A Socio-Economic Model of Sales Tax Compliance

,

,  and

and {kind=link}

Abstract

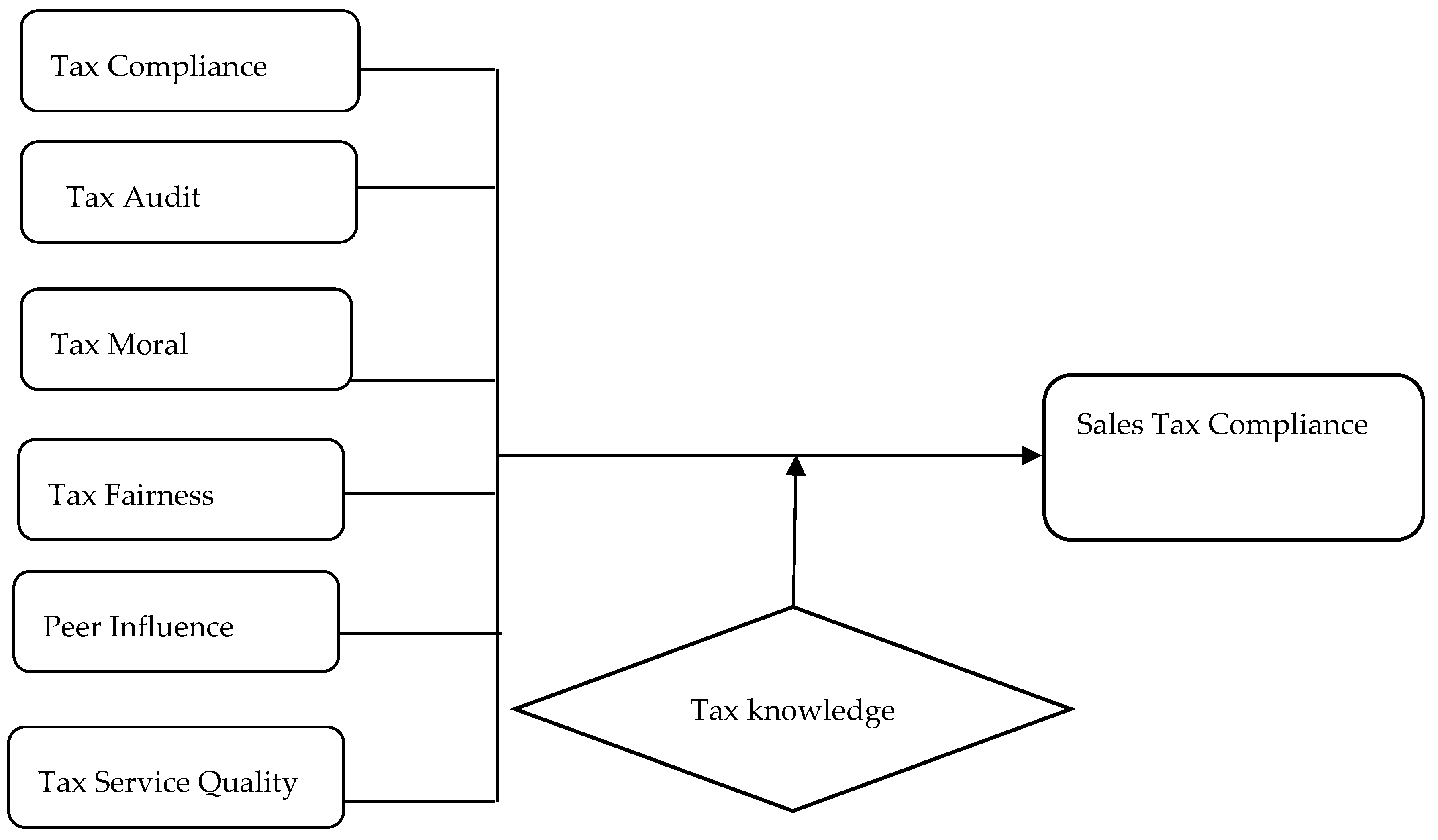

:1. Introduction

2. Literature Review

3. Study Implications

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Abdixhiku, Lumir, Besnik Krasniqi, Geoff Pugh, and Iraj Hashi. 2017. Firm-level determinants of tax evasion in transition economies. Economic Systems 41: 354–66. [Google Scholar] [CrossRef]

- Abdul-Jabbar, Hijattulah, and Jeff Pope. 2008. Exploring the relationship between tax compliance costs and compliance issues in Malaysia. Journal of Applied Law and Policy 1: 1–20. [Google Scholar]

- Adams, Caroline, and Paul Webley. 2001. Small business owners’ attitudes on VAT compliance in the UK. Journal of Economic Psychology 22: 195–21. [Google Scholar] [CrossRef]

- Alabede, James, and Zaimah Zainal Affrin. 2011. Tax service quality and compliance behaviour in Nigeria: Do taxpayer’s financial condition and risk preference play any moderating role? European Journal of Economics, Finance and Administrative Sciences 35: 90–108. [Google Scholar]

- Al-Bakri, Anas, Mohammed Matar, and Abdul Naser Nour. 2014. The required information and financial statements disclosure in SMEs. Journal of Finance and Accountancy 16: 1–15. [Google Scholar]

- Allingham, Michael, and Agnar Sandmo. 1972. Income tax evasion: A theoretical analysis. Journal of Public Economics 1: 323–38. [Google Scholar] [CrossRef] [Green Version]

- Alm, James. 1991. A perspective on the experimental analysis of taxpayer reporting. The Accounting Review 66: 577–93. [Google Scholar]

- Alm, James. 2012. Measuring, explaining, and controlling tax evasion: Lessons from theory, experiments, and field studies. International Tax and Public Finance 19: 54–77. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Asmaa El-Ganainy. 2013. Value-added taxation and consumption. International Tax and Public Finance 20: 105–28. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Chandler McClellan. 2012. Tax morale and tax compliance from the firm’s perspective. Kyklos 65: 1–17. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Michael McKee. 2006. Audit certainty, audit productivity, and taxpayer compliance. Andrew Young School of Policy Studies Research 59: 801–816. [Google Scholar]

- Alm, James, and Benno Torgler. 2011. Do ethics matter? Tax compliance and morality. Journal of Business Ethics 101: 635–51. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, Betty R. Jackson, and Michael McKee. 1993. Fiscal exchange, collective decision institutions, and tax compliance. Journal of Economic Behavior & Organization 22: 285–303. [Google Scholar] [CrossRef]

- Alm, James, Erich Kirchler, Stephan Muehlbacher, Katharina Gangl, Eva Hofmann, Christoph Kogler, and Maria Pollai. 2012. Rethinking the research paradigms for analysing tax compliance behaviour. In CESifo Forum. München: IfoInstitut-Leibniz-Institutfür Wirtschaftsforschung an der Universität München, vol. 13, pp. 33–40. [Google Scholar]

- Alm, James, Jeremy Clark, and Kara Leibel. 2016. Enforcement, socioeconomic diversity, and tax filing compliance in the United States. Southern Economic Journal 82: 725–47. [Google Scholar] [CrossRef] [Green Version]

- Alon, Anna, and Amy M. Hageman. 2013. The impact of corruption on firm tax compliance in transition economies: Whom do you trust? Journal of Business Ethics 116: 479–94. [Google Scholar] [CrossRef]

- Alrousan, Mohammad Kasem, and Eleri Jones. 2016. A conceptual model of factors affecting e-commerce adoption by SME owner/managers in Jordan. International Journal of Business Information Systems 21: 269–308. [Google Scholar] [CrossRef]

- AL-Shawawreh, Taha Barakat, and Belal Yousef AL-Smirat. 2016. Economic effects of tax evasion on Jordanian economy. International Journal of Economics and Finance 8: 344–48. [Google Scholar] [CrossRef] [Green Version]

- Alshira’h, Ahmad Farhan, Hijattulah Abdul-Jabbar, and Rose Shamsiah Samsudin. 2016. Determinants of sales tax compliance in small and medium enterprises in Jordan: A call for empirical research. World Journal of Management and Behavioral Studies 4: 41–46. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan. 2018. Determinants of Sales Tax Compliance among Jordanian SMEs: The Moderating Effect of Public Governance. Unpublished Doctoral dissertation, Universiti Utara Malaysia, Changlun, Malaysia. [Google Scholar]

- Alshira’h, Ahmad Farhan, and Hijattulah Abdul-Jabbar. 2019a. The effect of tax fairness on sales tax compliance among Jordanian manufacturing SMEs. Academy of Accounting and Financial Studies Journal 23: 1–11. [Google Scholar]

- Alshira’h, Ahmad Farhan, and Hijattulah Abdul-Jabbar. 2019b. A conceptual model of sales tax compliance among Jordanian SMEs and its implications for future research. International Journal of Economics and Finance 11: 114–14. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, and Hijattulah Abdul-Jabbar. 2020. Moderating role of patriotism on sales tax compliance among Jordanian SMEs. International Journal of Islamic and Middle Eastern Finance and Management 13: 389–415. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, Hijattulah Abdul-Jabbar, and Rose Shamsiah Samsudin. 2018. Sales tax compliance model for the Jordanian Small and medium enterprises research. Journal of Advanced Research in Social and Behavioural Sciences 10: 115–30. [Google Scholar]

- Alshira’h, Ahmad Farhan, Hijattulah Abdul-Jabbar, and Rose Shamsiah Samsudin. 2019. The effect of tax moral on sales tax compliance among Jordanian SMEs. International Journal of Academic Research in Accounting, Finance and Management Sciences 9: 30–41. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, Hasan Mahmoud AL-Shatnawi, Mohammad Khalil Alsqour, and Malek Hamed Alshirah. 2020. The Influence of Tax Complexity on Sales Tax Compliance among Jordanian SMEs. International Journal of Academic Research in Accounting, Finance and Management Sciences 10: 250–60. [Google Scholar] [CrossRef]

- Al-Smirat, Belal Yousef. 2013. The use of accounting information by small and medium enterprises in South District of Jordan (An empirical study). Research Journal of Finance and Accounting 4: 169–75. [Google Scholar]

- Al-Ttaffi, Lutfi Hassen Ali, and Hijattullah Abdul-Jabbar. 2015. A conceptual framework for tax non-compliance studies in a Muslim country: A proposed framework for the case of Yemen. International Postgraduate Business Journal 7: 1–16. [Google Scholar]

- Al-Ttaffi, Lutfi Hassen Ali, and Hijattullah Abdul-Jabbar. 2016. Service quality and income tax non-compliance among small and medium enterprises in Yemen. Journal of Advanced Research in Business and Management Studies 4: 12–21. [Google Scholar]

- Al-Zoubi, A., H. Khatatba, R. B. Salama, and M. Khatataba. 2013. Methods of tax avoidance and evasion: The incapability of the Jordanian income tax law to face tax avoidance and evasion. Journal Almanara 19: 9–36. [Google Scholar]

- Andreoni, James, Brian Erard, and Jonathan Feinstein. 1998. Tax compliance. Journal of Economic Literature 36: 818–60. [Google Scholar]

- Ariel, Barak. 2012. Deterrence and moral persuasion effects on corporate tax compliance: Findings from a randomized controlled trial. Criminology 50: 27–69. [Google Scholar] [CrossRef]

- Association of Banks in Jordan. 2016. Small and Medium Enterprises in Jordan, Analysis of Supplies-Side and Demand-Side Focusing on Banking Financing. Studies Department. Available online: http://www.abj.org.jo/ar-jo/otherstudies.aspx (accessed on 9 July 2017).

- Azmi, Anna, Noor Sharoja Sapiei, Mohd Zulkhairi Mustapha, and Mazni Abdullah. 2016. SMEs’ tax compliance costs and IT adoption: The case of a value-added tax. International Journal of Accounting Information Systems 23: 1–13. [Google Scholar] [CrossRef]

- Baron, Reuben M., and David A. Kenny. 1986. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Ppersonality and SsocialPpsychology 51: 1173. [Google Scholar] [CrossRef]

- Baru, A. 2016. The impact of tax knowledge on tax compliance. Journal of Advanced Research in Business and Management Studies 6: 22–30. [Google Scholar]

- Becker, Gary. 1968. Crime and punishment: An economic approach. The Journal of Political Economy 76: 169–217. [Google Scholar] [CrossRef] [Green Version]

- Benk, Serkan, Ahmet Ferda Cakmak, and Tamer Budak. 2011. An investigation of tax compliance intention: A theory of planned behavior approach. European Journal of Economics, Finance and Administrative Sciences 28: 180–88. [Google Scholar]

- Biabani, Shaer, and Adeleh Ramezani. 2011. An investigation of the factors effective on the compliance behavior of the tax payers in the VAT system: A case study of Qazvin tax affairs general department. African Journal of Business Management 5: 10760–68. [Google Scholar]

- Bird, Richard M., and Eric M. Zolt. 2014. Redistribution via taxation: The limited role of the personal income tax in developing countries. Annals of Economics and Finance 15: 625–83. [Google Scholar]

- Bird, Richard M., Jorge Martinez-Vazquez, and Benno Torgler. 2008. Tax effort in developing countries and high income countries: The impact of corruption, voice and accountability. Economic Analysis and Policy 38: 55–71. [Google Scholar] [CrossRef] [Green Version]

- Boonyarat, Nichapat, Syed Sofian, and Wanida Wadeecharoen. 2014. The antecedents of taxpayers’ compliance behavior and the effectiveness of Thai local government levied tax. International Business Management 9: 23–39. [Google Scholar]

- Brown, Robert E., and Mark J. Mazur. 2003. IRS’s comprehensive approach to compliance measurement. National Tax Journal 56: 689–700. [Google Scholar] [CrossRef] [Green Version]

- Brysland, Alexandria, and Adrienne Curry. 2001. Service improvements in public services using SERVQUAL. Managing Service Quality: An International Journal 11: 389–401. [Google Scholar] [CrossRef]

- Çevik, Savaş, and Harun Yeniçeri. 2013. The relationship between social norms and tax compliance: The moderating role of the effectiveness of tax administration. International Journal of Economic Sciences 2: 166–80. [Google Scholar]

- Chan, Chris W., Coleen S. Troutman, and David O’Bryan. 2000. An expanded model of taxpayer compliance: Empirical evidence from the United States and Hong Kong. Journal of International Accounting, Auditing and Taxation 9: 83–103. [Google Scholar] [CrossRef]

- Chau, K. K. G., and Patrick Leung. 2009. A critical review of Fischer tax compliance model: A research synthesis. Journal of Accounting and Taxation 1: 34–40. [Google Scholar]

- Clotfelter, Charles. 1983. Tax evasion and tax rates: An analysis of individual returns. The Review of Economics and Statistics 65: 363–73. [Google Scholar] [CrossRef]

- Crocker, Keith J., and Joel Slemrod. 2005. Corporate tax evasion with agency costs. Journal of Public Economics 89: 1593–610. [Google Scholar] [CrossRef] [Green Version]

- Cuccia, Andrew D., and Gregory A. Carnes. 2001. A closer look at the relation between tax complexity and tax equity perceptions. Journal of Economic Psychology 22: 113–40. [Google Scholar] [CrossRef]

- Cullis, John G., and Alan Lewis. 1997. Why people pay taxes: From a conventional economic model to a model of social convention. Journal of Economic Psychology 18: 305–21. [Google Scholar] [CrossRef]

- Das-Gupta, Arindam, and Ira Gang. 2003. Value added tax evasion, auditing and transactions matching. In Institutional Elements of Tax Design and Reform. Edited by John Maclarn. Washington, DC: The World Bank, pp. 25–48. [Google Scholar]

- Delone, William H., and Ephraim R. McLean. 2003. The DeLone and McLean model of information systems success: A ten-year update. Journal of Management Information Systems 19: 9–30. [Google Scholar] [CrossRef]

- Devos, Ken. 2008. Tax evasion behaviour and demographic factors: An exploratory study in Australia. Revenue Law Journal 18: 1–45. [Google Scholar]

- Devos, Ken. 2012. A comparative study of compliant and non-compliant individual taxpayers in Australia. Journal of Business and Policy Research 7: 180–96. [Google Scholar]

- Eriksen, Knut, and Lars Fallan. 1996. Tax knowledge and attitudes towards taxation; A report on a quasi-experiment. Journal of Economic Psychology 17: 387–402. [Google Scholar] [CrossRef]

- Faridy, Nahida, Richard Copp, Brett Freudenberg, and Tapan Sarker. 2014. Complexity, compliance costs and non compliance with VAT by small and medium enterprises in Bangladesh: Is there a relationship. Australian Tax Forum 29: 281–329. [Google Scholar] [CrossRef]

- Faridy, Nahida, Brett Freudenberg, Tapan Sarker, and Richard Copp. 2016. The hidden compliance cost of VAT: An exploration of psychological and corruption costs of VAT in a developing country. eJournal of Tax Research 14: 166–205. [Google Scholar]

- Fauvelle-Aymar, Christine. 1999. The political and tax capacity of government in developing countries. Kyklos 52: 391–413. [Google Scholar] [CrossRef]

- Fauziati, Penerbit, A. F. Minovia, R. Y. Muslim, and R. Nasrah. 2016. The impact of tax knowledge on tax compliance case study in kotapadang, Indonesia. Journal of Advanced Research in Business and Management Studies 2: 22–30. [Google Scholar]

- Feinstein, Jonathan S. 1991. An econometric analysis of income tax evasion and its detection. The RAND Journal of Economics 22: 14–35. [Google Scholar] [CrossRef]

- Feld, Lars P., and Bruno S. Frey. 2007. Tax compliance as the result of a psychological tax contract: The role of incentives and responsive regulation. Law and Policy 29: 102–20. [Google Scholar] [CrossRef] [Green Version]

- Feld, Lars P., and Claus Larsen. 2012. Self-perceptions, government policies and tax compliance in Germany. International Tax and Public Finance 19: 78–103. [Google Scholar] [CrossRef]

- Feld, Lars P., and Friedrich Schneider. 2010. Survey on the Shadow Economy and Undeclared Earnings in OECD Countries. German Economic Review 11: 109–49. [Google Scholar] [CrossRef]

- Feld, Lars P., Bruno S. Frey, and Benno Torgler. 2006. Rewarding Honest Taypayers? Evidence on the Impact of Rewards from Field Exeperiments. Working Paper. Basel and Zürich: Center for Research in Economics, Management and the Arts. [Google Scholar]

- Fellner, Gerlinde, Rupert Sausgruber, and Christian Traxler. 2013. Testing enforcement strategies in the field: Threat, moral appeal and social information. Journal of the European Economic Association 11: 634–60. [Google Scholar] [CrossRef] [Green Version]

- Fischer, Carol M., Martha Wartick, and Melvin M. Mark. 1992. Detection probability and taxpayer compliance: A review of the literature. Journal of Accounting Literature 11: 1–25. [Google Scholar]

- Fochmann, Martin, and Eike B. Kroll. 2015. The effects of rewards on tax compliance decisions. Journal of Economic Psychology 52: 38–55. [Google Scholar] [CrossRef] [Green Version]

- Franzoni, Luigi A. 1999. Tax evasion and tax compliance. In Encyclopedia of Law and Economics. Edited by B. Bouckaert and G. De Geest. Cheltenham: Edward Elgar, pp. 52–94. [Google Scholar]

- Frecknall-Hughes, Jane, and Peter Moizer. 2015. Assessing the quality of services provided by UK tax practitioners. eJournal of Tax Research 13: 51. [Google Scholar]

- Frey, Bruno S. 2003. Deterrence and tax morale in the European Union. European Review 11: 385–406. [Google Scholar] [CrossRef]

- Frey, Bruno S., and Benno Torgler. 2007. Tax morale and conditional cooperation. Journal of Comparative Economics 35: 136–59. [Google Scholar] [CrossRef] [Green Version]

- Giesecke, James, and Nhi Hoang Tran. 2012. A general framework for measuring VAT compliance rates. Applied Economics 44: 1867–89. [Google Scholar] [CrossRef] [Green Version]

- Hanefah, H. 1996. An Evaluation of the Malaysian Tax Administrative System and Tax Payers’ Perceptions towards Assessment Systems, Tax Law Fairness, and Tax Law Complexity. Ph.D. thesis, Universiti Utara Malaysia, Bukit KayuHitam, Malaysia. Unpublished. [Google Scholar]

- Hansford, Ann, and John Hasseldine. 2012. Tax compliance costs for small and medium sized enterprises: The case of the UK. eJournal of Tax Research 10: 288–303. [Google Scholar]

- Harris, Thomas Donald. 2013. The effect of tax knowledge on individual’s perceptions of fairness and compliance with federal income tax system: An empirical study. Unpublished manuscript. South Carolina: University of South Carolina. [Google Scholar]

- Hite, Peggy A. 1988. The effect of peer reporting behavior on taxpayer compliance. Journal of the American Taxation Association 9: 47–64. [Google Scholar]

- Jackson, Betty R., and Valerie C. Milliron. 1986. Tax compliance research: Findings, problems and prospects. Journal of Accounting Literature 5: 125–65. [Google Scholar]

- Jordan Independent Economic Watch. 2014. Tax Burden in Jordan, Reality & Prospects. Available online: http://www.identity-center.org (accessed on 12 July 2018).

- Joulfaian, David. 2000. Corporate income tax evasion and managerial preferences. Review of Economics and Statistics 82: 698–701. [Google Scholar] [CrossRef]

- Joulfaian, David. 2009. Bribes and business tax evasion. European Journal of Comparative Economics 6: 227–44. [Google Scholar]

- Kasipillai, Jeyapalan, and Hijattullah Abdul-Jabbar. 2006. Gender and ethnicity differences in tax compliance. Asian Academy of Management Journal 11: 73–88. [Google Scholar]

- Kasipillai, Jeyapalan, and Mustafa Mohd Hanefah. 2000. Tax professionals’ views on self assessment system. Analisis 7: 107–22. [Google Scholar]

- Kinsey, Karyl A., and Harold G. Grasmick. 1993. Did the Tax Reform Act of 1986 improve compliance? Three studies of pre-and post-TRA compliance attitudes. Law & Policy 15: 293–325. [Google Scholar]

- Kirchler, Erich, and Boris Maciejovsky. 2001. Tax compliance within the context of gain and loss situations, expected and current asset position, and profession. Journal of Economic Psychology 22: 173–94. [Google Scholar] [CrossRef]

- Kirchler, Erich, and Ingrid Wah. 2010. Tax compliance inventory TAX-I: Designing an inventory for surveys of tax compliance. Journal of Economic Psychology 31: 331–46. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kirchler, Erich, Apolonia Niemirowski, and Alexander Wearing. 2006. Shared subjective views, intent to cooperate and tax compliance: Similarities between Australian taxpayers and tax officers. Journal of Economic Psychology 27: 502–17. [Google Scholar] [CrossRef]

- Kirchler, Erich, Stephan Muehlbacher, Barbara Kastlunger, and Ingrid Wahl. 2007. Why Pay Taxes? A Review of Tax Compliance Decisions. International Studies Program Working Paper. Atlanta: Georgia State University. [Google Scholar]

- Kirchler, Erich, Christoph Kogler, and Stephan Muehlbacher. 2014. Cooperative tax compliance: From deterrence to deference. Current Directions in Psychological Science 23: 87–92. [Google Scholar] [CrossRef]

- Lee, Dongwon, Dongil Kim, and Thomas E. Borcherding. 2013. Tax structure and government spending: Does the value-added tax increase the size of government? National Tax Journal 66: 541–70. [Google Scholar] [CrossRef] [Green Version]

- Lutf, Abd Alwali, Kamil Md Idris, and Rosli Mohamad. 2016. The influence of technological, organizational and environmental factors on accounting information system usage among Jordanian small and medium-sized enterprises. International Journal of Economics and Financial Issues 6: 240–48. [Google Scholar]

- Lutfi, Abd Alwali, Kamil Md Idris, and Rosli Mohamad. 2017. AIS usage factors and impact among Jordanian SMEs: The moderating effect of environmental uncertainty. Journal of Advanced Research in Business and Management Studies 6: 24–38. [Google Scholar]

- Matthews, Shelley Keith, and Robert Agnew. 2008. Extending deterrence theory: Do delinquent peers condition the relationship between perceptions of getting caught and offending? Journal of Research in Crime and Delinquency 45: 91–118. [Google Scholar] [CrossRef]

- McKerchar, Margaret, Kim Bloomquist, and Jeff Pope. 2013. Indicators of tax morale: An exploratory study. eJournal of Tax Research 11: 5–22. [Google Scholar]

- Ministry of Finance. 2016. General Government Financial Statements. General Government Bulletins for December. Available online: http://www.mof.gov.jo (accessed on 20 February 2018).

- Morse, Susan Cleary, Stewart Karlinsky, and Joseph Bankman. 2009. Cash businesses and tax evasion. Stanford Law and Policy Review 20: 1–67. [Google Scholar]

- Muche, B. 2014. Determinants of tax payer’s voluntary compliance with taxation in east Gojjam-Ethiopia. Research Journal of Economics &Businrss Studies 3: 41–50. [Google Scholar]

- Mustapha, Bojuwon, and Siti Normala Bt Sheikh Obid. 2014. The influence of technology characteristics towards an online tax system usage: The case of Nigerian self-employed taxpayer. International Journal of Computer Applications 105: 30–36. [Google Scholar]

- Nura, Mohammed, Hijattulah Abdul-Jabbar, and Idawati Ibrahim. 2017. VAT compliance and the influence of political and business environment: A proposed framework for Nigerian SMEs. Asian Journal of Business Management Studies 8: 13–20. [Google Scholar]

- Nur-Tegin, Kanybek. 2008. Determinants of business tax compliance. The BE Journal of Economic Analysis & Policy 8: 1–28. [Google Scholar] [CrossRef]

- Palil, Mohd Rizal, and Ahmad Fariq Mustapha. 2011. Determinants of tax compliance in Asia: A case of Malaysia. European Journal of Social Sciences 24: 7–32. [Google Scholar]

- Palil, M. R., N. H. M. Zain, and S. M. Faizal. 2012. Political affiliation and tax compliance in Malaysia. Humanities and Social Sciences Review 1: 395–402. [Google Scholar]

- Park, Chang-Gyun, and Jin Kwon Hyun. 2003. Examining the determinants of tax compliance by experimental data: A case of Korea. Journal of Policy Modeling 25: 673–84. [Google Scholar] [CrossRef]

- Pommerehne, Werner W., and Hannelore Weck-Hannemann. 1996. Tax rates, tax administration and income tax evasion in Switzerland. Public Choice 88: 161–70. [Google Scholar] [CrossRef]

- Randlane, Kerly. 2016. Tax Compliance as a system: Mapping the field. International Journal of Public Administration 39: 515–25. [Google Scholar] [CrossRef]

- Richardson, Grant. 2006. Determinants of tax evasion: A cross-country investigation. Journal of International Accounting, Auditing and Taxation 15: 150–69. [Google Scholar] [CrossRef]

- Ritsatos, Titos. 2014. Tax evasion and compliance: From the neo classical paradigm to behavioural economics, a review. Journal of Accounting & Organizational Change 10: 244–62. [Google Scholar] [CrossRef]

- Roth, Jeffrey A., John T. Scholz, and Ann Dryden Witte. 1989. Taxpayer Compliance, Volume 1: An Agenda for Research. Philadelphia: University of Pennsylvania Press. [Google Scholar] [CrossRef]

- Saad, Natrah. 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-Social and Behavioral Sciences 109: 1069–75. [Google Scholar] [CrossRef] [Green Version]

- Samuel, Mutarindwa, and Rutikanga Jean De Dieu. 2014. The impact of taxpayers’ financial statements audit on tax revenue growth. International Journal of Business and Economic Development 2: 51–60. [Google Scholar]

- Sawyer, Adrian. 2014. Comparing the Swiss and United Kingdom cooperation agreements with their respective agreements under the Foreign account tax compliance act. eJournal of Tax Research 12: 285–318. [Google Scholar]

- Saymeh, Abdul Aziz Farid, and Sulieman Abu Sabha. 2014. Assessment of Small Enterprise Financing, case of Jordan. Global Journal of Management and Business Research 14: 6–18. [Google Scholar]

- Saymeh, Abdul Aziz Farid, and Sulieman Abu Sabha. 2015. A proposed model of non-compliance behaviour on excise duty: A moderating effects of tax agents. Procedia—Social and Behavioral Sciences 2011: 299–305. [Google Scholar] [CrossRef] [Green Version]

- Slemrod, Joel. 2007. Cheating ourselves: The economics of tax evasion. The Journal of Economic Perspectives 21: 25–48. [Google Scholar] [CrossRef] [Green Version]

- Slemrod, Joel, Marsha Blumenthal, and Charles Christian. 2001. Taxpayer response to an increased probability of audit: Results from a controlledexperiement in Minnesota. Journal of Public Economics 79: 455–83. [Google Scholar] [CrossRef] [Green Version]

- Song, Young-dahl, and Tinsley E. Yarbrough. 1978. Tax ethics and taxpayer attitudes: A survey. Public Administration Review 38: 442–52. [Google Scholar] [CrossRef]

- Spicer, Michael W., and Scott B. Lundstedt. 1976. Understanding tax evasion. Public Finance = Finances Publiques 31: 295–305. [Google Scholar]

- Tehulu, Tilahun Aemiro, and Yidersal Dagnaw Dinberu. 2014. Determinants of tax compliance behavior in Ethiopia: The case of bahirdar city taxpayers. Journal of Economics and Sustainable Development 5: 268–74. [Google Scholar]

- Torgler, Benno, and Friedrich Schneider. 2009. The impact of tax morale and institutional quality on the shadow economy. Journal of Economic Psychology 30: 228–45. [Google Scholar] [CrossRef] [Green Version]

- Trisnawati, Rina, and Destia Nugraheni. 2015. The analysis of information asymmetry, profitability, and deferred tax expense on integrated earning management. South East Asia Journal of Contemporary Business, Economics and Law 7: 17–24. [Google Scholar]

- Tusubira, Festo Nyende, and Isaac Nabeta Nkote. 2013. Social Norms, taxpayers’ morale and tax compliance: The case of small business enterprises in Uganda. Journal of Accounting Taxation and Performance Evaluation 2: 1–10. [Google Scholar]

- United Nations Development Programme. 2012. The Panoramic Study of the Informal Economy in Jordan. Ministry of Planning. Available online: http://inform.gov.jo/en-us/By-Date/Report-Details/ArticleId/37/mid/420/Article-Category/205/The-Panoramic-Study-of-the-Informal-Economy-in-Jordan (accessed on 23 September 2017).

- Vadde, Suresh. 2014. Compliance and non compliance behavior of business profit taxpayers’ towards the tax system: A case study of Mekelle city. Scholars Journal of Economics, Business and Management 1: 525–31. [Google Scholar] [CrossRef]

- Varvarigos, Dimitrios. 2016. Cultural norms, the persistence of tax evasion, and economic growth. Economic Theory 21: 1–35. [Google Scholar] [CrossRef] [Green Version]

- Vigoda-Gadot, Eran. 2007. Citizens’ perceptions of politics and ethics in public administration: A five-year national study of their relationship to satisfaction with services, trust in governance, and voice orientations. Journal of Public Administration Research and Theory 17: 285–305. [Google Scholar] [CrossRef]

- Webley, Paul, Carolyn Adams, and Henk Elffers. 2002. VAT Compliance in the United Kindom. (Working Paper No. 41). Canberra: Centre for Tax System Integrity Research School of Social Sciences, Australian National University. [Google Scholar]

- Wenzel, MichaelM. 2004. An analysis of norm processes in tax compliance. Journal of Economic Psychology 25: 213–28. [Google Scholar] [CrossRef] [Green Version]

- Witte, Ann D., and Diane F. Woodbury. 1985. The effect of tax laws and tax administration on tax compliance: The case of the US individual income tax. National Tax Journal 38: 1–13. [Google Scholar]

- Woodward, Lynley, and Lin Mei Tan. 2015. Small business owners attitudes toward GST compliance: A preliminary study. Australian Tax Forum 30: 517–50. [Google Scholar] [CrossRef]

- Yahaya, Lawan. 2015. The perception of corporate taxpayers’ compliance behaviour under self-assessment system in Nigeria. Journal of Management Research 7: 343. [Google Scholar] [CrossRef] [Green Version]

- Young Entrepreneur Association. 2011. Small and Medium Business Agenda. Available online: http://www.cipe-Arabia.org (accessed on 20 August 2018).

- Young, Angus, Lawrence Lei, Brossa Wong, and Betty Kwok. 2016. Individual tax compliance in China: A review. International Journal of Law and Management 58: 1–12. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alshira’h, A.F.; Alsqour, M.; Lutfi, A.; Alsyouf, A.; Alshirah, M. A Socio-Economic Model of Sales Tax Compliance. Economies 2020, 8, 88. https://doi.org/10.3390/economies8040088

Alshira’h AF, Alsqour M, Lutfi A, Alsyouf A, Alshirah M. A Socio-Economic Model of Sales Tax Compliance. Economies. 2020; 8(4):88. https://doi.org/10.3390/economies8040088

Chicago/Turabian StyleAlshira’h, Ahmad Farhan, Moh’d Alsqour, Abdalwali Lutfi, Adi Alsyouf, and Malek Alshirah. 2020. "A Socio-Economic Model of Sales Tax Compliance" Economies 8, no. 4: 88. https://doi.org/10.3390/economies8040088

APA StyleAlshira’h, A. F., Alsqour, M., Lutfi, A., Alsyouf, A., & Alshirah, M. (2020). A Socio-Economic Model of Sales Tax Compliance. Economies, 8(4), 88. https://doi.org/10.3390/economies8040088