Evolutionary Game of Small and Medium-Sized Enterprises’ Accounts-Receivable Pledge Financing in the Supply Chain

Abstract

:1. Introduction

2. Literature Review

3. Evolutionary Game Analysis of SCARPF

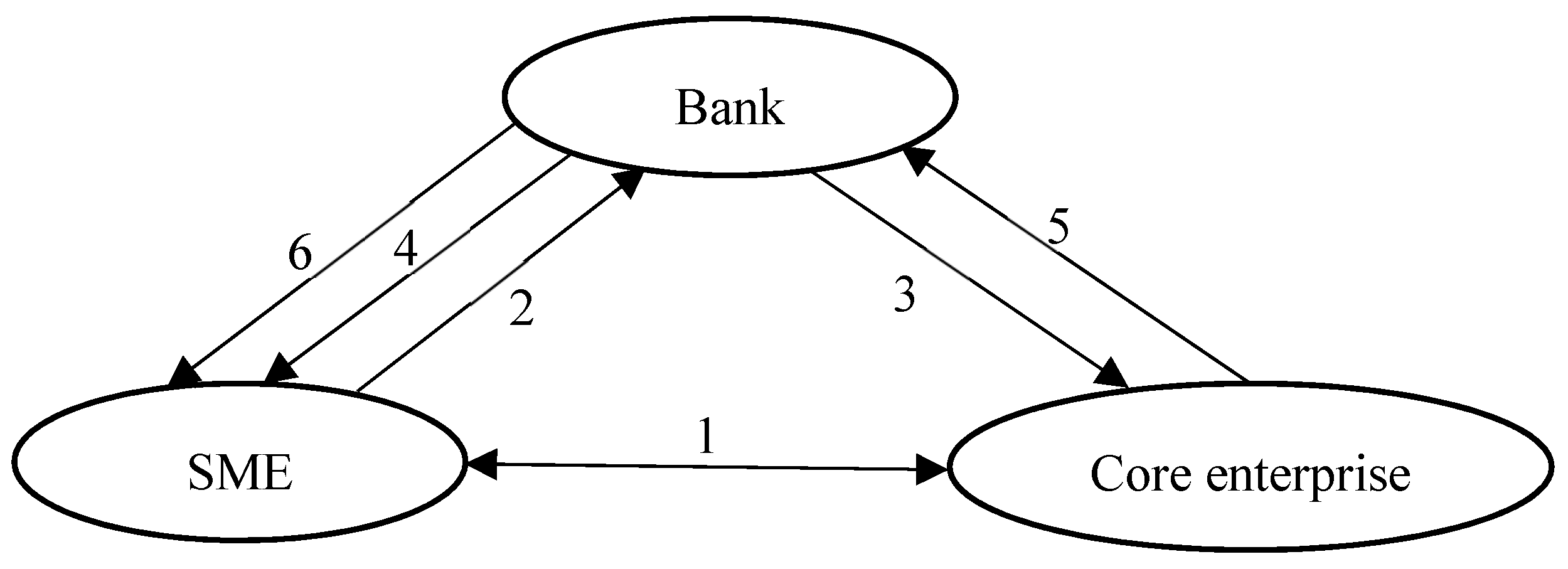

3.1. Business Process of SCARPF

- The SME trades with the core enterprise to generate accounts receivable;

- The SME in the upstream of the supply chain submits an application for SCARPF to the bank;

- After receiving the SME financing application, the bank confirms the creditor’s rights to these accounts receivable to the downstream core enterprise;

- After the creditor’s rights to the core enterprise’s bill are confirmed, the bank and the SME will sign an agreement on financing matters to lend to SMEs. At the same time, the SME establishes a collection account in the bank and informs the core enterprise;

- The core enterprise will transfer the accounts receivable to the collection account by the due date of the agreed financing period;

- The bank will liquidate the financing and transfer the remaining funds to the SME after deducting the income.

3.2. The Strategic Space of Supply Chain Members

3.3. Model Specification

- (1)

- The total number of accounts receivable of the SME is . The rate of return for normal production of the SME is . The rate of return for normal production of the core enterprise is .

- (2)

- The bank’s pledge rate for accounts receivable is . The interest rate is . The financing period is 1 year. The supervision cost of a single SCARPF is (). The probability that the bank chooses the lending strategy is (), then the probability that the bank chooses the non-lending strategy is .

- (3)

- The unilateral breach of the contract by the SME has caused losses in the creditworthiness of the core enterprise. The core enterprise will punish the SME, that is, punishment from the supply chain, such as reducing cooperation opportunities or terminating cooperation, which is recorded as . Due to the unilateral default of the SME, based on the confirmation of the creditor’s rights of the core enterprise bill, the core enterprise must pay () to the bank according to the agreement. The probability that the SME breaks the contract is (), and the probability that the SME keeps the contract is .

- (4)

- The probability of core enterprise and SME joint loan fraud is (). The benefits of core enterprise and SME joint loan fraud will be distributed between the SME and the core enterprise. The proportion of the benefits received by the SME is (). The proportion of benefits received by the core enterprise is .

- (5)

- The SME can obtain financing to produce, and due to the important position of the core enterprise in the business of the SME, the SME will give priority to meeting the procurement needs of the core enterprise. At the same time, the SME will supply the core enterprise in a fixed cycle and fixed batch. SCARPF is based on the confirmation of the creditor’s rights relationship of the core enterprise, so when the SME can obtain financing, it will meet the core enterprise’s procurement needs. However, when the SME unilaterally breaks the contract, it will not supply the core enterprise.

- (1)

- When the bank decides to lend to the SME, the SME can also keep the contract when the core enterprise transfers the accounts receivable to the collection account. That is, the strategic combination of the bank and the SME is (lending, keep the contract). At this time, the three-party income expressions of the bank, the core enterprise and the SME are , , , respectively.

- (2)

- When the bank decides not to lend to the SME, due to the constraints of procurement contracts between the SME and the core enterprise, and considering the impact of the core enterprise on the business of the SME, the SME will still give priority to meeting the procurement needs of the core enterprise. The strategic combination of the bank and the SME is (no lending, keep the contract). At this time, the three-party income expressions of the bank, the core enterprise and the SME are , , , respectively.

- (3)

- When the bank decides to lend to the SME and there is no joint loan fraud between the core enterprise and the SME, the SME unilaterally breaks the contract. In this case, the strategic combination of the bank, the core enterprise, and the SME is (lending, no joint loan fraud, break the contract). At this time, the three-party income expressions of the bank, the core enterprise and the SME are , , , respectively.

- (4)

- When the bank decides not to lend to the SME, the SME unilaterally breaks the contract. That is, the strategic combination of the bank, the core enterprise, and the SME is (no lending, no joint loan fraud, break the contract). At this time, the three-party income expressions of the bank, the core enterprise and the SME are , , , respectively.

- (5)

- When the bank decides to lend to the SME, and there is joint loan fraud between the core enterprise and the SME, the strategic combination of the bank, the core enterprise, and the SME is (lending, joint loan fraud, break the contract). At this time, the three-party income expressions of the bank, the core enterprise and the SME are , , , respectively.

- (6)

- When the bank decides not to lend to the SME and there is no joint loan fraud between the core enterprise and the SME, the strategic combination of the bank, the core enterprise, and the SME is (no lending, joint loan fraud, break the contract). At this time, the three-party income expressions of the bank, the core enterprise and the SME are 0, 0, 0, respectively.

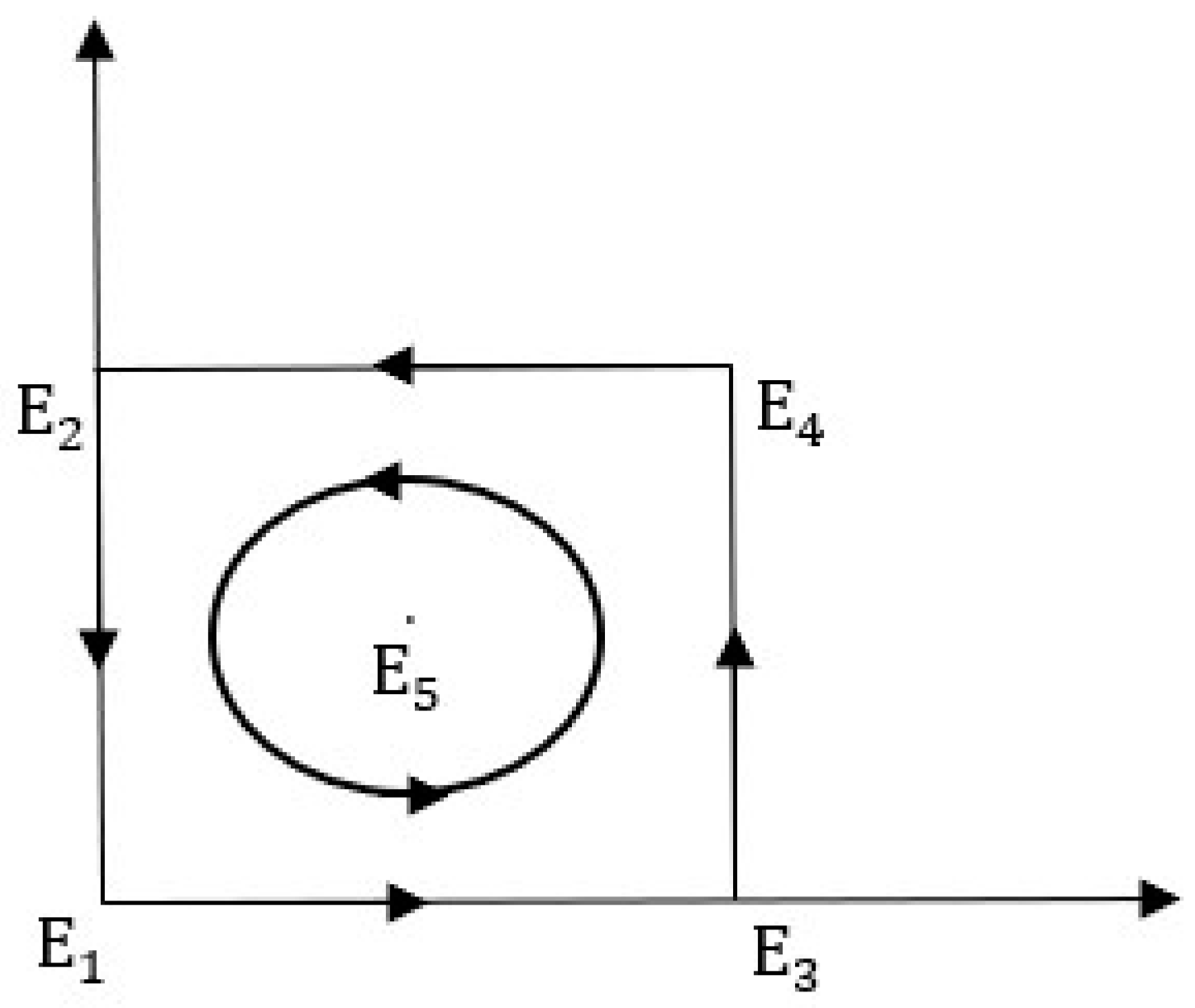

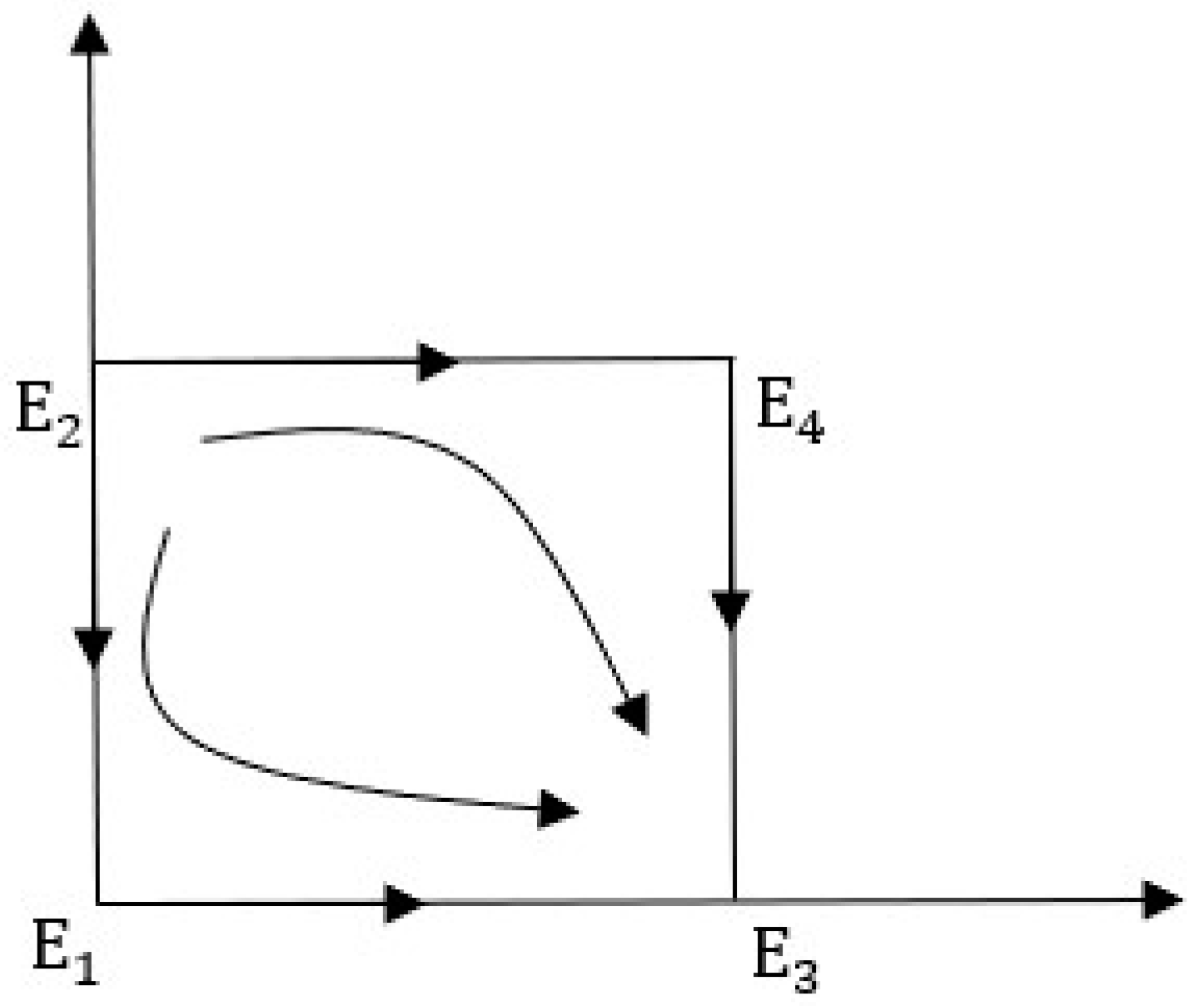

3.4. Stability and Evolution Path Analysis

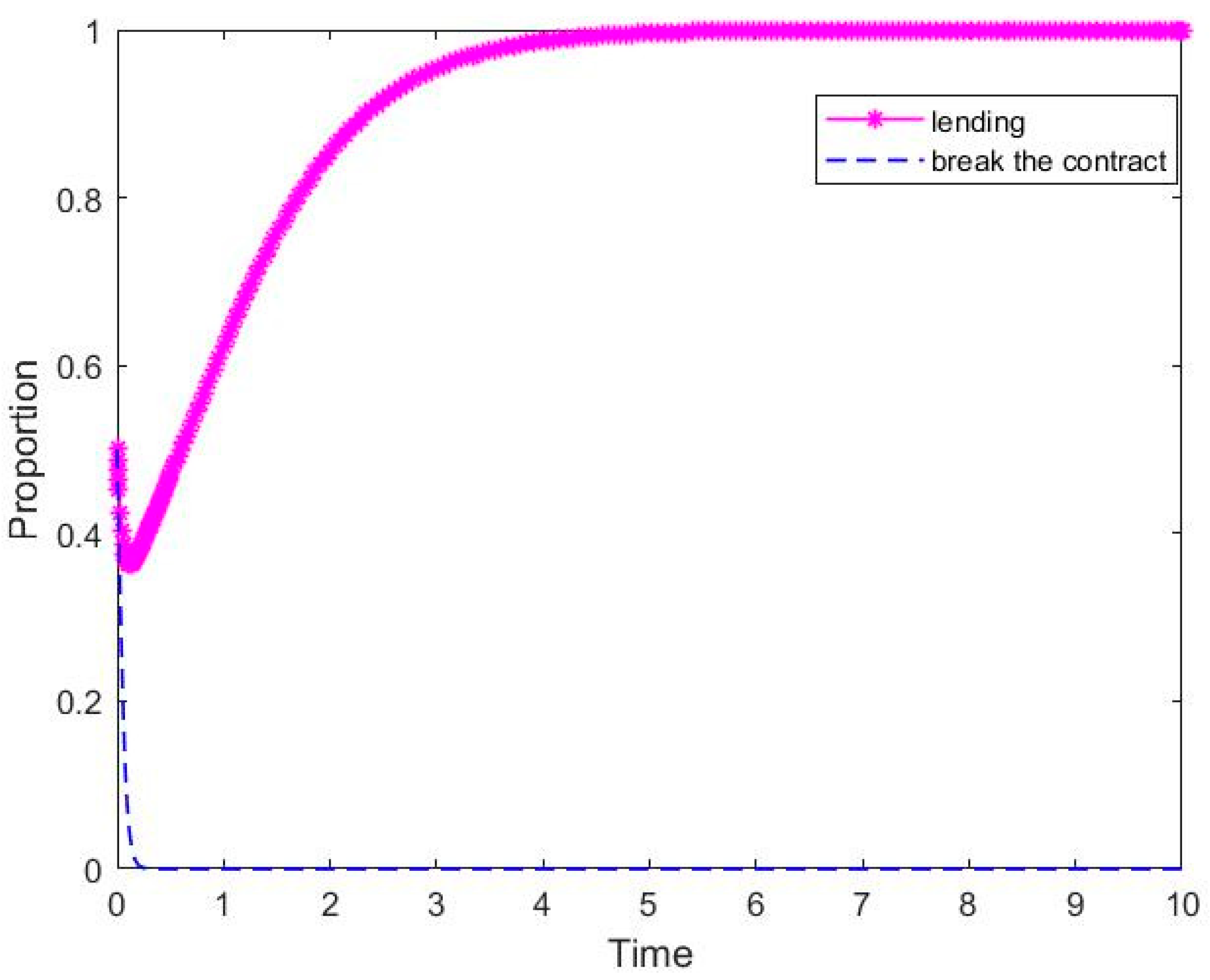

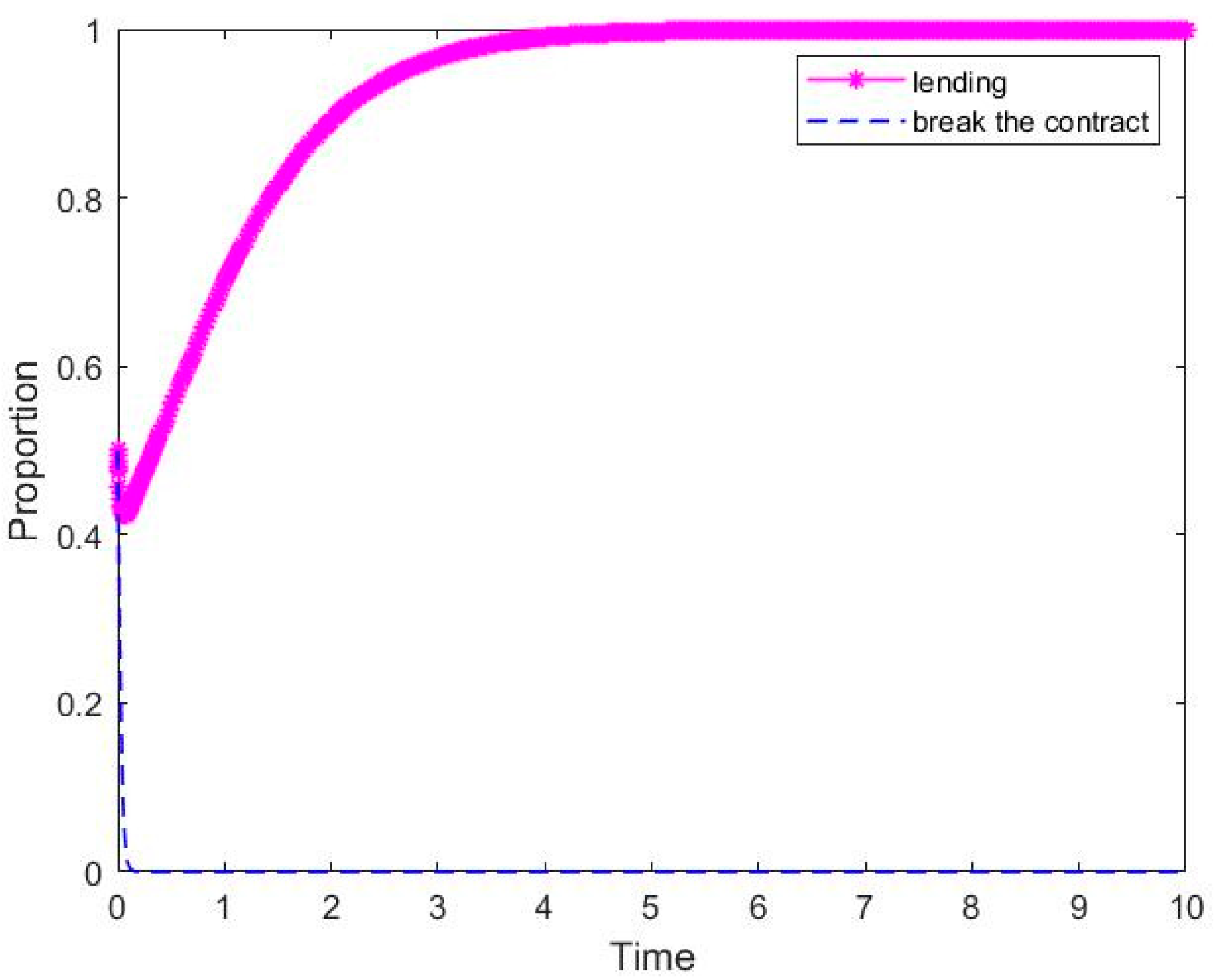

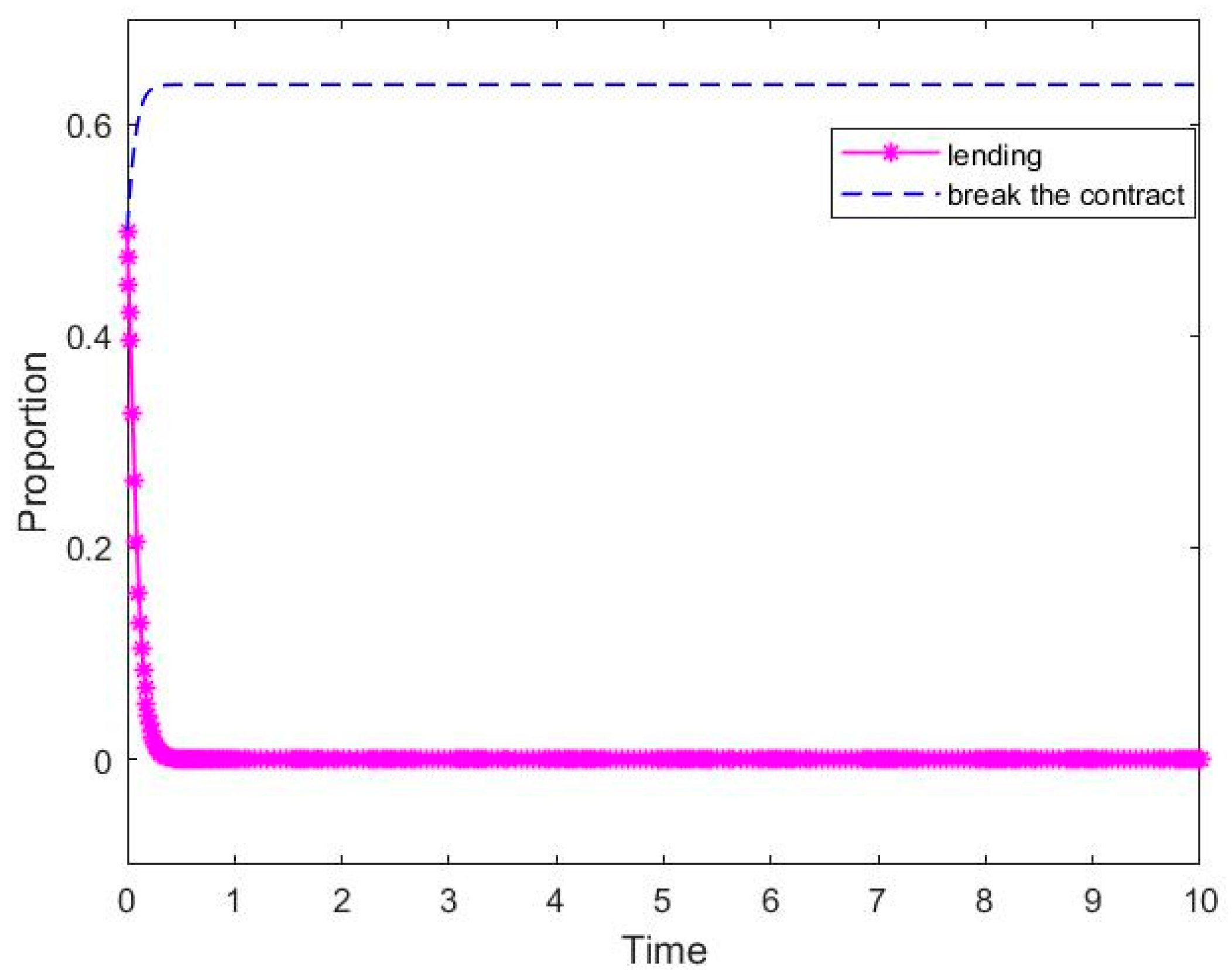

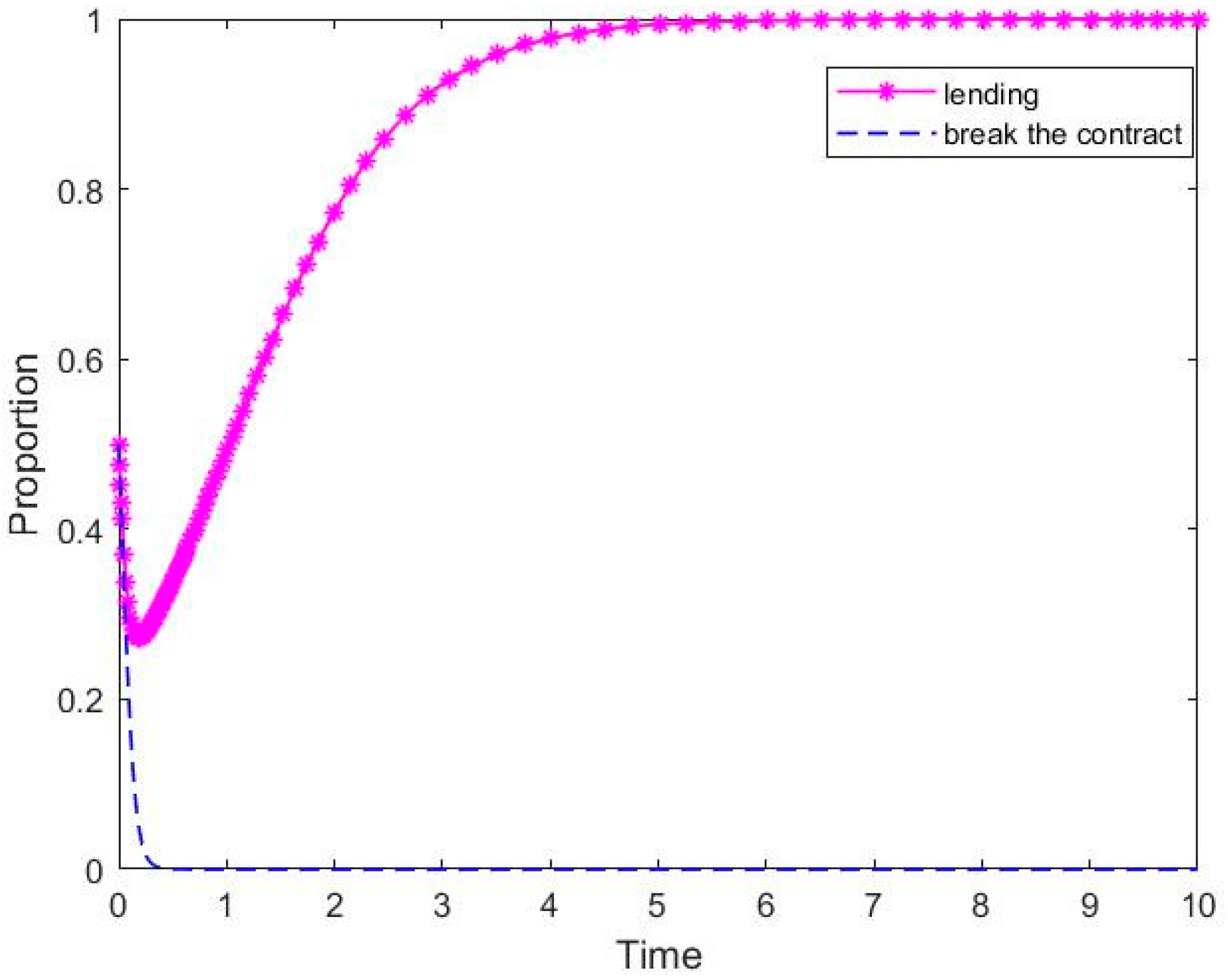

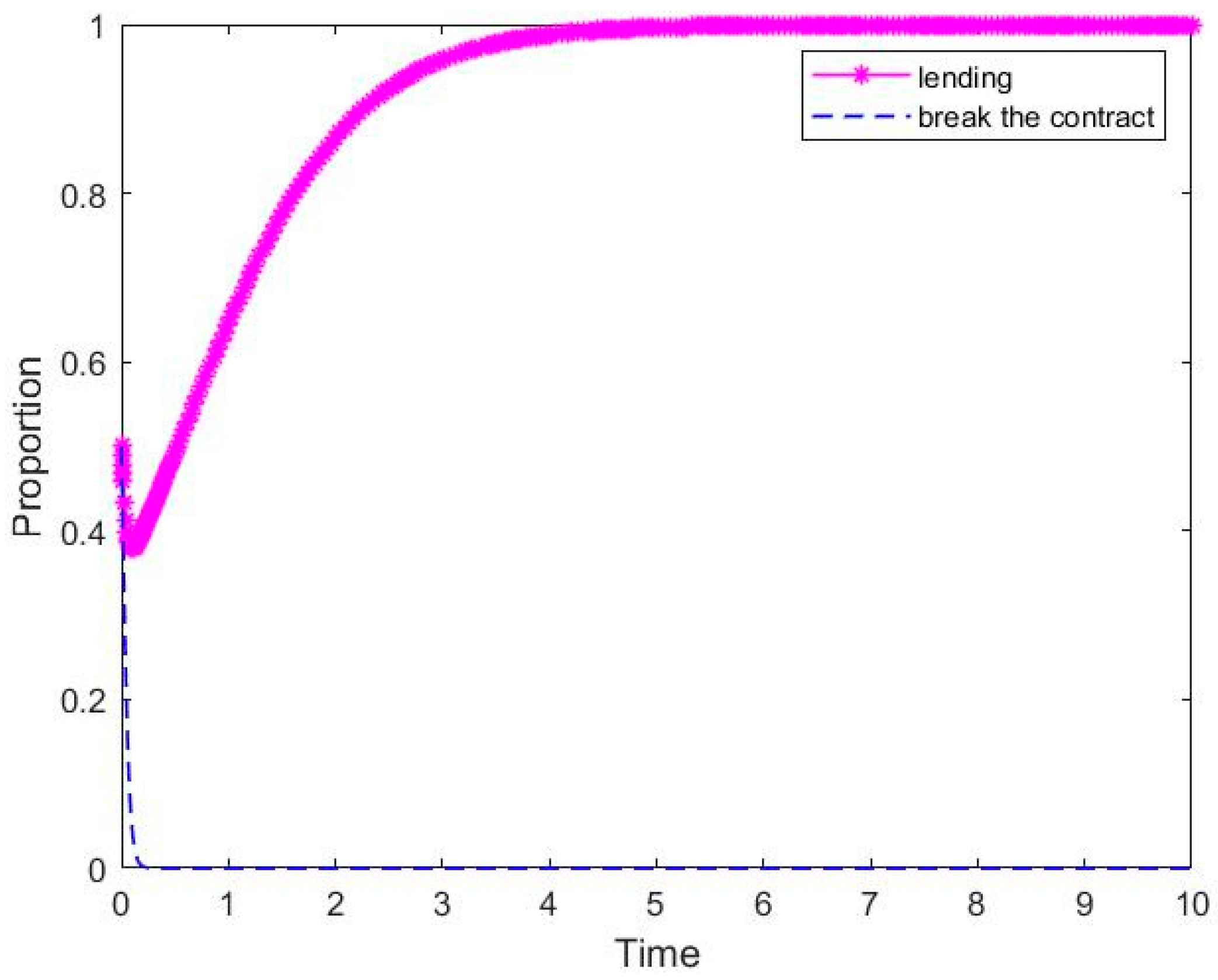

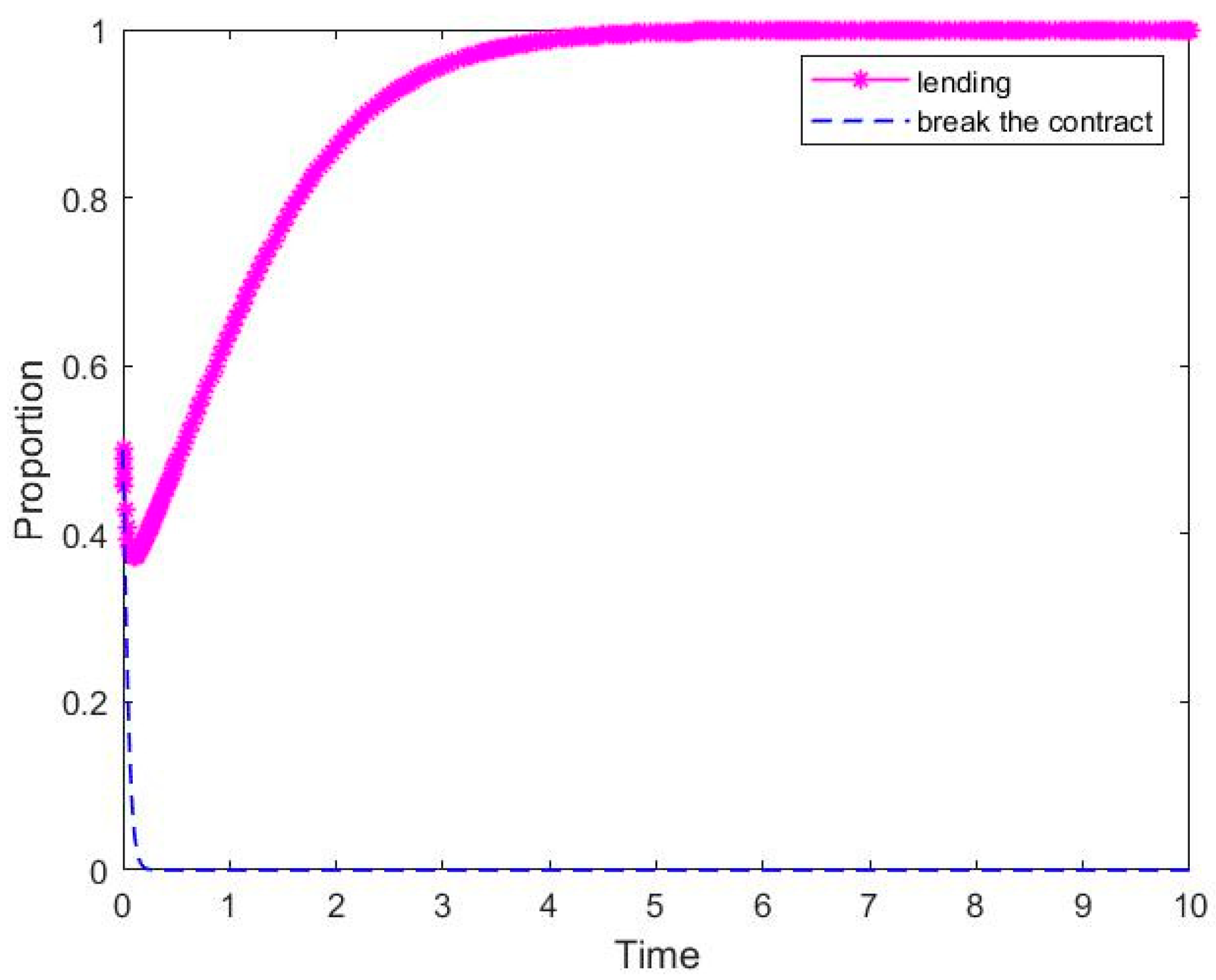

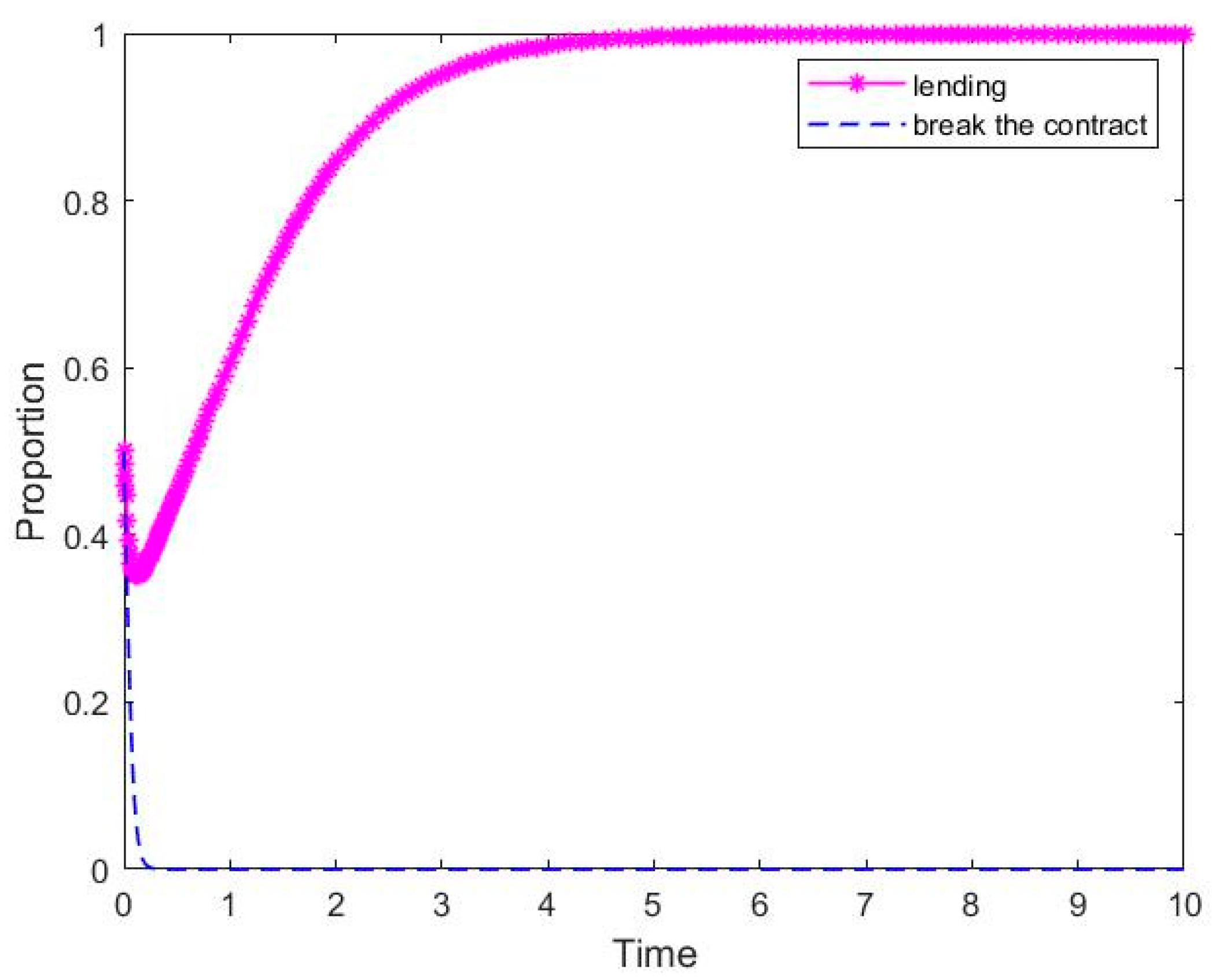

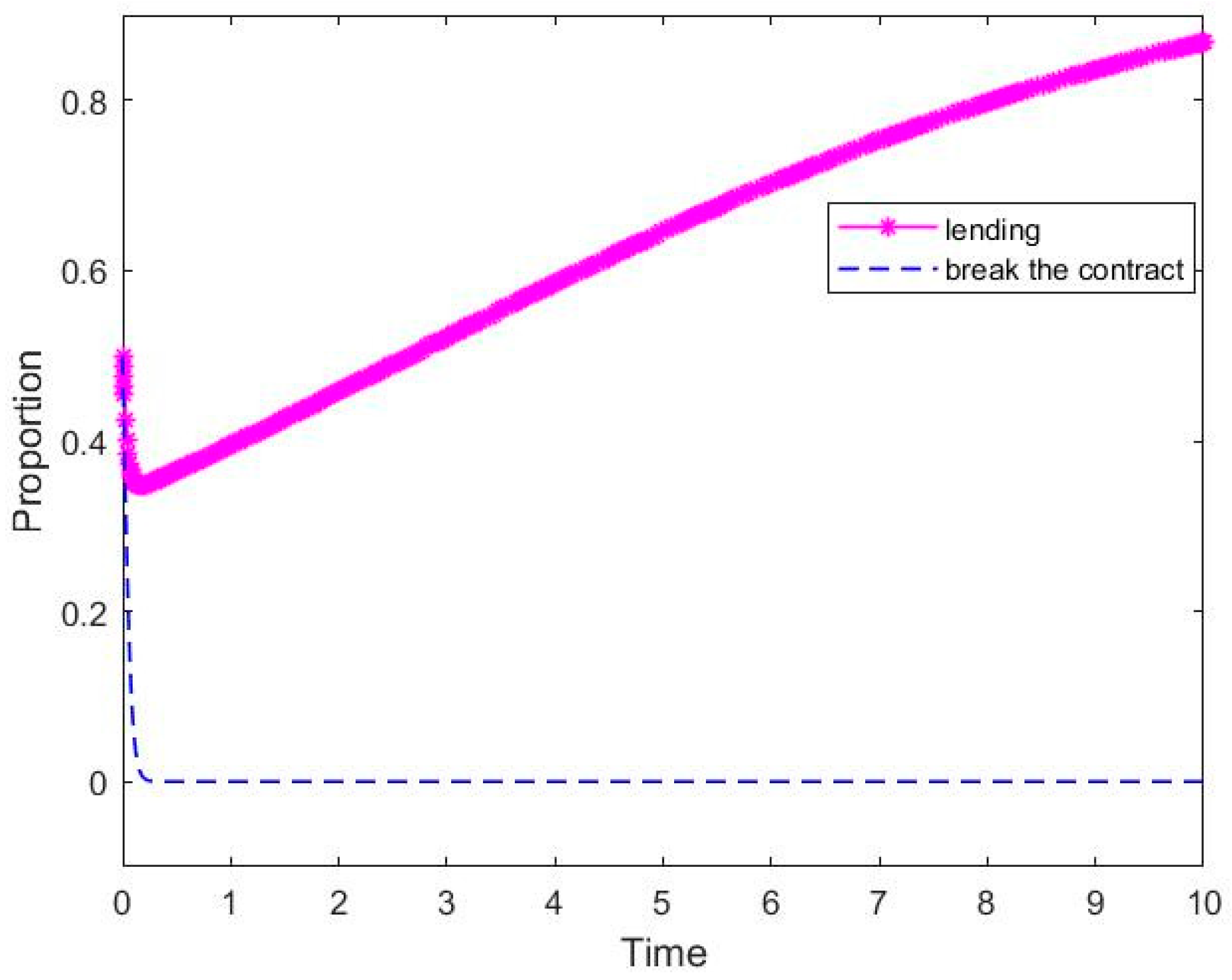

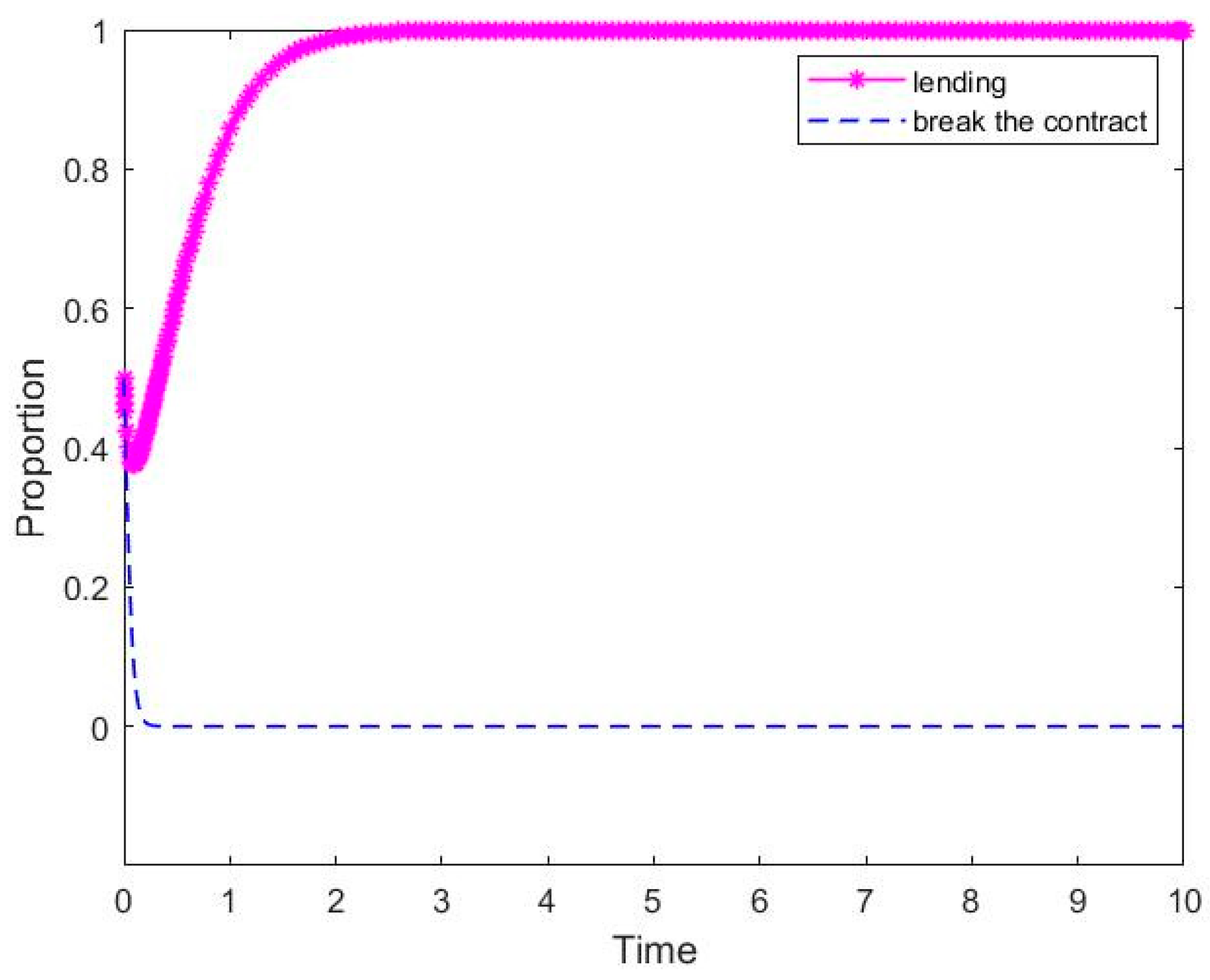

4. Numerical Simulation

5. Research Results

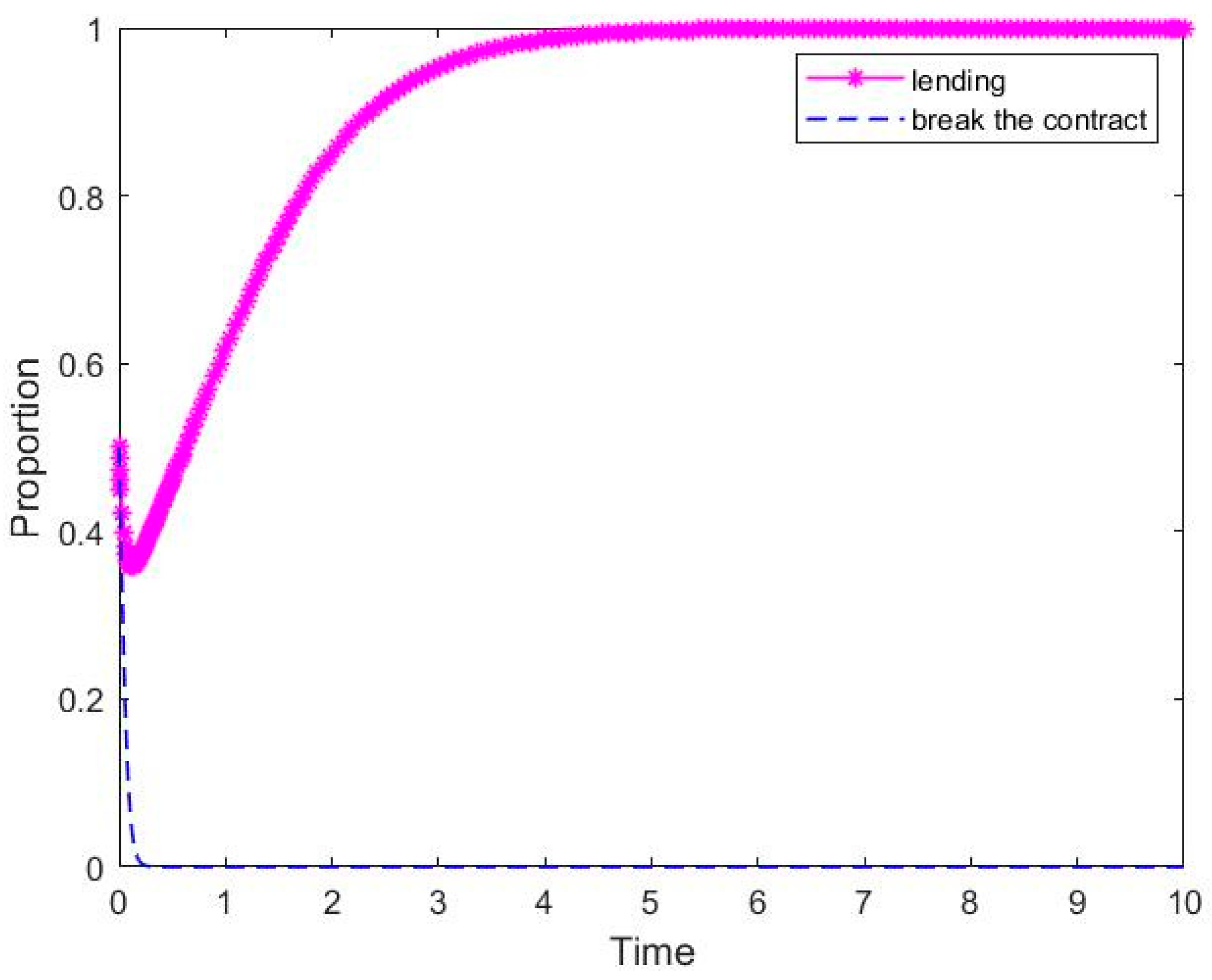

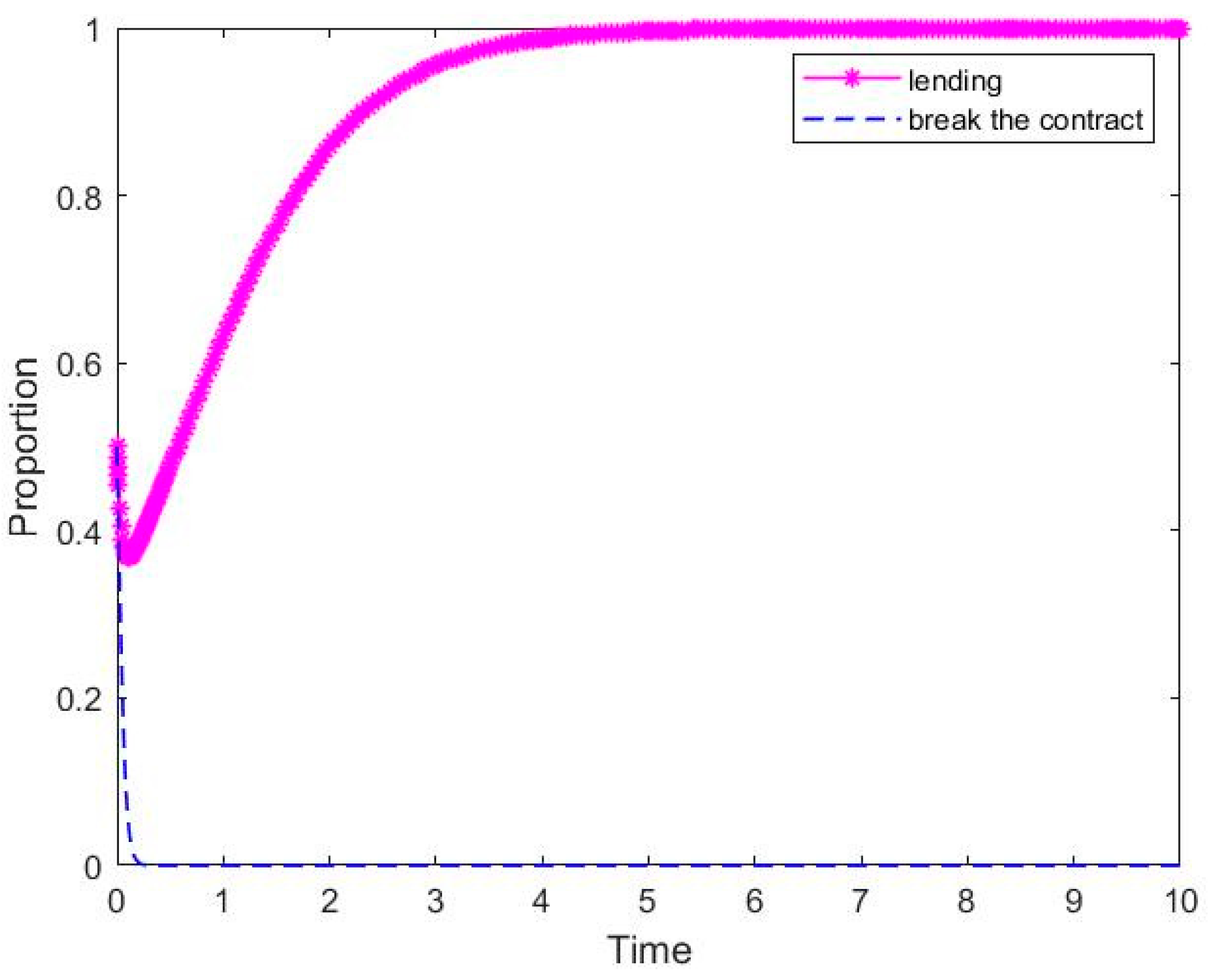

- The evolutionary game model will have two different evolutionary cases under different initial conditions: one without ESS and the other with ESS (lending, keep the contract);

- The higher the rate of return during normal production of the SME, the more profits it obtains through normal production. The SME will be more inclined to keep the contract. This is consistent with [30,31]. That is, the system will tend to evolve in the direction of (lending, keep the contract). As the SME can obtain more profits through production, there is no need to conduct default operations;

- The higher the bank loan interest rate, the more the bank tends to lend. This is because the bank can make more profit by lending. However, the high interest rate means a high capital cost for the SME, which has also been pointed out by [28]. As a result, although the bank tends to lend, the SME may give up loans because it cannot repay the exorbitant interest rate;

- The greater the supply chain punishment when the SME unilaterally breaks the contract, the more likely that the SME will keep the contract. This is consistent with [11]. Therefore, the punishment mechanism of the supply chain is conducive to the evolution of the system to stable equilibrium;

- When the probability of joint loan fraud is small enough or equal to zero, the bank will be able to avoid risks based on the strong credit of the core enterprise. The bank will be happy to carry out SCARPF with the SME, and the SME can solve financing problems. The existence of joint loan fraud is not conducive to the SME obtaining financing;

- The smaller the proportion of income distribution of the SME under joint loan fraud, the less income the SME will obtain through default. Accordingly, its motivation for default will be reduced.

6. Conclusions

- (1)

- In order to solve the financing problems of SMEs and help banks and core enterprises to obtain more profits, the relevant parameters of the model should be limited to a reasonable range. When the conditions of Case 2 are met, the system will evolve in a direction that is beneficial to banks, core enterprises and SMEs. When banks, core enterprises and SMEs make decisions, they should fully consider the decisions that other participants may make and try to make relevant decision parameters meet the conditions of Case 2. This will benefit all game participants in the entire supply chain system to obtain better results.

- (2)

- It is very important that supply chain members make reasonable decisions. Reasonable decisions can help the system reach an evolutionary stable state faster. For banks, they should pay attention to the supervision of core enterprises, focusing on preventing the joint loan fraud of core enterprises and SMEs. When confirming the bill creditor’s rights to core enterprises, banks should not only stay at the level of confirmation, but also consider whether there is intentional confirmation to achieve the purpose of joint loan fraud, especially for those core enterprises that have had major events of default. Banks can also raise lending interest rates, because the higher the lending interest rate, the more banks tend to lend, and SMEs can increase the availability of financing. However, banks should raise the lending interest rate within an appropriate range. For SMEs, if they want to obtain a benign SCARPF cycle, on the one hand, they must not default on their own contracts and, on the other hand, they must not cooperate with core enterprises to commit joint loan fraud. SMEs should place the growth point of financing income on how to improve their own rate of return during normal production. For core enterprises, they cannot commit joint loan fraud with SMEs. Core enterprises should also increase the punishment when SMEs break the contract. When the punishment is greater, the breach of contract of SMEs will be restricted, and evolution can become a virtuous circle. Based on this, core enterprises should improve the credit investigation system for SMEs that cooperate with themselves for SCARPF, take dishonesty as an important consideration of enterprise cooperation, establish a dishonesty event threshold, and terminate the cooperative relationship after reaching the threshold.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Motta, V.; Sharma, A. Lending technologies and access to finance for SMEs in the hospitality industry. Int. J. Hosp. Manag. 2019, 86, 102371. [Google Scholar] [CrossRef]

- Lin, M.S.; Song, H.J.; Sharma, A.; Lee, S. Formal and informal SME financing in the restaurant industry: The impact of macroenvironment. J. Hosp. Tour. Manag. 2020, 45, 276–284. [Google Scholar] [CrossRef]

- Oztemel, E.; Ozel, S. A conceptual model for measuring the competency level of Small and Medium-sized Enterprises (SMEs). Adv. Prod. Eng. Manag. 2021, 16, 47–66. [Google Scholar] [CrossRef]

- Shi, J. The Financial Services Development Report of China’s Small, Medium and Micro Enterprises; China Financial Publishing House: Beijing, China, 2020; pp. 1–10. [Google Scholar]

- Barkley, B.; Mille, C.K.; Recto, M.C. 2015 Small Business Credit Survey: Report on Employer; Springer: New York, NY, USA, 2016. [Google Scholar]

- Chen, X. A model of trade credit in a capital-constrained distribution channel. Int. J. Prod. Econ. 2015, 159, 347–357. [Google Scholar] [CrossRef]

- Zhou, Y.W.; Wen, Z.L.; Wu, X. A single-period inventory and payment model with partial trade credit. Comput. Ind. Eng. 2015, 90, 132–145. [Google Scholar] [CrossRef]

- Owens, J.; Wilhelm, L. Alternative Data Transforming SME Finance. 2017. Available online: https://documents.shihang.org (accessed on 1 January 2021).

- Tsai, K.S. Financing small and medium enterprises in China: Recent trends and prospects beyond shadow banking. Hkust IEMS Work. Paper 2015, 1, 1–47. [Google Scholar] [CrossRef] [Green Version]

- Kouvelis, P.; Zhao, W. Who should finance the supply chain? Impact of credit ratings on supply chain decisions. M & SOM Manuf. Serv. Op. 2018, 20, 19–35. [Google Scholar]

- Cao, W.; Ma, C. A game analysis of account receivable financing based on supply chain finance. Commun. Res. 2013, 55, 168–173. [Google Scholar]

- Hofmann, E.; Kotzab, H. A supply chain-oriented approach of working capital management. J. Bus. Logist. 2010, 31, 305–330. [Google Scholar] [CrossRef]

- Jing, B.; Seidmann, A. Finance sourcing in a supply chain. Decis. Support Syst. 2013, 58, 15–20. [Google Scholar] [CrossRef]

- Caniato, F.; Gelsomino, L.M.; Perego, A.; Ronchi, S. Does finance solve the supply chain financing problem? Supply. Chain. Manag. 2016, 21, 534–549. [Google Scholar] [CrossRef]

- Yan, N.; Sun, B. Comparative analysis of supply chain financing strategies between different financing modes. J. Ind. Manag. Optim. 2015, 11, 1073–1087. [Google Scholar] [CrossRef]

- Shi, J.; Li, Q.; Chu, L.K.; Shi, Y. Effects of demand uncertainty reduction on the selection of financing approach in a capital-constrained supply chain. Transport. Res. E Log. 2021, 148, 102266. [Google Scholar] [CrossRef]

- Wang, M.; Zhao, R.; Li, B. Impact of financing models and carbon allowance allocation rules in a supply chain. J. Clean. Prod. 2021, 302, 126794. [Google Scholar] [CrossRef]

- Zhang, Y.; Chen, W.; Li, Q. Third-party remanufacturing mode selection for a capital-constrained closed-loop supply chain under financing portfolio. Comput. Ind. Eng. 2021, 157, 107315. [Google Scholar] [CrossRef]

- Yan, N.; Sun, B.; Zhang, H.; Liu, C. A partial credit guarantee contract in a capital-constrained supply chain: Financing equilibrium and coordinating strategy. Int. J. Prod. Econ. 2016, 173, 122–133. [Google Scholar] [CrossRef]

- Zhao, J.; Duan, Y. The coordination mechanism of supply chain finance based on tripartite game theory. J. Shanghai Jiaotong Univ. 2016, 21, 370–373. [Google Scholar] [CrossRef]

- Gao, G.; Fan, Z.; Fang, X.; Yun, F. Optimal Stackelberg strategies for financing a supply chain through online peer-to-peer lending. Eur. J. Oper. Res. 2018, 267, 585–597. [Google Scholar] [CrossRef]

- Jing, B.; Chen, X.; Cai, G. Equilibrium financing in a distribution channel with capital constraint. Prod. Oper. Manag. 2012, 21, 1090–1101. [Google Scholar] [CrossRef]

- Wu, D.D.; Yang, L.; Olson, D.L. Green supply chain management under capital constraint. Int. J. Prod. Econ. 2019, 215, 3–10. [Google Scholar]

- Yang, H.; Sun, F.; Chen, J.; Chen, B. Financing decisions in a supply chain with a capital-constrained manufacturer as new entrant. Int. J. Prod. Econ. 2019, 216, 321–332. [Google Scholar] [CrossRef]

- Luo, Y.; Wei, Q.; Ling, Q.; Huo, B. Optimal decision in a green supply chain: Bank financing or supplier financing. J. Clean. Prod. 2020, 271, 122090. [Google Scholar] [CrossRef]

- An, S.; Li, B.; Song, D.; Chen, X. Green credit financing versus trade credit financing in a supply chain with carbon emission limits. Eur. J. Oper. Res. 2021, 292, 125–142. [Google Scholar] [CrossRef]

- Jin, W.; Zhang, Q.; Luo, J. Non-collaborative and collaborative financing in a bilateral supply chain with capital constraints. Omega 2019, 88, 210–222. [Google Scholar] [CrossRef]

- Lin, Q.; He, J. Supply chain contract design considering the supplier’s asset structure and capital constraints. Comput. Ind. Eng. 2019, 137, 106044. [Google Scholar] [CrossRef]

- Liu, W.; Long, S.; Xie, D.; Liang, Y.; Wang, J. How to govern the big data discriminatory pricing behavior in the platform service supply chain? An examination with a three-party evolutionary game model. Int. J. Prod. Econ. 2021, 231, 107910. [Google Scholar] [CrossRef]

- Cui, H.; Wang, R.; Wang, H. An evolutionary analysis of green finance sustainability based on multi-agent game. J. Clean. Prod. 2020, 269, 121799. [Google Scholar] [CrossRef]

- Zhang, Y.; Khan, S.A.R. Evolutionary game analysis of green agricultural product supply chain financing system: COVID-19 pandemic. Int. J. Logist. Res. Appl. 2021, 4, 1–21. [Google Scholar]

- Friedman, D. Evolutionary games in economics. Econometrica 1991, 59, 637–666. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Literature | Supply Chain Member Behavior | Financing Subject | Game Participants | Joint Fraud | |||||

|---|---|---|---|---|---|---|---|---|---|

| Perfectly Rational | Bounded Rational | Manufacturer | Retailer | SME | Two Sides | Tripartite | Yes | No | |

| [19] | √ | √ | √ | √ | |||||

| [20] | √ | √ | √ | √ | |||||

| [21] | √ | √ | √ | √ | |||||

| [22] | √ | √ | √ | √ | |||||

| [23] | √ | √ | √ | √ | |||||

| [24] | √ | √ | √ | √ | |||||

| [25] | √ | √ | √ | √ | |||||

| [26] | √ | √ | √ | √ | |||||

| [30] | √ | √ | √ | √ | |||||

| This paper | √ | √ | √ | √ | |||||

| SME Core Enterprise Bank | |||

|---|---|---|---|

| 0 | 0 | 0 | |

| 0 | |||

| 0 | 0 | ||

| Condition | Equilibrium Point | Conclusion | |||

|---|---|---|---|---|---|

| Case 1 | . | − | uncertain | Saddle point | |

| − | uncertain | Saddle point | |||

| − | uncertain | Saddle point | |||

| − | uncertain | Saddle point | |||

| + | 0 | Central point | |||

| Case 2 | . | − | uncertain | Saddle point | |

| − | uncertain | Saddle point | |||

| + | − | ESS | |||

| + | + | Unstable | |||

| / | / | / | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hu, H.; Li, Y.; Tian, M.; Cai, X. Evolutionary Game of Small and Medium-Sized Enterprises’ Accounts-Receivable Pledge Financing in the Supply Chain. Systems 2022, 10, 21. https://doi.org/10.3390/systems10010021

Hu H, Li Y, Tian M, Cai X. Evolutionary Game of Small and Medium-Sized Enterprises’ Accounts-Receivable Pledge Financing in the Supply Chain. Systems. 2022; 10(1):21. https://doi.org/10.3390/systems10010021

Chicago/Turabian StyleHu, Haiju, Yakun Li, Mao Tian, and Xinjiang Cai. 2022. "Evolutionary Game of Small and Medium-Sized Enterprises’ Accounts-Receivable Pledge Financing in the Supply Chain" Systems 10, no. 1: 21. https://doi.org/10.3390/systems10010021

APA StyleHu, H., Li, Y., Tian, M., & Cai, X. (2022). Evolutionary Game of Small and Medium-Sized Enterprises’ Accounts-Receivable Pledge Financing in the Supply Chain. Systems, 10(1), 21. https://doi.org/10.3390/systems10010021