The Enabling Role of Digital Technologies in Sustainability Accounting: Findings from Norwegian Manufacturing Companies

Abstract

:1. Introduction

2. Literature

2.1. Sustainability and Sustainability Accounting

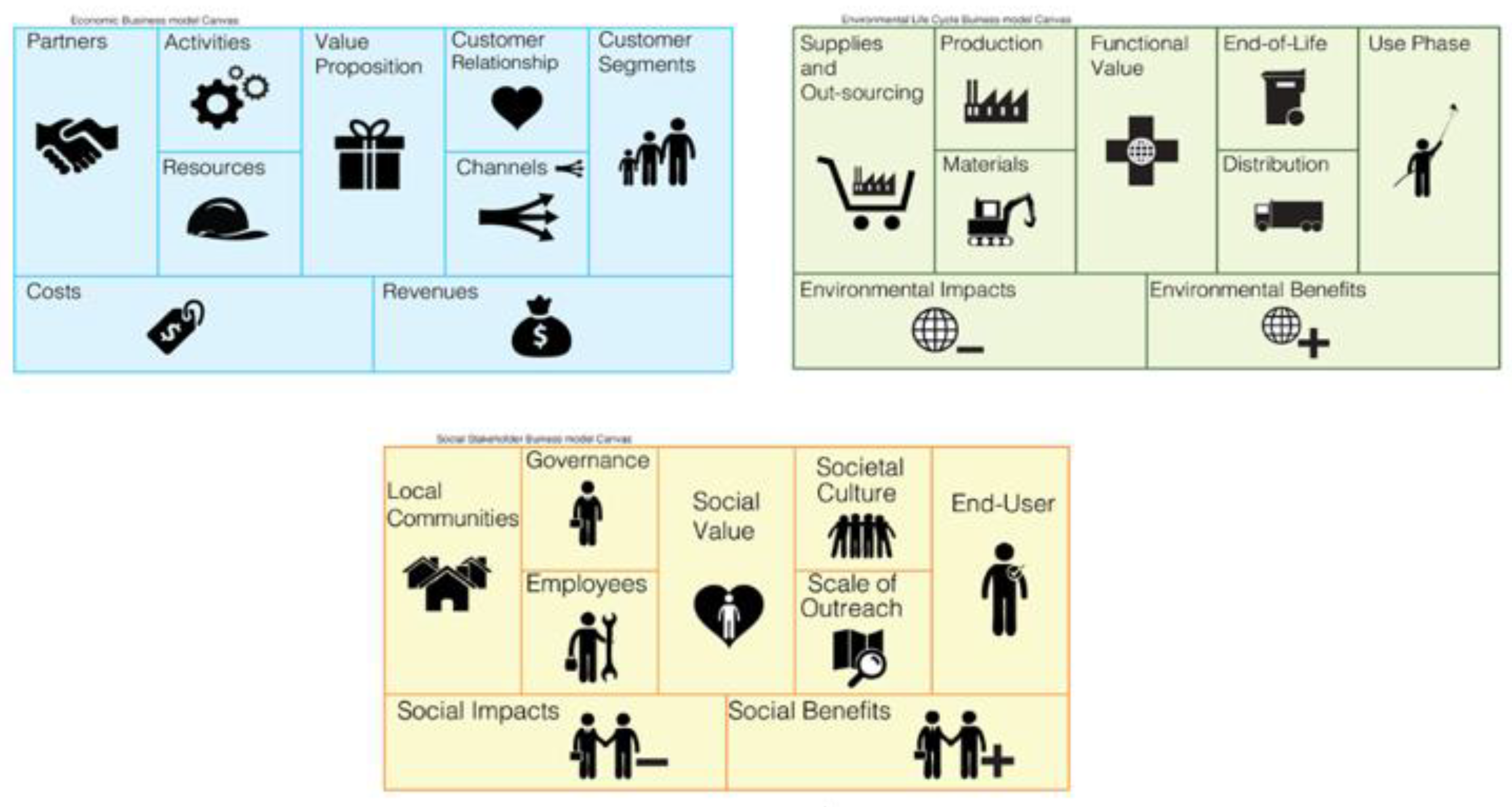

2.2. The Triple Layered Business Model Canvas (TLBMC)

2.3. Digitalization and Industry 4.0

2.4. Digitalization and Sustainability

- Better data quality (timeliness, accuracy, reliability, comparability)

- Reduced opportunity for “greenwash” and “brownwash”

- Less management discretion regarding measurements

- Higher credibility of data

3. Research Method

Case Companies and Data Collection

4. Results

4.1. Company A, Pipe Manufacturer

4.1.1. Company A’s Sustainability Accounting and Reporting

“We have two concepts that we have extensively worked on for decades. We had already stated in the 1980s that it is appropriate to address environmental protection. Then we started with EPD, LCA, and third-party certified documentation, and we realized that with the available materials and properties, we can document it.”(Respondent)

“In future, we will address two types of accounting: environmental and economic accounting. With focus on sustainability, we can achieve positive results for both. At the same time, we can leave a sustainable planet for future generations.”(Respondent)

“Until now, there has been no requirement that has asked about CO2 emissions and EPD, so we have not clarified our climate accounts, but it is something that if we do it, we want to show it. Having said that, the EU Green Deal is under implementation …”(Respondent)

4.1.2. The Role of Digital Technologies in Company A

“Combined with lifting the sensor data up in a Cloud platform, applying algorithms, machine learning, artificial intelligence, and everything that is possible now, preferably combined with data on weather conditions, we can predict events before they happen”[58]

4.2. Company B, Furniture Producer

4.2.1. Sustainability Accounting and Reporting at Company B

“We have customers with their own end-user perspective where it is about sustainable materials and how they see a sustainable product; it also concerns the entire value chain and everyone around us.”(Respondent)

4.2.2. The Role of Digital Technologies at Company B

“New technologies, environment-friendly materials, and new product solutions have resulted in one of the most efficient manufacturing environments in the furniture industry today.”(Respondent)

“Obtaining relevant data and—not least—the opportunity to make good analyses across different data sources is becoming more and more important in order to be able to make the right decisions”[61]

4.3. Company C, Maritime Equipment Manufacturer

4.3.1. Sustainability Accounting and Reporting at Company C

4.3.2. The Role of Digital Technologies at Company C

“Many suppliers would like to be connected with the customer, but it does not always mean that the customer wants it to become dependent on the supplier, so this is a negative aspect of the digitalized value chain. On the other hand, we have an ideal cooperation with one supplier for optimizing the production processes. If you make sure that the entire supply chain is digitally traceable, you can see all the components and simultaneously plan the entire supply chain. Then, you can perform a great deal of optimization regarding waste in the value chain.”(Respondent)

4.4. Company D, Plastic Products Manufacturer

4.4.1. Sustainability Accounting and Reporting at Company D

“There will be regulations, and there will be pushes from the market, and if we can be at the forefront and have the solution ready, it will create dependence on us and create new opportunities in new markets that place greater emphasis on sustainability and responsibility for consumption and production.”(Respondent)

4.4.2. The Role of Digital Technologies at Company D

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Grin, J.; Rotmans, J.; Schot, J. Transitions to Sustainable Development: New Directions in the Study of Long Term Transformative Change; Routledge: New York, NY, USA, 2010. [Google Scholar]

- Joyce, A.; Paquin, R.L. The triple layered business model canvas: A tool to design more sustainable business models. J. Clean. Prod. 2016, 135, 1474–1486. [Google Scholar] [CrossRef]

- United Nations. The sustainable development agenda. In Department of Public Information; United Nations: New York, NY, USA, 2015. [Google Scholar]

- European Commission. Communication from the Commission—The European Green Deal, COM(2019) 640 Final. 2019. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM%3A2019%3A640%3AFIN (accessed on 26 March 2021).

- Global Reporting Initiative. Global Reporting Initiative. 2021. Available online: https://www.globalreporting.org/ (accessed on 24 March 2021).

- International Organization for Standardization. ISO Standards. 2021. Available online: https://www.iso.org/standards.html (accessed on 24 March 2021).

- Arbeids- og Sosialdepartementet. (1997, 01.07.2017). Forskrift om Systematisk Helse-, Miljø- og Sikkerhetsarbeid i Virksomheter (Internkontrollforskriften). FOR-1996-12-06. Available online: https://lovdata.no/dokument/SF/forskrift/1996-12-06-1127 (accessed on 22 March 2021).

- Finansdepartementet. Lov om Årsregnskap m.v. (regnskapsloven). LOV-1998-07-17. 1998. Available online: https://lovdata.no/dokument/NL/lov/1998-07-17-56#KAPITTEL_3 (accessed on 21 March 2021).

- The Global Language of Business. GS1 General Specifications: The Foundational GS1 Standard that Defines How Identification Keys, Data Attributes and Barcodes Must Be Used in Business Applications. Release 21.0.1. 2018. Available online: https://www.gs1.org/docs/barcodes/GS1_General_Specifications.pdf (accessed on 22 March 2021).

- Jaeger, B.; Upadhyay, A. Understanding barriers to circular economy: Cases from the manufacturing industry. J. Enterp. Inf. Manag. 2020, 33, 729–745. [Google Scholar] [CrossRef]

- Lieder, M.; Rashid, A. Towards circular economy implementation: A comprehensive review in context of manufacturing industry. J. Clean. Prod. 2016, 115, 36–51. [Google Scholar] [CrossRef]

- Burritt, R.; Christ, K. Industry 4.0 and environmental accounting: A new revolution? Asian J. Sustain. Soc. Responsib. 2016, 1, 23–38. [Google Scholar] [CrossRef] [Green Version]

- Hörisch, J.; Schaltegger, S.; Freeman, R.E. Integrating stakeholder theory and sustainability accounting: A conceptual synthesis. J. Clean. Prod. 2020, 275, 124097. [Google Scholar] [CrossRef]

- Ng, A.W. From sustainability accounting to a green financing system: Institutional legitimacy and market heterogeneity in a global financial centre. J. Clean. Prod. 2018, 195, 585–592. [Google Scholar] [CrossRef]

- Rodriguez, A.; Cotran, H.; Stewart, L.S. Evaluating the effectiveness of sustainability disclosure: Findings from a recent SASB study. J. Appl. Corp. Financ. 2017, 29, 100–108. [Google Scholar] [CrossRef]

- Clarke-Sather, A.R.; Hutchins, M.J.; Zhang, Q.; Gershenson, J.K.; Sutherland, J.W. Development of social, environmental, and economic indicators for a small/medium enterprise. Int. J. Account. Inf. Manag. 2011, 19, 247–266. [Google Scholar] [CrossRef]

- International Electrotechnical Commission. Factory of the Future. White Paper. 2015. Available online: http://pubweb2.iec.ch/whitepaper/pdf/iecWP-futurefactory-LR-en.pdf (accessed on 21 March 2021).

- Porter, M.E.; Heppelmann, J.E. How smart, connected products are transforming companies. Harv. Bus. Rev. 2015, 93, 96–114. [Google Scholar]

- Morlet, A.; Blériot, J.; Opsomer, R.; Linder, M.; Henggeler, A.; Bluhm, A.; Carrera, A. Intelligent Assets: Unlocking the Circular Economy Potential; Ellen MacArthur Foundation: Cowes, UK, 2016; pp. 1–25. [Google Scholar]

- Bonilla, S.H.; Silva, H.R.; Terra da Silva, M.; Franco Gonçalves, R.; Sacomano, J.B. Industry 4.0 and Sustainability Implications: A Scenario-Based Analysis of the Impacts and Challenges. Sustainability 2018, 10, 3740. [Google Scholar] [CrossRef] [Green Version]

- Stock, T.; Obenaus, M.; Kunz, S.; Kohl, H. Industry 4.0 as enabler for a sustainable development: A qualitative assessment of its ecological and social potential. Process. Saf. Environ. Prot. 2018, 118, 254–267. [Google Scholar] [CrossRef]

- Tiwari, K.; Khan, M.S. Sustainability accounting and reporting in the industry 4.0. J. Clean. Prod. 2020, 258, 120783. [Google Scholar] [CrossRef]

- UNWCED. Report of the World Commision on Evironment and Development: Our Common Future; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- Rockström, J.; Steffen, W.; Noone, K.; Persson, Å.; Chapin, F.S.; Lambin, E.F.; Lenton, T.M.; Scheffer, M.; Folke, C.; Schellnhuber, H.J.; et al. A safe operating space for humanity. Nature 2009, 461, 472–475. [Google Scholar] [CrossRef] [PubMed]

- Bebbington, J.; Larrinaga, C. Accounting and sustainable development: An exploration. Account. Organ. Soc. 2014, 39, 395–413. [Google Scholar] [CrossRef]

- Kolk, A. Trajectories of sustainability reporting by MNCs. J. World Bus. 2010, 45, 367–374. [Google Scholar] [CrossRef] [Green Version]

- Berthelot, S.; Cormier, D.; Magnan, M. Environmental, disclosure research: Review and synthesis. J. Account. Lit. 2003, 22, 1–44. [Google Scholar]

- Laine, M. Ensuring legitimacy through rhetorical changes? A longitudinal interpretation of the environmental disclosures of a leading Finnish chemical company. Account. Audit. Account. J. 2009, 22, 1029–1054. [Google Scholar] [CrossRef] [Green Version]

- Stock, T.; Seliger, G. Opportunities of Sustainable Manufacturing in Industry 4.0. Procedia CIRP 2016, 40, 536–541. [Google Scholar] [CrossRef] [Green Version]

- Hsu, C.-W.; Lee, W.-H.; Chao, W.-C. Materiality analysis model in sustainability reporting: A case study at Lite-On Technology Corporation. J. Clean. Prod. 2013, 57, 142–151. [Google Scholar] [CrossRef]

- Yu, E.P.-Y.; Van Luu, B.; Chen, C.H. Greenwashing in environmental, social and governance disclosures. Res. Int. Bus. Financ. 2020, 52, 101192. [Google Scholar] [CrossRef]

- Pimonenko, T.; Bilan, Y.; Horák, J.; Starchenko, L.; Gajda, W. Green Brand of Companies and Greenwashing under Sustainable Development Goals. Sustainability 2020, 12, 1679. [Google Scholar] [CrossRef] [Green Version]

- Hourneaux, F., Jr.; da Silva Gabriel, M.L.; Gallardo-Vázquez, D.A. Triple bottom line and sustainable performance measurement in industrial companies. Rev. Gestão 2018, 25, 413–429. [Google Scholar] [CrossRef] [Green Version]

- Lee, T.M.; Hutchison, P.D. The Decision to Disclose Environmental Information: A Research Review and Agenda. Adv. Account. 2005, 21, 83–111. [Google Scholar] [CrossRef]

- York, J.; Dembek, C.; Potter, B. Sustainability Reporting to Improve Organizational Performance; Ivey Business School: London, ON, Canada, 2017; 55p. [Google Scholar]

- Kamp, B.; Parry, G. Servitization and advanced business services as levers for competitiveness. Ind. Mark. Manag. 2017, 60, 11–16. [Google Scholar] [CrossRef]

- Baines, T.; Lightfoot, H.W. Servitization of the manufacturing firm. Int. J. Oper. Prod. Manag. 2014, 34, 2–35. [Google Scholar] [CrossRef] [Green Version]

- Bressanelli, G.; Adrodegari, F.; Perona, M.; Saccani, N. Exploring How Usage-Focused Business Models Enable Circular Economy through Digital Technologies. Sustainability 2018, 10, 639. [Google Scholar] [CrossRef] [Green Version]

- Hartmann, J.; Moeller, S. Chain liability in multitier supply chains? Responsibility attributions for unsustainable supplier behavior. J. Oper. Manag. 2014, 32, 281–294. [Google Scholar] [CrossRef] [Green Version]

- Porter, M.E.; van der Linde, C. Green and Competitive: Ending the Stalemate. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar]

- Osterwalder, A.; Pigneur, Y.; Tucci, C. Clarifying Business Models: Origins, Present, and Future of the Concept. Commun. Assoc. Inf. Syst. 2005, 16, 1. [Google Scholar] [CrossRef] [Green Version]

- Zuboff, S. In the Age of the Smart Machine: The Future of Work and Power; Basic Books: New York, NY, USA, 1998. [Google Scholar]

- Bocken, N.M.; de Pauw, I.; Bakker, C.; van der Grinten, B. Product design and business model strategies for a circular economy. J. Ind. Prod. Eng. 2016, 33, 308–320. [Google Scholar] [CrossRef] [Green Version]

- Schwab, K. The Fourth Industrial Revolution; Portfolio Penguin: London, UK, 2017. [Google Scholar]

- Brettel, M.; Friederichsen, N.; Keller, M.; Rosenberg, M. How virtualization, decentralization and network building change the manufacturing landscape: An industry 4.0 perspective. Int. Sch. Sci. Res. Innov. 2017, 8, 37–44. [Google Scholar] [CrossRef]

- Vyatkin, V.; Salcic, Z.; Roop, P.S.; Fitzgerald, J. Now That’s Smart! IEEE Ind. Electron. Mag. 2007, 1, 17–29. [Google Scholar] [CrossRef]

- Hermann, M.; Pentek, T.; Otto, B. Design principles for industrie 4.0 scenarios. In Proceedings of the 2016 IEEE 49th Hawaii International Conference on System Sciences (HICSS), Koloa, HI, USA, 5–8 January 2016; pp. 3928–3937. [Google Scholar]

- De Sousa Jabbour, A.B.L.; Jabbour, C.J.C.; Foropon, C.; Filho, M.G. When titans meet—Can industry 4.0 revolutionise the environmentally-sustainable manufacturing wave? The role of critical success factors. Technol. Forecast. Soc. Chang. 2018, 132, 18–25. [Google Scholar] [CrossRef]

- Strandhagen, J.O.; Vallandingham, L.R.; Fragapane, G.; Stangeland, A.B.H.; Sharma, N. Logistics 4.0 and emerging sustainable business models. Adv. Manuf. 2017, 5, 359–369. [Google Scholar] [CrossRef]

- Gürdür, D.; El-Khoury, J.; Törngren, M. Digitalizing Swedish industry: What is next? Data analytics readiness assessment of Swedish industry, according to survey results. Comput. Ind. 2019, 105, 153–163. [Google Scholar] [CrossRef]

- Burritt, R.L.; Herzig, C.; Schaltegger, S.; Viere, T. Diffusion of environmental management accounting for cleaner production: Evidence from some case studies. J. Clean. Prod. 2019, 224, 479–491. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research and Applications: Design and Methods, 6th ed.; SAGE: Los Angeles, CA, USA, 2018. [Google Scholar]

- Eisenhardt, K.M. Building Theories from Case Study Research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Public Sector Protocol. The Greenhouse Gas Protocol Initiative. A Corporate Accounting and Reporting Standard. 2008. Available online: https://ghgprotocol.org/public-sector-protocol-0 (accessed on 5 January 2021).

- Ji, G.; Gunasekaran, A.; Yang, G. Constructing sustainable supply chain under double environmental medium regulations. Int. J. Prod. Econ. 2014, 147, 211–219. [Google Scholar] [CrossRef]

- Centobelli, P.; Cerchione, R.; Esposito, E. Environmental sustainability in the service industry of transportation and logistics service providers: Systematic literature review and research directions. Transp. Res. Part D Transp. Environ. 2017, 53, 454–470. [Google Scholar] [CrossRef]

- Gong, M.; Gao, Y.; Koh, L.; Sutcliffe, C.; Cullen, J. The role of customer awareness in promoting firm sustainability and sustainable supply chain management. Int. J. Prod. Econ. 2019, 217, 88–96. [Google Scholar] [CrossRef]

- Strand, S.S. Pipelife Lanserer IoT-Løsninger for Rør og Kummer. Byggeindustrien. 2020. Available online: https://www.bygg.no/article/1430750 (accessed on 20 February 2021).

- Norsk Industri. Møbelfakta. 2021. Available online: https://www.norskindustri.no/kampanjesider/mobelfakta/mobelfakta/ (accessed on 24 March 2021).

- United Nations Global Compact. About the UN Global Compact. 2021. Available online: https://www.unglobalcompact.org/about (accessed on 29 March 2021).

- Norwegian Rooms. Digitalisering gir økt Konkurransekraft. 2018. Available online: https://www.norwegianrooms.no/nyheter1/digitalisering-gir-okt-konkurransekraft/ (accessed on 21 March 2021).

- Rosa, P.; Sassanelli, C.; Urbinati, A.; Chiaroni, D.; Terzi, S. Assessing relations between Circular Economy and Industry 4.0: A systematic literature review. Int. J. Prod. Res. 2020, 58, 1662–1687. [Google Scholar] [CrossRef] [Green Version]

- Burritt, R.; Schaltegger, S. Accounting towards sustainability in production and supply chains. Br. Account. Rev. 2014, 46, 327–343. [Google Scholar] [CrossRef]

- Frederico, G.F.; Garza-Reyes, J.A.; Anosike, A.; Kumar, V. Supply Chain 4.0: Concepts, maturity and research agenda. Supply Chain Manag. Int. J. 2019, 25, 262–282. [Google Scholar] [CrossRef]

- Dalenogare, L.S.; Benitez, G.B.; Ayala, N.F.; Frank, A.G. The expected contribution of Industry 4.0 technologies for industrial performance. Int. J. Prod. Econ. 2018, 204, 383–394. [Google Scholar] [CrossRef]

{kind=link}

| Company | Revenue NOK, Mill | Number of Employees | |

|---|---|---|---|

| Company A | Pipe manufacturer | 1079 | 276 |

| Company B | Furniture producer | 236 | 112 |

| Company C | Maritime equipment manufacturer | 1095 | 347 |

| Company D | Plastic products manufacturer | 74 | 31 |

| Company | Digital Technology: Implemented/in Planning Phase | How It Contributes to Sustainability Accounting and Reporting |

|---|---|---|

| Company A | Sensors for product lines—implemented. Installation of sensors is the first operation conducted for newly implemented product lines. It provides data on energy and material use in production. | Provides data that contribute to the general environmental profile with economic evaluation of a product at the manufacturing stage. |

| Machine learning—implemented. It processes data provided through sensors and directed to the optimization of product line processes, energy efficiency in production, more efficient material use, and general optimization of a product profile. | Provides data on improvement in production efficiency, environmental performance, and economic gains that in total can present changes gained during the taken period compared to the previous ones. | |

| 3D printing—implemented. Product development and improvement of product design that can reduce defects in manufacturing. | Not directly associated with sustainability accounting and reporting. | |

| Sensors and system—implemented, provide data on internal water and energy use. | Internal reporting requires these types of data. | |

| PIM and BIM databases—implemented. Collect and structure data for digitalized value chains. All data that include all physical, mechanical, hydraulic, and environmental information on a product are saved in the PIM database. Thus, the building company can easily access complete data regarding the whole building as well as data on a specific component. | Primarily for internal accounting and reporting that contains complete data on both the whole project or building and each specific component. | |

| Digital monitoring systems for pipes—implemented. With the help of small sensors mounted inside pipes combined with NB-IoT telecommunication technology, the information on water conditions, temperature, water level, and other data will be collected and sent to a Cloud platform. This remote monitoring control providew an opportunity for customers to have an early identification of problems. | Can potentially track data for sustainability accounting and reporting. | |

| Company B | Digitalization of product development—implemented. Joint digital platform based on 3D modeling accessible to employees responsible for each stage from design to final manufacturing. Reduces lead time. | Not directly associated with sustainability accounting and reporting. |

| Robotization and automation of manufacturing processes—implemented. Make production processes more effective. Planning of operations with painting robot reduces water wastage during processes. | Not directly associated with sustainability accounting but can be equipped with tools and programs for monitoring energy and material use, amount of waste. | |

| QR-codes—in planning phase. Directed toward tracing a product’s information along the lifespan supplemented by supplier information. | Can potentially store and provide data on supplier environmental and social performance. | |

| Machine learning—in planning phase. (a) Evaluates collected information on energy consumption for forecasting energy demand, and can manage energy usage, reducing it. (b) Facilitates the sorting of complex materials, separation of complex waste, improves recycling efficiency. | Machine learning monitors and collects information on energy consumption in production and recycling of materials. This information can be used for internal and external reporting. | |

| Company C | Sensors that provide data on product location and how the equipment were used during the lifespan—in planning phase. These data can be used for maintenance based on the conditions in which the equipment were used. At the end of the skip life cycle, the equipment can be detected and taken back to the producer to prolong its use through rebuilding, reusing, or recycling. | Sustainability accounting and reporting can be expanded using data on how the products are being treated during and at the end of the life cycle—for example, recyclability and reuse rates. |

| Sensors, RFID—in planning phase. This could provide more transparent data regarding suppliers, the company’s environmental performance, social, and ethical practices. The company plans to demand documentation regarding recyclability of components and detailed data on materials used. | Ability to expand sustainability accounting to the supply chain level by incorporating information regarding suppliers toward management practices at the end of the life cycle. | |

| Digitalized supply chain for maritime equipment—in planning phase. Provide an overview of all the components and materials that the product consists of, including various materials and electric and electronic components. Mapping of the components and elements can simplify the recycling process. | Ability to expand sustainability accounting to the supply chain level by incorporating information regarding product components, materials, and emissions. | |

| Company D | Blockchain technology for digitalized plastic supply chain—in planning phase. Tracking and storing information on plastic from cleanup to processing. Contribute to sustainable and circular production and consumption. | Provide data on reuse and recycling of plastic. |

| ERP systems—implemented. Allows tracking information on manufactured products. Each component is registered in the database with information on raw materials batch used for production, some of the parameters, and the date of production. | Allows tracking of basic parameters of raw materials that were used for production of components. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Klymenko, O.; Lillebrygfjeld Halse, L.; Jæger, B. The Enabling Role of Digital Technologies in Sustainability Accounting: Findings from Norwegian Manufacturing Companies. Systems 2021, 9, 33. https://doi.org/10.3390/systems9020033

Klymenko O, Lillebrygfjeld Halse L, Jæger B. The Enabling Role of Digital Technologies in Sustainability Accounting: Findings from Norwegian Manufacturing Companies. Systems. 2021; 9(2):33. https://doi.org/10.3390/systems9020033

Chicago/Turabian StyleKlymenko, Olena, Lise Lillebrygfjeld Halse, and Bjørn Jæger. 2021. "The Enabling Role of Digital Technologies in Sustainability Accounting: Findings from Norwegian Manufacturing Companies" Systems 9, no. 2: 33. https://doi.org/10.3390/systems9020033

APA StyleKlymenko, O., Lillebrygfjeld Halse, L., & Jæger, B. (2021). The Enabling Role of Digital Technologies in Sustainability Accounting: Findings from Norwegian Manufacturing Companies. Systems, 9(2), 33. https://doi.org/10.3390/systems9020033