Intellectual Structure and Evolution of Accounting Conservatism Research: Past Trends and Future Research Suggestions

, , , , and

, , , , and

Abstract

:1. Introduction

2. Methods

Scientific Tools and Support

3. Results

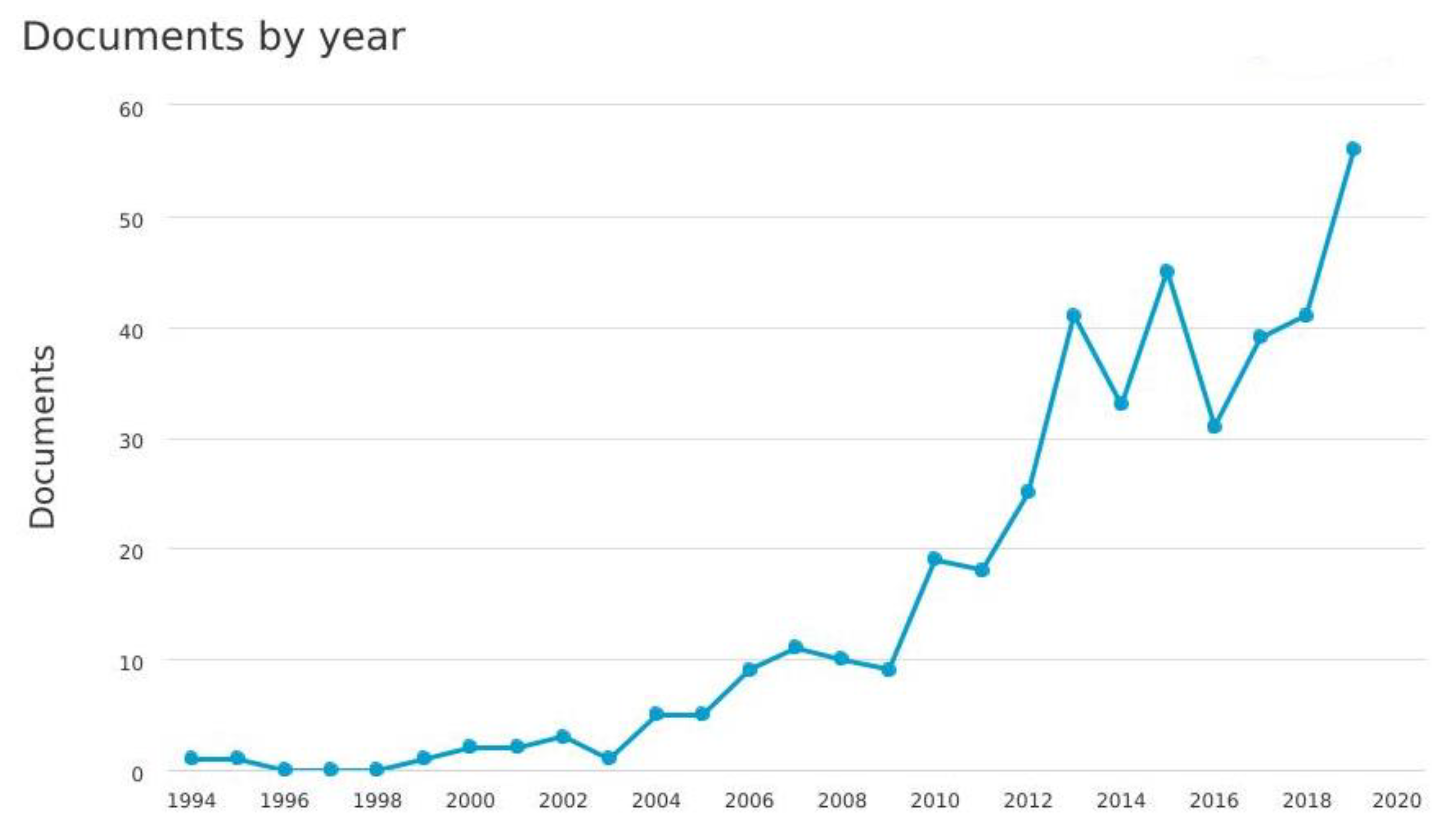

3.1. Publication Trend

3.2. Countries and Languages of Publications

3.3. The Most Productive Universities

3.4. Leading Journals

3.5. The Most Productive Authors in AC

3.6. The Most Cited Publication

4. Discussion and Future Research

5. Conclusions and Limitations

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ahmed, Anwer S., and Scott Duellman. 2013. Managerial overconfidence and accounting conservatism. Journal of Accounting Research 51: 1–30. [Google Scholar] [CrossRef]

- Ahmed, Imran, Misbah Ahmad, Joel J.P.C. Rodrigues, Gwanggil Jeon, and Sadia Din. 2021. A deep learning-based social distance monitoring framework for COVID-19. Sustainable Cities and Society 65: 102571. [Google Scholar] [CrossRef]

- Albort-Morant, Gema, and Domingo Ribeiro-Soriano. 2016. A bibliometric analysis of international impact of business incubators. Journal of Business Research 69: 1775–9. [Google Scholar] [CrossRef]

- Ball, Ray, and Lakshmanan Shivakumar. 2005. Earnings quality in UK private firms: Comparative loss recognition timeliness. Journal of Accounting and Economics 39: 83–128. [Google Scholar] [CrossRef]

- Barth, Mary E., William H. Beaver, and Wayne R. Landsman. 2001. The relevance of the value relevance literature for financial accounting standard setting: Another view. Journal of Accounting and Economics 31: 77–104. [Google Scholar] [CrossRef]

- Basu, Sudipta. 1997. The conservatism principle and the asymmetric timeliness of earnings1. Journal of Accounting and Economics 24: 3–37. [Google Scholar] [CrossRef] [Green Version]

- Basu, Sudipta, Lee-Seok Hwang, and Ching-Lih Jan. 2001. Differences in Conservatism between Big Eight and Non-Big Eight Auditors. Available online: http://ssrn.com/abstract=2428836 (accessed on 1 June 2021).

- Beatty, Anne, Joseph Weber, and Jeff Jiewei Yu. 2008. Conservatism and Debt. Journal of Accounting and Economics 45: 154–74. [Google Scholar] [CrossRef]

- Björk, Tomas, Agatha Murgoci, and Xun Yu Zhou. 2014. Mean–variance portfolio optimization with state-dependent risk aversion. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 24: 1–24. [Google Scholar] [CrossRef]

- Boulton, Thomas J., Scott B. Smart, and Chad J. Zutter. 2017. Conservatism and international IPO underpricing. Journal of International Business Studies 48: 763–85. [Google Scholar] [CrossRef]

- Bouyssou, Denis, and Thierry Marchant. 2011. Bibliometric rankings of journals based on impact factors: An axiomatic approach. Journal of Informetrics 5: 75–86. [Google Scholar] [CrossRef] [Green Version]

- Cadavid Higuita, Lorena, Gabriel Awad, and Carlos Jaime Franco Cardona. 2012. A bibliometric analysis of a modeled field for disseminating innovation. Estudios Gerenciales 28: 213–36. [Google Scholar] [CrossRef] [Green Version]

- Cao, Viet Nga, and Anh Viet Pham. 2021. Behavioral spillover between firms with shared auditors: The monitoring role of capital market investors. Journal of Corporate Finance 68: 101914. [Google Scholar] [CrossRef]

- Chang, Xin, Gilles Hilary, Jun-koo Kang, and Wenrui Zhang. 2013. Does accounting conservatism impede corporate innovation. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Collazo-Reyes, Francisco. 2014. Growth of the number of indexed journals of Latin America and the Caribbean: The effect on the impact of each country. Scientometrics 98: 197–209. [Google Scholar] [CrossRef]

- Daim, Tugrul U., Guillermo Rueda, Hilary Martin, and Pisek Gerdsri. 2006. Forecasting emerging technologies: Use of bibliometrics and patent analysis. Technological Forecasting and Social Change 73: 981–1012. [Google Scholar] [CrossRef]

- De Bakker, Frank G. A., Peter Groenewegen, and Frank Den Hond. 2005. A bibliometric analysis of 30 years of research and theory on corporate social responsibility and corporate social performance. Business & Society 44: 283–17. [Google Scholar]

- Dhaliwal, Dan, Shawn Huang, Inder K. Khurana, and Raynolde Pereira. 2014. Product market competition and conditional conservatism. Review of Accounting Studies 19: 1309–45. [Google Scholar] [CrossRef]

- Donthu, Naveen, Satish Kumar, and Debidutta Pattnaik. 2020. Forty-five years of Journal of Business Research: A bibliometric analysis. Journal of Business Research 109: 1–14. [Google Scholar] [CrossRef]

- Duque-Oliva, Edison Jair, Amparo Cervera Taulet, and Carlos Rodríguez Romero. 2006. Estudio bibliométrico de los modelos de medición del concepto de calidad percibida del servicio en Internet. INNOVAR. Revista de Ciencias Administrativas y Sociales 1: 223–43. [Google Scholar]

- Durieux, Valérie, and Pierre Alain Gevenois. 2010. Bibliometric indicators: Quality measurements of scientific publication. Radiology 255: 342–51. [Google Scholar] [CrossRef]

- Fagerberg, Jan, Morten Fosaas, and Koson Sapprasert. 2012. Innovation: Exploring the knowledge base. Research Policy 41: 1132–53. [Google Scholar] [CrossRef]

- Farrukh, Muhammad, Fanchen Meng, and Ali Raza. 2020. Twenty-Seven Years of Sustainable Development Journal: A Bibliometric Analysis. Sustainable Development 28: 1725–37. [Google Scholar] [CrossRef]

- Farrukh, Muhammad, Ali Raza, Sarfaraz Javed, and Jason Wai Chow Lee. 2021. Twenty Years of Green Innovation Research: Trends and Way Forward. World Journal of Entrepreneurship. ahead-of-print. [Google Scholar] [CrossRef]

- FASB. 1975. Financial Accounting Standards Board (FASB). Accountingfor Contingencies. Statement of Financial Accounting Standards No. 5. Norwalk: FASB. [Google Scholar]

- FASB. 2009. Financial Accounting Standards Board (FASB). Intangibles–Goodwill and Other. Accounting Standards Codification 350. Norwalk: FASB. [Google Scholar]

- FASB. 2010. Financial Accounting Standards Board (FASB). Conceptual Framework for Financial Reporting: Chapter 1. The Objective of General Purpose Financial Reporting, and Chapter 3, Qualitative Characteristics of Useful Financial Reporting Information. Statement of Financial Accounting Concepts No. 8. Norwalk: FASB. [Google Scholar]

- Feltham, Gerald A., and James A. Ohlson. 1995. Valuation and clean surplus accounting for operating and financial activities. Contemporary Accounting Research 11: 689–731. [Google Scholar] [CrossRef]

- Francis, Bill, Iftekhar Hasan, and Qiang Wu. 2013. The benefits of conservative accounting to shareholders: Evidence from the financial crisis. Accounting Horizons 27: 319–46. [Google Scholar] [CrossRef]

- Gao, Weiwei, Ting Cao, and Zhen Huang. 2020. Do outsiders listen to insiders? The role of government support in market reactions to earnings announcements. Managerial and Decision Economics 42: 781–95. [Google Scholar] [CrossRef]

- Garfield, Eugene. 2006. Citation indexes for science. A new dimension in documentation through association of ideas. International Journal of Epidemiology 35: 1123–7. [Google Scholar] [CrossRef] [Green Version]

- Gaviria-Marin, Magaly, Jose M. Merigo, and Simona Popa. 2018. Twenty years of the Journal of Knowledge Management: A bibliometric analysis. Journal of Knowledge Management 22: 1655–87. [Google Scholar] [CrossRef] [Green Version]

- Gigler, Frank, Chandra Kanodia, Haresh Sapra, and Raghu Venugopalan. 2009. Accounting conservatism and the efficiency of debt contracts. Journal of Accounting Research 47: 767–97. [Google Scholar] [CrossRef]

- Glover, Jonathan C., and Haijin H. Lin. 2018. Accounting conservatism and incentives: Intertemporal considerations. The Accounting Review 93: 181–201. [Google Scholar] [CrossRef]

- Gu, Zhouyang, Fanchen Meng, and Muhammad Farrukh. 2021. Mapping the Research on Knowledge Transfer: A Scientometrics Approach. IEEE Access 9: 34647–59. [Google Scholar] [CrossRef]

- Guay, Wayne, and Robert Verrecchia. 2006. Discussion of an economic framework for conservative accounting and Bushman and Piotroski 2006. Journal of Accounting and Economics 42: 149–65. [Google Scholar] [CrossRef] [Green Version]

- Healy, Paul M., and James M. Wahlen. 1999. A review of the earnings management literature and its implications for standard setting. Accounting Horizons 13: 365–83. [Google Scholar] [CrossRef]

- Ho, Simon S., Annie Yuansha Li, Kinsun Tam, and Feida Zhang. 2015. CEO gender, ethical leadership, and accounting conservatism. Journal of Business Ethics 127: 351–70. [Google Scholar] [CrossRef] [Green Version]

- Holthausen, Robert W., and Ross L. Watts. 2001. The relevance of the Value-relevance Literature for Financial Accounting Standard Setting. Journal of Accounting and Economics 31: 3–75. [Google Scholar] [CrossRef] [Green Version]

- Hui, Kai Wai, Steve Matsunaga, and Dale Morse. 2009. The impact of conservatism on management earnings forecasts. Journal of Accounting and Economics 47: 192–207. [Google Scholar] [CrossRef]

- Jackson, Scott B., and Xiaotao Liu. 2010. The Allowancefor Uncollectible Accounts, Conservatism, and Earnings Management. Journal of Accounting Research 48: 565–601. [Google Scholar] [CrossRef]

- Kabir, M. Humayun, and Fawzi Laswad. 2014. The behaviour of earnings, accruals and impairment losses of failed New Zealand finance companies. Australian Accounting Review 24: 262–75. [Google Scholar] [CrossRef]

- Kessler, Maxwell Mirton. 1963. Comparison of the results of bibliographic coupling and analytic subject indexing. American Documentation 16: 223–33. [Google Scholar] [CrossRef]

- Khalilov, Akram, and Beatriz Garcia Osma. 2020. Accounting conservatism and the profitability of corporate insiders. Journal of Business Finance and Accounting 47: 333–64. [Google Scholar] [CrossRef]

- Khan, Mozaffar, and Ross L. Watts. 2009. Estimation and empirical properties of a firm-year measure of accounting conservatism. Journal of Accounting and Economics 48: 132–50. [Google Scholar] [CrossRef]

- Kim, Yongtae, Siqi Li, Carrie Pan, and Luo Zuo. 2013. The Role of Accounting Conservatism in the Equity Market: Evidence from Seasoned Equity Offerings. The Accounting Review 88: 1327–56. [Google Scholar] [CrossRef]

- Kothari, S. P., Karthik Ramanna, and Douglas J. Skinner. 2010. Implications for GAAP from an Analysis of Positive Research in Accounting. Journal of Accounting and Economics 50: 246–86. [Google Scholar] [CrossRef] [Green Version]

- Lafond, Ryan, and Sugata Roychowdhury. 2008. Managerial Ownership and Accounting Conservatism. Journal of Accounting Research 46: 101–35. [Google Scholar] [CrossRef]

- Lara, Juan Manuel García, Beatriz García Osma, and Fernando Penalva. 2009. Accounting conservatism and corporate governance. Review of Accounting Studies 14: 161–201. [Google Scholar] [CrossRef] [Green Version]

- Lara, Juan Manuel García, Beatriz García Osma, and Fernando Penalva. 2016. Accounting conservatism and firm investment efficiency. Journal of Accounting and Economics 61: 221–38. [Google Scholar] [CrossRef] [Green Version]

- Li, Jing. 2013. Accounting Conservatism and Debt Contracts: Efficient Liquidation and Covenant Renegotiation. Contemporary Accounting Research 30: 1082–98. [Google Scholar] [CrossRef]

- Merigó, José M., Christian A. Cancino, Freddy Coronado, and David Urbano. 2016. Academic research in innovation: A country analysis. Scientometrics 108: 559–93. [Google Scholar] [CrossRef]

- Nawaz, Kalsoom, Hafiza Anum Saeed, and Tanveer Aslam Sajeel. 2020. Covid-19 and the State of Research from the Perspective of Psychology. International Journal of Business and Psychology 2: 35–44. [Google Scholar]

- Nerur, Sridhar P., Abdul A. Rasheed, and Vivek Natarajan. 2008. The intellectual structure of the strategic management field: An author co-citation analysis. Strategic Management Journal 29: 319–36. [Google Scholar] [CrossRef]

- Nikolaev, Valeri V. 2010. Debt Covenants and Accounting Conservatism. Journal of Accounting Research 48: 51–89. [Google Scholar] [CrossRef]

- Persson, Olle, Rickard Danell, and J. Wiborg Schneider. 2009. How to use Bibexcel for various types of bibliometric analysis. Celebrating Scholarly Communication Studies: A Festschrift for Olle Persson at His 60th Birthday 5: 9–24. [Google Scholar]

- Pilkington, Alan, and Jack Meredith. 2009. The evolution of the intellectual structure of operations management—1980–2006: A citation/co-citation analysis. Journal of Operations Management 27: 185–202. [Google Scholar] [CrossRef]

- Podsakoff, Philip M., Scott B. MacKenzie, Nathan P. Podsakoff, and Daniel G. Bachrach. 2008. Scholarly influence in the field of management: A bibliometric analysis of the determinants of university and author impact in the management literature in the past quarter century. Journal of Management 34: 641–720. [Google Scholar] [CrossRef] [Green Version]

- Small, Henry. 1973. Co-citation in the scientific literature: A new measure of the relationship between two documents. Journal of the American Society for Information Science 24: 265–69. [Google Scholar] [CrossRef]

- Sterling, Robert. R. 1982. The Theory of the Measurement of Enterprise Income. London: Routledge, pp. 233–82. [Google Scholar]

- Van Eck, Nees Jan, and Ludo Waltman. 2010. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 84: 523–38. [Google Scholar] [CrossRef] [Green Version]

- Watts, Ross L. 2003. Conservatism in accounting part I: Explanations and implications. Accounting Horizons 17: 207–21. [Google Scholar] [CrossRef] [Green Version]

- Wu, Yihua, Muhammad Farrukh, Ali Raza, Fanchen Meng, and Imtiaz Alam. 2021. Framing the Evolution of the Corporate Social Responsibility and Environmental Management Journal. Corporate Social Responsibility and Environmental Management. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Year | Publication | Citations |

|---|---|---|

| 2019 | 56 | 1624 |

| 2018 | 41 | 1240 |

| 2017 | 39 | 967 |

| 2016 | 31 | 955 |

| 2015 | 45 | 856 |

| 2014 | 33 | 627 |

| 2013 | 41 | 609 |

| 2012 | 25 | 409 |

| 2011 | 18 | 430 |

| 2010 | 19 | 297 |

| 2009 | 9 | 210 |

| 2008 | 10 | 154 |

| 2007 | 11 | 115 |

| 2006 | 9 | 82 |

| 2005 | 5 | 83 |

| 2004 | 5 | 47 |

| 2003 | 1 | 50 |

| 2002 | 3 | 36 |

| 2001 | 2 | 33 |

| 2000 | 2 | 29 |

| 1999 | 1 | 25 |

| 1998 | 0 | 14 |

| 1997 | 0 | 14 |

| 1996 | 0 | 14 |

| 1995 | 1 | 2 |

| 1994 | 1 | 0 |

| Total | 408 | 8922 |

| Rank | Country | Total Publications |

|---|---|---|

| 1 | United States | 156 |

| 2 | China | 71 |

| 3 | United Kingdom | 39 |

| 4 | Canada | 31 |

| 5 | Australia | 30 |

| 6 | South Korea | 23 |

| 7 | Hong Kong | 20 |

| 8 | Spain | 20 |

| 9 | Iran | 17 |

| 10 | Taiwan | 15 |

| Rank | Name of Institute | No. of Documents |

|---|---|---|

| 1. | National Taiwan University | 7 |

| 2. | University of Houston | 7 |

| 3. | University of Missouri | 7 |

| 4. | The University of Texas at Austin | 7 |

| 5. | MIT Sloan School of Management | 7 |

| 6. | Islamic Azad University | 7 |

| 7. | Universidad Carlos III de Madrid | 6 |

| 8. | University of Valencia | 6 |

| 9. | Korea University | 6 |

| 10. | Hong Kong University of Science and Technology | 6 |

| Rank | Title | NP |

|---|---|---|

| 1 | Contemporary Accounting Research | 23 |

| 2 | Journal Of Accounting And Economics | 20 |

| 3 | Journal Of Business Finance And Accounting | 18 |

| 4 | Accounting Review | 17 |

| 5 | Review Of Accounting Studies | 16 |

| 6 | European Accounting Review | 13 |

| 7 | Journal Of Accounting Research | 11 |

| 8 | Journal Of Applied Business Research | 11 |

| 9 | Accounting And Finance | 10 |

| 10 | Journal Of Accounting And Public Policy | 8 |

| 11 | Journal Of Accounting Auditing And Finance | 8 |

| 12 | Review Of Quantitative Finance And Accounting | 8 |

| 13 | Accounting Horizons | 7 |

| 14 | Journal Of International Accounting Auditing And Taxation | 6 |

| 15 | Asian Review Of Accounting | 5 |

| 16 | International Journal Of Accounting And Information Management | 5 |

| 17 | Revista Espanola De Financiacion Y Contabilidad | 5 |

| Rank | Authors | Affiliation | No. Papers | TC |

|---|---|---|---|---|

| 1. | Lobo, G.J. | C. T. Bauer College of Business, Department of Accountancy and Taxation, Houston, United States | 6 | 172 |

| 2. | Pae, J. | Korea University, Seoul, South Korea | 6 | 127 |

| 3. | Ahmed, A.S. | Texas AandM University, College Station, United States | 5 | 842 |

| 4. | Zhang, F. | The University of Queensland, Brisbane, Australia | 5 | 89 |

| Authors | Title | Year | Source Title | Cited by |

|---|---|---|---|---|

| FELTHAM G.A., OHLSON J.A. | Valuation and Clean Surplus Accounting for Operating and Financial Activities | 1995 | Contemporary Accounting Research | 853 |

| Barth M.E., Beaver W.H., Landsman W.R. | The relevance of the value relevance literature for financial accounting standard setting: Another view | 2001 | Journal of Accounting and Economics | 578 |

| Francis J.R., Wang D. | The joint effect of investor protection and big 4 audits on earnings quality around the world | 2008 | Contemporary Accounting Research | 394 |

| Khan M., Watts R.L. | Estimation and empirical properties of a firm-year measure of accounting conservatism | 2009 | Journal of Accounting and Economics | 383 |

| Penman S.H., Zhang X.-J. | Accounting conservatism, the quality of earnings, and stock returns | 2002 | Accounting Review | 334 |

| Ahmed A.S., Billings B.K., Morton R.M., Stanford-Harris M. | The role of accounting conservatism in mitigating bondholder-shareholder conflicts over dividend policy and in reducing debt costs | 2002 | Accounting Review | 315 |

| Zhang J. | The contracting benefits of accounting conservatism to lenders and borrowers | 2008 | Journal of Accounting and Economics | 299 |

| Ahmed A.S., Duellman S. | Accounting conservatism and board of director characteristics: An empirical analysis | 2007 | Journal of Accounting and Economics | 297 |

| Lafond R., Roychowdhury S. | Managerial ownership and accounting conservatism | 2008 | Journal of Accounting Research | 225 |

| Roychowdhury S., Watts R.L. | Asymmetric timeliness of earnings, market-to-book and conservatism in financial reporting | 2007 | Journal of Accounting and Economics | 220 |

| Krishnan G.V., Visvanathan G. | Does the SOX definition of an accounting expert matter? The association between Audit committee directors’ accounting expertise and accounting conservatism | 2008 | Contemporary Accounting Research | 212 |

| García Lara J.M., García Osma B., Penalva F. | Accounting conservatism and corporate governance | 2009 | Review of Accounting Studies | 174 |

| Wittenberg-Moerman R. | The role of information asymmetry and financial reporting quality in debt trading: Evidence from the secondary loan market | 2008 | Journal of Accounting and Economics | 151 |

| Kim J.-B., Zhang L. | Accounting Conservatism and Stock Price Crash Risk: Firm-level Evidence | 2016 | Contemporary Accounting Research | 148 |

| Nikolaev V.V. | Debt covenants and accounting conservatism | 2010 | Journal of Accounting Research | 145 |

| Dietrich J.R., Muller III K.A., Riedl E.J. | Asymmetric timeliness tests of accounting conservatism | 2007 | Review of Accounting Studies | 138 |

| Altamuro J., Beatty A. | How does internal control regulation affect financial reporting? | 2010 | Journal of Accounting and Economics | 135 |

| Ahmed A.S., Duellman S. | Managerial Overconfidence and Accounting Conservatism | 2013 | Journal of Accounting Research | 127 |

| Francis J.R., Martin X. | Acquisition profitability and timely loss recognition | 2010 | Journal of Accounting and Economics | 127 |

| Ramalingegowda S., Yu Y. | Institutional ownership and conservatism | 2012 | Journal of Accounting and Economics | 121 |

| Gigler F., Kanodia C., Sapra H., Venugopalan R. | Accounting conservatism and the efficiency of debt contracts | 2009 | Journal of Accounting Research | 115 |

| García Lara J.M., García Osma B., Penalva F. | Accounting conservatism and firm investment efficiency | 2016 | Journal of Accounting and Economics | 106 |

| Qiang X. | The effects of contracting, litigation, regulation, and tax costs on conditional and unconditional conservatism: Cross-sectional evidence at the firm level | 2007 | Accounting Review | 103 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bhutta, U.; Martins, J.N.; Mata, M.N.; Raza, A.; Dantas, R.M.; Correia, A.B.; Rafiq, M. Intellectual Structure and Evolution of Accounting Conservatism Research: Past Trends and Future Research Suggestions. Int. J. Financial Stud. 2021, 9, 35. https://doi.org/10.3390/ijfs9030035

Bhutta U, Martins JN, Mata MN, Raza A, Dantas RM, Correia AB, Rafiq M. Intellectual Structure and Evolution of Accounting Conservatism Research: Past Trends and Future Research Suggestions. International Journal of Financial Studies. 2021; 9(3):35. https://doi.org/10.3390/ijfs9030035

Chicago/Turabian StyleBhutta, Umair, Jéssica Nunes Martins, Mário Nuno Mata, Ali Raza, Rui Miguel Dantas, Anabela Batista Correia, and Muhammad Rafiq. 2021. "Intellectual Structure and Evolution of Accounting Conservatism Research: Past Trends and Future Research Suggestions" International Journal of Financial Studies 9, no. 3: 35. https://doi.org/10.3390/ijfs9030035

APA StyleBhutta, U., Martins, J. N., Mata, M. N., Raza, A., Dantas, R. M., Correia, A. B., & Rafiq, M. (2021). Intellectual Structure and Evolution of Accounting Conservatism Research: Past Trends and Future Research Suggestions. International Journal of Financial Studies, 9(3), 35. https://doi.org/10.3390/ijfs9030035