COVID-19, Government Response, and Market Volatility: Evidence from the Asia-Pacific Developed and Developing Markets

Abstract

:1. Introduction

2. Materials and Methods

2.1. Methodology

2.1.1. The Continuous Wavelet Transformation (CWT)

2.1.2. The GJR-GARCH Model

3. Results

3.1. Continuous Wavelet Transform Results

3.2. GJR-GARCH (1,1)

4. Discussion

5. Conclusions and Implication of the Study

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

Appendix A.1. China

Appendix A.2. Japan

Appendix A.3. South Korea

Appendix A.4. Indonesia

Appendix A.5. Laos

Appendix A.6. Malaysia

Appendix A.7. Myanmar

Appendix A.8. Singapore

Appendix A.9. Thailand

Appendix A.10. Philippines

Appendix A.11. Vietnam

References

- Aggarwal, Reena, Carla Inclan, and Ricardo Leal. 1999. Volatility in Emerging Stock Markets. Journal of Financial and Quantitative Analysis 34: 33–55. [Google Scholar] [CrossRef]

- Al-Awadhi, Abdullah M., Khaled Al-Saifi, Ahmad Al-Awadhi, and Salah Alhamadi. 2020. Death and contagious infectious diseases: Impact of the COVID-19 virus on stock market returns. Journal of Behavioral and Experimental Finance 27: 100326. [Google Scholar] [CrossRef] [PubMed]

- Albulescu, Claudiu. 2020. Coronavirus and Financial Volatility: 40 Days of Fasting and Fear. SSRN Electronic Journal, 1–7. [Google Scholar] [CrossRef] [Green Version]

- Ali, Mohsin, Nafis Alam, and Syed Aun R. Rizvi. 2020. Coronavirus (COVID-19)—An epidemic or pandemic for financial markets. Journal of Behavioral and Experimental Finance 27: 100341. [Google Scholar] [CrossRef] [PubMed]

- Ashraf, Badar Nadeem. 2020. Stock markets’ reaction to COVID-19: Cases or fatalities? Research in International Business and Finance 54: 101249. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, Kyle Kost, Marco Sammon, and Tasaneeya Viratyosin. 2020. The unprecedented stock market reaction to Covid-19. Pandemics: Long-Run Effects Effects 1: 33–42. [Google Scholar]

- Bekaert, Geert, and Campbell R. Harvey. 1997. Emerging equity market volatility. Journal of Financial Economics 43: 29–77. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, Geert, and Michael S. Urias. 1999. Is there a free lunch in emerging market equities?: In some market, but investors need to be more selective going forward. Journal of Portfolio Management 25: 83–95. [Google Scholar] [CrossRef]

- Donoho, David L., Iain M. Johnstone, Gérard Kerkyacharian, and Dominique Picard. 1995. Wavelet Shrinkage: Asymptopia? Journal of the Royal Statistical Society. Series B (Methodological) 57: 301–69. [Google Scholar] [CrossRef]

- Gérard, Bruno, Kessara Thanyalakpark, and Jonathan A. Batten. 2003. Are the East Asian markets integrated? Evidence from the ICAPM. Journal of Economics and Business 55: 585–607. [Google Scholar] [CrossRef]

- Glosten, Lawrence R., Ravi Jagannathan, and David E. Runkle. 1993. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. The Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Goodell, John W. 2020. COVID-19 and finance: Agendas for future research. Finance Research Letters 35. [Google Scholar] [CrossRef] [PubMed]

- Gormsen, Niels Joachim, and Ralph S. J. Koijen. 2020. Coronavirus: Impact on Stock Prices and Growth Expectations. SSRN Electronic Journal, 1–45. [Google Scholar] [CrossRef]

- Goupillaud, Pierre, Alex Grossmann, and Jean Morlet. 1984. Cycle-octave and related transforms in seismic signal analysis. Geoexploration 23: 85–102. [Google Scholar] [CrossRef]

- Hale, Thomas, Anna Petherick, Toby Phillips, and Samuel Webster. 2020. Variation in government responses to COVID-19. In Blavatnik Working Paper Series. Available online: https://www.bsg.ox.ac.uk/research/publications/variation-government-responses-covid-19 (accessed on 6 November 2020).

- Khalfaoui, Rabeh K., and Mohamed B. Boutahar. 2011. A Time-Scale Analysis of Systematic Risk: Wavelet-Based Approach. In Munich Personal RePEc Archive. Munich: University Library of Munich, p. 31938. [Google Scholar]

- Kit, Tang See. 2020. Singapore Stocks Near 4-Year Low as Oil Rout, COVID-19 Fears Send Investors ‘Dumping Everything’. Available online: https://www.channelnewsasia.com/news/business/singapore-stocks-four-year-low-oil-rout-covid19-fears-12518786 (accessed on 6 November 2020).

- Kupferschmidt, Kai, and Jon Cohen. 2020. Can China’s COVID-19 strategy work elsewhere? Science. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2020. COVID-19 and March 2020 Stock Market Crash. Evidence from S&P1500. Finance Research Letters, 101690. [Google Scholar] [CrossRef]

- Ministry of Trade and Industry. 2020. *Advance Estimates of Singapore’s GDP. Available online: https://www.mti.gov.sg/Newsroom/Press-Releases/2020/10/Singapore-GDP-Contracted-by-7_0-Per-Cent-in-the-Third-Quarter-of-2020 (accessed on 6 November 2020).

- Mzoughi, Hela, Christian Urom, Gazi Salah Uddin, and Khaled Guesmi. 2020. The Effects of COVID-19 Pandemic on Oil Prices, CO2 Emissions and the Stock Market: Evidence from a VAR Model. SSRN Electronic Journal, 1–8. [Google Scholar] [CrossRef]

- Newey, Whitney K., and Kenneth D. West. 1987. A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix. Econometrica 55: 703–8. [Google Scholar] [CrossRef]

- Nurunnabi, Mohammad, Syed Far Abid Hossain Hossain, Karuthan Chinna, Sheela Sundarasen, Heba Bakr Khoshaim, Kamilah Kamaludin, Gul Mohammad Baloch, Areej Sukayt, and Xu Shan. 2020. Coping strategies of students for anxiety during the COVID-19 pandemic in China: A cross-sectional study. F1000Research 9. [Google Scholar] [CrossRef]

- Onali, Enrico. 2020. COVID-19 and Stock Market Volatility. SSRN Electronic Journal, 1–24. [Google Scholar] [CrossRef]

- Ramsey, James B. 1999. The Contribution of Wavelets to the Analysis of Economic and Financial Data. Philosophical Transactions: Mathematical, Physical and Engineering Sciences 357: 2593–606. [Google Scholar] [CrossRef]

- Shanaev, Savva, Arina Shuraeva, and Binam Ghimire. 2020. The Financial Pandemic: COVID-19 and Policy Interventions on Rational and Irrational Markets. SSRN Electronic Journal, 1–49. [Google Scholar] [CrossRef]

- Sharif, Arshian, Chaker Aloui, and Larisa Yarovaya. 2020. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis 70: 101496. [Google Scholar] [CrossRef]

- Thampanya, Natthinee, Junjie Wu, Muhammad Ali Nasir, and Jia Liu. 2020. Fundamental and behavioural determinants of stock return volatility in ASEAN-5 countries. Journal of International Financial Markets, Institutions and Money 65: 101193. [Google Scholar] [CrossRef]

- Torrence, Christopher, and Gilbert P. Compo. 1998. A Practical Guide to Wavelet Analysis. Bulletin of the American Meteorological Society 79: 61–78. [Google Scholar] [CrossRef] [Green Version]

- Wagner, Alexander F. 2020. What the stock market tells us about the post-COVID-19 world. Nature Human Behaviour 4: 440. [Google Scholar] [CrossRef]

- Yarovaya, Larisa, Janusz Brzeszczynski, John W. Goodell, Brian M. Lucey, and Chi Keung Lau. 2020. Rethinking Financial Contagion: Information Transmission Mechanism During the COVID-19 Pandemic. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Zaremba, Adam, Renatas Kizys, David Y. Aharon, and Ender Demir. 2020. Infected Markets: Novel Coronavirus, Government Interventions, and Stock Return Volatility around the Globe. Finance Research Letters, 101597. [Google Scholar] [CrossRef]

- Zhang, Dayong, Min Hu, and Qiang Ji. 2020. Financial markets under the global pandemic of COVID-19. Finance Research Letters, 101528. [Google Scholar] [CrossRef]

| 1 | |

| 2 | |

| 3 | |

| 4 | |

| 5 | |

| 6 | |

| 7 | |

| 8 | |

| 9 | March 2020 Stock Market Crash also records single-day extreme events: Black Monday I (9 March), Black Thursday (12 March) and Black Monday II (16 March). |

| 10 |

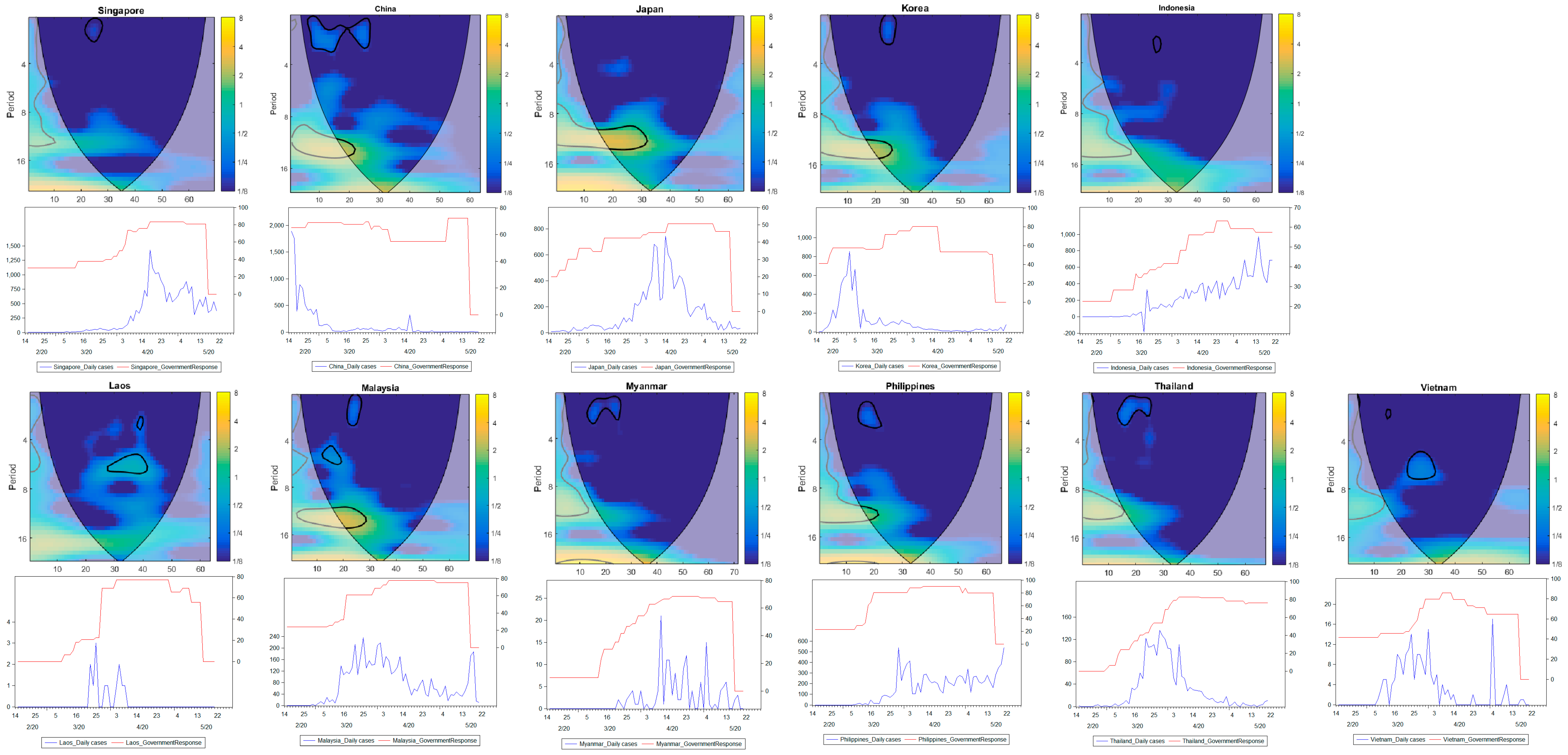

{kind=link}

| Country | Significant Volatility | Range of SD | Period of Significant Volatility | Freq. Bands | Horizon | Govt. Response | COVID-19 Trend | Factors or Reasons for Volatilities |

|---|---|---|---|---|---|---|---|---|

| Vietnam | very low volatility | ⅛ | 6–10 March | 1–2 | short-term | An increasing index score of 42 to 46 | 2nd stage—a resurgence of new cases | Second waves detected and moderate government response—Overlapping with international events |

| Indonesia | very low volatility | ⅛ | 20–26 March | 2–3 | short-term | An increasing index score of 37 to 40 | Early-stage—increasing trend | The spread of COVID-19 cases and moderate government response |

| Singapore | low volatility | ⅛–¼ | 17–26 March | 0–2 | short-term | Index score of 38 | Early-stage—increasing trend | The spread of COVID-19 cases and moderate government response |

| South Korea | low volatility | ¼–½ | 18–26 March | 0–2 | short-term | An increasing index score of 56 to 72 | Mid-stage—decreasing trend | Reduction of COVID-19 cases and high government response |

| China | low volatility | ¼–½ | 24 February–24 March | 0–3 | short-term | Index score at 69 | End-stage—decreasing trend | Reduction of COVID-19 cases and high government response |

| Philippines | low volatility | ¼–½ | 6–23 March | 1–3 | short-term | An increasing index score of 22 to 80 | Very early stage—an increasing trend | Initial reaction to COVID-19 cases and rapid government response |

| Laos | low volatility | ¼–½ | 20–22 April | 2–3 | short-term | An index score of 77 | End-stage—zero cases | Containment of COVID-19 infection through a high government response |

| Myanmar | low volatility | ¼–½ | 4–23 March | 0–2 | short-term | An increasing index score of 10 to 35 | Very early stage—First 2 cases detected on 23 March | Anticipation period before COVID-19 spread in the country—Overlapping with international events |

| Thailand | low volatility | ¼–½ | 5–25 March | 0–3 | short-term | An increasing index score of 6 to 50 | Early-stage—increasing trend | The spread of COVID-19 cases and high government response—Overlapping with international events |

| Malaysia | low volatility | ¼–½ | 18–25 March | 0–3 | short-term | An increasing index score of 32 to 61 | Early-stage—increasing trend | COVID-19 spread (local transmission) and high government response |

| Vietnam | medium-low volatility | ½–1 | 18 March–1 April | 5–7 | medium-term | An increasing index score of 46 to 80 | Third stage—increasing trend | High government response at peaked of COVID-19 cases |

| Malaysia | medium volatility | 1–2 | 4–16 March | 4–6 | medium-term | An increasing index score of 24 to 32 | Early-stage—increasing trend | Political turmoil |

| Laos | medium volatility | 1–2 | 27 March–23 April | 5–7 | medium-term | An increasing index score of 22 to 77 | Early period—mixed trend | High government response at initial reaction to a spike of COVID-19 cases |

| China | high volatility | 2–4 | 9–18 March | 11–14 | long-term | An index score of 69 | End-stage—declining trend | Timeline is overlapping with international events |

| Japan | high volatility | 2–4 | 9 March–3 April | 9–13 | long-term | An increasing index score of 35 to 44 | Early-stage—increasing trend | Timeline is overlapping with international events |

| South Korea | high volatility | 2–4 | 9–25 March | 12–15 | long-term | An increasing index score of 58 to 72 | Mid-stage—declining trend | Timeline is overlapping with international events |

| Malaysia | high volatility | 2–4 | 9–27 March | 11–15 | long-term | An increasing index score of 32 to 61 | Early-stage—increasing trend | Timeline is overlapping with international events |

| Philippines | high volatility | 2–4 | 9–20 March | 10–13 | long-term | An increasing index score of 22 to 80 | Very early stage—an increasing trend | The timeline is overlapping with international events. |

| Country | Equation | Independent Variables | Coefficient | Std. Error | t-Value | t-Prob |

|---|---|---|---|---|---|---|

| China | Mean | Cst(M) | 2835.486 ** | 5.908 | 479.900 | 0.000 |

| Variance | Cst(V) | 157.100 * | 84.032 | 1.870 | 0.066 | |

| ARCH(Alpha1) | 0.769 ** | 0.173 | 4.435 | 0.000 | ||

| GARCH(Beta1) | 0.226 | 0.142 | 1.596 | 0.115 | ||

| GJR(Gamma1) | −0.019 | 0.185 | −0.103 | 0.918 | ||

| Indonesia | Mean | Cst(M) | 4590.870 ** | 16.978 | 270.400 | 0.000 |

| Variance | Cst(V) | 869.320 ** | 407.290 | 2.134 | 0.037 | |

| ARCH(Alpha1) | 0.309 ** | 0.116 | 2.670 | 0.010 | ||

| GARCH(Beta1) | 0.574 ** | 0.145 | 3.955 | 0.000 | ||

| GJR(Gamma1) | 0.038 | 0.196 | 0.193 | 0.848 | ||

| Japan | Mean | Cst(M) | 19.801 ** | 0.331 | 59.830 | 0.000 |

| Variance | Cst(V) | 0.109 | 0.088 | 1.234 | 0.222 | |

| ARCH(Alpha1) | 0.823 ** | 0.147 | 5.593 | 0.000 | ||

| GARCH(Beta1) | 0.063 | 0.053 | 1.188 | 0.239 | ||

| GJR(Gamma1) | 0.271 | 0.367 | 0.739 | 0.463 | ||

| Korea | Mean | Cst(M) | 1930.973 ** | 5.351 | 360.900 | 0.000 |

| Variance | Cst(V) | 498.527 | 442.600 | 1.126 | 0.265 | |

| ARCH(Alpha1) | 0.900 ** | 0.153 | 5.876 | 0.000 | ||

| GARCH(Beta1) | −0.004 | 0.047 | −0.084 | 0.933 | ||

| GJR(Gamma1) | 0.267 | 0.269 | 0.991 | 0.326 | ||

| Laos | Mean | Cst(M) | 620.694 ** | 0.563 | 1103.000 | 0.000 |

| Variance | Cst(V) | 2.899 | 2.150 | 1.349 | 0.182 | |

| ARCH(Alpha1) | 0.706 ** | 0.098 | 7.188 | 0.000 | ||

| GARCH(Beta1) | 0.159 ** | 0.062 | 2.573 | 0.013 | ||

| GJR(Gamma1) | 1.192 * | 0.637 | 1.872 | 0.066 | ||

| Malaysia | Mean | Cst(M) | 1386.135 ** | 4.651 | 298.100 | 0.000 |

| Variance | Cst(V) | 117.720 ** | 37.055 | 3.177 | 0.002 | |

| ARCH(Alpha1) | 0.988 ** | 0.171 | 5.774 | 0.000 | ||

| GARCH(Beta1) | 0.017 | 0.102 | 0.165 | 0.870 | ||

| GJR(Gamma1) | 0.097 | 0.300 | 0.325 | 0.747 | ||

| Myanmar | Mean | Cst(M) | 111.980 ** | 0.342 | 327.200 | 0.000 |

| Variance | Cst(V) | 0.261 | 0.224 | 1.166 | 0.248 | |

| ARCH(Alpha1) | 0.543 ** | 0.129 | 4.223 | 0.000 | ||

| GARCH(Beta1) | 0.467 ** | 0.126 | 3.710 | 0.000 | ||

| GJR(Gamma1) | −0.060 | 0.162 | −0.368 | 0.714 | ||

| Philippines | Mean | Cst(M) | 5583.420 ** | 23.226 | 240.400 | 0.000 |

| Variance | Cst(V) | 223.271 | 439.170 | 0.508 | 0.613 | |

| ARCH(Alpha1) | 0.173 * | 0.089 | 1.951 | 0.056 | ||

| GARCH(Beta1) | 0.785 ** | 0.101 | 7.800 | 0.000 | ||

| GJR(Gamma1) | −0.146 ** | 0.068 | −2.158 | 0.035 | ||

| Singapore | Mean | Cst(M) | 2562.246 ** | 15.944 | 160.700 | 0.000 |

| Variance | Cst(V) | 422.448 | 482.860 | 0.875 | 0.385 | |

| ARCH(Alpha1) | 0.363 | 0.245 | 1.481 | 0.143 | ||

| GARCH(Beta1) | 0.462 | 0.350 | 1.319 | 0.192 | ||

| GJR(Gamma1) | 0.143 | 0.265 | 0.540 | 0.591 | ||

| Thailand | Mean | Cst(M) | 857.434 ** | 24.235 | 35.380 | 0.000 |

| Variance | Cst(V) | 124.572 | 152.740 | 0.816 | 0.418 | |

| ARCH(Alpha1) | 0.865 | 0.578 | 1.498 | 0.139 | ||

| GARCH(Beta1) | 0.032 | 0.526 | 0.060 | 0.952 | ||

| GJR(Gamma1) | 0.434 | 0.933 | 0.465 | 0.643 | ||

| Vietnam | Mean | Cst(M) | 770.208 ** | 1.805 | 426.700 | 0.000 |

| Variance | Cst(V) | 27.578 * | 14.700 | 1.876 | 0.065 | |

| ARCH(Alpha1) | 1.097 ** | 0.110 | 9.976 | 0.000 | ||

| GARCH(Beta1) | 0.008 | 0.014 | 0.593 | 0.556 | ||

| GJR(Gamma1) | 0.150 | 0.283 | 0.529 | 0.599 |

| Country | Independent Variables | Coef. | Std. Err. | t-Stat | p > t | [95% Conf. Interval] | |

|---|---|---|---|---|---|---|---|

| China | Daily COVID-19 cases | 0.101 ** | 0.049 | 2.05 | 0.044 | 0.003 | 0.200 |

| Government Response | 1.644 ** | 0.452 | 3.64 | 0.001 | 0.743 | 2.546 | |

| Constant | −16.630 | 23.690 | −0.70 | 0.485 | −63.903 | 30.643 | |

| Indonesia | Daily COVID-19 cases | 0.000 | 0.000 | 0.63 | 0.529 | 0.000 | 0.001 |

| Government Response | −0.022 ** | 0.005 | −3.94 | 0.000 | −0.033 | −0.011 | |

| Constant | 1.218 ** | 0.221 | 5.50 | 0.000 | 0.776 | 1.660 | |

| Japan | Daily COVID-19 cases | −0.005 ** | 0.001 | −4.16 | 0.000 | −0.007 | −0.003 |

| Government Response | −0.076 * | 0.042 | −1.79 | 0.078 | −0.160 | 0.009 | |

| Constant | 6.481 ** | 1.859 | 3.49 | 0.001 | 2.767 | 10.194 | |

| Korea | Daily COVID-19 cases | −0.143 | 0.144 | −1.00 | 0.323 | −0.430 | 0.144 |

| Government Response | 3.990 | 4.571 | 0.87 | 0.386 | −5.147 | 13.128 | |

| Constant | 129.916 | 278.452 | 0.47 | 0.642 | −426.703 | 686.534 | |

| Laos | Daily COVID-19 cases | −3.346 ** | 1.342 | −2.49 | 0.015 | −6.027 | −0.665 |

| Government Response | −0.194 ** | 0.050 | −3.84 | 0.000 | −0.295 | −0.093 | |

| Constant | 18.944 ** | 3.119 | 6.07 | 0.000 | 12.713 | 25.175 | |

| Malaysia | Daily COVID-19 cases | 0.035 | 0.081 | 0.43 | 0.666 | −0.126 | 0.196 |

| Government Response | −1.360 ** | 0.277 | −4.91 | 0.000 | −1.914 | −0.807 | |

| Constant | 129.644 ** | 20.442 | 6.34 | 0.000 | 88.830 | 170.458 | |

| Philippines | Daily COVID-19 cases | −0.210 ** | 0.058 | −3.61 | 0.001 | −0.326 | −0.094 |

| Government Response | −1.194 ** | 0.303 | −3.95 | 0.000 | −1.799 | −0.589 | |

| Constant | 163.757 ** | 28.521 | 5.74 | 0.000 | 106.779 | 220.735 | |

| Singapore | Daily COVID-19 cases | −0.006 | 0.005 | −1.40 | 0.166 | −0.015 | 0.003 |

| Government Response | −0.124 * | 0.069 | −1.80 | 0.076 | −0.261 | 0.013 | |

| Constant | 15.680 ** | 3.549 | 4.42 | 0.000 | 8.596 | 22.763 | |

| Thailand | Daily COVID-19 cases | 1.580 ** | 0.391 | 4.04 | 0.000 | 0.800 | 2.360 |

| Government Response | −1.691 ** | 0.318 | −5.32 | 0.000 | −2.326 | −1.057 | |

| Constant | 143.196 ** | 24.283 | 5.90 | 0.000 | 94.728 | 191.664 | |

| Vietnam | Daily COVID-19 cases | −1.842 | 1.312 | −1.40 | 0.165 | −4.459 | 0.776 |

| Government Response | −1.554 ** | 0.421 | −3.69 | 0.000 | −2.394 | −0.714 | |

| Constant | 166.550 ** | 30.085 | 5.54 | 0.000 | 106.516 | 226.584 | |

| Myanmar | Daily COVID-19 cases | 0.187 | 0.288 | 0.65 | 0.518 | −0.387 | 0.761 |

| Government Response | −0.491 ** | 0.095 | −5.18 | 0.000 | −0.680 | −0.302 | |

| Constant | 145.770 ** | 5.842 | 24.95 | 0.000 | 134.122 | 157.419 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ibrahim, I.; Kamaludin, K.; Sundarasen, S. COVID-19, Government Response, and Market Volatility: Evidence from the Asia-Pacific Developed and Developing Markets. Economies 2020, 8, 105. https://doi.org/10.3390/economies8040105

Ibrahim I, Kamaludin K, Sundarasen S. COVID-19, Government Response, and Market Volatility: Evidence from the Asia-Pacific Developed and Developing Markets. Economies. 2020; 8(4):105. https://doi.org/10.3390/economies8040105

Chicago/Turabian StyleIbrahim, Izani, Kamilah Kamaludin, and Sheela Sundarasen. 2020. "COVID-19, Government Response, and Market Volatility: Evidence from the Asia-Pacific Developed and Developing Markets" Economies 8, no. 4: 105. https://doi.org/10.3390/economies8040105

APA StyleIbrahim, I., Kamaludin, K., & Sundarasen, S. (2020). COVID-19, Government Response, and Market Volatility: Evidence from the Asia-Pacific Developed and Developing Markets. Economies, 8(4), 105. https://doi.org/10.3390/economies8040105