The Relation between Intraday Limit Order Book Depth and Spread

Abstract

:1. Introduction

2. Data and Methodology

2.1. Data

2.2. Methdology

2.2.1. Variable Definitions

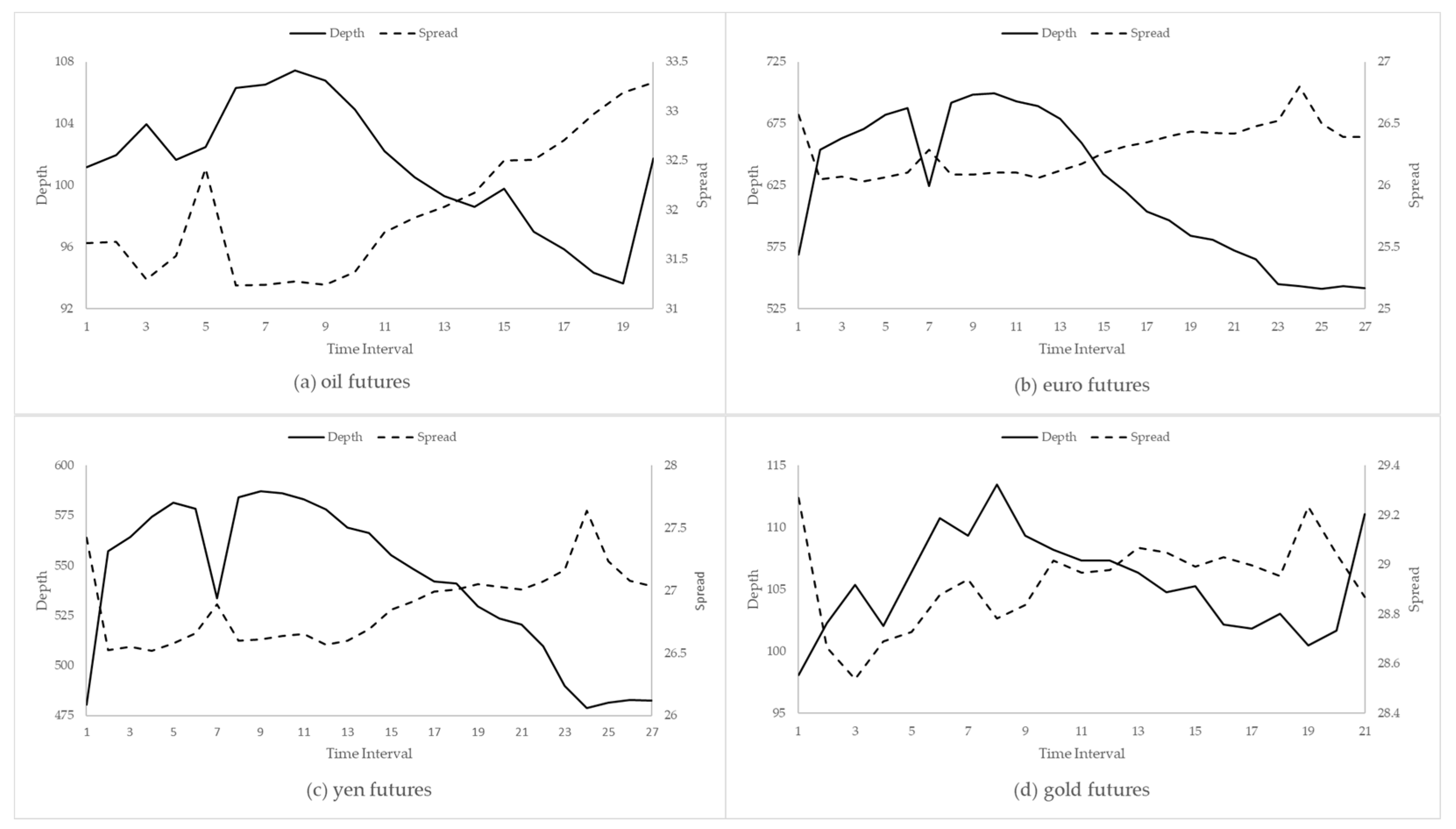

2.2.2. Intraday Behavior of Depth and Spread

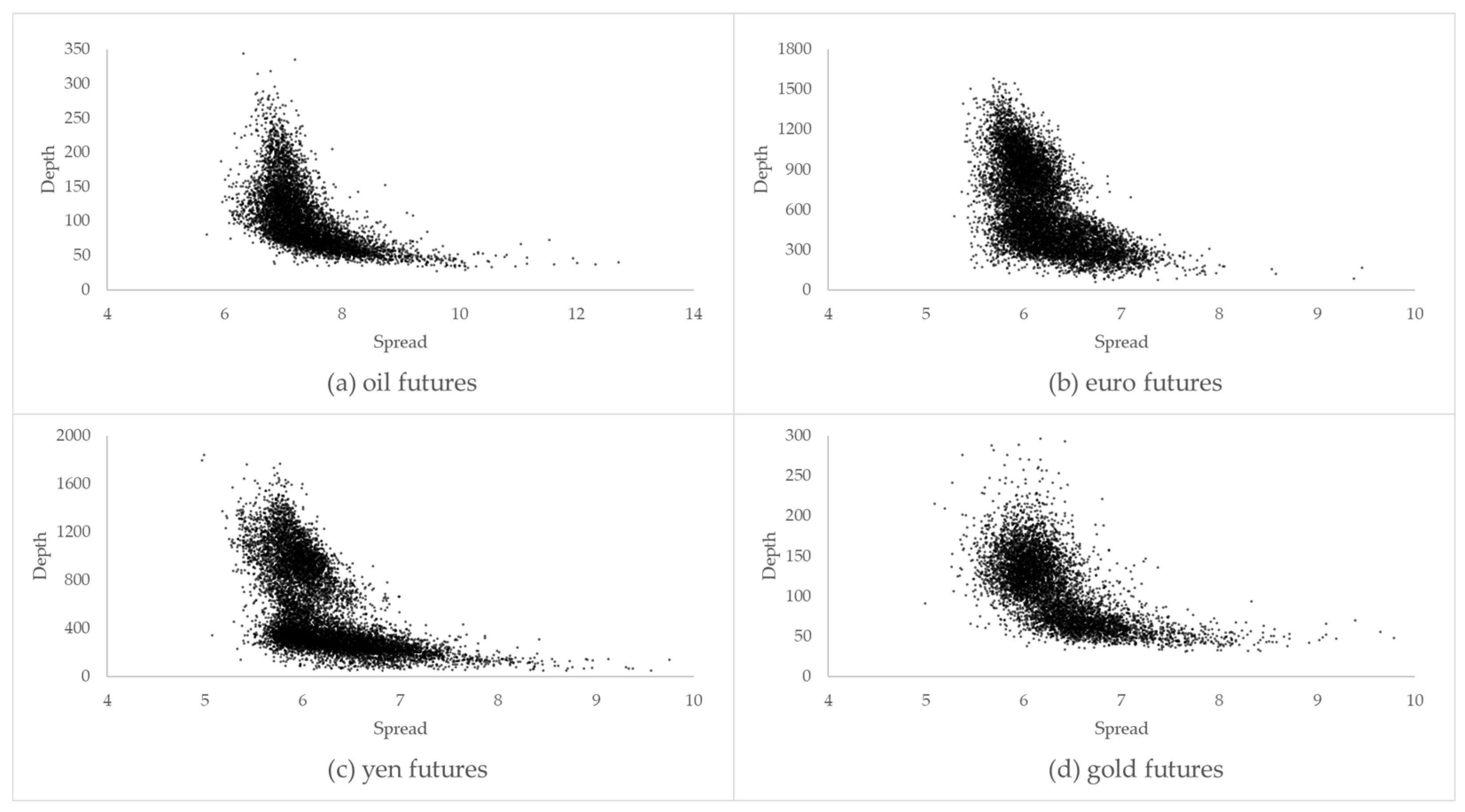

2.2.3. Relation between Depth and Spread

3. Results and Discussion

3.1. Summary Statistics

3.2. Intraday Depth and Spread Patterns

3.3. Relation between Depth and Spread

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | For ease of exposition, the light sweet crude oil (WTI) is referred to as “oil,” the euro/U.S. dollar total is referred to as the “euro,” and the yen/U.S. dollar futures is called the “yen.” |

| 2 | The date range for each contract is limited by the data provided to us by the CME Group. The end range of the data coincided with the period when the CME Group changed its data format from RLC to FIX/Fast format. |

| 3 | For example, there can be 30 depth updates in one second and only one depth update in another second. In order to sample the data at equal intervals, it is sampled every second. |

| 4 | To confirm that results are robust to the selection of the time interval, five-minute intervals are also employed. Similar results are obtained in the case of five-minute intervals and are available upon request. |

| 5 | The total spread is weighted by the percentage depth at each level for several reasons. Absence any weighting, the sum of absolute bid–ask spreads across each level becomes very noisy, especially in volatile and trending markets. In addition, the goal is to capture the size of the average difference between the bid and ask at different levels and this can be accomplished by measuring each spread as a percentage of the entire depth. |

| 6 | For ease of exposition, the total depth henceforth is referred to as “depth,” and the total spread is referred to as “spread.” |

| 7 |

References

- Ahn, Hee-Joon, and Yan-Leung Cheung. 1999. The intraday patterns of the spread and depth in a market without market makers: The stock exchange of Hong Kong. Pacific-Basin Finance Journal 7: 539–56. [Google Scholar] [CrossRef]

- Aidov, Alexandre, and Robert T. Daigler. 2015. Depth characteristics for the electronic futures limit order book. Journal of Futures Markets 35: 542–60. [Google Scholar] [CrossRef]

- Aitken, Michael, and Alex Frino. 1996. The determinants of market bid ask spreads on the Australian stock exchange: Cross-sectional analysis. Accounting & Finance 36: 51–63. [Google Scholar]

- Aitken, Michael, Niall Almeida, Frederick H. de B. Harris, and Thomas H. McInish. 2007. Liquidity supply in electronic markets. Journal of Financial Markets 10: 144–68. [Google Scholar] [CrossRef]

- Biais, Bruno, Pierre Hillion, and Chester Spatt. 1995. An empirical analysis of the limit order book and the order flow in the Paris bourse. The Journal of Finance 50: 1655–89. [Google Scholar] [CrossRef]

- Bouchaud, Jean-Philippe, Marc Mézard, and Marc Potters. 2002. Statistical properties of stock order books: Empirical results and models. Quantitative Finance 2: 251–56. [Google Scholar] [CrossRef]

- Brockman, Paul, and Dennis Y. Chung. 2000. An empirical investigation of trading on asymmetric information and heterogeneous prior beliefs. Journal of Empirical Finance 7: 417–54. [Google Scholar] [CrossRef]

- Cao, Charles, Oliver Hansch, and Xiaoxin Wang. 2009. The information content of an open limit-order book. Journal of Futures Markets 29: 16–41. [Google Scholar] [CrossRef]

- Chan, Kalok, Y. Peter Chung, and Herb Johnson. 1995. The intraday behavior of bid-ask spreads for NYSE stocks and CBOE options. The Journal of Financial and Quantitative Analysis 30: 329–46. [Google Scholar] [CrossRef]

- Chiu, Junmao, Huimin Chung, and George H. K. Wang. 2014. Intraday liquidity provision by trader types in a limit order market: Evidence from Taiwan index futures. Journal of Futures Markets 34: 145–72. [Google Scholar] [CrossRef]

- Ding, David K. 1999. The determinants of bid-ask spreads in the foreign exchange futures market: A microstructure analysis. Journal of Futures Markets 19: 307–24. [Google Scholar] [CrossRef]

- Frino, Alex, Andrew Lepone, and Grant Wearin. 2008. Intraday behavior of market depth in a competitive dealer market: A note. Journal of Futures Markets 28: 294–307. [Google Scholar] [CrossRef]

- Gwilym, Owain Ap, Mike Buckle, and Stephen H. Thomas. 1997. The intraday behavior of bid-ask spreads, returns, and volatility for FTSE-100 stock index options. The Journal of Derivatives 4: 20–32. [Google Scholar] [CrossRef]

- Hansen, Lars Peter. 1982. Large sample properties of generalized method of moments estimators. Econometrica 50: 1029–54. [Google Scholar] [CrossRef]

- Harris, Lawrence E. 1991. Liquidity, trading rules, and electronic trading systems. In Monograph Series in Finance and Economics. New York: New York University Salomon Center. [Google Scholar]

- Harris, Lawrence E. 1994. Minimum price variations, discrete bid-ask spreads, and quotation sizes. The Review of Financial Studies 7: 149–78. [Google Scholar] [CrossRef] [Green Version]

- Hautsch, Nikolaus, and Ruihong Huang. 2012. The market impact of a limit order. Journal of Economic Dynamics and Control 36: 501–22. [Google Scholar] [CrossRef] [Green Version]

- Lee, Charles M. C., Belinda Mucklow, and Mark J. Ready. 1993. Spreads, depths, and the impact of earnings information: An intraday analysis. The Review of Financial Studies 6: 345–74. [Google Scholar] [CrossRef]

- Newey, Whitney K., and Kenneth D. West. 1987. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55: 703–8. [Google Scholar] [CrossRef]

- Parlour, Christine A. 1998. Price dynamics in limit order markets. The Review of Financial Studies 11: 789–816. [Google Scholar] [CrossRef]

- Sheikh, Aamir M., and Ehud I. Ronn. 1994. A characterization of the daily and intraday behavior of returns on options. The Journal of Finance 49: 557–79. [Google Scholar] [CrossRef]

- Vo, Minh T. 2007. Limit orders and the intraday behavior of market liquidity: Evidence from the Toronto stock exchange. Global Finance Journal 17: 379–96. [Google Scholar] [CrossRef] [Green Version]

- Yura, Yoshihiro, Hideki Takayasu, Didier Sornette, and Misako Takayasu. 2014. Financial brownian particle in the layered order-book fluid and fluctuation-dissipation relations. Physical Review Letters 112: 1–5. [Google Scholar] [CrossRef] [PubMed] [Green Version]

{kind=link}

{kind=link}

| Futures Contract | Symbol | Hours | Date |

|---|---|---|---|

| Oil | CL | 08:00–13:30 | 01/02/2008–04/17/2009 |

| Euro | 6E | 07:20–14:00 | 01/03/2008–10/02/2009 |

| Yen | 6J | 07:20–14:00 | 01/03/2008–10/02/2009 |

| Gold | GC | 07:20–12:30 | 01/02/2008–04/17/2009 |

| Panel A: Oil | Mean | Median | Stan. Dev. | Skew. | Kurt. | 5th | 95th |

| Depth | 101.83 | 92.79 | 42.33 | 0.80 | 0.08 | 48.53 | 185.91 |

| Spread | 7.40 | 7.26 | 0.68 | 2.68 | 20.33 | 6.63 | 8.58 |

| Volume | 17,894.34 | 13,882.00 | 13,067.82 | 2.52 | 9.08 | 6265.00 | 45,489.00 |

| Level | 87.45 | 95.04 | 33.90 | −0.12 | −1.42 | 39.49 | 136.62 |

| Volatility | 0.18 | 0.15 | 0.13 | 3.40 | 18.50 | 0.06 | 0.40 |

| Panel B: Euro | Mean | Median | Stan. Dev. | Skew. | Kurt. | 5th | 95th |

| Depth | 640.25 | 601.37 | 298.48 | 0.21 | −1.17 | 226.45 | 1135.22 |

| Spread | 6.19 | 6.11 | 0.36 | 0.96 | 0.77 | 5.74 | 6.91 |

| Volume | 9123.99 | 7163.00 | 7328.55 | 2.51 | 11.59 | 2084.00 | 22,682.00 |

| Level | 14.19 | 14.18 | 0.99 | 0.05 | −1.12 | 12.67 | 15.72 |

| Volatility | 0.01 | 0.01 | 0.01 | 6.81 | 70.01 | 0.00 | 0.02 |

| Panel C: Yen | Mean | Median | Stan. Dev. | Skew. | Kurt. | 5th | 95th |

| Depth | 549.92 | 419.56 | 336.86 | 0.67 | −0.84 | 161.77 | 1188.86 |

| Spread | 6.20 | 6.10 | 0.45 | 1.23 | 2.20 | 5.65 | 7.07 |

| Volume | 4599.84 | 3546.00 | 3718.58 | 2.32 | 10.00 | 968.00 | 11,722.00 |

| Level | 0.01 | 0.01 | 0.00 | 0.04 | −1.13 | 0.01 | 0.01 |

| Volatility | 0.00 | 0.00 | 0.00 | 3.44 | 21.29 | 0.00 | 0.00 |

| Panel D: Gold | Mean | Median | Stan. Dev. | Skew. | Kurt. | 5th | 95th |

| Depth | 105.40 | 104.48 | 41.22 | 0.30 | −0.71 | 46.50 | 175.19 |

| Spread | 6.36 | 6.25 | 0.49 | 1.52 | 4.23 | 5.78 | 7.29 |

| Volume | 7084.21 | 5789.00 | 5076.28 | 2.58 | 12.15 | 1981.00 | 16,399.00 |

| Level | 88.21 | 89.25 | 6.28 | −0.72 | 0.12 | 74.72 | 97.15 |

| Volatility | 0.10 | 0.08 | 0.09 | 5.44 | 44.69 | 0.03 | 0.22 |

| Panel A: Model 1 | Oil | Euro | Yen | Gold |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 102.107 (0.0000) | 648.640 (0.0000) | 558.853 (0.0000) | 105.786 (0.0000) |

| Time1 | −0.624 (0.3990) | −68.727 (0.0018) | −75.864 (0.0020) | −7.877 (0.0064) |

| Time2 | 0.291 (0.4508) | 14.752 (0.1730) | 1.399 (0.4697) | −3.416 (0.1020) |

| TimeN−1 | −8.833 (0.0038) | −95.244 (0.0005) | −78.138 (0.0018) | −4.256 (0.0572) |

| TimeN | 0.893 (0.3494) | −101.56 (0.0004) | −81.241 (0.0016) | 6.460 (0.0247) |

| Panel B: Model 2 | Oil | Euro | Yen | Gold |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 7.388 (0.0000) | 6.196 (0.0000) | 6.208 (0.0000) | 6.368 (0.0000) |

| Time1 | −0.078 (0.0376) | −0.103 (0.0008) | −0.041 (0.0659) | −0.063 (0.0391) |

| Time2 | −0.063 (0.0610) | −0.116 (0.0004) | −0.084 (0.0051) | −0.084 (0.0105) |

| TimeN−1 | 0.255 (0.0013) | 0.053 (0.0167) | 0.032 (0.1102) | 0.030 (0.1952) |

| TimeN | 0.154 (0.0106) | 0.011 (0.2843) | 0.000 (0.5000) | −0.083 (0.0250) |

| Panel A: Oil | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 10.241 (0.0000) | 16.263 (0.0000) | 22.134 (0.0000) | 27.226 (0.0000) | 30.919 (0.0000) |

| Time1 | −0.267 (0.0958) | −0.077 (0.8274) | −0.161 (0.7813) | −0.497 (0.5272) | −0.896 (0.3104) |

| Time2 | −0.291 (0.0619) | 0.046 (0.8932) | −0.003 (0.9964) | −0.112 (0.8872) | −0.813 (0.3466) |

| TimeN−1 | −0.004 (0.9794) | −1.407 (0.0000) | −2.281 (0.0000) | −2.353 (0.0009) | −1.730 (0.0300) |

| TimeN | 2.933 (0.0000) | 2.726 (0.0000) | 2.464 (0.0004) | 1.959 (0.0270) | 1.399 (0.1486) |

| Panel B: Euro | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 43.819 (0.0000) | 114.447 (0.0000) | 164.574 (0.0000) | 173.778 (0.0000) | 162.100 (0.0000) |

| Time1 | −0.565 (0.6078) | −9.861 (0.0005) | −20.076 (0.0000) | −23.293 (0.0000) | −27.057 (0.0000) |

| Time2 | 4.494 (0.0001) | 5.745 (0.0574) | 2.725 (0.4879) | 2.512 (0.5078) | −5.780 (0.0629) |

| TimeN−1 | −6.285 (0.0000) | −19.839 (0.0000) | −25.448 (0.0000) | −26.164 (0.0000) | −17.563 (0.0000) |

| TimeN | −4.808 (0.0000) | −19.359 (0.0000) | −27.107 (0.0000) | −29.328 (0.0000) | −23.901 (0.0000) |

| Panel C: Yen | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 40.053 (0.0000) | 104.107 (0.0000) | 148.393 (0.0000) | 146.843 (0.0000) | 124.395 (0.0000) |

| Time1 | −3.143 (0.0107) | −14.765 (0.0000) | −23.336 (0.0000) | −23.237 (0.0000) | −21.084 (0.0000) |

| Time2 | 2.059 (0.1410) | 1.072 (0.7709) | −0.772 (0.8714) | −0.981 (0.8191) | −3.698 (0.2664) |

| TimeN−1 | −4.889 (0.0000) | −14.737 (0.0001) | −21.841 (0.0000) | −21.024 (0.0000) | −12.972 (0.0000) |

| TimeN | −3.898 (0.0010) | −16.429 (0.0000) | −23.344 (0.0000) | −22.754 (0.0000) | −16.186 (0.0000) |

| Panel D: Gold | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 13.098 (0.0000) | 20.717 (0.0000) | 23.838 (0.0000) | 25.166 (0.0000) | 27.292 (0.0000) |

| Time1 | 1.243 (0.0001) | −0.854 (0.0842) | −2.081 (0.0001) | −2.676 (0.0000) | −3.363 (0.0000) |

| Time2 | 0.152 (0.5765) | −0.468 (0.3274) | −0.930 (0.0892) | −0.774 (0.1871) | −1.048 (0.1040) |

| TimeN−1 | 0.073 (0.8305) | −0.631 (0.2488) | −0.690 (0.2817) | −0.751 (0.2467) | −0.387 (0.5680) |

| TimeN | 2.750 (0.0000) | 2.139 (0.0018) | 1.743 (0.0225) | 1.687 (0.0303) | 1.058 (0.2320) |

| Panel A: Oil | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 2.191 (0.0000) | 4.365 (0.0000) | 6.417 (0.0000) | 8.443 (0.0000) | 10.461 (0.0000) |

| Time1 | −0.032 (0.2474) | −0.046 (0.2148) | −0.057 (0.1669) | −0.064 (0.1398) | −0.069 (0.1275) |

| Time2 | −0.024 (0.3859) | −0.042 (0.2579) | −0.053 (0.1952) | −0.060 (0.1616) | −0.066 (0.1414) |

| TimeN−1 | 0.157 (0.0000) | 0.250 (0.0000) | 0.283 (0.0000) | 0.301 (0.0000) | 0.320 (0.0000) |

| TimeN | 0.127 (0.0002) | 0.223 (0.0000) | 0.267 (0.0000) | 0.297 (0.0000) | 0.325 (0.0000) |

| Panel B: Euro | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 1.251 (0.0000) | 3.254 (0.0000) | 5.255 (0.0000) | 7.256 (0.0000) | 9.257 (0.0000) |

| Time1 | 0.030 (0.0026) | 0.048 (0.0001) | 0.059 (0.0000) | 0.071 (0.0000) | 0.085 (0.0000) |

| Time2 | −0.042 (0.0000) | −0.044 (0.0000) | −0.044 (0.0000) | −0.045 (0.0000) | −0.047 (0.0000) |

| TimeN−1 | 0.023 (0.0104) | 0.023 (0.0136) | 0.022 (0.0170) | 0.022 (0.0217) | 0.022 (0.0249) |

| TimeN | 0.023 (0.0118) | 0.024 (0.0131) | 0.023 (0.0161) | 0.023 (0.0195) | 0.023 (0.0220) |

| Panel C: Yen | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 1.362 (0.0000) | 3.368 (0.0000) | 5.372 (0.0000) | 7.376 (0.0000) | 9.382 (0.0000) |

| Time1 | 0.051 (0.0033) | 0.085 (0.0004) | 0.111 (0.0002) | 0.141 (0.0002) | 0.179 (0.0001) |

| Time2 | −0.055 (0.0000) | −0.059 (0.0000) | −0.062 (0.0000) | −0.066 (0.0000) | −0.072 (0.0000) |

| TimeN−1 | 0.036 (0.0159) | 0.037 (0.0262) | 0.037 (0.0416) | 0.038 (0.0561) | 0.046 (0.0489) |

| TimeN | 0.030 (0.0642) | 0.033 (0.0854) | 0.034 (0.1197) | 0.036 (0.1498) | 0.044 (0.1340) |

| Panel D: Gold | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 1.714 (0.0000) | 3.787 (0.0000) | 5.807 (0.0000) | 7.817 (0.0000) | 9.825 (0.0000) |

| Time1 | −0.002 (0.9345) | 0.047 (0.1098) | 0.075 (0.0264) | 0.098 (0.0081) | 0.116 (0.0035) |

| Time2 | −0.060 (0.0017) | −0.057 (0.0267) | −0.056 (0.0484) | −0.056 (0.0630) | −0.056 (0.0691) |

| TimeN−1 | 0.024 (0.3022) | 0.030 (0.3309) | 0.036 (0.3064) | 0.042 (0.2777) | 0.052 (0.2376) |

| TimeN | −0.034 (0.1330) | −0.018 (0.5652) | −0.008 (0.8237) | 0.001 (0.9856) | 0.007 (0.8744) |

| Panel A: Model 3 | Oil | Euro | Yen | Gold |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 361.089 (0.0000) | 3776.38 (0.0000) | 3312.76 (0.0000) | 444.490 (0.0000) |

| Spread | −35.054 (0.0000) | −504.79 (0.0000) | −443.61 (0.0000) | −53.185 (0.0000) |

| Time1 | −3.341 (0.0078) | −120.84 (0.0000) | −93.864 (0.0001) | −11.230 (0.0002) |

| Time2 | −1.934 (0.1671) | −43.666 (0.0039) | −35.821 (0.0164) | −7.865 (0.0012) |

| TimeN−1 | 0.109 (0.4732) | −68.329 (0.0004) | −64.006 (0.0009) | −2.676 (0.1027) |

| TimeN | 6.283 (0.0053) | −95.921 (0.0000) | −81.231 (0.0003) | 2.049 (0.1918) |

| Panel B: Model 4 | Oil | Euro | Yen | Gold |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 349.961 (0.0000) | −220.630 (0.0797) | 4599.47 (0.0000) | 329.926 (0.0000) |

| Spread | −35.647 (0.0000) | −245.44 (0.0000) | −178.15 (0.0000) | −46.794 (0.0000) |

| Time1 | −3.384 (0.0528) | −96.322 (0.0000) | −87.120 (0.0000) | −14.187 (0.0000) |

| Time2 | −2.430 (0.1046) | −26.633 (0.0091) | −32.173 (0.0075) | −9.885 (0.0001) |

| TimeN−1 | 0.445 (0.3966) | −72.275 (0.0000) | −57.626 (0.0001) | 0.223 (0.4497) |

| TimeN | 2.526 (0.1672) | −87.405 (0.0000) | −68.193 (0.0000) | 5.360 (0.0153) |

| Volume | 0.000 (0.0007) | 0.004 (0.0000) | 0.012 (0.0000) | 0.001 (0.0000) |

| Level | 0.240 (0.0000) | 154.104 (0.0000) | −291,173 (0.0000) | 0.762 (0.0001) |

| Volatility | −77.901 (0.0000) | −4333.8 (0.0003) | −9.26E6 (0.0000) | −29.177 (0.0310) |

| Panel A: Oil | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 16.054 (0.0000) | 41.965 (0.0000) | 76.297 (0.0000) | 112.825 (0.0000) | 139.610 (0.0000) |

| Spread | −4.105 (0.0000) | −6.577 (0.0000) | −9.305 (0.0000) | −10.953 (0.0000) | −10.933 (0.0000) |

| Time1 | −0.529 (0.0000) | −0.561 (0.0122) | −0.886 (0.0202) | −1.379 (0.0114) | −1.860 (0.0029) |

| Time2 | −0.430 (0.0000) | −0.303 (0.1641) | −0.600 (0.1191) | −0.905 (0.1003) | −1.583 (0.0086) |

| TimeN−1 | 0.332 (0.0109) | −0.192 (0.4158) | −0.102 (0.7874) | 0.544 (0.2884) | 0.399 (0.4987) |

| TimeN | 1.365 (0.0000) | 1.063 (0.0199) | 1.384 (0.0452) | 1.593 (0.0797) | 0.522 (0.6034) |

| Volume | 0.000 (0.0000) | 0.000 (0.0000) | 0.000 (0.0000) | 0.000 (0.0000) | 0.000 (0.0000) |

| Level | 0.022 (0.0000) | 0.018 (0.0000) | 0.048 (0.0000) | 0.068 (0.0000) | 0.068 (0.0000) |

| Volatility | −0.737 (0.3086) | −4.380 (0.0025) | −8.352 (0.0010) | −13.432 (0.0003) | −19.321 (0.0000) |

| Panel B: Euro | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | −78.185 (0.0000) | 20.844 (0.6749) | 277.847 (0.0156) | 422.225 (0.0052) | 462.937 (0.0037) |

| Spread | −42.234 (0.0000) | −113.05 (0.0000) | −140.95 (0.0000) | −117.81 (0.0000) | −87.411 (0.0000) |

| Time1 | −0.339 (0.6239) | −5.649 (0.0030) | −13.035 (0.0000) | −16.452 (0.0000) | −19.877 (0.0000) |

| Time2 | 0.379 (0.6045) | −2.426 (0.1993) | −7.351 (0.0027) | −7.138 (0.0044) | −10.660 (0.0000) |

| TimeN−1 | −3.461 (0.0000) | −14.733 (0.0000) | −19.369 (0.0000) | −20.286 (0.0000) | −17.791 (0.0000) |

| TimeN | −1.557 (0.0420) | −13.656 (0.0000) | −20.338 (0.0000) | −22.638 (0.0000) | −20.466 (0.0000) |

| Volume | 0.001 (0.0000) | 0.001 (0.0000) | 0.001 (0.0000) | 0.001 (0.0000) | 0.001 (0.0000) |

| Level | 12.101 (0.0000) | 32.280 (0.0000) | 43.969 (0.0000) | 42.431 (0.0000) | 35.335 (0.0000) |

| Volatility | −219.13 (0.0000) | −541.50 (0.0000) | −764.98 (0.0000) | −768.68 (0.0000) | −691.65 (0.0000) |

| Panel C: Yen | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 298.940 (0.0000) | 972.961 (0.0000) | 1365.99 (0.0000) | 1257.23 (0.0000) | 1001.04 (0.0000) |

| Spread | −20.241 (0.0000) | −46.512 (0.0000) | −54.679 (0.0000) | −36.748 (0.0000) | −22.802 (0.0000) |

| Time1 | −2.740 (0.0013) | −12.004 (0.0000) | −18.070 (0.0000) | −19.040 (0.0000) | −19.310 (0.0000) |

| Time2 | −1.174 (0.2098) | −6.251 (0.0081) | −9.162 (0.0039) | −8.256 (0.0047) | −9.015 (0.0001) |

| TimeN−1 | −2.398 (0.0017) | −9.176 (0.0008) | −15.621 (0.0000) | −15.546 (0.0000) | −13.810 (0.0000) |

| TimeN | −1.668 (0.0376) | −11.416 (0.0000) | −17.830 (0.0000) | −17.816 (0.0000) | −15.656 (0.0000) |

| Volume | 0.001 (0.0000) | 0.003 (0.0000) | 0.003 (0.0000) | 0.003 (0.0000) | 0.003 (0.0000) |

| Level | −23,039 (0.0000) | −70,750 (0.0000) | −91,600 (0.0000) | −83,277 (0.0000) | −65,712 (0.0000) |

| Volatility | −931,044 (0.0000) | −2.12E6 (0.0000) | −2.65E6 (0.0000) | −2.46E6 (0.0000) | −1.95E6 (0.0000) |

| Panel D: Gold | Level 1 | Level 2 | Level 3 | Level 4 | Level 5 |

| Variables | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) | Coeff. (p-Val.) |

| Intercept | 21.360 (0.0000) | 57.304 (0.0000) | 85.706 (0.0000) | 99.060 (0.0000) | 95.542 (0.0000) |

| Spread | −7.952 (0.0000) | −11.758 (0.0000) | −11.906 (0.0000) | −10.941 (0.0000) | −9.539 (0.0000) |

| Time1 | 0.493 (0.0337) | −1.250 (0.0007) | −2.365 (0.0000) | −2.748 (0.0000) | −2.934 (0.0000) |

| Time2 | −0.863 (0.0000) | −1.833 (0.0000) | −2.462 (0.0000) | −2.221 (0.0000) | −1.964 (0.0001) |

| TimeN−1 | 0.940 (0.0005) | 0.593 (0.1537) | 0.822 (0.1006) | 0.762 (0.1472) | 1.121 (0.0471) |

| TimeN | 3.118 (0.0000) | 2.743 (0.0000) | 2.659 (0.0000) | 2.680 (0.0000) | 2.855 (0.0002) |

| Volume | 0.000 (0.0000) | 0.000 (0.0000) | 0.000 (0.0000) | 0.000 (0.0000) | 0.000 (0.0000) |

| Level | 0.042 (0.0005) | 0.066 (0.0049) | 0.052 (0.0794) | 0.102 (0.0022) | 0.253 (0.0000) |

| Volatility | −0.966 (0.4134) | −2.312 (0.3125) | −2.905 (0.2972) | −2.219 (0.4804) | −5.678 (0.1209) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aidov, A.; Lobanova, O. The Relation between Intraday Limit Order Book Depth and Spread. Int. J. Financial Stud. 2021, 9, 60. https://doi.org/10.3390/ijfs9040060

Aidov A, Lobanova O. The Relation between Intraday Limit Order Book Depth and Spread. International Journal of Financial Studies. 2021; 9(4):60. https://doi.org/10.3390/ijfs9040060

Chicago/Turabian StyleAidov, Alexandre, and Olesya Lobanova. 2021. "The Relation between Intraday Limit Order Book Depth and Spread" International Journal of Financial Studies 9, no. 4: 60. https://doi.org/10.3390/ijfs9040060

APA StyleAidov, A., & Lobanova, O. (2021). The Relation between Intraday Limit Order Book Depth and Spread. International Journal of Financial Studies, 9(4), 60. https://doi.org/10.3390/ijfs9040060