1. Introduction

One of the challenges for local government officers, surveyors, property managers and administrators is the generation of meaningful and timely information and analysis to inform strategic management of the public sector estate and strategic policy development across the wider built environment. In today’s world of big and open data, the challenge is less the generation of urban property data, but more how this information can be exploited and integrated successfully into contemporary public sector strategic property management and wider decision making. Wyatt [

1] identified a large number of applications of GIS in land and property management, including: property conveyancing; local authority property management (council tax and rates, maintenance, identification of under-used property); development planning; agriculture and habitat management. Central to this is the opportunity afforded by ’big data’ for society and its institutions to glean insight into urban land and property markets from comprehensive datasets that are increasingly available open source or under licence in digital form. However, Jozefowicz et al. [

2] found that the exploitation of geospatial data in the UK was still hampered by a number of factors, including: lack of awareness of the potential of the data; data ownership and availability issues; shortage of skills; data quality and consistency.

One such big dataset in the realm of land administration and taxation is the National Non-Domestic Rating list that is used in the UK to levy business rates on the occupiers of all non-domestic (non-residential) property. Business rates income is an increasingly important component of the UK’s national tax regime, with the Ministry of Housing, Communities and Local Government predicting that it will raise £25 bn in 2019–2020, an increase in £206 m from the previous year [

3]. Local authorities in England and Wales are increasingly reliant on income from business rates due to £16 bn reduction in central ‘block grant’ funding since 2010 [

4]. Since 2013 all local authorities in England and Wales retain 50% of their business rates, with pilot authorities retaining 100% of their business rates income since 2017 [

5]. This article explores the potential for central and local government and its agencies to exploit this comprehensive national dataset to explore the distribution of commercial property, its quantity and value by adding geospatial and temporal dimensions in visualising the data through the application of Geographical Information Systems (GIS)

The ability to analyse metadata pertaining to geolocated points within a GIS provides researchers and policy makers with the ability to investigate spatial and temporal patterns in data and is a fundamental methodological approach in a diverse range of disciplines including epidemiology [

6,

7], criminology [

8] and political science [

9]. In the discipline of real estate economics, the distribution of the quantity and price of both commercial and residential property can be evaluated. In many cases, this leads on to an investigation of the relationship between property price and one or more spatial variables. For example, Seo et al. [

10] investigated commercial property values in relation to light rail and highway infrastructure, considering both their negative and positive effects. Koramaz and Dolmeci [

11] explored the spatial determinants of house prices in Istanbul whilst Atreya et al. [

12] specifically investigated “implicit flood risk premium”, revealing a discount in property prices in previously-inundated areas than in comparable areas that had not flooded. Cellmer and Trojanek [

7,

13] used data on apartment sales to create a price map with which to explore the influence of positive and negative externalities such as proximity to green spaces or “bad neighbours” as sources of noise or pollution; they also mapped temporal variability—the distribution of the average annual price change. Netek et al. [

8,

14] demonstrated that value maps can be used to better understand the locational preference of creative industries. Despite such examples, there has been relatively little progress made in exploiting Rating List data in the UK since the pioneering work of Thurstain-Goodwin and Unwin in 2000 [

15], the Office of the Deputy Prime Minister (ODPM) and Centre for Advanced Spatial Analysis (CASA) in 2002 [

16], and Katyoka and Wyatt in 2008 [

17]. Indeed, the UK Government’s own Cabinet Office recently admitted that whilst it recognises that better use of geospatial data in the public sector would create additional economic and social value, this has yet to be accurately estimated [

18].

Geospatial analysis of commercial property data also presents us with an opportunity to investigate whether commercial and industrial location theories, established by the likes of Weber [

19], Losch [

20], Isard [

21] and Alonso [

22], in the early to mid-twentieth century, are still relevant in this age of private mobility, footloose industries and ICT-enabled e-commerce and business. In particular, retail land use theories such as Central Place [

23], Spatial Interaction [

24], Bid Rent [

25] and Minimum Differentiation [

26], are being challenged as never before, by e-tailing and next-day fulfilment, as consumers continue to move from ‘bricks to clicks’. At the same time, researchers should be mindful that causal relationships are unpredictable; relationships are interactive, dynamic and complex: social, environmental and economic factors affect one another, including proximity to resources and to markets, transport infrastructure, suitability of accommodation and topography, agglomeration economics and state intervention [

27,

28]

In the UK, all non-residential property is taxed on the basis of its ‘rateable value’ (RV), which is benchmarked, or revalued, by the Valuation Office Agency (hereafter referred to as the VOA), on behalf of Government, every 5–7 years [

29]. Due to the predominantly privately owned, complex and fragmented tenure of commercial real estate in the UK, RVs are calculated for hereditaments, which represent smaller units of property rather than whole buildings. A hereditament is defined by Myers and Wyatt [

30] as:

‘a piece of real, inheritable and taxable property on which (business) rates can be charged. A hereditament generally corresponds to an extent of floor space suitable for a single occupant and might comprise a piece of land, a number of separate buildings, a single complete building, one or more floors within a building, or part of one floor.’

(Myers and Wyatt (2007), p. 288)

According to the VOA [

31] there are approximately 1.95 million hereditaments in England and Wales (Scotland and Northern Ireland operate separate systems based on broadly similar principles). Of those hereditaments where floorspace data are published, there are approximately 7 billion sq ft (659 million sq m) of floorspace, 60% of which is industrial, 13% offices, 16% retail and 11% other. Local authorities in England and Wales bill occupiers and owners of all non-domestic property for payment of rates using the National Summary Valuation Data Set, which is created and maintained by the VOA on behalf of the UK Government. The non-domestic rating dataset is published online in order to allow parties with an interest in a property to check rating valuations and that of comparable properties, but also to enable anyone to exercise their right to view rating assessments in the compiled rating lists [

32]

The VOA generates and holds information on every single non-residential premise in England and Wales, along with postcodes, RV, business type and total floor space, the list of which is provided to all local authorities as the basis on which they levy business rates. These are calculated by multiplying the RV (based on the market rent at the date of valuation) by the business rates multiplier set by central government (the standard rate is currently just over 50p in the £ or 50%) [

33]. Periodic downward adjustment to the national business rate multipliers coincides with business rate revaluation and the introduction of the ‘new’ rating list which occurred in 2000, 2005, 2010 and 2017.

All non-domestic premises are revalued periodically based on an antecedent date of valuation. Thus, the most recent business rates revaluation, 1st April 2017, based on each property’s RV on 1st April 2015 [

29] effectively means that RVs are already two years out of date when the ‘new’ rating list is introduced. Similarly, the previous 2010 rating list was based on 2008 values and the next revaluation, due in 2021, is based on market values as of at 1st April 2019. It is worth noting that the date of valuation of the 2010 rating list (1st April 2008) coincided with the pre-recession peak of the property market in the UK, resulting in business rates being higher for many premises than ‘market’ rents for seven years [

4]. In 2017, the UK Government announced that revaluations would take place every three years instead of five years after the next revaluation in 2022. The Government subsequently announced that the next revaluation was to be brought forward to 2021, with the following revaluation taking place in April 2024 [

34].

It is pertinent to note that, unusual among developed economies, the UK does not have a single, complete cadastre [

35]. Even the Land Registry, which records the details of all property transactions in the country, does not have records pertaining to the entire country, since registration has only been compulsory since 1990 and some properties have not changed hands in many decades or even centuries; nor does it record the exact boundaries of parcels of land [

36,

37]. Effectively, the UK has two partial cadastres, the Rural Land Register, a database of agricultural land with sizes and geo-references, linked to farmers and their applications for EU funding; and the fiscal cadastre consisting of the VOA’s database, together with council tax data [

35].

As Dale and McClaren [

38] observe, whilst the need for land (and property) information in support of development becomes ever more urgent, there is opportunity to improve land administration systems, driven by developments in technology, and land and property datasets that grow ever larger. Thus, the VOA’s comprehensive dataset affords the opportunity not only to represent the quantity (m

2) and relative value of non-domestic property in the UK at the date of the new rating list being published (albeit with a 2 year time-lag), but also to capture changes in the quantum of floorspace and value between census points.

The research seeks to explore the potential to use the VOA’s dataset to create a methodology that can be used to portray, analyse and manage the non-domestic real estate at a local level, as the backdrop against which robust strategic decisions about capital investment and spatial interventions can be made. Such analysis would potentially be of use to metropolitan and city mayors, chief executives of local authorities, public sector estate managers, spatial and transport planners, economic development officers, town and city centre managers and other functions that require comprehensive representation of changes in the stock and performance of all commercial and industrial within their jurisdiction, at a variety of spatial scales.

Specifically, all local authorities in the UK need to conduct regular employment land reviews. These are currently subsumed within Housing and Economic Land Availability Assessments (HELAA) that require them to capture the quantum and distribution of all employment floorspace in their area by bulk class, relative values (strength of market demand) and performance between census points (periodic rating revaluations) to reveal changes in stock and value (tell tales of market changes). The aims of such reviews are to determine whether existing employment land and buildings meet the needs of the economy and identify how much additional land should be allocated for employment use within a local authority’s jurisdiction [

39]. Typically, local authorities pay private sector consultants to carry out such reviews on their behalf when they already have a comprehensive dataset of all employment floorspace in their borough or district. It is surprising that local authorities do not make more use of the VOA rating list as the basis of such studies, as it represents, by bulk class or subsector, the distribution and quantum of all employment floorspace in any given local council district.

Thus, the aim of this research project is to explore the potential of non-domestic business rates (big) dataset to capture/represent distribution and change in stock and value of commercial and industrial property (hereditaments) in England and seek to answer the following questions for a given area:

How has the stock of retail, office and industrial floorspace changed between 2010 and 2017?

What is the efficacy of using geospatial techniques and rating list data to measure stock and value change?

What is the most effective way of visualising business rates data in GIS to analyse the quantum and spatial distribution of employment floorspace?

2. Materials and Methods

2.1. General Approach

This research seeks to develop a general methodology for analysing and portraying the spatial distribution and temporal performance of commercial real estate markets using a three stage approach (

Figure 1), comprising the three domains of data classification, quantification, spatial granularity, connected by two interfaces.

2.2. Methodology

Commercial and industrial property data, in the form of the ‘National Non-Domestic Rating’ (NNDR) list, were supplied in an Excel spreadsheet. Each record pertains to a single hereditament, containing the name and address of each business, the business’ type of activity, the floorspace of the premises, and its RV. The total number of hereditaments in York was 5953 in 2010, 6562 in 2017 and 6802 in 2019. This increase in the number of hereditaments between revaluations is consistent with national trend where the number of hereditaments increases over time but not necessarily aggregate floorspace.

Filtering and classification of data into three bulk classes followed the approach developed by Muldoon-Smith et al. [

40]. Each record was classified by the VOA as falling within one of several hundred Special Categories (SCats) denoting the type of business. These are grouped into four aggregate categories—the three “bulk classes” of retail, office and industrial properties, and a catch-all “other” category which includes a wide variety of properties (i.e., leisure, education and sui generis uses; easements, wayleaves, advertising hoardings, bus shelters, sponsored roundabouts, telecommunications infrastructure etc.). Each bulk class contained a sufficiently large subset of records, pertaining to hereditaments with some common features, for broad trends to be observed and outliers to be identified. For example, in York in 2019, after filtering and classification, the dataset comprised 1210 industrial, 1522 office and 1867 retail property units, respectively.

Floorspace data were obtained by linking the NNDR data to a second VOA dataset, known as the ‘Summary valuations list’. This dataset provides more detailed information as to how the RV for each hereditament was calculated, which, for most types of commercial property, is based on a calculation of the open market rental value per m

2 of a given type of property in a given area. Hereditaments were geocoded by postcode using the online geocoding tool provided by Bell [

41]. Three different datasets were generated in this way. One was based on records from the 2010 revaluation of commercial property, another was based on the 2017 revaluation and the final one was based on the complete rating list as at April 2019.

RV and floorspace (m

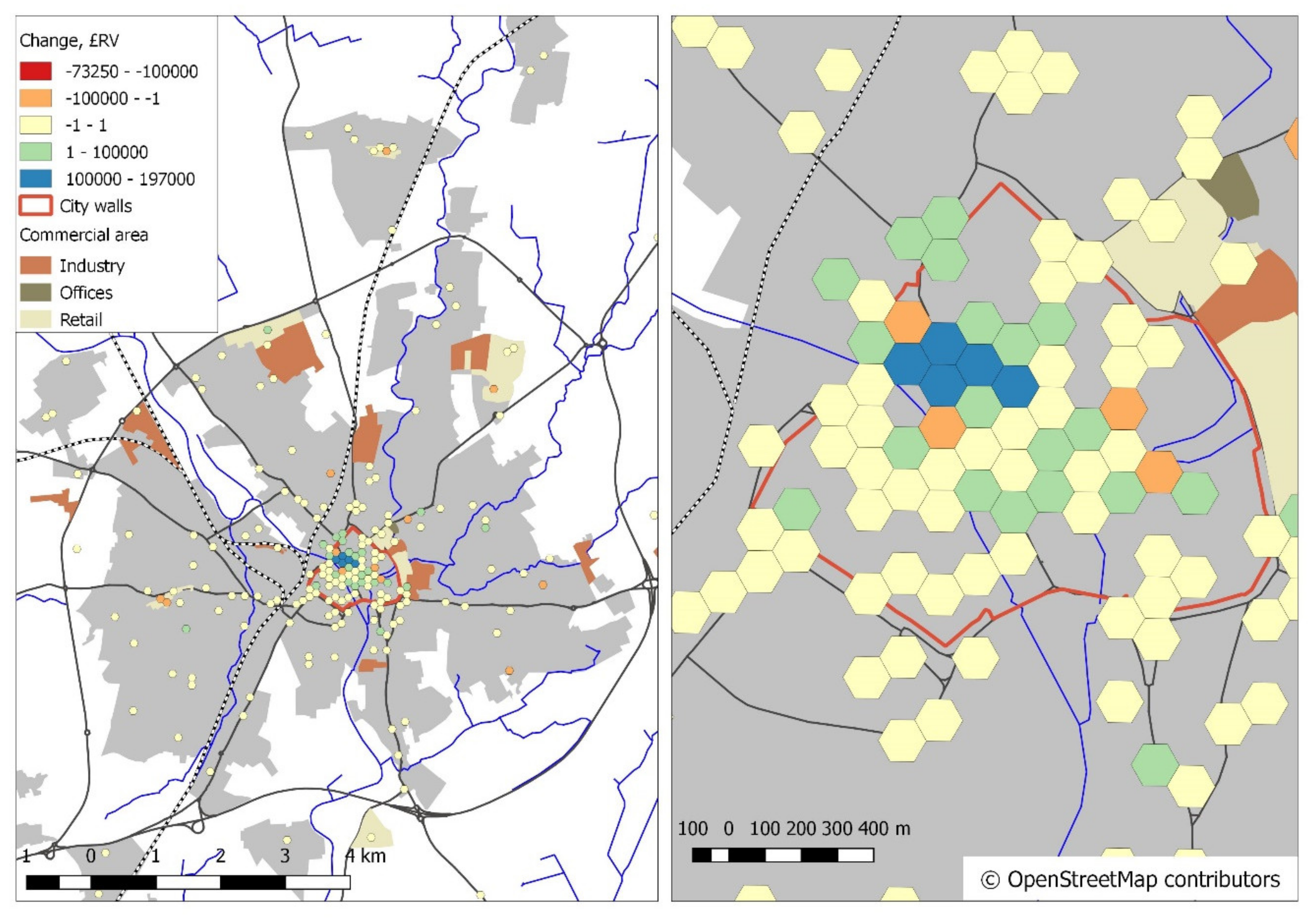

2) for hereditaments within each bulk class were then aggregated within a 100 m diameter hexagonal grid and RV per metre squared (RV/m

2) was calculated for each grid tile. The use of a hexagonal grid was determined by a process of experimentation with different geographies. As Ben-Joseph and Gordon [

42] note, the advantage of hexagonal or octagonal street layouts in the built environment is that they permit movement in six or eight directions, whereas square grids do not permit diagonal movement. A related point with the use of hexagonal grids in spatial analysis is that a grid tile’s adjacent neighbours in all directions are equidistant, forming a ring around it; this makes it easier to analyse movement or connectivity as exemplified by Burdziej [

43]. In our study, the use of hexagons helped to address the modifiable area unit problem (MAUP) first identified by Openshaw and Taylor [

44]: because streets in York generally run diagonally relative to the north axis, the hexagonal grid offered the potential for closer alignment with the underlying street pattern and therefore, reduced boundary problems. It was determined that the use of a coarser-grained grid (500 m diameter) was insufficiently sensitive to display patterns of clustering, growth and decline across a given urban area. The use of smaller hexagons, meanwhile, was too fine-grained for general trends to be observed.

The process was then repeated using a different geography—the polygons indicating the coverage of each postcode within the study area (i.e., in theory, the polygon containing all the addresses that are classified within a given postcode). The aggregated results could then be displayed in choropleth maps to indicate patterns of growth and decline across the study area, and within the city centre. It is worth noting that in map form, the impression of variability in RV/m2 depends on appropriate classification, since, if the same categories are employed as for retail properties, most values fall into the lowest-value category in which properties have a RV/m2 of less than £100/m2. In all cases, classification was by the Pretty Breaks function in QGIS, modified by conflating higher-valued classes and by altering classification breaks to make up for the distorting effect of outliers.

2.3. Methodological Caveats

2.3.1. Geocoding

Items were geocoded by postcode which meant that rather than being geocoded to the exact location of the relevant hereditament, they were actually geocoded to the centroid of the relevant postcode polygon. As Jacquez notes, the fundamental process of converting text-based addresses into geographic coordinates is often prone to positional error and the difference between a true location and that returned from the geocoded address is not routinely addressed [

45]. Postcodes generally contain a similar number of addresses; postcode polygons vary in size according to the density of development and addresses, within the area in question. Therefore, within densely populated areas, the granularity of the resultant mapping is greater when postcode polygons are used, because they cover a smaller area than grid hexagons. They also tend to correspond well to the underlying street pattern because they contain a certain group of addresses in close proximity. However, in less-densely-populated areas, postcode polygons cover larger areas, often covering relatively large areas of undeveloped or unoccupied land. This leads to some less than informative, perhaps misleading, results where, for example, a large amount of commercial property is found on a site that falls within a very large postcode polygon; following aggregation, it is not possible to tell which part of the larger polygon is commercially attractive, and which is not. This is particularly true for industrial property, which is often located in areas with large postcode areas. If values are aggregated within any other polygon geography, not based on postcode polygons, there is the potential for values being aggregated within the wrong polygon altogether (i.e., the correct location should be within polygon A, but the centroid of the relevant postcode polygon falls within polygon B).

2.3.2. Inertia in the Stock

There is likely to be a time-lag affecting the relationship between the indicator, and market demand. The quantity (m2) of commercial property changes only when units are demolished, constructed, or when existing properties undergo a change of use. This may take place some time after the property falls out of its original use. Consequently, for example, the former Terry’s factory in York, which closed in 2005, was still recorded within the 2010 dataset.

2.3.3. Absence of Vacancy Data

There is one significant shortcoming in the VOA’s data—they do not indicate whether the property is occupied. When businesses fail, in the first instance, it is likely to lead to an increase in vacant properties rather than a decrease in properties per se. From the point of view of local authorities’ immediate finances, this may not be very important, since landlords are still liable to pay rates on empty properties, after a 3-month reprieve [

46]. In order for policy makers to understand the relative performance, resilience or vulnerability of employment locations, the levels of occupation and vacancy of business units needs to be captured and portrayed.

2.3.4. Inertia in Valuation

All hereditaments in the 2010 and 2017 datasets are ascribed RVs at the respective antecedent date of valuation, that are two years out of date at publication of the ‘new’ rating list. Datasets obtained at later dates will continue to be valued at the antecedent date (although individual properties may be revalued at other times on request, or if circumstances change—for example, if the property changes use or is extended). When market value increases or decreases, then the static RVs become out of line with prevailing market rents. This fixed census date also prevents the opportunity to use the dataset to investigate gradual, market-based change in RV from one year to the next.

2.3.5. Data Inaccuracies

The research encountered errors in the National Rating List dataset mainly due to inconsistencies in the categorisation of properties within SCat codes. For example, some supermarkets were categorised as retail warehouses; some shops below 750 m2 were mistakenly categorised as “large shops”; similar shops were categorised as “shops” and “food shops” in different areas. The research also discovered that some postcode polygon boundaries do not correspond exactly to the divisions of space found in the built environment. In particular, outside dense residential areas, postcodes often subdivide parcels of land and larger buildings, and sometimes do not include properties with the appropriate postcodes within their boundaries.

2.3.6. Zero-Rated Properties

A small number of properties in the ratings list are recorded as having a RV of 0 or 1. This applied to relatively few units (less than 2000) but, if larger properties were involved, there was potential for this to skew the results—for example, by bringing down the average RV/m2, or by bringing down the aggregate RV in a given area.

2.3.7. Non-bulk Class and “Other” Properties

The starting point for the valuation of most commercial properties is a calculation of the market rental value per m2 of a given type of property in a given area (the tone of the market). However, there are certain property types whose value is calculated by alternative methods such as profits method or contractor’s test (depreciated replacement cost). Therefore, their floorspace is not published within the “summary valuations list”. This includes some categories of business which may be particularly significant in certain areas, including public houses and bed and breakfast accommodation.

It is worth noting that the “other” category, containing heterogeneous premises that cannot be regarded as a single class of property, does contain some types of business, such as cafes and restaurants, that are important to the socio-economic vitality of town and city centres. When contemplating trends affecting retail and office property, it is necessary to have regard to the interaction between bulk class properties and some “other” subcategories, including those for which floorspace is not recorded.

2.4. Description of Study Area

The City of York, in North Yorkshire in England, has a small, compact but pronounced retail core, with most commercial activity focused within the city’s unusually complete mediaeval city walls. York has three prominent out-of-town shopping centres: Monk’s Cross/Vangarde, to the East of the city; Clifton Moor, to the north; and the York Designer Retail Outlet, to the south. The city is heavily reliant on tourism, being a popular stopping-off destination for international tourists travelling between London to Edinburgh, and domestic demand from its large rural hinterland.

York City Council’s own research on the city’s economy listed the following strengths: a highly-skilled population; low unemployment; good digital infrastructure; the city’s position on the East Coast Main Line with excellent connections to London and Edinburgh; high employment in industrial biotechnology and agri-food research, insurance and rail; its 7 million visitors per year. Weaknesses included: lack of available land for business expansion, low-productivity and part-time jobs, and a mismatch between skills and jobs; congestion on the Outer Ring Road; and competition from other centres. Retail and wholesale made up 16% of the city’s employment but 11% of its Gross Value Added. The number of retail jobs was predicted to grow by 2% in the 10 years from 2016 [

39]. The study area included the entire conurbation.

As we note above, the aforementioned hexagonal grid was particularly efficacious with regard to the City of York because the underlying (predominantly medieval) street pattern in the centre of the city, in which streets (colloquially known as Gates) generally run southeast to northwest, or at 90 degrees to these, partly due to the River Ouse running through the city in a northwest to southeast direction.

York City Council has produced a new Local Plan (hereafter referred to as the Plan), which is currently awaiting approval from the Planning Inspectorate that assesses local planning policy against national requirements on behalf of the Government. The Plan defines certain areas within the Council’s jurisdiction for various purposes—notably, areas within which development is more tightly controlled than elsewhere for the protection of the natural or built environment, and areas where particular types of development are encouraged, such as retail or other employment [

47,

48].

The Plan establishes a hierarchy of retail centres, at the top of which is the city centre, much of it classified as “primary shopping area”, below this are two suburban areas of Acomb and Haxby, classified as “district retail centres”, then clusters of shops, known as “local retail centres”. Although the Plan acknowledges the existence of out-of-town retail centres at Monk’s Cross, Clifton Moor and the York Designer Retail Outlet, it does not allocate their sites for retail, or for any other type of development. Rather, it states that further proposals for out-of-town retail will only be permitted if they cannot be accommodated upon a sequentially preferable site (that is, a site further up the retail hierarchy).

The Plan allocates eleven sites for employment, of which five are classified as “strategic” because they are over 5 hectares in size, despite covering a combined area that is smaller than existing employment areas, as indicated in

Figure 2. The Plan implies that established sites should continue to be used for industrial or other commercial purposes but does not explicitly identify which sites are covered by the policy [

47,

48].

Having regard to both the potential and limitations of the data, the following section presents results of the aggregation and spatio-temporal analysis of the stock and value for the three bulk classes of property in the City of York, between 2010 and 2017.

4. Discussion

The study has demonstrated the potential opportunities for national and local governments to exploit national non-domestic rating (NNDR) data to capture and represent changes in the quantum, spatial distribution and relative value of employment floorspace by sector e.g., retail, office and industrial premises over time. The use of this comprehensive dataset means that all premises, regardless of size, status or sector, are captured. The authors propose that RV/m2 can be used as a proxy for market attractiveness, since it provides a consistent measurement of the value of properties of different sizes in different locations.

The study revealed that whilst retail and office agglomeration persisted in the city centre, consistent with classical commercial property location theory [

20,

22,

23], there were significant clusters of commercial floorspace on the peri-urban fringe, particularly at intersections between radial transport corridors and the city’s ring road. The result of this effect is an emerging binary commercial property market generating increased vehicle movements, not only by customers but also employees working in retail and office sectors. The industrial sector in York, by contrast, is relatively small, dominated by two large concentrations of manufacturing floorspace, and has recorded a decline in floorspace that is inconsistent with the national trend. Of all property sectors, location is most critical to retail property, relying as it does on footfall and pedestrian flows; it is also the sector that appears most vulnerable to change. Temporal analysis of rating list data has revealed that polarised growth of out-of-town retail has created a binary commercial property market that risks hollowing out the historic city core. Further refinement of the methodology allowed data to be segmented within bulk class categories, for example retail bulk class data could be segmented between traditional retailing and the food and drink sector. Analysis confirms that York’s city centre is changing, with increased representation of food and drink uses that, to some degree, has compensated for the hollowing out of traditional retailing. The methodology also offers potential to differentiate between smaller and larger shops, convenience and comparison shops, or higher and lower order goods.

The methodology presented in this article could usefully be employed in the administration of land and property by a variety of stakeholders, including central and local government, regional, sub-regional and metropolitan authorities, economic development agencies, spatial planners, economic development strategists and town and city centre managers. It may also prove useful to real estate investors, landlords and the firms and businesses that occupy employment floorspace. The method creates opportunity to explore relationships between the performance of employment floorspace and wider socio-economic factors such as technological change, government fiscal and spatial policy, transport and demographics, all of which have an impact on the future viability of commercial and industrial property markets.

Geospatial data have an important role to play in understanding prevailing physical, economic and social conditions within urban areas and offer a way of exploring and representing the interrelationship between the location of fixed infrastructure and built environment (physical) assets, and more dynamic patterns of market performance (economic) and movements (social). The use of a large corpus of up-to-date data can improve our ability to model the potential outcomes of anticipated urban interventions, perhaps as part of scenario modelling or options appraisal. As Thompson et al. [

52] observe, urban policy makers and planners are hampered by a mismatch between the future world in which their decisions will take effect, and the past world on which they have information:

“planning (for the future) is always conducted through the rear view mirror.”.

(Thompson et al. (2016) p. 81)

The case study presented in this article demonstrates that, whilst this might be true, there is big data available in the UK with which to accurately track changes in the distribution and relative value of prevailing land uses over time and space. Having comprehensive and accurate quantification of the stock and value of all employment floorspace would inform local government officers, surveyors, property managers and planners when conducting land administration, spatial planning, economic development, and other policy making. We have shown that geospatial analysis is a powerful tool that can ‘add value’ to existing big datasets, by mapping and analysing the quantum, spatial distribution and relative value of commercial and industrial floorspace across an urban area relative to other spatial characteristics. The analysis of rateable value and floorspace data also affords the opportunity to investigate the relationship between economic performance and variables for which spatial data are available such as transport networks, flood risk, urban form and population distribution. The use of temporal data across census points offers the opportunity to map and analyse patterns of change, revealing which sectors of the economy are growing, in terms of the quantity of floorspace occupied, and which are declining. Analysis employing such data can be used to test whether ‘traditional’ theories of industrial and commercial location are still as relevant in economic sectors that are prone to disruption through technological advances and mobile communications. The next steps are to exploit NNDR data to replicate the methodology for other towns and cities in the UK to permit comparative analysis of the performance of different locations, over time, to determine whether trends in the quantum, distribution and value of employment floorspace observed in York are being experienced more widely.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}