The Degree of Big Data Technology Transformation and Green Operations in the Banking Sector

Abstract

:1. Introduction

2. Theoretical Background and Hypotheses

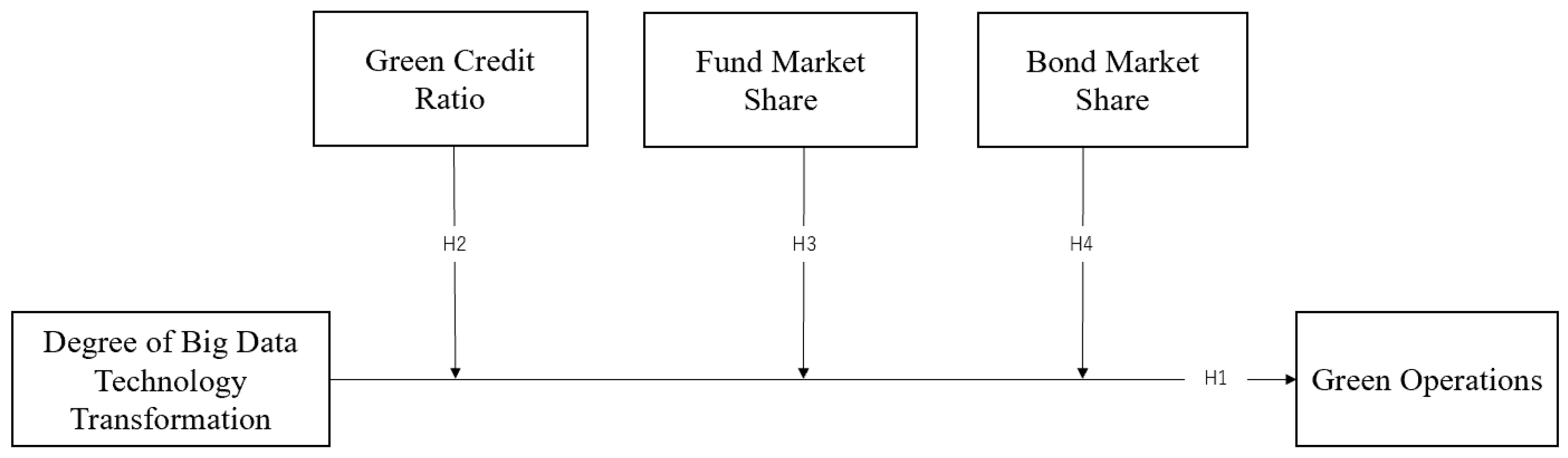

2.1. Impact of Degree of Big Data Technology Transformation on Green Operations in Banking Sector

2.2. The Moderating Role of Green Credit

2.3. The Moderating Role of the Fund

2.4. The Moderating Role of Bonds

3. Methodology

3.1. Sample Selection and Data Sources

3.2. Definition of Variables

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Moderating Variable

Green Credit Ratio

3.2.4. Control Variable

3.3. Research Model

4. Empirical Analysis Results

4.1. Descriptive Statistics

4.2. Correlation Analysis

4.3. Analysis of Empirical Results

5. Conclusions and Implications

5.1. Discussion

5.2. Conclusions

5.3. Limitations and Future Outlook

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Hasan, M.M.; Popp, J.; Oláh, J. Current landscape and influence of big data on finance. J. Big Data 2020, 7, 21. [Google Scholar] [CrossRef]

- Cao, S.; Nie, L.; Sun, H.; Sun, W.; Taghizadeh-Hesary, F. Digital Finance, Green Technological Innovation and Energy-Environmental Performance: Evidence from China’s Regional Economies. J. Clean. Prod. 2021, 327, 129458. [Google Scholar] [CrossRef]

- Zuo, L.; Strauss, J.; Zuo, L. The Digitalization Transformation of Commercial Banks and Its Impact on Sustainable Efficiency Improvements through Investment in Science and Technology. Sustainability 2021, 13, 11028. [Google Scholar] [CrossRef]

- Diener, F.; Špaček, M. Digital Transformation in Banking: A Managerial Perspective on Barriers to Change. Sustainability 2021, 13, 2032. [Google Scholar] [CrossRef]

- Akter, S.; Michael, K.; Uddin, M.R.; McCarthy, G.; Rahman, M. Transforming Business Using Digital Innovations: The Application of AI, Blockchain, Cloud and Data Analytics. Ann. Oper. Res. 2022, 308, 7–39. [Google Scholar] [CrossRef]

- Wang, Y.; Sui, X.; Zhang, Q. Can Fintech Improve the Efficiency of Commercial Banks? An Analysis Based on Big Data. Res. Int. Bus. Financ. 2021, 55, 101338. [Google Scholar] [CrossRef]

- Broby, D. Financial Technology and the Future of Banking. Financ. Innov. 2021, 7, 47. [Google Scholar] [CrossRef]

- Bătae, O.M.; Dragomir, V.D.; Feleagă, L. The Relationship between Environmental, Social, and Financial Performance in the Banking Sector: A European Study. J. Clean. Prod. 2021, 290, 125791. [Google Scholar] [CrossRef]

- Naeem, M.; Jamal, T.; Diaz-Martinez, J.; Butt, S.A.; Montesano, N.; Tariq, M.I.; De-la-Hoz-Franco, E.; De-La-Hoz-Valdiris, E. Trends and future perspective challenges in big data. In Advances in Intelligent Data Analysis and Applications, Proceeding of the Sixth Euro-China Conference on Intelligent Data Analysis and Applications, Arad, Romani, 15–18 October 2019; Springer: Singapore, 2022; pp. 309–325. [Google Scholar]

- Ghelani, D.; Hua, T.K.; Koduru, S.K.R. Cyber security threats, vulnerabilities, and security solutions models in banking. Authorea Prepr. 2022. [Google Scholar] [CrossRef]

- Thach, N.N.; Hanh, H.T.; Huy, D.T.N.; Vu, Q.N. Technology quality management of the industry 4.0 and cybersecurity risk management on current banking activities in emerging markets-the case in Vietnam. Int. J. Qual. Res. 2021, 15, 845. [Google Scholar] [CrossRef]

- Gunduz, M.Z.; Das, R. Cyber-security on smart grid: Threats and potential solutions. Comput. Netw. 2020, 169, 107094. [Google Scholar] [CrossRef]

- Wang, K.H.; Zhao, Y.X.; Jiang, C.F.; Li, Z.Z. Does green finance inspire sustainable development? Evidence from a global perspective. Econ. Anal. Policy 2022, 75, 412–426. [Google Scholar] [CrossRef]

- Liu, Z.; Song, J.; Wu, H.; Gu, X.; Zhao, Y.; Yue, X.; Shi, L. Impact of Financial Technology on Regional Green Finance. Comput. Syst. Sci. Eng. 2021, 39, 391–401. [Google Scholar] [CrossRef]

- Akomea-Frimpong, I.; Adeabah, D.; Ofosu, D.; Tenakwah, E.J. A review of studies on green finance of banks, research gaps and future directions. J. Sustain. Financ. Invest. 2022, 12, 1241–1264. [Google Scholar] [CrossRef]

- Wang, X.; Zhao, H.; Bi, K. The Measurement of Green Finance Index and the Development Forecast of Green Finance in China. Environ. Ecol. Stat. 2021, 28, 263–285. [Google Scholar] [CrossRef]

- Zhang, S.; Wu, Z.; Wang, Y.; Hao, Y. Fostering Green Development with Green Finance: An Empirical Study on the Environmental Effect of Green Credit Policy in China. J. Environ. Manag. 2021, 296, 113159. [Google Scholar] [CrossRef] [PubMed]

- Umar, M.; Mirza, N.; Rizvi, S.K.A.; Furqan, M. Asymmetric volatility structure of equity returns: Evidence from an emerging market. Q. Rev. Econ. Financ. 2023, 87, 330–336. [Google Scholar] [CrossRef]

- Cheng, C.; Ge, C. Green Development Assessment for Countries Along the Belt and Road. J. Environ. Manag. 2020, 263, 110344. [Google Scholar]

- Wang, Y.; Guo, C.H.; Chen, X.J.; Jia, L.Q.; Guo, X.N.; Chen, R.S.; Zhang, M.S.; Chen, Z.Y.; Wang, H.D. Carbon Peak and Carbon Neutrality in China: Goals, Implementation Path and Prospects. China Geol. 2021, 4, 720–746. [Google Scholar] [CrossRef]

- Shi, J.; Yu, C.; Li, Y.; Wang, T. Does Green Financial Policy Affect Debt-Financing Cost of Heavy-Polluting Enterprises? An Empirical Evidence Based on Chinese Pilot Zones for Green Finance Reform and Innovations. Technol. Forecast. Soc. Chang. 2022, 179, 121678. [Google Scholar] [CrossRef]

- Lian, Y.; Gao, J.; Ye, T. How Does Green Credit Affect the Financial Performance of Commercial Banks? Evidence from China. J. Clean. Prod. 2022, 344, 131069. [Google Scholar] [CrossRef]

- Kitsios, F.; Giatsidis, I.; Kamariotou, M. Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services. J. Open Innov. Technol. Mark. Complex. 2021, 7, 204. [Google Scholar] [CrossRef]

- Königstorfer, F.; Thalmann, S. Applications of Artificial Intelligence in Commercial Banks: A Research Agenda for Behavioral Finance. J. Behav. Exp. Financ. 2020, 27, 100352. [Google Scholar] [CrossRef]

- Zhou, G.; Zhu, J.; Luo, S. The Impact of Fintech Innovation on Green Growth in China: Mediating Effect of Green Finance. Ecol. Econ. 2022, 193, 107308. [Google Scholar] [CrossRef]

- Li, Y.; Dai, J.; Cui, L. The Impact of Digital Technologies on Economic and Environmental Performance in the Context of Industry 4.0: A Moderated Mediation Model. Int. J. Prod. Econ. 2020, 229, 107777. [Google Scholar] [CrossRef]

- Sharma, P.K.; Kumar, N.; Park, J.H. Blockchain Technology Toward Green Iot: Opportunities and Challenges. IEEE Netw. 2020, 34, 263–269. [Google Scholar] [CrossRef]

- Wen, H.; Zhong, Q.; Lee, C.C. Digitalization, Competition Strategy and Corporate Innovation: Evidence from Chinese Manufacturing Listed Companies. Int. Rev. Financ. Anal. 2022, 82, 102166. [Google Scholar] [CrossRef]

- Du, K.; Cheng, Y.; Yao, X. Environmental Regulation, Green Technology Innovation, and Industrial Structure Upgrading: The Road to the Green Transformation of Chinese Cities. Energy Econ. 2021, 98, 105247. [Google Scholar] [CrossRef]

- Yang, Y.; Su, X.; Yao, S. Nexus Between Green Finance, Fintech, and High-Quality Economic Development: Empirical Evidence from China. Resour. Policy 2021, 74, 102445. [Google Scholar] [CrossRef]

- Irfan, M.; Razzaq, A.; Sharif, A.; Yang, X. Influence Mechanism Between Green Finance and Green Innovation: Exploring Regional Policy Intervention Effects in China. Technol. Forecast. Soc. Chang. 2022, 182, 121882. [Google Scholar] [CrossRef]

- Muganyi, T.; Yan, L.; Sun, H.P. Green Finance, Fintech and Environmental Protection: Evidence from China. Environ. Sci. Ecotechnol. 2021, 7, 100107. [Google Scholar] [CrossRef]

- Zhao, J.; Li, X.; Yu, C.H.; Chen, S.; Lee, C.C. Riding the Fintech Innovation Wave: Fintech, Patents and Bank Performance. J. Int. Money Financ. 2022, 122, 102552. [Google Scholar] [CrossRef]

- Khan, P.A.; Johl, S.K.; Akhtar, S. Vinculum of Sustainable Development Goal Practices and Firms’ Financial Performance: A Moderation Role of Green Innovation. J. Risk Financ. Manag. 2022, 15, 96. [Google Scholar] [CrossRef]

- Wang, L.; Xu, H. Research on the Path of Green Finance to Support the Digital Transformation of the Banking Industry. Financ. Eng. Risk Manag. 2023, 6, 84–91. [Google Scholar]

- Bag, S.; Wood, L.C.; Xu, L.; Dhamija, P.; Kayikci, Y. Big data analytics as an operational excellence approach to enhance sustainable supply chain performance. Resour. Conserv. Recycl. 2020, 153, 104559. [Google Scholar] [CrossRef]

- Feng, S.; Zhang, R.; Li, G. Environmental decentralization, digital finance and green technology innovation. Struct. Chang. Econ. Dyn. 2022, 61, 70–83. [Google Scholar] [CrossRef]

- Umar, M.; Ji, X.; Kirikkaleli, D.; Xu, Q. COP21 Roadmap: Do innovation, financial development, and transportation infrastructure matter for environmental sustainability in China? J. Environ. Manag. 2020, 271, 111026. [Google Scholar] [CrossRef]

- Feroz, A.K.; Zo, H.; Chiravuri, A. Digital Transformation and Environmental Sustainability: A Review and Research Agenda. Sustainability 2021, 13, 1530. [Google Scholar] [CrossRef]

- Gupta, S.; Chen, H.; Hazen, B.T.; Kaur, S.; Gonzalez, E.D.S. Circular Economy and Big Data Analytics: A Stakeholder Perspective. Technol. Forecast. Soc. Chang. 2019, 144, 466–474. [Google Scholar] [CrossRef]

- Zhao, Q.; Tsai, P.H.; Wang, J.L. Improving Financial Service Innovation Strategies for Enhancing China’s Banking Industry Competitive Advantage During the Fintech Revolution: A Hybrid MCDM Model. Sustainability 2019, 11, 1419. [Google Scholar] [CrossRef]

- Mondejar, M.E.; Avtar, R.; Diaz, H.L.B.; Dubey, R.K.; Esteban, J.; Gómez-Morales, A.; Hallam, B.; Mbungu, N.T.; Okolo, C.C.; Prasad, K.A. Digitalization to Achieve Sustainable Development Goals: Steps Towards a Smart Green Planet. Sci. Total Environ. 2021, 794, 148539. [Google Scholar] [CrossRef] [PubMed]

- Dhamija, P.; Bag, S. Role of Artificial Intelligence in Operations Environment: A Review and Bibliometric Analysis. TQM J. 2020, 32, 869–896. [Google Scholar] [CrossRef]

- Duchêne, S. Review of handbook of green finance. Ecol. Econ. 2020, 177, 106766. [Google Scholar] [CrossRef]

- Kamble, S.S.; Gunasekaran, A. Big data-driven supply chain performance measurement system: A review and framework for implementation. Int. J. Prod. Res. 2020, 58, 65–86. [Google Scholar] [CrossRef]

- Luo, S.; Yu, S.; Zhou, G. Does Green Credit Improve the Core Competence of Commercial Banks? Based on Quasi-Natural Experiments in China. Energy Econ. 2021, 100, 105335. [Google Scholar] [CrossRef]

- Ling, S.; Han, G.; An, D.; Hunter, W.C.; Li, H. The Impact of Green Credit Policy on Technological Innovation of Firms in Pollution-Intensive Industries: Evidence from China. Sustainability 2020, 12, 4493. [Google Scholar] [CrossRef]

- Jin, Y.; Gao, X.; Wang, M. The Financing Efficiency of Listed Energy Conservation and Environmental Protection Firms: Evidence and Implications for Green Finance in China. Energy Policy 2021, 153, 112254. [Google Scholar] [CrossRef]

- Cheng, Q.; Lai, X.; Liu, Y.; Yang, Z.; Liu, J. The influence of green credit on China’s industrial structure upgrade: Evidence from industrial sector panel data exploration. Environ. Sci. Pollut. Res. 2022, 29, 22439–22453. [Google Scholar] [CrossRef] [PubMed]

- Zhang, K.; Li, Y.; Qi, Y.; Shao, S. Can green credit policy improve environmental quality? Evidence from China. J. Environ. Manag. 2021, 298, 113445. [Google Scholar] [CrossRef]

- Xing, C.; Zhang, Y.; Wang, Y. Do banks value green management in China? The perspective of the green credit policy. Financ. Res. Lett. 2020, 35, 101601. [Google Scholar] [CrossRef]

- Yin, W.; Zhu, Z.; Kirkulak-Uludag, B.; Zhu, Y. The Determinants of Green Credit and Its Impact on the Performance of Chinese Banks. J. Clean. Prod. 2021, 286, 124991. [Google Scholar] [CrossRef]

- Xi, B.; Wang, Y.; Yang, M. Green Credit, Green Reputation, and Corporate Financial Performance: Evidence from China. Environ. Sci. Pollut. Res. 2022, 29, 2401–2419. [Google Scholar] [CrossRef] [PubMed]

- Zhou, X.Y.; Caldecott, B.; Hoepner, A.G.; Wang, Y. Bank Green Lending and Credit Risk: An Empirical Analysis of China’s Green Credit Policy. Bus. Strategy Environ. 2022, 31, 1623–1640. [Google Scholar] [CrossRef]

- Zhou, G.; Sun, Y.; Luo, S.; Liao, J. Corporate Social Responsibility and Bank Financial Performance in China: The Moderating Role of Green Credit. Energy Econ. 2021, 97, 105190. [Google Scholar] [CrossRef]

- Wang, F.; Cai, W.; Elahi, E. Do Green Finance and Environmental Regulation Play a Crucial Role in the Reduction of CO2 Emissions? An Empirical Analysis of 126 Chinese Cities. Sustainability 2021, 13, 13014. [Google Scholar] [CrossRef]

- Song, M.; Xie, Q.; Shen, Z. Impact of Green Credit on High-Efficiency Utilization of Energy in China Considering Environmental Constraints. Energy Policy 2021, 153, 112267. [Google Scholar] [CrossRef]

- Wang, M.; Li, X.; Wang, S. Discovering Research Trends and Opportunities of Green Finance and Energy Policy: A Data-Driven Scientometric Analysis. Energy Policy 2021, 154, 112295. [Google Scholar] [CrossRef]

- Debrah, C.; Chan, A.P.C.; Darko, A. Green Finance Gap in Green Buildings: A Scoping Review and Future Research Needs. Build. Environ. 2020, 207, 108443. [Google Scholar] [CrossRef]

- Crona, B.; Folke, C.; Galaz, V. The Anthropocene Reality of Financial Risk. One Earth 2021, 4, 618–628. [Google Scholar] [CrossRef]

- Berrou, R.; Dessertine, P.; Migliorelli, M. An Overview of Green Finance. In The Rise of Green Finance in Europe: Opportunities and Challenges for Issuers, Investors and Marketplaces; Migliorelli, M., Dessertine, P., Eds.; Palgrave Macmillan: London, UK, 2019; pp. 3–29. [Google Scholar]

- Lee, C.C.; Lee, C.C. How Does Green Finance Affect Green Total Factor Productivity? Evidence from China. Energy Econ. 2022, 107, 105863. [Google Scholar] [CrossRef]

- Naqvi, B.; Rizvi, S.K.A.; Hasnaoui, A.; Shao, X. Going Beyond Sustainability: The Diversification Benefits of Green Energy Financial Products. Energy Econ. 2022, 111, 106111. [Google Scholar] [CrossRef]

- Chen, X.; Chen, Z. Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces. Sustainability 2021, 13, 12137. [Google Scholar] [CrossRef]

- Guo, Y.; Xia, X.; Zhang, S.; Zhang, D. Environmental Regulation, Government R&D Funding and Green Technology Innovation: Evidence from China Provincial Data. Sustainability 2018, 10, 940. [Google Scholar] [CrossRef]

- Park, H.; Kim, J.D. Transition Towards Green Banking: Role of Financial Regulators and Financial Institutions. Asian J. Sustain. Soc. Responsib. 2020, 5, 1–25. [Google Scholar] [CrossRef]

- Lee, J.W. Green Finance and Sustainable Development Goals: The Case of China. J. Asian Financ. Econ. Bus. 2020, 7, 577–586. [Google Scholar] [CrossRef]

- Sartzetakis, E.S. Green Bonds as an Instrument to Finance Low Carbon Transition. Econ. Chang. Restruct. 2021, 54, 755–779. [Google Scholar] [CrossRef]

- Zhao, L.; Chau, K.Y.; Tran, T.K.; Sadiq, M.; Xuyen, N.T.M.; Phan, T.T.H. Enhancing Green Economic Recovery through Green Bonds Financing and Energy Efficiency Investments. Econ. Anal. Policy 2022, 76, 488–501. [Google Scholar] [CrossRef]

- Maltais, A.; Nykvist, B. Understanding the Role of Green Bonds in Advancing Sustainability. J. Sustain. Financ. Invest. 2020, 1–20. [Google Scholar] [CrossRef]

- Gianfrate, G.; Peri, M. The Green Advantage: Exploring the Convenience of Issuing Green Bonds. J. Clean. Prod. 2019, 219, 127–135. [Google Scholar] [CrossRef]

- Löffler, K.U.; Petreski, A.; Stephan, A. Drivers of green bond issuance and new evidence on the “greenium”. Eurasian Econ. Rev. 2021, 11, 1–24. [Google Scholar] [CrossRef]

- Cao, X.; Jin, C.; Ma, W. Motivation of Chinese Commercial Banks to Issue Green Bonds: Financing Costs or Regulatory Arbitrage? China Econ. Rev. 2021, 66, 101582. [Google Scholar] [CrossRef]

- Yeow, K.E.; Ng, S.H. The Impact of Green Bonds on Corporate Environmental and Financial Performance. Manag. Financ. 2021, 47, 1486–1510. [Google Scholar] [CrossRef]

- Fatica, S.; Panzica, R.; Rancan, M. The Pricing of Green Bonds: Are Financial Institutions Special? J. Financ. Stab. 2021, 54, 100873. [Google Scholar] [CrossRef]

- Navaretti, G.B.; Calzolari, G.; Mansilla-Fernandez, J.M.; Pozzolo, A.F. Fintech and Banking: Friends or Foes? Friends or Foes. 2018. Available online: https://european-economy.eu/wp-content/uploads/2017/07/EE_2.2017.pdf#page=11 (accessed on 18 January 2024).

- Zhu, Y.; Jin, S. How Does the Digital Transformation of Banks Improve Efficiency and Environmental, Social, and Governance Performance? Systems 2023, 11, 328. [Google Scholar] [CrossRef]

- Feng, H.; Wang, F.; Song, G.; Liu, L. Digital Transformation on Enterprise Green Innovation: Effect and Transmission Mechanism. Int. J. Environ. Res. Public Health 2022, 19, 10614. [Google Scholar] [CrossRef]

- Song, X.; Deng, X.; Wu, R. Comparing the Influence of Green Credit on Commercial Bank Profitability in China and Abroad: Empirical Test Based on a Dynamic Panel System Using GMM. Int. J. Financ. Stud. 2019, 7, 64. [Google Scholar] [CrossRef]

- Le, T.D.; Ngo, T. The Determinants of Bank Profitability: A Cross-Country Analysis. Cent. Bank Rev. 2020, 20, 65–73. [Google Scholar] [CrossRef]

- Wang, J.; Chen, X.; Li, X.; Yu, J.; Zhong, R. The Market Reaction to Green Bond Issuance: Evidence from China. Pac.-Basin Financ. J. 2020, 60, 101294. [Google Scholar] [CrossRef]

- He, F.; Guo, X.; Yue, P. Media Coverage and Corporate ESG Performance: Evidence from China. Int. Rev. Financ. Anal. 2024, 91, 103003. [Google Scholar] [CrossRef]

- Hu, G.; Wang, X.; Wang, Y. Can the Green Credit Policy Stimulate Green Innovation in Heavily Polluting Enterprises? Evidence from a Quasi-Natural Experiment in China. Energy Econ. 2021, 98, 105134. [Google Scholar] [CrossRef]

- Li, Y.; Zhu, D. Share Pledging and Corporate Environmental Investment. Financ. Res. Lett. 2022, 50, 103348. [Google Scholar] [CrossRef]

- Yuan, X.; Li, Z.; Xu, J.; Shang, L. ESG Disclosure and Corporate Financial Irregularities: Evidence from Chinese Listed Firms. J. Clean. Prod. 2022, 332, 129992. [Google Scholar] [CrossRef]

- Wang, Q.; Zhang, F. Does Increasing Investment in Research and Development Promote Economic Growth Decoupling from Carbon Emission Growth? An Empirical Analysis of BRICS Countries. J. Clean. Prod. 2020, 252, 119853. [Google Scholar] [CrossRef]

- Liu, D.; Jin, S. How Does Corporate ESG Performance Affect Financial Irregularities? Sustainability 2023, 15, 9999. [Google Scholar] [CrossRef]

- Xuan, D.; Ma, X.; Shang, Y. Can China’s policy of carbon emission trading promote carbon emission reduction? J. Clean. Prod. 2020, 270, 122383. [Google Scholar] [CrossRef]

- Wu, L.; Jin, S. Corporate Social Responsibility and Sustainability: From a Corporate Governance Perspective. Sustainability 2022, 14, 15457. [Google Scholar] [CrossRef]

- Wu, F.; Lu, C.; Zhu, M.; Chen, H.; Zhu, J.; Yu, K.; Li, L.; Li, M.; Chen, Q.; Li, X.; et al. Towards a New Generation of Artificial Intelligence in China. Nat. Mach. Intell. 2020, 2, 312–316. [Google Scholar] [CrossRef]

- Elia, G.; Polimeno, G.; Solazzo, G.; Passiante, G. A Multi-Dimension Framework for Value Creation through Big Data. Ind. Mark. Manag. 2020, 90, 617–632. [Google Scholar] [CrossRef]

- Cheng, M.; Qu, Y. Does Bank Fintech Reduce Credit Risk? Evidence from China. Pac. Basin Financ. J. 2020, 63, 101398. [Google Scholar] [CrossRef]

- Ahmad, M.; Jiang, P.; Majeed, A.; Umar, M.; Khan, Z.; Muhammad, S. The Dynamic Impact of Natural Resources, Technological Innovations and Economic Growth on Ecological Footprint: An Advanced Panel Data Estimation. Resour. Policy 2020, 69, 101817. [Google Scholar] [CrossRef]

- Lee, C.C.; Li, X.; Yu, C.H.; Zhao, J. Does Fintech Innovation Improve Bank Efficiency? Evidence from China’s Banking Industry. Int. Rev. Econ. Financ. 2021, 74, 468–483. [Google Scholar] [CrossRef]

- Abkenar, S.B.; Kashani, M.H.; Mahdipour, E.; Jameii, S.M. Big Data Analytics Meets Social Media: A Systematic Review of Techniques, Open Issues, ond Future Directions. Telemat. Inform. 2021, 57, 101517. [Google Scholar] [CrossRef]

- Reza-Gharehbagh, R.; Hafezalkotob, A.; Makui, A.; Sayadi, M.K. Government intervention policies in competition of financial chains: A game theory approach. Kybernetes 2020, 49, 960–981. [Google Scholar] [CrossRef]

{kind=link}

| Name | Non-Cash Payment Services (Billion Transactions) | Non-Cash Payment Services (Trillion Yuan) | Electronic Payment Services (Billion Transactions) | Electronic Payment Services (Trillion Yuan) |

|---|---|---|---|---|

| 2015 | 943.22 | 3448.85 | 1052.34 | 2506.23 |

| 2016 | 1251.11 | 3687.24 | 1395.61 | 2494.45 |

| 2017 | 1608.78 | 3759.94 | 1525.8 | 2419.2 |

| 2018 | 2203.12 | 3768.67 | 1751.92 | 2539.7 |

| 2019 | 3310.19 | 3779.49 | 2233.88 | 2607.04 |

| 2020 | 2547.21 | 4013.01 | 2352.25 | 2711.81 |

| 2021 | 4395.06 | 4415.56 | 2749.69 | 2976.22 |

| 2022 | 4626.49 | 4805.77 | 2789.65 | 3110.13 |

| Name | Variable Name | Abbreviation | Definition of Variable |

|---|---|---|---|

| Independent Variables | Degree of Big Data Technology Transformation | FTLF | Ln (keyword word frequency + 1) |

| Dependent Variables | Green Operations | GES | Bloomberg Environmental Rating |

| Moderating Variables | Green Credit Ratio | GCR | Ln (green credit balance/total loans + 1) |

| Fund Market Share | MSF | Ln (fund issuance/total commercial bank fund issuance + 1) | |

| Bond Market Share | BIR | Ln (bond issuance/total commercial bank bond issuance + 1) | |

| control variable | Company Size | Size | Ln (book value of total assets at year-end) |

| Gearing Ratio | Lev | Total liabilities at year-end/total assets at year-end | |

| Company Age | AGE | Ln (year of observation − year of establishment + 1) | |

| Company Performance | ROA | Net profit/total assets | |

| Revenue Growth Rate | GRO | Revenue growth rate | |

| Nature of the Largest Shareholder | SOE | 1 for state-owned enterprises, 0 for others | |

| Shareholding Ratio of the Largest Shareholder | TOP1 | Shareholding ratio of the largest shareholder |

| Variables | N | Mean | sd | Min | Max |

|---|---|---|---|---|---|

| GES | 235 | 3.082 | 0.884 | 0.0837 | 4.303 |

| FTLF | 235 | 1.957 | 0.771 | 0 | 3.526 |

| GCR | 235 | 0.0363 | 0.0372 | 0 | 0.171 |

| MSF | 235 | 1.217 | 1.517 | 0 | 7.429 |

| BIR | 235 | 0.00407 | 0.00587 | 0 | 0.0438 |

| Size | 235 | 28.42 | 1.570 | 25.56 | 31.31 |

| Lev | 235 | 0.924 | 0.00972 | 0.897 | 0.947 |

| AGE | 235 | 3.253 | 0.452 | 2.079 | 4.710 |

| ROA | 235 | 0.875 | 0.176 | 0.424 | 1.437 |

| GRO | 235 | 0.0858 | 0.0864 | −0.156 | 0.428 |

| TOP1 | 235 | 24.46 | 17.05 | 4.180 | 67.39 |

| SOE | 235 | 0.630 | 0.484 | 0 | 1 |

| GES | FTLF | GCR | MSF | BIR | Size | Lev | AGE | ROA | GRO | TOP1 | SOE | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GES | 1 | |||||||||||

| FTLF | 0.211 *** | 1 | ||||||||||

| GCR | 0.152 ** | 0.0300 | 1 | |||||||||

| MSF | 0.166 ** | 0.110 * | 0.126 * | 1 | ||||||||

| BIR | 0.221 *** | 0.162 ** | 0.486 *** | 0.180 *** | 1 | |||||||

| Size | 0.474 *** | 0.179 *** | 0.00700 | 0.0520 | 0.0410 | 1 | ||||||

| Lev | −0.215 *** | 0.157 ** | −0.0830 | −0.190 *** | −0.0420 | −0.0640 | 1 | |||||

| AGE | 0.309 *** | 0.116 * | 0.0100 | 0.140 ** | 0.0350 | 0.682 *** | −0.281 *** | 1 | ||||

| ROA | −0.0910 | −0.117 * | −0.0490 | 0.0810 | 0.00200 | 0.202 *** | −0.111 * | 0.306 *** | 1 | |||

| GRO | −0.155 ** | 0.0870 | −0.0190 | −0.0400 | −0.00700 | −0.218 *** | 0.245 *** | −0.184 *** | 0.202 *** | 1 | ||

| TOP1 | 0.308 *** | 0.266 *** | 0.0920 | 0.0590 | 0.148 ** | 0.659 *** | −0.0240 | 0.648 *** | 0.0100 | −0.151 ** | 1 | |

| SOE | 0.131 ** | 0.0250 | −0.0130 | 0.0390 | 0.0220 | 0.250 *** | −0.00600 | 0.137 ** | 0.141 ** | −0.0860 | 0.193 *** | 1 |

| (1) | (2) | |

|---|---|---|

| Variables | GES | GES |

| FTLF | 0.194 *** | 0.134 * |

| (2.76) | (1.88) | |

| Lev | −7.295 | |

| (−1.02) | ||

| AGE | −0.081 | |

| (−0.47) | ||

| Size | 0.374 *** | |

| (6.41) | ||

| ROA | −0.465 | |

| (−1.34) | ||

| GROWTH | 0.550 | |

| (0.78) | ||

| SOE | 0.014 | |

| (0.14) | ||

| TOP1 | −0.002 | |

| (−0.51) | ||

| Constant | 1.921 *** | −0.659 |

| (8.36) | (−0.10) | |

| City fixed | Yes | Yes |

| Year fixed | Yes | Yes |

| Observations | 235 | 235 |

| R-squared | 0.311 | 0.440 |

| F test | 0 | 0 |

| r2_a | 0.277 | 0.393 |

| F | 9.158 | 9.431 |

| (1) | (2) | |

|---|---|---|

| GES | GES | |

| FTLF | 0.134 * | |

| (1.88) | ||

| DTA | 0.529 * | |

| (1.90) | ||

| Lev | −7.295 | −7.376 |

| (−1.02) | (−1.03) | |

| AGE | −0.081 | −0.081 |

| (−0.47) | (−0.47) | |

| Size | 0.374 *** | 0.374 *** |

| (6.41) | (6.41) | |

| ROA | −0.465 | −0.465 |

| (−1.34) | (−1.34) | |

| GROWTH | 0.550 | 0.550 |

| (0.78) | (0.78) | |

| SOE | 0.014 | 0.015 |

| (0.14) | (0.14) | |

| TOP1 | −0.002 | −0.002 |

| (−0.51) | (−0.52) | |

| Constant | −0.659 | −0.585 |

| (−0.10) | (−0.09) | |

| City fixed | Yes | Yes |

| Year fixed | Yes | Yes |

| Observations | 235 | 235 |

| R-squared | 0.440 | 0.440 |

| F test | 0 | 0 |

| r2_a | 0.393 | 0.394 |

| F | 9.431 | 9.441 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | GES | GES | GES | GES |

| FTLF | 0.169 ** | 0.179 *** | 0.150 ** | 0.135 ** |

| (2.52) | (2.69) | (2.22) | (2.04) | |

| GCR | 1.975 * | |||

| (1.93) | ||||

| GCR x FTLF | 3.764 ** | |||

| (2.08) | ||||

| MSF | 0.001 | |||

| (0.39) | ||||

| MSF x FTLF | 0.063 * | |||

| (1.92) | ||||

| BIR | 0.003 | |||

| (0.66) | ||||

| BIR x FTLF | 0.353 *** | |||

| (3.42) | ||||

| Size | 0.308 *** | 0.289 *** | 0.314 *** | 0.317 *** |

| (6.48) | (6.00) | (6.60) | (6.80) | |

| Lev | −22.933 *** | −19.883 *** | −21.375 *** | −21.617 *** |

| (−4.10) | (−3.54) | (−3.77) | (−3.93) | |

| AGE | −0.067 | −0.050 | −0.087 | −0.011 |

| (−0.38) | (−0.28) | (−0.49) | (−0.06) | |

| ROA | −1.105 *** | −1.072 *** | −1.159 *** | −1.202 *** |

| (−3.37) | (−3.32) | (−3.50) | (−3.70) | |

| GRO | 0.437 | 0.389 | 0.437 | 0.433 |

| (0.68) | (0.61) | (0.68) | (0.69) | |

| TOP1 | −0.004 | −0.005 | −0.004 | −0.007 |

| (−0.89) | (−1.09) | (−0.91) | (−1.51) | |

| SOE | 0.078 | 0.057 | 0.071 | 0.077 |

| (0.75) | (0.55) | (0.68) | (0.75) | |

| Constant | 16.383 *** | 14.040 *** | 14.886 *** | 14.772 *** |

| (3.11) | (2.68) | (2.79) | (2.84) | |

| Observations | 235 | 235 | 235 | 235 |

| R-squared | 0.329 | 0.355 | 0.340 | 0.363 |

| r2_a | 0.31 | 0.33 | 0.31 | 0.33 |

| F | 13.841 | 12.304 | 11.550 | 12.765 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yun, J.; Jin, S. The Degree of Big Data Technology Transformation and Green Operations in the Banking Sector. Systems 2024, 12, 135. https://doi.org/10.3390/systems12040135

Yun J, Jin S. The Degree of Big Data Technology Transformation and Green Operations in the Banking Sector. Systems. 2024; 12(4):135. https://doi.org/10.3390/systems12040135

Chicago/Turabian StyleYun, Jiawen, and Shanyue Jin. 2024. "The Degree of Big Data Technology Transformation and Green Operations in the Banking Sector" Systems 12, no. 4: 135. https://doi.org/10.3390/systems12040135

APA StyleYun, J., & Jin, S. (2024). The Degree of Big Data Technology Transformation and Green Operations in the Banking Sector. Systems, 12(4), 135. https://doi.org/10.3390/systems12040135