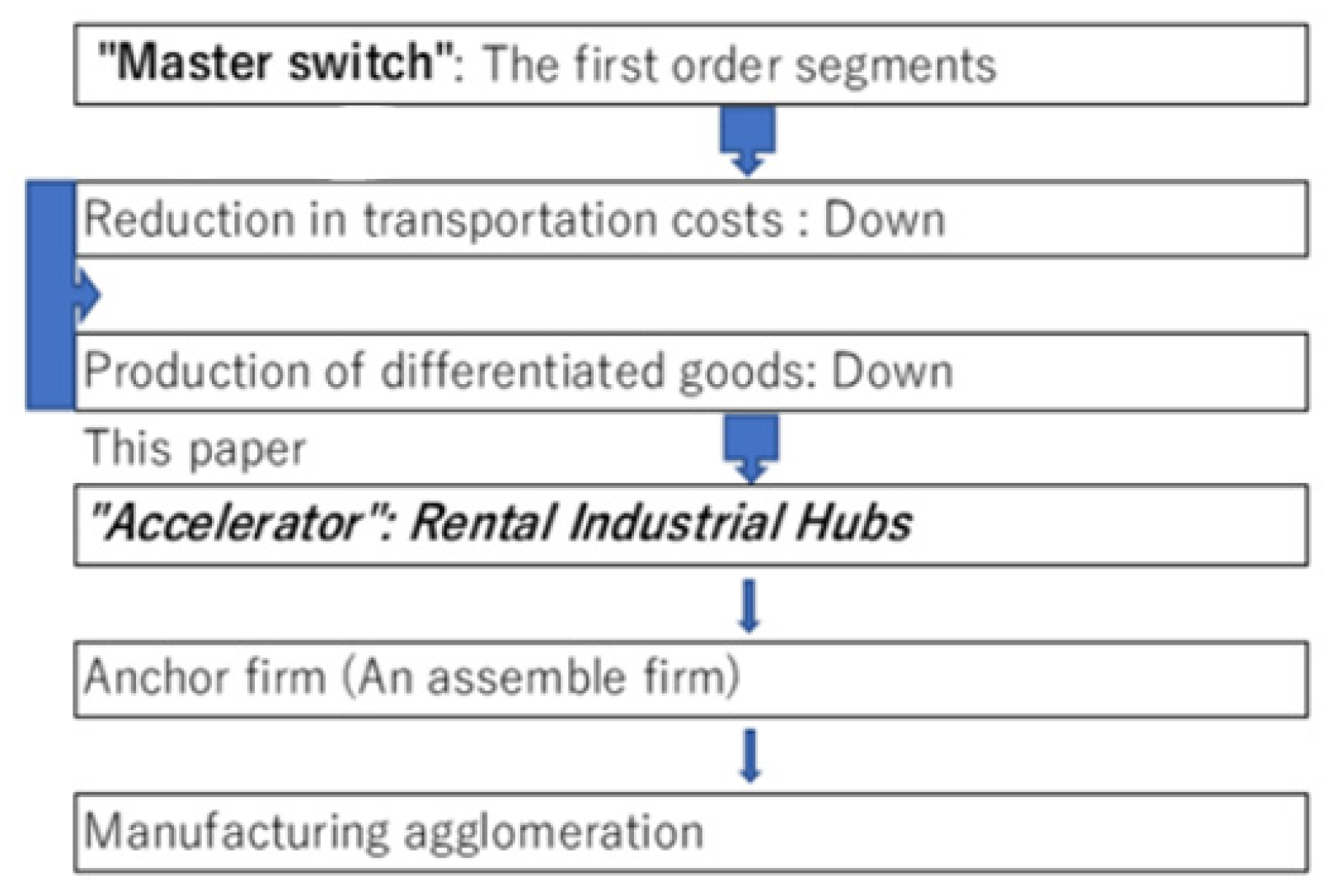

Accelerator for Agglomeration in Sequencing Economics: “Leased” Industrial Zones

Abstract

:1. Introduction

2. Chronology of the Chinese Industrial Agglomeration Policy

- (1)

- Establishment of “Special Economic Zones”: the start of industrial agglomeration policy (1978–1984) (see Table 1).

- (2)

- The beginning of industrial policy (1984–1992) (see Table 1).

- (3)

- The coexistence of industrial agglomeration policy and industrial policy (1992–1997) (see Table 2).

- (4)

- Industrial agglomeration policy with an emphasis on international competitiveness of enterprises (1997–2004) (see Table 2).

- (5)

- Scientific View of Development after the turning point (2004–2010) (see Table 3).

- (6)

- “Strategic emerging industries” as an industrial policy to escape from the middle-income-country trap (2010–2013) (see Table 3).

- (7)

- Industrial agglomeration policy via “pilot free trade zones” (2013–2022) (see Table 3).

3. The Role of Economic Development Zones as Industrial Zones

4. Statistical Analyses of Industrial Agglomeration Policy

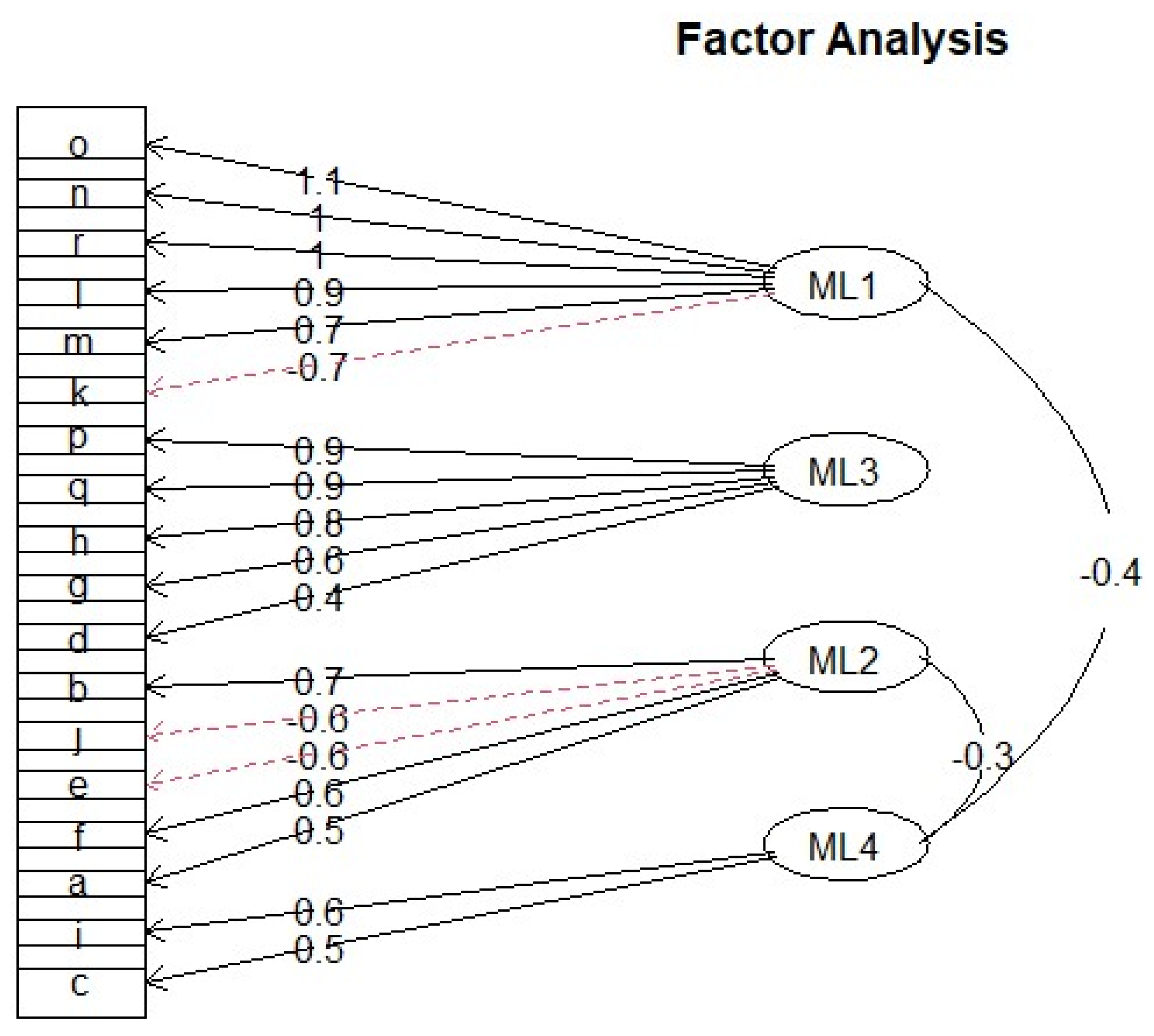

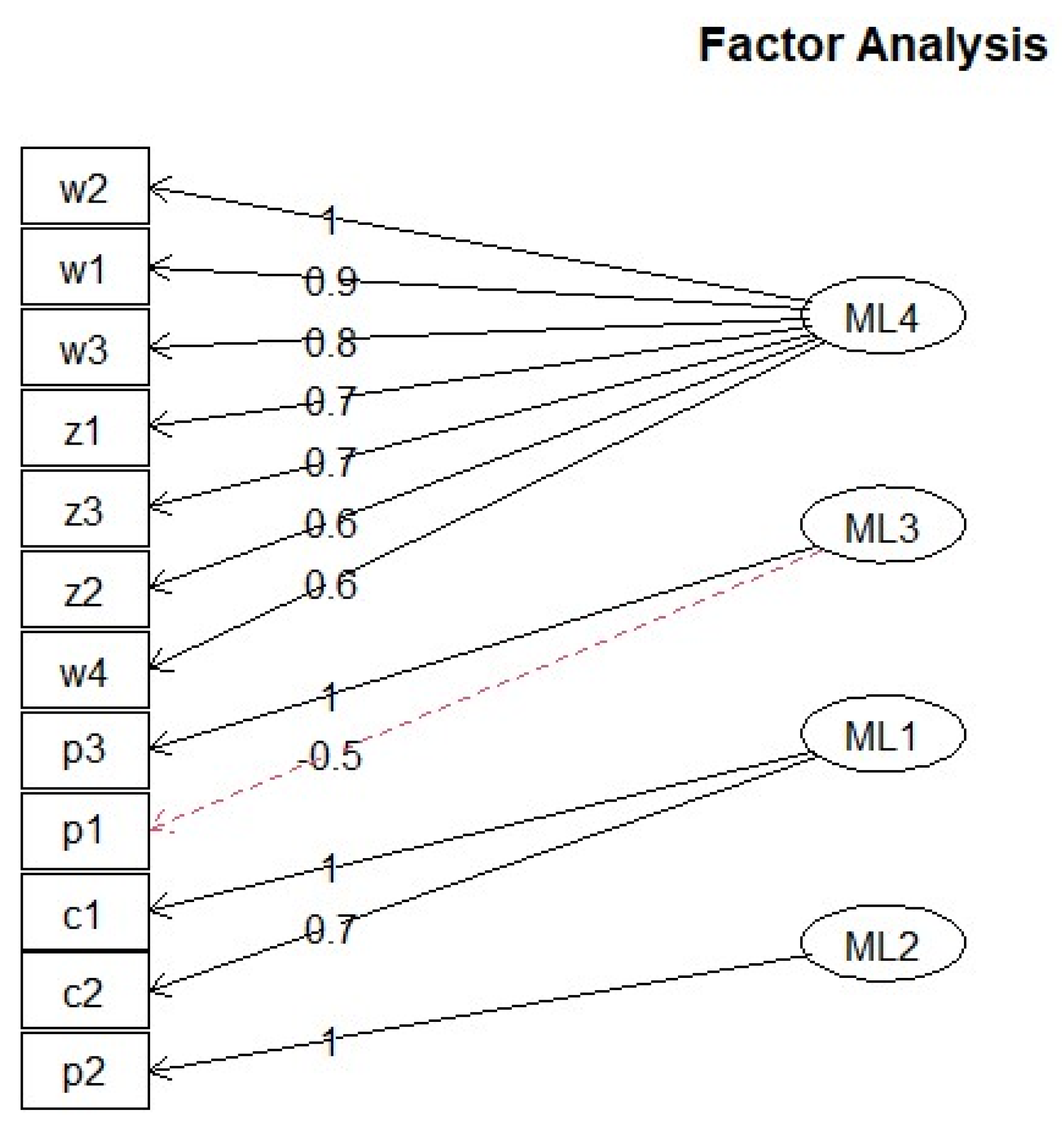

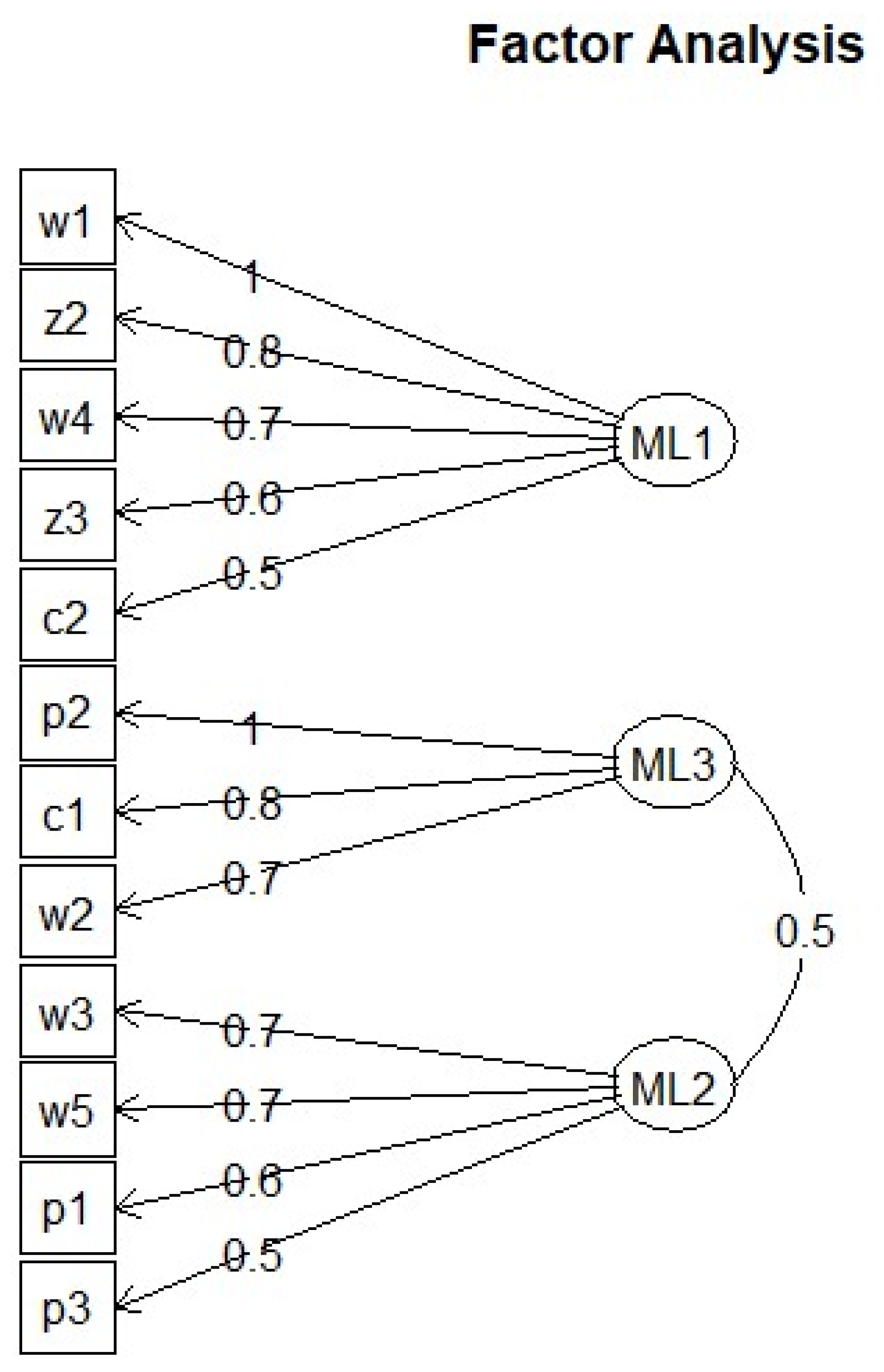

5. Factor Analysis

- (1)

- FDI-led agglomeration as an incentive for foreign direct investment

- (2)

- Accelerators of agglomeration policies

6. Summary and Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| r | y | g | i | x | m | f | F22 | a |

|---|---|---|---|---|---|---|---|---|

| 1987 | 10.9 | 13.7 | 39.7 | 34.9 | 4.3 | 23 | 23 | 4.5 |

| 1988 | 11.3 | 14.5 | 39.6 | 18.2 | 27.4 | 32 | 32 | 39.1 |

| 1989 | 4.3 | 3.8 | 36.8 | 5.3 | 5.3 | 34 | 34 | 6.3 |

| 1990 | 3.9 | 3.2 | 35.2 | 19.2 | −13.3 | 35 | 35 | 2.9 |

| 1991 | 9.3 | 13.3 | 34.7 | 14.4 | 18.5 | 44 | 44 | 25.7 |

| 1992 | 14.2 | 21.7 | 36.2 | 18.1 | 28.3 | 110 | 110 | 150 |

| 1993 | 13.5 | 20.7 | 43.4 | 8.8 | 34.1 | 275 | 275 | 150 |

| 1994 | 11.8 | 17.4 | 40 | 35.6 | 10.4 | 337 | 337 | 22.5 |

| 1995 | 10.2 | 13.6 | 41.2 | 24.9 | 15.5 | 375 | 375 | 11.3 |

| 1996 | 9.7 | 12.3 | 39.6 | 1.5 | 5.1 | 416 | 416 | 10.9 |

| 1997 | 9 | 11.1 | 39.8 | 10 | 15.5 | 417 | 417 | 0.2 |

| 1998 | 7.8 | 8.9 | 37.7 | 3.3 | 0.5 | 454 | 454 | 8.9 |

| 1999 | 7.1 | 8.1 | 37.4 | 2.1 | 6.1 | 403 | 403 | −11.2 |

| 2000 | 8 | 9.4 | 36.3 | 1.9 | 27.9 | 407 | 407 | 1 |

| 2001 | 7.5 | 8.4 | 38.5 | 1.5 | 6.8 | 468 | 468 | 15 |

| 2002 | 9.1 | 9.8 | 37.9 | 22.4 | 21.3 | 527 | 527 | 12.6 |

| 2003 | 10 | 12.7 | 41.2 | 34.6 | 39.8 | 535 | 535 | 1.5 |

| 2004 | 10.1 | 11.1 | 43.3 | 35.4 | 35.8 | 606 | 606 | 13.3 |

| 2005 | 10.4 | 11.7 | 43.6 | 28.5 | 17.6 | 724 | 724 | 19.5 |

| 2006 | 11.6 | 13 | 43.6 | 27.2 | 19.7 | 727 | 727 | 0.4 |

| 2007 | 13 | 14.7 | 41.7 | 25.8 | 20.3 | 835 | 835 | 14.9 |

| 2008 | 9.6 | 9.8 | 42.5 | 17.6 | 18.7 | 1083 | 1083 | 29.7 |

| 2009 | 8.7 | 9.5 | 45.8 | −16.1 | −11.2 | 940 | 940 | −13.2 |

| 2010 | 10.4 | 12.3 | 0 | 31.4 | 39.1 | 1147 | 1147 | 22 |

| 2011 | 9.3 | 10.3 | 0 | 20.4 | 25.1 | 1239 | 1239 | 8 |

| 2012 | 7.9 | 8.4 | 0 | 9.2 | 5.2 | 1210 | 1210 | −2.3 |

| 2013 | 7.8 | 8 | 0 | 8.9 | 7.7 | 1239 | 1239 | 2.4 |

| 2014 | 7.3 | 7.4 | 0 | 4.4 | 1.1 | 1285 | 1285 | 3.7 |

| 2015 | 6.9 | 6.2 | 0 | −4.5 | −13.4 | 1355 | 1355 | 5.4 |

| 2016 | 6.7 | 6.3 | 0 | −7.2 | −4.2 | 1337 | 1337 | −1.3 |

| 2017 | 6.8 | 5.9 | 0 | 11.4 | 16 | 1363 | 1363 | 1.9 |

| 2018 | 6.6 | 5.8 | 0 | 9.1 | 16.2 | 1349 | 1349 | −1 |

| w1 | w2 | w3 | w4 | w5 | z1 | z2 | z3 | p1 | p2 | p3 | c1 | c2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 636 | 984 | 2000 | 891 | 1782 | 103 | 3.09 | 20.5 | 0.075 | 0.76 | 0.48 | 1855 | 20,000 |

| 2 | 506 | 822 | 1268 | 1037 | 2185 | 96 | 2.79 | 22 | 0.095 | 0.68 | 0.46 | 804 | 13,915 |

| 3 | 669 | 1239 | 1865 | 1155 | 2530 | 218 | 6.96 | 29 | 0.095 | 0.75 | 0.61 | 1000 | 16,500 |

| 4 | 705 | 868 | 1435 | 1022 | 1928 | 46 | 3.53 | 20 | 0.15 | 0.83 | 0.53 | 750 | 3092 |

| 5 | 1124 | 1304 | 2509 | 1441 | 2973 | 203 | 6.49 | 43 | 0.1 | 0.59 | 0.5 | 900 | 24,000 |

| 6 | 595 | 1122 | 1601 | 1499 | 2968 | 660 | 2.18 | 28 | 0.15 | 0.58 | 0.68 | 900 | 16,000 |

| 7 | 572 | 903 | 1606 | 1240 | 2300 | 73.5 | 3.48 | 17.5 | 0.1 | 0.54 | 0.48 | 911 | 18,089 |

| 8 | 669 | 1125 | 1811 | 1001 | 1613 | 59 | 4.63 | 12 | 0.09 | 0.7 | 0.37 | 1546 | 20,000 |

| 9 | 1389 | 1856 | 3161 | 1576 | 3199 | 199 | 5.8 | 106 | 0.12 | 1.43 | 0.47 | 1250 | 16,000 |

| 10 | 2199 | 2138 | 4027 | 2506 | 4366 | 16035 | 25.5 | 80.5 | 0.15 | 0.995 | 1.8 | 880 | 19,000 |

| 11 | 1363 | 1725 | 2419 | 1658 | 2802 | 4152 | 9.83 | 14 | 0.1 | 0.355 | 0.37 | 900 | 16,000 |

| 12 | 225 | 483 | 1401 | 655 | 1437 | 47 | 2.73 | 5.02 | 0.05 | 0.57 | 1.12 | 1490 | 12,600 |

| 13 | 424 | 538 | 1320 | 572 | 1415 | 57 | 3.64 | 24 | 0.105 | 1.05 | 1.18 | 2500 | 12,200 |

| 14 | 277 | 546 | 1270 | 576 | 1440 | 51 | 3.38 | 10 | 0.09 | 1.46 | 1.21 | 1940 | 11,680 |

| 15 | 469 | 768 | 1677 | 722 | 1584 | 27.8 | 4.76 | 30.1 | 0.54 | 0.77 | 0.64 | 1420 | 12,450 |

| 16 | 281 | 516 | 1194 | 585 | 1644 | 49 | 5 | 26 | 0.08 | 0.18 | 1.18 | 1860 | 13,850 |

| 17 | 395 | 1335 | 3454 | 1390 | 3108 | 48 | 4.24 | 8.71 | 0.09 | 0.71 | 5.3 | 2300 | 1750 |

| 18 | 406 | 1804 | 7119 | 1660 | 6407 | 483 | 6.1 | 21 | 0.9 | 0.55 | 5.3 | 2770 | 2300 |

| 19 | 434 | 1969 | 3351 | 1588 | 3016 | 180 | 4.91 | 19 | 0.08 | 0.71 | 5.38 | 3070 | 850 |

| 20 | 480 | 1969 | 5083 | 1505 | 4575 | 113 | 4.88 | 16 | 0.09 | 0.55 | 5.3 | 2680 | 1650 |

| 21 | 357 | 1588 | 1742 | 928 | 1568 | 47 | 5.03 | 13 | 0.08 | 1.52 | 5.3 | 3320 | 1550 |

| 22 | 590 | 1866 | 4021 | 765 | 3619 | 105 | 6.44 | 12 | 0.05 | 7.26 | 11 | 5000 | 950 |

| 23 | 351 | 1412 | 3237 | 1340 | 2914 | 62 | 4.88 | 14 | 0.93 | 3.38 | 5.3 | 3130 | 1700 |

| 24 | 348 | 1297 | 1433 | 478 | 1720 | 200 | 2.6 | 11.55 | 0.021 | 0.38 | 1.5 | 2584 | 1800 |

| 25 | 923 | 2857 | 3780 | 1002 | 4716 | 108 | 4.25 | 25.89 | 0.06 | 0.34 | 0.007 | 2200 | 2600 |

| 26 | 542 | 3043 | 3650 | 591 | 3386 | 612 | 2.65 | 14.9 | 0.1045 | 4.02 | 0.6367 | 3900 | 2400 |

| 27 | 482 | 2807 | 3514 | 528 | 3240 | 122.01 | 3.67 | 1.67 | 0.11 | 10.211 | 0.5145 | 4200 | 3700 |

| 28 | 535 | 3028 | 3672 | 584 | 3386 | 200.32 | 3.06 | 22.52 | 0.1311 | 11.2213 | 0.8155 | 4400 | 2900 |

| 29 | 1270 | 3089 | 6491 | 1203 | 6491 | 124 | 9.49 | 23 | 0.09 | 0.8 | 0.68 | 1300 | 1100 |

| 30 | 567 | 3221 | 3921 | 619 | 3619 | 1009 | 4.14 | 35.66 | 0.095 | 9.37 | 0.63 | 3900 | 2400 |

| 31 | 385 | 663 | 1884 | 744 | 1642 | 181 | 6.07 | 24.5 | 0.145 | 2.37 | 0.57 | 1764 | 4554 |

| 32 | 407 | 614 | 1353 | 590 | 1470 | 208 | 5.1 | 20.13 | 0.07 | 4.42 | 0.38 | 2300 | 4500 |

| 33 | 430 | 818 | 1649 | 941 | 2076 | 139 | 4.56 | 14 | 0.65 | 0.46 | 0.23 | 1244 | 2144 |

| 34 | 294 | 495 | 1051 | 516 | 1863 | 157 | 4.74 | 31 | 0.2 | 1.605 | 1.405 | 1450 | 2100 |

| 35 | 1905 | 2681 | 4195 | 2692 | 4722 | 32 | 2.64 | 71 | 0.16 | 1.93 | 0.16 | 800 | 1500 |

| JBIC 2007~2022 | MR1 | MR3 | MR2 | MR4 |

|---|---|---|---|---|

| a | 0.147 | 0.136 | 0.531 | −0.126 |

| b | −0.374 | 0.282 | 0.699 | 0.274 |

| c | −0.336 | 0.191 | 0.482 | |

| d | −0.134 | 0.435 | −0.398 | 0.252 |

| e | 0.42 | 0.455 | −0.605 | |

| f | −0.134 | 0.424 | 0.571 | −0.346 |

| g | 0.644 | 0.218 | ||

| h | −0.25 | 0.824 | ||

| i | 0.208 | 0.595 | ||

| j | 0.404 | −0.314 | −0.618 | |

| k | −0.702 | −0.417 | 0.13 | |

| l | 0.855 | −0.124 | ||

| m | 0.749 | −0.191 | 0.207 | |

| n | 1.008 | 0.28 | −0.1 | 0.143 |

| o | 1.055 | 0.148 | ||

| p | 0.203 | 0.949 | ||

| q | 0.292 | 0.858 | 0.134 | −0.103 |

| r | 0.968 | −0.115 | 0.483 | |

| MR1 | MR3 | MR2 | MR4 | |

| SS loadings | 5.736 | 3.867 | 2.336 | 1.002 |

| Proportion Var | 0.319 | 0.215 | 0.13 | 0.056 |

| Cumulative Var | 0.319 | 0.533 | 0.663 | 0.719 |

| JETRO 2010 Asia | MR4 | MR3 | MR1 | MR2 |

| w1 | 0.866 | −0.188 | −0.223 | 0.293 |

| w2 | 0.999 | |||

| w3 | 0.807 | 0.296 | 0.186 | 0.116 |

| w4 | 0.56 | −0.3 | ||

| z1 | 0.735 | 0.378 | −0.141 | |

| z2 | 0.568 | 0.498 | 0.146 | |

| z3 | 0.683 | −0.244 | −0.326 | |

| p1 | −0.262 | −0.525 | 0.261 | −0.394 |

| p2 | −0.127 | 0.173 | 0.974 | |

| p3 | −0.288 | 1.029 | −0.111 | |

| c1 | 0.961 | 0.175 | ||

| c2 | −0.287 | 0.655 | 0.654 | |

| MR4 | MR3 | MR1 | MR2 | |

| SS loadings | 4.215 | 1.869 | 1.811 | 1.792 |

| Proportion Var | 0.351 | 0.156 | 0.151 | 0.149 |

| Cumulative Var | 0.351 | 0.507 | 0.658 | 0.807 |

| JETRO 2021–22 World | MR1 | MR3 | MR2 | |

| w1 | 1.007 | 0.111 | −0.111 | |

| w2 | 0.447 | 0.717 | 0.175 | |

| w3 | 0.382 | 0.292 | 0.716 | |

| w4 | 0.725 | −0.289 | 0.398 | |

| w5 | 0.48 | 0.201 | 0.687 | |

| z2 | 0.833 | |||

| z3 | 0.639 | −0.183 | ||

| p1 | −0.109 | −0.262 | 0.565 | |

| p2 | 0.96 | −0.293 | ||

| p3 | −0.18 | 0.477 | ||

| c1 | −0.323 | 0.812 | ||

| c2 | 0.508 | −0.268 | −0.303 | |

| MR1 | MR3 | MR2 | ||

| SS loadings | 3.627 | 2.471 | 1.945 | |

| Proportion Var | 0.302 | 0.206 | 0.162 | |

| Cumulative Var | 0.302 | 0.508 | 0.67 |

| 2010 Asia | ML4 |

|---|---|

| 1. Beijing | 1.758 |

| 2. Shanghai | 1.1933 |

| 7. Shinzhen | 0.693 |

| 8. Bangkok | 0.8087 |

| 12. Bengaluru | 0.5813 |

| 2021–22 World | ML1 |

| 5. Shanghai | 1.3888 |

| 9. Beijing | 1.9823 |

| 10. Hong Kong | 3.9729 |

| 11. Taiwan | 1.8993 |

| 25. Buenos Aires | 0.8725 |

| 29. San Paulo | 1.8692 |

Appendix B

The Model

| 1 | See Oqubay and Lin (2020) at p. 10 and p. 28. Kuchiki (2020) defined the concept of “economies of sequence.”. |

| 2 | According to Kou and Zhang (2020), by the end of 2018, there were 2447 industrial hubs in China, including 218 national ETDZs, 153 national HIDZs, and 110 other national development zones. |

| 3 | |

| 4 | It should be noted that here, for example, the corporate tax rate was reduced from 30% to 15% in “state−level” development zones but not in “provincial−level’ development zones. |

| 5 | The “industry−specific” and “region−specific” policies were implemented during this period (Hong Kong Grand Gazette, 19 June 1992). |

| 6 | The government emphasised the importance of Shanghai, with three major projects implemented in the 1990s. The first was the development of Pudong in Shanghai; the second was the construction of the Three Gorges Dam; and the third was the development of high−tech industries via HTDZs. |

| 7 | We provide an explanation of the conditions for what we refer to as the “turning point”‘ in the Chinese economy. Consider the industry sector and the agriculture sector in China, with a fixed wage regarded as a subsistence−level wage. Suppose that there is surplus labour in the agriculture sector. A firm can employ an unlimited number of people on the subsistence−level wage, and this situation is regarded as an unlimited labour supply. However, as the industry sector develops, it hires labour from the agriculture sector and the surplus labour in the agriculture sector disappears. Thus, it becomes impossible to hire at subsistence−level wages. The industrial sector can only hire at higher than subsistence−level wages and the minimum wage starts to rise. The point at which the industry sector can no longer hire at subsistence−level wages without restriction so that wages start to rise is called the “turning point”. |

| 8 | This scientific development perspective is a guiding ideology launched in 2004 by the Hu Jintao Government of China, which took office in 2003. It aims for all−round, balanced, and sustainable development from a scientific and rational perspective, with people as the fundamental factor. It also involves a unified five−point plan on the basic premise of high economic growth, comprising urban and rural development, regional development, economic and social development, development in harmony with people and nature, and domestic development and opening−up to the outside world. The Chinese Government changed the central issues from a growth−oriented approach to one that sought to narrow the income gap and solve environmental problems while upgrading industrial infrastructure. |

| 9 | In the first phase, the Shanghai Pilot Free−Trade Zone aimed to act as a base at which to agglomerate various modern service industries (Tang Wenhong, Director General, Foreign Investment Bureau, Ministry of Commerce of China, Xinhua, 29 May 2019). Six industries were designated as “Modern Service Industries”, with the financial industry the major one, followed by the aviation and transport service industry, commerce and trade services, professional services, culture and content, and social services. It is a bonded zone that is exempt from import duties on equipment and raw materials. |

| 10 | In the second phase, pilot free−trade zones were established in three regions in 2015—Guangdong, Tianjin, and Fujian—and in seven regions in 2017—Liaoning, Zhejiang, Henan, Hubei, and Sichuan, and Shaanxi provinces, and Chongqing. As part of the third phase, implemented in 2018, Hainan Province was designated as the 12th pilot free−trade zone; with pilot free−trade zones later established in six provinces and autonomous regions in 2019—Shandong, Jiangsu, Guangxi, Hebei, Yunnan, and Heilongjiang. |

| 11 | Note that industrial zones are not sold but rented in Cambodia, Vietnam, and Myanmar. |

References

- Chen, Xiaohong, and Akifumi Kuchiki. 2000. China’s Industrial Policy in International Comparison. In China’s Industrial Policy in Transition. Edited by Tomoo Marukawa. Tokyo: Institute of Developing Economies−Japan External Trade Organization, (In Japanese, Kokusaihikaku kara Mita Chugoku no Sangyouseisaku, Ikouki Chugoku no Sangyoseisaku). [Google Scholar]

- Council of Local Authorities for International Relations (CLAIR) Foundation, Beijing Office. 2003. China’s Enterprise Attraction Policy. In CLAIR Report. Santa Monica: CLAIR Foundation, No. 248. Available online: http://www.clairbj.org/sys/wp-content/uploads/2017/04/248-1.pdf (accessed on 11 August 2021).

- Dixit, Avinash K., and Joseph E. Stiglitz. 1977. Monopolistic Competition and Optimum Product Diversity. American Economic Review 67: 27–49. [Google Scholar]

- Fujita, Masahisa, and Akifumi Kuchiki, eds. 2006. Asian Economic Regional Integration from Viewpoint of Spatial Economics. Joint Research Program Series No.138; Chiba: IDE−Japan External Trade Organization. [Google Scholar]

- Fujita, Masahisa, Paul R. Krugman, and Anthony Venables. 1999. The Spatial Economy. Cambridge: MIT Press. [Google Scholar]

- Helpman, Elhanan, and Paul Krugman. 1985. Market Structure and Foreign Trade. Oxford: Oxford University Press. [Google Scholar]

- Hirschman, Albert O. 1958. The Strategy of Economic Development. New Haven: Yale University Press. [Google Scholar]

- JBIC (Japan Bank for International Cooperation). 2022. Report on Survey of Overseas Business Expansion of Japanese Manufacturing Companies. Available online: https://www.jbic.go.jp/ja/information/press/press−2022/1216−017128.html (accessed on 25 September 2023).

- JETRO (Japan External Trade Organization). 2010. Comparison of Investment Related Costs 2010. Available online: https://www.jetro.go.jp/world/reports/2010/07000312.html (accessed on 25 September 2023).

- JETRO (Japan External Trade Organization). 2022. Investment−Related Cost Comparison of Major Cities 2022. Available online: https://www.jetro.go.jp/world/search/cost.html (accessed on 25 September 2023).

- Kanai, Kazuyori, and Syuichi Ishida. 2000. Accumulation Process of Regional Industry and Entrepreneurship: Case Study of Sapporo Valley. Presented at the Entrepreneurship on the Technology Frontier in the USA, the UK and Japan Working Paper, International Conference in Vanderbilt University, Nashville, TN, USA, 13 October; October 13. [Google Scholar]

- Kou, Zonglai, and Jun Zhang. 2020. Industrial Hubs in ‘Sphinx’ China. In The Oxford Handbook of Industrial Hubs and Economic Development. Edited by Arkebe Oqubay and Justin Yifu Lin. Oxford: Oxford University Press, pp. 575–91. [Google Scholar]

- Kuchiki, Akifumi. 2020. On ‘Economies of Sequence’ in the Architectural Theory of Agglomeration: A Case of the Kyoto Tourism Industry. Economies 8: 15. [Google Scholar] [CrossRef]

- Kuchiki, Akifumi, and Hideyoshi Sakai. 2023. Symmetry Breaking as “Master Switch” for Agglomeration Policy. Review of Public Administration and Management 11: 1–8. Available online: https://www.walshmedicalmedia.com/archive/rpam−volume−11−issue−2−year−2023.html (accessed on 11 November 2023).

- Markusen, Ann. 1996. Sticky Places in Slippery Space: A Typology of Industrial Districts. Economic Geography 72: 293–313. [Google Scholar] [CrossRef]

- National Bureau of Statistics of China 2008. China Statistical Yearbook. China Statistics Press. Available online: https://www.stats.gov.cn/sj/ndsj/2008/indexeh.htm (accessed on 5 December 2023).

- National Bureau of Statistics of China 2019. China Statistical Yearbook. China Statistics Press. Available online: https://www.stats.gov.cn/sj/ndsj/2019/indexeh.htm (accessed on 5 December 2023).

- Oqubay, Arkebe. 2020. Industrial Hubs as Development Incubator. In The Oxford Handbook of Industrial Hubs and Economic Development. Edited by Arkebe Oqubay and Justin Yifu Lin. Oxford: Oxford University Press, pp. 523–58. [Google Scholar]

- Oqubay, Arkebe, and Justin Yifu Lin, eds. 2020. Industrial Hubs and Economic Development. In The Oxford Handbook of Industrial Hubs and Economic Development. Oxford: Oxford University Press, pp. 3–14. [Google Scholar]

- Pietrobelli, Carlo. 2020. Modern Industrial Policy in Latin America. In The Oxford Handbook of Industrial Hubs and Economic Development. Edited by Arkebe Oqubay and Justin Yifu Lin. Oxford: Oxford University Press, pp. 783–98. [Google Scholar]

- State Council of China. 2020a. Some Opinions on Promoting the Quality Development of National High−tech Industrial Development Zones. August 17. Available online: http://www.gov.cn/zhengce/content/2020−07/17/content_5527765.htm (accessed on 11 August 2021).

- State Council of China. 2020b. Notice of the State Council on the Overall Plan of Beijing, Hunan and Anhui Pilot Free Trade Zones and the Regional Expansion Plan of Zhejiang Pilot Free Trade Zone. August 30. Available online: http://www.gov.cn/zhengce/content/2020−09/21/content_5544926.htm (accessed on 11 August 2021).

- UNCTAD. 2019. Special Economic Zones. Available online: https://unctad.org/system/files/official−document/wir2019_en.pdf (accessed on 2 June 2023).

- Wei, Jigang. 2020. China’s Industrial Policy: Evolution and Experience, South−South Integration and the SDGs: Enhancing Structural Transformation in Key Partner Countries of the Belt and Road Initiatives. UNCTAD/BRI PROJECT/RP11. Available online: https://unctad.org/system/files/official−document/BRI−Project_RP11_en.pdf (accessed on 11 November 2023).

- World Bank. 1993. East Asian Miracle. Oxford: Oxford University Press. [Google Scholar]

| Period 1: Start of (i) Industrial Agglomeration Policy (IAP) | Period 2: Start of (ii) Industrial Policy (IP) | |

|---|---|---|

| Period | 1978–1984 | 1984–1992 |

| Classification | Introduction of market economy | Formation of market economy |

| Basic | Elimination of supply shortage | Formation of unified markets (commodities, labour etc.) |

| Idea | Industrial structure adjustment | |

| Policy | (i) “SEZ: Special Economic Zones 1979” | (i) ETDZ: State-level Economic and Technological Development Zones 1984 |

| Industry | Light industries by | Basic industries |

| Township and Villege Enterprises Reform | ||

| Textile | Infrastructure | |

| Agriculture | Energy industry | |

| Steel and other materials industries | ||

| Regional | (i) “SEZ (Special Economic Zones): 4 locations” Shenzhen, Zhuhai, Xiantou, Xiamen (i)980 | (i) ETDZ: Dalian, Shanghai, Guangzhou, etc. 14 places |

| Policy | (i) Economic Region in Southern China | |

| Means | Direct control of quantity and price | (i) ETDZ: FDI introduction policy |

| Allocation of capital and foreign currency | (ii) IP: Establishment of Industrial Policy Department 1988 | |

| System of distribution tickets of goods | (ii) IP: Announcement of the list of priority industries in 1989 | |

| Special note | (i) SEZ: Industrial agglomeration policy 1979 Establishment of Special Economic Zones | (ii) IP: Merger and reorganization of enterprises |

| Period 3: Coexistence of (i) Industrial Agglomeration Policy and (ii) Industrial Policy | Period 4: Emphasis on (i) Industrial Agglomeration Policy | |

|---|---|---|

| Period | 1992–1997 | 1997–2004 |

| Classification | (i) Industrial agglomeration policy and (ii) Industrial policy | (i) Industrial agglomeration policy |

| Basic | Emphasis on international competition | Globalization: |

| Idea | Industrial structure rationalization | Competition with multinationals |

| Policy | (i) HTDZ: State-level High-Tech Development Zones 1992: 52 locations | (i) “WTO Accession in 2001” |

| (ii) IP: Protection policy for infant industry | ||

| Industry | (ii) Industrial Policy Outline 1994: Four Major Pillar Industries | (i) Emphasis on international competitiveness |

| (ii) IP: Automobile Industry Policy 1994 | ||

| (ii) IP: Four Major Pillar Industries: | (ii) Information Communication Industry | |

| “Automobile, Machinery & Electronics, Petrochemicals, Construction” | New materials, Biotechnology | |

| Regional | (i) “Yangtze River Economic Region” | (i) Bohai Sea Rim Economic Region |

| Policy | (i) Western Great Development 2000 | |

| Means | (i) FDI introduction through development zones: ETDZ, HTDZ | (i) Joint venture, technical cooperation |

| (ii) Industrial policy | (ii) Merger and restructuring of enterprises | |

| Special note | (i) IAP: Deng Xiaoping’s “Southern Tour Speech 1992” | (i) Asian currency crisis 1997 |

| (i) IAP: Announcement of “Industrial Policy” Priority industries for foreign investment 1997 | (ii) Zhu Rongji: | |

| (ii) IP: ’Industrial Policy Outline’ and ’Automobile Industry Policy’ 1994 | IP: Reform of state-owned enterprises 1998 |

| Period 5: Emphasis on Harmonious Society | Period 6: New Start of (i) IAP and (ii) IP | Period 7: Integration of (i) IAP and (ii) IP | |

|---|---|---|---|

| Year | 2004–2010 | 2010–2013 Rebalancing | 2013–2022 |

| Classification | Harmonious Society | Change in pattern of economic development | Socialist Market Economy with Chinese Characteristics (i) (ii) |

| Basic | Scientific View of Development | Escape from the “Trap of Middle-income Countries” | (i) (ii) Domestic Circulation: Target 2035 |

| Ideology | Passing the “turning point” | ||

| Policy | Reduction of disparities | (i) PFTZ: Shanghai Pilot Free Trade Zone 2013 | (i) (ii) SEI: Strategic Emerging Industries |

| Environmental conservation | (ii) IP: Strategic Emerging Industries 2010 | (i) (ii) PFTZ: Beijing Pilot Free Trade Zone 2021 | |

| One Belt, One Road Joint Construction 2013 | |||

| Industry | Upgrading industrial structure: | (ii) IP: 7 major industries: | (i) IP: Modern Service Industries 2013 |

| (ii) High-tech industries | Environmental protection, | (ii) IP: Strategic Emerging Industries | |

| (ii) Biomedicine | Information Communication, | Post COVID-19 | |

| (ii) High-tech informatization | New energy, New energy automobiles, etc. | Green economy and Digital economy | |

| Regional | (i) Western Development | (i) Northeast Regional Development Plan (2016–2020) | (i) (ii) PFTZ: 21 Pilot Free Trade Zones 2021 |

| Means | (ii) Creation of independent technology | New rural construction | (i) (ii) New infrastructure construction 2020 |

| Special note | Increase in minimum wage | Reduction of corruption | (i) (ii) 1st in the world: |

| Three-farm problem | Emphasis on green industry | Fortune’s World 500 largest companies: | |

| Lehman Shock 2008 | China’s GDP 2nd in the world 2010 | 124 companies 2020 |

| Segments | ||

|---|---|---|

| Capacity | 1. Infrastructure | (1) Water |

| (2) Electricity | ||

| (3) Communication | ||

| (4) Transport (Transport costs) | ||

| 2. Institutions | (1) One-stop services (Transport costs) | |

| (2) Deregulation | ||

| (3) Preferential treatments (tax incentives, etc.) (Transport costs) | ||

| (4) Laws and regulations (bankruptcy laws and intellectual property right) | ||

| 3. Human resource | (1) Unskilled labor | |

| (2) Skilled labor | ||

| (3) Professionals | ||

| 4. Living conditions | (1) Housing | |

| (2) International schools | ||

| (3) Hospitals | ||

| (4) Entertainment | ||

| 1997 | 1998 | 1997 | 1998 | |||||

|---|---|---|---|---|---|---|---|---|

| Export | Share | Export | Share | Import | Share | Import | Share | |

| Machinery, Transport equipment | 488.16 | 26.7 | 564.21 | 30.7 | 578.66 | 40.6 | 620.89 | 44.3 |

| Machinery: machinery, appliances, electrical equipment and parts, recorders and playback equipment, equipment for recording and reproducing video images and sound, and parts and accessories. | 382.7 | 20.9 | 436.29 | 23.7 | 467.58 | 32.8 | 509.09 | 36.3 |

| Vehicles: Aircraft, ships and related transport equipment | 52.73 | 2.9 | 63.96 | 3.5 | 55.54 | 3.9 | 55.9 | 4.0 |

| Railway and tramway locomotives, rolling stock and parts, railway and tramway fixtures and accessories, various mechanical (electrical), traffic signalling equipment | 11.95 | 0.7 | 18.21 | 1.0 | 1.19 | 0.1 | 2.24 | 0.2 |

| Vehicles and their parts and accessories, excluding railways and trams. | 21.57 | 1.2 | 22.72 | 1.2 | 18.96 | 1.3 | 20.03 | 1.4 |

| Aircraft, spacecraft and parts thereof | 2.91 | 0.2 | 4.4 | 0.2 | 32.35 | 2.3 | 31.75 | 2.3 |

| Ships and floating structures | 16.3 | 0.9 | 18.63 | 1.0 | 3.04 | 0.2 | 1.88 | 0.1 |

| Optical, photographic, cinematographic, measuring, testing, medical or surgical instruments, precision instruments and apparatus, clocks and watches, musical instruments, and parts and accessories thereof | 63.21 | 3.5 | 65.64 | 3.6 | 46.72 | 3.3 | 49.26 | 3.5 |

| Total | 1827.92 | 100.0 | 1837.57 | 100.0 | 1423.7 | 100.0 | 1401.66 | 100.0 |

| 2008 | 2009 | 2017 | 2018 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Classification | Value | Share | Value | Share | Value | Share | Value | Share | |

| Industrial products | 1,352,736 | 94.5511 | 1,138,564 | 94.74903 | 2,145,813 | 94.79974 | 2,352,021 | 94.6 | |

| Machinery, Transport equitment | 673,329 | 47.06314 | 590,427 | 49.13416 | 1,082,905 | 47.84159 | 1,208,055 | 48.6 | |

| Textile, rubber and mineral products | 262,391 | 18.34013 | 184,775 | 15.37661 | 368,054 | 16.26024 | 404,753 | 16.3 | |

| Chemicals and related products | 79,346 | 5.545984 | 62,048 | 5.163511 | 141,329 | 6.243765 | 167,525 | 6.7 | |

| Miscellaneous products | 335,959 | 23.48226 | 299,670 | 24.93794 | 547,767 | 24.19976 | 565,814 | 22.7 | |

| Unclassified other products | 1710 | 0.119522 | 1645 | 0.136894 | 5758 | 0.254382 | 5873 | 0.2 | |

| Primary products | 77,957 | 5.448898 | 63,099 | 5.250973 | 117,709 | 5.200259 | 135,086 | 5.4 | |

| Total | 1,430,693 | 100 | 1,201,663 | 100 | 2,263,522 | 100 | 2,487,401 | 100 | |

| Import (CIF) | |||||||||

| 2008 | 2009 | 2017 | 2018 | ||||||

| Classification | Value | Share | Value | Share | Value | Share | Value | Share | |

| Industrial products | 770,167 | 68.00219 | 716,353 | 71.2 | 1,263,918 | 68.65456 | 1,434,025 | 67.1 | |

| Machinery, Transport equitment | 441,765 | 39.00581 | 407,999 | 40.6 | 734,846 | 39.91598 | 839,524 | 39.3 | |

| Textile, rubber and mineral products | 107,165 | 9.462175 | 107,732 | 10.7 | 135,075 | 7.337117 | 151,452 | 7.1 | |

| Chemicals and related products | 119,188 | 10.52375 | 112,124 | 11.2 | 193,744 | 10.52395 | 233,683 | 10.9 | |

| Miscellaneous products | 97,641 | 8.62125 | 85,192 | 8.5 | 134,175 | 7.28823 | 143,759 | 6.7 | |

| Unclassified other products | 4409 | 0.389294 | 3306 | 0.3 | 66,079 | 3.589334 | 75,607 | 3.5 | |

| Primary products | 362,395 | 31.99781 | 289,202 | 28.8 | 577,064 | 31.34544 | 701,613 | 32.9 | |

| Total | 1,132,562 | 100 | 1,005,555 | 100 | 1,840,982 | 100 | 2,135,637 | 100 | |

| Hypothesis | Lag Years | F-Test | p-Value | Period |

|---|---|---|---|---|

| (i) domestic investment—GDP ratio causes (x) export growth rate | 3 | 3.186 | 0.03905 * | 1987–2009 |

| (i) domestic investment—GDP ratio causes (g) industy growth rate | 2 | 5.7014 | 0.007324 *** | 1987–2009 |

| (i) -> (x), (i) -> (g) | ||||

| (f) foreign direct investment causes (m) import growth rate | 2 | 3.5913 | 0.0346 * | 1987–2018 |

| (f) -> (m) -> (g) -> (y) (1987–2009) |

| Coefficients | p-Value | Adjusted R-Squared | Period | |

|---|---|---|---|---|

| (g) industry growth rate | 1987–2018 | |||

| Intercept | 9.23654 | 4.61 × 10−16 *** | ||

| (a) growth rate of foreign direct investment | 0.08552 | 2.24 × 10−6 *** | ||

| 0.5157 | ||||

| (y) GDP growth rate | 1987–2018 | |||

| Intercept | 8.379637 | 2.750743 × 10−20 *** | ||

| (a) growth rate of foreign direct investment | 0.040663 | 0.000148 *** | ||

| 0.3655 | ||||

| (Δf/f) = (a) <-> (g) <-> (y) |

| Survey Cities for Factor Analysis | ||

|---|---|---|

| China | 1. Chengdu | |

| area | 2. Dalian | |

| Year | 3. Guangzhou | |

| 2021 | 4. Qingdao | |

| 5. Shanghai | ||

| 6. Shinzhen | ||

| 7. Wuhan | ||

| 8. Chongqing | ||

| 9. Beijing | ||

| 10. Hong Kong | ||

| 11. Taiwan | ||

| India | 12. Ahmedabad | |

| 2022 | 13. Bengaluru | |

| 14. Chennai | ||

| 15. Munbai | ||

| 16. New Delhi | ||

| Asia | 1. Beijing | |

| Year | 2. Shanghai | |

| 2010 | 3. Guangzhou | |

| 4. Dalian | ||

| 5. Shenyang | ||

| 6. Qingdao | ||

| 7. Shinzhen | ||

| 8. Bangkok | ||

| 9. Jakarta | ||

| 10. Manila | ||

| 11. Sebu | ||

| 12. Bengaluru | ||

| 13. Colombo | ||

| Mexico | 17. Irapuato | |

| Year 2022 | 18. Mexico City | |

| 19. Monterrey | ||

| 20. Queretaro | ||

| 21. San Luis Potosi | ||

| 22. Tijuana | ||

| 23. Aguascalientes | ||

| South | 24. Asuncion | Paraguay |

| America | 25. Buenos Aires | Argentina |

| 2022 | 26. Campinas | Brasil |

| 27. Manaus | Brasil | |

| 28. Rio de Janeiro | Brasil | |

| 29. San Paulo | Brasil | |

| 30. Santiago | Chile | |

| ASEAN | 31. Bangkok | Thailand |

| 2022 | 32. Jakarta | Indonesia |

| 33. Kuala Lumpur | Malaysia | |

| 32. Jakarta | Vietnam | |

| 35. Danang | Vietnam | |

| 36. Hanoi | Vietnam | |

| 37. Hochiminh | Lao | |

| 38. Yangon | Myanmer | |

| 39. Bientian | Cambosia | |

| 40. Punon Phen | Cambosia | |

| City: Dalian, China | ||

|---|---|---|

| Survey Period: November 2022~January 2023 | ||

| Exchange Rate: 1US$ = (1 November 2022, Interbank) | ||

| Including VAT | ||

| Survey items | US$ | |

| W1 | worker (general laborer) (per month) (manufacturing) | 506 |

| W2 | engineer (intermediate technitian) (per month) (same as above) | 822 |

| W3 | middle management (section chief) (per month) (same) | 1268 |

| W4 | staff (general office work) (per month) (non-manufacturing) | 1037 |

| W5 | manager (section chief) (per month) (same as above) | 2185 |

| Z1 | industrial zone (land) (purchase price) (per square meter) | 96 |

| Z2 | industrial zone rent (per square meter, per month) | 2.97 |

| Z3 | office rent (per squre meter, per month | 22 |

| P1 | commercial electricity rates (pre 1 kWh) | 0.095 |

| P2 | commercial water rates (per cubic meter) | 0.68 |

| P3 | commercial gas rates (per 1 kg) | 0.46 |

| C1 | container transport to Japan (40 ft) | 804 |

| C2 | container transport to the third country (40 ft) | 13,915 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kuchiki, A. Accelerator for Agglomeration in Sequencing Economics: “Leased” Industrial Zones. Economies 2023, 11, 295. https://doi.org/10.3390/economies11120295

Kuchiki A. Accelerator for Agglomeration in Sequencing Economics: “Leased” Industrial Zones. Economies. 2023; 11(12):295. https://doi.org/10.3390/economies11120295

Chicago/Turabian StyleKuchiki, Akifumi. 2023. "Accelerator for Agglomeration in Sequencing Economics: “Leased” Industrial Zones" Economies 11, no. 12: 295. https://doi.org/10.3390/economies11120295

APA StyleKuchiki, A. (2023). Accelerator for Agglomeration in Sequencing Economics: “Leased” Industrial Zones. Economies, 11(12), 295. https://doi.org/10.3390/economies11120295