1. Introduction

The objectives of this article are two-fold: (i) to analyze the growth of potential output per worker, as well as the changes in the output gap per worker in the EA-12 MS net contributors and net recipients of the European Union (EU) budget, and (ii) to explore the existence of hysteresis or long-lasting effects of shocks within the specified member states (MS). To this end, we employ an innovative empirical approach that integrates the analysis of both growth and cycles.

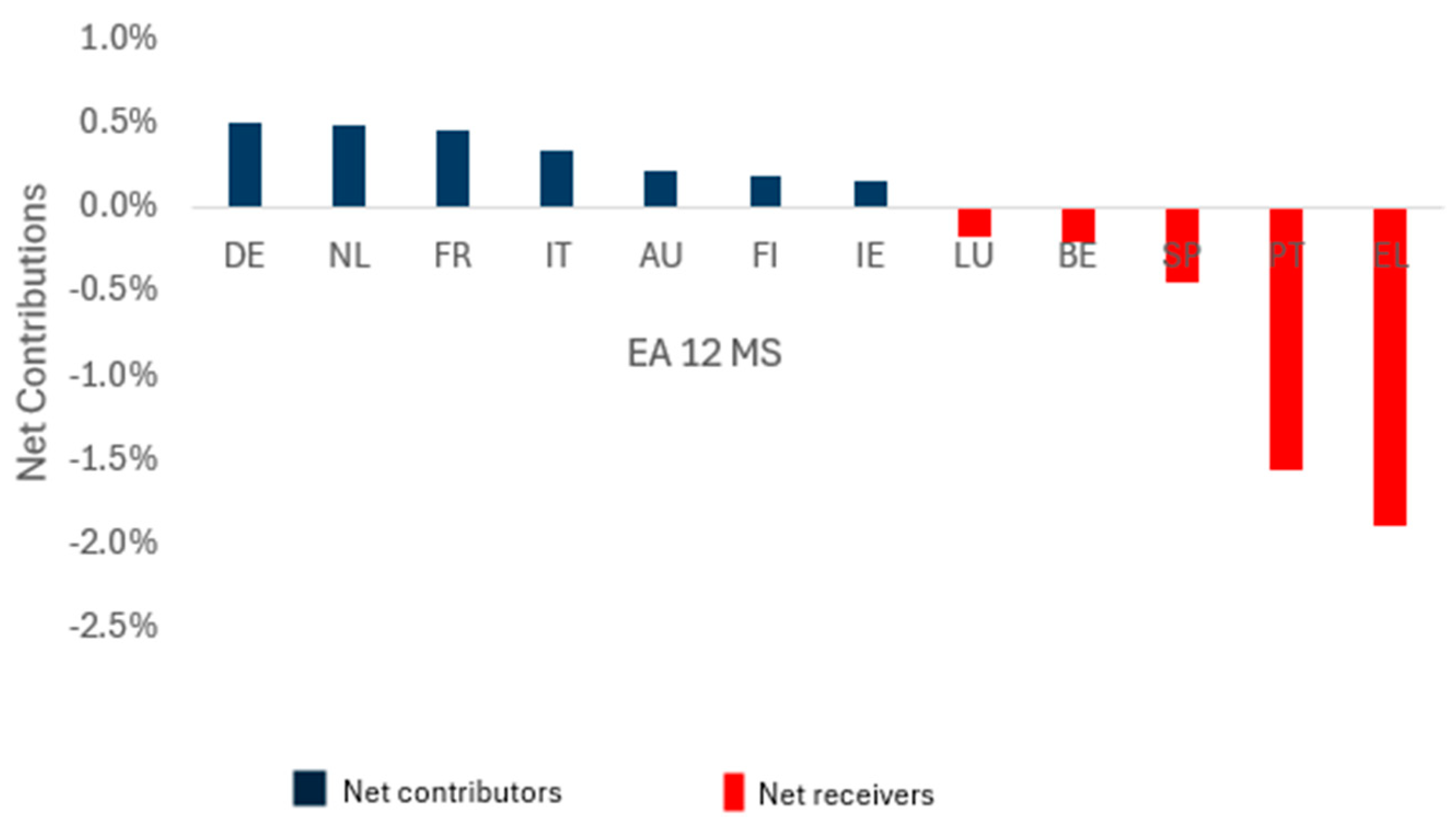

Figure 1 illustrates which of the EA-12 Member States were, on average, net contributors and net recipients of the EU budget, with net contributions expressed as a percentage of their Gross Domestic Product (GDP) during the analyzed period. In order of contribution, Germany, the Netherlands, France, Italy, Austria, Finland, and Ireland were net contributors, while Luxembourg, Belgium, Spain, Portugal, and Greece were net recipients. This order will be considered in the analysis carried out. Its significance lies in the fact that, since the 2008 Global Financial Crisis (GFC), MS that have contributed the most to the EU budget—notably Germany and the Netherlands—have begun to question their net contributions and have elevated this issue to the forefront of the European debate.

We used the SURE model to estimate a translog production frontier (

Christensen et al. 1973) and an equation that captures the impacts of lagging output gaps on potential output, for each of the economies under analysis, in the period from 1998 to 2022, in first differences, with quarterly data filtered through the Kalman filter. The Seemingly Unrelated Regression Equations (SURE) model was utilized in the estimation, because the 12 MS belong to the EA-12 and, thus, we expect the error terms to be correlated across equations.

The empirical approach adopted enables us not only to decompose actual and potential output growth per worker into their latent components, but also to accommodate Cerra and Saxena’s new stylized fact of the business cycle (

Cerra and Saxena 2008,

2017;

Cerra et al. 2023). The new stylized fact posits that, on average, all types of recessions lead to permanent output losses. This results in a downward shift in the GDP trend and permanently reduces the country’s potential output or productive capacity. Such findings imply the existence of hysteresis or lasting impacts of temporary shocks on the trajectory of the economy.

Dosi et al. (

2018) and

Cerra et al. (

2023) have undertaken extensive research on hysteresis, its dynamics, and its implications for economic growth and business cycles.

Dosi et al.’s (

2018) research illuminates the intricate interplay among firms, workers, and macroeconomic variables. They emphasized the critical importance of understanding hysteresis for designing effective economic policies. In their interpretation, hysteresis arises from the heterogeneous and nonlinear responses of a system characterized by multiple equilibria or path-dependent trajectories. The authors identified coordination failures and persistent effects of aggregate demand on productivity as the primary sources of long-term jumps across multiple growth trajectories. By revealing the intricate dynamics among various macroeconomic variables, they challenged the conventional view that rigid labor markets exacerbate hysteresis. Instead, they highlighted that sustaining aggregate demand during severe downturns can mitigate hysteretic dynamics.

In their literature review,

Cerra et al. (

2023) identified the development of an alternative business cycle model over the past 25 years. In this model, GDP is history-dependent, and all shocks can have permanent or scarring effects on output—a phenomenon referred to as hysteresis. In the presence of endogenous growth, hysteresis naturally emerges in many business cycle models. To mitigate the scarring effects of shocks, the authors asserted that aggressive and swift action during recessions becomes the optimal policy. However, during expansions, the cost of acting too early due to fears of inflationary pressure can be detrimental, potentially hindering positive developments in the labor market or reducing the economy’s growth potential.

Since 2008, the EU and Euro Area (EA) have been experiencing significant shocks, including the 2008 GFC, the 2020 COVID-19 pandemic, the 2022 Russia–Ukraine war escalation, and the 2023 Israel–Hamas war.

Barro and Ursúa (

2008) ranked macroeconomic disasters since 1870. If the crisis induced by the 2020 COVID-19 pandemic and the policy response to it were anything like what happened with the 1918 Spanish Flu pandemic, referred to by the authors, the world economy would have experienced one of the worst recessions to date. However, this time was different in the EU and the EA, particularly in terms of the policy reaction to the 2020 COVID-19 pandemic. The EU and EA were still recovering from the 2008 GFC when the 2022 Russian invasion of Ukraine occurred. This hit Germany particularly hard, considering the country’s energy dependence on Russia, and brought by itself inflation to the EU and the EA. That is, this war and the financial speculation related to it have, at least in part, contributed to the latest inflation crisis in the EU and EA. The Israel–Hamas conflict in the Middle East also holds the potential to trigger inflation in the EU and the EA.

This article unfolds as follows. Following this introductory section,

Section 2 addresses the ongoing neoclassical debate on hysteresis. It is followed by

Section 3, which discusses the effects and expected effects found in the literature of the main shocks suffered by the EA in the period under analysis.

Section 4 presents the empirical model and data, while

Section 5 yields and discusses the results. Finally,

Section 6 concludes the article.

2. The Ongoing Neoclassical Debate Regarding Hysteresis

The disagreement among neoclassical macroeconomists is not new. The New Neoclassical Synthesis (NNS,

Goodfriend and King 1997) assumes that demand-side shocks, namely monetary policy, lead to temporary short-term fluctuations in actual GDP around its long-term trend, the effects of which on growth dissipate after some time. The long-term trend is seen as the economy’s production capacity over time, corresponding to the potential or frontier output, which can only be changed by supply-side factors (

Lucas 2003). Consequently, the autonomous nature of variations in the trend should not be mistaken for movements along the short-term supply curve itself, as the latter are simply outcomes of present or past changes in aggregate demand (

Gordon 1984). However,

Campbell and Mankiw (

1987), along with

Blanchard and Quah (

1989), questioned this perspective.

Campbell and Mankiw (

1987) investigated the dynamics of economic fluctuations, with a specific focus on differentiating between the permanent and transitory components of real Gross National Product (GNP) fluctuations. Based on post-war quarterly data, the authors found it challenging to refute the notion that real GNP behaves like a persistent random walk with drift. This suggests that shocks to output have a significant and lasting impact, rather than being purely transitory.

Blanchard and Quah (

1989) explored the intricate relationship between economic fluctuations, focusing on aggregate demand and supply shocks. They distinguished between supply disturbances (with a permanent effect on output) and demand disturbances (with a transitory effect). The authors acknowledged that quantifying the individual contributions of these disturbances remains challenging. Moreover, their research underscores the critical importance of comprehending the intricate interplay between demand and supply for effective economic policymaking and skillfully managing fluctuations.

The New Keynesian variant of Dynamic Stochastic General Equilibrium (DSGE) models of the business cycle, which has served as the cornerstone for many central banks’ analyses, assumes that temporary shocks, whether affecting demand or supply, do not impact the productive capacity of the economy. Notable examples of these models include works by

Clarida et al. (

1998),

Blanchard and Galí (

2007), and

Avouyi-Dovi and Sahuc (

2016). The 2008 GFC and the 2020 COVID-19 pandemic have raised questions about their empirical validity and highlighted the presence of hysteresis.

The concept of hysteresis has played a central role in contemporary economic discourse. At its core, hysteresis challenges traditional economic logic, as emphasized by

Blanchard and Summers (

1986), who examined the persistent effects of economic shocks on the trajectory of unemployment. They highlighted that such equilibria may be unstable and fragile, pointing to the complexities inherent in unemployment dynamics.

Expanding upon these perspectives, empirical research by

Ball and Onken (

2022) provides evidence of hysteresis dynamics across a diverse set of Organization for Economic Cooperation and Development (OECD) countries. Their findings revealed that deviations from the natural rate of unemployment have lasting effects, with decreases in unemployment exhibiting larger long-term impacts. This empirical validation echoes

Ball’s (

2009) argument that hysteresis fundamentally shapes the long-term behavior of unemployment, particularly in response to shifts in aggregate demand. Moreover, the comprehensive analysis by

Cerra et al. (

2023) underscores the broader interplay between economic growth, business cycles, and hysteresis effects. Advocating for a unified analytical framework, their research emphasized the need to integrate the persistent impact of shocks on GDP levels into economic models. By highlighting the critical role of active monetary and fiscal policies in mitigating the enduring scars of economic downturns, while leveraging expansions to yield lasting positive effects,

Cerra et al.’s (

2023) findings provide valuable insights for policymakers grappling with economic stabilization efforts.

Beyond the realm of unemployment,

Blanchard et al. (

2015) delved into how prolonged recessions can fundamentally alter the trajectory of an economy. This analysis emphasized the imperative of integrating hysteresis effects into macroeconomic frameworks to better understand and address economic fluctuations.

Similarly,

Vines and Wills (

2018) contributed to the discussion by examining structural factors contributing to hysteresis. Through their research, they proposed targeted policy interventions aimed at mitigating hysteresis’s adverse effects on long-term economic performance. Their recommendations underscore the need for a comprehensive reevaluation of core economic models, incorporating heterogeneity to foster economic stability and growth.

Moreover,

Ball (

2014) delved into the implications of hysteresis within the context of monetary and fiscal policies, illustrating how such policies can influence long-term economic dynamics. The persistence of economic downturns, caused by hysteresis effects, can lead to enduring challenges, such as elevated unemployment rates or reduced productive capacity. Various monetary and fiscal policy tools, such as interest rate adjustments or government spending initiatives, can impact these long-term economic dynamics. For instance, monetary policies or targeted fiscal stimulus measures help mitigate the effects of hysteresis by stimulating demand and promoting economic recovery. Overall,

Ball’s (

2014) research sheds light on the role of monetary and fiscal policies in addressing the long-term consequences of hysteresis-induced economic downturns.

Ioannides and Pissarides (

2015) delved into the intricacies of the Greek crisis, labor market dynamics, and the impact of hysteresis on employment levels. They contended that Greece’s economic challenges arise from both supply-side and demand-side factors, issues that have persisted since Greece’s accession to the EU in 1981. Throughout the Greek crisis, the sharp decline in demand has been particularly pronounced, exacerbated by austerity measures and wage reductions. These not only compound the demand-side difficulties faced by the Greek economy but also aggravate its underlying structural supply challenges. Additionally, the timing of labor market reforms has played a role in contributing to the crisis. The authors underscore the importance of adopting a balanced approach to tackle both supply and demand issues within the Greek economy.

Yellen (

2017) provided valuable insights into hysteresis within monetary policy and uncertainty. The forces driving inflation in the US economy remained uncertain, and the low inflation was likely reflecting factors whose influence should fade over time. However, there were several uncertainties associated with her assessment. Downward pressures on inflation could unexpectedly persist, and the strength of the labor market, inflation expectations, and fundamental forces driving inflation may have been misjudged. Moreover, the persistent low inflation in the US at the time, despite the improvement in labor market conditions, limited the scope for easing monetary policy during normal times.

Costa et al. (

2021) employed a vector autoregression (VAR) model to analyze the relationship between the output gap and potential output in Germany and Portugal. Their study illuminated the lasting effects of shocks on potential output within distinct economic contexts. Notably, they explored how country-specific factors, such as business cycle volatility, can influence hysteresis dynamics. Specifically, they discovered that the amplitude of the business cycle and the persistence of shocks are greater in the Portuguese economy than in the German one. The insights gleaned from their analysis provide crucial information for policymakers, enabling them to devise targeted interventions that mitigate adverse effects and promote economic recovery.

Tervala (

2021) extended the New Keynesian model to incorporate hysteresis. Hysteresis implies that recessions reduce the level of potential output. Contrary to

Lucas (

2003), who argued that the welfare costs of business cycles are negligible without hysteresis, Tervala demonstrated that the welfare costs of recessions are significant when hysteresis is considered.

Tervala and Watson (

2022) analyzed the output and welfare multipliers of fiscal stimulus during a recession. Transfer payments, public consumption, and investment all have high output and welfare multipliers due to their positive effects on total factor productivity (TFP) in a recessionary environment. Public investment, in particular, has the highest output and welfare multipliers because it positively impacts labor productivity through an increase in the public capital stock. Policymakers should consider these factors when designing effective fiscal stimulus measures during economic downturns. Understanding hysteresis’s impact on welfare costs and the effectiveness of fiscal policies during recessions is crucial for informed policy decisions and societal wellbeing.

The new stylized fact from

Cerra and Saxena (

2008,

2017) and

Cerra et al. (

2023) asserts that, on average, all types of recessions lead to permanent output losses. This implies that short-term, temporary shocks have lasting effects on the economy in the long term, rather than being neutral. Such findings provide strong support for the existence of hysteresis.

Cerra and Saxena (

2008) examined the role of fiscal and monetary policies in either reversing or perpetuating economic shocks, shedding light on the dynamics of hysteresis. Using panel data from a diverse set of countries (including high-income, emerging market, developing, and transition countries), the authors revealed compelling evidence that substantial output losses resulting from financial crises and specific types of political crises tend to be remarkably persistent. While there is no significant rebound for these crises, they observed that civil wars exhibited a partial recovery in output. In summary, civil wars follow a distinctive recovery trajectory compared to other crises.

Blanchard (

2016) reexamined the behavior of inflation and unemployment. Inflation expectations have become steadily more anchored. The Phillips Curve has become flatter, with a larger standard error when compared with the low level of inflation. This uncertainty poses challenges for the conduct of monetary policy. Blanchard’s findings underscore the evolving dynamics of inflation and unemployment and highlight the complexities policymakers face in navigating these phenomena effectively.

Romer’s (

2016) paper primarily critiqued the field of neoclassical macroeconomics. He contended that the discipline has stagnated over the past three decades, regressing in its ability to understand economic reality. The author argued that the methods and conclusions in contemporary neoclassical macroeconomics no longer qualify as scientific research. In his analysis, he sheds light on issues concerning identification within macroeconomic models and raises doubts about the reliability of responses to fundamental inquiries. Notably, Romer questions whether the Federal Reserve possesses the capacity to influence the actual federal funds rate.

Romer’s (

2016) insights prompt policymakers and experts to reevaluate the state of neoclassical macroeconomics and consider alternative approaches in the field.

As a corollary to the literature discussed above, and in contrast to Lucas’ assertions in 2003, the benefit of employing demand-side countercyclical macroeconomic policies to mitigate cyclical output fluctuations is not insignificant. These policies can effectively reduce permanent output losses resulting from recessions, thereby positively influencing the pace of economic recovery.

However, the COVID-19 pandemic in 2020 had the potential to directly impact the economy’s supply (as highlighted by

Cerra et al. 2023). For instance, it disrupted global supply chains and led to layoffs of workers. Similarly, the escalation of the Russia–Ukraine war in 2022 and the Israel–Hamas war in 2023, which are still ongoing, also directly impact the economy’s supply.

In summary, hysteresis in macroeconomics refers to the long-lasting effects of shocks, even when the factors that initially caused the shocks have been removed or resolved. This challenges the assumption of rapid economic recovery after shocks. For instance, after an economic downturn (such as a recession) has technically ended, the unemployment rate may continue to rise. Workers who lose their jobs during a recession may be less employable, even when the economy recovers.

Hysteresis can also emerge due to shifts in market participants’ attitudes following extreme events, such as financial crises, pandemics, and wars. For instance, after a stock market crash, investors may exhibit reluctance to reinvest due to recent losses. This phenomenon can result in prolonged periods of depressed stock prices, influenced more by investor sentiment than fundamental market factors, ultimately affecting long-term growth trajectories. Similarly, consumer spending patterns may bear the scars of past economic shocks, impacting the overall dynamics of demand and supply.

Hysteresis has policy implications. Policymakers must recognize that economic shocks can have lasting impacts beyond their immediate occurrence. Labor market policies should address long-term unemployment and skill loss. Monetary and fiscal policies need to account for the potential persistence of economic downturns. Therefore, when designing these policies, considering hysteresis effects is crucial.

Finally, hysteresis underscores the need for nuanced modeling that captures both short-term and long-term effects. It calls for a unified analysis of growth and cycles.

5. Results and Discussion

5.1. Potential and Actual Output per Worker

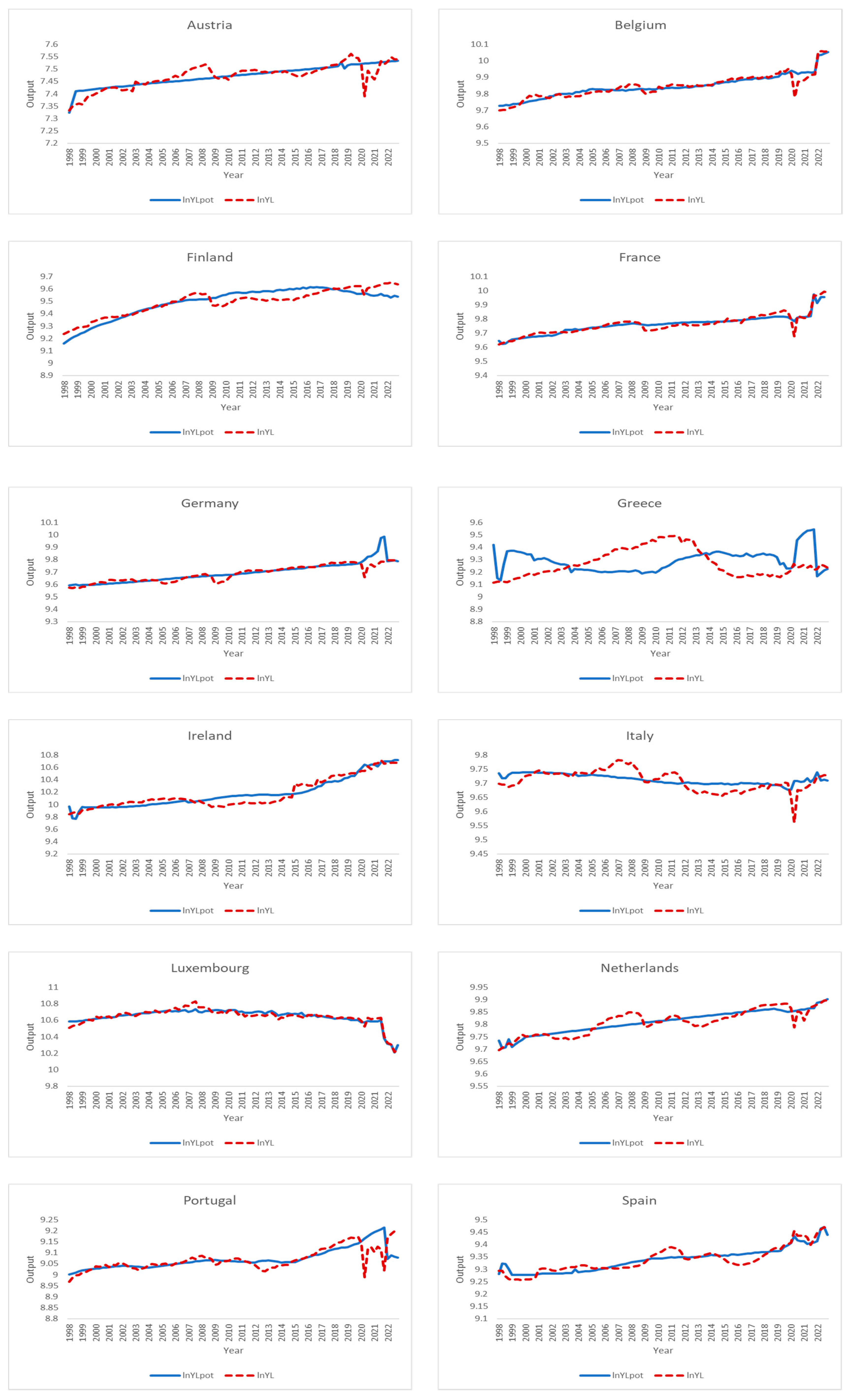

Figure 3 depicts the natural logarithms of potential and actual output per worker for all EA-12 economies, in the period 1998–2022.

There are several impressive factors revealed in

Figure 3. Italy has seen a steady decline in its potential output per worker since the country adopted the Euro, a situation that was not changed with the 2008 GFC. Greece recorded a decline in potential output per worker and, after 2010, an increase, followed by stagnation. All other countries recorded an increase in their potential output per worker, with Ireland and Portugal improving in their increase after implementation of quantitative easing by the ECB, in 2015.

As expected, actual output per worker was more volatile than potential output per worker, with the output gap per worker being sometimes positive and other times negative.

Costa et al. (

2021) found that the amplitude of the business cycle and the persistence of shocks were higher in the Portuguese economy than in the German one. We obtained the same result regarding Germany and Portugal, but we cannot say that the amplitude of the business cycle and the persistence of shocks were necessarily higher in EA-12 MS that are net recipients of the EU budget than they were in EA-12 MS that are net contributors of the EU budget. Germany and France, the two larger economies of the EA-12, seem to have a business cycle with lower amplitude and persistence of the shocks than the other EA-12 MS, while the opposite occurs with Greece, followed by Italy. In Portugal, it is noteworthy that austerity pursued in the EA as a response to the 2008 GFC had a higher impact as a negative shock than the 2008 GFC itself.

Still looking at actual output per worker, the impacts of the COVID-19 pandemic are visible, proving to be more severe than the 2008 GFC in most EA-12 MS. MS relying heavily on the tourism sector, such as Portugal, were severely hit by the COVID-19 pandemic.

5.2. SURE Model Estimation Results, Partial Output Elasticities, and Allen Input Substitution Elasticities

Equations (3) and (4) were simultaneously estimated for all the EA-12 economies using the SURE model.

Table 1 and

Table 2 show the estimation results.

The explanatory power of the estimated SURE model in first differences was high. Most of the coefficients were also significant in the second equation (which corroborates the existence of hysteresis). The latter coefficients are elasticities that indicate the percentage increase in potential output when the lagging ratios of actual output to potential output increase by one percent. It is important to note that these lagging ratios can be either less than or greater than one, depending on the MS, which may explain the different signs of the coefficients found in the various MS and lagging periods.

With the empirical approach employed in this research, it is feasible to compute other elasticities mentioned in the literature (see

Tervala 2021).

Table 3 illustrates the partial potential output and Allen input substitution elasticities for the period 1998–2022, evaluated at the sample mean. Regarding the estimated results, it is worth noting that Luxembourg stands out as an outlier. Consequently, we present the results for this country separately, excluding it from the calculation of average net recipients in

Table 3 and throughout the article, as well as from the discussion of the results.

The partial potential output with respect to physical (human) capital elasticity, εk (εh), quantifies how responsive the potential output is to variations in the trend of physical (human) capital. The Allen elasticity of substitution between trends of physical and human capital (σhk) quantifies the extent to which these two production factors can be substituted for or complement each other. EA-12 MS net contributors and net recipients of the EU budget had, on average, similar elasticities. Except for Austria, εk was always higher than εh. Concerning σhk, it was positive in all EA-12 economies, showing substitution between physical capital and human capital in all of them.

Regarding physical capital, France stood out with the highest positive εk (0.66), indicating that a 1% increase in the trend of physical capital resulted in an increase in potential output of 0.66%. In contrast, Greece exhibited the lowest εk value (0.21), indicating that a 1% increase in the trend of physical capital led to an increase in potential output of 0.21%. These findings highlight the substantial variation in the impact of the trend of physical capital on potential output among the EA-12 MS, even within those that are net contributors and net recipients of the EU budget.

Concerning human capital, Austria boasted the highest εh value (0.52), signifying that a 1% increase in the trend of human capital resulted in a 0.52% increase in potential output. In stark contrast, Greece exhibited the lowest εh (0.18), suggesting that a 1% increase in the trend of human capital led to a 0.18% increase in potential output. These findings echo the significant variation in the impact of the trend of human capital on potential output among EA-12 MS, even within net contributors and net recipients of the EU budget.

When it comes to the substitution between the trends of physical and human capital, Germany exhibited the highest positive value of σhk (0.69), suggesting a relatively strong likelihood of substitution between these two factors. Conversely, the Netherlands exhibited the lowest value of σhk (0.16), suggesting weaker possibilities of substitution between physical and human capital compared to Germany. These findings underscore that the degree of substitution between trends of physical and human capital varies significantly across EA-12 economies, even within MS that are net contributors and those that are net recipients of the EU budget.

In summary, the elasticity values revealed diverse responsiveness in potential output to changes in trend input factors across the EA-12 MS. Interestingly, this heterogeneity persisted even within MS net contributors and net recipients of the EU budget. The varying magnitudes of these elasticities underscore the distinct effects of trends of physical and human capital on potential output, as well as the degree of substitution between these production factors within the EA-12 MS.

5.3. Output Gap and Returns to Scale Rankings

Table 4 presents two rankings of the EA-12 MS, respectively, based on the output gap and returns to scale. The output gap and returns to scale for each MS are average values computed for the entire period (1998–2022).

Once again, the heterogeneity of values goes beyond the division between MS net contributors and net recipients of the EU budget. The output gap measures the difference between actual output per worker and potential output per worker as a percentage of the latter, reflecting the level of demand observed in relation to installed capacity, while returns to scale assess changes in potential output in response to proportional changes in trend inputs. In terms of the output gap, Finland led the ranking, with a positive value of 0.24%. Portugal, the Netherlands, Ireland, Italy, Greece, and Germany presented negative output gaps. Concerning these MS, Germany’s leadership in terms of output gap magnitude can be explained by the fact that the country relies heavily on external demand. In terms of returns to scale, Spain stood out with the highest value (1.06) and Greece with the lowest (0.39), with Spain (1.06) and Finland (1.05) presenting increasing returns to scale.

5.4. The Decomposition of Growth

Table 5 and

Table 6 show the decomposition of growth in potential and actual output per worker by MS and groups of MS. The average values were computed for the period 1998–2022.

The average quarterly growth rates of potential and actual output per worker exhibited significant variations among EA-12 MS, which go beyond the division between net contributors and net recipients of the EU budget. Nonetheless, as a group and on average, EA-12 MS net contributors of the EU budget have grown more in terms of potential output per worker (0.30%) than EA-12 MS net recipients in the period (0.14%), with both groups of countries having small output gap changes (0.02% and 0.08%, respectively). Ireland, Finland, and France are the MS with the highest growth rates, while Greece, Portugal, and Spain are the MS with the lowest growth rates. In Greece, the average quarterly growth rate of potential output per worker was negative in the period (−0.05%).

Looking at the decomposition of potential output growth by EA-12 MS, net contributors of the EU budget showed a positive TFP change (1.84%), while for net recipients of the EU budget, the TFP change was negative (−0.33%). This is mainly explained by technical change (0.85% and −0.19%, respectively). The scale effects were negative for both groups of countries (−0.08% and −0.14%, respectively).

TFA change was positive for both groups of economies, being smaller for MS net contributors of the EU budget than for MS net recipients (1.35% and 1.84%, respectively), with less accumulation of both the trend of physical capital (1.24% and 1.69%, respectively) and the trend of human capital (0.11% and 0.16%, respectively).

Finally, the random shocks component, on average, negatively affected the growth in potential output of EA-12 MS net contributors and net recipients of the EU budget (−1.82% and −1.38%, respectively). It is important in magnitude, but barely explained by lagging output gaps.

6. Conclusions

The objectives of this article were: (i) to analyze the growth of potential output per worker, as well as the changes in the output gap per worker in the EA-12 MS net contributors and net recipients of the EU budget, and (ii) to explore the existence of hysteresis or long-lasting effects of shocks within the specified MS. To this end, we employed an innovative empirical approach that integrates the analysis of both growth and cycles.

A SURE model was employed to estimate a translog production frontier and to analyze the impacts of lagging output gaps on potential output per worker for each of the EA-12 MS. This was achieved using quarterly data, filtered through the Kalman filter, over the period spanning from 1998 to 2022. The model was estimated in first differences.

The results confirmed the existence of hysteresis, but the impact of a lagging output gap on potential output appeared to be minimal. Additionally, they revealed a pronounced degree of heterogeneity across the EA-12 economies. This heterogeneity transcends the binary classification of MS net contributors and net recipients of the EU budget, manifesting itself within each of these two groups in terms of the business cycle, potential output per worker, potential output partial elasticities, Allen input substitution elasticities, output gaps, returns scale, the decomposition of growth, and hysteresis.

Despite the heterogeneity across EA-12 MS within each of the two groups, TFP change, specifically technical change, played a more prominent role in explaining potential output per worker growth in EA-12 MS that are net contributors to the EU budget than in MS that are net recipients. Conversely, TFA change, particularly physical capital accumulation, was more influential in explaining potential output per worker growth in EA-12 MS that are net recipients of the EU budget than in MS that are net contributors. These specific results seem to reflect the budgetary stance of each MS group and the utilization of European funds by net recipients of the EU budget.

The observed heterogeneity across the EA-12 MS also raised important questions regarding the effectiveness of the one-size-fits-all monetary policy approach adopted by the ECB. A singular monetary policy is hardly adequate to address the varying needs and challenges faced by each MS, as their economies possess different structural characteristics and respond differently to the same monetary measures. Consequently, there arises a need for the ECB to adopt a more tailored approach—one that recognizes and accommodates the unique economic circumstances of individual EA MS. Such a customized approach may require not only the use of unconventional monetary policy, but also the incorporation of fiscal policy within the context of a complete EA.

This research has limitations. The results may be sensitive to the Kalman filter employed. For sensitivity analysis regarding the filter, an alternative filter that is widely used in the literature, despite its limitations, is the Hodrick–Prescott (HP) filter.

The choice of functional form for the production frontier can also influence the results. While the translog functional form is widely used in frontier literature due to its flexibility, it necessitates estimating a substantial number of parameters. This requirement is particularly challenging with a limited sample size. Since our results point toward the substitution of inputs, an alternative functional form worth exploring is the Constant Elasticity of Substitution (CES) production function, which is widely used in the production function literature. It offers some flexibility while potentially overcoming the parameter estimation issue.

Similar to common practice in the production function literature, we can enhance our estimation of each MS production frontier within the SURE framework by incorporating additional equations and/or imposing specific restrictions that provide more information for model estimation.

Finally, our results may be sensitive to both the sample size and the number of considered MS. Although the MS of the EU are not necessarily part of the EA, the single market connects them. To enhance our analysis, we could extend the time period from 1995 to 2022, including all EA-12 MS as well as Denmark and Sweden. The latter are two MS that did not adopt the Euro.

{kind=link}

{kind=link}

{kind=link}