Does Monetary Policy Influence the Profitability of Banks in New Zealand?

Abstract

:1. Introduction

2. Literature Review

3. Data and Methods

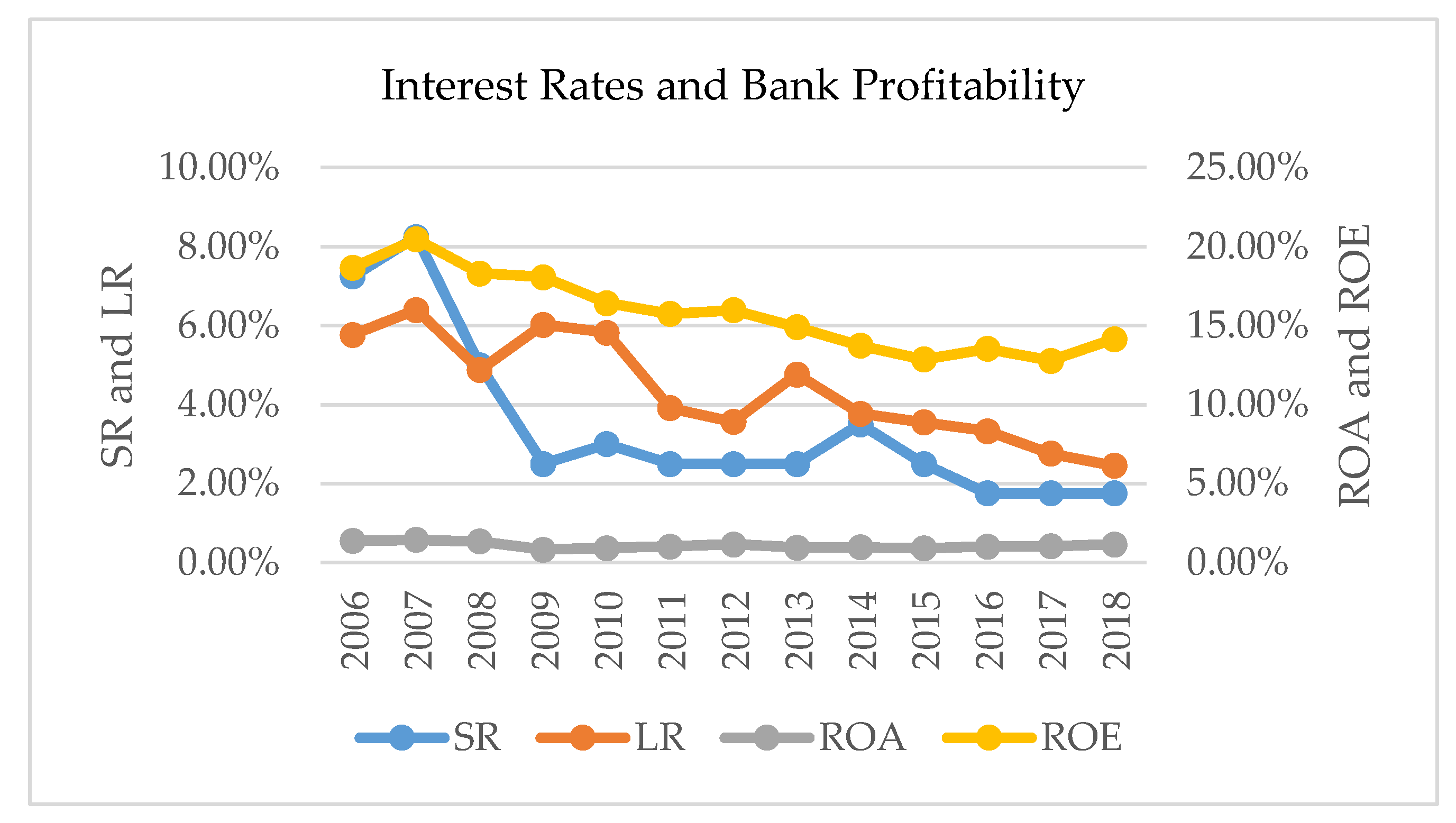

3.1. Description and Sources of Data

3.2. Descriptive Statistics

3.3. Dependent and Independent Variables

3.3.1. Dependent Variables

3.3.2. Independent Variables

Monetary Policy Variables: The Study Uses the Following Two Monetary Policy Variables

Control Variables: The Study Uses the Following Control Variables

3.4. Method

4. Results and Discussions

4.1. Regression Results

4.2. Regression Results with the Unconventional Monetary Policy Tool

5. Robustness Tests

5.1. Regression Results with Using Firm Fixed-Effect Model AR(1)

5.2. Unit Root Tests

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Variables | ROA | ROE | SR | LR | CAR | NPLR | COST | SIZE | LAR | INF | GDP | VIF |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 1 | |||||||||||

| ROE | 0.2289 * | 1 | ||||||||||

| SR | 0.1331 | −0.0051 | 1 | 2.97 | ||||||||

| LR | 0.0233 | −0.0333 | 0.6944 * | 1 | 3.61 | |||||||

| CAR | −0.3413 * | −0.0964 | −0.0223 | −0.035 | 1 | 1.36 | ||||||

| NPLR | −0.0993 | 0.1112 | −0.2327 | −0.0514 | 0.0287 | 1 | 1.43 | |||||

| COST | −0.6612 * | −0.1705 | 0.0142 | −0.0008 | 0.7254 * | −0.1585 | 1 | 2.52 | ||||

| SIZE | 0.4951 * | 0.1093 | 0.1959 | 0.2838 * | −0.4983 * | −0.1417 | −0.5688 * | 1 | 2.76 | |||

| LAR | 0.192 | −0.0179 | 0.0806 | 0.0596 | −0.193 | 0.0861 | 0.0423 | 0.3569 * | 1 | 1.30 | ||

| INF | 0.1082 | −0.0015 | 0.5231 * | 0.6623 * | −0.1235 | −0.0365 | −0.1138 | 0.2971 * | 0.1924 | 1 | 1.81 | |

| GDP | −0.0036 | 0.0331 | 0.0398 | −0.4570 * | 0.0996 | −0.1247 | 0.1056 | −0.3067 * | −0.1023 | −0.4194 * | 1 | 2.06 |

References

- Abduh, Muhamad, and Yameen Idrees. 2013. Determinants of Islamic Banking Profitability in Malaysia. Australian Journal of Basic and Applied Sciences 7: 204–10. [Google Scholar]

- Acharya, Sanjeev. 2018. Improving Corporate Governance in Nepalese Financial Institutions to Promote Growth and Performance. Doctoral thesis, The University of Waikato, Hamilton, New Zealand. [Google Scholar]

- Aharony, Joseph, Anthony Saunders, and Ithzak Swary. 1986. The Effects of a Shift in Monetary Policy Regime on the Profitability and Risk of Commercial Banks. Journal of Monetary Economics 17: 363–77. [Google Scholar] [CrossRef]

- Akhtar, Muhammad Farhan, Khizer Ali, and Shama Sadaqat. 2011. Factors Influencing the Profitability of Islamic Banks of Pakistan. International Research Journal of Finance and Economics 66: 1–8. [Google Scholar]

- Albertazzi, Ugo, and Leonardo Gambacorta. 2009. Bank Profitability and the Business Cycle. Journal of Financial Stability 5: 393–409. [Google Scholar] [CrossRef]

- Arellano, Manuel, and Stephen Bond. 1991. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. The Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef] [Green Version]

- Arellano, Manuel, and Olympia Bover. 1995. Another Look at the Instrumental Variable Estimation of Error-Components Models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef] [Green Version]

- Asia News Monitor. 2017. Monetary Policy and Bank Profitability in a Low Interest Rate Environment. Dublin: European Union. [Google Scholar]

- Athanasoglou, Panayiotis P., Sophocles N. Brissimis, and Matthaios D. Delis. 2008. Bank-Specific, Industry-Specific and Macroeconomic Determinants of Bank Profitability. Journal of International Financial Markets, Institutions and Money 18: 121–36. [Google Scholar] [CrossRef] [Green Version]

- Bassetti, Massimo. 2020. New Zealand Monetary Policy May 2020. Available online: https://www.focus-economics.com/countries/new-zealand/news/monetary-policy/rbnz-ramps-up-asset-purchasing-program-in-may (accessed on 17 May 2020).

- Berger, Allen N. 1995. The Relationship between Capital and Earnings in Banking. Journal of Money, Credit and Banking 27: 432–56. [Google Scholar] [CrossRef]

- Berger, Allen N., William C. Hunter, and Stephen G. Timme. 1993. The Efficiency of Financial Institutions: A Review and Preview of Research Past, Present and Future. Journal of Banking and Finance 17: 221–49. [Google Scholar] [CrossRef]

- Berument, Hakan, and Richard T. Froyen. 2015. Monetary Policy and Interest Rates under Inflation Targeting in Australia and New Zealand. New Zealand Economic Papers 49: 171–88. [Google Scholar] [CrossRef]

- Bikker, Jacob A., and Tobias M. Vervliet. 2018. Bank Profitability and Risk-Taking under Low Interest Rates. International Journal of Finance and Economics 23: 3–18. [Google Scholar] [CrossRef] [Green Version]

- Blundell, Richard, and Stephen Bond. 1998. Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef] [Green Version]

- Stephen R., Bond. 2002. Dynamic panel data models: a guide to micro data methods and practice. Portuguese Rconomic Journal 2: 141–62. [Google Scholar]

- Borio, Claudio, Leonardo Gambacorta, and Boris Hofmann. 2017. The Influence of Monetary Policy on Bank Profitability. International Finance 20: 48–63. [Google Scholar] [CrossRef] [Green Version]

- Bourke, Philip. 1989. Concentration and Other Determinants of Bank Profitability in Europe, North America and Australia. Journal of Banking and Finance 13: 65–79. [Google Scholar] [CrossRef]

- Brei, Michael, Claudio Borio, and Leonardo Gambacorta. 2019. Bank Intermediation Activity in a Low Interest Rate Environment. BIS Working Papers 807: 1–29. [Google Scholar] [CrossRef]

- Christensen, Jens H. E., and Glenn D. Rudebusch. 2016. Modeling Yields at the Zero Lower Bound: Are Shadow Rates the Solution? Advances in Econometrics 35: 75–125. [Google Scholar]

- Croy, David, and Zollner Sharon. 2020. RBNZ Announces Quantitative Easing. ANZ Research. Available online: https://www.anz.co.nz/content/dam/anzconz/documents/economics-and-market-research/2020/ANZ-RBNZ-announces-QE−20200323.pdf (accessed on 18 May 2020).

- Culling, Jamie, Michael Callaghan, and Adam Richardson. 2019. Effective Monetary Stimulus: Measuring the Stance of Monetary Policy in New Zealand. No. AN2019/05. Wellington: Reserve Bank of New Zealand. [Google Scholar]

- DeJong, David N., John C. Nankervis, N. Eugene Savin, and Charles H. Whiteman. 1992. Integration versus trend stationary in time series. Econometrica: Journal of the Econometric Society, 423–33. [Google Scholar] [CrossRef]

- Delis, Manthos D., and Georgios P. Kouretas. 2011. Interest Rates and Bank Risk-Taking. Journal of Banking and Finance 35: 840–55. [Google Scholar] [CrossRef] [Green Version]

- Demirguc-Kunt, Asli, and Harry Huizinga. 1999. Determinants of Commercial Bank Interest Margins and Profitability: Some International Evidence. The World Bank Economic Review 13: 379–408. [Google Scholar] [CrossRef] [Green Version]

- Dickey, David A., and Wayne A. Fuller. 1981. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica: Journal of the Econometric Society 49: 1057–72. [Google Scholar] [CrossRef]

- Dietrich, Andreas, and Gabrielle Wanzenried. 2011. Determinants of Bank Profitability before and During the Crisis: Evidence from Switzerland. Journal of International Financial Markets, Institutions and Money 21: 307–27. [Google Scholar] [CrossRef]

- Dietrich, Andreas, and Gabrielle Wanzenried. 2014. The Determinants of Commercial Banking Profitability in Low-, Middle-, and High-Income Countries. Quarterly Review of Economics and Finance 54: 337–54. [Google Scholar] [CrossRef]

- Drought, Sarah, Roger Perry, and Adam Richardson. 2018. Aspects of implementing unconventional monetary policy in New Zealand. The Reserve Bank of New Zealand Bulletin 81: 4. [Google Scholar]

- Galariotis, Emilios, Panagiota Makrichoriti, and Spyros Spyrou. 2018. The impact of conventional and unconventional monetary policy on expectations and sentiment. Journal of Banking and Finance 86: 1–20. [Google Scholar] [CrossRef] [Green Version]

- García-Herrero, Alicia, Sergio Gavilá, and Daniel Santabárbara. 2009. What Explains the Low Profitability of Chinese Banks? Journal of Banking and Finance 33: 2080–92. [Google Scholar] [CrossRef] [Green Version]

- Genay, Hesna, and Rich Podjasek. 2014. What Is the Impact of a Low Interest Rate Environment on Bank Profitability? Chicago Fed Letter 324: 1–4. [Google Scholar]

- Hancock, Diana. 1985. Bank Profitability, Interest Rates, and Monetary Policy. Journal of Money, Credit and Banking 17: 189–202. [Google Scholar] [CrossRef]

- Harris, Richard, and Robert Sollis. 2003. Applied Time Series Modelling and Forecasting. Hoboken: Wiley. [Google Scholar]

- Hasanov, Fakhri J., Nigar Bayramli, and Nayef Al-Musehel. 2018. Bank-Specific and Macroeconomic Determinants of Bank Profitability: Evidence from an Oil-Dependent Economy. International Journal of Financial Studies 6: 78. [Google Scholar] [CrossRef] [Green Version]

- Hassan, M. Kabir, and Abdel-Hameed M. Bashir. 2003. Determinants of Islamic Banking Profitability. Paper presented at the 10th ERF Annual Conference, Marrakesh, Morocco, December 16–18. [Google Scholar]

- Hughes, Joseph P., and Loretta J. Mester. 2013. Who Said Large Banks Don’t Experience Scale Economies? Evidence from a Risk-Return-Driven Cost Function. Journal of Financial Intermediation 22: 559–85. [Google Scholar] [CrossRef] [Green Version]

- Klein, Paul-Olivier, and Laurent Weill. 2017. Bank Profitability: Good for Growth? Paris: Institut de France. [Google Scholar]

- Krishnamurthy, Arvind, and Annette Vissing-Jorgensen. 2011. The Effects of Quantitative Easing on Interest Rates: Channels and Implications for Policy. No. w17555. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Kulish, Mariano. 2005. Should Monetary Policy Use Long-Term Rates? In Boston College Working Papers in Economics. Chestnut Hill: Boston College. [Google Scholar]

- Kumar, Vijay. 2018. The Profitability of Banking Sectors in the Asia-Pacific Region and Their Contributions to Economic Growth. Doctoral thesis, The University of Waikato, Hamilton, New Zealand. [Google Scholar]

- Lambert, Frederic, and Kenichi Ueda. 2014. The Effects of Unconventional Monetary Policies on Bank Soundness. No. 14−152. Washington: International Monetary Fund. [Google Scholar]

- Madaschi, Christophe, and Irene Pablos Nuevo. 2017. The Profitability of Banks in a Context of Negative Monetary Policy Rates: The Cases of Sweden and Denmark. Edited by Eurpoean Central Bank. Germany: Eurpoean Central Bank, Available online: https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op195.en.pdf (accessed on 15 January 2020).

- Mamatzakis, Emmanuel, and Theodora Bermpei. 2016. What is the effect of unconventional monetary policy on bank performance? Journal of International Money and Finance 67: 239–63. [Google Scholar] [CrossRef] [Green Version]

- Mamatzakis, Emmanuel, Roman Matousek, and Anh Nguyet Vu. 2016. What is the impact of bankrupt and restructured loans on Japanese bank efficiency? Journal of Banking and Finance 72: S187–S202. [Google Scholar] [CrossRef] [Green Version]

- McGough, Bruce, Glenn D. Rudebusch, and John C. Williams. 2005. Using a Long-Term Interest Rate as the Monetary Policy Instrument. Journal of Monetary Economics 52: 855–79. [Google Scholar] [CrossRef] [Green Version]

- Minh To, Huong, and David Tripe. 2002. Factors Influencing the Performance of Foreign-Owned Banks in New Zealand. Journal of International Financial Markets, Institutions and Money 12: 341–57. [Google Scholar] [CrossRef]

- Mirzaei, Ali, Tomoe Moore, and Guy Liu. 2013. Does Market Structure Matter on Banks’ Profitability and Stability? Emerging vs. Advanced Economies. Journal of Banking and Finance 37: 2920–37. [Google Scholar] [CrossRef]

- Nickell, Stephen. 1981. Biases in dynamic models with fixed effects. Econometrica: Journal of the Econometric Society 49: 1417–26. [Google Scholar] [CrossRef]

- Pasiouras, Fotios, and Kyriaki Kosmidou. 2007. Factors Influencing the Profitability of Domestic and Foreign Commercial Banks in the European Union. Research in International Business and Finance 21: 222–37. [Google Scholar] [CrossRef]

- Philippas, Dionisis, Stephanos Papadamou, and Iuliana Tomuleasa. 2019. The role of leverage in quantitative easing decisions: Evidence from the UK. The North American Journal of Economics and Finance 47: 308–24. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., and Pierre Perron. 1988. Testing for a unit root in time series regression. Biometrika 75: 335–46. [Google Scholar] [CrossRef]

- Quagliariello, Mario. 2007. Banks’ Riskiness over the Business Cycle: A Panel Analysis on Italian Intermediaries. Applied Financial Economics 17: 119–38. [Google Scholar] [CrossRef]

- Reserve Bank of New Zealand. 2019b. The Impact of Very Low Interest Rates on Bank Profitability. Available online: https://www.rbnz.govt.nz/financial-stability/financial-stability-report/fsr-november-2019/the-impact-of-very-low-interest-rates-on-bank-profitability (accessed on 18 January 2020).

- Reserve Bank of New Zealand. 2020a. Official Cash Rate (OCR) Decisions and Current Rate. Reserve Bank of New Zealand. Available online: https://www.rbnz.govt.nz/monetary-policy/official-cash-rate-decisions (accessed on 15 May 2020).

- Reserve Bank of New Zealand. 2020b. The Banking System. Available online: https://www.rbnz.govt.nz/financial-stability/overview-of-the-new-zealand-financial-system/the-banking-system (accessed on 18 May 2020).

- Reserve Bank of New Zealand. 2020c. Overview of the New Zealand Financial System. Available online: https://www.rbnz.govt.nz/financial-stability/overview-of-the-new-zealand-financial-system (accessed on 18 May 2020).

- Revell, Jack. 1979. Inflation and Financial Institutions. London: Financial Times Limited. [Google Scholar]

- Rios, Antonio Diez de los, and Maral Shamloo. 2017. Quantitative Easing and Long-Term Yields in Small Open Economies. IMF Working Pape 17: 1–46. [Google Scholar] [CrossRef]

- Rudebusch, Glenn. 2018. A Review of the Fed’s Unconventional Monetary Policy. FRBSF Economic Letter 27: 1–5. [Google Scholar]

- Sääskilahti, Jaakko. 2015. Retail Bank Interest Margins in Low Interest Rate Environments. Journal of Financial Services Research 53: 37–68. [Google Scholar] [CrossRef]

- Short, Brock K. 1979. The Relation between Commercial Bank Profit Rates and Banking Concentration in Canada, Western Europe, and Japan. Journal of Banking and Finance 3: 209–19. [Google Scholar] [CrossRef]

- Smirlock, Michael. 1985. Evidence on the (Non) Relationship between Concentration and Profitability in Banking. Journal of Money, Credit and Banking 17: 69–83. [Google Scholar] [CrossRef]

- Somoye, R. O. C. 2010. The Variation of Risks on Non-Performing Loans on Bank Performances in Nigeria. Indian Journal of Economics and Business 9: 87. [Google Scholar]

- Stráský, Jan, and Hyunjeong Hwang. 2019. Negative Interest Rates in the Euro Area: Does It Hurt Banks? OECD Economics Department Working Papers 1574: 1–4. [Google Scholar]

- Tan, Yong, and Christos Floros. 2012. Bank Profitability and GDP Growth in China: A Note. Journal of Chinese Economic and Business Studies 10: 267–73. [Google Scholar] [CrossRef] [Green Version]

- West, Kenneth D. 2003. Monetary Policy and the Volatility of Real Exchange Rates in New Zealand. New Zealand Economic Papers 37: 175–96. [Google Scholar] [CrossRef]

- Yao, Hongxing, Muhammad Haris, and Gulzara Tariq. 2018. Profitability Determinants of Financial Institutions: Evidence from Banks in Pakistan. International Journal of Financial Studies 6: 53. [Google Scholar] [CrossRef] [Green Version]

- Zimmermann, Kaspar. 2017. Breaking Banks? Monetary Policy and Banks Profitability. Available online: https://www.bde.es/f/webbde/INF/MenuHorizontal/SobreElBanco/Conferencias/2017/papers/171005_15.30-17.00_1_ZIMMERMANN_paper.pdf (accessed on 28 February 2020).

| 1 | The number of obervations are 105 bacause Bankscope does not have data of every bank for all the years from 2006 to 2018. |

| 2 | |

| 3 | We have not reported results of pooled OLS estimator as they are largely consistent with system GMM estimator and fixed effects estimator. |

| 4 | Data were collected from: https://fred.stlouisfed.org/series/DDDI06NZA156NWDB. |

| Variables | Notation | Measure | Expected Sign | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|---|---|

| Dependent Variables | |||||||

| Return on Assets | ROA | Profit before tax/Total Assets (%) | 0.01 | 0.01 | −0.02 | 0.02 | |

| Return on Equity | ROE | Profit before tax/Total Equity (%) | 0.14 | 0.21 | −0.09 | 0.24 | |

| Independent Variables | |||||||

| Monetary Policy Variables | |||||||

| Short-term interest rate | SR | Cash rate set by Reserve Bank New Zealand (%) | +/− | 3.44 | 2.03 | 1.75 | 8.25 |

| Long-term interest rate | LR | 10-year bond rate (%) | +/− | 4.38 | 1.26 | 2.45 | 6.4 |

| Control Variables | |||||||

| Capital Adequacy Ratio | CAR | Tier 1 Capital + Tier 2 Capital / Risk-Weighted Assets (%) | +/− | 19.82 | 49.84 | 9.81 | 36.33 |

| Non-Performing Loan Ratio | NPLR | Non-performing Loans/Total Loans (%) | − | 0.01 | 0.01 | 0 | 0.04 |

| Cost to income ratio | COST | Operating Cost / Total Income (%) | − | 53.5 | 21.46 | 29.42 | 78.24 |

| Total Assets (Bank Size) | SIZE | Natural log of total assets of bank | +/− | 15.61 | 2.1 | 10.88 | 18.53 |

| Loan to Asset Ratio | LAR | Total Loans / Total Assets (%) | +/− | 0.77 | 0.14 | 0.38 | 0.91 |

| Inflation | INF | Yearly percentage change in Consumer Price Index (CPI) (%) | + | 1.94 | 1.07 | 0.1 | 4 |

| Gross Domestic Product | GDP | Yearly GDP growth rate (%) | + | 2.32 | 1.42 | −1.2 | 3.9 |

| ROA (Panel A) | ROE (Panel B) | |||||

|---|---|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (1) | (2) | (3) |

| SR | 0.0006 *** | 0.0006 *** | 0.0107 *** | 0.0175 *** | ||

| (0.0001) | (0.0002) | (0.0019) | (0.0052) | |||

| LR | −0.0004 ** | −0.0006 ** | −0.0019 | −0.0017 | ||

| (0.0001) | (0.0003) | (0.0042) | (0.0104) | |||

| Lagged ROA | 0.4935 *** | 0.8529 *** | 1.0058 *** | |||

| (0.1393) | (0.1964) | (0.1748) | ||||

| Lagged ROE | 0.5188 *** | 0.4795 *** | −0.4033 ** | |||

| (0.0876) | (0.1246) | (0.1831) | ||||

| CAR | 0.0001 *** | 0.0001 *** | 0.0001 *** | −0.0003 | 0.0001 | −0.0003 |

| (0.0000) | (0.0000) | (0.0000) | (0.0003) | (0.0004) | (0.0005) | |

| NPLR | −0.0314 | −0.0058 | 0.0349 | −1.2205 *** | 0.0477 | −1.7720 |

| (0.0444) | (0.0558) | (0.0552) | (0.3937) | (1.5428) | (2.3244) | |

| COST | −0.0002 *** | −0.0001 | −0.0000 | −0.0017 *** | −0.0012 * | −0.0028 *** |

| (0.0000) | (0.0001) | (0.0001) | (0.0005) | (0.0007) | (0.0008) | |

| SIZE | −0.0001 | −0.0000 | −0.0001 | 0.0009 | 0.0107 * | 0.0208 * |

| (0.0004) | (0.0003) | (0.0003) | (0.0046) | (0.0055) | (0.0102) | |

| LAR | 0.0082 ** | 0.0032 | 0.0041 | 0.0348 | 0.0361 | 0.1501 * |

| (0.0033) | (0.0036) | (0.0041) | (0.0474) | (0.0418) | (0.0833) | |

| INF | 0.0002 | 0.0007 *** | 0.0002 | −0.0012 | 0.0006 | −0.0054 |

| (0.0002) | (0.0002) | (0.0004) | (0.0035) | (0.0021) | (0.0036) | |

| GDP | 0.0006 * | 0.0008 *** | 0.0004 | 0.0016 | 0.0045 | 0.0116 ** |

| (0.0003) | (0.0002) | (0.0002) | (0.0061) | (0.0044) | (0.0050) | |

| Constant | 0.0058 | 0.0004 | −0.0029 | 0.0996 | −0.0719 | −0.0868 |

| (0.0054) | (0.0069) | (0.0060) | (0.0942) | (0.1165) | (0.1759) | |

| Observations | 94 | 94 | 94 | 94 | 94 | 94 |

| Number of id | 13 | 13 | 13 | 13 | 13 | 13 |

| AR(2) (p-value) | 0.731 | 0.791 | 0.913 | 0.260 | 0.224 | 0.141 |

| Sargan test (p-value) | 0.122 | 0.474 | 0.474 | 0.470 | 0.328 | 1.000 |

| ROA (Panel A) | ROE (Panel B) | |||

|---|---|---|---|---|

| Variables | (1) | (2) | (1) | (2) |

| SR | 0.0006 * | 0.0023 | ||

| (0.0004) | (0.0047) | |||

| LR | −0.0009 *** | −0.0291 *** | ||

| (0.0003) | (0.0107) | |||

| CBA | −0.0014 ** | 0.0012 | −0.0238 * | 0.046 |

| (0.0007) | (0.0014) | (0.0132) | (0.0177) | |

| (0.0467) | (0.2923) | |||

| CAR | 0.0001 | 0.0000 | −0.0022 | −0.0087 |

| (0.0001) | (0.0002) | (0.0035) | (0.0061) | |

| NPLR | −0.0297 | −0.0392 | −1.1519 | 17.6412 |

| (0.0461) | (0.0469) | (0.7464) | (17.2384) | |

| COST | −0.0005 *** | −0.0004 *** | −0.0063 *** | −0.0022 |

| (0.0001) | (0.0001) | (0.0014) | (0.0023) | |

| SIZE | −0.0061 ** | −0.0043 | −0.0945 ** | −0.3252 |

| (0.0030) | (0.0039) | (0.0438) | (0.2425) | |

| LAR | 0.0216 | 0.0224 | −0.1004 | 0.9744 |

| (0.0149) | (0.0137) | (0.1838) | (0.9008) | |

| INF | 0.0002 | 0.0001 | 0.0029 | −0.0116 |

| (0.0002) | (0.0003) | (0.0026) | (0.0140) | |

| GDP | 0.0004 | −0.0002 | 0.0029 | −0.0026 |

| (0.0003) | (0.0003) | (0.0031) | (0.0023) | |

| Constant | −0.0003 *** | −0.0000 | −0.0047 * | 0.0040 |

| 0.0006 * | 0.0023 | |||

| Observations | 81 | 81 | 81 | 81 |

| Number of id | 12 | 12 | 12 | 12 |

| AR(2) (p-value) | 0.774 | 0.478 | 0.198 | 0.299 |

| Sargan test (p-value) | 0.277 | 0.24 | 1.000 | 1.000 |

| ROA (Panel A) | ROE (Panel B) | |||||

|---|---|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (1) | (2) | (3) |

| SR | 0.0010 ** | 0.0008 * | 0.0027 | 0.0002 | ||

| (0.0004) | (0.0004) | (0.0071) | (0.0070) | |||

| LR | −0.0009 ** | −0.0008 * | −0.0129 ** | −0.0128 ** | ||

| (0.0004) | (0.0004) | (0.0061) | (0.0062) | |||

| CAR | 0.0002 | 0.0002 | 0.0001 | −0.0014 | −0.0031 | −0.0032 |

| (0.0003) | (0.0003) | (0.0003) | (0.0055) | (0.0054) | (0.0054) | |

| NPLR | −0.0533 | −0.0486 | −0.0422 | −1.0133 | −0.8483 | −0.8449 |

| (0.0582) | (0.0582) | (0.0571) | (0.9463) | (0.9129) | (0.9256) | |

| COST | −0.0004 *** | −0.0004 *** | −0.0004 *** | −0.0066 *** | −0.0061 *** | −0.0061 *** |

| (0.0001) | (0.0001) | (0.0001) | (0.0017) | (0.0016) | (0.0017) | |

| SIZE | −0.0026 | −0.0058 * | −0.0047 | −0.0935 * | −0.1299 ** | −0.1296 ** |

| (0.0031) | (0.0033) | (0.0033) | (0.0515) | (0.0519) | (0.0531) | |

| LAR | 0.0205 | 0.0316 ** | 0.0266 * | 0.2123 | 0.3196 | 0.3178 |

| (0.0146) | (0.0146) | (0.0146) | (0.2385) | (0.2307) | (0.2380) | |

| INF | −0.0001 | 0.0001 | 0.0000 | −0.0009 | 0.0008 | 0.0008 |

| (0.0003) | (0.0003) | (0.0003) | (0.0053) | (0.0052) | (0.0053) | |

| GDP | −0.0002 | 0.0004 | −0.0001 | −0.0023 | −0.0013 | −0.0015 |

| (0.0004) | (0.0002) | (0.0003) | (0.0056) | (0.0038) | (0.0055) | |

| Constant | 0.0001 | −0.0004 | −0.0000 | −0.0021 | −0.0050 | −0.0049 |

| (0.0004) | (0.0004) | (0.0004) | (0.0068) | (0.0058) | (0.0068) | |

| Observations | 81 | 81 | 81 | 81 | 81 | 81 |

| R-squared | 0.428 | 0.433 | 0.464 | 0.367 | 0.41 | 0.41 |

| Fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| ADF | PP | |||

|---|---|---|---|---|

| Variables | Z | p Value | Z | p Value |

| ROA | −2.9281 | 0.0017 *** | −4.6831 | 0.0000 *** |

| ROE | −3.3620 | 0.0004 *** | −4.3572 | 0.0000 *** |

| SR | −21.7400 | 0.0000 *** | −1.8549 | 0.0318 ** |

| LR | 3.4686 | 0.9997 | 3.9818 | 1.0000 |

| CAR | −5.2699 | 0.0000 *** | −7.0991 | 0.0000 *** |

| NPLR | −3.7224 | 0.0001 *** | −1.4948 | 0.0675 * |

| COST | −1.3210 | 0.0932 * | −0.4200 | 0.3372 |

| SIZE | −2.5764 | 0.0050 *** | −5.0285 | 0.0000 *** |

| LAR | −2.3044 | 0.0106 ** | −3.0246 | 0.0012 *** |

| INF | 0.7065 | 0.7600 | −1.6607 | 0.0484 ** |

| GDP | −1.6595 | 0.0485 ** | −1.4994 | 0.0669 ** |

| ROA (Panel A) | ROE (Panel B) | |||||

|---|---|---|---|---|---|---|

| Variables | (1) | (2) | (3) | (1) | (2) | (3) |

| SR | 0.0011 ** | 0.0008 ** | 0.0116 * | 0.0056 | ||

| (0.0004) | (0.0003) | (0.0061) | (0.0051) | |||

| LR | −0.0010 *** | −0.0009 *** | −0.0201 *** | −0.0178 *** | ||

| (0.0002) | (0.0002) | (0.0056) | (0.0056) | |||

| CAR | 0.0000 | −0.0000 | −0.0000 | −0.0026 | −0.0042 | −0.0017 |

| (0.0002) | (0.0002) | (0.0002) | (0.0040) | (0.0029) | (0.0041) | |

| NPLR | −0.0585 | −0.0674 | −0.0503 | −0.5496 | −0.7574 | −0.3762 |

| (0.0624) | (0.0718) | (0.0578) | (0.7046) | (0.6283) | (0.6277) | |

| COST | −0.0004 *** | −0.0003 *** | −0.0004 ** | −0.0055 *** | −0.0048 *** | −0.0042 ** |

| (0.0001) | (0.0001) | (0.0001) | (0.0016) | (0.0012) | (0.0018) | |

| SIZE | −0.0032 | −0.0045 * | −0.0043 | −0.0334 | −0.0893 ** | −0.0813 |

| (0.0025) | (0.0025) | (0.0035) | (0.0440) | (0.0366) | (0.0591) | |

| LAR | 0.0115 | 0.0259 *** | 0.0163 * | −0.2352 | −0.0268 | −0.1094 |

| (0.0104) | (0.0050) | (0.0075) | (0.2456) | (0.1968) | (0.2473) | |

| INF | 0.0001 | −0.0000 | 0.0002 | 0.0017 | 0.0047 | 0.0063 |

| (0.0002) | (0.0002) | (0.0003) | (0.0026) | (0.0028) | (0.0055) | |

| GDP | −0.0003 | −0.0000 | −0.0003 | −0.0025 | −0.0004 | −0.0012 |

| (0.0002) | (0.0002) | (0.0003) | (0.0026) | (0.0022) | (0.0040) | |

| Constant | 0.0003 | −0.0005 ** | −0.0000 | 0.0020 | −0.0075 ** | −0.0037 |

| (0.0003) | (0.0002) | (0.0003) | (0.0028) | (0.0031) | (0.0047) | |

| Observations | 81 | 81 | 81 | 81 | 81 | 81 |

| Number of id | 12 | 12 | 12 | 12 | 12 | 12 |

| AR(2) (p-value) | 0.377 | 0.219 | 0.352 | 0.200 | 0.259 | 0.326 |

| Sargan test (p-value) | 0.951 | 0.564 | 0.997 | 0.844 | 0.466 | 0.280 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kumar, V.; Acharya, S.; Ho, L.T.H. Does Monetary Policy Influence the Profitability of Banks in New Zealand? Int. J. Financial Stud. 2020, 8, 35. https://doi.org/10.3390/ijfs8020035

Kumar V, Acharya S, Ho LTH. Does Monetary Policy Influence the Profitability of Banks in New Zealand? International Journal of Financial Studies. 2020; 8(2):35. https://doi.org/10.3390/ijfs8020035

Chicago/Turabian StyleKumar, Vijay, Sanjeev Acharya, and Ly T. H. Ho. 2020. "Does Monetary Policy Influence the Profitability of Banks in New Zealand?" International Journal of Financial Studies 8, no. 2: 35. https://doi.org/10.3390/ijfs8020035

APA StyleKumar, V., Acharya, S., & Ho, L. T. H. (2020). Does Monetary Policy Influence the Profitability of Banks in New Zealand? International Journal of Financial Studies, 8(2), 35. https://doi.org/10.3390/ijfs8020035