There exist

n clubs from a total of

N clubs in a league (

n ≤

N), indexed by 1, …,

n, bidding to purchase a single player from a single seller (the Japanese club). Each buyer places a private valuation,

vi, on the player ideally equal to the player’s discounted lifetime marginal revenue product for the club

4. We abstract from any strategic value contained in

vi that arises from preventing other clubs from signing the player. For a given player for sale, the distribution of valuations is assumed to be uniform with unknown upper and lower limits. We denote the highest private valuation as

. The position of a specific club’s valuation within the distribution is not known. We assume that the ordering of private valuations is independent of the type of auction (collusive or non-collusive) and that the attributes of the player to be sold that determines each

vi can be obtained at zero cost. The seller places a minimum reserve price of

Rmin on the player so that any bid below this price will not be successful. This reserve price is ideally determined by the surplus value from the player by remaining in Japan. Bidders do not know the value of

Rmin, instead they must form its expectation denoted as

, using an information set that is identical for all bidders. We assume that expectations are formed rationally, so that the relationship between

Rmin and its expectation is given by

, where

.

Losing bidders suffer an externality that we assume is different for each losing bidder. The magnitude of the externality is assumed to increase the greater is the value of

vi for the winning bidder. This is appropriate due to presence of diminishing marginal revenue product with each club’s winning percentage. This is a standard feature of models of professional sports clubs, beginning with

Rottenberg (

1956). The nature of sporting contests is that for one club to be more successful, others must be less successful. Clubs that lose contests move down their concave revenue schedules at increasing rates and the externality becomes larger.

For now, we assume an auction without side payments. Without a side payment (revenue sharing), all losing bidders will prefer that the player not be sold. The winning bidder will obtain a net profit of , where is the amount of the winning bid in the non-collusive auction and is the salary paid to the player. Any losing bidder incurs a loss equal to the monetary value of the negative externality imposed on it (it might win fewer games). A higher anticipated salary will lower the winning bid for a given valuation.

4.2. The Collusive Bidding Model

We now develop an auction model with collusive side payments. The bidding model is a three-stage game. In stage 1, each buyer formulates his or her private valuation of the player under the collusive arrangement, , based on assumedly costless information about the player to be sold. In stage 2, the bidders play a collusion sub-game during in which they implicitly choose a winning bid from among a set of bids that interested clubs will offer to submit to the auction (one of which is known to the bidders as the winning bid) and they decide the distribution of side payments associated with the winning bid. In stage 3, the Commissioner selects the highest bid as the winning bid and informs the seller of the amount without revealing the identity of the winner. At this point, the seller may accept or reject the winning bid. We do not explicitly model a fourth stage, the salary bargaining process between the Japanese player and the winning bidder if the bid is accepted. Instead we assume that the Japanese player will receive a salary of si dollars, which is higher than the salary he is currently earning.

We focus on stage 2 of the bidding model as this largely determines the outcome for stage 3. Without defection by any of the bidding clubs, the collusive sub-game in stage 2 results in efficiency (

Graham and Marshall 1987) if the side payments to all clubs, including the winning bidder, sum to zero (the winning bidder cannot borrow to make the necessary side payments). In our model, side payments are automatically collected and paid through a revenue sharing system in which each club is allowed to keep a share equal to

α of its local revenues (0 ≤

α ≤ 1), the rest being contributed into a league pool that is distributed evenly among every team in MLB at the end of the playing season. The revenue for the winning bidder club

i after revenue sharing is denoted

.

In this way, each of the other

N − 1 clubs receives a positive side payment if the winning bidder experiences a significant increase in local revenue after acquiring the player. The same can be said for the expected marginal revenue product of the NPL player: any gain in revenue for the winning bidder must be shared with the rest of the league. We have that

is the expected marginal revenue product. Ring efficiency requires that the net profit for the winning bidder is the maximal winning profit among all bidders after all side payments have been paid, thus the ring efficiency condition is

where

is the collusive winning bid. The first term on the left-hand side of (2) constitutes the total net revenue the winning bidder will keep from acquiring the player under the revenue sharing agreement. The winner must also pay the amount of the winning bid and the player salary. It is in the best interest of the losing bidders to select the bidder with the highest valuation to “win” the auction and to “arrange” a winning collusive bid,

, as close to

Rmin from above as possible in order to guarantee the ring efficiency condition is met and the maximum side payments can be made. If this does not occur, an ascending bid auction takes place during the pre-auction in stage 2 so that bidding club with a private valuation equal to

prevails.

Condition (2) essentially determines which bidder is chosen to win the auction. Note that there are two circumstances under which the seller (the NPL club) will refuse the winning bid in stage 3 of the game. First, the private valuation of the winning bidder, , might not be high enough so that even the highest bid falls short of the seller’s true reservation price. Second, the winning bidder could underestimate the seller’s true reservation price (u < 0) by enough to violate condition (2) and walk away from the auction. In this way, condition (2) represents the winning bidder’s expectation of the ring efficiency condition.

Under the MLB revenue sharing agreement, an additional condition is that the winning bidder is expected to be at least as well as off by colluding as by not colluding. This makes the ring efficiency condition feasible with revenue sharing.

Condition (3) places a constraint on the maximum valuation of the player among all bidders with revenue sharing.

Condition (4) states that the post-revenue sharing maximum valuation must exceed the difference in maximum bids under strategic (or implicit) collusive bidding with revenue sharing.

Conditions (2)–(4) are enough to describe the set of possible equilibria in the collusive bargaining game.

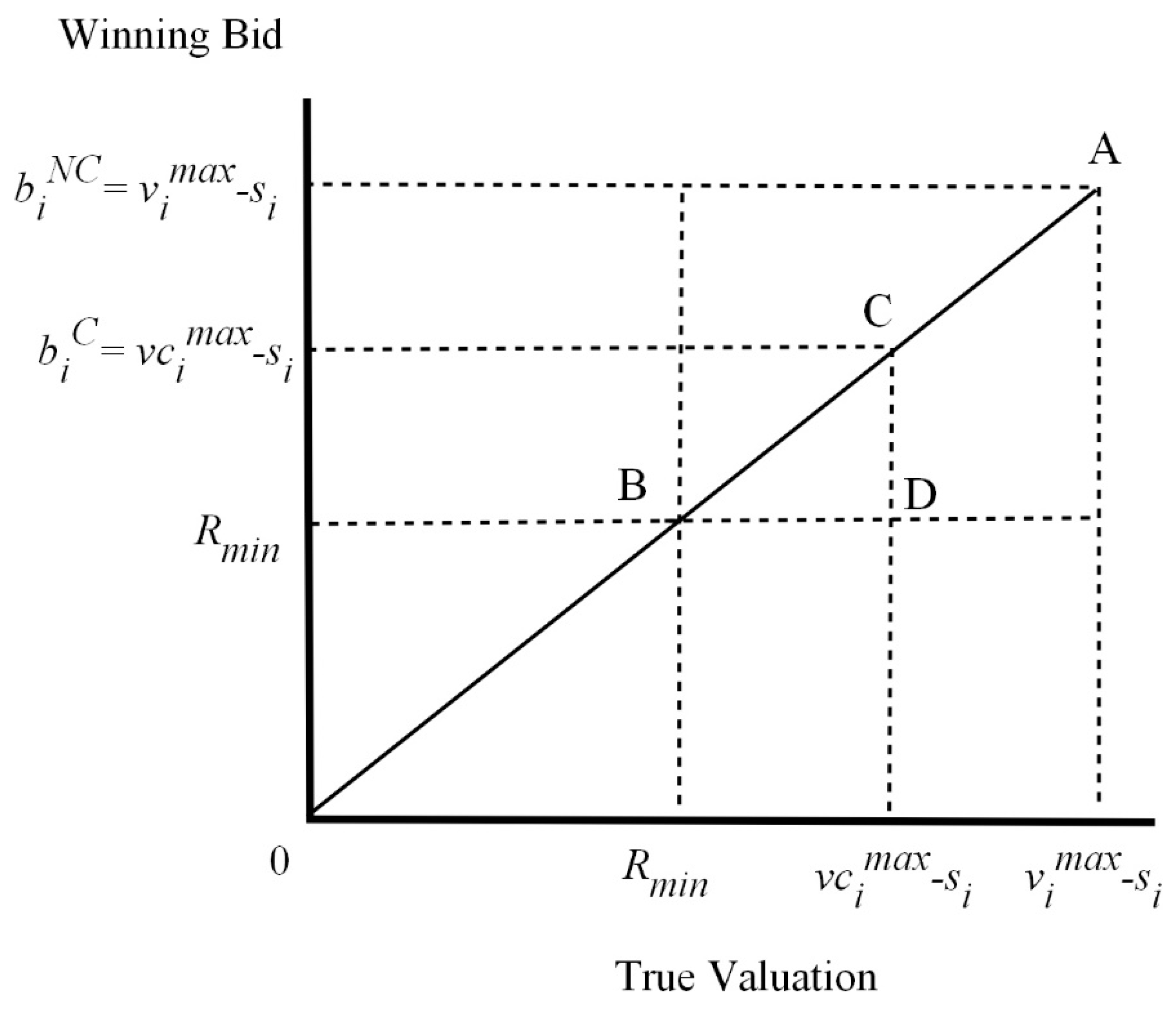

Figure 1 plots the actual winning bid on the vertical axis and the actual valuation of the player to the winning bidder on the horizontal axis. Any equilibrium falling on the 45-degree line denotes a winning bid that is confirmed by the actual valuation (

u = 0). In a sealed bid auction with no collusion and revenue sharing, the winning bidder will just pay his or her private valuation to the seller net of the player’s salary,

. The non-collusive equilibrium is denoted by point A in

Figure 1 and provides a limit on the magnitude of the surplus for a specific player and highest bidder.

Recall that the NPL club knows the minimum bid it will accept for the posted player, Rmin. Any bid below this valuation is not accepted as bounded by the horizontal dashed line at Rmin on the vertical axis. Each bidder must form an expectation of Rmin that is subject to the random error u. If , the MLB club is not interested in bidding for the posted player, represented by the vertical dashed line on the horizontal axis. The set of equilibria is then limited to the rectangle bounded by on the vertical axis and on the horizontal axis. Point B is a winning bid that is just equal to the minimum bid the NPL club will accept. The MLB club is indifferent to acquiring this player as there is no surplus earned. Perhaps most posted players fall around point B since they are marginal players with relatively low salaries.

Consider point C in

Figure 1 that represents an NPL player of considerable talent. Point C is an equilibrium bid that falls on the 45-degree line so that the winning bid is just equal to the player’s true valuation to the winner and there is no surplus to the winning bidder. Condition (2) is an equality, while conditions (3) and (4) are satisfied since the winning bidder has evaluated them before making the bid. Any bid above the 45-degree line results in a negative surplus for the MLB club. These bids are be offered. The only equilibrium bids occur below the 45-degree line in the triangle region greater than or equal to

Rmin. A bid such as at point D generates the maximum surplus to the winning bidder equal to the vertical distance between points C and D. Any point in between C and D generates a positive surplus to the winning bidder.

Revenue sharing reduces the amount of the winning bid since positive side payments must be made to all of the other clubs. Formally, the change in the amount of the collusive winning bid is the change in the marginal revenue product of the posted player with the change in the revenue sharing coefficient

α.

In (5),

is the average of the local revenues for the other teams in the league. An increase in the revenue sharing contribution rate is a reduction in

α, so that the net change in revenue for team

i is positive if team is equal to or below the average revenue for all of the other teams. If

N is large, this equates to the being below the average local revenue for all teams in the league (

Easton and Rockerbie 2005). Greater revenue sharing moves the boundary of the equilibrium region of bids to the left, reducing the likelihood of a successful transaction. The distribution of highest bids by each club in the league is compressed, but there cannot be a situation where the overall highest bidding club is changed

5. This could be offset somewhat by a reduction in

si, the salary offered to the posted player.

{kind=link}