The Business Sector, Firm Age, and Performance: The Mediating Role of Foreign Ownership and Financial Leverage

Abstract

:1. Introduction

2. Materials and Methods

2.1. Materials

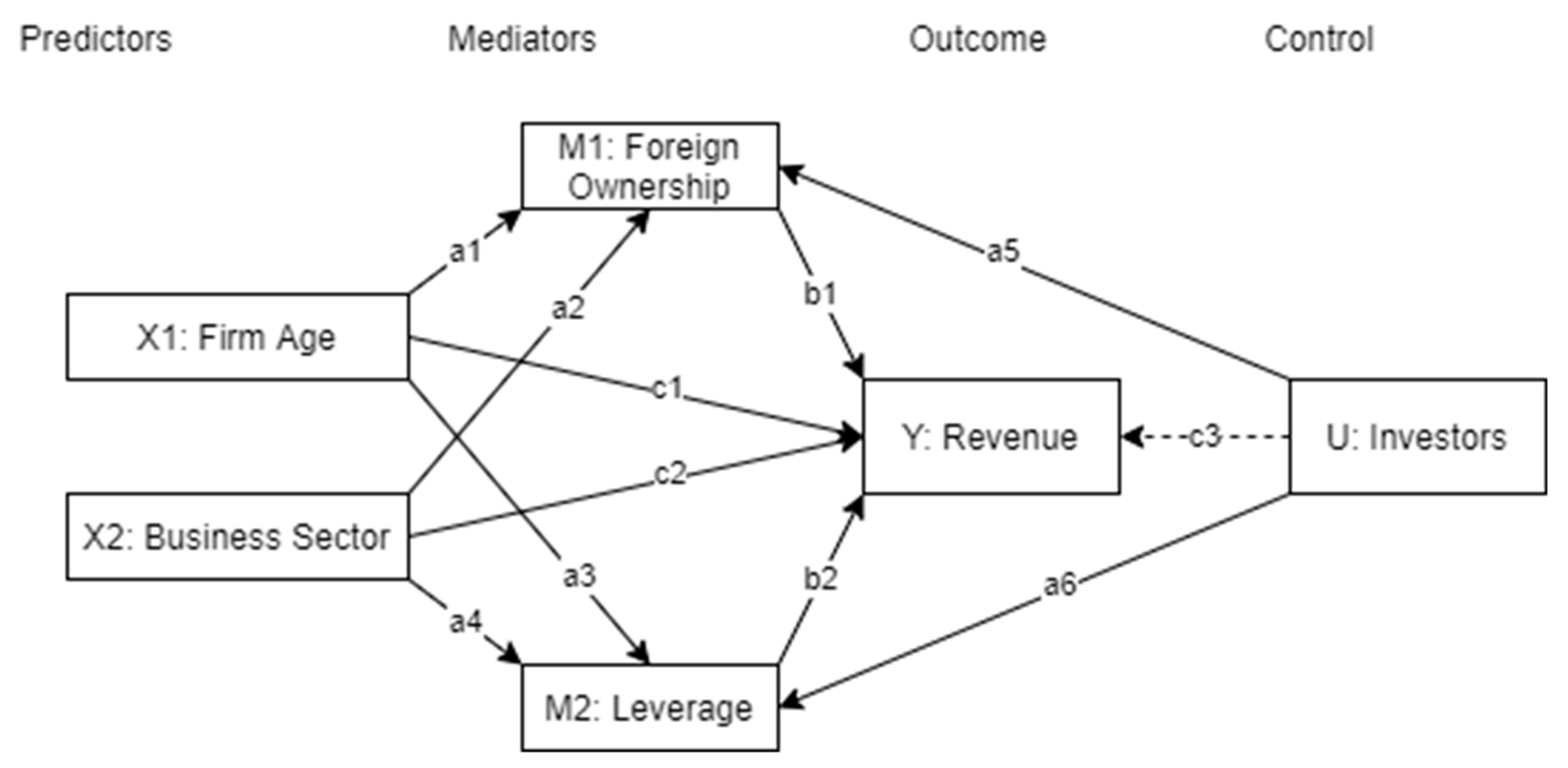

2.2. Methods

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Akolaa, Andrews Adugudaa. 2018. Foreign Market Entry through Acquisition and Firm Financial Performance: Empirical Evidence from Ghana. International Journal of Emerging Markets 13: 1348–71. [Google Scholar] [CrossRef]

- Anton, Sorin Gabriel. 2019. Leverage and Firm Growth: An Empirical Investigation of Gazelles from Emerging Europe. International Entrepreneurship and Management Journal 15: 209–32. [Google Scholar] [CrossRef]

- Arnold, Jens Matthias, Beata Javorcik, Molly Lipscomb, and Aaditya Mattoo. 2016. Services Reform and Manufacturing Performance: Evidence from India. The Economic Journal 126: 1–39. [Google Scholar] [CrossRef] [Green Version]

- Benfratello, Luigi, and Alessandro Sembenelli. 2006. Foreign Ownership and Productivity: Is the Direction of Causality so Obvious? International Journal of Industrial Organization 24: 733–51. [Google Scholar] [CrossRef] [Green Version]

- Bentivogli, Chiara, and Litterio Mirenda. 2017. Foreign Ownership and Performance: Evidence from Italian Firms Foreign Ownership and Performance: Evidence From. International Journal of the Economics of Business 1516: 1–23. [Google Scholar] [CrossRef]

- Campello, Murillo. 2006. Debt Financing: Does It Boost or Hurt Firm Performance in Product Markets? Journal of Financial Economics 82: 135–72. [Google Scholar] [CrossRef]

- Canales, Rodrigo, and Ramana Nanda. 2012. A Darker Side to Decentralized Banks: Market Power and Credit Rationing in SME Lending. Journal of Financial Economics 105: 353–66. [Google Scholar] [CrossRef]

- Capasso, Arturo, Carmen Gallucci, and Matteo Rossi. 2015. Standing the Test of Time. Does Firm Performance Improve with Age? An Analysis of the Wine Industry. Business History 57: 37–41. [Google Scholar] [CrossRef]

- Casey, Eddie, and Conor M. OToole ’. 2014. Bank Lending Constraints, Trade Credit and Alternative Financing during the Financial Crisis: Evidence from European SMEs. Journal of Corporate Finance 27: 173–93. [Google Scholar] [CrossRef]

- Chen, Homin, and Tain-jy Chen. 1998. Network Linkages and Location Choice in Foreign Direct Investment. Journal of International Business Studies 29: 445–67. [Google Scholar] [CrossRef]

- Cheong, Calvin W. H., Miin Huui Lee, and Marc Arul Weissmann. 2020. Credit Access, Tax Structure and the Performance of Malaysian Manufacturing SMEs. International Journal of Managerial Finance 16: 433–54. [Google Scholar] [CrossRef]

- Coad, Alex. 2018. Firm Age: A Survey. Journal of Evolutionary Economics 28: 13–43. [Google Scholar] [CrossRef]

- Coad, Alex, Agustí Segarra, and Mercedes Teruel. 2013. Like Milk or Wine: Does Firm Performance Improve with Age? Structural Change and Economic Dynamics 24: 173–89. [Google Scholar] [CrossRef] [Green Version]

- Cubillas, Elena, and Nuria Suárez. 2018. Bank Market Power and Lending during the Global Financial Crisis. Journal of International Money and Finance 89: 1–22. [Google Scholar] [CrossRef]

- Duggan, Victor, Sjamsu Rahardja, and Gonzalo Varela. 2013. Service Sector Reform and Manufacturing Productivity: Evidence from Indonesia. Policy Research Working Papers. Washington: The World Bank. [Google Scholar] [CrossRef] [Green Version]

- Esteve-Pérez, Silviano, Fabio Pieri, and Diego Rodriguez. 2018. Age and Productivity as Determinants of Firm Survival over the Industry Life Cycle. Industry and Innovation 25: 167–98. [Google Scholar] [CrossRef]

- Ettlie, John E., and Stephen R. Rosenthal. 2011. Service versus Manufacturing Innovation. Journal of Product Innovation Management 28: 285–99. [Google Scholar] [CrossRef]

- Fowowe, Babajide. 2017. Access to Finance and Firm Performance: Evidence from African Countries. Journal of Advanced Research 7: 6–17. [Google Scholar] [CrossRef]

- Fungáčová, Zuzana, Laura Solanko, and Laurent Weill. 2014. Does Competition Influence the Bank Lending Channel in the Euro Area? Journal of Banking & Finance 49: 356–66. [Google Scholar] [CrossRef]

- Hande, Karadag. 2017. The Impact of Industry, Firm Age and Education Level on Financial Management Performance in Small and Medium-Sized Enterprises (SMEs): Evidence from Turkey. Journal of Entrepreneurship in Emerging Economies 9: 300–314. [Google Scholar] [CrossRef]

- Ibhagui, Oyakhilome W., and Felicia O. Olokoyo. 2018. Leverage and Firm Performance: New Evidence on the Role of Firm Size. The North American Journal of Economics and Finance 45: 57–82. [Google Scholar] [CrossRef]

- Ilhan, Dalci. 2018. Impact of Financial Leverage on Profitability of Listed Manufacturing Firms in China. Pacific Accounting Review 30: 410–32. [Google Scholar] [CrossRef]

- Jin, Man, Shunan Zhao, and Subal C. Kumbhakar. 2019. Financial Constraints and Firm Productivity: Evidence from Chinese Manufacturing. European Journal of Operational Research 275: 1139–56. [Google Scholar] [CrossRef]

- Joshua, Abor. 2007. Debt Policy and Performance of SMEs: Evidence from Ghanaian and South African Firms. Edited by Michael R Powers. The Journal of Risk Finance 8: 364–79. [Google Scholar] [CrossRef]

- Kashefi Pour, Eilnaz, and Ehsan Khansalar. 2015. Does Debt Capacity Matter in the Choice of Debt in Reducing the Underinvestment Problem? Research in International Business and Finance 34: 251–64. [Google Scholar] [CrossRef]

- Kücher, Alexander, Stefan Mayr, Christine Mitter, Christine Duller, and Birgit Feldbauer Durstmüller. 2018. Firm Age Dynamics and Causes of Corporate Bankruptcy: Age Dependent Explanations for Business Failure. Review of Managerial Science, 0123456789. [Google Scholar] [CrossRef] [Green Version]

- Lahiri, Somnath, and Saptarshi Purkayastha. 2017. Impact of Industry Sector on Corporate Diversification and Firm Performance: Evidence from Indian Business Groups. Canadian Journal of Administrative Sciences/Revue Canadienne Des Sciences de l’Administration 34: 77–88. [Google Scholar] [CrossRef]

- Lang, Larry, Eli Ofek, and René M. Stulz. 1996. Leverage, Investment, and Firm Growth. Journal of Financial Economics 40: 3–29. [Google Scholar] [CrossRef] [Green Version]

- Lefever, Samúel, Michael Dal, and Ásrún Matthíasdóttir. 2007. Online Data Collection in Academic Research: Advantages and Limitations. British Journal of Educational Technology 38: 574–82. [Google Scholar] [CrossRef]

- Legesse, Guta. 2018. An Analysis of the Effects of Aging and Experience on Firms’ Performance BT—Economic Growth and Development in Ethiopia. Edited by Almas Heshmati and Haeyeon Yoon. Singapore: Springer, pp. 255–76. [Google Scholar] [CrossRef]

- Li, Yao Amber, Wei Liao, and Chen Carol Zhao. 2018. Credit Constraints and Firm Productivity: Microeconomic Evidence from China. Research in International Business and Finance 45: 134–49. [Google Scholar] [CrossRef]

- Lindemanis, Mārtiņš, Artūrs Loze, and Anete Pajuste. 2019. The Effect of Domestic to Foreign Ownership Change on Firm Performance in Europe. International Review of Financial Analysis, 101341. [Google Scholar] [CrossRef]

- Loderer, Claudio, and Urs Waelchli. 2010. Munich Personal RePEc Archive Firm Age and Performance Firm Age and Performance. no. 26450. Available online: http://mpra.ub.unimuenchen.de/26450/1/MPRA_paper_26450.pdf (accessed on 26 October 2020).

- Love, James H., Brian Ashcroft, and Stewart Dunlop. 1996. Corporate Structure, Ownership and the Likelihood of Innovation. Applied Economics 28: 737–46. [Google Scholar] [CrossRef]

- Lwango, Albert, Régis Coeurderoy, and Gabriel A. Giménez Roche. 2017. Family Influence and SME Performance under Conditions of Firm Size and Age. Journal of Small Business and Enterprise Development 24: 629–48. [Google Scholar] [CrossRef]

- MacKinnon, David P., Stefany Coxe, and Amanda N. Baraldi. 2012. Guidelines for the Investigation of Mediating Variables in Business Research. Journal of Business and Psychology 27: 1–14. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Majumdar, Sumit K. 1997. The Impact of Size and Age on Firm-Level Performance: Some Evidence from India. Review of Industrial Organization 12: 231–41. [Google Scholar] [CrossRef]

- Mallinguh, Edmund, Christopher Wasike, and Zoltan Zeman. 2020. Technology Acquisition and Smes Performance, the Role of Innovation, Export and the Perception of Owner-Managers. Journal of Risk and Financial Management 13: 258. [Google Scholar] [CrossRef]

- Mattoo, Aaditya, Marcelo Olarreaga, and Kamal Saggi. 2004. Mode of Foreign Entry, Technology Transfer, and FDI Policy. Journal of Development Economics 75: 95–111. [Google Scholar] [CrossRef]

- Nachum, Lilach. 2009. When Is Foreignness an Asset or a Liability? Explaining the Performance Differential Between Foreign and Local Firms. Journal of Management 36: 714–39. [Google Scholar] [CrossRef]

- Prajogo, Daniel I. 2006. The Relationship between Innovation and Business Performance—A Comparative Study between Manufacturing and Service Firms. Knowledge and Process Management 13: 218–25. [Google Scholar] [CrossRef]

- Prajogo, Daniel I. 2016. The Strategic Fit between Innovation Strategies and Business Environment in Delivering Business Performance. International Journal of Production Economics 171: 241–49. [Google Scholar] [CrossRef]

- Preacher, Kristopher J., and Andrew F. Hayes. 2008. Asymptotic and Resampling Strategies for Assessing and Comparing Indirect Effects in Multiple Mediator Models. Behavior Research Methods 40: 879–91. [Google Scholar] [CrossRef]

- Reed, Richard, and Susan F Storrud-Barnes. 2009. Systematic Performance Differences across the Manufacturing-Service Continuum. Service Business 3: 319. [Google Scholar] [CrossRef]

- Seo, Yong Won, Youn Sung Kim, DaeSoo Kim, Yung-Mok Yu, and Sung Hee Lee. 2016. Innovation Patterns of Manufacturing and Service Firms in Korea. Total Quality Management & Business Excellence 27: 718–34. [Google Scholar] [CrossRef]

- Srholec, Martin. 2009. Does Foreign Ownership Facilitate Cooperation on Innovation? Firm-Level Evidence from the Enlarged European Union. The European Journal of Development Research 21: 47–62. [Google Scholar] [CrossRef]

- Thai, An. 2019. The Effect of Foreign Ownership on Capital Structure in Vietnam. Review of Integrative Business and Economics Research 8: 20–32. [Google Scholar]

- Trung, Tran Quoc. 2020. Foreign Ownership and Investment Efficiency: New Evidence from an Emerging Market. International Journal of Emerging Markets 15: 1185–99. [Google Scholar] [CrossRef]

- Tsuruta, Daisuke. 2015. Leverage and Firm Performance of Small Businesses: Evidence from Japan. Small Business Economics 44: 385–410. [Google Scholar] [CrossRef]

- Tsuruta, Daisuke. 2017. Variance of Firm Performance and Leverage of Small Businesses. Journal of Small Business Management 55: 404–29. [Google Scholar] [CrossRef]

- Vithessonthi, Chaiporn, and Jittima Tongurai. 2015. The Effect of Leverage on Performance: Domestically-Oriented versus Internationally-Oriented Firms. Research in International Business and Finance 34: 265–80. [Google Scholar] [CrossRef]

- Wang, Xiaodong, Liang Han, and Xing Huang. 2020. Bank Competition, Concentration and EU SME Cost of Debt. International Review of Financial Analysis 71: 101534. [Google Scholar] [CrossRef]

- Zaborek, Piotr, and Jolanta Mazur. 2019. Enabling Value Co-Creation with Consumers as a Driver of Business Performance: A Dual Perspective of Polish Manufacturing and Service SMEs. Journal of Business Research 104: 541–51. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Min Stat | Mean Stat | Max Stat | STD Deviation | VIF | 1 | 2 | 3 | 4 | 5 | 6 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue (1) | 4.14 | 6.5535 | 8.16 | 0.8596 | 1 | ||||||

| Firm Age (2) | 0.9 | 1.7293 | 2.18 | 0.29125 | 1.248 | 0.204 | 1 | ||||

| Sector (3) | 1 | 4.03 | 8 | 2.179 | 1.293 | 0.88 | 0.07 | 1 | |||

| Investors (4) | 1 | 3.7587 | 5.75 | 0.7841 | 1.491 | 0.204 | −0.15 | 0.32 | 1 | ||

| Leverage (5) | 3.65 | 6.0453 | 8.14 | 6.0453 | 1.262 | 0.57 | 0.009 | 0.31 | 0.411 | 1 | |

| Foreign Owned (6) | −3.52 | −0.959 | 1.67 | 0.8440 | 1.477 | 0.207 | 0.444 | 0.2 | −0.298 | −0.021 | 1.00 |

| Antecedent | Estimates | Standard Error | p-Value | 95% Bootstrap Confidence Interval |

|---|---|---|---|---|

| X1M1: Firm Age~Foreign Own | 0.109 | 0.036 | 0.002 | 0.0480→0.0740 |

| X2M1: Sector~Foreign Own | −0.393 | 0.427 | 0.357 | −1.3190→0.5000 |

| X1M2: Firm Age~Leverage | −0.085 | 0.000 | 0.096 | −0.1820→0.0031 |

| X2M2: Sector~Leverage | 1.113 | 0.0607 | 0.067 | −0.1000→2.2480 |

| M1U: Investors~Foreign Own | 0.000 | 0.000 | 0.062 | 0.0000→0.0000 |

| M2U: Investors~Leverage | 0.000 | 0.000 | 0.474 | 0.0000→0.0000 |

| M1; Y: Foreign Own~Revenue | 0.434 | 0.163 | 0.008 | 0.1230→0.7200 |

| M2; Y: Leverage~Revenue | 0.241 | 0.118 | 0.042 | 0.0100→0.7200 |

| X1; Y: Firm Age~Revenue | 0.237 | 0.068 | 0.000 | 0.0990→0.3660 |

| X2; Y: Sector~Revenue | −1.830 | 0.816 | 0.025 | −3.464→−0.2580 |

| U; Y: Investors~Revenue | 0.000 | 0.000 | 0.000 | 0.0000→0.0000 |

| Indirect Effect 1 | 0.047 | 0.025 | 0.041 | 0.0100→0.1100 |

| Indirect Effect 2 | −0.02 | 0.017 | 0.231 | −0.0580→0.0070 |

| Indirect Effect 3 | −0.17 | 0.213 | 0.424 | −0.6130→0.2660 |

| Indirect Effect 4 | 0.268 | 0.218 | 0.219 | −0.0310→0.8050 |

| Comp1: | 0.068 | 0.030 | 0.022 | 0.0170→0.1340 |

| Comp2: | −0.439 | 0.319 | 0.169 | −1.1220→0.1550 |

| Comp3: | 0.218 | 0.211 | 0.303 | −0.1910→0.6630 |

| Comp4: | −0.289 | 0.224 | 0.198 | −0.8230→0.0210 |

| T. Effect 1: | 0.263 | 0.063 | 0.000 | 0.1460→0.3920 |

| T. Effect 2: | −1.732 | 0.850 | 0.042 | −3.4530→−0.1040 |

| T. Effect 3: | 0.000 | 0.00 | 0.000 | 0.0000→0.000 |

| R Square Estimates: | Revenue | 0.350 | ||

| Foreign Own | 0.107 | |||

| Leverage | 0.041 |

| Sector | Effect (Standard Error) | p-Value | 95% Bootstrap Confidence Interval |

|---|---|---|---|

| Agriculture | −0.5450 (0.2731) | 0.0504 | −1.0909→0.009 |

| Commercial and Service | −0.6210 (0.3089) | 0.0487 | −1.2386→−0.0035 |

| Construction and Allied | 0.4367 (0.3899) | 0.2670 | −0.3427→1.2160 |

| Energy and Petroleum | −1.2016 (0.3152) | 0.0003 | −1.8317→−0.5716 |

| Insurance | −1.3351 (0.7523) | 0.809 | −2.8390→0.1687 |

| Investment | −0.6576 (0.3165) | 0.0419 | −1.2902→−0.0249 |

| Manufacturing and Allied | 1.1765 (0.4155) | 0.0062 | 0.3459→2.0071 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mallinguh, E.; Wasike, C.; Zoltan, Z. The Business Sector, Firm Age, and Performance: The Mediating Role of Foreign Ownership and Financial Leverage. Int. J. Financial Stud. 2020, 8, 79. https://doi.org/10.3390/ijfs8040079

Mallinguh E, Wasike C, Zoltan Z. The Business Sector, Firm Age, and Performance: The Mediating Role of Foreign Ownership and Financial Leverage. International Journal of Financial Studies. 2020; 8(4):79. https://doi.org/10.3390/ijfs8040079

Chicago/Turabian StyleMallinguh, Edmund, Christopher Wasike, and Zeman Zoltan. 2020. "The Business Sector, Firm Age, and Performance: The Mediating Role of Foreign Ownership and Financial Leverage" International Journal of Financial Studies 8, no. 4: 79. https://doi.org/10.3390/ijfs8040079

APA StyleMallinguh, E., Wasike, C., & Zoltan, Z. (2020). The Business Sector, Firm Age, and Performance: The Mediating Role of Foreign Ownership and Financial Leverage. International Journal of Financial Studies, 8(4), 79. https://doi.org/10.3390/ijfs8040079