossRef]

- Mingaleva, Z.A.; Lobova, E.S. “Portfolio analysis of innovative projects, taking into account endogenous and exogenous risks”. Programmy Dlia EVM. Bazy Dannykh. Topologii Integral’nykh Mikroskhem [Computer Programs. Database. Topologies of Integrated Circuits]. Computer program RU 2022664434. 29 July 2022. [Google Scholar]

- Jiang, J.; Feng, Y. The interaction of risk management tools: Financial hedging, corporate diversification and liquidity. Int. J. Financ. Econ. 2021, 26, 2396–2413. [Google Scholar] [CrossRef]

- Alekseev, A. Control of a complex objects, states of which are describing by the matrix rating mechanisms. Appl. Math. Control Sci. 2020, 1, 114–139. [Google Scholar] [CrossRef] [PubMed]

- Mingaleva, Z.; Akatov, N.; Butakova, M. A Syndinic approach to enterprise risk management. Lect. Notes Netw. Syst. 2021, 315, 293–305. [Google Scholar] [CrossRef]

- Beyth-Marom, R. How probable is probable? A numerical translation of verbal probability expressions. J. Forecast. 1982, 1, 257–269. [Google Scholar] [CrossRef]

- Ristić, D. A tool for risk assessment. Saf. Eng. 2013, 3, 121–127. [Google Scholar] [CrossRef]

- Thomas, P.; Bratvold, R.B.; Bickel, J.E. The risk of using risk matrices. SPE Econ. Manag. 2014, 6, 56–66. [Google Scholar] [CrossRef]

- Alekseev, A. The additive-multiplicative fuzzy aggregation matrix mechanism and equivalent it’s the continuous mechanism. In Proceedings of the 12th International Scientific and Practical Conference “Modern Complex Control Systems 2017”, Lipetsk, Russia, 25–27 October 2017; Volume 1, pp. 15–20. [Google Scholar]

- Alekseev, A. On strategy-proofness of matrix integrated rating mechanism. In Proceedings of the Socio-Physics and Socio-Engineering, Moscow, Russia, 23–25 May 2018; pp. 179–180. [Google Scholar]

- Alekseev, A.; Salamatina, A.; Kataeva, T. Rating and Control Mechanisms Design in the Program “Research of Dynamic Systems”. In Proceedings of the 2019 IEEE 21st Conference on Business Informatics (CBI), Moscow, Russia, 15–17 July 2019; pp. 96–105. [Google Scholar] [CrossRef]

- Cobb, C.W.; Douglas, P.H. A Theory of production. Am. Econ. Rev. 1928, 18, 139–165. [Google Scholar]

- Alekseev, A.; Noskova, A.; Neifeld, V. The Software Modules “Insider” as a KYC-Solution for Industrial Verification and Bankruptcy Prediction. In Proceedings of the 2022 4th International Conference on Control Systems, Mathematical Modeling, Automation and Energy Efficiency (SUMMA), Lipetsk, Russia, 9–11 November 2022; pp. 623–626. [Google Scholar] [CrossRef]

- Löffler, G.; Posch, P.N. Credit Risk Modeling Using Excel and VBA; John Wiley & Sons Ltd.: Hoboken, NJ, USA, 2007; p. 278. [Google Scholar]

- Alexander, C. Market Risk Analysis, Practical Financial Econometrics; John Wiley & Sons Ltd.: Chichester, UK, 2008; p. 387. [Google Scholar]

- Lewis, N. Operational Risk with Excel and VBA: Applied Statistical Methods for Risk Management; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2004; 259p. [Google Scholar]

- Tysiak, W.; Sereseanu, A. Monte Carlo simulation in risk management in projects using Excel. In Proceedings of the IEEE International Workshop on Intelligent Data Acquisition and Advanced Computing Systems: Technology and Applications, Cosenza, Italy, 21–23 September 2009; pp. 581–585. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Risk Significant Score | Generalized Risk Category | Risk Response Strategy |

|---|---|---|

| 4 | extreme risk (e) | avoidance |

| 3 | high risk (h) | transfer |

| 2 | medium risk (m) | mitigation |

| 1 | negligible risk (n) | acceptance |

| Risk Significant Score | Risk Event Likelihood/ Probability 1 | Risk Event Consequences |

|---|---|---|

| 4 | very likely (v) | disastrous (d) |

| 3 | likely (l) | critical (c) |

| 2 | possible (p) | significant (s) |

| 1 | unlikely (u) | acceptable (a) |

| No. | Risk Register | Current Values of Risk-Forming Parameters: Likelihood (Probability) and Consequences | Minimal Values of Risk-Forming Parameters (Limits for Reducing) | ||

|---|---|---|---|---|---|

| XL | XC | XLmin | XCmin | ||

| 1 | Risk factor 1 | 3.0 | 4.0 | 2.0 | 2.5 |

| 2 | Risk factor 2 | 4.0 | 4.0 | 1.3 | 1.2 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alekseev, A.; Mingaleva, Z.; Alekseeva, I.; Lobova, E.; Oksman, A.; Mitrofanov, A. Developing a Numerical Method of Risk Management Taking into Account the Decision-Maker’s Subjective Attitude towards Multifactorial Risks. Computation 2023, 11, 132. https://doi.org/10.3390/computation11070132

Alekseev A, Mingaleva Z, Alekseeva I, Lobova E, Oksman A, Mitrofanov A. Developing a Numerical Method of Risk Management Taking into Account the Decision-Maker’s Subjective Attitude towards Multifactorial Risks. Computation. 2023; 11(7):132. https://doi.org/10.3390/computation11070132

Chicago/Turabian StyleAlekseev, Aleksandr, Zhanna Mingaleva, Irina Alekseeva, Elena Lobova, Alexander Oksman, and Alexander Mitrofanov. 2023. "Developing a Numerical Method of Risk Management Taking into Account the Decision-Maker’s Subjective Attitude towards Multifactorial Risks" Computation 11, no. 7: 132. https://doi.org/10.3390/computation11070132

APA StyleAlekseev, A., Mingaleva, Z., Alekseeva, I., Lobova, E., Oksman, A., & Mitrofanov, A. (2023). Developing a Numerical Method of Risk Management Taking into Account the Decision-Maker’s Subjective Attitude towards Multifactorial Risks. Computation, 11(7), 132. https://doi.org/10.3390/computation11070132