Research on Credit Evaluation Indicator System of High-Tech SMEs: From the Social Capital Perspective

Abstract

:1. Introduction

2. Literature Review

2.1. Credit Evaluation Indicator Systems of High-Tech SMEs

2.2. Influencing Factors of Enterprise Credit

2.3. Comment on Literature

3. Research on Credit Evaluation Indicator System of High-Tech SMEs

3.1. Construction of Indicator System

3.1.1. Financial Indicators

3.1.2. Nonfinancial Indicators

3.2. Empirical Application of Indicator System

3.2.1. Sample Selection

3.2.2. Data Collection and Processing

3.2.3. Evaluation Process

- Financial indicators

- Nonfinancial indicators

0.0230 X18 + 0.0071 X19 + 0.0272 X20 + 0.0232 X21 + 0.0624 X22

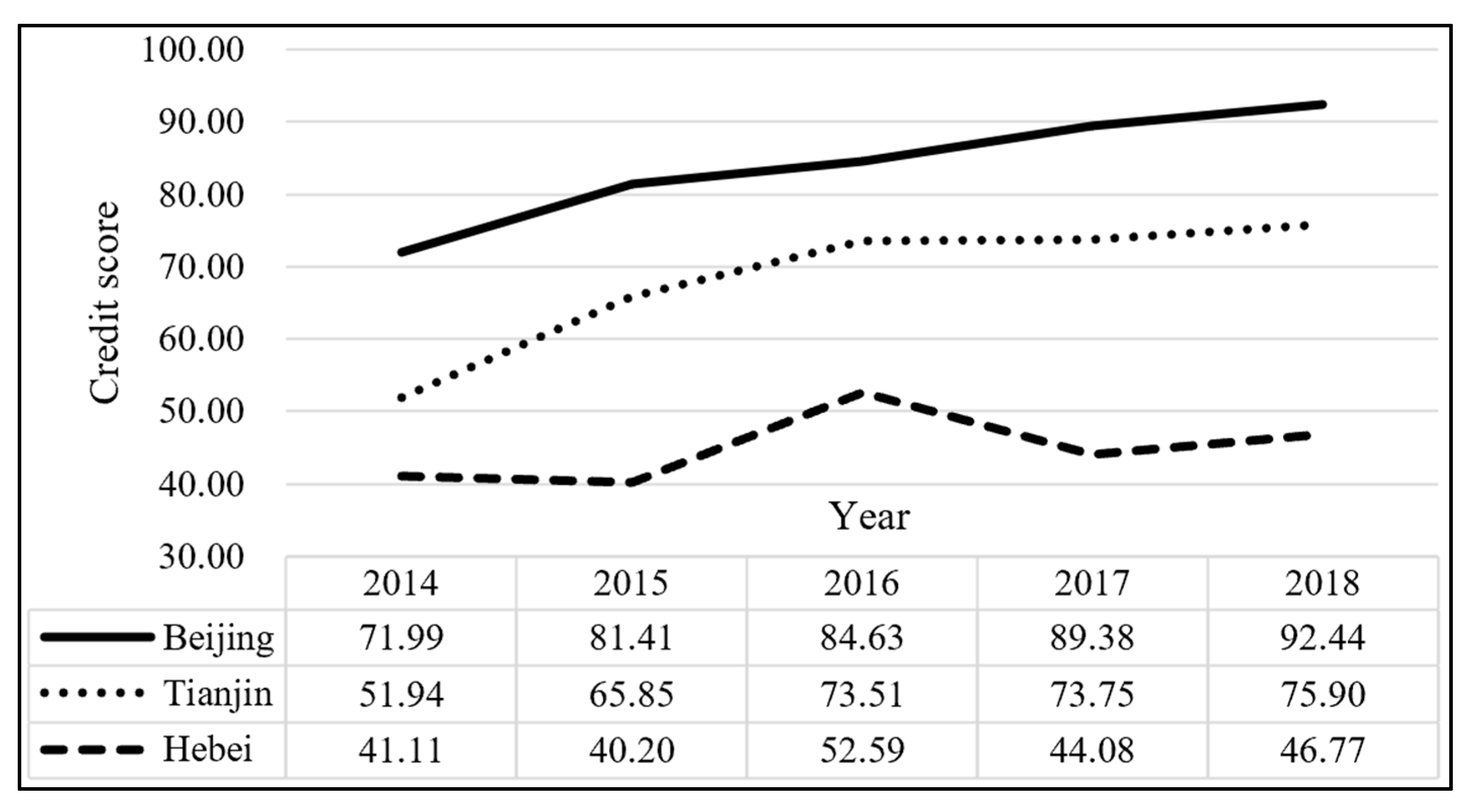

3.2.4. Evaluation Results

4. Empirical Study on External Environment’s Impact on Credit Levels

4.1. Hypotheses Development

4.2. Empirical Test

4.2.1. Data Collection

4.2.2. Data Analysis and Results

- PCA

- Regression model

5. Discussion

5.1. Summary

5.2. Theoretical Contribution

5.3. Practical Implications

5.4. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Number | Company Name | Location | Stock Code |

|---|---|---|---|

| 1 | Beijing Zhongkehaixun Digital S&T Co., Ltd. | Beijing | 300810 |

| 2 | Beijing Compass Technology Development Co., Ltd. | Beijing | 300803 |

| 3 | Beijing Zuojiang Technology Co., Ltd. | Beijing | 300799 |

| 4 | NCS TESTING TECHNOLOGY Co., Ltd. | Beijing | 300797 |

| 5 | Citic Press Corporation | Beijing | 300788 |

| 6 | Beijing Zhidemai Technology Co., Ltd. | Beijing | 300785 |

| 7 | Lakala Payment Co., Ltd. | Beijing | 300773 |

| 8 | CSPC Innovation Pharmaceutical Co., Ltd. | Hebei | 300765 |

| 9 | Pharmaron Beijing Co., Ltd. | Beijing | 300759 |

| 10 | BYBON Group Company Limited | Beijing | 300736 |

| 11 | Beijing Andawell Science& Technology Co., Ltd | Beijing | 300719 |

| 12 | Dark Horse Technology Group Co., Ltd. | Beijing | 300688 |

| 13 | JONES TECH PLC | Beijing | 300684 |

| 14 | Yusys Technologies Co., Ltd. | Beijing | 300674 |

| 15 | Beijing Beetech Inc. | Beijing | 300667 |

| 16 | Client Service International, Inc. | Beijing | 300663 |

| 17 | Beijing Career International Co., Ltd. | Beijing | 300662 |

| 18 | SG MICRO CORP | Beijing | 300661 |

| 19 | Shunya International Martech (Beijing) Co., Ltd. | Beijing | 300612 |

| 20 | Si-Tech Information Technology Co., Ltd. | Beijing | 300608 |

| 21 | Rianlon Corporation | Tianjin | 300596 |

| 22 | Suplet Power Co., Ltd. | Beijing | 300593 |

| 23 | BeiJing Certificate Authority Co., Ltd. | Beijing | 300579 |

| 24 | BEIJING WANJI TECHNOLOGY Co., Ltd. | Beijing | 300552 |

| 25 | Brilliance Technology Co., Ltd. | Beijing | 300542 |

| 26 | Beijing Advanced Digital Technology Co., Ltd. | Beijing | 300541 |

| 27 | Beijing Global Safety Technology Co., Ltd. | Beijing | 300523 |

| 28 | Beijing E-techstar Co., Ltd | Beijing | 300513 |

| 29 | Thunder Software Technology Co., Ltd. | Beijing | 300496 |

| 30 | Shijiazhuang Tonhe Electronics Technologies Co., Ltd. | Hebei | 300491 |

| 31 | Beijing Science Sun Pharmaceutical Co., Ltd. | Beijing | 300485 |

| 32 | Beijing Hezong Science&Technology Co., Ltd. | Beijing | 300477 |

| 33 | Global Infotech Co., Ltd. | Beijing | 300465 |

| 34 | NAVTECH INC. | Beijing | 300456 |

| 35 | Beijing Ctrowell Technology Corporation Limited | Beijing | 300455 |

| 36 | Beijing Hanbang Technology Corp. | Beijing | 300449 |

| 37 | Baoding Lucky Innovative Materials Co., Ltd. | Hebei | 300446 |

| 38 | Beijing ConST Instruments Technology Inc. | Beijing | 300445 |

| 39 | Beijing SOJO Electric Co., Ltd. | Beijing | 300444 |

| 40 | Baofeng Group Co., Ltd. | Beijing | 300431 |

| 41 | Beijing Chieftain Control Engineering Technology Co., Ltd. | Beijing | 300430 |

| 42 | Hebei Sitong New Metal Material Co., Ltd. | Hebei | 300428 |

| 43 | BEIJING INTERACT TECHNOLOGY Co., Ltd. | Beijing | 300419 |

| 44 | Beijing Kunlun Tech Co., Ltd. | Beijing | 300418 |

| 45 | Tianjin Keyvia Electric Co., Ltd | Tianjin | 300407 |

| 46 | Beijing Strong Biotechnologies, Inc | Beijing | 300406 |

| 47 | Beijing Tianli Mobile Service Integration, INC. | Beijing | 300399 |

| 48 | Beijing Tensyn Digital Marketing Technology Joint Stock Company | Beijing | 300392 |

| 49 | Feitian Technologies Co., Ltd. | Beijing | 300386 |

| 50 | Beijing Sanlian Hope Shin-Gosen Technical Service Co., Ltd. | Beijing | 300384 |

| 51 | Beijing Sinnet Technology Co., Ltd. | Beijing | 300383 |

| 52 | BEIJING TONGTECH Co., Ltd. | Beijing | 300379 |

| 53 | TIANJIN PENGLING GROUP CO., LTD | Tianjin | 300375 |

| 54 | Beijing Hengtong Innovation Luxwood Technology Co., Ltd. | Beijing | 300374 |

| 55 | Huizhong Instrumentation Co., Ltd. | Hebei | 300371 |

| 56 | Beijing Etrol Technologies Co., Ltd. | Beijing | 300370 |

| 57 | Nsfocus Information Technology Co., Ltd. | Beijing | 300369 |

| 58 | Hebei Huijin Electromechanical Co., Ltd. | Hebei | 300368 |

| 59 | NetPosa Technologies, Ltd. | Beijing | 300367 |

| 60 | BEIJING FOREVER TECHNOLOGY CO., LTD | Beijing | 300365 |

| 61 | COL Digital Publishing Group Co., Ltd. | Beijing | 300364 |

| 62 | Kyland Technology Co., Ltd. | Beijing | 300353 |

| 63 | Beijing VRV Software Corporation Limited. | Beijing | 300352 |

| 64 | Taikong Intelligent Construction Co., Ltd. | Beijing | 300344 |

| 65 | TIANJIN MOTIMO MEMBRANE TECHNOLOGY Co., Ltd. | Tianjin | 300334 |

| 66 | Top Resource Conservation & Environment Corp. | Beijing | 300332 |

| 67 | Beijing Watertek Information Technology Co., Ltd. | Beijing | 300324 |

| 68 | Beijing Bohui Innovation Biotechnology Co., Ltd. | Beijing | 300318 |

| 69 | OURPALM Co., Ltd. | Beijing | 300315 |

| 70 | Boomsense Technology Co., Ltd. | Beijing | 300312 |

| 71 | GI Technologies Group Co., Ltd. | Beijing | 300309 |

| 72 | TOYOU FEIJI ELECTRONICS Co., Ltd. | Beijing | 300302 |

| 73 | Leyard Optoelectronic Co., Ltd. | Beijing | 300296 |

| 74 | Beijing HualuBaina Film&Tv Co., Ltd. | Beijing | 300291 |

| 75 | BEIJING LEADMAN BIOCHEMISTRY Co., Ltd. | Beijing | 300289 |

| 76 | Beijing Philisense Technology Co., Ltd. | Beijing | 300287 |

| 77 | Sansheng Intellectual Education Technology CO., LTD | Beijing | 300282 |

| 78 | BEIJING THUNISOFT CORPORATION LIMITED | Beijing | 300271 |

| 79 | Hebei Changshan Biochemical Pharmaceutical Co., Ltd. | Hebei | 300255 |

| 80 | Beijing Enlight Media Co., Ltd. | Beijing | 300251 |

| 81 | Beijing Trust&Far Technology CO., LTD | Beijing | 300231 |

| 82 | TRS Information Technology Co., Ltd. | Beijing | 300229 |

| 83 | Ingenic Semiconductor Co., Ltd. | Beijing | 300223 |

| 84 | Beijing Jiaxun Feihong Electrical Co., Ltd | Beijing | 300213 |

| 85 | BEIJING E-HUALU INFORMATION TECHNOLOGY CO., LTD | Beijing | 300212 |

| 86 | Staidson (Beijing) Biopharmaceuticals Co., Ltd. | Beijing | 300204 |

| 87 | Beijing Comens New Materials Co., Ltd. | Beijing | 300200 |

| 88 | MASTERWORK GROUP Co., Ltd. | Tianjin | 300195 |

| 89 | SINO GEOPHYSICAL CO., LTD | Beijing | 300191 |

| 90 | Beijing Jetsen Technology Co., Ltd. | Beijing | 300182 |

| 91 | Business-intelligence of Oriental Nations Corporation Ltd. | Beijing | 300166 |

| 92 | LandOcean Energy Services Co., Ltd. | Beijing | 300157 |

| 93 | Shenwu Environmental Technology CO., LTD | Beijing | 300156 |

| 94 | Xiongan Kerong Environment Technology Co., Ltd. | Hebei | 300152 |

| 95 | Beijing Century Real Technology Co., Ltd. | Beijing | 300150 |

| 96 | Beijing XIAOCHENG Technology Stock Co., Ltd. | Beijing | 300139 |

| 97 | CHENGUANG BIOTECH GROUP Co., Ltd. | Hebei | 300138 |

| 98 | Hebei Sailhero Environmental Protection High-tech Co., ltd. | Hebei | 300137 |

| 99 | Tianjin Jingwei Huikai Optoelectronic Co., Ltd. | Tianjin | 300120 |

| 100 | Tianjin Ringpu Bio-Technology Co., Ltd. | Tianjin | 300119 |

| 101 | Beijing JIAYU Door, Window and Curtain Wall Joint-Stock Co., Ltd. | Beijing | 300117 |

| 102 | Hebei Jianxin Chemical Co., Ltd. | Hebei | 300107 |

| 103 | LESHI INTERNET INFORMATION & TECHNOLOGY CORP., BEIJING | Beijing | 300104 |

| 104 | HENGXIN SHAMBALA CULTURE Co., Ltd. | Beijing | 300081 |

| 105 | Sumavision Technologies Co., Ltd | Beijing | 300079 |

| 106 | Beijing eGOVA Co., Ltd. | Beijing | 300075 |

| 107 | Beijing Easpring Material Technology Co., Ltd. | Beijing | 300073 |

| 108 | Beijing Sanju Environmental Protection & New Materials Co., Ltd. | Beijing | 300072 |

| 109 | Spearhead Integrated Marketing Communication Group | Beijing | 300071 |

| 110 | BEIJING ORIGINWATER TECHNOLOGY Co., Ltd. | Beijing | 300070 |

| 111 | Beijing Highlander Digital Technology Co., Ltd. | Beijing | 300065 |

| 112 | BlueFocus Intelligent Communications Group Co., Ltd. | Beijing | 300058 |

| 113 | Beijing Water Business Doctor Co., Ltd. | Beijing | 300055 |

| 114 | Hiconics Eco-energy Technology Co., Ltd. | Beijing | 300048 |

| 115 | Hwa Create Co., Ltd. | Beijing | 300045 |

| 116 | Beijing Shuzhi Technology Co., Ltd | Beijing | 300038 |

| 117 | Beijing SuperMap Software Co., Ltd. | Beijing | 300036 |

| 118 | Gaona Aero Material Co., Ltd. | Beijing | 300034 |

| 119 | Tianjin Chase Sun Pharmaceutical Co., Ltd. | Tianjin | 300026 |

| 120 | Beijing Beilu Pharmaceutical Co., Ltd | Beijing | 300016 |

| 121 | Beijing Dinghan Technology Group Co., Ltd. | Beijing | 300011 |

| 122 | BEIJING LANXUM TECHNOLOGY Co., Ltd. | Beijing | 300010 |

| 123 | Toread Holdings Group Co., Ltd. | Beijing | 300005 |

| 124 | Lepu Medical Technology (Beijing) Co., Ltd. | Beijing | 300003 |

| 125 | Beijing Ultrapower Software Co., Ltd. | Beijing | 300002 |

Appendix B

| Y | d1 | d2 | d3 | d4 | d5 | d6 | d7 | d8 | d9 | d10 | d11 | d12 | d13 | d14 | d15 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Y | 1 | 0.511 ** | −0.358 | 0.409 ** | 0.750 ** | 0.344 ** | 0.297 | 0.145 * | −0.442 ** | −0.289 ** | 0.021 | 0.500 ** | 0.442 ** | 0.830 ** | 0.717 ** | 0.238 ** |

| d1 | 0.511 ** | 1 | 0.350 ** | −0.650 ** | 0.262 ** | 0.368 | −0.015 | 0.317 | −0.507 ** | −0.959 ** | 0.263 | 0.712 ** | 0.242 ** | 0.252 ** | 0.181 ** | 0.612 ** |

| d2 | −0.358 | 0.350 ** | 1 | −0.342 | 0.900 ** | 0.675 ** | 0.276 | 0.681 ** | −0.119 ** | −0.406 ** | 0.071 | 0.879 ** | 0.549 ** | 0.302 ** | 0.862 ** | 0.495 ** |

| d3 | 0.409 ** | −0.650 ** | −0.342 | 1 | −0.191 | 0.438 | 0.153 ** | 0.354 | 0.641 ** | 0.690 ** | −0.504 | −0.485 | 0.123 | 0.057 | −0.145 | −0.545 * |

| d4 | 0.750 ** | 0.262 ** | 0.900 ** | −0.191 | 1 | 0.375 ** | 0.453 | 0.539 * | −0.782 ** | −0.804 ** | −0.033 | 0.479 ** | 0.117 ** | 0.500 ** | 0.930 ** | 0.609 ** |

| d5 | 0.344 ** | 0.368 | 0.675 ** | 0.438 | 0.375 ** | 1 | 0.274 ** | 0.874 ** | −0.366 | −0.341 | −0.334 | 0.553 * | 0.937 ** | 0.104 ** | 0.305 ** | 0.431 |

| d6 | 0.297 | −0.015 | 0.276 | 0.0153 ** | 0.453 | 0.274 ** | 1 | 0.734 ** | 0.069 | 0.093 | −0.399 | 0.133 | 0.109 ** | 0.436 * | 0.479 | 0.088 |

| d7 | 0.145 * | 0.317 | 0.681 ** | 0.354 | 0.539 * | 0.874 ** | 0.734 ** | 1 | −0.426 | −0.349 | −0.201 | 0.560 * | 0.239 ** | 0.857 ** | 0.764 ** | 0.491 |

| d8 | −0.442 ** | −0.507 ** | −0.119 ** | 0.0641 ** | −0.782 ** | −0.366 | 0.069 | −0.426 | 1 | 0.967 ** | −0.253 | −0.256 ** | −0.622 * | −0.406 ** | -0.081 | −0.724 ** |

| d9 | −0.289 ** | −0.959 ** | −0.406 ** | 0.0690 ** | −0.804 ** | −0.341 | 0.093 | −0.349 | 0.967 ** | 1 | −0.254 ** | −0.955 ** | −0.114 * | −0.006 | −0.083 | −0.920 ** |

| d10 | 0.021 | 0.263 | 0.071 | −0.504 | −0.033 | −0.334 | −0.399 | −0.201 | −0.253 | −0.254 ** | 1 | 0.207 | −0.177 | −0.142 | 0.002 | 0.364 |

| d11 | 0.500 ** | 0.712 ** | 0.879 ** | −0.485 | 0.479 ** | 0.553 * | 0.133 | 0.560 * | −0.256 ** | −0.955 ** | 0.207 | 1 | 0.165 ** | 0.714 ** | 0.309 ** | 0.931 ** |

| d12 | 0.442 ** | 0.242 ** | 0.549 ** | 0.123 | 0.117 ** | 0.937 ** | 0.109 ** | 0.239 ** | −0.622 * | −0.114 * | −0.177 | 0.165 ** | 1 | 0.972 ** | 0.635 ** | 0.056 |

| d13 | 0.830 ** | 0.252 ** | 0.302 ** | 0.057 | 0.500 ** | 0.104 ** | 0.436 * | 0.857 ** | −0.406 ** | −0.006 | −0.142 | 0.714 ** | 0.972 ** | 1 | 0.958 ** | 0.334 ** |

| d14 | 0.717 ** | 0.181 ** | 0.862 ** | −0.145 | 0.930 ** | 0.305 ** | 0.479 | 0.764 ** | −0.081 | −0.083 | 0.002 | 0.309 ** | 0.635 ** | 0.958 ** | 1 | 0.434 ** |

| d15 | 0.238 ** | 0.612 ** | 0.495 ** | −0.545 * | 0.609 ** | 0.431 | 0.088 | 0.491 | −0.724 ** | −0.0920 ** | 0.364 | 0.931 ** | 0.056 | 0.334** | 0.434 ** | 1 |

Appendix C

| PCs | Initial Eigenvalues | Sum of the Squares of Extracted Loads | Sum of the Squares of Rotated Loads | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Total | Var% | Sum% | Total | Var% | Sum% | Total | Var% | Sum% | |

| F1 | 9.837 | 65.577 | 65.577 | 9.837 | 65.577 | 65.577 | 9.023 | 60.150 | 60.150 |

| F2 | 3.847 | 25.646 | 91.223 | 3.847 | 25.646 | 91.223 | 4.661 | 31.073 | 91.223 |

| F3 | 0.727 | 4.850 | 96.073 | ||||||

| F4 | 0.319 | 2.126 | 98.199 | ||||||

| F5 | 0.099 | 0.661 | 98.859 | ||||||

| F6 | 0.066 | 0.440 | 99.299 | ||||||

| F7 | 0.040 | 0.266 | 99.565 | ||||||

| F8 | 0.032 | 0.213 | 99.778 | ||||||

| F9 | 0.019 | 0.125 | 99.903 | ||||||

| F10 | 0.010 | 0.066 | 99.969 | ||||||

| F11 | 0.002 | 0.016 | 99.985 | ||||||

| F12 | 0.001 | 0.009 | 99.994 | ||||||

| F13 | 0.001 | 0.005 | 99.999 | ||||||

| F14 | 0.000 | 0.001 | 100.000 | ||||||

| F15 | 0.000 | 0.000 | 100.000 | ||||||

| Variables | Elements | |

|---|---|---|

| PC1 | PC2 | |

| GDP per capita (d1) | 0.122 | −0.070 |

| Total import and export volume (d2) | 0.101 | 0.017 |

| Total retail sales of social consumer goods (d3) | −0.116 | 0.220 |

| Average monetary wage (d4) | 0.083 | 0.053 |

| Balance of loans of financial institutions (d5) | 0.007 | 0.187 |

| General budget expenditure of local finance (d6) | −0.048 | 0.227 |

| Scale of social financing (d7) | 0.015 | 0.161 |

| Urban road area at the end of the year (d8) | −0.124 | 0.069 |

| Turnover of goods (d9) | −0.127 | 0.080 |

| Internet penetration rate (d10) | 0.066 | −0.150 |

| Average number of students in colleges of per 100,000 residents (d11) | 0.114 | −0.025 |

| Number of patents licensing (d12) | 0.049 | 0.128 |

| Turnover of technology market (d13) | 0.058 | 0.112 |

| Internal expenditure of R&D funds (d14) | 0.082 | 0.065 |

| Main business income of high-tech enterprises (d15) | 0.118 | −0.050 |

Appendix D

References

- Neville, C.; Lucey, B.M. Financing Irish High-Tech SMEs: The Analysis of Capital Structure. Int. Rev. Financ. Anal. 2022, 83, 102219. [Google Scholar] [CrossRef]

- Nunes, P.M.; Serrasqueiro, Z.; Leitão, J. Is There a Linear Relationship between R&D Intensity and Growth? Empirical Evidence of Non-High-Tech vs. High-Tech SMEs. Res. Policy 2012, 41, 36–53. [Google Scholar] [CrossRef]

- Siegel, D.S.; Westhead, P.; Wright, M. Science Parks and the Performance of New Technology-Based Firms: A Review of Recent U.K. Evidence and an Agenda for Future Research. Small Bus. Econ. 2003, 20, 177–184. [Google Scholar] [CrossRef]

- Balkin, D.B.; Markman, G.D.; Gomez-Mejia, L.R. Is Ceo Pay in High-Technology Firms Related to Innovation? Acad. Manag. J. 2000, 43, 1118–1129. [Google Scholar] [CrossRef]

- Ogubazghi, S.K.; Muturi, W. The Effect of Age and Educational Level of Owner/Managers on SMMEs’ Access to Bank Loan in Eritrea: Evidence from Asmara City. Am. J. Ind. Bus. Manag. 2014, 4, 632–643. [Google Scholar] [CrossRef] [Green Version]

- Terziovski, M. Innovation Practice and Its Performance Implications in Small and Medium Enterprises (SMEs) in the Manufacturing Sector: A Resource-Based View. Strateg. Manag. J. 2010, 31, 892–902. [Google Scholar] [CrossRef]

- Partanen, J.; Möller, K.; Westerlund, M.; Rajala, R.; Rajala, A. Social Capital in the Growth of Science-and-Technology-Based SMEs. Ind. Mark. Manag. 2008, 37, 513–522. [Google Scholar] [CrossRef]

- Moro, A.; Fink, M. Loan Managers’ Trust and Credit Access for SMEs. J. Bank. Financ. 2013, 37, 927–936. [Google Scholar] [CrossRef]

- Chen, Y.; Huang, R.J.; Tsai, J.; Tzeng, L.Y. Soft Information and Small Business Lending. J. Financ. Serv. Res. 2015, 47, 115–133. [Google Scholar] [CrossRef]

- D’Aurizio, L.; Oliviero, T.; Romano, L. Family Firms, Soft Information and Bank Lending in a Financial Crisis. J. Corp. Financ. 2015, 33, 279–292. [Google Scholar] [CrossRef] [Green Version]

- Tsolas, I.E. Firm Credit Risk Evaluation: A Series Two-Stage DEA Modeling Framework. Ann. Oper. Res. 2015, 233, 483–500. [Google Scholar] [CrossRef]

- Calabrese, R.; Marra, G.; Osmetti, S.A. Bankruptcy Prediction of Small and Medium Enterprises Using a Flexible Binary Generalized Extreme Value Model. J. Oper. Res. Soc. 2016, 67, 604–615. [Google Scholar] [CrossRef] [Green Version]

- Chen, D. Initial Analysis on Index Selection of Science and Technology SME Financing Credit Evaluation. Sci. Technol. Manag. Res. 2017, 37, 64–68. [Google Scholar] [CrossRef]

- Chen, Y. Construction and Application of the Technology-Based SMEs Credit Risk Assessment Index System. In 2018 International Conference on Economy, Management and Entrepreneurship (ICOEME 2018); Atlantis Press: Boao, China, 2018. [Google Scholar]

- Tong, Q.; Zhang, D.; Yu, J. Construction of credit evaluation indicator system for technology-based SMEs. Econ. Res. Guide 2017, 13, 19–20. [Google Scholar]

- Du, J. Research on the Construction of Credit Rating System for Technological SMEs Based on Big Data—Take Zhangjiang Enterprise Credit System as an Example. Econ. Res. Guide 2022, 18, 13–15. [Google Scholar]

- Nahapiet, J.; Ghoshal, S. Social Capital, Intellectual Capital, and the Organizational Advantage. Acad. Manag. Rev. 1998, 23, 242–266. [Google Scholar] [CrossRef]

- Guiso, L.; Sapienza, P.; Zingales, L. The Role of Social Capital in Financial Development. Am. Econ. Rev. 2004, 94, 526–556. [Google Scholar] [CrossRef] [Green Version]

- Paal, B.; Wiseman, T. Group Insurance and Lending with Endogenous Social Collateral. J. Dev. Econ. 2011, 94, 30–40. [Google Scholar] [CrossRef]

- Gao, G.; Wang, H.; Gao, P. Establishing a Credit Risk Evaluation System for SMEs Using the Soft Voting Fusion Model. Risks 2021, 9, 202. [Google Scholar] [CrossRef]

- Xie, R.; Liu, R.; Liu, X.-B.; Zhu, J.-M. Evaluation of SMEs’ Credit Decision Based on Support Vector Machine-Logistics Regression. J. Math. 2021, 2021, e5541436. [Google Scholar] [CrossRef]

- Wang, W. A SME Credit Evaluation System Based on Blockchain. In Proceedings of the 2020 International Conference on E-Commerce and Internet Technology (ECIT), Zhangjiajie, China, 24–26 April 2020; pp. 248–251. [Google Scholar]

- Bao, S.; Yin, Y. Credit evaluation and empirical analysis of small and medium-sized technology-based enterprises. Sci. Technol. Prog. Policy 2009, 26, 143–148. [Google Scholar]

- Huo, H. Credit risk index system and evaluation method of high-tech small and medium-sized enterprises. J. Beijing Univ. Technol. Soc. Sci. Ed. 2012, 14, 60–65. [Google Scholar] [CrossRef]

- Voulgaris, F.; Zopounidis, D.C. On the Evaluation of Greek Industrial SME’s Performance via Multicriteria Analysis of Financial Ratios. Small Bus. Econ. 2000, 15, 127–136. [Google Scholar] [CrossRef]

- Ma, Y.; Ansell, J.; Andreeva, G. Exploring Management Capability in SMEs Using Transactional Data. J. Oper. Res. Soc. 2016, 67, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Piskorski, T.; Seru, A.; Witkin, J. Asset Quality Misrepresentation by Financial Intermediaries: Evidence from the RMBS Market: Asset Quality Misrepresentation by Financial Intermediaries. J. Financ. 2015, 70, 2635–2678. [Google Scholar] [CrossRef]

- Grunert, J.; Norden, L. Bargaining Power and Information in SME Lending. Small Bus. Econ. 2012, 39, 401–417. [Google Scholar] [CrossRef] [Green Version]

- Lugovskaya, L. Predicting Default of Russian SMEs on the Basis of Financial and Non-Financial Variables. J. Financ. Serv. Mark. 2010, 14, 301–313. [Google Scholar] [CrossRef]

- Angilella, S.; Mazzù, S. The Financing of Innovative SMEs: A Multicriteria Credit Rating Model. Eur. J. Oper. Res. 2015, 244, 540–554. [Google Scholar] [CrossRef] [Green Version]

- Psillaki, M.; Tsolas, I.E.; Margaritis, D. Evaluation of Credit Risk Based on Firm Performance. Eur. J. Oper. Res. 2010, 201, 873–881. [Google Scholar] [CrossRef]

- Tsai, M.F.; Wang, C.J. On the Risk Prediction and Analysis of Soft Information in Finance Reports. Eur. J. Oper. Res. 2017, 257, 243–250. [Google Scholar] [CrossRef]

- Tobback, E.; Bellotti, T.; Moeyersoms, J.; Stankova, M.; Martens, D. Bankruptcy Prediction for SMEs Using Relational Data. Decis. Support Syst. 2017, 102, 69–81. [Google Scholar] [CrossRef] [Green Version]

- Zhu, Y.; Xie, C.; Wang, G.-J.; Yan, X.-G. Comparison of Individual, Ensemble and Integrated Ensemble Machine Learning Methods to Predict China’s SME Credit Risk in Supply Chain Finance. Neural Comput. Appl. 2017, 28, 41–50. [Google Scholar] [CrossRef]

- Chen, X.; Wang, X.; Wu, D.D. Credit Risk Measurement and Early Warning of SMEs: An Empirical Study of Listed SMEs in China. Decis. Support Syst. 2010, 49, 301–310. [Google Scholar] [CrossRef]

- Dietrich, A. Explaining Loan Rate Differentials between Small and Large Companies: Evidence from Switzerland. Small Bus. Econ. 2012, 38, 481–494. [Google Scholar] [CrossRef]

- Altman, E.I. Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy. J. Financ. 1968, 23, 589–609. [Google Scholar] [CrossRef]

- Zhang, M.; He, Y.; Zhou, Z. Study on the Influence Factors of High-Tech Enterprise Credit Risk: Empirical Evidence from China’s Listed Companies. Procedia Comput. Sci. 2013, 17, 901–910. [Google Scholar] [CrossRef] [Green Version]

- Bao, M.X.; Billett, M.T.; Smith, D.B.; Unlu, E. Does Other Comprehensive Income Volatility Influence Credit Risk and the Cost of Debt? Contemp. Account. Res. 2020, 37, 457–484. [Google Scholar] [CrossRef]

- Cao, Z.; Chen, S.X.; Lee, E. Does Business Strategy Influence Interfirm Financing? Evidence from Trade Credit. J. Bus. Res. 2022, 141, 495–511. [Google Scholar] [CrossRef]

- Liu, J.; Zeng, J.F. Multi-Stage Game of Government Supervision and Green Manufacture. Syst. Eng. 2014, 32, 12–17. [Google Scholar]

- Chi, Q.; Li, W. Economic Policy Uncertainty, Credit Risks and Banks’ Lending Decisions: Evidence from Chinese Commercial Banks. China J. Account. Res. 2017, 10, 33–50. [Google Scholar] [CrossRef]

- Li, W.; Xu, X.; Long, Z. Confucian Culture and Trade Credit: Evidence from Chinese Listed Companies. Res. Int. Bus. Financ. 2020, 53, 101232. [Google Scholar] [CrossRef]

- Zhao, X.; Chen, H. Research on Influencing Factors and Transmission Mechanisms of Green Credit Risk. Environ. Sci. Pollut. Res. 2022, 29, 89168–89183. [Google Scholar] [CrossRef] [PubMed]

- Yang, Y.; Chu, X.; Pang, R.; Liu, F.; Yang, P. Identifying and Predicting the Credit Risk of Small and Medium-Sized Enterprises in Sustainable Supply Chain Finance: Evidence from China. Sustainability 2021, 13, 5714. [Google Scholar] [CrossRef]

- Yu, X.; Fang, J. Tax Credit Rating and Corporate Innovation Decisions. China J. Account. Res. 2022, 15, 73–93. [Google Scholar] [CrossRef]

- Huang, X.; Liu, X.; Ren, Y. Enterprise Credit Risk Evaluation Based on Neural Network Algorithm. Cogn. Syst. Res. 2018, 52, 317–324. [Google Scholar] [CrossRef]

- Li, G. Research on the Mechanism of Internet Public Opinion Risk Evolution and Management for Chinese State-Owned Enterprise. In Proceedings of the 2013 5th International Conference on Intelligent Human-Machine Systems and Cybernetics, Hangzhou, China, 26–27 August 2013; pp. 368–373. [Google Scholar]

- Kleinknecht, A.; Van Montfort, K.; Brouwer, E. The Non-Trivial Choice between Innovation Indicators. Econ. Innov. New Technol. 2002, 11, 109–121. [Google Scholar] [CrossRef]

- Pavitt, K. Patent Statistics as Indicators of Innovative Activities: Possibilities and Problems. Scientometrics 2005, 7, 77–99. [Google Scholar] [CrossRef]

- Zahra, S.A. Harvesting Family Firms’ Organizational Social Capital: A Relational Perspective. J. Manag. Stud. 2010, 47, 345–366. [Google Scholar] [CrossRef]

- The Coordinated Development of the Beijing-Tianjin-Hebei Region is Fundamentally Driven by Innovation. Available online: http://www.gov.cn/zhengce/2015-09/16/content_2932641.htm (accessed on 4 September 2022).

- China’s Regional Innovation Capacity Monitoring Report 2016-2017 and China’s Regional Science and Technology Innovation Evaluation Report 2016–2017 Were Officially Released. Available online: https://www.most.gov.cn/kjbgz/201709/t20170901_134714.html (accessed on 4 September 2022).

- China’s Regional Science and Technology Innovation Evaluation Report 2018 Was Released. Available online: http://www.ce.cn/culture/gd/201810/30/t20181030_30657850.shtml (accessed on 4 September 2022).

- Coordinated Development of the Beijing-Tianjin-Hebei Region. Available online: https://www.ndrc.gov.cn/gjzl/jjjxtfz/201911/t20191127_1213171.html (accessed on 4 September 2022).

- Jinping Xi Visited and Presided over a Forum on the Coordinated Development of the Beijing-Tianjin-Hebei Region. Available online: http://www.cppcc.gov.cn/zxww/2019/01/21/ARTI1548029666876103.shtml (accessed on 4 September 2022).

- He, P.; Shen, Y.; Li, G. Research on Credit Risk of Science and Technology SMEs in Beijing-Tianjin-Hebei Region. Rev. Econ. Res. 2022, 119–133. [Google Scholar] [CrossRef]

- Statistical Classification of Large, Small and Micro Enterprises. Available online: https://view.officeapps.live.com/op/view.aspx?src=http%3A%2F%2Fwww.stats.gov.cn%2Ftjgz%2Ftzgb%2F201801%2FP020180103343283760282.docx&wdOrigin=BROWSELINK (accessed on 7 September 2022).

- Fan, J.; Zhong, D.; Zhang, Y.; Yu, S.; Chu, J.; Yu, M.; Zhao, H.; Huang, Y. A Hybrid Approach Based on Rough-AHP for Evaluation in-Flight Service Quality. Multimed. Tools Appl. 2022, 81, 30797–30819. [Google Scholar] [CrossRef]

- Liu, R.X.; Kuang, J.; Gong, Q.; Hou, X.L. Principal Component Regression Analysis with Spss. Comput. Methods Programs Biomed. 2003, 71, 141–147. [Google Scholar] [CrossRef] [PubMed]

- Miškić, S.; Stević, Ž.; Marinković, D. Evaluating the Efficiency of a Transport Company Applying an Objective-Subjective Model. Int. J. Manag. Sci. Eng. Manag. 2022, 1–15. [Google Scholar] [CrossRef]

- Diakoulaki, D.; Mavrotas, G.; Papayannakis, L. Determining Objective Weights in Multiple Criteria Problems: The Critic Method. Oper. Res. 1995, 22, 763–770. [Google Scholar] [CrossRef]

- Zoraghi, N.; Amiri, M.; Talebi, G.; Zowghi, M. A Fuzzy MCDM Model with Objective and Subjective Weights for Evaluating Service Quality in Hotel Industries. J. Ind. Eng. Int. 2013, 9, 38. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Z. Construction of Mathematical Modeling for Teaching Evaluation Index System Based on the Delphi AHP Method. Sci. Program. 2022, 2022, e7744067. [Google Scholar] [CrossRef]

- Development Plan for High-Tech SMEs in Hebei Province (2016–2020). Available online: https://kjt.hebei.gov.cn/www/xxgk2020/228104/228107/229136/index.html (accessed on 3 December 2022).

- Maksimovic, V.; Demirgüç-Kunt, A. Firms as Financial Intermediaries: Evidence from Trade Credit Data; Available SSRN 632764; World Bank Group: Washington, DC, USA, 2001. [Google Scholar]

- Tan, Y.Z.; Wang, C.; Guo-Feng, L.I. Economic Performance and Influencing Factors of the Credit Environment—Empirical Study Based on CEI and Chinese Provincial and Prefecture-Level City Data. Econ. Surv. 2014, 31, 144–149. [Google Scholar] [CrossRef]

- Aivazian, V.A.; Santor, E. Financial Constraints and Investment: Assessing the Impact of a World Bank Credit Program on Small and Medium Enterprises in Sri Lanka. Can. J. Econ. Can. Déconomique 2008, 41, 475–500. [Google Scholar] [CrossRef]

- Zhao, B.; Lyu, X.; Qi, N. Construction and Optimization of Transboundary Business Financial Credit Network in the Era of 5G Communication. Wirel. Commun. Mob. Comput. 2022, 2022, 1–14. [Google Scholar] [CrossRef]

- Moro, A.; Fink, M.; Maresch, D. Reduction in Information Asymmetry and Credit Access for Small and Medium-Sized Enterprises. J. Financ. Res. 2015, 38, 121–143. [Google Scholar] [CrossRef]

- Kusi, B.A.; Agbloyor, E.K.; Ansah-Adu, K.; Gyeke-Dako, A. Bank Credit Risk and Credit Information Sharing in Africa: Does Credit Information Sharing Institutions and Context Matter? Res. Int. Bus. Finance 2017, 42, 1123–1136. [Google Scholar] [CrossRef]

- Aman, J.; Abbas, J.; Shi, G.; Ain, N.U.; Gu, L. Community Wellbeing Under China-Pakistan Economic Corridor: Role of Social, Economic, Cultural, and Educational Factors in Improving Residents’ Quality of Life. Front. Psychol. 2022, 12, 6718. [Google Scholar] [CrossRef] [PubMed]

- Belás, J.; Sopková, G. Significant Determinants of the Competitive Environment for SMEs in the Context of Financial and Credit Risks. J. Int. Stud. 2016, 9, 139–149. [Google Scholar] [CrossRef] [Green Version]

- Griffin, P.A.; Hong, H.A.; Woo, R.J. Corporate Innovative Efficiency: Evidence of Effects on Credit Ratings. J. Corp. Financ. 2018, 6, 352–373. [Google Scholar] [CrossRef]

- Zhu, C.; Zhang, R.; Zhang, X.; Zhu, C. SMEs’ Technological Innovation and Entrepreneur Credit: Based on a Social Capital Perspective. Sci. Technol. Prog. Policy 2010, 10, 65–69. [Google Scholar]

- Piga, C.A.; Atzeni, G. R&d Investment, Credit Rationing and Sample Selection. Bull. Econ. Res. 2007, 59, 149–178. [Google Scholar] [CrossRef] [Green Version]

- Zhou, X.; Tang, X.; Zhang, R. Impact of Green Finance on Economic Development and Environmental Quality: A Study Based on Provincial Panel Data from China. Environ. Sci. Pollut. Res. 2020, 27, 19915–19932. [Google Scholar] [CrossRef]

- Awokuse, T.O. Trade Openness and Economic Growth: Is Growth Export-Led or Import-Led? Appl. Econ. 2008, 40, 161–173. [Google Scholar] [CrossRef]

- Fisher, W.H.; Hof, F.X. Conspicuous Consumption, Economic Growth, and Taxation: A Generalization. J. Econ. 1997, 66, 35–42. [Google Scholar] [CrossRef]

- Guariglia, A.; Poncet, S. Could Financial Distortions Be No Impediment to Economic Growth after All? Evidence from China. J. Comp. Econ. 2008, 36, 633–657. [Google Scholar] [CrossRef] [Green Version]

- Chen, H. Development of Financial Intermediation and Economic Growth: The Chinese Experience. China Econ. Rev. 2006, 17, 347–362. [Google Scholar] [CrossRef] [Green Version]

- Donaldson, D. Railroads of the Raj: Estimating the Impact of Transportation Infrastructure. Am. Econ. Rev. 2018, 108, 899–934. [Google Scholar] [CrossRef] [Green Version]

- Kleinrock, L. An Internet Vision: The Invisible Global Infrastructure. Ad. Hoc. Netw. 2003, 1, 3–11. [Google Scholar] [CrossRef] [Green Version]

- Belas, J.; Smrcka, L.; Gavurova, B.; Dvorsky, J. The Impact of Social and Economic Factors in the Credit Risk Management of SME. Technol. Econ. Dev. Econ. 2018, 24, 1215–1230. [Google Scholar] [CrossRef] [Green Version]

- Abraham, B.P.; Moitra, S.D. Innovation Assessment through Patent Analysis. Technovation 2001, 21, 245–252. [Google Scholar] [CrossRef]

- Guellec, D.; Van Pottelsberghe de la Potterie, B. From R&D to Productivity Growth: Do the Institutional Settings and the Source of Funds of R&D Matter? Oxf. Bull. Econ. Stat. 2010, 66, 353–378. [Google Scholar] [CrossRef]

- Senaviratna, N.; Cooray, T. Diagnosing Multicollinearity of Logistic Regression Model. Asian J. Probab. Stat. 2019, 5, 1–9. [Google Scholar] [CrossRef]

- Mansfield, E.R.; Helms, B.P. Detecting Multicollinearity. Am. Stat. 1982, 36, 158–160. [Google Scholar] [CrossRef]

- Tran, H.; Kim, J.; Kim, D.; Choi, M.; Choi, M. Impact of Air Pollution on Cause-Specific Mortality in Korea: Results from Bayesian Model Averaging and Principle Component Regression Approaches. Sci. Total Environ. 2018, 636, 1020–1031. [Google Scholar] [CrossRef]

- Sedghi, S.; Sadeghian, A.; Huang, B. Mixture Semisupervised Probabilistic Principal Component Regression Model with Missing Inputs. Comput. Chem. Eng. 2017, 103, 176–187. [Google Scholar] [CrossRef]

- Jørgensen, F.; Ulhøi, J.P. Enhancing Innovation Capacity in SMEs through Early Network Relationships. Creat. Innov. Manag. 2010, 19, 397–404. [Google Scholar] [CrossRef]

- Shi, Y.; Ge, X.; Yuan, X.; Wang, Q.; Kellett, J.; Li, F.; Ba, K. An Integrated Indicator System and Evaluation Model for Regional Sustainable Development. Sustainability 2019, 11, 2183. [Google Scholar] [CrossRef] [Green Version]

- Fisher, A.; Caffo, B.; Schwartz, B.; Zipunnikov, V. Fast, Exact Bootstrap Principal Component Analysis for p > 1 Million. J. Am. Stat. Assoc. 2016, 111, 846–860. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Wang, D.; Hua, Y.; Zhu, J. Research on personal credit dynamic evaluation index system based on big data technology—From the social capital perspective. Int. Bus. 2020, 115–127. [Google Scholar] [CrossRef]

| References | Key Evaluation Attributes of Indicator System |

|---|---|

| Bao, S.; Yin, Y. (2009) [23] | Debt paying ability, Profitability, Operating ability, Cash flow analysis, Innovation ability, Development ability, Basic enterprise quality, Enterprise development prospects, Historical credit record |

| Huo, H. (2012) [24] | Profitability, Solvency, Operation ability, Development ability, Enterprise scientific and technological value, Enterprise basic quality, Innovation ability, Development potential |

| Chen, D. (2017) [13] | Basic quality, Profitability, Operation ability, Cash flow status, Solvency, Innovation ability, Growth ability |

| Tong, Q.; et al. (2017) [15] | Asset credit, Financial credit, Innovation and development ability, Public credit supervision, Bidding supervision |

| Chen, Y. (2018) [14] | Solvency, Profitability, Operating capability, Growth capability, Technology innovation capability, Enterprise quality, Enterprise credit record, Enterprise development prospects |

| Du, J. (2022) [16] | Enterprise quality, Operators quality, Industry prospects, Financial situation, Innovation ability |

| Dimensions | First-Level Indicators | Second-Level Indicators | Third-Level Indicators | Data Description |

|---|---|---|---|---|

| Financial indicators | Enterprise operation status | Operating capacity | Accounts receivable turnover rate (x1) | Net income from credit sales/average balance of accounts receivable |

| Inventory turnover rate (x2) | Operating cost/average inventory balance | |||

| Turnover rate of current assets (x3) | Net main business income/average total current assets | |||

| Enterprise development potential | Solvency | Current ratio (x4) | Current assets/current liabilities | |

| Quick ratio (x5) | Quick assets/current liabilities | |||

| Asset liability ratio (x6) | Total liabilities/total assets | |||

| Profitability | Return on equity (x7) | Net profit/net assets | ||

| Growth ability | Growth rate of operating revenue (x8) | Increase in operating Revenue/revenue of the previous period | ||

| Net profit growth rate (x9) | Net profit growth/net profit of the previous period | |||

| Capital accumulation rate (x10) | Increase in owner’s equity/amount at the beginning of the year | |||

| Nonfinancial indicators | Enterprise quality | Enterprise credit activity record | Tax credit rating (x11) | Rated by the tax assessment score |

| Number of lawsuits (x12) | Number of judicial cases related to the enterprise | |||

| External evaluation | Risk information (x13) | Self-risk + associated risk + prompt risk information | ||

| Public opinion information (x14) | Positive information/negative information | |||

| Enterprise competitiveness | Innovation ability | Total content of scientific and technological innovation (x15) | Converted from several intellectual property right indicators | |

| R&D investment (x16) | Investment amount in research and development | |||

| Patent implementation rate (x17) | Number of patents authorized/total number of patents | |||

| Social capital | Working years of senior manager (x18) | Average number of working years of the legal person and the chairman | ||

| Educational level of senior manager (x19) | Associate degree or below = 1, bachelor degree = 2, master degree = 3, doctor degree = 4 | |||

| Number of affiliated enterprises of senior manager (x20) | Number of enterprises that is directly or indirectly controlled by the senior manager | |||

| Number of foreign investment enterprises (x21) | Number of enterprises abroad that is invested by the focal enterprise | |||

| Number of suppliers and customers (x22) | Number of suppliers + number of customers |

| Financial Indicators | Elements | |||

|---|---|---|---|---|

| PC1 | PC2 | PC3 | PC4 | |

| Accounts receivable turnover rate (X1) | −0.005 | 0.527 | −0.070 | 0.055 |

| Inventory turnover rate (X2) | 0.009 | 0.535 | −0.014 | −0.014 |

| Turnover rate of current assets (X3) | 0.025 | 0.125 | 0.392 | −0.286 |

| Current ratio (X4) | 0.492 | 0.002 | 0.046 | −0.120 |

| Quick ratio (X5) | 0.495 | 0.013 | 0.049 | −0.128 |

| Asset liability ratio (X6) | −0.052 | −0.007 | 0.118 | −0.503 |

| Return on equity (X7) | −0.166 | 0.022 | 0.062 | 0.604 |

| Growth rate of operating revenue (X8) | 0.064 | −0.060 | 0.506 | −0.028 |

| Net profit growth rate (X9) | −0.033 | −0.003 | 0.158 | 0.146 |

| Capital accumulation rate (X10) | 0.018 | −0.072 | 0.398 | 0.002 |

| Influencing Factors | Specific Variables | References |

|---|---|---|

| Economic environment (D1) | Per capita GDP (d1) | [77,78,79] |

| Total imports and exports (d2) | ||

| Total retail sales of social consumer goods (d3) | ||

| Average monetary wage (d4) | ||

| Financial environment (D2) | Balance of loans of financial institutions (d5) | [80,81] |

| General budget expenditure of local finance (d6) | ||

| Scale of social financing (d7) | ||

| Infrastructural environment (D3) | Urban road area at the end of the year (d8) | [82,83] |

| Turnover of goods (d9) | ||

| Internet penetration rate (d10) | ||

| Cultural environment (D4) | Average number of students in colleges per 100,000 residents (d11) | [73,84] |

| Scientific and technological innovation environment (D5) | Number of patents licensing (d12) | [85,86] |

| Turnover of technology market (d13) | ||

| Internal expenditure of R&D funds (d14) | ||

| Main business income of high-tech enterprises (d15) |

| Variables | Model (10) |

|---|---|

| F1 | 16.426 *** |

| (1.750) | |

| F2 | 4.861 *** |

| (1.750) | |

| Constant | 65.569 *** |

| (1.691) | |

| Observations | 15 |

| R-squared | 0.889 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liang, Z.; Du, J.; Hua, Y.; Si, Y.; Li, M. Research on Credit Evaluation Indicator System of High-Tech SMEs: From the Social Capital Perspective. Systems 2023, 11, 141. https://doi.org/10.3390/systems11030141

Liang Z, Du J, Hua Y, Si Y, Li M. Research on Credit Evaluation Indicator System of High-Tech SMEs: From the Social Capital Perspective. Systems. 2023; 11(3):141. https://doi.org/10.3390/systems11030141

Chicago/Turabian StyleLiang, Zhihao, Jinming Du, Ying Hua, Yanbo Si, and Miao Li. 2023. "Research on Credit Evaluation Indicator System of High-Tech SMEs: From the Social Capital Perspective" Systems 11, no. 3: 141. https://doi.org/10.3390/systems11030141

APA StyleLiang, Z., Du, J., Hua, Y., Si, Y., & Li, M. (2023). Research on Credit Evaluation Indicator System of High-Tech SMEs: From the Social Capital Perspective. Systems, 11(3), 141. https://doi.org/10.3390/systems11030141