M&A Open Innovation, and Its Obstacle: A Case Study on GCC Region

Abstract

:1. Introduction and Literature Review

2. Methodology

2.1. Techniques to the Study

2.1.1. Qualitative and Quantitative Techniques

2.1.2. Deductive and Inductive Reasonings

2.1.3. Relevant Approach

2.2. Stewardship Theory

3. Results

4. Discussions

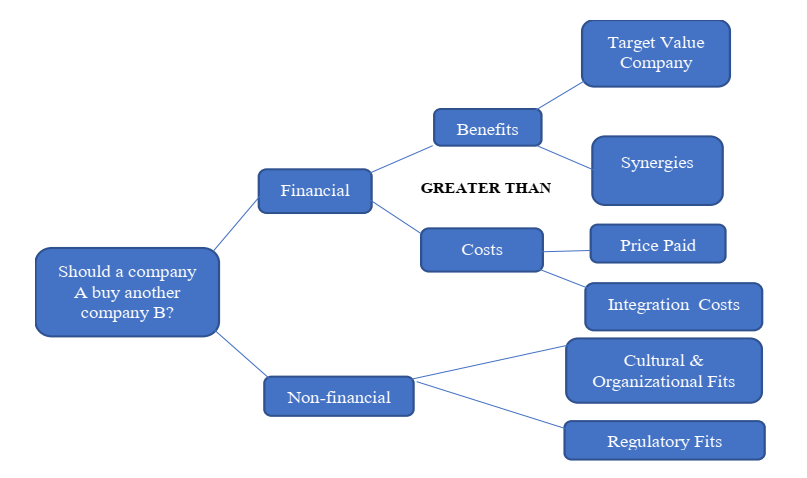

4.1. Open Innovation by M&As

4.2. Future Implementation of M&As

- sociocultural factors;

- global factors;

- human factors.

5. Conclusions

- This study contributed to furthering scholarly understanding of:

- (1)

- what constitutes Islamic CG and how it differs from the conventional CG models;

- (2)

- how and to what extent Islamic CG is practiced and its limitations;

- (3)

- compatibility and challenges in accommodating various stakeholders’ interests in enforcing shariah compliance;

- (4)

- how issues needed to be considered for successful cross-border M&A between the Islamic and non-Islamic companies.

- The second contribution of this thesis is the development of the CG model (see Figure 4) which helps to further our understanding of the complex issues involved in the process of cross-border M&A between Islamic and non-Islamic companies.

- The third contribution of the study is to extend agency, stewardship and stakeholder theories in view of the development of a behavioral Shariah CG model in a critical manner.

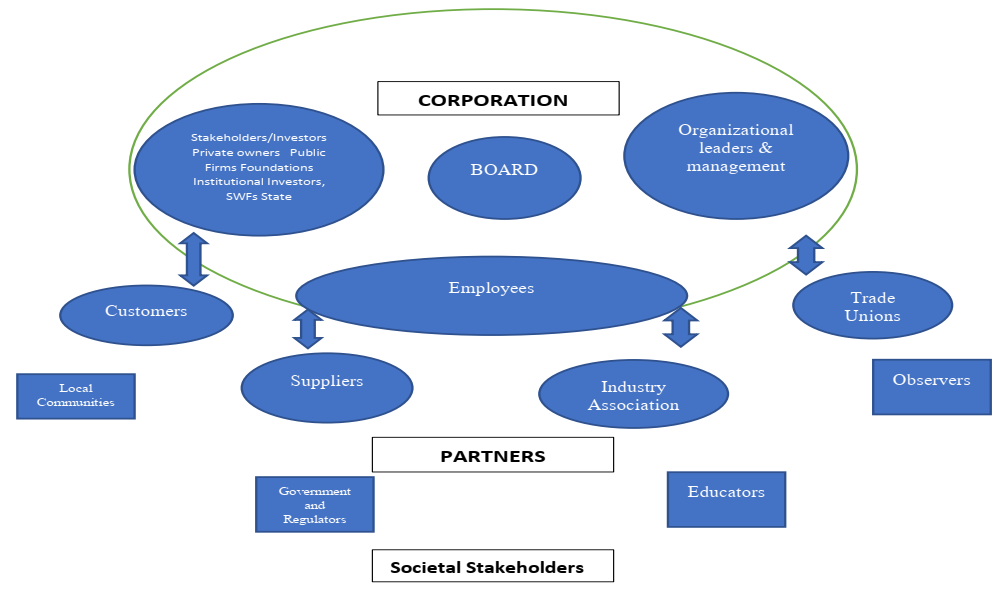

- Whilst the stakeholder approach is likely to provide holistic perspectives in informing the expectations, behavior and actions of different stakeholders, agency and stewardship by different interest groups could also play an important role in enabling or constraining the firms’ motivation and ability to expand internationally or nationally.

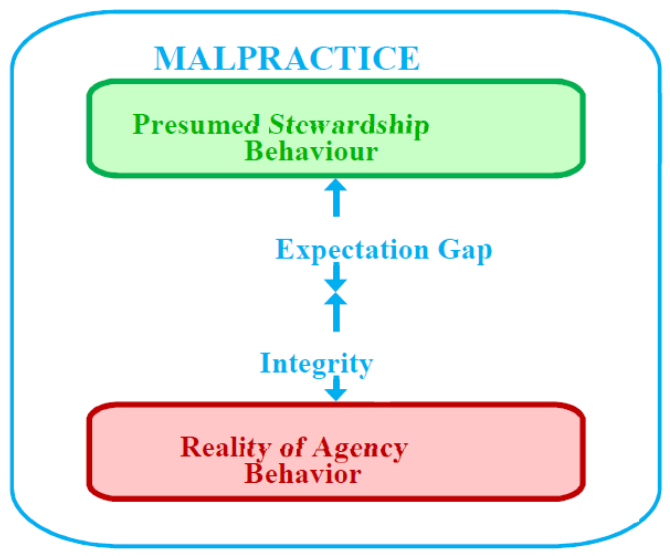

- Fourthly, the study identified gaps in the existing Islamic CG model, in particular the difficulties of knowledge regarding deficiency of the advice provided regarding shariah compliance, underdevelopment of relevant infrastructure, inadequate or limited business knowledge by management, BOD, SSB and Shariah scholars of the Western business context and under defined or emergent legal provisions in support of Shariah principles, low level awareness of the conventional CG and its code of conduct and the possible cause of variations in Shariah compliance which highlighted the difference between the presumed stewardship behavior and the reality of agency behavior.

- The fifth theoretical contribution is what might explain the gap between rhetoric and reality of stewardship and agency problems in the study context.

- This study identified malpractice as the source of a lack of integrity of agents (e.g., corrupt or selfish Shariah scholars or collusion between the BOD and SSB to gain unfair advantages), and such a situation heightens the expectation gap between what is presumed and what can reasonably be presumed for a human being.

Funding

Conflicts of Interest

References

- Nguyen, H.T.; Yung, K.; Sun, Q. Motives for mergers and acquisitions: Ex-post market evidence from the US. J. Bus. Financ. Account. 2012, 39, 1357–1375. [Google Scholar] [CrossRef]

- Kummer, C. Motivation and retention of key people in mergers and acquisitions. Strat. HR Rev. 2008, 7, 5–10. [Google Scholar] [CrossRef]

- Yun, J.J.; Lee, M.; Park, K.; Zhao, X. Open innovation and serial entrepreneurs. Sustainability 2019, 11, 5055. [Google Scholar] [CrossRef] [Green Version]

- Florio, M.; Ferraris, M.; Vandone, D. Motives of mergers and acquisitions by state-owned enterprises. Int. J. Public Sect. Manag. 2018, 31, 142–166. [Google Scholar] [CrossRef]

- Al-Nodel, A.; Hussainey, K. Corporate Governance and Financing Decisions by Saudi Companies? J. Mod. Account. Audit. 2010, 6, 1–14. [Google Scholar]

- Thomas, D.A.; Ely, R. Making Differences Matter: A New Paradigm for Managing Diversity. 1996. Available online: https://hbr.org/1996/09/making-differences-matter-a-new-paradigm-for-managing-diversity (accessed on 11 May 2020).

- Trąpczyński, P.; Zaks, O.; Polowczyk, J. The Effect of Trust on Acquisition Success: The Case of Israeli Start-Up M&A. Sustainability 2018, 10, 2499. [Google Scholar]

- Trompenaars, F.; Asser, M.N. The global M&A tango: How to reconcile cultural differences in mergers, acquisitions and strategic partnerships. Hum. Resour. Manag. Int. Dig. 2012, 20. [Google Scholar] [CrossRef]

- Pollok, P.; Lüttgens, D.; Piller, F.T. How firms develop capabilities for crowdsourcing to increase open innovation performance: The interplay between organizational roles and knowledge processes. J. Prod. Innov. Manag. 2019, 36, 412–441. [Google Scholar] [CrossRef]

- Cooke, F.L.; Wood, G.; Wang, M.; Li, A.S. Riding the tides of mergers and acquisitions by building a resilient workforce: A framework for studying the role of human resource management. Hum. Resour. Manag. Rev. 2020, 100747. [Google Scholar] [CrossRef]

- Yun, J.J.; Zhao, X.; Jung, K.; Yigitcanlar, T. The culture for open innovation dynamics. Sustainability 2020, 12, 5076. [Google Scholar] [CrossRef]

- Christofi, M.; Vrontis, D.; Thrassou, A.; Shams, S.R. Triggering technological innovation through cross-border mergers and acquisitions: A micro-foundational perspective. Technol. Forecast. Soc. Chang. 2019, 146, 148–166. [Google Scholar] [CrossRef]

- Wang, Y.; Roijakkers, N.; Vanhaverbeke, W.; Chen, J. How Chinese firms employ open innovation to strengthen their innovative performance. Int. J. Technol. Manag. 2012, 59, 235–254. [Google Scholar] [CrossRef]

- Stahl, G.K.; Voigt, A. Do cultural differences matter in mergers and acquisitions? A tentative model and examination. Organ. Sci. 2008, 19, 160–176. [Google Scholar]

- Srivastava, S.; Singh, S.; Dhir, S. Culture and International business research: A review and research agenda. Int. Bus. Rev. 2020, 29, 101709. [Google Scholar] [CrossRef]

- Yun, J.J.; Liu, Z. Micro-and macro-dynamics of open innovation with a quadruple-helix model. Sustainability 2019, 10, 3301. [Google Scholar] [CrossRef] [Green Version]

- Soualhi, Y. Models of Shariah Governance Across Jurisdictions. Islamic Commer. Law Rep. 2016, 2016, 22. [Google Scholar] [CrossRef]

- Raman, A.A.; Bukair, A.A. The influence of the Shariah supervision board on corporate social responsibility disclosure by Islamic banks of Gulf Co-operation Council countries. AJBA 2013, 6, 2180–3137. [Google Scholar]

- El Gattoufi, S.; Al Muharrami, S.; Shamas, G. Assessment of mergers and acquisitions in GCC banking. Int. J. Account. Financ. 2014, 4, 358–377. [Google Scholar] [CrossRef]

- Lzeban, A.; Gwilliam, D. Factors affecting the internal audit effectiveness: A survey of the Saudi public sector. J. Int. Account. Audit. Tax. 2014, 23, 74–86. [Google Scholar] [CrossRef]

- Hassan, M.K.; Aliyu, S.; Huda, M.; Rashid, M. A survey on Islamic Finance and accounting standards. Borsa Istanb. Rev. 2019, 19, S1–S13. [Google Scholar] [CrossRef]

- Siew, J. Value Creation–as Seen from Asia and Ride-Sharing. Available online: https://www.insead.edu/sites/default/files/assets/dept/centres/gpei/docs/insead-isp-value-creation-asia-and-ride-sharing-jan-2019.pdf (accessed on 11 May 2020).

- Sole, M.J. Introducing Islamic Banks into Coventional Banking Systems (EPub); International Monetary Fund: Washington, DC, USA, 2007. [Google Scholar]

- Saunders, M.; Lewis, P.; Thornhill, A. Research Methods for Business Students; Pearson Education: London, UK, 2009. [Google Scholar]

- Elo, S.; Kyngäs, H. The qualitative content analysis process. J. Adv. Nurs. 2008, 62, 107–115. [Google Scholar] [CrossRef] [PubMed]

- Lietz, C.A.; Zayas, L.E. Evaluating Qualitative Research for Social Work Practitioners. Adv. Soc. Work. 2010, 11, 188–202. [Google Scholar] [CrossRef] [Green Version]

- Bernard, A.B.; Redding, S.J.; Schott, P.K. Multiproduct Firms and Trade Liberalization. Q. J. Econ. 2011, 126, 1271–1318. [Google Scholar] [CrossRef] [Green Version]

- Silverman, D. Qualitative Research; Sage: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Corti, L.; Bishop, L. Strategies in Teaching Secondary Analysis of Qualitative Data. In Forum Qualitative Sozialforschung; FQS: Berlin, Germany, 2005. [Google Scholar]

- Sarala, R.M.; Vaara, E.; Junni, P. Beyond merger syndrome and cultural differences: New avenues for research on the “human side” of global mergers and acquisitions (M&As). J. World Bus. 2019, 54, 307–321. [Google Scholar]

- Rossi, S.; Volpin, P.F. Cross-country determinants of mergers and acquisitions. J. Financ. Econ. 2004, 74, 277–304. [Google Scholar] [CrossRef]

- Rottig, D.; Reus, T.H. Research on Culture and International Acquisition Performance: A Critical Evaluation and New Directions. Int. Stud. Manag. Organ. 2018, 48, 3–42. [Google Scholar] [CrossRef]

- Othman, R.; Ameer, R. Conceptualizing the duties and roles of auditors in Islamic financial institutions. Humanomics 2015, 31, 201–213. [Google Scholar] [CrossRef]

- Rokan, M.K. Optimalisasi peran dewan pengawas syariah (dps) dalam perbankan syariah di medan. Equilib. J. Ékon. Syariah 2018, 5, 292–305. [Google Scholar] [CrossRef]

- Qiao, L.; Wu, J. Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums. Sustainability 2019, 11, 1291. [Google Scholar] [CrossRef] [Green Version]

- Reuer, J.J.; Shenkar, O.; Ragozzino, R. Mitigating risk in international mergers and acquisitions: The role of contingent payouts. J. Int. Bus. Stud. 2003, 35, 19–32. [Google Scholar] [CrossRef]

- Ouyang, S.; Li, Y. Li Confucius Institute and the Completion of Chinese Cross-Border Acquisitions. Sustainability 2019, 11, 5088. [Google Scholar] [CrossRef]

- Piesse, J.; Strange, R.; Toonsi, F. Is there a distinctive MENA model of corporate governance? J. Manag. Gov. 2011, 16, 645–681. [Google Scholar] [CrossRef]

- Najeeb, S.F.; Ibrahim, S.H.M. Professionalizing the role of Shari’ah auditors: How Malaysia can generate economic benefits. Pac. Basin Financ. J. 2014, 28, 91–109. [Google Scholar] [CrossRef]

- Khalid, A.A.; Haron, H.; Masron, T.A. Competency and effectiveness of internal Shariah audit in Islamic financial institutions. J. Islam. Account. Bus. Res. 2018, 9, 201–221. [Google Scholar] [CrossRef]

- Oak, S.; Dalbor, M.C. The Impact of International Acquisition Announcements on the Returns of U.S. Lodging Firms. J. Hosp. Financ. Manag. 2009, 17, 19–32. [Google Scholar] [CrossRef] [Green Version]

- Muammar, A.N.; Widodo, J.; Sulhadi, S. Evaluation of zakat management program in the badan amil zakat national of banten province. J. Res. Educ. Res. Eval. 2018, 7, 19–28. [Google Scholar]

- McGuire, S.T.; Omer, T.C.; Sharp, N.Y. The impact of religion on financial reporting irregularities. Account. Rev. 2012, 87, 645–673. [Google Scholar] [CrossRef]

- Moeller, S.B.; Schlingemann, F.P. Global diversification and bidder gains: A comparison between cross-border and domestic acquisitions. J. Bank. Financ. 2005, 29, 533–564. [Google Scholar] [CrossRef]

- Al Naeemy, T.M.Y. Consequences of Mergers and Acquisitions and Their Effect on Employees: A Case Study from the Banking Industry in the UAE. In Human Capital in the Middle East; Springer: Berlin, Germany, 2020; pp. 179–223. [Google Scholar]

- Maswadeh, S. A Compliance of Islamic Banks with the Principles of Islamic Finance (shariah): An Empirical Survey of the Jordanian Business Firms. Int. J. Account. Financ. Rep. 2014, 4, 169. [Google Scholar] [CrossRef] [Green Version]

- Lewis, M.K. Principles of Islamic corporate governance. In Handbook on Islam and Economic Life; Edward Elgar Publishing: Cheltenham, UK, 2014. [Google Scholar]

- Licht, A.N.; Goldschmidt, C.; Schwartz, S.H. Culture, Law, and Corporate Governance. Int. Rev. Law Econ. 2005, 25, 229–255. [Google Scholar] [CrossRef]

- Maali, B.; Casson, P.; Napier, C. Social reporting by islamic banks. Abacus 2006, 42, 266–289. [Google Scholar] [CrossRef]

- Koldertsova, A. The Second Corporate Governance Wave in the Middle East and North Africa. OECD J. Financ. Mark. Trends 2011, 2010, 219–226. [Google Scholar] [CrossRef]

- Karim, S.; Capron, L. Reconfiguration: Adding, redeploying, recombining and divesting resources and business units. Strat. Manag. J. 2016, 37, E54–E62. [Google Scholar] [CrossRef]

- Botiș, S. Mergers and Acquisitions in the International Banking Sector; Bulletin of the Transilvania University of Braşov: Brașov, Romania, 2013; Volume 6. [Google Scholar]

- Iqbal, Z.; Mirakhor, A. An Introduction to Islamic Finance: Theory and Practice; John Wiley & Sons: Hoboken, NJ, USA, 2011; Volume 687. [Google Scholar]

- Kammer, A.; Norat, M.; Pinon, M.; Prasad, A.; Towe, C.; Zeidane, Z. Islamic Finance: Opportunities, Challenges, and Policy Options; International Monetary Fund: Washington, DC, USA, 2015. [Google Scholar]

- Hečková, J.; Štefko, R.; Frankovský, M.; Birknerová, Z.; Chapčáková, A.; Zbihlejová, L. Cross-Border Mergers and Acquisitions as a Challenge for Sustainable Business. Sustainability 2019, 11, 3130. [Google Scholar]

- Hečková, J.; Frankovský, M.; Birknerová, Z.; Chapčáková, A.; Zbihlejová, L. Analysis of the Post Merger and Acquisition Process of Implementation of the Cross-border Mergers and Acquisitions by Means of the pDM&A Methodology. J. Manag. Bus. Res. Prac. 2017, 9, 26–34. [Google Scholar]

- Hečková, J.; Chapčáková, A.; Badida, P. Aktuálne problémy ohodnocovania podnikov pri fúziách a akvizíciách a ich riešenie. Ekon. Časopis J. Econ. 2014, 7, 743–766. [Google Scholar]

- Georgieva, D.; Jandik, T.; Lee, W.Y. The impact of laws, regulations, and culture on cross-border joint ventures. J. Int. Financ. Mark. Inst. Money 2012, 22, 774–795. [Google Scholar] [CrossRef]

- Öberg, C. Acquisitions and open innovation–a literature review and extension. In Mergers and Acquisitions, Entrepreneurship and Innovation; Emerald Publishing Limited: Bentley, UK, 2016; pp. 31–58. [Google Scholar]

- Eckbo, B.E.; Thorburn, K.S. Gains to Bidder Firms Revisited: Domestic and Foreign Acquisitions in Canada. J. Financ. Quant. Anal. 2000, 35, 1–25. [Google Scholar] [CrossRef]

- Farook, S.; Farooq, M.O. Sharīʻah Governance, Expertise and Profession: Educational Challenges in Islamic Finance. ISRA Int. J. Islam. Financ. 2013, 5, 137–160. [Google Scholar] [CrossRef]

- Garas, S.N.; Pierce, C. Shari’a supervision of Islamic financial institutions. J. Financ. Regul. Compliance 2010, 18, 386–407. [Google Scholar] [CrossRef]

- Brammer, S.; Williams, G.; Zinkin, J. Religion and attitudes to corporate social responsibility in a large cross-country sample. J. Bus. Ethics 2007, 71, 229–243. [Google Scholar] [CrossRef]

- Buch, C.M.; Delong, G. Cross-border bank mergers: What lures the rare animal? J. Bank. Financ. 2004, 28, 2077–2102. [Google Scholar] [CrossRef] [Green Version]

- Alam Choudhury, M.; Alam, M.N. Corporate governance in Islamic perspective. Int. J. Islam. Middle East. Financ. Manag. 2013, 6, 180–199. [Google Scholar] [CrossRef]

- Ali, A.J.; Al-Aali, A.Y. Marketing and Ethics: What Islamic Ethics Have Contributed and the Challenges Ahead. J. Bus. Ethics 2014, 129, 833–845. [Google Scholar] [CrossRef]

- Al-Shammari, B.; Brown, P.; Tarca, A. An investigation of compliance with international accounting standards by listed companies in the Gulf Co-Operation Council member states. Int. J. Account. 2008, 43, 425–447. [Google Scholar] [CrossRef]

- Ayub, M. Islamic Finance: Laying Down an Overarching Schema for Value based Sharī ‘ah Advisory and Governance Framework. J. Islam. Bus. Manag. 2013, 219, 1–64. [Google Scholar] [CrossRef]

- Elmquist, M.; Fredberg, T.; Ollila, S. Exploring the field of open innovation. Eur. J. Innov. Manag. 2009, 12, 326–345. [Google Scholar] [CrossRef]

- Santoro, G.; Ferraris, A.; Winteler, D.J. Open innovation practices and related internal dynamics: Case studies of Italian ICT SMEs. EuroMed J. Bus. 2019, 14, 47–61. [Google Scholar] [CrossRef]

- Bindabel, W.A. The Influence of Shariah (Islamic principles) Corporate Governance on Cross-Border Merger and Acquisitions Involving Islamic Companies in the Gulf Countries. Ph.D. Thesis, Law De Montfort University, Leicester, UK, June 2017. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Paradigm | Interpretivism (Constructivism) |

|---|---|

| Approach | Inductive |

| Epistemology | Subjective |

| Ontology | Relativism |

| Methods | Qualitative |

| Companies | Saudi Arabia | Kuwait | UAE | Total |

|---|---|---|---|---|

| Banks | 10 | 5 | 7 | 22 |

| Insurance | 7 | 5 | 6 | 18 |

| Total | 17 | 10 | 13 | 40 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bindabel, W. M&A Open Innovation, and Its Obstacle: A Case Study on GCC Region. J. Open Innov. Technol. Mark. Complex. 2020, 6, 138. https://doi.org/10.3390/joitmc6040138

Bindabel W. M&A Open Innovation, and Its Obstacle: A Case Study on GCC Region. Journal of Open Innovation: Technology, Market, and Complexity. 2020; 6(4):138. https://doi.org/10.3390/joitmc6040138

Chicago/Turabian StyleBindabel, Wardah. 2020. "M&A Open Innovation, and Its Obstacle: A Case Study on GCC Region" Journal of Open Innovation: Technology, Market, and Complexity 6, no. 4: 138. https://doi.org/10.3390/joitmc6040138

APA StyleBindabel, W. (2020). M&A Open Innovation, and Its Obstacle: A Case Study on GCC Region. Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 138. https://doi.org/10.3390/joitmc6040138