Do Rare Earths and Energy Commodities Drive Volatility Transmission in Sustainable Financial Markets? Evidence from China, Australia, and the US

,

,

,

,  ,

,

Abstract

:1. Introduction

2. Related Studies

3. Material and Methods

3.1. Data

3.2. TVP-VAR Approach

4. Empirical Results

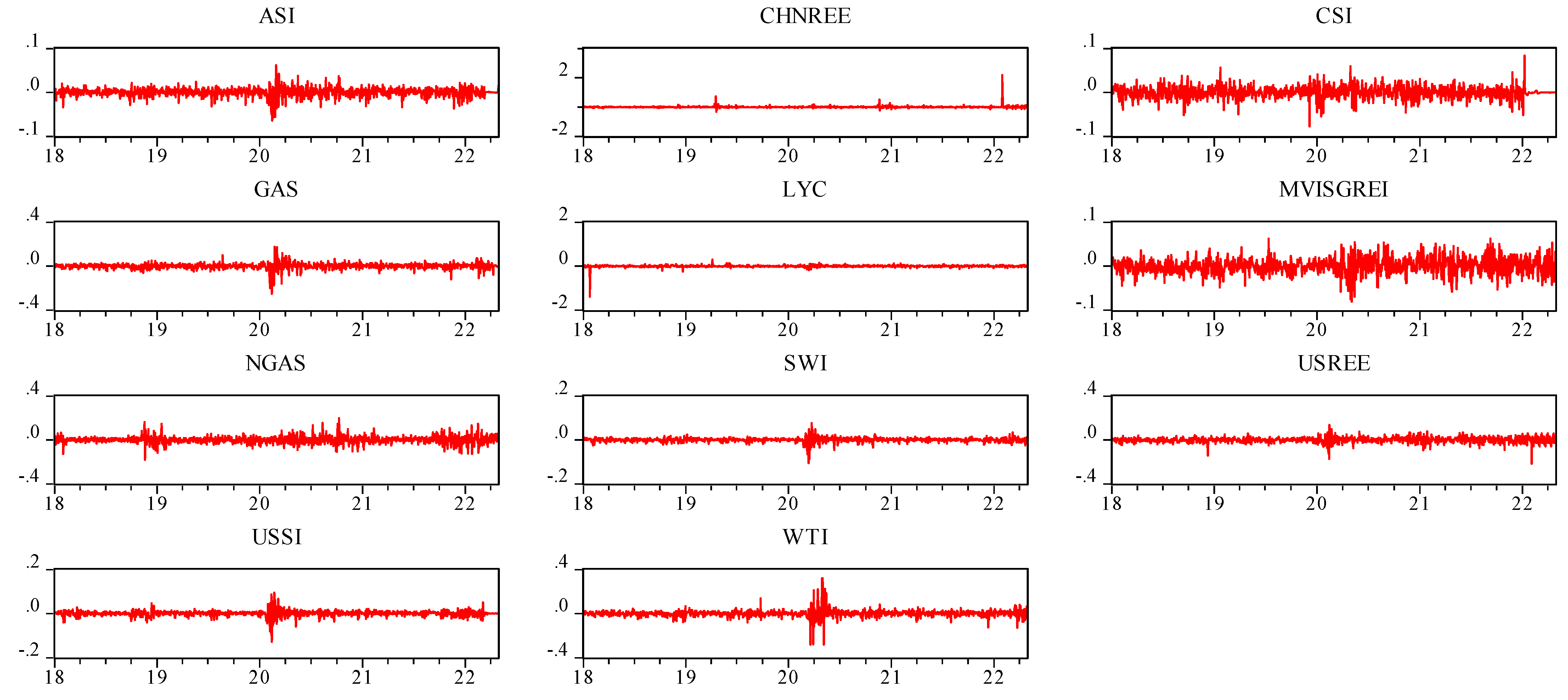

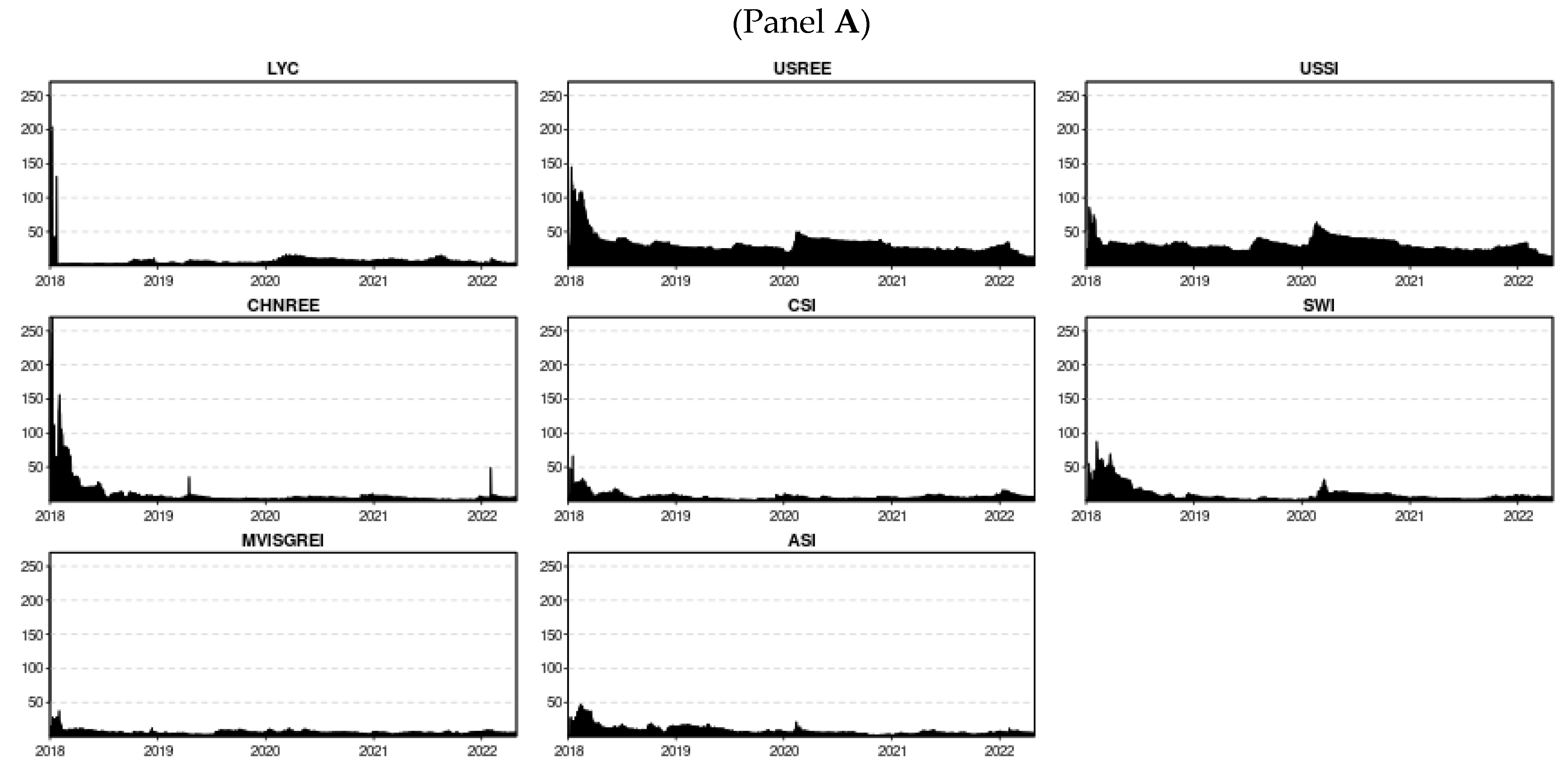

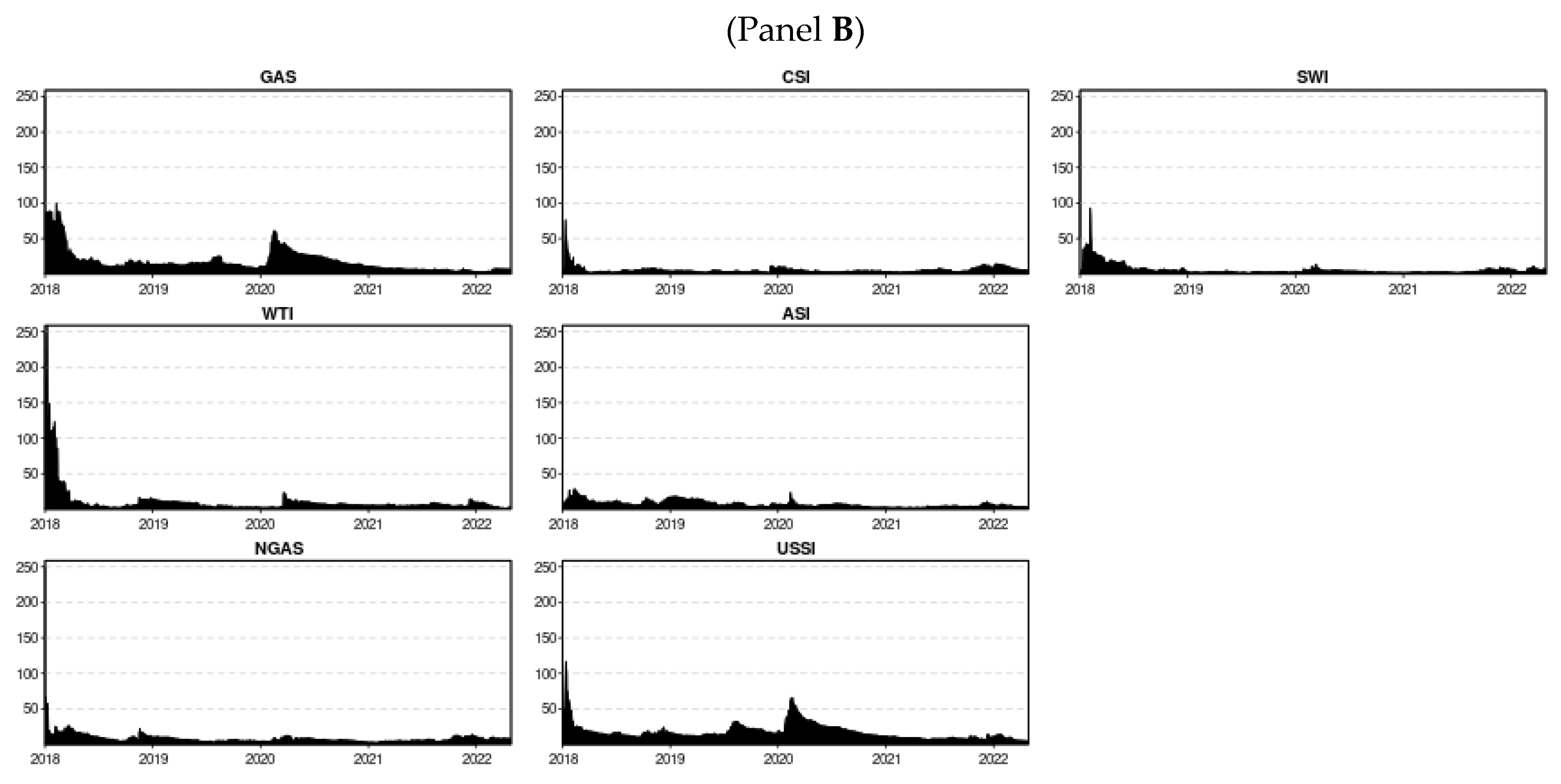

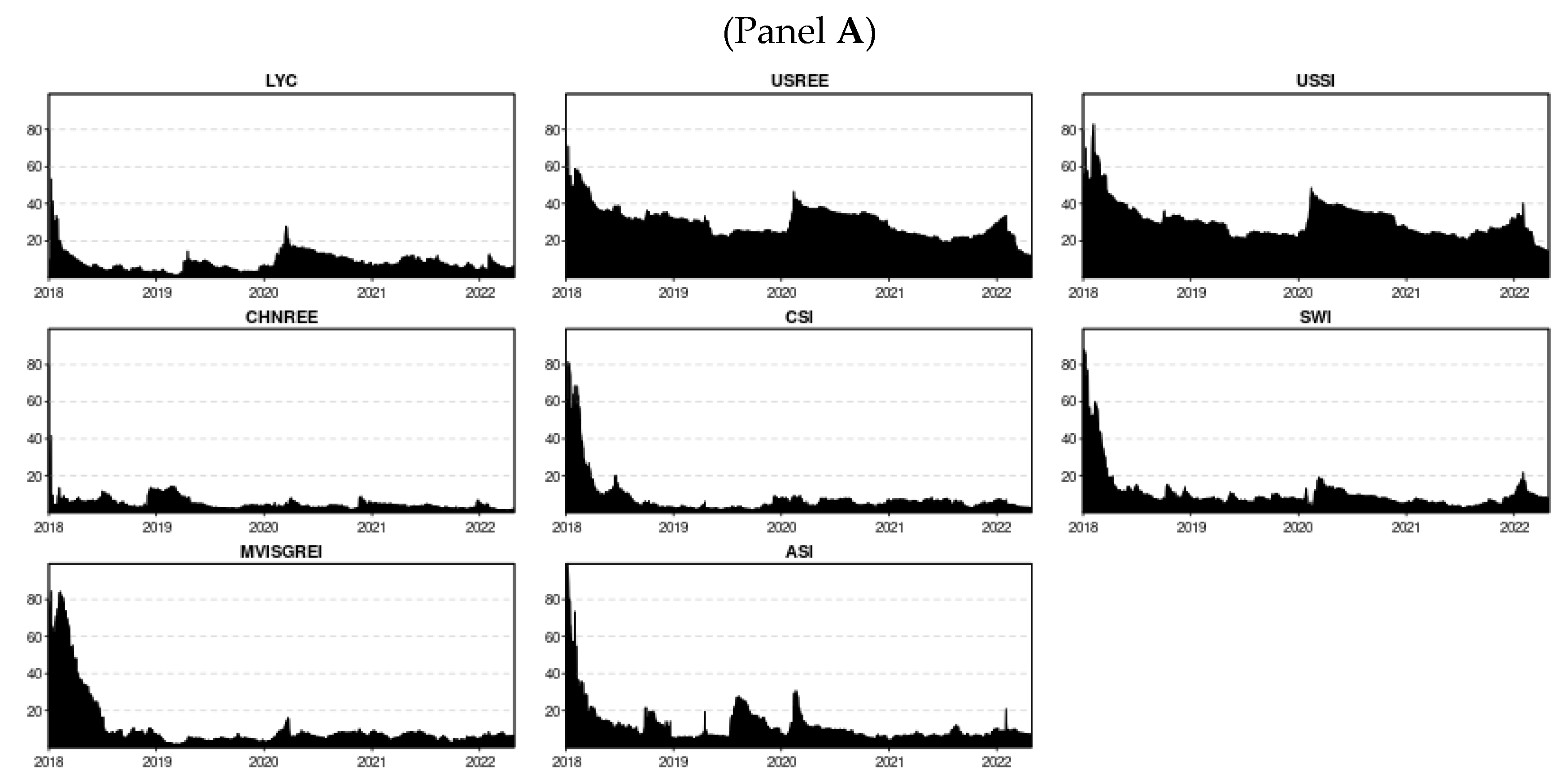

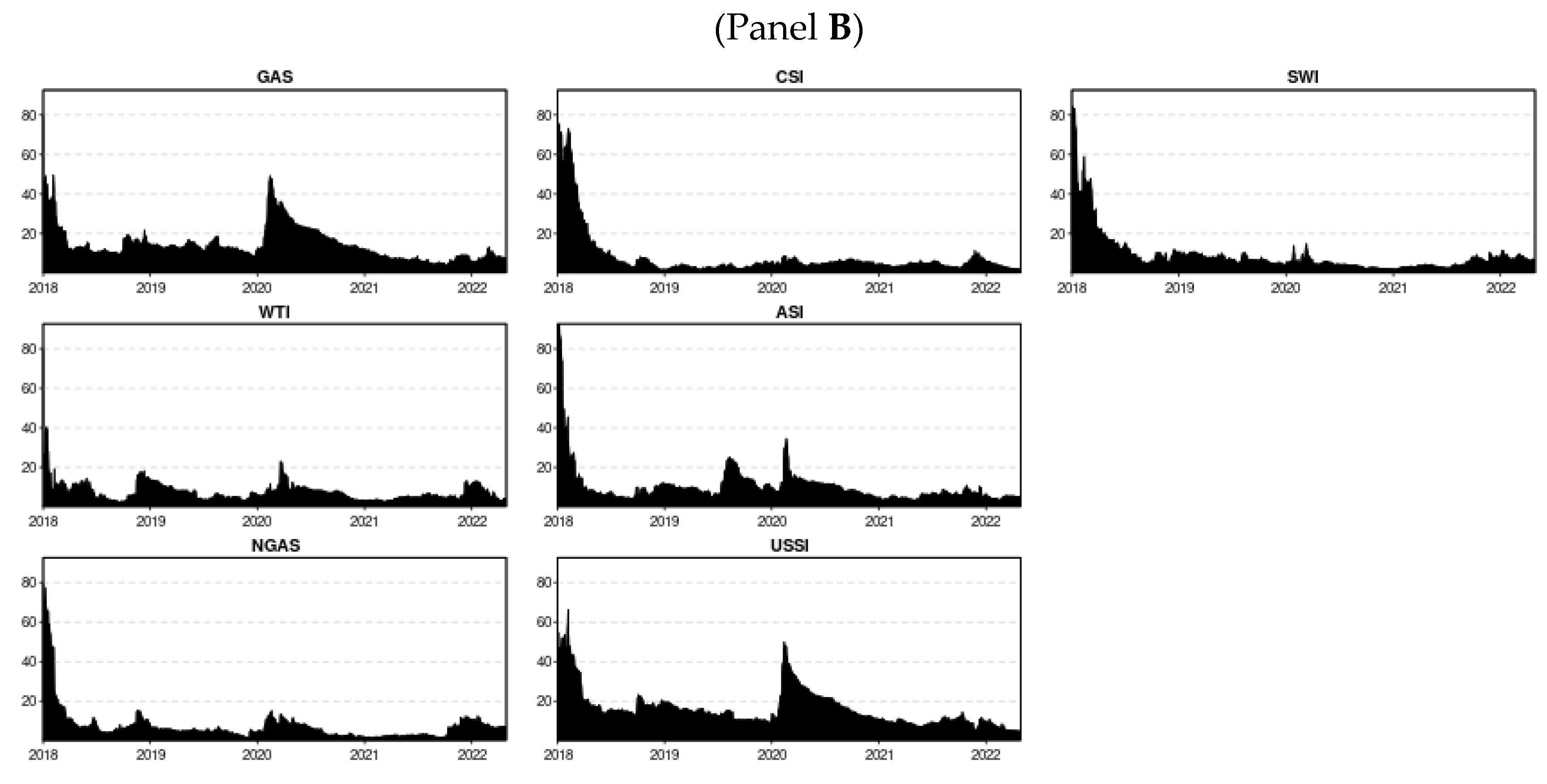

4.1. Preliminary Statistics

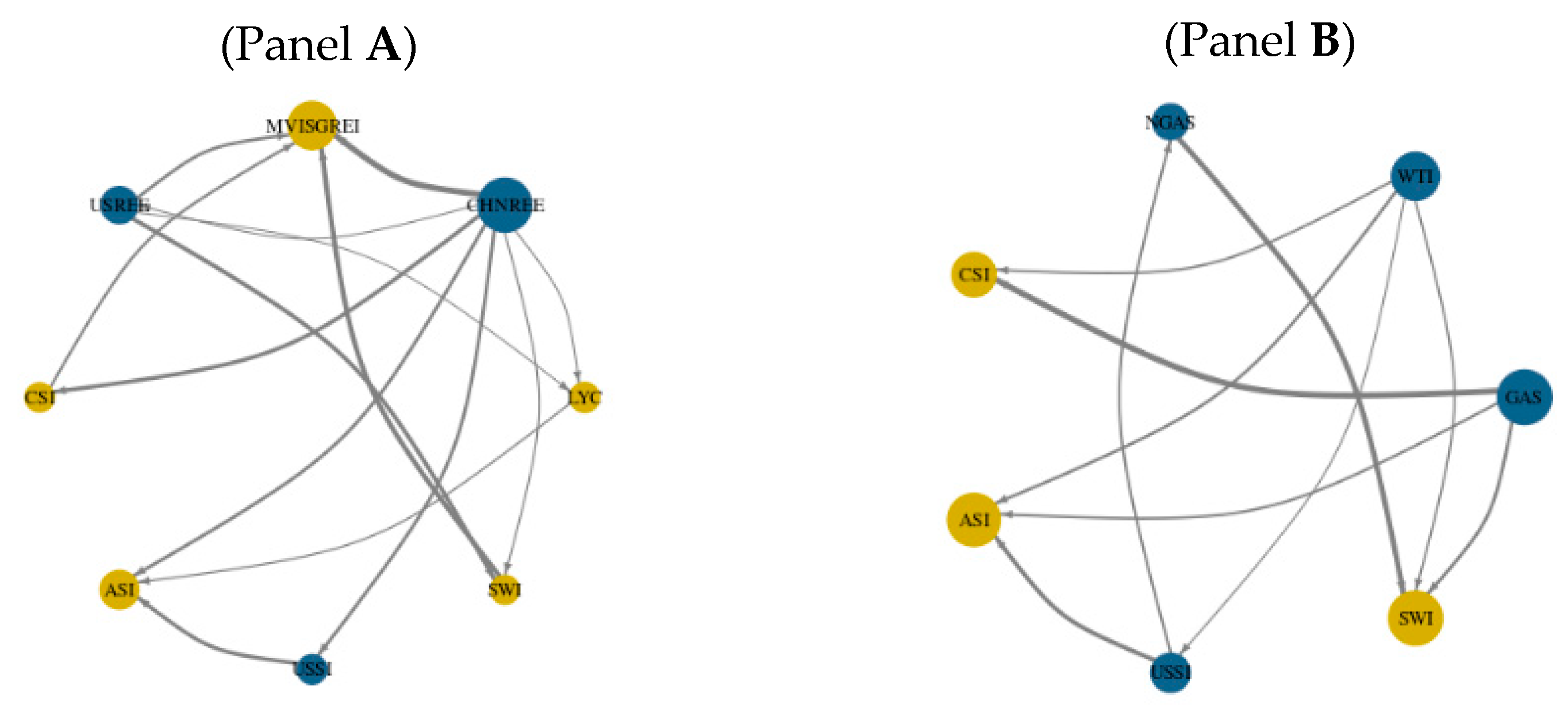

4.2. Evidence from Dynamic TVP-VAR Approach

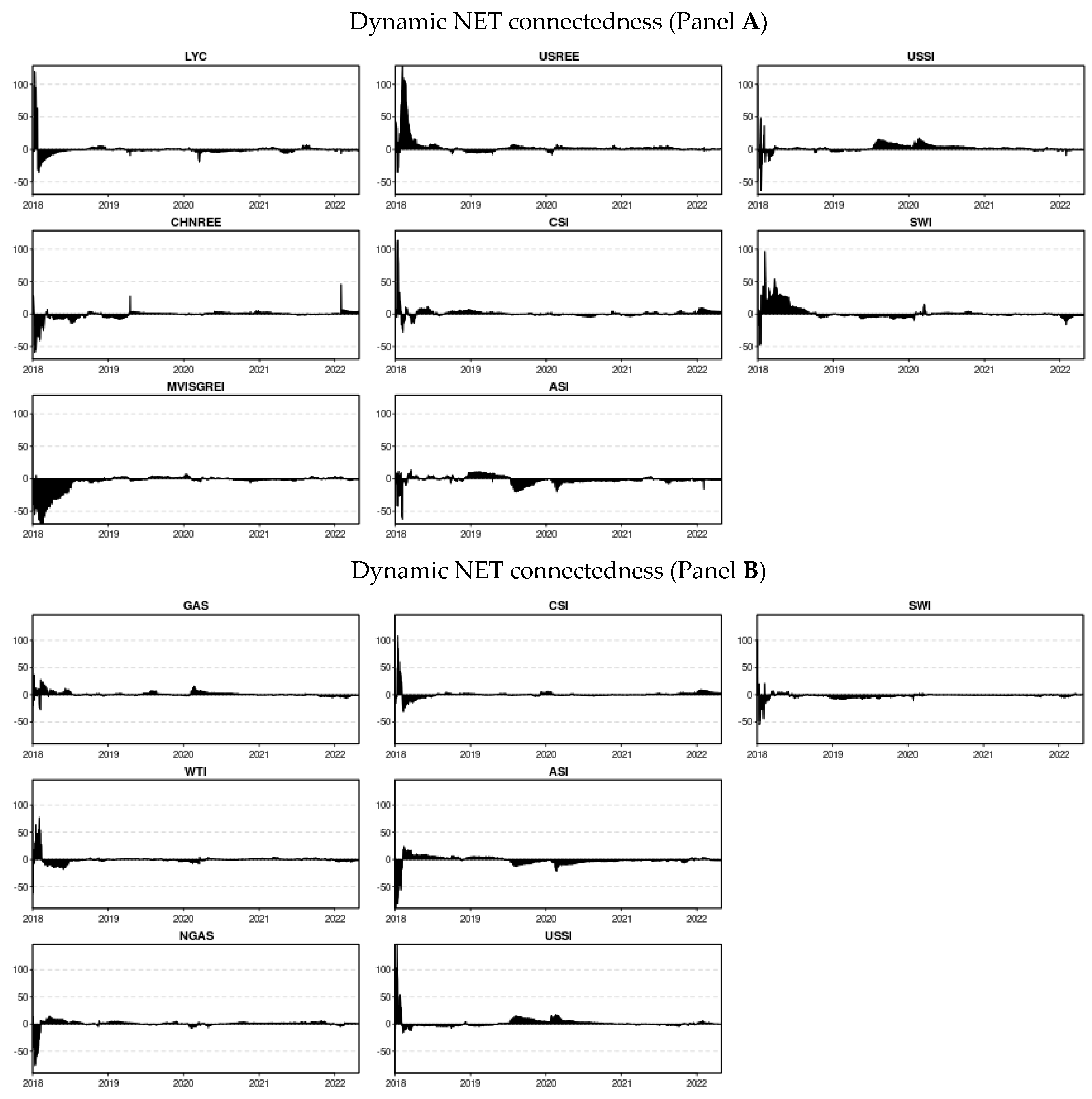

4.3. Time-Varying Total Connectedness

5. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| 1 |

References

- Ajmi, Hechem, Nadia Arfaoui, and Karima Saci. 2021. Volatility transmission across international markets amid COVID 19 pandemic. Studies in Economics and Finance 38: 926–45. [Google Scholar]

- Akhtaruzzaman, Md, Sabri Boubaker, and Ahmet Sensoy. 2021a. Financial contagion during COVID–19 crisis. Finance Research Letters 38: 101604. [Google Scholar] [CrossRef] [PubMed]

- Akhtaruzzaman, Md, Sabri Boubaker, Brian M. Lucey, and Ahmet Sensoy. 2021b. Is gold a hedge or a safe-haven asset in the COVID–19 crisis? Economic Modelling 102: 105588. [Google Scholar]

- Akhtaruzzaman, Md, Sabri Boubaker, Mardy Chiah, and Angel Zhong. 2021c. COVID-19 and oil price risk exposure. Finance Research Letters 42: 101882. [Google Scholar]

- Ameur, Hachmi Ben, Zied Ftiti, and Waël Louhichi. 2021. Intraday spillover between commodity markets. Resources Policy 74: 102278. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, and David Gabauer. 2017. Refined measures of dynamic connectedness based on TVP-VAR. Available online: https://mpra.ub.uni-muenchen.de/id/eprint/78282 (accessed on 12 July 2022).

- Antonakakis, Nikolaos, Ioannis Chatziantoniou, and David Gabauer. 2020. Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions. Journal of Risk and Financial Management 13: 84. [Google Scholar] [CrossRef]

- Aslam, Faheem, Paulo Ferreira, Haider Ali, and Ana Ercília José. 2022. Application of Multifractal Analysis in Estimating the Reaction of Energy Markets to Geopolitical Acts and Threats. Sustainability 14: 5828. [Google Scholar]

- Awan, Tahir Mumtaz, Muhammad Shoaib Khan, Inzamam Ul Haq, and Sarwat Kazmi. 2021. Oil and stock markets volatility during pandemic times: A review of G7 countries. Green Finance 3: 15–27. [Google Scholar]

- Aziz, Tariq, Ranjeeta Sadhwani, Ume Habibah, and Mazin AM Al Janabi. 2020. Volatility spillover among equity and commodity markets. SAGE Open 10: 2158244020924418. [Google Scholar] [CrossRef]

- Balali, Yasaman, and Sascha Stegen. 2021. Review of energy storage systems for vehicles based on technology, environmental impacts, and costs. Renewable and Sustainable Energy Reviews 135: 110185. [Google Scholar]

- Balaram, V. 2019. Rare earth elements: A review of applications, occurrence, exploration, analysis, recycling, and environmental impact. Geoscience Frontiers 10: 1285–303. [Google Scholar]

- Balcilar, Mehmet, David Gabauer, and Zaghum Umar. 2021. Crude Oil futures contracts and commodity markets: New evidence from a TVP-VAR extended joint connectedness approach. Resources Policy 73: 102219. [Google Scholar]

- Barakos, G., and H. Mischo. 2017. A review of misleading methods and biased practices in evaluating the feasibility of rare earth mining projects. Paper presented at the 28th SOMP Annual Meeting & Conference, Torino, Italy, July 3. [Google Scholar]

- Beylot, Antoine, Dominique Guyonnet, Stéphanie Muller, Stéphane Vaxelaire, and Jacques Villeneuve. 2019. Mineral raw material requirements and associated climate-change impacts of the French energy transition by 2050. Journal of Cleaner Production 208: 1198–205. [Google Scholar]

- Bouri, Elie, Kakali Kanjilal, Sajal Ghosh, David Roubaud, and Tareq Saeed. 2021a. Rare earth and allied sectors in stock markets: Extreme dependence of return and volatility. Applied Economics 53: 5710–30. [Google Scholar]

- Bouri, Elie, Oguzhan Cepni, David Gabauer, and Rangan Gupta. 2021b. Return connectedness across asset classes around the COVID-19 outbreak. International Review of Financial Analysis 73: 101646. [Google Scholar]

- Bouri, Elie, Xiaojie Lei, Naji Jalkh, Yahua Xu, and Hongwei Zhang. 2021c. Spillovers in higher moments and jumps across US stock and strategic commodity markets. Resources Policy 72: 102060. [Google Scholar]

- Brahim, Jamal Ait, Sara Ait Hak, Brahim Achiou, Rachid Boulif, Redouane Beniazza, and Rachid Benhida. 2022. Kinetics and mechanisms of leaching of rare earth elements from secondary resources. Minerals Engineering 177: 107351. [Google Scholar]

- Cai, Xiang, Bangzhu Zhu, Haijing Zhang, Liang Li, and Meiying Xie. 2020. Can direct environmental regulation promote green technology innovation in heavily polluting industries? Evidence from Chinese listed companies. Science of the Total Environment 746: 140810. [Google Scholar] [PubMed]

- Cetin, Murat, Eyyup Ecevit, and Ali Gokhan Yucel. 2018. The impact of economic growth, energy consumption, trade openness, and financial development on carbon emissions: Empirical evidence from Turkey. Environmental Science and Pollution Research 25: 36589–603. [Google Scholar] [PubMed]

- Chen, Ruoyu, Najaf Iqbal, Muhammad Irfan, Farrukh Shahzad, and Zeeshan Fareed. 2022. Does financial stress wreak havoc on banking, insurance, oil, and gold markets? New empirics from the extended joint connectedness of TVP-VAR model. Resources Policy 77: 102718. [Google Scholar]

- Chen, Zhe, Zhongzhong Hu, and Kai Li. 2021. The spillover effect of trade policy along the value Chain: Evidence from China’s rare earth-related sectors. The World Economy 44: 3550–82. [Google Scholar] [CrossRef]

- Dai, Zhifeng, and Haoyang Zhu. 2022. Time-varying spillover effects and investment strategies between WTI crude oil, natural gas and Chinese stock markets related to belt and road initiative. Energy Economics 108: 105883. [Google Scholar] [CrossRef]

- Danish, Mohammed, and Tanweer Ahmad. 2018. A review on utilization of wood biomass as a sustainable precursor for activated carbon production and application. Renewable and Sustainable Energy Reviews 87: 1–21. [Google Scholar] [CrossRef]

- De Koning, Arjan, René Kleijn, Gjalt Huppes, Benjamin Sprecher, Guus Van Engelen, and Arnold Tukker. 2018. Metal supply constraints for a low-carbon economy? Resources, Conservation and Recycling 129: 202–8. [Google Scholar] [CrossRef]

- Degiannakis, Stavros, George Filis, and Vipin Arora. 2018. Oil prices and stock markets: A review of the theory and empirical evidence. The Energy Journal 39: 85–130. [Google Scholar] [CrossRef]

- Du, Kerui, Pengzhen Li, and Zheming Yan. 2019. Do green technology innovations contribute to carbon dioxide emission reduction? Empirical evidence from patent data. Technological Forecasting and Social Change 146: 297–303. [Google Scholar] [CrossRef]

- Dudley, Bob. 2018. BP statistical review of world energy. BP Statistical Review 6: 00116. [Google Scholar]

- Dushyantha, Nimila, Nadeera Batapola, I. M. S. K. Ilankoon, Sudath Rohitha, Ranjith Premasiri, Bandara Abeysinghe, Nalin Ratnayake, and Kithsiri Dissanayake. 2020. The story of rare earth elements (REEs): Occurrences, global distribution, genesis, geology, mineralogy and global production. Ore Geology Reviews 122: 103521. [Google Scholar] [CrossRef]

- Ehigiamusoe, Kizito Uyi, and Hooi Hooi Lean. 2019. Effects of energy consumption, economic growth, and financial development on carbon emissions: Evidence from heterogeneous income groups. Environmental Science and Pollution Research 26: 22611–24. [Google Scholar] [CrossRef]

- Evans, John L., and Stephen H. Archer. 1968. Diversification and the reduction of dispersion: An empirical analysis. The Journal of Finance 23: 761–67. [Google Scholar]

- Fernandez, Viviana. 2017. Rare-earth elements market: A historical and financial perspective. Resources Policy 53: 26–45. [Google Scholar]

- Fishman, Tomer, Rupert J. Myers, Orlando Rios, and T. E. Graedel. 2018. Implications of emerging vehicle technologies on rare earth supply and demand in the United States. Resources 7: 9. [Google Scholar] [CrossRef]

- Gaustad, Gabrielle, Eric Williams, and Alexandra Leader. 2021. Rare earth metals from secondary sources: Review of potential supply from waste and byproducts. Resources, Conservation and Recycling 167: 105213. [Google Scholar]

- Hadi, Dlawar Mahdi, Muhammad Abubakr Naeem, and Sitara Karim. 2022. The exposure of the US tourism subsector stocks to global volatility and uncertainty factors. Current Issues in Tourism, 1–14. [Google Scholar] [CrossRef]

- Haq, Inzamam Ul. 2022. Cryptocurrency Environmental Attention, Green Financial Assets, and InformationTransmission: Evidence from COVID-19 Pandemic. Energy Research Letters 3. early view. [Google Scholar]

- Haq, Inzamam Ul, and Tahir Mumtaz Awan. 2020. Impact of e-banking service quality on e-loyalty in pandemic times through interplay of e-satisfaction. Vilakshan-XIMB Journal of Management 17: 39–55. [Google Scholar]

- Haq, Inzamam Ul, Apichit Maneengam, Supat Chupradit, Wanich Suksatan, and Chunhui Huo. 2021a. Economic policy uncertainty and cryptocurrency market as a risk management avenue: A systematic review. Risks 9: 163. [Google Scholar]

- Haq, Inzamam Ul, Paulo Ferreira, Apichit Maneengam, and Worakamol Wisetsri. 2022. Rare Earth Market, Electric Vehicles and Future Mobility Index: A Time–frequency Analysis with Portfolio Implications. Risks 10: 137. [Google Scholar]

- Haq, Inzamam Ul, Supat Chupradit, and Chunhui Huo. 2021b. Do Green Bonds Act as a Hedge or a Safe Haven against Economic Policy Uncertainty? Evidence from the USA and China. International Journal of Financial Studies 9: 40. [Google Scholar]

- Hau, Liya, Huiming Zhu, Yang Yu, and Dongwei Yu. 2022. Time–frequency coherence and quantile causality between trade policy uncertainty and rare earth prices: Evidence from China and the US. Resources Policy 75: 102529. [Google Scholar]

- Hazgui, Samah, Saber Sebai, and Walid Mensi. 2021. Dynamic frequency relationships between bitcoin, oil, gold and economic policy uncertainty index. Studies in Economics and Finance 39: 419–43. [Google Scholar] [CrossRef]

- He, Zhifang, Fangzhao Zhou, Xiaohua Xia, Fenghua Wen, and Yiyuan Huang. 2019. Interaction between oil price and investor sentiment: Nonlinear causality, time-varying influence, and asymmetric effect. Emerging Markets Finance and Trade 55: 2756–73. [Google Scholar] [CrossRef]

- Huang, Jianbai, Xuesong Dong, Jinyu Chen, and Meirui Zhong. 2022. Do oil prices and economic policy uncertainty matter for precious metal returns? New insights from a TVP-VAR framework. International Review of Economics & Finance 78: 433–45. [Google Scholar]

- Huynh, Nhan, Anh Dao, and Dat Nguyen. 2021. Openness, economic uncertainty, government responses, and international financial market performance during the coronavirus pandemic. Journal of Behavioral and Experimental Finance 31: 100536. [Google Scholar] [CrossRef]

- Inshakov, Oleg V., Lyudmila Y. Bogachkova, and Elena G. Popkova. 2019. The transformation of the global energy markets and the problem of ensuring the sustainability of their development. In Energy Sector: A Systemic Analysis of Economy, Foreign Trade and Legal Regulations. New York: Springer, pp. 135–48. [Google Scholar]

- Jebabli, Ikram, Mohamed Arouri, and Frédéric Teulon. 2014. On the effects of world stock market and oil price shocks on food prices: An empirical investigation based on TVP-VAR models with stochastic volatility. Energy Economics 45: 66–98. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, David Roubaud, and Syed Jawad Hussain Shahzad. 2018. Risk spillover between energy and agricultural commodity markets: A dependence-switching CoVaR-copula model. Energy Economics 75: 14–27. [Google Scholar] [CrossRef]

- Kang, Ho-Jun, Sang-Gun Lee, and Soo-Yong Park. 2022. Information efficiency in the cryptocurrency market: The efficient-market hypothesis. Journal of Computer Information Systems 62: 622–31. [Google Scholar] [CrossRef]

- Karim, Sitara, and Muhammad Abubakr Naeem. 2022. Do global factors drive the interconnectedness among green, Islamic and conventional financial markets? International Journal of Managerial Finance 18: 639–60. [Google Scholar] [CrossRef]

- Kennedy, James. 2019. China solidifies dominance in rare earth processing. National Defense 103: 17–19. [Google Scholar]

- Khan, Muhammad Kamran, Jian-Zhou Teng, Muhammad Imran Khan, and Muhammad Owais Khan. 2019. Impact of globalization, economic factors and energy consumption on CO2 emissions in Pakistan. Science of the Total Environment 688: 424–36. [Google Scholar] [CrossRef]

- Khorasanipour, Mehdi, and Zahra Jafari. 2018. Environmental geochemistry of rare earth elements in Cu-porphyry mine tailings in the semiarid climate conditions of Sarcheshmeh mine in southeastern Iran. Chemical Geology 477: 58–72. [Google Scholar] [CrossRef]

- Kihombo, Shauku, Arif I. Vaseer, Zahoor Ahmed, Songsheng Chen, Dervis Kirikkaleli, and Tomiwa Sunday Adebayo. 2022. Is there a tradeoff between financial globalization, economic growth, and environmental sustainability? An advanced panel analysis. Environmental Science and Pollution Research 29: 3983–93. [Google Scholar] [CrossRef] [PubMed]

- Klinger, Julie Michelle. 2018. Rare earth elements: Development, sustainability and policy issues. The Extractive Industries and Society 5: 1–7. [Google Scholar] [CrossRef]

- Liang, Tao, Kexin Li, and Lingqing Wang. 2014. State of rare earth elements in different environmental components in mining areas of China. Environmental Monitoring and Assessment 186: 1499–513. [Google Scholar] [CrossRef]

- Liu, Jingshan. 2020. Impact of uncertainty on foreign exchange market stability: Based on the LT-TVP-VAR model. China Finance Review International 11: 53–72. [Google Scholar] [CrossRef]

- Liu, Lu, En-Ze Wang, and Chien-Chiang Lee. 2020. Impact of the COVID-19 pandemic on the crude oil and stock markets in the US: A time-varying analysis. Energy Research Letters 1: 13154. [Google Scholar] [CrossRef]

- Maghyereh, Aktham I., Basel Awartani, and Hussein Abdoh. 2019. The co-movement between oil and clean energy stocks: A wavelet-based analysis of horizon associations. Energy 169: 895–913. [Google Scholar] [CrossRef]

- Maghyereh, Aktham, and Hussein Abdoh. 2022. Bubble contagion effect between the main precious metals. Studies in Economics and Finance. [Google Scholar] [CrossRef]

- Managi, Shunsuke, and Tatsuyoshi Okimoto. 2013. Does the price of oil interact with clean energy prices in the stock market? Japan and the World Economy 27: 1–9. [Google Scholar] [CrossRef]

- Mancheri, Nabeel A., Benjamin Sprecher, Gwendolyn Bailey, Jianping Ge, and Arnold Tukker. 2019. Effect of Chinese policies on rare earth supply chain resilience. Resources, Conservation and Recycling 142: 101–12. [Google Scholar] [CrossRef]

- Marques, Rosa, Maria I. Prudêncio, and Dulce Russo. 2021. Rare earths and other chemical elements determined by neutron activation analysis in new reference USGS materials: Carbonatite, nephelinite, syenite, granite, stream sediment and marine shale. Journal of Radioanalytical and Nuclear Chemistry 327: 1229–36. [Google Scholar] [CrossRef]

- Mensi, Walid, Mobeen Ur Rehman, and Xuan Vinh Vo. 2020. Spillovers and co-movements between precious metals and energy markets: Implications on portfolio management. Resources Policy 69: 101836. [Google Scholar] [CrossRef]

- Mensi, Walid, Mobeen Ur Rehman, and Xuan Vinh Vo. 2022. Impacts of COVID-19 outbreak, macroeconomic and financial stress factors on price spillovers among green bond. International Review of Financial Analysis 81: 102125. [Google Scholar] [CrossRef]

- Mensi, Walid, Shawkat Hammoudeh, Idries Mohammad Wanas Al-Jarrah, Ahmet Sensoy, and Sang Hoon Kang. 2017. Dynamic risk spillovers between gold, oil prices and conventional, sustainability and Islamic equity aggregates and sectors with portfolio implications. Energy Economics 67: 454–75. [Google Scholar] [CrossRef]

- Murshed, Muntasir. 2018. Does improvement in trade openness facilitate renewable energy transition? Evidence from selected South Asian economies. South Asia Economic Journal 19: 151–70. [Google Scholar] [CrossRef]

- Nakajima, Jouchi. 2011. Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Available online: https://www.imes.boj.or.jp/research/papers/english/me29-6.pdf (accessed on 12 July 2022).

- Nathaniel, Solomon, Ozoemena Nwodo, Abdulrauf Adediran, Gagan Sharma, Muhammad Shah, and Ngozi Adeleye. 2019. Ecological footprint, urbanization, and energy consumption in South Africa: Including the excluded. Environmental Science and Pollution Research 26: 27168–79. [Google Scholar] [CrossRef]

- Nathaniel, Solomon Prince, and Chimere Okechukwu Iheonu. 2019. Carbon dioxide abatement in Africa: The role of renewable and non-renewable energy consumption. Science of the Total Environment 679: 337–45. [Google Scholar] [CrossRef]

- Newell, Richard G., and Daniel Raimi. 2020. Global Energy Outlook Comparison Methods: 2020 Update. Resources for the Future. Available online: https://www.rff.org/documents/2456/Global_Energy_Outlook_Comparison_Methods_2020.pdf (accessed on 12 July 2022).

- Özdurak, Caner, and Veysel Ulusoy. 2020. Spillovers from the Slowdown in China on Financial and Energy Markets: An Application of VAR–VECH–TARCH Models. International Journal of Financial Studies 8: 52. [Google Scholar] [CrossRef]

- Pablo-Romero, Maria del P., and Josué De Jesús. 2016. Economic growth and energy consumption: The energy-environmental Kuznets curve for Latin America and the Caribbean. Renewable and Sustainable Energy Reviews 60: 1343–50. [Google Scholar] [CrossRef]

- Packey, Daniel J., and Dudley Kingsnorth. 2016. The impact of unregulated ionic clay rare earth mining in China. Resources Policy 48: 112–16. [Google Scholar] [CrossRef]

- Pantos, Themistoclis, Efstathios Polyzos, Angelos Armenatzoglou, and Elias Kampouris. 2019. Volatility spillovers in electricity markets: Evidence from the United States. International Journal of Energy Economics and Policy 9: 131–43. [Google Scholar] [CrossRef]

- Papathanasiou, Spyros, Dimitrios Vasiliou, Anastasios Magoutas, and Drosos Koutsokostas. 2022a. Do hedge and merger arbitrage funds actually hedge? A time-varying volatility spillover approach. Finance Research Letters 44: 102088. [Google Scholar] [CrossRef]

- Papathanasiou, Spyros, Drosos Koutsokostas, and Georgios Pergeris. 2022b. Novel alternative assets within a transmission mechanism of volatility spillovers: The role of SPACs. Finance Research Letters 47: 102602. [Google Scholar] [CrossRef]

- Papathanasiou, Spyros, Ioannis Dokas, and Drosos Koutsokostas. 2022c. Value investing versus other investment strategies: A volatility spillover approach and portfolio hedging strategies for investors. The North American Journal of Economics and Finance 62: 101764. [Google Scholar] [CrossRef]

- Primiceri, Giorgio E. 2005. Time varying structural vector autoregressions and monetary policy. The Review of Economic Studies 72: 821–52. [Google Scholar] [CrossRef]

- Proelss, Juliane, Denis Schweizer, and Volker Seiler. 2020. The economic importance of rare earth elements volatility forecasts. International Review of Financial Analysis 71: 101316. [Google Scholar] [CrossRef]

- Rahman, Mohammad Mafizur, and Mohammad Abul Kashem. 2017. Carbon emissions, energy consumption and industrial growth in Bangladesh: Empirical evidence from ARDL cointegration and Granger causality analysis. Energy Policy 110: 600–8. [Google Scholar] [CrossRef]

- Reboredo, Juan C., and Andrea Ugolini. 2020. Price spillovers between rare earth stocks and financial markets. Resources Policy 66: 101647. [Google Scholar] [CrossRef]

- Rubbaniy, Ghulame, Ali Awais Khalid, Abiot Tessema, and Abdelrahman Baqrain. 2022. Do stock market fear and economic policy uncertainty co-move with COVID-19 fear? Evidence from the US and UK. Studies in Economics and Finance. ahead-of-print. [Google Scholar] [CrossRef]

- Sadiq, Muhammad, Riazullah Shinwari, Muhammad Usman, Ilhan Ozturk, and Aktham Issa Maghyereh. 2022. Linking nuclear energy, human development and carbon emission in BRICS region: Do external debt and financial globalization protect the environment? Nuclear Engineering and Technology. in press. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, and Elias Kampouris. 2019. Financial illness and political virus: The case of contagious crises in the Eurozone. International Review of Applied Economics 33: 209–27. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Elias Kampouris, and Stathis Polyzos. 2022a. Covid-19 pandemic and spillover effects in stock markets: A financial network approach. International Review of Financial Analysis 80: 102005. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Elias Kampouris, and Zaghum Umar. 2022b. Financial contagion in real economy: The key role of policy uncertainty. International Journal of Finance and Economics 27: 1633–82. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Elias Kampouris, Stathis Polyzos, and Anastasia Spyridou. 2020. Spillover effects between greece and cyprus: A DCC model on the interdependence of small economies. Investment Management and Financial Innovations 17: 121–35. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Spyros Papathanasiou, and Drosos Koutsokostas. 2021. The connectedness between Sukuk and conventional bond markets and the implications for investors. International Journal of Islamic and Middle Eastern Finance and Management 14: 928–49. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Spyros Papathanasiou, Drosos Koutsokostas, and Elias Kampouris. 2022c. Are timber and water investments safe-havens? A volatility spillover approach and portfolio hedging strategies for investors. Finance Research Letters 47: 102657. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, Spyros Papathanasiou, Drosos Koutsokostas, and Elias Kampouris. 2022d. Volatility spillovers between fine wine and major global markets during COVID-19: A portfolio hedging strategy for investors. International Review of Economics & Finance 78: 629–42. [Google Scholar]

- Schulze, Rita, and Matthias Buchert. 2016. Estimates of global REE recycling potentials from NdFeB magnet material. Resources, Conservation and Recycling 113: 12–27. [Google Scholar] [CrossRef]

- Shahbaz, Muhammad, Thi Hong Van Hoang, Mantu Kumar Mahalik, and David Roubaud. 2017. Energy consumption, financial development and economic growth in India: New evidence from a nonlinear and asymmetric analysis. Energy Economics 63: 199–212. [Google Scholar] [CrossRef]

- Shahzad, Syed Jawad Hussain, Elie Bouri, Ghulam Mujtaba Kayani, Rana Muhammad Nasir, and Ladislav Kristoufek. 2020. Are clean energy stocks efficient? Asymmetric multifractal scaling behaviour. Physica A: Statistical Mechanics and Its Applications 550: 124519. [Google Scholar] [CrossRef]

- Sharpe, William F. 1964. Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance 19: 425–42. [Google Scholar]

- Shezan, S. K. A., Narottam Das, and Hasan Mahmudul. 2017. Techno-economic analysis of a smart-grid hybrid renewable energy system for Brisbane of Australia. Energy Procedia 110: 340–45. [Google Scholar]

- Shin, Seo-Ho, Hyun-Ock Kim, and Kyung-Taek Rim. 2019. Worker safety in the rare earth elements recycling process from the review of toxicity and issues. Safety and Health at Work 10: 409–19. [Google Scholar] [PubMed]

- Singh, Ajit Pratap, and Kunal Dhadse. 2021. Economic evaluation of crop production in the Ganges region under climate change: A sustainable policy framework. Journal of Cleaner Production 278: 123413. [Google Scholar]

- Song, Ying, Elie Bouri, Sajal Ghosh, and Kakali Kanjilal. 2021. Rare earth and financial markets: Dynamics of return and volatility connectedness around the COVID-19 outbreak. Resources Policy 74: 102379. [Google Scholar]

- Sorknæs, Peter, Henrik Lund, I. R. Skov, Søren Djørup, Klaus Skytte, Poul Erik Morthorst, and Felipe Fausto. 2020. Smart Energy Markets-Future electricity, gas and heating markets. Renewable and Sustainable Energy Reviews 119: 109655. [Google Scholar]

- Tang, Chaofeng, and Kentaka Aruga. 2021. Relationships among the fossil fuel and financial markets during the COVID-19 pandemic: Evidence from bayesian DCC-MGARCH models. Sustainability 14: 51. [Google Scholar]

- Tiwari, Aviral Kumar, Emmanuel Joel Aikins Abakah, David Gabauer, and Richard Adjei Dwumfour. 2022. Dynamic spillover effects among green bond, renewable energy stocks and carbon markets during COVID-19 pandemic: Implications for hedging and investments strategies. Global Finance Journal 51: 100692. [Google Scholar]

- Toparlı, Elif Akay, Abdurrahman Nazif Çatık, and Mehmet Balcılar. 2019. The impact of oil prices on the stock returns in Turkey: A TVP-VAR approach. Physica A: Statistical Mechanics and Its Applications 535: 122392. [Google Scholar]

- Tran, Quang Thien, Nhan Huynh, and Nhu An Huynh. 2022. Trading-Off between Being Contaminated or Stimulated: Are Emerging Countries Doing Good Jobs in Hosting Foreign Resources? Available online: https://ssrn.com/abstract=4112396 (accessed on 12 July 2022).

- Tsagkanos, Athanasios, Aarzoo Sharma, and Bikramaditya Ghosh. 2022. Green Bonds and Commodities: A New Asymmetric Sustainable Relationship. Sustainability 14: 6852. [Google Scholar]

- Ul Haq, Inzamam, Apichit Maneengam, Supat Chupradit, and Chunhui Huo. 2022. Are green bonds and sustainable cryptocurrencies truly sustainable? Evidence from a wavelet coherence analysis. Economic Research-Ekonomska Istraživanja, 1–20. [Google Scholar] [CrossRef]

- Usman, Ahmed, Sana Ullah, Ilhan Ozturk, Muhammad Zubair Chishti, and Syeda Maria Zafar. 2020. Analysis of asymmetries in the nexus among clean energy and environmental quality in Pakistan. Environmental Science and Pollution Research 27: 20736–47. [Google Scholar] [CrossRef] [PubMed]

- Wang, Yizhi, Brian M. Lucey, Samuel Vigne, and Larisa Yarovaya. 2022. An index of cryptocurrency environmental attention (ICEA). China Finance Review International 12: 378–414. [Google Scholar] [CrossRef]

- Zhang, Hua, Jinyu Chen, and Liuguo Shao. 2021. Dynamic spillovers between energy and stock markets and their implications in the context of COVID-19. International Review of Financial Analysis 77: 101828. [Google Scholar] [CrossRef]

- Zhang, Wenting, Xie He, Tadahiro Nakajima, and Shigeyuki Hamori. 2020. How does the spillover among natural gas, crude oil, and electricity utility stocks change over time? Evidence from North America and Europe. Energies 13: 727. [Google Scholar] [CrossRef]

- Zhao, Zhexuan, Zhaofu Qiu, Ji Yang, Shuguang Lu, Limei Cao, Wei Zhang, and Yongye Xu. 2017. Recovery of rare earth elements from spent fluid catalytic cracking catalysts using leaching and solvent extraction techniques. Hydrometallurgy 167: 183–88. [Google Scholar] [CrossRef]

- Zheng, Biao, Yuquan W. Zhang, Fang Qu, Yong Geng, and Haishan Yu. 2022. Do rare earths drive volatility spillover in crude oil, renewable energy, and high-technology markets?—A wavelet-based BEKK–GARCH-X approach. Energy 251: 123951. [Google Scholar] [CrossRef]

- Zheng, Biao, Yuquan Zhang, and Yufeng Chen. 2021. Asymmetric connectedness and dynamic spillovers between renewable energy and rare earth markets in China: Evidence from firms’ high-frequency data. Resources Policy 71: 101996. [Google Scholar] [CrossRef]

- Zhou, Baolu, Zhongxue Li, and Congcong Chen. 2017. Global potential of rare earth resources and rare earth demand from clean technologies. Minerals 7: 203. [Google Scholar] [CrossRef]

- Zhou, Mei-Jing, Jian-Bai Huang, and Jin-Yu Chen. 2020. The effects of geopolitical risks on the stock dynamics of China’s rare metals: A TVP-VAR analysis. Resources Policy 68: 101784. [Google Scholar] [CrossRef]

- Zhou, Mei-Jing, Jian-Bai Huang, and Jin-Yu Chen. 2022. Time and frequency spillovers between political risk and the stock returns of China’s rare earths. Resources Policy 75: 102464. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Reserves in Tones (in Terms of REO) | % Share |

|---|---|---|

| Australia | 3,400,000 | 2.56 |

| Brazil | 22,000,000 | 16.67 |

| Canada | 830,000 | 0.63 |

| China | 44,000,000 | 33.33 |

| Greenland | 1,500,000 | 1.14 |

| India | 6,900,000 | 5.23 |

| Malaysia | 30,000 | 0.02 |

| Malawi | 140,000 | 0.11 |

| Russia | 18,000,000 | 13.64 |

| South Africa | 860,000 | 0.65 |

| Vietnam | 22,000,000 | 16.67 |

| USA | 1,400,000 | 1.06 |

| M | Max | Min | SD | Skew | Kurt | JB | ADF | Obs. | |

|---|---|---|---|---|---|---|---|---|---|

| ASI | 0.000 | 0.062 | −0.064 | 0.010 | −0.634 | 8.335 | 1415.900 * | −36.226 | 1130 |

| CHNREE | 0.001 | 2.183 | −0.318 | 0.082 | 17.293 | 442.130 | 9,135,629.000 * | −34.645 | 1130 |

| CSI | 0.000 | 0.084 | −0.078 | 0.014 | −0.142 | 6.297 | 515.500 * | −33.259 | 1130 |

| GAS | 0.001 | 0.180 | −0.253 | 0.028 | −1.394 | 20.064 | 14,075.300 * | −32.343 | 1130 |

| LYC | 0.000 | 0.300 | −1.390 | 0.055 | −14.168 | 362.027 | 6,106,863.000 * | −33.742 | 1130 |

| MVISGREI | 0.000 | 0.063 | −0.081 | 0.018 | −0.120 | 4.232 | 74.100 * | −28.814 | 1130 |

| NGAS | 0.001 | 0.198 | −0.181 | 0.035 | 0.174 | 7.033 | 771.600 * | −34.610 | 1130 |

| SWI | 0.000 | 0.077 | −0.106 | 0.010 | −1.464 | 23.769 | 20,712.600 * | −35.249 | 1130 |

| USREE | 0.000 | 0.137 | −0.216 | 0.026 | −0.877 | 10.835 | 3035.400 * | −34.816 | 1130 |

| USSI | 0.001 | 0.095 | −0.129 | 0.014 | −0.894 | 18.793 | 11,893.700 * | −40.983 | 1130 |

| WTI | 0.002 | 0.320 | −0.282 | 0.037 | 1.211 | 31.844 | 39,449.600 * | −28.605 | 1130 |

| ASI | CHNREE | CSI | GAS | LYC | MVISGREI | NGAS | SWI | USREE | USSI | WTI | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ASI | 1.000 | −0.009 | −0.009 | 0.080 | 0.015 | −0.017 | 0.005 | 0.056 | 0.036 | −0.001 | −0.072 |

| CHNREE | −0.009 | 1.000 | 0.005 | −0.014 | −0.028 | −0.007 | −0.025 | 0.015 | −0.049 | 0.004 | 0.008 |

| CSI | −0.009 | 0.005 | 1.000 | −0.037 | 0.039 | 0.031 | −0.009 | −0.010 | 0.012 | 0.005 | 0.025 |

| GAS | 0.080 | −0.014 | −0.037 | 1.000 | −0.020 | 0.054 | 0.022 | −0.015 | 0.248 | 0.326 | 0.055 |

| LYC | 0.015 | −0.028 | 0.039 | −0.020 | 1.000 | −0.015 | −0.034 | −0.001 | −0.017 | −0.026 | −0.035 |

| MVISGREI | −0.017 | −0.007 | 0.031 | 0.054 | −0.015 | 1.000 | −0.020 | 0.034 | 0.007 | 0.040 | −0.017 |

| NGAS | 0.005 | −0.025 | −0.009 | 0.022 | −0.034 | −0.020 | 1.000 | 0.007 | 0.065 | 0.042 | −0.041 |

| SWI | 0.056 | 0.015 | −0.010 | −0.015 | −0.001 | 0.034 | 0.007 | 1.000 | −0.029 | −0.091 | 0.004 |

| USREE | 0.036 | −0.049 | 0.012 | 0.248 | −0.017 | 0.007 | 0.065 | −0.029 | 1.000 | 0.551 | 0.034 |

| USSI | −0.001 | 0.004 | 0.005 | 0.326 | −0.026 | 0.040 | 0.042 | −0.091 | 0.551 | 1.000 | 0.041 |

| WTI | −0.072 | 0.008 | 0.025 | 0.055 | −0.035 | −0.017 | −0.041 | 0.004 | 0.034 | 0.041 | 1.000 |

| LYC | CHNREE | MVISGREI | USREE | CSI | ASI | USSI | SWI | FROM | |

|---|---|---|---|---|---|---|---|---|---|

| LYC | 91.890 | 1.150 | 0.870 | 1.130 | 0.770 | 1.680 | 0.710 | 1.800 | 8.110 |

| CHNREE | 0.710 | 95.260 | 0.610 | 0.860 | 0.580 | 0.650 | 0.760 | 0.580 | 4.740 |

| MVISGREI | 0.950 | 2.210 | 89.070 | 1.720 | 1.730 | 0.740 | 0.890 | 2.690 | 10.930 |

| USREE | 0.730 | 1.290 | 0.860 | 70.320 | 0.830 | 1.490 | 23.650 | 0.830 | 29.680 |

| CSI | 0.660 | 1.670 | 0.990 | 1.110 | 92.640 | 0.910 | 0.760 | 1.260 | 7.360 |

| ASI | 2.190 | 1.560 | 0.840 | 1.780 | 0.830 | 88.380 | 2.950 | 1.460 | 11.620 |

| USSI | 0.520 | 1.680 | 0.810 | 23.350 | 0.910 | 1.910 | 69.490 | 1.340 | 30.510 |

| SWI | 1.690 | 1.060 | 1.390 | 1.970 | 1.200 | 1.670 | 1.450 | 89.570 | 10.430 |

| TO | 7.430 | 10.620 | 6.370 | 31.930 | 6.850 | 9.050 | 31.170 | 9.970 | 113.390 |

| NET | −0.680 | 5.880 | −4.560 | 2.250 | −0.510 | −2.570 | 0.660 | −0.460 | TCI = 14.17% |

| GAS | WTI | NGAS | CSI | ASI | USSI | SWI | FROM | |

|---|---|---|---|---|---|---|---|---|

| GAS | 85.780 | 1.380 | 0.920 | 1.070 | 1.030 | 9.130 | 0.690 | 14.220 |

| WTI | 1.180 | 92.620 | 2.110 | 0.640 | 1.530 | 0.900 | 1.020 | 7.380 |

| NGAS | 1.180 | 1.830 | 92.980 | 1.040 | 0.670 | 1.750 | 0.560 | 7.020 |

| CSI | 2.560 | 1.250 | 1.070 | 92.550 | 0.750 | 0.810 | 1.000 | 7.450 |

| ASI | 1.690 | 2.280 | 0.940 | 0.870 | 90.020 | 3.010 | 1.190 | 9.980 |

| USSI | 9.070 | 1.330 | 1.100 | 0.890 | 1.940 | 84.230 | 1.440 | 15.770 |

| SWI | 1.510 | 1.570 | 1.850 | 1.100 | 1.270 | 1.490 | 91.220 | 8.780 |

| TO | 17.190 | 9.630 | 7.990 | 5.610 | 7.200 | 17.090 | 5.900 | 70.600 |

| NET | 2.970 | 2.250 | 0.970 | −1.840 | −2.790 | 1.310 | −2.880 | TCI = 10.09% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Haq, I.U.; Nadeem, H.; Maneengam, A.; Samantreeporn, S.; Huynh, N.; Kettanom, T.; Wisetsri, W. Do Rare Earths and Energy Commodities Drive Volatility Transmission in Sustainable Financial Markets? Evidence from China, Australia, and the US. Int. J. Financial Stud. 2022, 10, 76. https://doi.org/10.3390/ijfs10030076

Haq IU, Nadeem H, Maneengam A, Samantreeporn S, Huynh N, Kettanom T, Wisetsri W. Do Rare Earths and Energy Commodities Drive Volatility Transmission in Sustainable Financial Markets? Evidence from China, Australia, and the US. International Journal of Financial Studies. 2022; 10(3):76. https://doi.org/10.3390/ijfs10030076

Chicago/Turabian StyleHaq, Inzamam UI, Hira Nadeem, Apichit Maneengam, Saowanee Samantreeporn, Nhan Huynh, Thasporn Kettanom, and Worakamol Wisetsri. 2022. "Do Rare Earths and Energy Commodities Drive Volatility Transmission in Sustainable Financial Markets? Evidence from China, Australia, and the US" International Journal of Financial Studies 10, no. 3: 76. https://doi.org/10.3390/ijfs10030076

APA StyleHaq, I. U., Nadeem, H., Maneengam, A., Samantreeporn, S., Huynh, N., Kettanom, T., & Wisetsri, W. (2022). Do Rare Earths and Energy Commodities Drive Volatility Transmission in Sustainable Financial Markets? Evidence from China, Australia, and the US. International Journal of Financial Studies, 10(3), 76. https://doi.org/10.3390/ijfs10030076