Monetary Policy Implications on Macroeconomic Performance in the Common Monetary Area: A Panel-SVAR Framework

Abstract

:1. Introduction

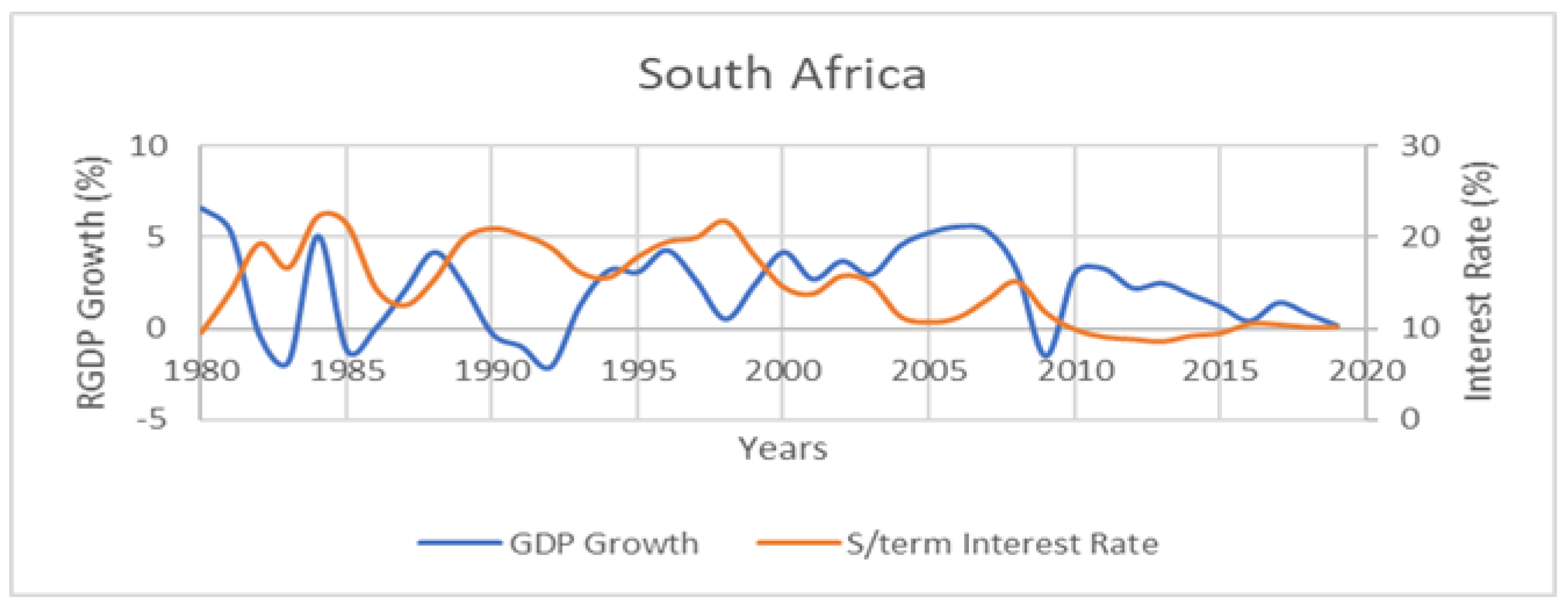

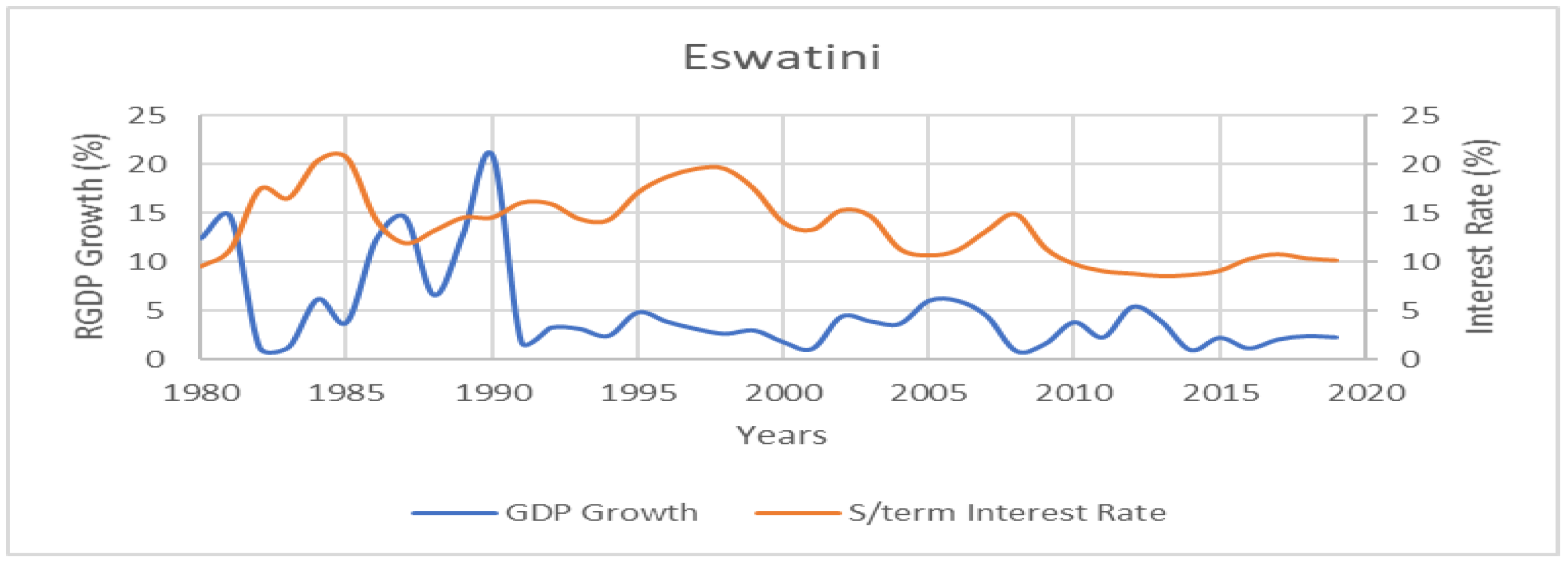

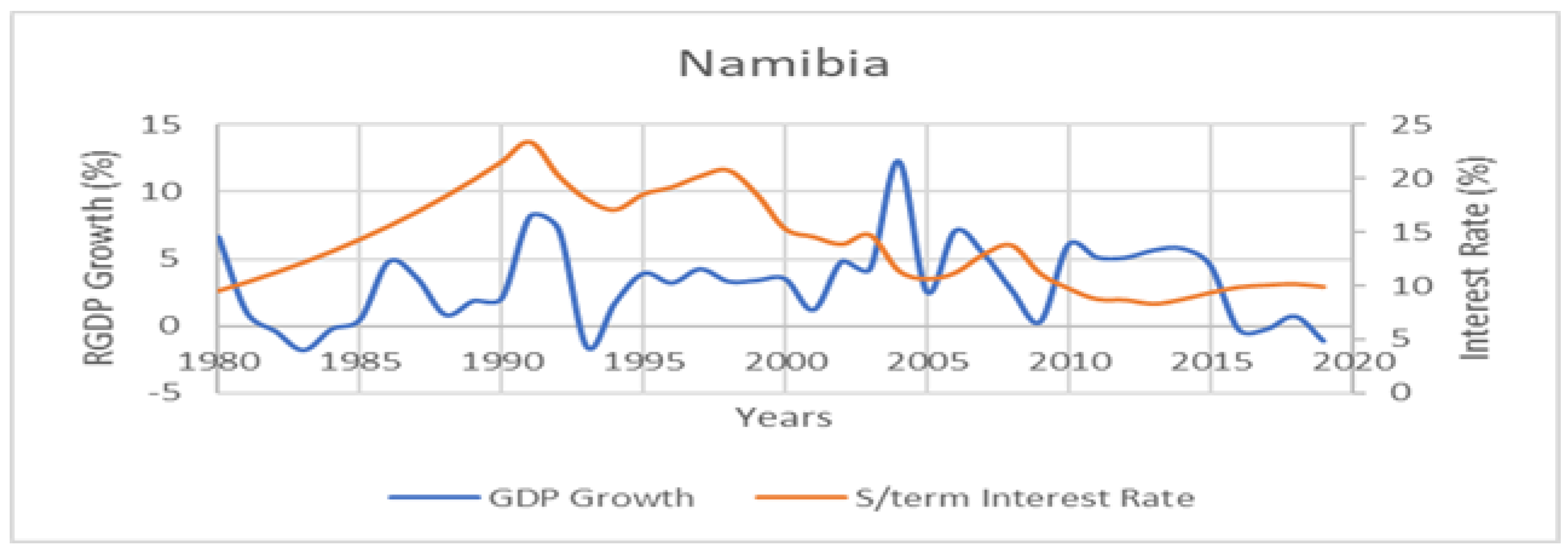

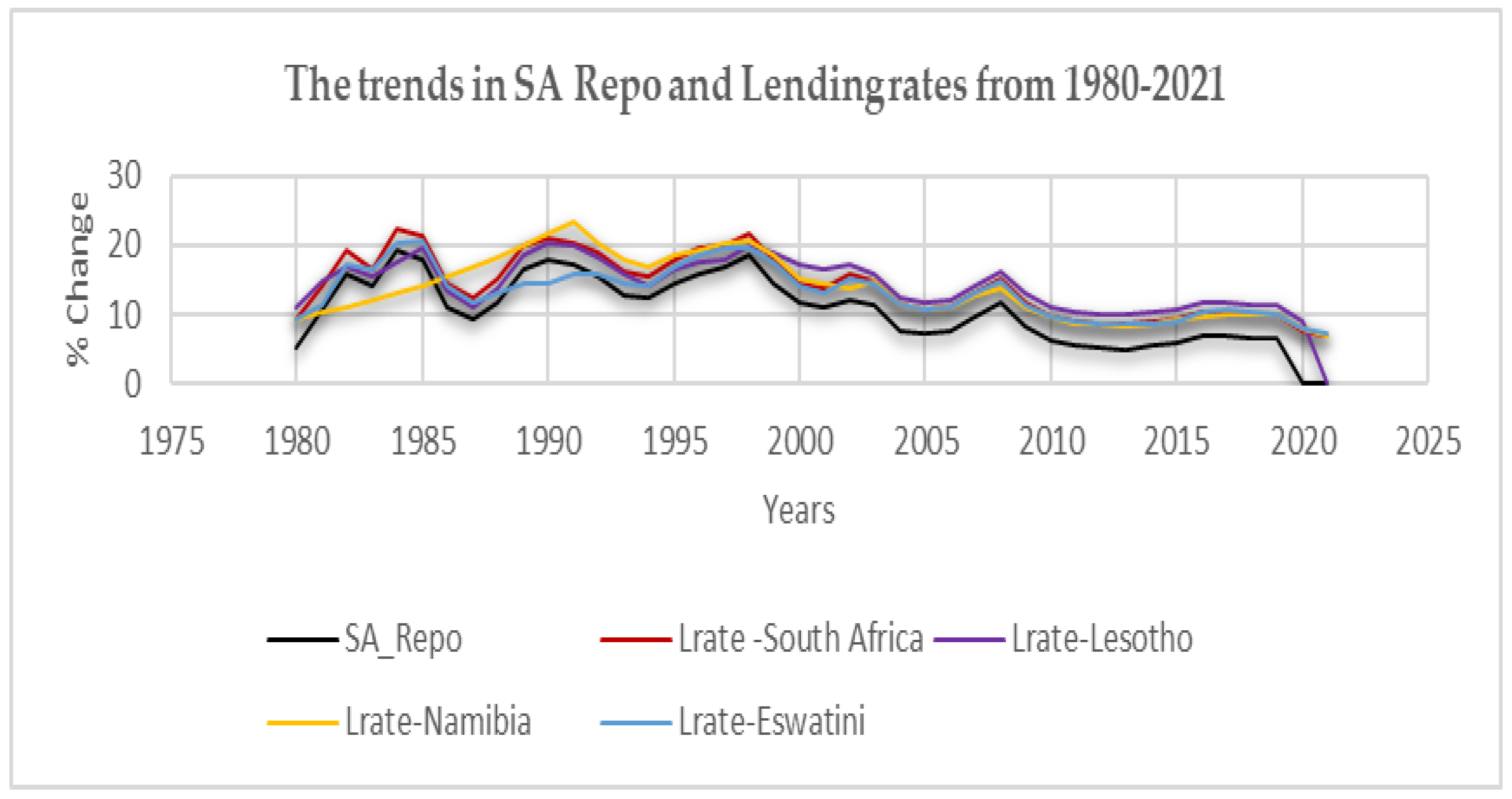

2. Economic Performance in CMA

3. Monetary Policy Shocks and Economic Performance

4. Methodology

4.1. Theoretical Framework

4.2. Model Specification

4.3. Data

4.4. Shocks Identification

5. Estimation Results and Discussion

5.1. Pre-Estimation Tests Results

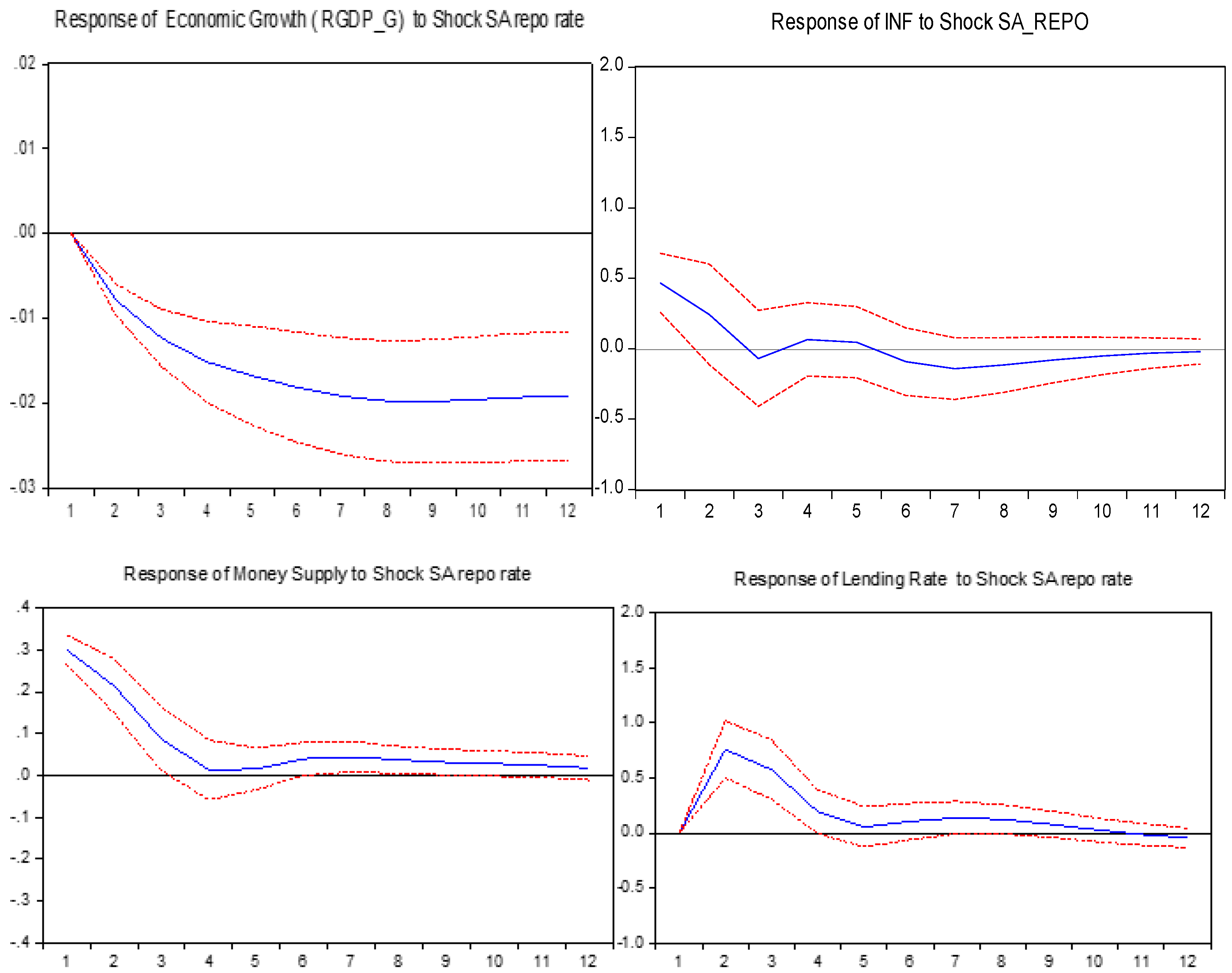

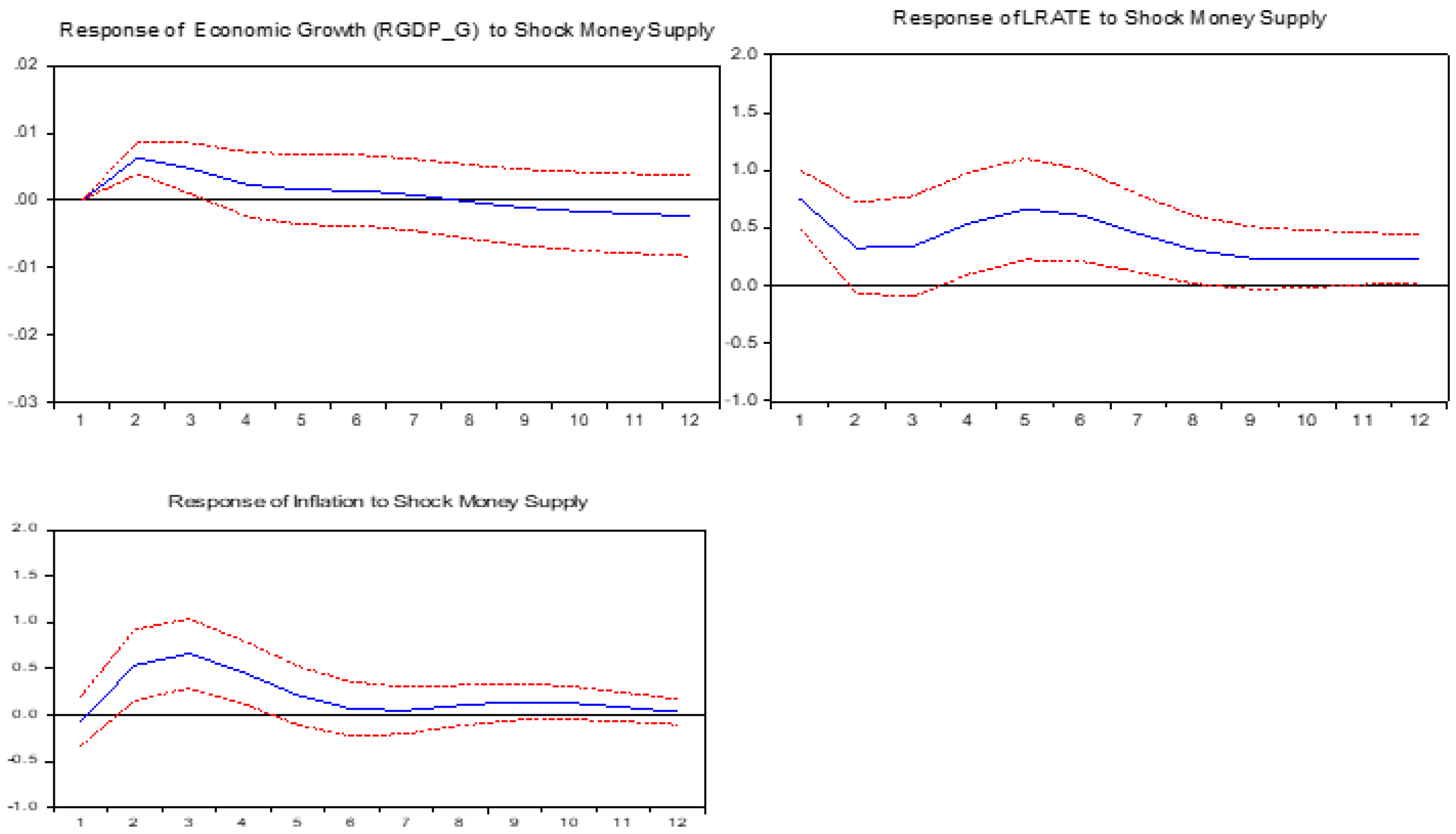

5.2. Impulse Response Functions (IRFs)

5.3. Results of Variance Decomposition Analysis

6. Conclusions and Recommendation

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Akande, Joseph Olorunfemi. 2017. Competition, Regulation, and Stability in Sub-Saharan Africa Commercial Banks. Ph.D. thesis, University of Kwazulu-Natal, Durban, South Africa. [Google Scholar]

- Amisano, Gianni, and Carlo Giannini. 1997. From var models to structural var models. In Topics in Structural VAR Econometrics. Berlin/Heidelberg: Springer, pp. 1–28. [Google Scholar]

- Angeloni, Ignazio, Kashyap Anil, Mojon Benoit, and Daniele Terlizzese. 2003. A Difference in Monetary Transmission in the Euro Area and US. Journal of Money, Credit and Banking 35: 1309–17. Available online: http://www.jstor.org/stable/3649886 (accessed on 7 July 2022). [CrossRef]

- Ayopo, Babajide Abiola, Lawal Adedoyin Isola, and Somoye Russel Olukayode. 2016. Stock market response to economic growth and interest rate volatility. Evidence from Nigeria. International Journal of Economics and Financial Issues 6: 354–60. [Google Scholar]

- Bank of Namibia. 2022. Namibia’s Monetary Policy Framework. Tech. Rep. Bank of Namibia. Available online: https://www.bon.com.na (accessed on 9 September 2022).

- Barigozzi, Matteo, Antonio M. Conti, and Matteo Luciani. 2014. Do Euro Area countries respond asymmetrically to the common monetary policy? Oxford Bulletin of Economics and Statistics 76: 693–714. [Google Scholar] [CrossRef]

- Berkelmans, Leon. 2005. The Set-up of the SVAR RDP 2005–2006: Credit and Monetary Policy: An Australian SVAR. Reserve Bank of Australia Research Discussion Papers 2: 6. [Google Scholar]

- Bikai, J. Landry, and Guy Albert Kenkouo. 2015. Analysis and Evaluation of the Monetary Policy Transmission Channels in the CEMAC: A SVAR and SPVAR Approaches. Munich: IMF Paper. Available online: https://mpra.ub.uni-muenchen.de/78227/ (accessed on 15 June 2022).

- Buigut, Steven. 2009. Monetary Policy Transmission Mechanism: Implications for the Proposed East African. Available online: http://www.csae.ox.ac.uk/conferences/2009-EdiA/paperlist.html (accessed on 12 February 2021).

- Cavallo, Antonella, and Antonio Ribba. 2015. Common macroeconomic shocks and business cycle fluctuations in Euro area countries. International Review of Economics & Finance 38: 377–92. [Google Scholar]

- Central Bank of Eswatini. 2022. Eswatini’s Monetary Policy. Available online: https://www.centralbank.org.sz/monthly-statistical-releases/ (accessed on 9 September 2022).

- Central Bank of Lesotho. 2022. CBL Monetary Policy. Available online: https://www.centralbank.org.ls/index.php/statistics (accessed on 7 September 2022).

- Cheng, Kevin C. 2006. A VAR analysis of Kenya’s monetary policy transmission mechanism: How does the central bank’s repo rate affect the economy? IMF Working Papers 6: 17–25. [Google Scholar] [CrossRef]

- Chileshe, Patrick Mumbi, Keegan Chisha, and Masauso Ngulube. 2018. The effect of external shocks on macroeconomic performance and monetary policy in a small open economy: Evidence from Zambia. International Journal of Sustainable Economy 10: 18–40. [Google Scholar] [CrossRef]

- Dillner, Gustaf. 2021. Determinants of business cycle synchronisation in the Common Monetary Area in Southern Africa. Undergraduate Economic Review 17: 7. [Google Scholar]

- Dlamini, Dumsile F. 2018. Convergence, asymmetry, and monetary policy in a common monetary area. Postgraduate Economic Review 61: 135–78. [Google Scholar]

- Enders, Walter. 2004. Applied Econometric Time Series, 4th ed. Hoboken: John Wiley & Sons, Inc. [Google Scholar]

- Ennis, Huberto M. 2018. A simple general equilibrium model of large excess reserves. Journal of Monetary Economics 98: 50–56. [Google Scholar] [CrossRef]

- Georgiadis, Georgios. 2016. Determinants of global spillovers from US monetary policy. Journal of international Money and Finance 67: 41–61. [Google Scholar] [CrossRef]

- Herve, Drama Bedi Guy. 2017. Estimation of the impact of monetary policy on economic growth: The case of Cote d Ivoire in line with SVAR methodology. Applied Economics and Finance 4: 66–83. [Google Scholar] [CrossRef]

- Ikhide, Sylvanus, and Ebson Uanguta. 2010. Impact of South Africa’s monetary policy on the LNS economies. Journal of Economic Integration 2: 324–52. [Google Scholar] [CrossRef]

- Jane, Kaboro, Kalio Aquilars, and Kibet Lawrence. 2018. The effect of real gross domestic product (GDP) growth rate convergence on exchange rate volatility in search for the East African monetary union. Journal of Economics and International Finance 10: 65–76. [Google Scholar] [CrossRef]

- Kabundi, Alain, and Nonhlanhla Ngwenya. 2011. Assessing monetary policy in South Africa in a data-rich environment. South African Journal of Economics 79: 91–107. [Google Scholar] [CrossRef]

- Kamati, Katrina Namutenya. 2020. An Analysis of Macroeconomic Determinants of House Price Volatility in Namibia. Ph.D. thesis, University of Namibia, Windhoek, Namibia; pp. 12–25. [Google Scholar]

- Kamati, Reinhold. 2014. Monetary Policy Transmission Mechanism and Interest Rate Spreads. Ph.D. thesis, University of Glasgow, Glasgow, UK. [Google Scholar]

- Kashima, Grace. 2017. Analysis of the Impact of Monetary Policy on Economic Growth in Namibia. Ph.D. thesis, University of Namibia, Windhoek, Namibia. [Google Scholar]

- Kato, Hisakazu. 2019. Did Fiscal and Monetary Policies Affect Positively to Economic Activity of Thailand? Asian Administration & Management Review 2: 3367985. [Google Scholar]

- Kutu, Adebayo Augustine, and Harold Ngalawa. 2016. Monetary policy shocks and industrial output in BRICS countries. SPOUDAI-Journal of Economics and Business 66: 3–24. [Google Scholar]

- Masha, Iyabo, Jian-Ye Wang, Kazuko Shirono, and Leighton Harris. 2007. The Common Monetary Area in Southern Africa: Shocks, Adjustment, and Policy Challenges. IMF Journal 31: 355–76. [Google Scholar] [CrossRef]

- Mirdala, Rajmund. 2009. Shocking aspects of monetary integration (SVAR approach). Journal of Applied Research in Finance (JARF) 1: 52–63. [Google Scholar]

- Mishkin, Frederic S. 1995. Symposium on the monetary transmission mechanism. Journal of Economic Perspectives 9: 3–10. [Google Scholar] [CrossRef]

- Mohr, Philip, and Louis Fourie. 2011. Economics for South African Students. Pretoria: Van Schaik Publishers. [Google Scholar]

- Nagar, Dawn. 2020. Southern Africa’s regionalism driven by realism. In The Palgrave Handbook of African Political Economy. Berlin/Heidelberg: Springer, vol. 20, pp. 1027–49. [Google Scholar]

- Nielsen, Hannah, Ebson Uanguta, and Sylvanus Ikhide. 2005. Financial integration in the Common Monetary Area. South African Journal of Economics 73: 710–21. [Google Scholar] [CrossRef]

- Rossouw, Jannie, and Vishnu Padayachee. 2020. The independence of the South African Reserve Bank: Coming full circle in 25 years? In The Political Economy of Central Banking in Emerging Economies. Pretoria: Routledge, pp. 134–48. [Google Scholar]

- Seleteng, Monaheng. 2016. Slow growth in South Africa: Spill overs to other CMA countries. In Central Bank of Lesotho Working Paper (01/16). Maseru: Central Bank of Lesotho. [Google Scholar]

- Seoela, Bonang N. 2020. The effects of South Africa’s unexpected monetary policy shocks in the Common Monetary. Master’s thesis, Boise State University, Boise, ID, USA. [Google Scholar]

- Sims, Christopher A. 1992. Interpreting the macroeconomic time series facts: The effects of monetary policy. European Economic Review 36: 975–1000. [Google Scholar] [CrossRef]

- Sokhanvar, Amin. 2019. Does foreign direct investment accelerate tourism and economic growth within Europe? Tourism Management Perspectives 29: 86–96. [Google Scholar] [CrossRef]

- Stats SA (Statistics South Africa). 2022. Quarterly labour force survey: Quarter 1; Pretoria: Government Printer. Available online: https://www.statssa.gov.za/publications/P0211/P02111stQuarter2021.pdf (accessed on 29 September 2022).

- Wörgötter, Andreas, and Zuzana Brixiova. 2019. Monetary unions of small currencies and a dominating member: What policies work best for benefiting from CMA? Journal of Development Perspectives 3: 13–28. [Google Scholar] [CrossRef]

- World Bank Development Indicators. 2022. Available online: https://databank.worldbank.org/source/world-development-indicators/.aspx?source=2&series=IQ.CPA.BREG.XQ (accessed on 12 October 2022).

- Yingi, Edwin. 2022. Beyond the pandemic: Implications of COVID-19 on regional economic integration in Southern Africa. International Journal of Research in Business and Social Science (2147–4478) 11: 270–79. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Lag | LogL | LR | FPE | AIC | SC | HQ |

|---|---|---|---|---|---|---|

| 0 | 197.3920 | NA | 2.82 × 10−9 | −2.658222 | −2.534480 | −2.607941 |

| 1 | 927.5774 | 1389.381 | 1.84 × 10−13 | −12.29969 | −11.43349 | −11.94771 |

| 2 | 1096.575 | 307.4821 | 2.90 × 10−14 | −14.14688 | −12.53823 | −13.49321 |

| 3 | 1228.303 | 228.6946 | 7.72 × 10−15 | −15.47643 | −13.12533 | −14.52108 |

| 4 | 1588.826 | 595.8636 * | 8.62 × 10−17 * | −19.98369 * | −16.89014 * | −18.72665 * |

| Com | Skewness | Kurtosis | Jarque–Bera | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Skew | Chi-sq | Df | Prob | Kurtosis | Chi-sq | Df | Prob | Chi-sq | Df | Prob | |

| 1 | 0.0749 | 8.0213 | 1 | 0.3247 | 4.7432 | 5.4356 | 1 | 0.8294 | 7.5438 | 2 | 0.7382 |

| 2 | −4.0987 | 3.5021 | 1 | 0.9823 | 6.7854 | 5.1245 | 1 | 0.6959 | 8.7659 | 2 | 0.3521 |

| 3 | 0.6548 | 2.6749 | 1 | 0.4325 | 8.7630 | 6.2321 | 1 | 0.2998 | 6.8765 | 2 | 0.7694 |

| 4 | −3.7654 | 3.2325 | 1 | 0.6329 | 2.6574 | 2.4327 | 1 | 0.9432 | 8.3478 | 2 | 0.5439 |

| 5 | −1.8765 | 3.5237 | 1 | 0.7322 | 4.2109 | 8.2319 | 1 | 0.7320 | 6.7845 | 2 | 0.3098 |

| 6 | −3.0789 | 6.4122 | 1 | 0.9654 | 2.5470 | 3.2359 | 1 | 0.8120 | 5.3298 | 2 | 0.2754 |

| Joint | 4.6544 | 6 | 0.2134 | 3.9750 | 6 | 0.5450 | 7.3294 | 12 | 0.4329 | ||

| Null: There Is No Serial Correlation | ||

|---|---|---|

| Lags | LM-Stat | Prob |

| 1 | 132.7654 | 0.2978 |

| 2 | 320.7021 | 0.3290 |

| 3 | 129.5780 | 0.4329 |

| 4 | 321.2134 | 0.5482 |

| 5 | 128.6520 | 0.7429 |

| 6 | 273.4376 | 0.4321 |

| Null: There Is No Heteroscedasticity | ||

|---|---|---|

| Chi-sq | Df | Prob. |

| 5738.214 | 412 | 0.7542 |

| Block Exogeneity Wald Tests | ||||

|---|---|---|---|---|

| Null: There Is No Granger Causality | ||||

| Dependent Variable: RGDP_G | ||||

| Excluded | Chi-sq | Df | Prob | Decision |

| COMM_PRICES | 45.53247 | 3 | 0.0001 | Null rejected |

| SA_REPO | 32.32897 | 3 | 0.0000 | Null rejected |

| INF | 158.8709 | 3 | 0.0000 | Null rejected |

| MS | 62.21874 | 3 | 0.0000 | Null rejected |

| LRATE | 18.82309 | 3 | 0.0005 | Null rejected |

| All | 238.1297 | 15 | 0.0002 | Null rejected |

| Period | Standard Error | COMM_PRICES | SA_REPO | RGDP_G | INF | MS | LRATE |

|---|---|---|---|---|---|---|---|

| (a) Variance decomposition of COMM_PRICES; | |||||||

| 3 | 0.127 | 93.065 | 1.387 | 0.882 | 1.538 | 0.155 | 2.973 |

| 6 | 0.148 | 91.643 | 3.239 | 1.723 | 1.653 | 0.573 | 1.169 |

| 9 | 0.172 | 90.267 | 1.564 | 3.521 | 3.143 | 0.255 | 1.250 |

| 12 | 0.177 | 90.013 | 2.126 | 2.124 | 2.537 | 0.674 | 2.526 |

| (b) Variance decomposition of SA_REPO; | |||||||

| 3 | 0.212 | 1.480 | 96.538 | 0.159 | 0.166 | 1.630 | 0.027 |

| 6 | 0.344 | 1.659 | 91.978 | 0.762 | 1.288 | 1.733 | 2.580 |

| 9 | 0.472 | 1.456 | 90.179 | 1.538 | 1.376 | 1.439 | 4.012 |

| 12 | 0.585 | 1.861 | 88.364 | 2.176 | 2.004 | 1.173 | 4.422 |

| (c) Variance decomposition of RGDP_G; | |||||||

| 3 | 0.571 | 6.217 | 40.784 | 42.829 | 4.349 | 2.277 | 3.544 |

| 6 | 0.594 | 7.370 | 52.143 | 32.689 | 2.569 | 1.533 | 3.696 |

| 9 | 0.691 | 7.179 | 50.027 | 32.289 | 3.886 | 2.573 | 4.046 |

| 12 | 0.888 | 7.632 | 46.638 | 36.446 | 2.348 | 2.883 | 4.053 |

| (d) Variance decomposition of INF; | |||||||

| 3 | 0.847 | 12.422 | 11.378 | 7.861 | 62.009 | 3.651 | 2.679 |

| 6 | 0.328 | 24.829 | 6.986 | 6.143 | 56.153 | 2.222 | 3.667 |

| 9 | 0.986 | 28.898 | 7.828 | 5.879 | 51.621 | 2.184 | 3.590 |

| 12 | 0.587 | 29.976 | 7.975 | 5.544 | 50.549 | 2.765 | 3.191 |

| (e) Variance decomposition of MS | |||||||

| 3 | 0.076 | 1.027 | 37.602 | 8.231 | 5.828 | 35.988 | 11.324 |

| 6 | 0.950 | 2.486 | 37.002 | 8.244 | 5.769 | 34.042 | 12.457 |

| 9 | 0.574 | 3.575 | 38.246 | 5.873 | 5.984 | 35.768 | 10.554 |

| 12 | 0.682 | 3.273 | 37.824 | 7.829 | 8.724 | 32.873 | 9.477 |

| (f) Variance decomposition of LRATE | |||||||

| 3 | 0.247 | 8.853 | 76.231 | 0.678 | 0.787 | 2.861 | 10.590 |

| 6 | 0.548 | 9.207 | 73.647 | 1.748 | 3.472 | 1.219 | 10.707 |

| 9 | 0.576 | 9.631 | 66.482 | 2.032 | 5.465 | 2.808 | 13.582 |

| 12 | 0.583 | 9.826 | 67.233 | 2.535 | 5.932 | 4.624 | 9.850 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shumba, T.; Mukorera, S. Monetary Policy Implications on Macroeconomic Performance in the Common Monetary Area: A Panel-SVAR Framework. Economies 2023, 11, 144. https://doi.org/10.3390/economies11050144

Shumba T, Mukorera S. Monetary Policy Implications on Macroeconomic Performance in the Common Monetary Area: A Panel-SVAR Framework. Economies. 2023; 11(5):144. https://doi.org/10.3390/economies11050144

Chicago/Turabian StyleShumba, Theron, and Sophia Mukorera. 2023. "Monetary Policy Implications on Macroeconomic Performance in the Common Monetary Area: A Panel-SVAR Framework" Economies 11, no. 5: 144. https://doi.org/10.3390/economies11050144

APA StyleShumba, T., & Mukorera, S. (2023). Monetary Policy Implications on Macroeconomic Performance in the Common Monetary Area: A Panel-SVAR Framework. Economies, 11(5), 144. https://doi.org/10.3390/economies11050144