1. Introduction

With its dramatic political and economic transformation since the end of colonial rule by Japan in 1945, Korea is now regarded as an exceptional latecomer country that has established itself as a full-fledged democratic market economy. However, this process has not been even in the sense that the country experienced decades of political authoritarianism and a government-led economy [

1,

2,

3] as well as the 1997 financial crisis [

4,

5]. Korea’s achievement is often encapsulated in the term “catching up,” which is derived from Abramovitz’s seminal article [

6], “Catching-up, forging ahead and falling behind.” If catching up is defined as closing the gap between the current state and the benchmark [

7], Korea is an example of a successful catch up that joined a group of wealthy nations called the Organization for Economic Cooperation and Development (OECD) in 1996. It reached the income level of high-income countries, such as Japan or UK in PPP-based per capital incomes.

The country now faces serious challenges of growth slowdown, rapid aging, and rising income inequality between the rich and poor, which appear quite similar to the typical situations in advanced or mature economies. If these challenges become permanent features of Korea, then it signals the end of East Asian capitalism or ‘East Asian miracle’ [

8], which is characterized by high growth and low inequality; instead, a convergence toward the Anglo–Saxon capitalism characterized by low growth and high inequality is anticipated [

9]. Accordingly, the time has come to switch our focus from the past catch-up and post-catch-up frameworks to the new and futuristic focus on the convergence and divergence framework [

5].

In this regard, one useful piece of literature is the perspective of Varieties of Capitalism (VoC) pioneered by Hall and Soskice [

10]. It identifies several representative types of capitalism, such as liberal market economies (LMEs), coordinated market economies (CMEs), and mixed market economies (MMEs). If Korea can now be classified in the same group as the United States (US), United Kingdom (UK), or LMEs in terms of performance measures of economic growth and income inequality as Lee and Shin [

9] verified by a cluster analysis, then this shocking result raises an important puzzle of how Korea can thus be classified despite the possible existing differences in its underlying institutions, such as national innovation systems, corporate governance, financial system, and the role and power of the government. Indeed, whereas several authors [

11,

12,

13,

14] have argued for some tendency of convergence, and observed that the changing external and internal circumstances have diminished the developmental states’ capacities to devise and execute coherent techno-industrial strategies, others argued that a continuity of East Asian capitalism remains in several aspects [

15,

16,

17].

This potential mismatch or tension between underlying institutions and outcome variables (growth and income inequality) underscores the need to re-examine the continuity and change in capitalism in Korea. One reason explaining Korea’s ability to overcome the middle-income trap (MIT) and join the OECD is the increasingly high R & D investment that has existed since the mid-1980s [

18], which highlights the importance of examining the country’s national innovation systems (NIS). NIS is a key concept in Schumpeterian economics, which posits that differences in such systems among countries tend to result in differences in innovation and economic performance. This concept is defined as the “elements and relationships, which may interact with the production, diffusion and use of new and economically useful knowledge” [

19]. If NIS is considered a set of institutions related to innovation, then it can also be considered a part of diverse institutions that may underpin diverse types of capitalism or VoC.

Lee [

18] investigated the major characteristics of the catch-up stage by comparing the NIS of South Korea and Taiwan with those of other developing and developed countries, verifying the link between the NIS and economic growth in terms of per capita income growth. In country-level empirical studies, Chapter 3 of Lee [

18] and Lee et al. [

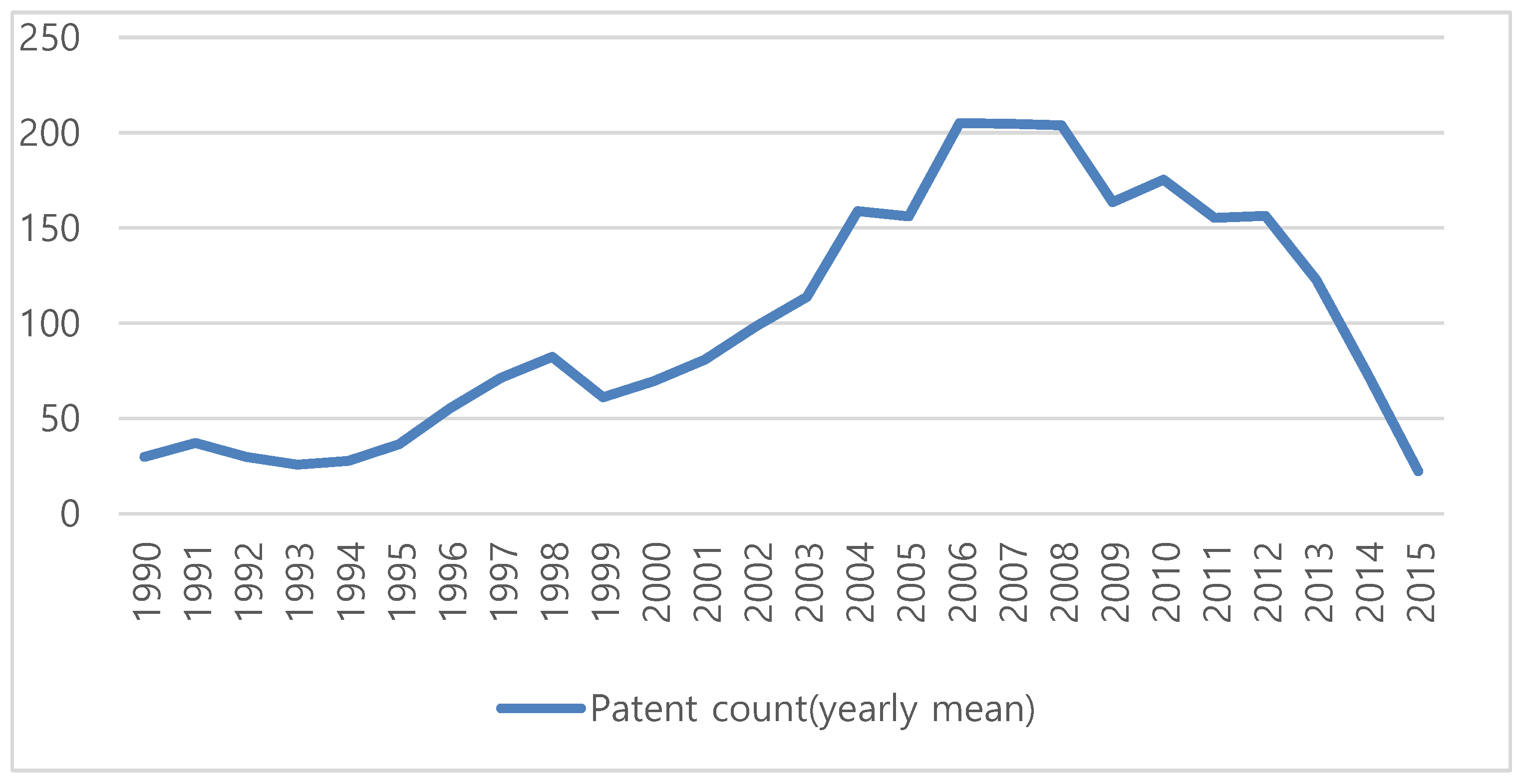

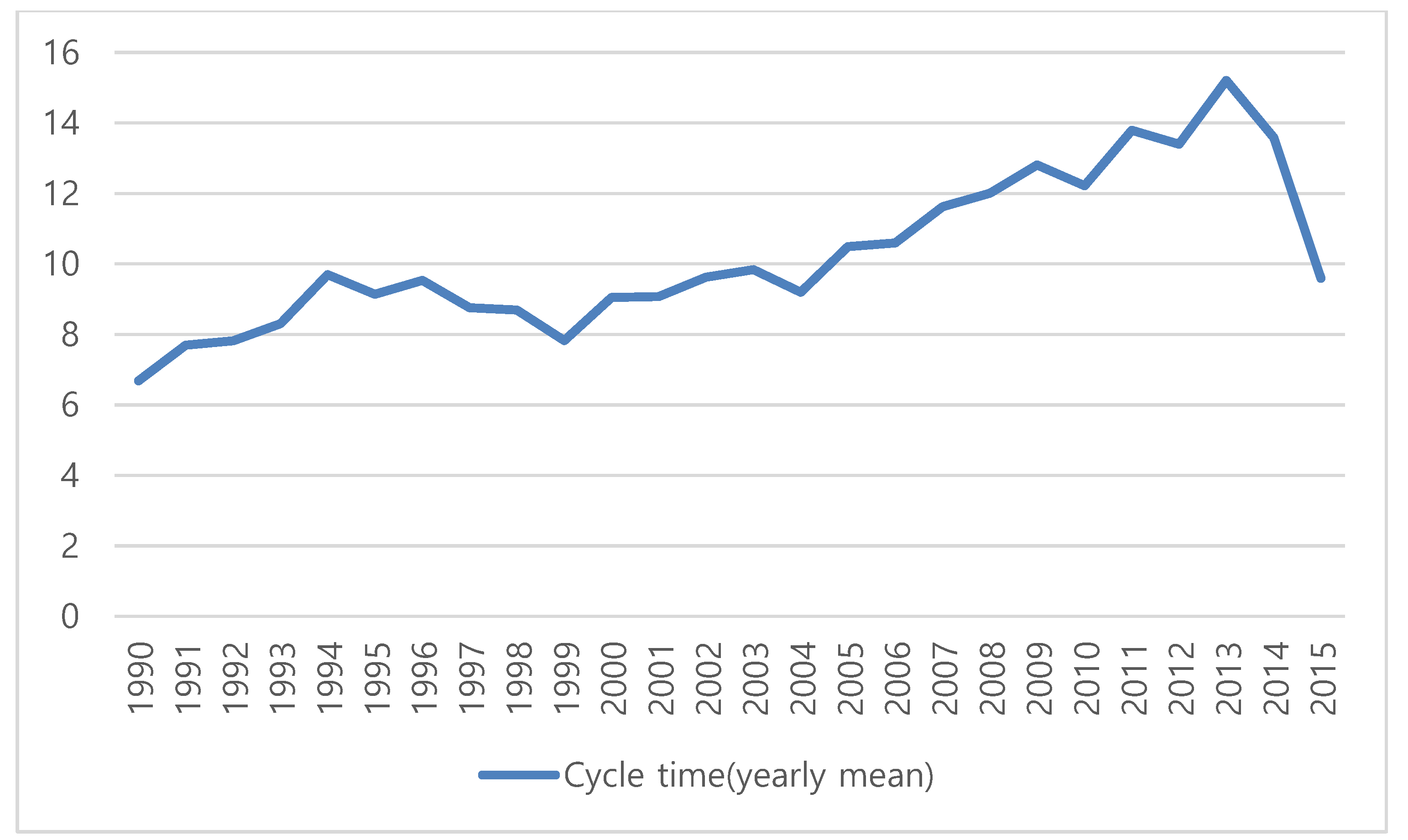

20] demonstrate a significant correlation existing between having more patent applications in fields related to short cycle time of technologies (CTT) and a higher per capita income growth rate in East Asia. This pattern of unbalanced NIS and growth mechanism is in sharp contrast with a more balanced NIS and growth mechanism, which prevails in high-income countries with economic growth showing a positive correlation with a specialization in technologies with long CTT.

Most recently, Lee and Lee [

21] confirm the changing nature of NIS in Korea and Taiwan since the 2000s or the post-catch-up stage, such that these two economies are moving away from sectors based on short-cycle technologies to sectors based on long-cycle technologies, trying to make their industry more balanced than before. Thus, their NIS is becoming similar to advanced or mature NIS characterized by all equally high values of knowledge localization, originality, technological diversification, de-concentration of assignees, and CTT. Their study thus verifies the so-called “detour” hypothesis, which posits that a successful catching-up economy executes a technological detour of initially specializing in short CTT sectors and later turning to challenging or long cycle technology-based sectors. This study also confirms a positive relationship between long cycle technologies and economic growth in Korea and Taiwan for the post-catch-up stages or since the 2000s.

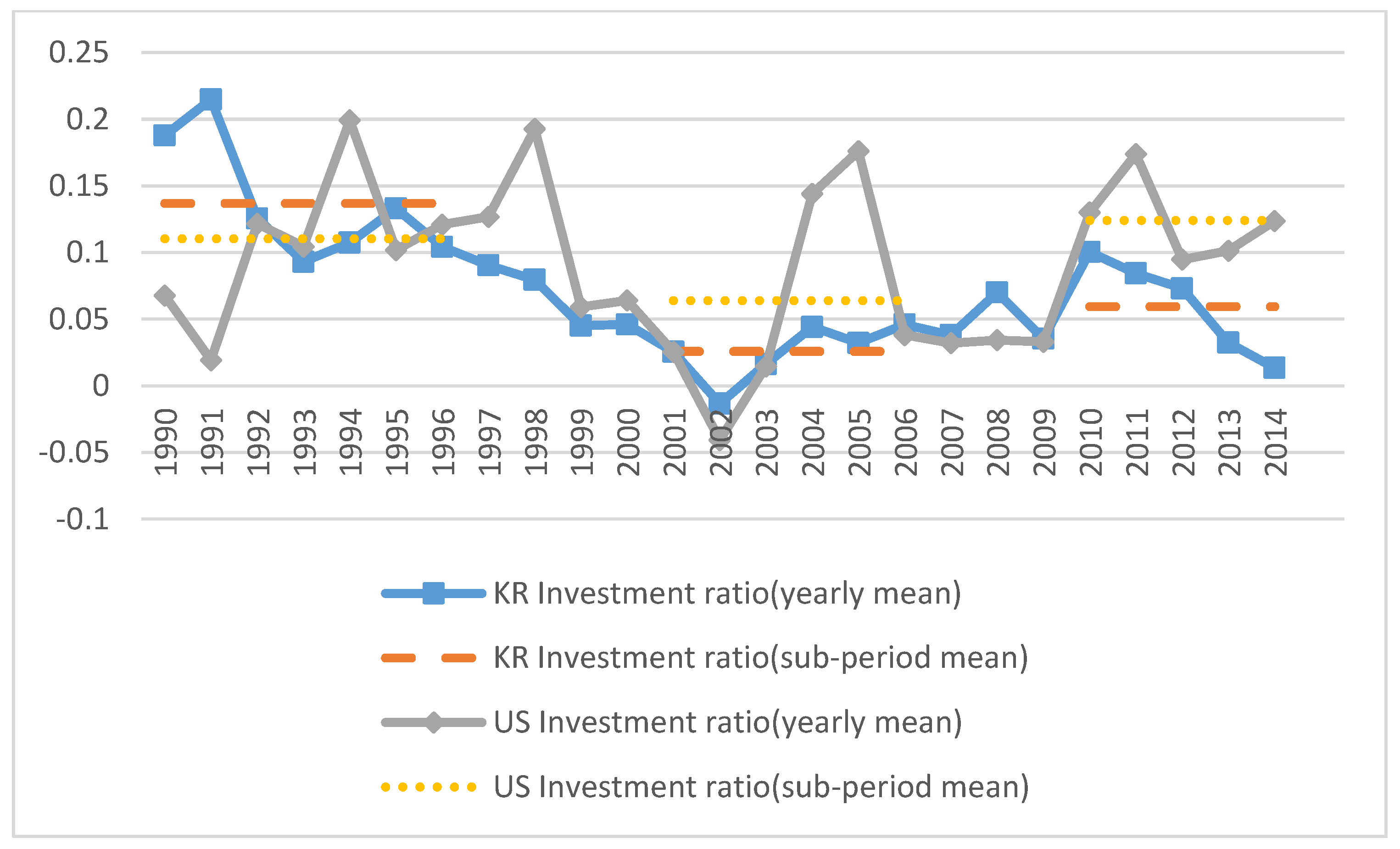

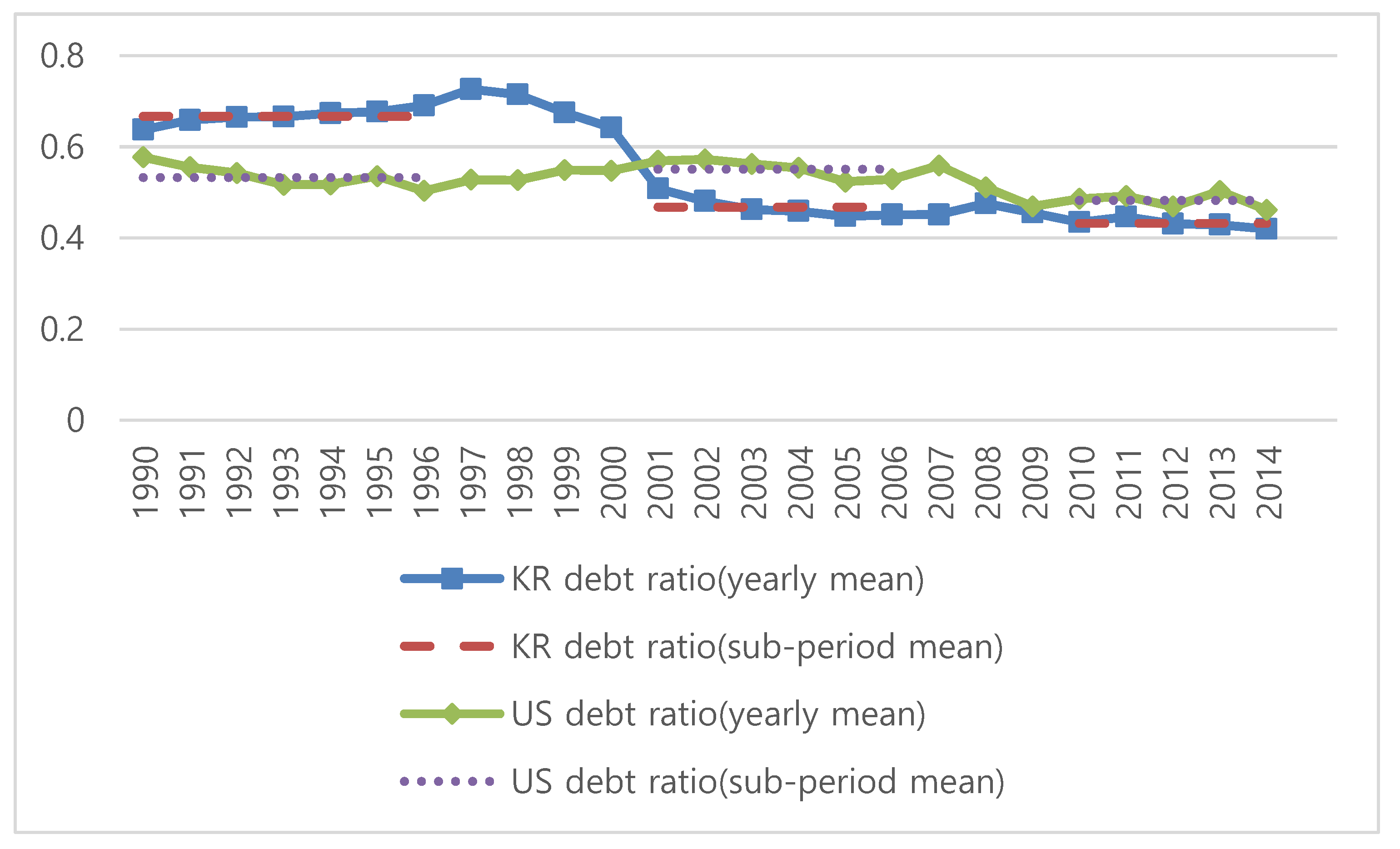

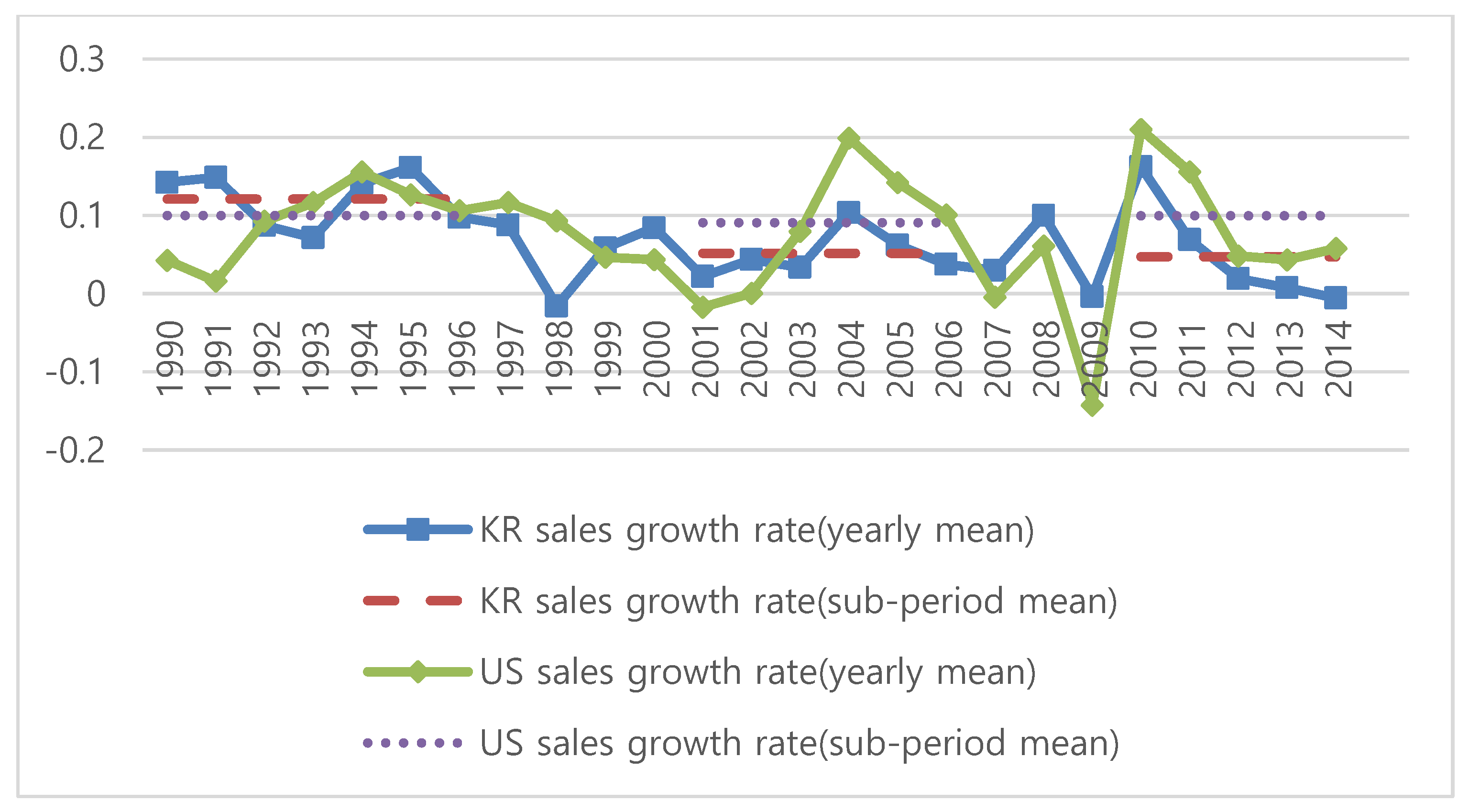

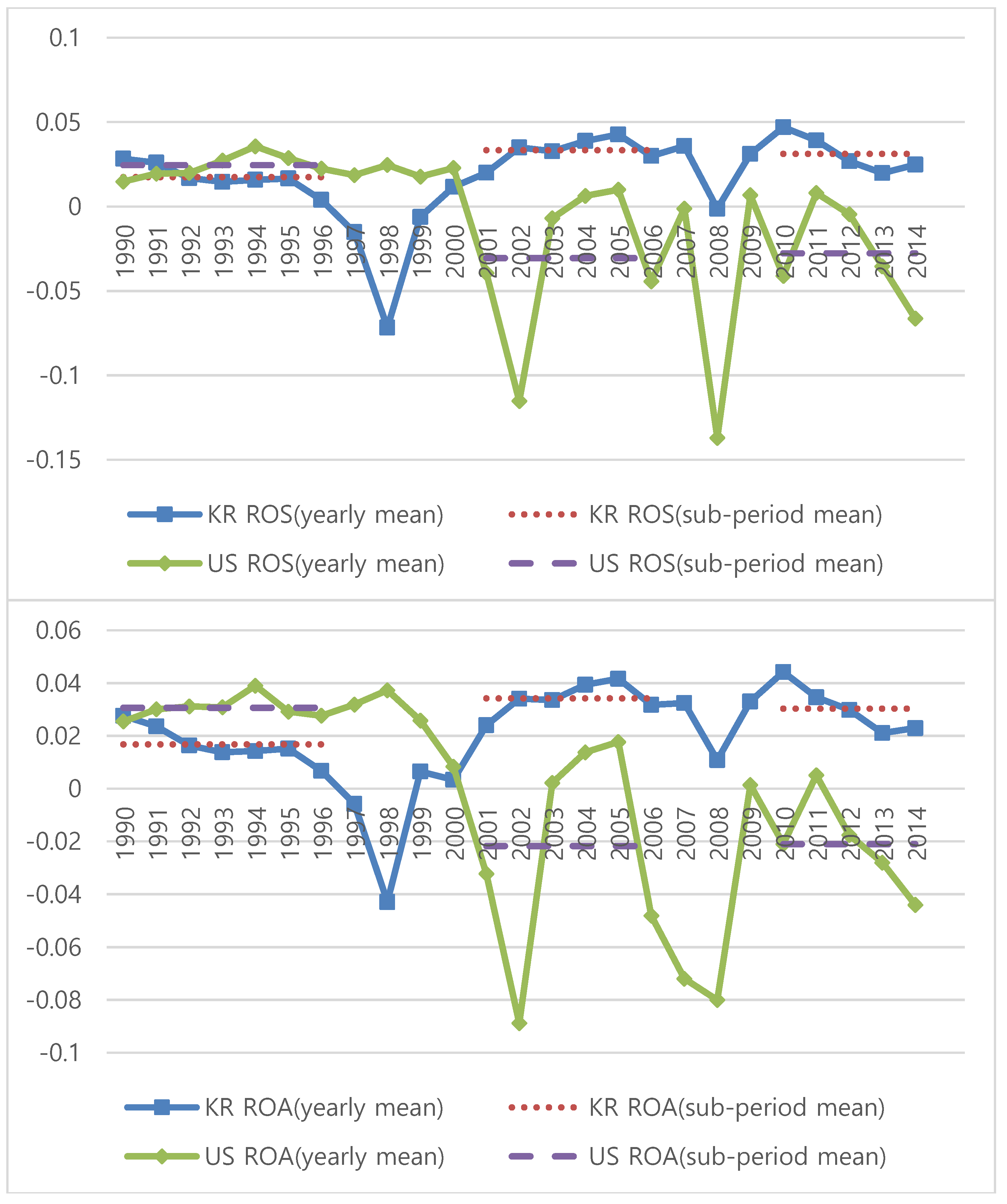

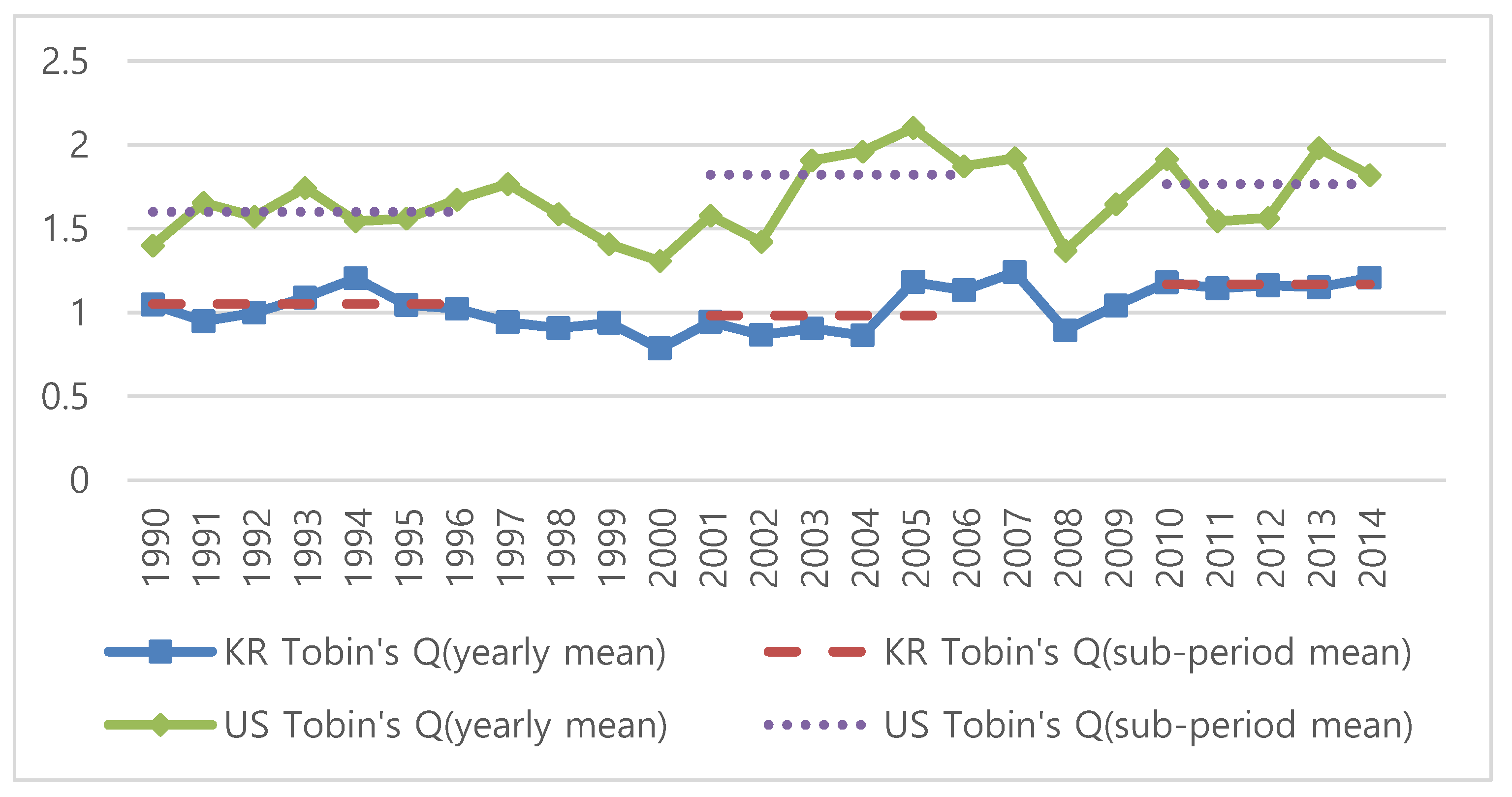

The current study takes up the same issue of catching and convergence now at the level of firms, and investigates whether Korean firms tend to converge toward mature firms represented by the US firms. Convergence is analyzed in two dimensions. First, in terms of conventional accounting variables, the paper will ask whether the Korean firms tend to keep the old behavior of high growth with low profitability and firm values or now switch to emphasize profitability and firm values, as is the case with the US firms. Second, in terms of innovation system variables, it will verify whether the Korean firms continue to pursue a niche-based strategy for profitability by specializing in short CTT, or have stopped such strategy.

This question of convergence is important because firms are real entities in charge of actual innovation activities, and some correspondence is necessary between country- and firm-level patterns. In fact, the Korean firms led by the family-controlled conglomerates (chaebols) have gone through radical reforms in corporate governance as imposed by the International Monetary Fund (IMF) during the 1997 Asian financial crisis [

22,

23]. Relatedly, a major stem of the Korean corporate change that emerged after the crisis was the transplantation of global standards into the Korean economy, and the global standard which Korean companies had to accept at the time was largely a U.S.-based shareholder capitalism. Particularly, opening to foreign investment led to considerable exposure to the influence of foreign investment capital, especially the U.S. investment capital, which pursues shareholder value. For instance, shares of foreign stockholders skyrocketed from less than 3% to 40% in the post-crisis period, which implies the possibility of increasing voices of foreign investors in matters related to management decision-making [

5,

24]. Actually, Kim and Cho [

24] confirms a negative relationship between the foreign shares and firm’s fixed investment.

Thus, this paper begins by first looking at conventional accounting variables to see if any significant change occurred over the period from the 1990s (pre-crisis) to the 2000s and 2010s. Thus, changes in Korean companies are evaluated through relative comparisons with the US firms. Second, and more importantly, this paper examines the change in firm-level innovation systems in Korea and investigates whether the Korean system is now converging to that of the US. In this analysis, the benchmark is the results in Chapter 5 of Lee [

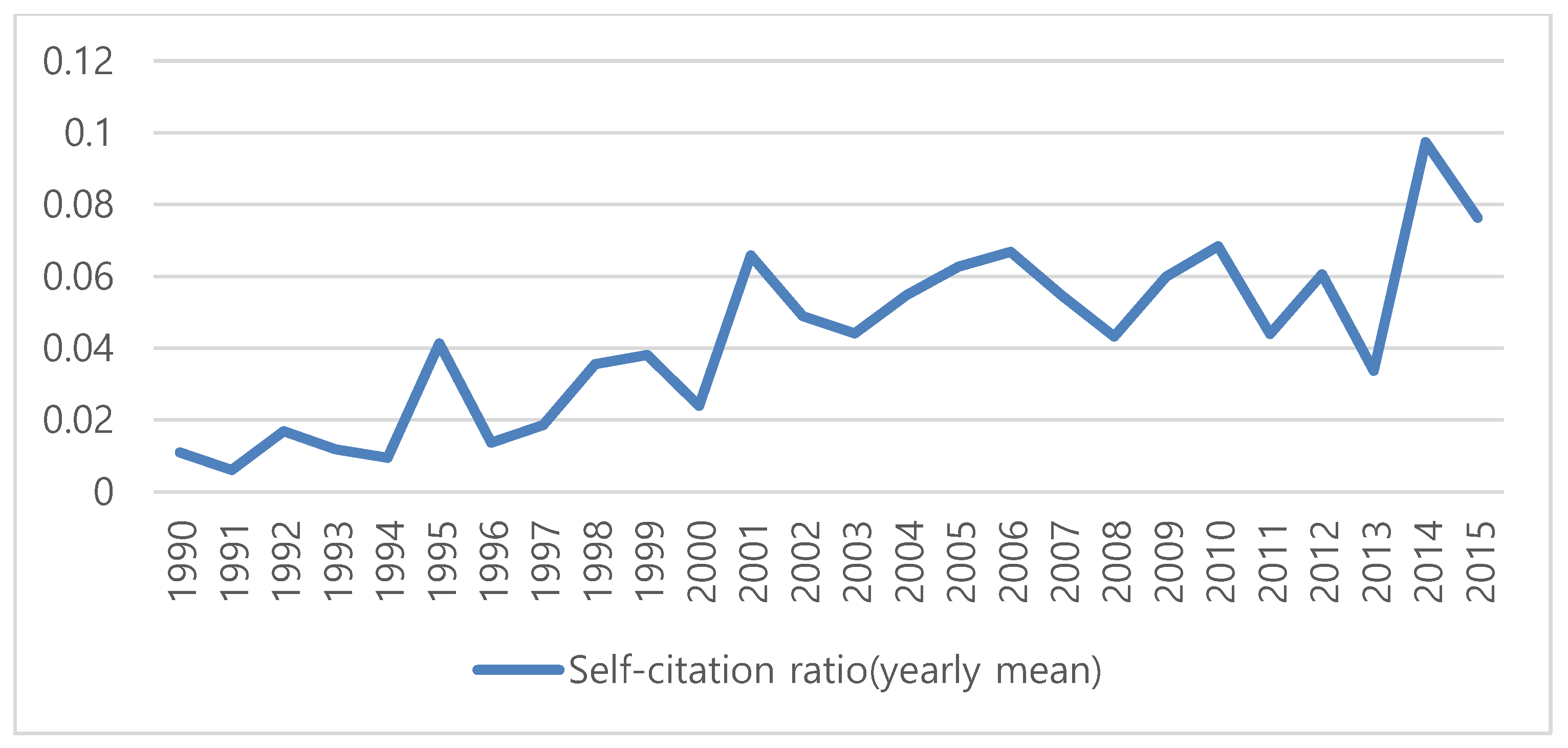

18] that the Korean firms tend to borrow more, invest more, and thus tend to grow faster but end up with low profitability and firm values than the US firms. Moreover, their innovation system in the 1990s was quite different from the US firms as Korean firms sought a niche-based strategy for profitability by specializing in short CTT, and their technological capability represented by self-citation is too low to be significantly affecting firm-values.

While various factors must have been involved during the transition in corporate Korea, this paper focuses on the innovation aspect of the firms. Then, the empirical analysis in this paper will confirm a thesis of “an ongoing but partially completed process of convergence.” Such pattern will be supported by showing that the Korean firms now borrow less, invest less, grow slowly, and thus achieve high profitability; however, their values in stock markets are not as high as those of the US firms, and it finds no significant linkage between (short or long) CTT and firm profitability but a significant linkage from higher self-citation to firm values, which is the pattern of the US firms in the 1990s according to Chapter 5 of Lee [

18].

In what follows,

Section 2 provides some more discussions of the related literature and hypothesis for the empirical analysis.

Section 3 discusses the method for econometric analysis and the data for the analysis.

Section 4 presents the results of the regression analyses of the convergence in terms of the account variables, such as investment ratio, borrowing tendency, and sales growth.

Section 5 analyzes how the innovation system of Korean companies has changed since the 1990s as well as the effect of the innovation system variables on the performance of the companies.

Section 6 presents a summary and concluding remarks.

6. Summary and Concluding Remarks

This paper addresses the issue of convergence of latecomer firms toward firms in advanced economy, with the Korean and US firms representing latecomers and advanced firms, respectively. Convergence is analyzed in two dimensions, namely, in terms of conventional accounting variables and innovation system variables. In this analysis, the benchmark is the results in Chapter 5 of Lee [

18] that the Korean firms tend to borrow more, invest more, and thus grow faster but end up with low profitability and firm values than the US firms, and that their innovation system is quite different from the US firms as Korean firms seek a niche-based strategy for profitability by specializing in short CTT, and their technological capability represented by self-citation is too low to be significantly affecting firm-values.

An emerging conclusion from the empirical analysis in this paper is a “partially completed and clear tendency toward convergence.” In terms of the first dimension of convergence in conventional accounting variables, the Korean firms are shown to now borrow less, invest less, grow slowly, and thus achieve high profitability. However, their firm values appreciated by stock markets are not as high as those of the US firms. In the second dimension of convergence in innovation systems, the paper finds some important evidence of convergence, such as no significant linkage between (short or long) CTT and firm profitability and a significant linkage from higher self-citation to firm values. This new pattern is exactly the same pattern found in the US firms by Lee [

18], which is a reflection of an increasing level of technological capabilities of the Korean firms and is indicative of convergence in the innovation system of Korean firms. The unfinished part comes from the finding that, although the Korean firms are shown to be diversifying into non-short CTT-based sectors, their growth mechanism is still shown to have not changed much, still relying on fixed investment associated with high capital–labor ratio than technological capability associated with self-citations.

The story of firm-level changes in Korea analyzed in this paper is consistent with a country-level finding by Lee and Lee [

21] that economic growth (per capita income) of Korea is now positively associated with long CTT of the country, as Korea is now moving toward long CTT-based sectors, such as bio medicines and products and high-tech materials and components. Given that the overall level of CTT in Korea (9 years) remains way shorter than that of Germany (12 years) (Figure 1A in [

21]), the shift toward long CTT continues to be an ongoing process. Interestingly, this gap between Korea and Germany is consistent with their gap in per capita GDP in PPP terms, such that that of Korea has now reached the level of Japan or 70% of the US, whereas that of Germany is approximately 85% of the US according to the more recent data from IMF released in 2021.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}