Empirical Evidence on the Development and Digitalization of the Accounting and Finance Profession in Europe

,

,  ,

,  , and

, and

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Data Collection

- European associations: Accountancy Europe, CFE Tax Advisers Europe, European Federation of Financial Analysts Society (EFFAS), European Accounting Association (EAA), European Confederation of Institutes of Internal Auditing (ECIIA), European Group of Valuers’ Associations (TEGOVA), the European Association of Corporate Treasurers (EACT), the Federation of European Risk Management Associations (FERMA), the European Organization of Supreme Audit Institutions (EUROSAI).

- International federations: International Federation of Accountants (IFAC) Global Impact Map, International Forum of Independent Audit Regulators (IFIAR), Global Accounting Alliance (GAA), International Association of Restructuring, Insolvency & Bankruptcy Professionals (INSOL), International Organization of Supreme Audit Institutions (INTOSAI), International Group of Treasury Associations (IGTA), Chartered Global Management Accountant (CGMA).

- The services provided by accounting professionals to other stakeholders, especially their clients (accounting services); and

- The services and benefits provided by accounting associations to their members (professional membership services).

3.2. Proposed Indicators for the Comparative Analysis

3.3. Group Analysis on Country Classifications

3.4. Regression Analysis: Model and Procedure

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

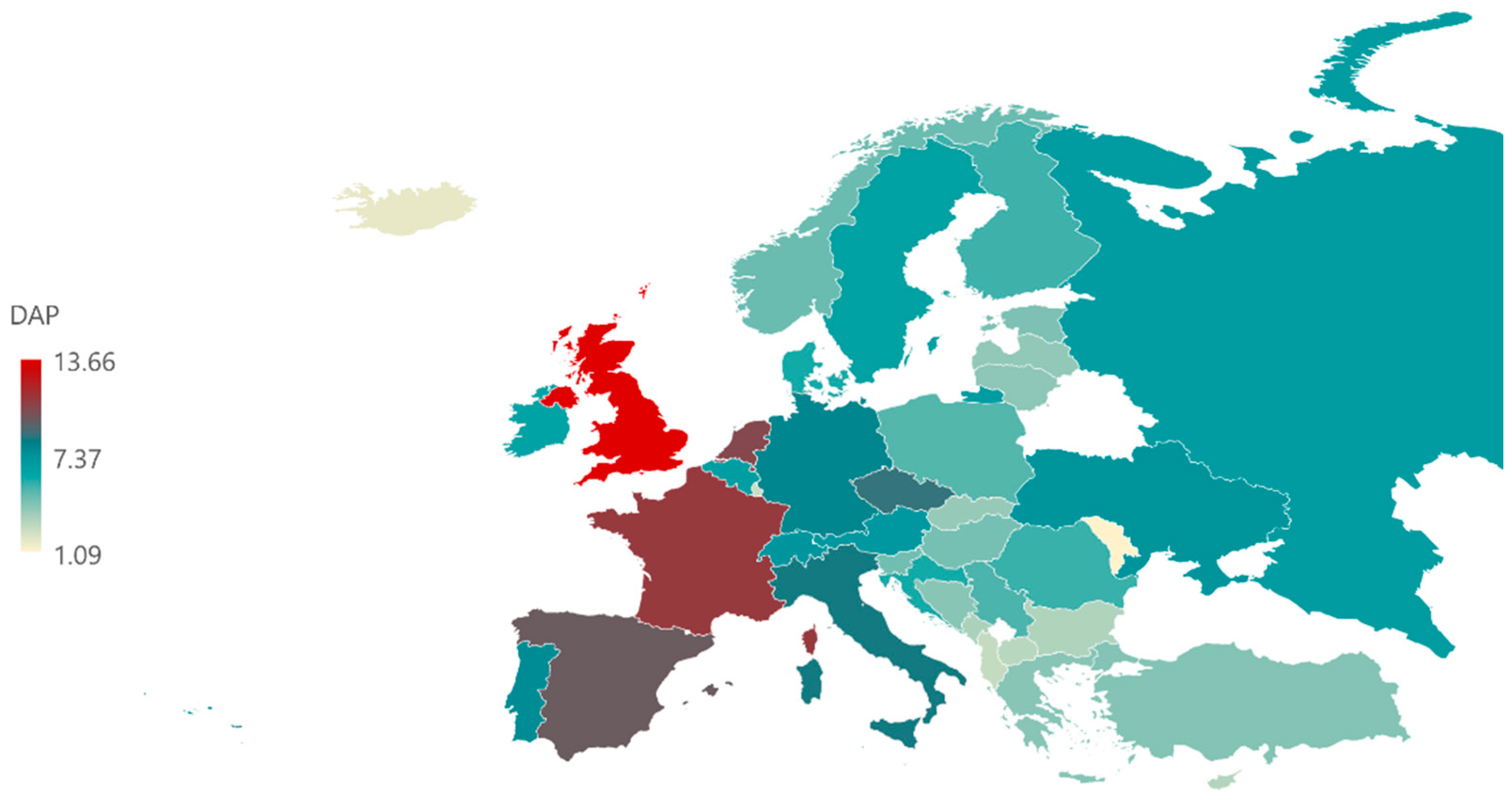

| Country | orgcount | Totalserv | CAS | EMB | DAP | Region | GCI | WBCa |

|---|---|---|---|---|---|---|---|---|

| Albania | 5 | 9 | 0.45 | 2.21 | 2.66 | Southern | 57.6 | M |

| Austria | 11 | 32 | 2.62 | 4.43 | 7.05 | Central | 76.6 | H |

| Belgium | 10 | 29 | 2.76 | 3.93 | 6.68 | Western | 76.4 | H |

| Bosnia and Herzegovina | 6 | 14 | 0.82 | 3.29 | 4.10 | Southern | 54.7 | M |

| Bulgaria | 6 | 14 | 1.17 | 2.00 | 3.17 | Southern | 64.9 | M |

| Croatia | 7 | 26 | 2.79 | 3.07 | 5.86 | Southern | 61.9 | H |

| Cyprus | 5 | 13 | 1.30 | 1.79 | 3.09 | Southern | 66.4 | H |

| Denmark | 7 | 25 | 2.68 | 3.21 | 5.89 | Northern | 81.2 | H |

| Estonia | 5 | 18 | 1.98 | 2.36 | 4.34 | Eastern | 70.9 | H |

| Finland | 8 | 26 | 2.28 | 3.14 | 5.42 | Northern | 80.2 | H |

| France | 21 | 42 | 1.80 | 9.21 | 11.01 | Western | 78.8 | H |

| Germany | 13 | 35 | 2.15 | 5.79 | 7.94 | Central | 81.8 | H |

| Greece | 7 | 16 | 1.37 | 2.71 | 4.09 | Southern | 62.6 | H |

| Hungary | 6 | 22 | 2.02 | 2.43 | 4.45 | Central | 65.1 | H |

| Iceland | 3 | 6 | 0.50 | 1.29 | 1.79 | Northern | 74.7 | H |

| Ireland | 10 | 24 | 1.68 | 4.64 | 6.32 | Western | 75.1 | H |

| Italy | 14 | 43 | 2.92 | 5.50 | 8.42 | Southern | 71.5 | H |

| Latvia | 6 | 15 | 1.25 | 2.64 | 3.89 | Eastern | 67.0 | H |

| Lithuania | 8 | 14 | 0.79 | 3.21 | 4.00 | Eastern | 68.4 | H |

| Luxembourg | 6 | 8 | 0.47 | 2.07 | 2.54 | Western | 77.0 | H |

| Malta | 5 | 8 | 0.48 | 1.86 | 2.34 | Southern | 68.5 | H |

| Montenegro | 6 | 14 | 0.70 | 2.57 | 3.27 | Southern | 60.8 | M |

| North Macedonia | 5 | 11 | 0.88 | 2.07 | 2.95 | Southern | 57.3 | M |

| Norway | 7 | 23 | 2.14 | 2.57 | 4.71 | Northern | 78.1 | H |

| Poland | 8 | 16 | 1.10 | 4.00 | 5.10 | Central | 68.9 | H |

| Portugal | 12 | 30 | 1.88 | 5.79 | 7.66 | Southern | 70.4 | H |

| Rep. of Moldova | 2 | 4 | 0.30 | 0.79 | 1.09 | Eastern | 56.7 | M |

| Romania | 10 | 18 | 0.33 | 5.14 | 5.48 | Southern | 64.4 | M |

| Russia | 13 | 24 | 1.20 | 5.57 | 6.77 | Eastern | 66.7 | M |

| Serbia | 5 | 20 | 2.40 | 2.86 | 5.26 | Southern | 60.9 | M |

| Slovakia | 6 | 14 | 1.05 | 2.71 | 3.76 | Central | 66.8 | H |

| Slovenia | 7 | 18 | 1.54 | 3.00 | 4.54 | Central | 70.2 | H |

| Spain | 15 | 47 | 2.98 | 6.79 | 9.76 | Southern | 75.3 | H |

| Sweden | 8 | 30 | 2.63 | 3.93 | 6.55 | Northern | 81.2 | H |

| Switzerland | 8 | 36 | 3.60 | 3.64 | 7.24 | Central | 82.3 | H |

| The Czech Rep. | 11 | 42 | 3.05 | 5.64 | 8.70 | Central | 70.9 | H |

| The Netherlands | 16 | 41 | 2.18 | 8.29 | 10.46 | Western | 82.4 | H |

| Turkey | 6 | 17 | 1.70 | 2.50 | 4.20 | Southern | 62.1 | M |

| U.K. | 15 | 61 | 3.66 | 10.00 | 13.66 | Western | 81.2 | H |

| Ukraine | 8 | 32 | 2.40 | 4.93 | 7.33 | Eastern | 57.0 | M |

References

- Anderson-Gough, F.; Grey, C.; Robson, K. Accounting Professionals and the Accounting Profession: Linking Conduct and Context. Account. Bus. Res. 2002, 32, 41–56. [Google Scholar] [CrossRef]

- Buchheit, S.; Dalton, D.W.; Harp, N.L.; Hollingsworth, C.W. A Contemporary Analysis of Accounting Professionals’ Work-Life Balance. Account. Horiz. 2016, 30, 41–62. [Google Scholar] [CrossRef]

- De Loo, I.; Verstegen, B.; Swagerman, D. Understanding the Roles of Management Accountants. Eur. Bus. Rev. 2011, 23, 287–313. [Google Scholar] [CrossRef]

- Bancel, F.; Mittoo, U.R. The Gap between the Theory and Practice of Corporate Valuation: Survey of European Experts. J. Appl. Corp. Financ. 2014, 26, 106–117. [Google Scholar] [CrossRef]

- COSO. Enterprise Risk Management. Integrating with Strategy and Performance; Committee of Sponsoring Organizations of the Treadway Commission: Nashville, TN, USA, 2017. [Google Scholar]

- Duff, A.; Hancock, P.; Marriott, N. The Role and Impact of Professional Accountancy Associations on Accounting Education Research: An International Study. Br. Account. Rev. 2020, 52, 100829. [Google Scholar] [CrossRef]

- Nerland, M.; Karseth, B. The Knowledge Work of Professional Associations: Approaches to Standardisation and Forms of Legitimisation. J. Educ. Work. 2015, 28, 1–23. [Google Scholar] [CrossRef]

- Greenwood, R.; Suddaby, R.; Hinings, C.R. Theorizing Change: The Role of Professional Associations in the Transformation of Institutionalized Fields. Acad. Manag. J. 2002, 45, 58–80. [Google Scholar] [CrossRef]

- Hopper, T.; Lassou, P.; Soobaroyen, T. Globalisation, Accounting and Developing Countries. Crit. Perspect. Account. 2017, 43, 125–148. [Google Scholar] [CrossRef]

- Polzer, T.; Grossi, G.; Reichard, C. Implementation of the International Public Sector Accounting Standards in Europe. Variations on a Global Theme. Account. Forum 2022, 46, 57–82. [Google Scholar] [CrossRef]

- Carter, D.P.; Mahallati, N. Coordinating Intermediaries: The Prospects and Limitations of Professional Associations in Decentralized Regulation. Regul. Gov. 2019, 13, 51–69. [Google Scholar] [CrossRef]

- Fraser, K.; Sheehy, B. Abundant Publications but Minuscule Impact: The Irrelevance of Academic Accounting Research on Practice and the Profession. Publications 2020, 8, 46. [Google Scholar] [CrossRef]

- Baker, C.R. A Comparative Analysis of the Development of the Auditing Profession in the United Kingdom and France. Account. Hist. 2014, 19, 97–114. [Google Scholar] [CrossRef]

- Ionescu-Feleagă, L.; Ionescu, B.-Ș.; Stoica, O.C. The Impact of Digitalization on Happiness: A European Perspective. Mathematics 2022, 10, 2766. [Google Scholar] [CrossRef]

- Dimitriu, O.; Matei, M. A New Paradigm for Accounting through Cloud Computing. Procedia Econ. Financ. 2014, 15, 840–846. [Google Scholar] [CrossRef]

- Kokina, J.; Blanchette, S. Early Evidence of Digital Labor in Accounting: Innovation with Robotic Process Automation. Int. J. Account. Inf. Syst. 2019, 35, 100431. [Google Scholar] [CrossRef]

- Brouard, F.; Bujaki, M.; Durocher, S.; Neilson, L.C. Professional Accountants’ Identity Formation: An Integrative Framework. J. Bus. Ethics 2017, 142, 225–238. [Google Scholar] [CrossRef]

- Carnegie, G.D.; Napier, C.J. Traditional Accountants and Business Professionals: Portraying the Accounting Profession after Enron. Account. Organ. Soc. 2010, 35, 360–376. [Google Scholar] [CrossRef]

- Tiron Tudor, A. Balancing the Public and the Private Interest—A Dilemma of Accounting Profession. Procedia Soc. Behav. Sci. 2013, 92, 930–935. [Google Scholar] [CrossRef] [Green Version]

- Ferry, L.; Ahrens, T. Using Management Control to Understand Public Sector Corporate Governance Changes: Localism, Public Interest, and Enabling Control in an English Local Authority. J. Addict. Offender Couns. 2017, 13, 548–567. [Google Scholar] [CrossRef] [Green Version]

- Adams, T.L. Professional Self-Regulation and the Public Interest in Canada. Prof. Prof. 2016, 6. [Google Scholar] [CrossRef]

- Fogarty, T.; Jones, D.A. Between a Rock and a Hard Place: How Tax Practitioners Straddle Client Advocacy and Professional Responsibilities. Qual. Res. Account. Manag. 2014, 11, 286–316. [Google Scholar] [CrossRef]

- Roussy, M. Internal Auditors’ Roles: From Watchdogs to Helpers and Protectors of the Top Manager. Crit. Perspect. Account. 2013, 24, 550–571. [Google Scholar] [CrossRef]

- Andreassen, R.-I. Digital Technology and Changing Roles: A Management Accountant’s Dream or Nightmare? J. Manag. Control 2020, 31, 209–238. [Google Scholar] [CrossRef]

- IFAC. IFAC Global Impact Map. Available online: https://www.ifac.org/what-we-do/global-impact-map/country-profiles (accessed on 1 December 2021).

- Stanciu, V.; Rîndașu, S.-M. The Impact of General Data Protection Regulation in the Accounting Profession—Evidences from Romania. J. Int. Acad. Case Stud. 2018, 2018, 1–9. [Google Scholar] [CrossRef]

- Thornburg, S.; Roberts, R.W. In Whose Interest? A Critical Examination of Public Interest Appeals Made by the Public Accounting Profession in the USA. Int. J. Comput. Appl. 2013, 5, 81. [Google Scholar] [CrossRef]

- Huber, W.D. Should the Forensic Accounting Profession Be Regulated? Res. Account. Regul. 2013, 25, 123–132. [Google Scholar] [CrossRef]

- Canning, M.; O’Dwyer, B. Professional Accounting Bodies’ Disciplinary Procedures: Accountable, Transparent and in the Public Interest? Eur. Account. Rev. 2001, 10, 725–749. [Google Scholar] [CrossRef]

- Loscher, G.; Löhlein, L.; Lenz, H. Dual Roles and Blurred Identities: A Framing Contest between Professional Associations in a Local Strategic Action Field. Eur. Account. Rev. 2021, 30, 503–529. [Google Scholar] [CrossRef]

- Del Baldo, M.; Tiron-Tudor, A.; Faragalla, W. Women’s Role in the Accounting Profession: A Comparative Study between Italy and Romania. Adm. Sci. 2018, 9, 2. [Google Scholar] [CrossRef] [Green Version]

- Albu, N.; Albu, C.N.; Gray, S.J. Institutional Factors and the Impact of International Financial Reporting Standards: The Central and Eastern European Experience. Account. Forum 2020, 44, 184–214. [Google Scholar] [CrossRef]

- Markova, G.; Ford, R.C.; Dickson, D.R.; Bohn, T.M. Professional Associations and Members’ Benefits: What’s in It for Me? Nonprofit Manag. Leadersh. 2013, 23, 491–510. [Google Scholar] [CrossRef]

- Robertson, J.C.; Houston, R.W. Investors’ Expectations of the Improvement in the Credibility of Audit Opinions Following PCAOB Inspection Reports with Identified Deficiencies. Account. Public Interest 2010, 10, 36–56. [Google Scholar] [CrossRef]

- Feleagă, L.; Dragomir, V.D.; Feleagă, N. National Accounting Culture and Empirical Evidence on the Application of Conservatism. Econ. Comput. Econ. Cybern. Stud. Res. 2010, 44, 43–60. [Google Scholar]

- Velayutham, S. The Accounting Profession’s Code of Ethics: Is It a Code of Ethics or a Code of Quality Assurance? Crit. Perspect. Account. 2003, 14, 483–503. [Google Scholar] [CrossRef]

- Curtis, M.B.; Taylor, E.Z. Whistleblowing in Public Accounting: Influence of Identity Disclosure, Situational Context, and Personal Characteristics. Account. Public Interest 2009, 9, 191–220. [Google Scholar] [CrossRef]

- Clements, C.E.; Neill, J.D.; Stovall, O.S. The Impact of Cultural Differences on the Convergence of International Accounting Codes of Ethics. J. Bus. Ethics 2009, 90, 383–391. [Google Scholar] [CrossRef]

- Spence, C.; Carter, C. An Exploration of the Professional Habitus in the Big 4 Accounting Firms. Work. Employ. Soc. 2014, 28, 946–962. [Google Scholar] [CrossRef] [Green Version]

- Coram, P.J.; Robinson, M.J. Professionalism and Performance Incentives in Accounting Firms. Account. Horiz. 2017, 31, 103–123. [Google Scholar] [CrossRef]

- Shafer, W.E.; Poon, M.C.C.; Tjosvold, D. An Investigation of Ethical Climate in a Singaporean Accounting Firm. Account. Audit. Account. J. 2013, 26, 312–343. [Google Scholar] [CrossRef] [Green Version]

- Bobek, D.D.; Hageman, A.M.; Radtke, R.R. The Influence of Roles and Organizational Fit on Accounting Professionals’ Perceptions of Their Firms’ Ethical Environment. J. Bus. Ethics 2015, 126, 125–141. [Google Scholar] [CrossRef]

- Richardson, A. The Accountancy Profession. In The Routledge Companion to Critical Accounting; Roslender, R., Ed.; Routledge: New York, NY, USA, 2018. [Google Scholar]

- Kavanagh, M.H.; Drennan, L. What Skills and Attributes Does an Accounting Graduate Need? Evidence from Student Perceptions and Employer Expectations. Account. Financ. 2008, 48, 279–300. [Google Scholar] [CrossRef]

- Marais, E.; Nel, C.; du Toit, C. Guidelines for the Development of a Professional Development Programme in Accordance with a Workshop, Support and Mentorship Model (WSM-Model). Tydskr. Geesteswet. 2015, 55, 75–91. [Google Scholar] [CrossRef] [Green Version]

- Paisey, C.; Paisey, N.J. Protecting the Public Interest? Continuing Professional Development Policies and Role-Profession Conflict in Accountancy. Crit. Perspect. Account. 2020, 67–68, 102040. [Google Scholar] [CrossRef]

- Kaspina, R. Continuing Professional Development of Accounting and Auditing: Russian Experience and Challenges. Procedia Soc. Behav. Sci. 2015, 191, 550–553. [Google Scholar] [CrossRef] [Green Version]

- Sucháček, J.; Koutský, J.; del Río, L.C.L.; Seďa, P. Econometric Analysis of Integration of Selected New EU Member CEE Stock Markets with Global Stock Market and Eurozone: Impact of Global Financial Crisis. Amfiteatru Econ. 2021, 23, 824–842. [Google Scholar] [CrossRef]

- Murphy, B. Professional Competence and Continuing Professional Development in Accounting: Professional Practice vs. Non-Practice. Account. Educ. 2017, 26, 482–500. [Google Scholar] [CrossRef]

- Bonzanini, O.A.; Silva, A.; Cokins, G.; Gonçalves, M.J. The Interaction between Higher Education Institutions and Professional Bodies in the Context of Digital Transformation: The Case of Brazilian Accountants. Educ. Sci. 2020, 10, 321. [Google Scholar] [CrossRef]

- Almasan, A.; Circa, C.; Dumitru, M.; Guse, R.G.; Mangiuc, D.M. Effects of Integrated Reporting on Corporate Disclosure Practices Regarding the Capitals and Performance. Amfiteatru Econ. 2019, 21, 572–589. [Google Scholar] [CrossRef]

- Dumitru, M.; Dyduch, J.; Gușe, R.-G.; Krasodomska, J. Corporate Reporting Practices in Poland and Romania—An Ex-Ante Study to the New Non-Financial Reporting European Directive. Account. Eur. 2017, 14, 279–304. [Google Scholar] [CrossRef]

- Dragomir, V.-D.; Dumitru, M.; Feleaga, L. The Predictors of Non-Financial Reporting Quality in Romanian State-Owned Enterprises. Account. Eur. 2022, 19, 1–42. [Google Scholar] [CrossRef]

- Pizzi, S.; Rosati, F.; Venturelli, A. The Determinants of Business Contribution to the 2030 Agenda: Introducing the SDG Reporting Score. Bus. Strat. Environ. 2021, 30, 404–421. [Google Scholar] [CrossRef]

- Hoppe, T.; Schanz, D.; Sturm, S.; Sureth-Sloane, C. The Tax Complexity Index—A Survey-Based Country Measure of Tax Code and Framework Complexity. Eur. Account. Rev. 2021, 1–35. [Google Scholar] [CrossRef]

- Campopiano, G.; De Massis, A. Corporate Social Responsibility Reporting: A Content Analysis in Family and Non-Family Firms. J. Bus. Ethics 2015, 129, 511–534. [Google Scholar] [CrossRef]

- Steenkamp, N.; Northcott, D. Content Analysis in Accounting Research: The Practical Challenges. Aust. Account. Rev. 2007, 17, 12–25. [Google Scholar] [CrossRef]

- Neuman, W.L. Social Research Methods: Qualitative and Quantitative Approaches, 7th ed.; Pearson Education Limited: Harlow, UK, 2014. [Google Scholar]

- Guthrie, J.; Petty, R.; Yongvanich, K.; Ricceri, F. Using Content Analysis as a Research Method to Inquire into Intellectual Capital Reporting. J. Intellect. Cap. 2004, 5, 282–293. [Google Scholar] [CrossRef]

- Worldometer How Many Countries in Europe? 2021. Available online: https://www.worldometers.info/geography/how-many-countries-in-europe/ (accessed on 1 January 2022).

- CIA The World Factbook. Available online: https://www.cia.gov/the-world-factbook/ (accessed on 1 January 2022).

- Bătae, O.M.; Dragomir, V.D.; Feleagă, L. Environmental, Social, Governance (ESG), and Financial Performance of European Banks. J. Account. Manag. Inf. Syst. 2020, 19, 480–501. [Google Scholar] [CrossRef]

- World Bank New World Bank Country Classifications by Income Level. 2022. Available online: https://blogs.worldbank.org/opendata/new-world-bank-country-classifications-income-level-2021-2022 (accessed on 1 January 2022).

- Harvard Growth Lab The Atlas of Economic Complexity. Available online: https://atlas.cid.harvard.edu/ (accessed on 1 August 2021).

- Schwab, K. The Global Competitiveness Report; World Economic Forum: Geneva, Switzerland, 2019. [Google Scholar]

- IMD. World Digital Competitiveness Ranking 2022; IMD World Competitiveness Center (WCC): Lausanne, Switzerland, 2022. [Google Scholar]

- Botzem, S.; Quack, S. (No) Limits to Anglo-American Accounting? Reconstructing the History of the International Accounting Standards Committee: A Review Article. Account. Organ. Soc. 2009, 34, 988–998. [Google Scholar] [CrossRef] [Green Version]

- Boikova, T.; Zeverte-Rivza, S.; Rivza, P.; Rivza, B. The Determinants and Effects of Competitiveness: The Role of Digitalization in the European Economies. Sustainability 2021, 13, 11689. [Google Scholar] [CrossRef]

- Schoenfeld, J.; Segal, G.; Borgia, D. Social Cognitive Career Theory and the Goal of Becoming a Certified Public Accountant. Account. Educ. 2017, 26, 109–126. [Google Scholar] [CrossRef]

- Kwilinski, A.; Vyshnevskyi, O.; Dzwigol, H. Digitalization of the EU Economies and People at Risk of Poverty or Social Exclusion. J. Risk Financ. Manag. 2020, 13, 142. [Google Scholar] [CrossRef]

- Hopper, T. Making Accounting Degrees Fit for a University. Crit. Perspect. Account. 2013, 24, 127–135. [Google Scholar] [CrossRef]

- Brown, P.; Preiato, J.; Tarca, A. Measuring Country Differences in Enforcement of Accounting Standards: An Audit and Enforcement Proxy. J. Bus. Financ. Account. 2014, 41, 1–52. [Google Scholar] [CrossRef]

- Harakeh, M.; Lee, E.; Walker, M. The Differential Impact of IFRS Adoption on Aspects of Seasoned Equity Offerings in the UK and France. Account. Eur. 2019, 16, 106–138. [Google Scholar] [CrossRef]

- Howcroft, D. Graduates’ Vocational Skills for the Management Accountancy Profession: Exploring the Accounting Education Expectation-Performance Gap. Account. Educ. 2017, 26, 459–481. [Google Scholar] [CrossRef]

- Bayerlein, L.; Timpson, M. Do Accredited Undergraduate Accounting Programmes in Australia Meet the Needs and Expectations of the Accounting Profession? Educ. Train. 2017, 59, 305–322. [Google Scholar] [CrossRef]

- Dima, A.; Begu, L.; Vasilescu, M.; Maassen, M. The Relationship between the Knowledge Economy and Global Competitiveness in the European Union. Sustainability 2018, 10, 1706. [Google Scholar] [CrossRef] [Green Version]

- Kitsantas, T.; Chytis, E. Blockchain Technology as an Ecosystem: Trends and Perspectives in Accounting and Management. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 1143–1161. [Google Scholar] [CrossRef]

- Huang, F.; No, W.G.; Vasarhelyi, M.A.; Yan, Z. Audit Data Analytics, Machine Learning, and Full Population Testing. J. Financ. Data Sci. 2022, 8, 138–144. [Google Scholar] [CrossRef]

- European Commission. The Digital Economy and Society Index (DESI). In Shaping Europe’s Digital Future; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- Polak, P.; Nelischer, C.; Guo, H.; Robertson, D.C. “Intelligent” Finance and Treasury Management: What We Can Expect. AI Soc. 2020, 35, 715–726. [Google Scholar] [CrossRef]

- Delgado, F.J. On the Determinants of Fiscal Decentralization: Evidence From the EU. Amfiteatru Econ. 2021, 23, 206–220. [Google Scholar] [CrossRef]

- OECD. Tax Administration 2021: Comparative Information on OECD and Other Advanced and Emerging Economies; OECD: Paris, France, 2021; ISBN 978-92-64-87076-5. [Google Scholar]

- IFAC. International Education Standards, 2019th ed.; International Federation of Accountants: New York, NY, USA, 2019; ISBN 978-1-60815-427-2. [Google Scholar]

- Alshurafat, H.; Al Shbail, M.O.; Mansour, E. Strengths and Weaknesses of Forensic Accounting: An Implication on the Socio-Economic Development. JBSED 2021, 1, 135–148. [Google Scholar] [CrossRef]

- IAASB. A Framework for Audit Quality. Key Elements That Create an Environment for Audit Quality; International Auditing and Assurance Standards Board: New York, NY, USA, 2014. [Google Scholar]

- Kleinman, G.; Lin, B.B.; Palmon, D. Audit Quality: A Cross-National Comparison of Audit Regulatory Regimes. J. Account. Audit. Financ. 2014, 29, 61–87. [Google Scholar] [CrossRef]

- ACFE. Report to the Nations. 2020 Global Study on Occupational Fraud and Abuse; Association of Certified Fraud Examiners: Austin, TX, USA, 2020. [Google Scholar]

| Abbreviation | Indicator | Source |

|---|---|---|

| orgcount | Total number of professional associations in European countries | Authors’ calculation |

| accserv | Total number of accounting services in European countries | Authors’ calculation |

| ASC | The degree of accounting service coverage | Authors’ calculation |

| PCO | The degree of overlap in professional coverage | Authors’ calculation |

| CAS | The complexity of accounting services | Authors’ calculation |

| MSC | The membership service coverage | Authors’ calculation |

| EMB | The extent of membership benefit and services | Authors’ calculation |

| APM | The average provision of membership services and benefits | Authors’ calculation |

| DAP | The development of the accounting profession in a country | Authors’ calculation |

| Region | The region from Europe where the country belongs | The CIA World Factbook |

| Gdppc | Real GDP per capita (2019) in USD | The CIA World Factbook |

| Pop | Population as of July 2021 | The CIA World Factbook |

| GCI | The Global Competitiveness Index 4.0 2019 | World Economic Forum |

| ECI | Economic Complexity Index (Country complexity ranking) | Harvard University |

| WDCR | World Digital Competitiveness Ranking 2022 | IMD.org |

| WBC | World Bank country classification by income (1 for high-income countries, 0 for middle-income countries) | World Bank |

| EUR | The currency of the country (1 if EUR, 0 otherwise) | The CIA World Factbook |

| Type of Professional Services | Minimum Number per Countries | Maximum Number per Countries | Number of Countries Having This Service | Number of Associations Regulating This Service |

|---|---|---|---|---|

| Accounting and financial reporting | 1 | 7 | 40 | 196 |

| External audit | 1 | 8 | 40 | 260 |

| Tax accounting | 0 | 6 | 29 | 112 |

| Treasury management | 0 | 2 | 22 | 57 |

| Financial analysis | 0 | 5 | 21 | 90 |

| Financial consultancy | 0 | 7 | 30 | 131 |

| Management accounting | 0 | 4 | 16 | 41 |

| Internal audit | 0 | 3 | 36 | 104 |

| Controlling | 0 | 5 | 28 | 96 |

| Risk management | 0 | 2 | 25 | 57 |

| Compliance and corporate governance | 0 | 5 | 25 | 90 |

| Real estate valuation | 0 | 8 | 32 | 132 |

| Accounting for restructuring, mergers, acquisitions, or insolvency | 0 | 3 | 14 | 45 |

| Mediation | 0 | 3 | 8 | 21 |

| Information systems audit and assurance | 0 | 2 | 19 | 50 |

| Forensic accounting and court testimonies | 0 | 2 | 22 | 52 |

| Public sector accounting and auditing | 1 | 4 | 40 | 135 |

| Asset management | 0 | 2 | 8 | 20 |

| Accounting education | 0 | 6 | 17 | 65 |

| Non-financial communication and integrated reporting | 0 | 4 | 17 | 77 |

| Membership Services and Benefits | Total Number in Europe | Minimum Number/Country | Maximum Number/Country | Average Number of Membership Services/Country |

|---|---|---|---|---|

| Public registry | 183 | 1 | 13 | 4.58 |

| Training | 232 | 1 | 16 | 5.80 |

| Apprenticeship | 90 | 0 | 8 | 2.25 |

| Exams | 172 | 1 | 14 | 4.30 |

| Standard-setting | 129 | 0 | 8 | 3.23 |

| Quality control | 199 | 2 | 12 | 4.98 |

| Legal protection | 63 | 0 | 8 | 1.58 |

| Technical support | 221 | 0 | 14 | 5.53 |

| Research | 141 | 0 | 12 | 3.53 |

| Forum | 211 | 0 | 19 | 5.28 |

| Digitalization | 70 | 0 | 10 | 1.75 |

| Job market | 77 | 0 | 11 | 1.93 |

| Collaboration | 269 | 2 | 13 | 6.73 |

| Other benefits | 93 | 0 | 8 | 2.33 |

| TOTAL | 2150 | - | - | - |

| Indicator | Count | Mean | SD | Min. (Country) | Max. (Country) |

|---|---|---|---|---|---|

| orgcount | 40 | 8.43 | 3.95 | 2.00 | 21.00 (France) |

| accserv | 40 | 23.43 | 12.73 | 4.00 | 61.00 (U.K.) |

| ASC | 40 | 0.61 | 0.21 | 0.15 | 0.95 |

| PCO | 40 | 2.72 | 0.86 | 0.56 | 4.50 (Switzerland) |

| CAS | 40 | 1.75 | 0.94 | 0.30 | 3.66 (U.K.) |

| MSC | 40 | 0.88 | 0.13 | 0.57 | 1.00 |

| EMB | 40 | 3.84 | 2.08 | 0.79 | 10.00 (U.K.) |

| APM | 40 | 0.45 | 0.07 | 0.33 | 0.67 (U.K.) |

| DAP | 40 | 5.59 | 2.70 | 1.09 | 13.66 (U.K.) |

| gdppc | 40 | 40,586.00 | 20,429.95 | 12,810.00 | 113,900.00 (Luxembourg) |

| population | 40 | 20,500,652 | 30,869,445 | 354,234 | 142,320,790 (Russia) |

| GCI | 40 | 69.87 | 8.25 | 54.70 | 82.40 (The Netherlands) |

| ECI | 36 | 0.98 | 0.63 | −0.44 | 2.13 (Switzerland) |

| WDCR | 31 | 69.83 | 15.86 | 44.36 | 100 (Denmark) |

| Indicator | orgcount | TotalServ | ASC | PCO | CAS | MSC | EMB | APM | DAP | gdppc | pop | GCI | ECI | WDCR |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| orgcount | 1 | |||||||||||||

| accserv | 0.83 ** | 1 | ||||||||||||

| ASC | 0.79 ** | 0.89 ** | 1 | |||||||||||

| PCO | 0.07 | 0.56 ** | 0.50 ** | 1 | ||||||||||

| CAS | 0.49 ** | 0.85 ** | 0.85 ** | 0.87 ** | 1 | |||||||||

| MSC | 0.63 ** | 0.65 ** | 0.75 ** | 0.33 * | 0.60 ** | 1 | ||||||||

| EMB | 0.95 ** | 0.88 ** | 0.74 ** | 0.17 | 0.52 ** | 0.63 ** | 1 | |||||||

| APM | 0.28 | 0.48 ** | 0.24 | 0.38 * | 0.36 * | 0.33 * | 0.55 ** | 1 | ||||||

| DAP | 0.90 ** | 0.97 ** | 0.87 ** | 0.43 ** | 0.75 ** | 0.69 ** | 0.96 ** | 0.55 ** | 1 | |||||

| gdppc | 0.23 | 0.21 | 0.30 | 0.03 | 0.23 | 0.38 * | 0.15 | −0.22 | 0.20 | 1 | ||||

| population | 0.59 ** | 0.46 ** | 0.40 ** | 0 | 0.21 | 0.43 ** | 0.57 ** | 0.20 | 0.51 ** | −0.09 | 1 | |||

| GCI | 0.53 ** | 0.57 ** | 0.62 ** | 0.27 | 0.54 ** | 0.55 ** | 0.47 ** | −0.02 | 0.55 ** | 0.78 ** | 0.12 | 1 | ||

| ECI | 0.39 * | 0.56 ** | 0.62 ** | 0.40 * | 0.59 ** | 0.52 ** | 0.39 * | 0.17 | 0.51 ** | 0.64 ** | 0.02 | 0.70 ** | 1 | |

| WDCR | 0.16 | 0.35 | 0.32 | 0.43 * | 0.46 ** | 0.28 | 0.19 | 0.23 | 0.31 | 0.51 ** | −0.09 | 0.86 ** | 0.37 | 1 |

| Indicator | High Income (n = 29) | Middle Income (n = 11) | df | t | p | Cohen’s d | ||

|---|---|---|---|---|---|---|---|---|

| M | SD | M | SD | |||||

| orgcount | 9.14 | 4.10 | 6.55 | 2.91 | 25.51 | 2.23 * | 0.035 | 0.73 |

| accserv | 26.21 | 13.27 | 16.09 | 7.56 | 31.63 | 3.01 ** | 0.005 | 0.94 |

| ASC | 0.67 | 0.20 | 0.45 | 0.17 | 20.90 | 3.38 ** | 0.003 | 1.19 |

| PCO | 2.84 | 0.79 | 2.39 | 0.98 | 15.21 | 1.38 | 0.187 | 0.51 |

| CAS | 1.99 | 0.90 | 1.12 | 0.75 | 21.49 | 3.06 ** | 0.006 | 1.05 |

| MSC | 0.91 | 0.10 | 0.79 | 0.15 | 13.42 | 2.47 * | 0.028 | 0.94 |

| EMB | 4.13 | 2.22 | 3.08 | 1.51 | 26.70 | 1.70 | 0.101 | 0.55 |

| APM | 0.44 | 0.06 | 0.46 | 0.87 | 14.34 | −0.85 | 0.411 | 0.03 |

| DAP | 6.11 | 2.80 | 4.21 | 1.86 | 27.32 | 2.49 * | 0.019 | 0.80 |

| gdppc | 48,411.66 | 18,332.60 | 19,954.73 | 6398.79 | 37.92 | 7.27 *** | 0.001 | 2.07 |

| pop | 17,357,956 | 23,662,661 | 28,785,942 | 45.215,765 | 12.14 | −0.80 | 0.440 | 0.32 |

| GCI | 73.51 | 6.29 | 60.28 | 3.93 | 29.07 | 7.96 *** | 0.001 | 2.52 |

| ECI | 1.21 | 0.52 | 0.37 | 0.49 | 17.35 | 4.54 *** | 0.001 | 1.66 |

| Indicator | Eurozone (n = 19) | Non-Eurozone (n = 21) Base Category | df | t | p | Cohen’s d | ||

|---|---|---|---|---|---|---|---|---|

| M | SD | M | SD | |||||

| orgcount | 9.74 | 4.47 | 7.24 | 3.05 | 31.33 | 2.04 * | 0.049 | 0.65 |

| accserv | 24.89 | 12.45 | 22.10 | 13.14 | 37.91 | 0.69 | 0.493 | 0.22 |

| ASC | 0.67 | 0.21 | 0.56 | 0.21 | 37.30 | 1.42 | 0.094 | 0.52 |

| PCO | 2.53 | 0.57 | 2.88 | 1.04 | 31.82 | −1.38 | 0.178 | 0.42 |

| CAS | 1.76 | 0.77 | 1.74 | 1.09 | 35.98 | 0.08 | 0.939 | 0.02 |

| MSC | 0.91 | 0.10 | 0.85 | 0.15 | 34.43 | 1.51 | 0.140 | 0.47 |

| EMB | 4.20 | 2.18 | 3.51 | 1.99 | 36.66 | 1.05 | 0.302 | 0.33 |

| APM | 0.42 | 0.05 | 0.47 | 0.08 | 31.86 | −2.18 * | 0.037 | 0.75 |

| DAP | 5.96 | 2.68 | 5.25 | 2.73 | 37.72 | 0.84 | 0.408 | 0.26 |

| gdppc | 48,627.16 | 20,593.13 | 33,310.67 | 17,754.53 | 35.79 | 2.51 * | 0.017 | 0.80 |

| pop | 18,052,616 | 25,600,007 | 22,715,524 | 35,461,677 | 36.30 | −0.48 | 0.634 | 0.15 |

| GCI | 72.96 | 5.73 | 67.08 | 9.28 | 33.75 | 2.44 * | 0.020 | 0.76 |

| ECI | 1.12 | 0.52 | 0.85 | 0.71 | 32.71 | 1.30 | 0.202 | 0.43 |

| Indicator | Central and Eastern (n = 14) | Western and Northern (n = 11) | Southern (n = 15) | One-Way ANOVA F | |||

|---|---|---|---|---|---|---|---|

| M | SD | M | SD | M | SD | ||

| orgcount | 8.00 | 3.11 | 10.09 | 5.22 | 7.60 | 3.44 | 1.41 |

| accserv | 23.00 | 10.82 | 28.64 | 15.46 | 20.00 | 11.73 | 1.51 |

| ASC | 0.60 | 0.19 | 0.70 | 0.22 | 0.56 | 0.22 | 1.43 |

| PCO | 2.87 | 0.89 | 2.82 | 0.84 | 2.49 | 0.84 | 0.85 |

| CAS | 1.78 | 0.92 | 2.06 | 0.94 | 1.48 | 0.93 | 1.30 |

| MSC | 0.88 | 0.14 | 0.92 | 0.10 | 0.83 | 0.13 | 1.61 |

| EMB | 3.65 | 1.47 | 4.75 | 3.00 | 3.34 | 1.63 | 1.58 |

| APM | 0.45 | 0.05 | 0.45 | 0.08 | 0.44 | 0.07 | 0.23 |

| DAP | 5.44 | 2.10 | 6.82 | 3.59 | 4.82 | 2.25 | 1.86 |

| gdppc | 36,710.29 ab | 15,254.06 | 62,057.36 a | 20,697.74 | 28,457.67 b | 10,285.51 | 15.76 ** |

| pop | 25,615,965 | 40,424,859 | 17,977,605 | 24,997,941 | 17,579,395 | 25,504,735 | 0.28 |

| GCI | 69.23 a | 7.50 | 78.75 b | 2.68 | 63.95 a | 5.69 | 20.58 ** |

| ECI | 1.15 ab | 0,.4 | 1.26 a | 0.33 | 0.58 b | 0.48 | 4.96 * |

| Dependent: DAP | Factors | Unstandardized Coef. | Standardized Coef. (Beta) | t | Sig. | Adj. R2 | |

|---|---|---|---|---|---|---|---|

| B | Std. Error | ||||||

| 1 | constant | −22.05 ** | 4.368 | n/a | −5.048 | 0.001 | 0.630 |

| gdppc | −0.00025 | 0 | −1.168 | −0.769 | 0.448 | ||

| ln(pop) | 1.069 ** | 0.243 | 0.540 | 4.506 | 0.001 | ||

| GCI | 0.932 | 0.946 | 0.479 | 1.911 | 0.066 | ||

| High income | 0.932 | 0.946 | 0.162 | 0.985 | 0.333 | ||

| ECI | 0.291 | 0.614 | 0.071 | 0.475 | 0.638 | ||

| 2 | constant | −22.73 ** | 4.074 | n/a | −5.579 | 0.001 | 0.639 |

| gdppc | −0.00024 | 0 | −1.157 | −0.733 | 0.469 | ||

| ln(pop) | 1.114 ** | 0.237 | 0.549 | 4.699 | 0.001 | ||

| GCI | 0.156 * | 0.075 | 0.504 | 2.080 | 0.046 | ||

| High income | 1.038 | 0.908 | 0.180 | 1.143 | 0.262 | ||

| 3 | constant | −21.415 ** | 3.631 | n/a | −5.898 | 0.001 | 0.644 |

| ln(pop) | 1.155 ** | 0.229 | 0.569 | 5.052 | 0.001 | ||

| GCI | 0.115 * | 0.050 | 0.372 | 2.312 | 0.027 | ||

| High income | 0.963 | 0.896 | 0.167 | 1.075 | 0.291 | ||

| 4 | constant | −22.06 ** | 3.589 | n/a | −6.147 | 0.001 | 0.643 |

| ln(pop) | 1.062 ** | 0.212 | 0.523 | 5.006 | 0.001 | ||

| GCI | 0.156 ** | 0.032 | 0.503 | 4.809 | 0.001 | ||

| Dependent: DAP | Factors | Unstandardized Coef. | Standardized Coef. (Beta) | t | Sig. | Adj. R2 | |

|---|---|---|---|---|---|---|---|

| B | Std. Error | ||||||

| 1 | constant | −23.486 ** | 4.859 | −4.833 | 0.001 | 0.588 | |

| gdppc | −0.0000575 | 0 | −0.032 | −0.171 | 0.866 | ||

| ln(pop) | 1.490 ** | 0.276 | 0.716 | 5.399 | 0.001 | ||

| WDCR | 0.047 | 0.029 | 0.296 | 1.625 | 0.118 | ||

| High income | 2.646 * | 1.156 | 0.319 | 2.289 | 0.032 | ||

| ECI | 0.307 | 0.709 | 0.062 | 0.434 | 0.699 | ||

| 2 | constant | −23.394 ** | 4.731 | −4.945 | 0.001 | 0.604 | |

| ln(pop) | 1.487 | .270 | 0.715 | 5.515 | 0.001 | ||

| WDCR | 0.043 | 0.021 | 0.276 | 2.036 | 0.053 | ||

| High income | 2.610 * | 1.114 | 0.315 | 2.344 | 0.028 | ||

| ECI | 0.282 | 0.679 | 0.057 | 0.415 | 0.682 | ||

| 3 | constant | −23.962 ** | 4.452 | −5.382 | 0.001 | 0.617 | |

| ln(pop) | 1.525 ** | 0.249 | 0.733 | 6.112 | 0.001 | ||

| WDCR | 0.046 * | 0.020 | 0.293 | 2.325 | 0.028 | ||

| High income | 2.710 * | 1.070 | 0.326 | 2.533 | 0.018 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ionescu-Feleagă, L.; Dragomir, V.D.; Bunea, Ș.; Stoica, O.C.; Barna, L.-E.-L. Empirical Evidence on the Development and Digitalization of the Accounting and Finance Profession in Europe. Electronics 2022, 11, 3970. https://doi.org/10.3390/electronics11233970

Ionescu-Feleagă L, Dragomir VD, Bunea Ș, Stoica OC, Barna L-E-L. Empirical Evidence on the Development and Digitalization of the Accounting and Finance Profession in Europe. Electronics. 2022; 11(23):3970. https://doi.org/10.3390/electronics11233970

Chicago/Turabian StyleIonescu-Feleagă, Liliana, Voicu D. Dragomir, Ștefan Bunea, Oana Cristina Stoica, and Laura-Eugenia-Lavinia Barna. 2022. "Empirical Evidence on the Development and Digitalization of the Accounting and Finance Profession in Europe" Electronics 11, no. 23: 3970. https://doi.org/10.3390/electronics11233970

APA StyleIonescu-Feleagă, L., Dragomir, V. D., Bunea, Ș., Stoica, O. C., & Barna, L. -E. -L. (2022). Empirical Evidence on the Development and Digitalization of the Accounting and Finance Profession in Europe. Electronics, 11(23), 3970. https://doi.org/10.3390/electronics11233970