During the research, the analysis of the annual financial statements was carried out with the objective to assess the AID quality of the non-current tangible assets in the annual financial statements of the private sector entities of Lithuania.

3.1. Data

First of all, in order to organise the research, the sampling, the investigated period, the data sources, and the sample size were determined.

3.1.1. Sampling and the Data Sources

The research analyses the annual financial statements of the unlisted enterprises of Lithuania. The sample of enterprises was formed in a few stages:

First, to reach the aim of the research, i.e., to examine and evaluate the AID quality in the annual financial statements, the notes, i.e., one of the financial statements, were analysed. However, the lower requirements for financial statements of micro-enterprises are established in the Law on Financial Statements of Entities of the Republic of Lithuania. Article 20 of this Law provides that micro-enterprises “can omit drawing up notes and then the set of their financial statements shall consist of the following financial statements: (i) short balance sheet and (ii) short profit and loss account”.

In this research, a micro-enterprise is understood as it is defined by the Law on Financial Statements of Entities of the Republic of Lithuania, i.e., an enterprise that has “at least two indicators of which do not exceed the following amounts on the last day of a financial year: (i) the value of assets on the balance sheet—EUR 350,000; (ii) net sales revenue during a reporting financial year—EUR 700,000; (iii) the average annual number of payroll employees during a reporting financial year—10 employees” (Article 4, Law on Financial Statements of Entities of the Republic of Lithuania). Hence, the research should analyse the small, medium, and large enterprises. Thus, the surveyed enterprises were selected from the list of business leaders TOP 500 (for 2007), i.e., the largest Lithuanian enterprises by sales revenue, published by the leading Lithuanian business newspaper “Verslo žinios” (English: “Business News”).

Second, the research analyses the annual financial statements of the unlisted enterprises of Lithuania that use national accounting standards, i.e., BASs. Therefore, the following companies were removed from this list: (i) Listed companies; (ii) companies providing financial services; (iii) companies that use accounting standards other than BASs, and (iv) companies that are not required to prepare financial statements, such as sole proprietorships, limited partnerships, and partnerships in Lithuania that are required to present financial statements only if specified in their instruments of incorporation. Thus, by the legal form, the sample of Lithuanian enterprises consists of public or private limited enterprises. In this way, the list of business leaders was reduced to 463 enterprises.

Third, the sample must exclude enterprises that have ceased or otherwise restricted their activities before 2016. Therefore, an additional requirement was imposed on the selection of enterprises. The enterprise must be in the list of TOP500 in both 2007 and 2016 or remain in the list of TOP1000. However, in Lithuania, the TOP500 list has been changing significantly, i.e., during this period, only 231 enterprises remained in the TOP500 list (46% of the 2007 TOP500); 75 enterprises dropped to the TOP501–1000 positions (15% of the 2007 TOP500). In this way, the list of business leaders was reduced to 306 enterprises. In terms of enterprise size, these enterprises were classified as follows: Large and medium-sized enterprises account for 82% of the total, while small enterprises account for the remaining part. This classification of enterprises was also followed in the sample of the surveyed enterprises.

Fourth, in order for the survey to be representative of the country’s enterprises, the selected enterprises must be classified by economic activities in a way that corresponds to this classification in the country.

As it was mentioned above, the survey does not analyse micro-enterprises as they do not prepare notes. As we see, the size of the enterprises is defined by three parameters: Assets, annual sales revenue, and the number of employees. Meanwhile, the Department of Statistics of the Republic of Lithuania details enterprises only by the number of employees, i.e., an enterprise is considered micro as with less than 10 employees. Hence, in this research, the enterprises with more than ten employees represent the group of small, medium, and large enterprises.

According to the data of the Department of Statistics of the Republic of Lithuania, the enterprises in operation at the beginning of 2016 in Lithuania with more than ten employees carried out the economic activities (measured by sales revenue) in the following sections: 28% of total revenue was generated in Manufacturing (C section); 3% in Electricity, gas, steam, and air conditioning supply (D); 6% in Construction (F); 40% in Wholesale and retail trade; repair of motor vehicles and motorcycles (G); 11% in Transportation and storage (H); 3% in Information and communication activities (J).

This revenue distribution must be maintained in the sample. As mentioned in Stage 3, the enterprises in the sample must maintain the classification of enterprises by the size of the enterprise. According to these requirements, the sample is formed.

It should be also mentioned that the accounting information provided in the set of financial statements cannot be a commercial secret. However, in practice, the unlisted enterprises do not publish the annual financial statements on their websites. According to the Civil Code of the Republic of Lithuania, companies submit a set of annual financial statements to the State Enterprise Centre of Registers every year within thirty days of their approval. Although administrative liability may be imposed for non-submission, only about 50% of legal entities (which were required to submit reports) submit financial statements to the Centre of Registers. These objective conditions limit access to the data of unlisted enterprises for research purposes. Consequently, for this research, the data of the Lithuanian enterprises’ financial statements were provided by the State Enterprise Centre of Registers and a credit bureau Creditinfo Lietuva. If, after selecting an enterprise in the sample, its financial statements were not available, the enterprise was removed from the sample, and the fourth selection stage was repeated.

Finally, subject to the criteria mentioned above and data availability, the sample was formed, and the financial statements data of 37 enterprises were analysed. It should also be noted that the sample size was limited by the methods used in the research: The content method chosen to determine the AID quality, i.e., the qualitative research method.

In order to examine the dynamics of DQI and its factors properly with regard to time, panel data models allowing the use of a greater volume of data are chosen. In this instance, the variation within a selected group of enterprises as well as the dynamics in the period of 2007–2008 and 2016 were examined. Thus, a single group consisting of 111 observations (37 enterprises × 3 years) allows for obtaining reliable results of the statistical analysis.

3.1.2. The Investigated Period

The investigated period is the period over which the financial data were analysed. The research includes the analysis of enterprises’ financial data of three years, i.e., 2007, 2008, and 2016. The assumptions of the selection of the investigated period are the following.

First, due to the selected period of 2007–2008, the National Accounting Standards started to be applied from 2004. Three years are considered to be a sufficient period of time for the accountants to be sufficiently familiar with the new accounting standards and to be sufficiently qualified to prepare sets of financial statements in accordance with the requirements of the accounting standards. Secondly, due to the selected period of 2016, not only the structure of financial statements but also the amount of the disclosed information has changed in Lithuania again since 2016. Therefore, the impact of regulatory changes on the quality of disclosures is examined. Third, the aim is to assess (i) whether the AID quality of enterprises is likely to change significantly in the short term (2007–2008) or in the long term (2008–2016) and (ii) which enterprise’s characteristics may affect the observed significant changes.

The period chosen is also interesting for the following economic reasons. First, according to (

Kiyak et al. 2011), the Lithuanian economy grew very rapidly in 2002–2007. Lithuania’s economic growth began to slow down and fell sharply in the fourth quarter of 2008 (this continued for 6 consecutive quarters). In 2008–2010, the Lithuanian economy went through a complex financial crisis, which operated both domestically (the bursting of the real estate bubble) and externally (the ongoing global financial crisis). For these reasons, it becomes important to assess whether the AID quality of enterprises changed in 2008 (when business faced a crisis) compared to 2007 (when it was observed the “record corporate profits earned in 2007” (

Bank of Lithuania 2008)). The relevance of this issue is particularly acute at a time when business is facing a crisis caused by the COVID-19 pandemic. Secondly, Lithuania from a developing country has become a developed country. (i) In 2007, Lithuania was considered a developing country. (ii) According to the World Bank (

World Bank 2019), since 2012, Lithuania’s economy has been classified as one of the “high-income economies”. According to the International Monetary Fund (

IMF 2011), since 2015, Lithuania’s economy has been classified as one of the “advanced economies”. Moreover, Lithuania became the latest country to join the euro area in 2015. Hence, in 2016, Lithuania’s economy is considered as one of the developed economies. In this way, we can compare the AID quality of enterprises when a country has been developing and has reached the level of a developed country.

3.2. The Dependent Variable: Accounting Information Disclosure Quality

In particular, it is reasonable to discuss the design of the accounting information disclosure quality (hereinafter referred to as AID quality) research model. AID quality is a variable that is difficult to measure directly. This problem is solved using the disclosure index, that is, according to

Beattie et al. (

2004), “a fairly objective, form-oriented content-analytic method”. It should be noted that the research model of the AID quality in the private sector profit-oriented entities’ (hereinafter referred to as enterprises) financial statements used in this article is the specification of the authors’ designed (

Kanapickienė and Keliuotytė-Staniulėnienė 2019) research model of the AID quality in the financial statements targeted on the public sector entities (municipalities).

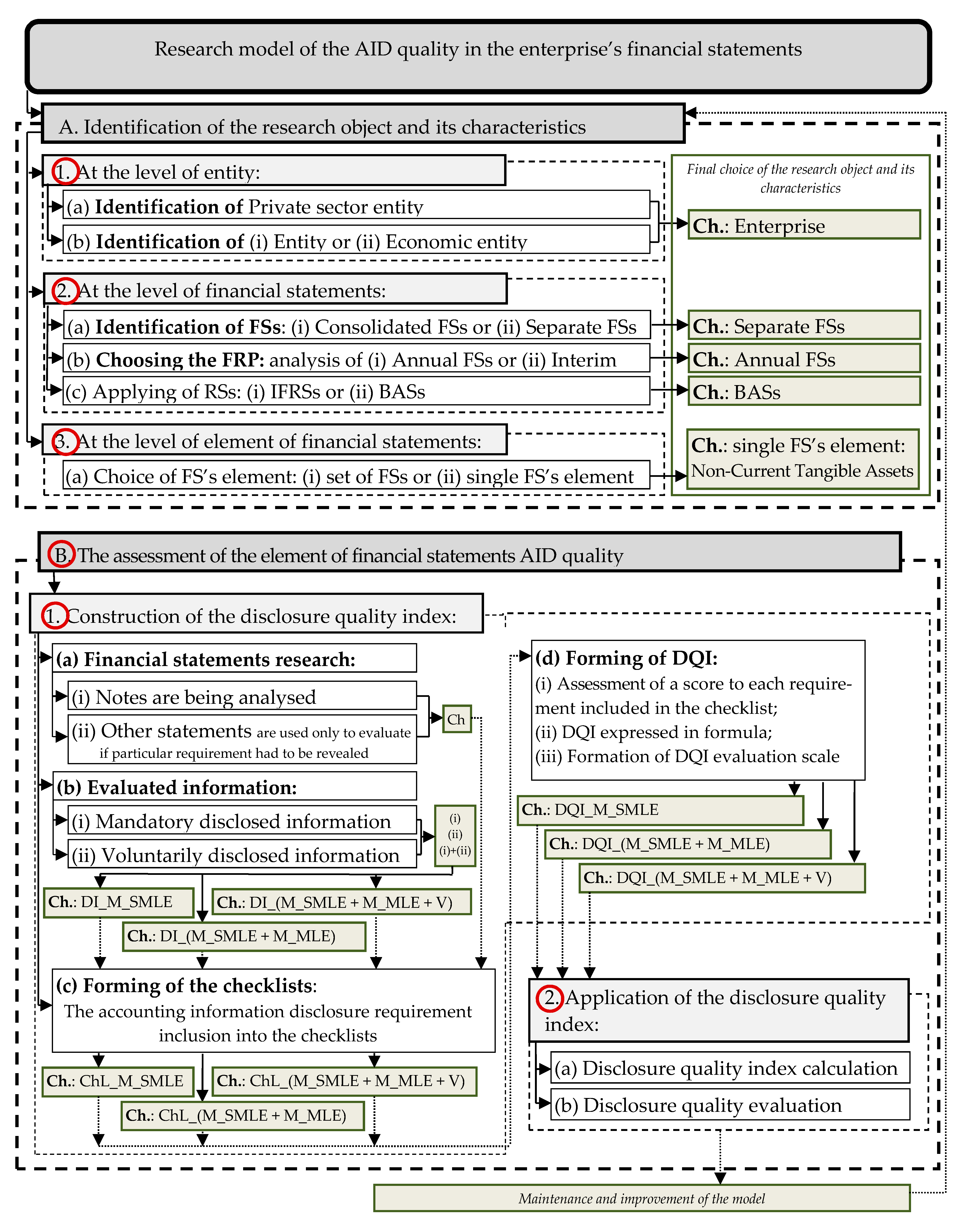

The research model of the AID quality in the enterprise’s financial statements consists of two stages (

Figure 1): (A) Identification of the research object and its characteristics and (B) the assessment of the element of financial statements AID quality.

In the first stage, the identification of the research object and its characteristics is carried out at the level (1) of an entity, (2) of financial statements, and (3) of an element of financial statements. To construct and apply the disclosure quality index in the enterprise’s financial statements, the following selections are made. (1) By identification of a private sector entity, the essential selection is made, i.e., in this research, the private sector profit-oriented entity (hereinafter referred to as an enterprise) is chosen. (2) To identify the main characteristics of financial statements, (a) having considered the possibility to choose between the consolidated financial statements or separate financial statements, it is decided to analyse the separate financial statements. (b) The opportunity to select either annual or interim financial statements is analysed, and the annual financial statements are selected. (c) It is considered that accounting standards, according to which the annual financial statements are prepared, will be analysed. In the private sector, the financial reports can be prepared according to either International Financial Reporting Standards (IFRSs) or National Accounting Standards (NASs)—in the case of Lithuania—Business Accounting Standards (BASs). The entities followed by Business Accounting Standards (BASs) are selected. (3) For the identification of the researched element of financial statements, two possibilities are considered, i.e., to evaluate the AID quality either of the whole set of financial statements or of its single elements. In this research, tangible assets are selected as the researched element of financial statements.

To sum up, the annual financial statements of the Lithuanian enterprises are selected for analysis as the private sector profit-oriented entities. Moreover, the enterprises prepare the annual financial statements using the BASs. In this research, tangible assets are selected as the element of financial statements.

In the second stage, the assessment process of the element of financial statements AID quality is investigated. The method of the disclosure index is used to measure the AID quality.

The stage of this assessment process can be broken down into two sub-stages including (1) construction and (2) application of the disclosure quality index (hereinafter referred to as DQI).

The sub-stage of the construction of the DQI involves (a) the financial statements research, (b) the evaluated information, (c) the forming of the checklist, and (d) the forming of the DQI, which will be discussed in detail.

(a) Financial statements research is made to determine what financial statements are used in AID quality research. The previous research has shown that the AID quality is evaluated (i) by analysing the notes, i.e., one of the financial statements, which, in accordance with the International Accounting Standard 1 (TAS 1) “Presentation of Financial Statements” (

International Financial Reporting Standards (IFRSs) 2008), comprise “significant accounting policies and other explanatory information” whereas (ii) other financial statements are used only to the extent necessary to evaluate whether a certain requirement should have been disclosed.

(b) In the AID quality research, evaluated information, which is disclosed in the annual financial statements of enterprises, can be mandatory or voluntary.

Definition of the mandatory disclosed information is highlighted in scientific papers.

Abdullah et al. (

2015) determine that “mandatory disclosure is the minimum information which promulgated regulation requires from a reporting entity”. According to

Andre et al. (

2018), “the rationale for this reporting approach is that this kind of disclosures assists users of the financial statements to understand a company’s underlying economics and how their values are measured and change from year to year”.

Mandatory disclosed information in notes is described in the TAS 1 as follows (

International Financial Reporting Standards (IFRSs) 2008): “Notes contain information in addition to that presented in the statement of financial position, statement(s) of profit or loss and other comprehensive income, a separate statement of comprehensive income (if presented), statement of changes in equity and statement of cash flows. Notes provide narrative descriptions or disaggregations of items presented in those statements and information about items that do not qualify for recognition in those statements”. Usually, accounting standards indicate the list of mandatory disclosed information.

In paragraph 122 of the TAS 1 (

International Financial Reporting Standards (IFRSs) 2008), the informational requirements for notes are described in detail: The notes shall: (a) “present information about the basis of preparation of the financial statements and the specific accounting policies used in accordance with paragraphs” referred”; (b) “disclose the information required by IFRSs that is not presented elsewhere in the financial statements”; and (c) “provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any of them”. In the case of Lithuania, according to BAS 6 (Business Accounting Standards (BASs)), (a) the notes provide the information on the enterprise’s operations required by BAS 6 and explain the material amounts of the financial statements and the reasons for the changes. (BAS 6, Article 15); (b) the section of the notes for the accounting policies discloses the information about accounting policies applied by the entity, which affected the data of the financial statements, and is likely to influence the decisions of the users of information of the financial statements (BAS 6, Article 19); and (c) explanatory notes should include the information required by BAS 6 that discloses the nature of the enterprise’s operations, financial position, financial performance, and cash flows and is not provided in other financial statements (BAS 6, Article 20).

Hellman et al. (

2018) evaluated the benefits of the mandatory disclosure and emphasise that “imposing mandatory disclosure requirements is done to ensure that companies with incentives to avoid disclosure will still provide a minimum level of information, i.e., comply with the mandatory disclosure requirements”. Furthermore, the researchers (

Hellman et al. 2018) point out that “entities, auditors and regulators might previously have interpreted ‘shall be disclosed’ as a mandatory requirement to disclose the item referred to (when applicable)”. However, in 2014, the revised version of International Accounting Standard 1 (hereinafter referred to as IAS) adopted the idea that “an entity need not provide a specific disclosure required by an IFRS if the information resulting from that disclosure is not material” (

International Financial Reporting Standards (IFRSs) 2008). Furthermore, this requirement has been transposed in the national accounting standards, i.e., BAS 6, Article 18. Hence, “an entity does not have to disclose the ‘shall be disclosed’ information if that information would not be material” (

Hellman et al. 2018). Thus, in the future, it becomes appropriate to revise interpretations of the definition of “mandatory disclosed information”.

Furthermore, “companies would provide disclosures even if they were not required to, and they do provide voluntary disclosures beyond regulatory requirements” (

Hellman et al. 2018).

In prior research (

Hassan and Marston 2010;

Pivac et al. 2017), it was indicated that the “disclosure index could include mandatory items of information and/or voluntary items of information”. In this research, the DQIs include both mandatory and voluntary information.

(c) The third phase of the construction of the AID quality index is the forming of the checklists.

According to

Pivac et al. (

2017), “disclosure indexes are commonly based on a text analysis” conducted through an a priori defined checklist. In this research, the original checklists are structured to evaluate the AID quality of the tangible assets in the annual financial statements of the private sector entities (enterprises) of Lithuania. This method of research is chosen since (i) the AID quality of tangible assets in private sector entities (enterprises) of Lithuania is investigated for the first time, while the checklists to evaluate the AID quality were not produced in previous research. (ii) Information on tangible assets, which is mandatory to be disclosed in BASs (in particular in BAS 6), differentiates from the required information in IFRSs (in particular in IAS 16 “Property, plant and equipment”). Hence, there is no possibility to use indexes previously compiled in other countries.

This research examines how the non-current tangible assets presented in the statement of financial position are detailed in notes. Three checklists are formed, which will be discussed in detail.

First, we will discuss the assumptions about why it is appropriate to make several different checklists. In accordance with the BASs (specifically BAS 6), the notes shall present information in order to provide a fairer understanding of the information contained “in other financial statements and to disclose additional material information excluded from such other statements”. Having conducted the theoretical analysis of the BASs (standards), three levels of information that could be included in the notes might be distinguished. Firstly, the BAS 6 establishes the general requirements for small, medium, and large enterprises for (a) the contents of notes and (b) the explanatory notes. Hence, the standard contains a list of specific requirements and describes them as minimum requirements. Secondly, the explanatory notes for medium, large, and public-interest enterprises must provide the additional information required by the standard BAS 6, i.e., this additional information is mandatory for medium, large, and public-interest enterprises, whereas for small enterprises, this additional information is optional, provided voluntarily.

Based on the above-mentioned information, a checklist is created to analyse the information that all enterprises—small, medium, and large—shall disclose, i.e., mandatory disclosed information for all—small, medium, and large—enterprises (hereinafter referred to as DI_M_SMLE). This checklist is given the abbreviation ChL_M_SMLE.

Appendix A (

Table A1) presents the checklist ChL_M_SMLE formed by information required by the BAS 6. The checklist consists of 22 requirements for the financial year 2016 (compared to the 16 requirements for the financial year 2008), which are divided into two groups: (1) Accounting policies of assets and its change (2 requirements) and (2) change of the carrying amount of an asset during the reporting period (20 requirements for the financial year 2016 and 14 requirements for the financial year 2008). It should be noted that this group is divided into two sub-groups including change of the carrying amount of (a) an asset presented in financial statements at the acquisition cost or revalued amount, as well as investment property presented in financial statements at the acquisition cost, and (b) investment property presented in financial statements at the fair value.

The second checklist is created from the information that should be disclosed by medium, large, and public-interest enterprises. Thus, this checklist includes (i) the information that shall be disclosed by all enterprises—small, medium, and large (DI_M_SMLE), and (ii) the additional information that shall be disclosed by medium, large, and public-interest enterprises (hereinafter referred to as ADI_M_MLE); it should be noted that this disclosure is voluntary for small enterprises. Thus, the checklist in question contains mandatory requirements for medium and large enterprises (hereinafter referred to as DI_(M_SMLE + M_MLE). The checklist in question is given the following abbreviation: ChL_(M_SMLE + M_MLE).

Appendix A (

Table A2) presents the checklist ChL_(M_SMLE + M_MLE) formed by information required by the BAS 6. The checklist consists of 11 requirements, which are divided into three groups: (1) Accounting policies of assets and its change (5 requirements), (2) change of the carrying amount of an asset during the reporting period (it is worth noting that in the checklist ChL_M_SMLE this group is analysed in detail, i.e., 20 requirements for the financial year 2016 and 14 requirements for the financial year 2008, whereas in this checklist, this group is evaluated as one summarised indicator), and (3) other information disclosed (5 requirements). As it is shown in

Appendix A (

Table A2), information ADI_M_MLE contains 8 requirements.

The third checklist (see

Appendix A (

Table A3)) not only includes (i) mandatory disclosed information (i.e., the information that shall be disclosed by all enterprises—small, medium, and large (DI_M_SMLE) and (ii) additional information, which shall be disclosed by medium, large, and public-interest enterprises (ADI_M_MLE), but also (iii) voluntarily disclosed information (referred to as DI_V). The checklist in question is given the following abbreviation: ChL_(M_SMLE + M_MLE + V). In comparison with the checklist ChL_(M_SMLE + M_MLE) (

Appendix A (

Table A2)), the checklist ChL_(M_SMLE + M_MLE + V) (see

Appendix A (

Table A3)) additionally includes 4 voluntary disclosures, which is further discussed in detail.

(i) Presentation of the definition of non-current tangible assets in notes (item G0.1). According to IAS 16, “Property, plant and equipment are tangible items that: (a) are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes; and (b) are expected to be used during more than one period”. Whereas in accordance with the national accounting standard (BAS 12), the definition of non-current tangible assets is augmented by one more requirement, i.e., the acquisition cost is equal to at least the minimum cost of non-current tangible assets established by the entity.

(ii) Presentation of the recognition criteria of non-current tangible assets in notes (item G0.2). In addition, Article 7 of BAS 12 provides two additional conditions: (1) “the entity can reliably measure the acquisition cost of the asset”, (2) “risk related to tangible asset has been transferred to the entity”. This is consistent with the discussion generated in the scientific literature (

Bullen and Crook 2005) that one of the issues to be discussed in accounting theory and practice is the possible insufficiency of the content of the definition of assets in terms of recognition of resources as assets, i.e., it is necessary to identify additional criteria for the conformity of assets to non-current tangible assets. Therefore, it becomes important to clarify the criteria according to which enterprises recognise non-current tangible assets and whether it is declared in the notes.

As these requirements (G0.1 and G0.2) are not required by BASs (standards), the disclosure of this information is considered voluntary.

(iii) Asset recognition methods (item G1.1). Tangible assets “are recorded in accounting at their acquisition cost” (BAS 12, Article 11), therefore the enterprise shall establish a methodology for calculating this cost. For example, this methodology should (i) discuss in detail the potential additional costs that are added to the purchase price (BAS 12, Article 12); (ii) in the case the assets are produced independently, the cost that will constitute the production cost (BAS 12, Article 16). Disclosure of asset recognition methods in the notes is not a mandatory requirement and is therefore considered voluntary.

(iv) Presentation of the residual value of an asset in notes (item G1.6). In the accounting of the non-current tangible assets’ exploitation, an enterprise selects the residual value (BAS 12, Article 57). BAS 12 declares that “the residual value is estimated by an entity”. The aforementioned disclosure is also voluntary.

(d) The fourth phase of the construction of the AID quality index is the forming of disclosure quality index (DQI). It involves the following: (i) Assessment of a score to each requirement included in the checklist, (ii) the DQI expressed in the formula, and (iii) the formation of the scale of the DQI evaluation.

(i) To assess a score to each requirement included in the checklist, in accordance with the scientific literature, the weights of the items included in the index can be equal (

Street and Bryant 2000;

Hassan et al. 2008) or differ (

Pivac et al. 2017). In this research, considering that every disclosure is equally important, the AID quality appertaining to an unweighted index has been assessed. A score of “one” is given to the disclosed requirement, and “zero”—otherwise.

In the research, a problem-solving approach (

Kanapickienė and Keliuotytė-Staniulėnienė 2019) is used to provide the criteria in notes, which are not followed by zero meaning (which confirms that the scope of the researched criterion during the reporting period equals zero) or a hyphen (which confirms that during the reporting period an enterprise did not have any assets); however, to leave the cell empty, without inserted data, is regarded as the refusal to present any specific information.

The accounting policies provided in the notes are considered analogically unless specified that there are no changes in the mandatory disclosures during the investigated period; then, the information is considered not disclosed regarding the research criterion.

(ii) The DQI is expressed in the formula following the viewpoint of

Street and Bryant (

2000) and

Pivac et al. (

2017). The researchers claim that “the total disclosure index is measured as the sum of scores awarded to a particular entity in a particular year divided by the maximum number of applicable items (in order not to penalise entities for disclosing clearly non-applicable items of information)”.

The

DQI of an enterprise is computed by the following equation:

where

ADS is the actual disclosure score of an enterprise,

N is the number of disclosed elements,

n—of non-applicable elements, and consequently (

N −

n) is the number of applicable elements.

The

ADS used in Equation (1) is calculated as follows:

where

xi is the score of

i component of the

DQI (

i = 1 to

N) (a score of 1 is assigned to the disclosed requirement, and 0—otherwise), and, as mentioned above,

N is the number of disclosed elements.

(iii) Finally, in the formation of the

DQI evaluation scale, it is considered to use the

DQI rating scale by

Pivac et al. (

2017). This means that the

DQI should be interpreted in the following way: (i)

DQI = 0: no information is disclosed, (ii) 0 <

DQI ≤ 20:

AID quality is poor, (iii) 20 <

DQI ≤ 40:

AID quality is low, (iv) 40 <

DQI ≤ 60:

AID quality is average, (v) 60 <

DQI ≤ 80:

AID quality is sufficient, (vi) 80 <

DQI ≤ 100

AID quality is high, and (vii)

DQI = 100: information is fully disclosed.

Finally, it is necessary to point out that in this research three DQIs are formed:

DQI_M_SMLE—disclosure quality index (DQI) formed by mandatory disclosed information required for all—small, medium, and large—enterprises;

DQI_(M_SMLE + M_MLE)—disclosure quality index (DQI) formed by (a) mandatory disclosed information required for all—small, medium, and large—enterprises, and (b) additional disclosed information required for medium, and large enterprises;

DQI_(M_SMLE + M_MLE + V)—disclosure quality index (DQI) formed by (a) mandatory disclosed information required for all—small, medium, and large—enterprises, (b) additional disclosed information required for medium, and large enterprises, and (c) voluntarily disclosed information.

The second stage of the assessment of the element of financial statements AID quality—the process of the DQI application—involves two key sub-steps (

Figure 1), the realisation results of which are defined in

Section 4. It is also worth mentioning that the maintenance and improvement of the model must be realised, which would ensure the feedback on the model.

In this research, the evaluation of the AID quality using the disclosure quality indexes consists of four stages. The first stage is the evaluation of the AID quality according to disclosure quality indexes (DQI1, DQI2, and DQI3) components (including the correlation between DQI components). The second stage is the trend analysis of the enterprises DQIs of the investigated period (including using the DQI rating scale). The third stage is the analysis of the results of the descriptive statistics. Finally, to answer the research question R1, concerning whether the AID quality increased statistically significant during the investigated period, statistical tests are used. In order to verify that data are drawn from a normally distributed population, the choice of a statistical test is needed. Regarding a small sample, the key tests for the assessment of normality include the test introduced by Shapiro–Wilk. The null hypothesis (H0) states that the data come from a normally distributed population. When the result of the Shapiro–Wilk’s test is significant (p < α = 0.05, α—the level of significance), rejecting the null hypothesis means rejecting the assumption of normality for the distribution. Therefore, DQI is explored with a non-parametric Wilcoxon signed-ranks test. If the assumption of normality is valid, the paired-samples t-test is used.

3.3. The Independent Variable and Development of Hypotheses

To explain accounting practice, the research is based on several theories, which we will briefly discuss.

As stated in the literature, in the private sector, the agency problem arises as principals (such as shareholders or investors of an enterprise) typically do not intend to participate in business management and that responsibility is delegated to the agents (such as managers of an enterprise). Therefore, when principals invest their resources or funds in a business, the agents have an incentive to make decisions in the best interest of principals. However, self-interested agents might make decisions that are useful only for them. On the other hand, according to the information asymmetry theory (

Healy and Palepu 2001;

Hassan et al. 2009;

Mamun and Kamardin 2014;

Abdullah et al. 2015;

Leung et al. 2015;

Hassan 2018), usually, principals are not involved in the enterprise management. Therefore, agents have access to higher-level information compared to principals, which, in turn, leads to an information asymmetry problem. Hence, as

Abdullah et al. (

2015) and

Fonseka et al. (

2019) have highlighted, the situation might arise when agents (managers) have incentives to withhold information in their own rather than the principals’ (shareholders’) interest (moral hazard). As a result, according to

Hellstrom (

2009), “the information asymmetry between the different types of investors may lead to low liquidity of company’s shares since the uninformed investors will be unwilling to trade under such circumstances”.

The concept of agency and information asymmetry theories are the background of positive accounting theory. As emphasised by researchers (

Falkman and Tagesson 2008), “accounting has the function of producing information for decision-makers”. Therefore, according to

Hellstrom (

2009), the selection of accounting principles becomes particularly important as “using different accounting principles will lead to different financial results even if the underlying activities are the same”; moreover, as

Falkman and Tagesson (

2008) have highlighted, the selection and applying of accounting methods depend on “the relative power between agents and principals”. Consequently,

Dey et al. (

2018) have argued that “disclosure is seen as a monitoring mechanism in agency theory”.

Another theory that is used to explain the disclosure issue is legitimacy theory that evolves “a social contract between the organisation and society” (

Dilling and Caykoylu 2019). This theory predicted that, as

Chalmers and Godfrey (

2004) state, “organisations react to demands of diverse groups with responses aimed to legitimise their actions”, and, according to Baber (1983) (as cited by

Susbiyani et al. (

2014)), “organisation will continue work to ensure that the organisation operates within the frame and norms that exist in community or environment in which the organisation was and continues to ensure that activities of the organisation accepted by stakeholders as legitimate”.

Gabrini (

2013) discusses an issue when disclosure is analysed as “a mechanism used by organisations to manage legitimacy”, where “legitimacy is affected more through voluntary actions”, however, the mandatory disclosure has “little influence over perceptions of legitimacy held by stakeholders”. Consequently, disclosure can be understood as a communication tool in order to inform stakeholders about the financial position and the performance of the organisation, which ensures the legitimacy of the organisation’s activities.

The signalling theory explains how, through information disclosure, an enterprise “sends a signal to the market to reduce information asymmetry, minimize financing costs, and increase company value” (

Dilling and Caykoylu 2019). According to this theory, as

Pivac et al. (

2017) have claimed, “voluntary disclosure signals the management’s desire to disclose its superior performance to external parties, because it will enhance the reputation of the company and its position in the market”. Lastly, political cost theory emphasises that enterprises that gained political visibility in the market “tend to increase disclosure as a means of mitigating potential political costs” (

Dey et al. 2018).

Accounting disclosure decisions are explained based on these theories. In order to improve understanding of the information contained in financial statements for financial statement users, enterprises disclose additional information in the notes. On the one hand, it increases the quality of the information in other financial statements. On the other hand, when relevant items are not disclosed properly, the value of information to financial statement users reduces. As a financial consequence, according to

Hellstrom (

2009), “the lack of information negatively affects the efficient allocation of resources in the capital markets”, i.e., “investors experience uncertainty about the enterprise value and potential risks” and accordingly the cost of capital increases, and the value of the enterprise decreases. Furthermore, the liquidity of shares might lower, whereas “the uninformed investors will be unwilling to trade under such circumstances”. To summarise, agency conflicts and information asymmetry increase the demand for proper disclosure.

The information gap between uninformed and informed financial statement users might be filled in a number of ways, by disclosing mandatory or voluntary information. The first alternative is the disclosure requirements by the standard-setters. The researchers (

Healy and Palepu 2001;

Hellstrom 2009) support that mandatory disclosure enhances the credibility of management disclosure. As previous studies showed (

Zimmerman 1977;

Adi et al. 2016), another alternative is the voluntary disclosure, i.e., “information provided by company management which is not compulsory according to the accounting regulation in a respective country” (

Hellstrom 2009), making “more private information as public” (Evan and Sridhar 1996 (as cited by

Mamun and Kamardin 2014)). According to the signalling theory, as

Pivac et al. (

2017) have stated, voluntary disclosure supports the most profitable enterprises to provide the market with more and better information.

In summary, in this research, independent variable selection is explained using these theories.

3.3.1. Size of Enterprise

The issue that large enterprises tend to disclose more financial information than smaller enterprises (

Riahi-Belkaoui 2001;

Ali et al. 2004;

Hassan et al. 2008;

Hellstrom 2009;

Hellman et al. 2018) is considered to be based on different theories. According to the agency theory, this dependence might exist due to (a) large enterprise tending to bear lower costs of the (i) processing (

Hassan et al. 2008) and (ii) accumulation of information (Singhvi and Desai (1971) (as cited by

Hassan et al. (

2008)); (b) it has (i) more marketable securities and (ii) greater ease of financing (Singhvi and Desai (1971) (as cited by

Hassan et al. (

2008);

Hall et al. 2014).

Hellstrom (

2009) has supported this approach and stated that the complexity of operations, as well as the costs for gathering and reporting financial information, might explain a different level of disclosure between large and small enterprises. Consequently, according to

Dey et al. (

2018) and

Hellman et al. (

2018), agency theory claims that larger enterprises have higher information asymmetry between agents (managers) and principals (owners); hence, agency’s costs increase. To reduce these costs, larger enterprises disclose more information than smaller enterprises. As

Gabrini (

2013) has implied, one of the factors related to the theory of legitimacy is the visibility that is determined by the size of the entity. According to the political cost theory, larger enterprises tend to provide greater transparency to reduce political costs (

Hassan et al. 2008;

Dey et al. 2018).

According to researchers (Ahmed and Courtis (1999) (as cited by

Barako et al. (

2006));

Wang et al. (

2008), studies conducted at the end of the last century demonstrated that the size of enterprise has a significant impact on the disclosure level. Furthermore, current research has shown mixed results. (i) One group of researchers (e.g.,

Barako et al. 2006;

Nandi and Ghosh 2013;

Dilling and Caykoylu 2019;

Rep et al. 2019) has supported that the size of an enterprise is positively related to high disclosure quality or disclosure level. The analysis of current research studies carried out by

Dilling and Caykoylu (

2019) has shown the same result. (ii) Other researchers (

Street and Bryant (

2000);

Street and Gray 2002) have indicated that the size of an enterprise is not related to the disclosure level. Based on these arguments, the first hypothesis is formulated:

Hypothesis 1 (H1). Size of enterprise is significantly positively related to the level of the accounting information disclosure quality (AID quality).

Different units of measurement are selected by researchers to measure the size of the enterprise. (1) Total assets are frequently used as the measurement unit of size by researchers both in the private sector (e.g.,

Street and Bryant 2000;

Street and Gray 2002;

Barako et al. 2006;

Hassan and Marston 2010;

Dilling and Caykoylu 2019) and public sector (e.g.,

Laswad et al. 2005;

Mir et al. 2019). Concerning the variability in total assets between enterprises, this variable is transformed into the logarithm of total assets (

Chalmers and Godfrey 2004;

Hassan et al. 2008;

Hellstrom 2009;

Nandi and Ghosh 2013;

Houcine 2017;

Wang 2017;

Dey et al. 2018;

Nguyen et al. 2020), as

Hassan et al. (

2008) emphasise, “to normalize the distribution”. (2)

Hassan and Marston (

2010) and

Street and Gray (

2002) agree that sales could be considered to measure the size of the enterprise. (3) The size of the enterprise is measured by market capitalisation. For instance, (i)

Street and Gray (

2002) have used market capitalisation; (ii)

Dargenidou et al. (

2006),

Wang et al. (

2008),

Leung et al. (

2015), and

Andre et al. (

2018) used the logarithm of the market capitalisation. The attention should be drawn to

Hassan and Marston’s (

2010) viewpoint that “market value can be developed without recourse to corporate disclosure vehicles”. Furthermore, in legal documents (e.g., the Republic of Lithuania Law on Small and Medium-size Business Development (2017)), the size of the enterprises is determined by three parameters: (i) Total assets, (ii) annual revenue, and (iii) a number of employees. Also, researchers have used several parameters in order to determine the size of the enterprise, e.g.,

Rep et al. (

2019) have taken into account both total assets and annual revenue.

As mentioned above, the following are units of measurement of an enterprise-size used in this research: The size of the enterprise is measured by (i) the natural logarithm of total assets (lnTA), (ii) the natural logarithm of sales (lnS), and (iii) the average annual number of employees (TEmp) (

Table 1).

3.3.2. Enterprise Debt-Paying Capacity and Enterprise Indebtedness

Different theories explain the debt-paying capacity and indebtedness impact on disclosure, and their approaches to this issue may vary. As

Dey et al. (

2018) have pointed out, the agency theory evolves that enterprises “with lower liquidity disclose more information to reduce conflict between shareholders and creditors”. On the other hand, the signalling theory argues that enterprise (

Dey et al. 2018) “with a high liquidity ratio tends to disclose more information in order to be differentiated from other firms with a lower liquidity ratio”.

This issue is also interpreted differently by researchers. The financial condition should be a significant factor for disclosure levels since, as

Giroux and McLelland (

2003) have stated, “an entity has incentives to signal financial health to creditors, voters and other users of financial information”.

Highly leveraged enterprises take a high financial risk (

Abudy et al. 2016). Therefore, according to

Lin et al. (

2019), they, particularly listed enterprises, could “tend to conceal such risk from investors by window-dressing their accounting information”; consequently, their AID quality decreases. This view is supported by other researchers. For instance, according to Einhorn (2007) (as cited by

Leung et al. 2015), indebted companies publish less information. The findings of studies (

Nandi and Ghosh 2013;

Dilling and Caykoylu 2019) have shown that the degree of disclosure is negatively related to leverage. The findings of the research by

Leung et al. (

2015) have suggested that enterprises with poor current performance “are more likely to engage in the concealment of voluntary narrative information in annual reports”. On the contrary,

Hassan et al. (

2008) and

Wang (

2017) have pointed out that enterprises with high leverage tend to disclose extensive information. Finally,

Nguyen et al. (

2020) have pointed out that experimental studies have shown two opposite perspectives: (i) The enterprises with higher solvency are more active to publish information by demonstrating the operational well-being of enterprises; and (ii) enterprises with low solvency tend to publish more information by justifying their status with external audiences.

Furthermore, a third alternative interpretation is possible. By investigating the derivative financial instrument disclosure,

Chalmers and Godfrey (

2004) have argued that “disclosure does not affect leverage related covenants directly”; however, “it can provide information that is vital to assessing the likelihood of such covenants being breached”. Moreover, “the disclosure of value relevant information reduces the price protection mechanisms instigated by debtholder”. The findings of research by

Wang et al. (

2008) are analogous, i.e., leverage “does not provide an explanation of the disclosure level variation in the Chinese context”.

Based on these statements, the second and third hypotheses are formulated as follows:

Hypothesis 2 (H2). Debt-paying capacity (solvency and liquidity) of enterprise is significantly positively related to the level of accounting information disclosure quality (AID quality).

Hypothesis 3 (H3). Indebtedness of enterprise is significantly positively related to the level of the accounting information disclosure quality (AID quality).

The researchers select different measures to assess debt-paying capacity.

For empirical research of the disclosure issues in annual reports, other researchers have used solvency and liquidity ratios as control variables. For instance,

Leung et al. (

2015) have measured the current performance of an enterprise by Tobin’s Q ratio, i.e., the ratio of the sum of the market value of equity and total debts to total assets. Moreover, these researchers have used the leverage (measured as debt ratio, i.e., long-term debt scaled by total assets) and the liquidity ratio (measured as the sum of cash and short-term investment-to-total assets) as control variables. As the control variable in the model of voluntary disclosure in the annual reports of Chinese listed firms,

Wang et al. (

2008) have used leverage (measured as the ratio of total debt to equity).

In this research, the debt-paying capacity of an enterprise is measured by these parameters (

Table 1): (a) To assess solvency, (i) the ratio of total liabilities to total assets (TL/TA), and (ii) the ratio of long-term liabilities to total assets (LTL/TA) is used; (b) to assess liquidity, the ratio of current assets to current liabilities (CA/CL) is used. Moreover, the indebtedness of an enterprise is measured by the natural logarithm of total liabilities (lnTL).

3.3.3. Tangible Assets of Enterprise

IAS 16 describes the non-current tangible assets, i.e., property, plant, and equipment, as “tangible items that: (a) are held for use in the production or supply of goods or services, for rental to others, or administrative purposes; and (b) are expected to be used during more than one period”.

Increasing tangible assets would be likely to influence economic decisions made by users of financial statements, and they should be more concerned about the performance of an enterprise.

The issue of influence assets on accounting information disclosure is more discussed in the research of the public sector. For instance, as stated by

Mir et al. (

2019), the assets of local government influence compliance with mandatory disclosure.

Garcia and Garcia-Garcia (

2010) have established that when local governments invest heavily, they consider more the reporting of financial information. Moreover,

Bunget et al. (

2014) show that “the municipalities with the largest value of intangible assets show a higher disclosure index”.

Analysing the size of an entity as an independent variable, it can be seen that in the works of some researchers, the size of an entity is measured by entity assets both (i) in the private sector (e.g.,

Street and Bryant 2000;

Street and Gray 2002;

Hassan and Marston 2010) and the public sector (e.g.,

Gordon et al. 2002;

Laswad et al. 2005;

Mir et al. 2019). As the object of this research is the tangible assets of an enterprise, these assets are selected as an independent variable. Based on this statement, the fourth hypothesis is formulated as follows:

Hypothesis 4 (H4). Tangible assets of the enterprise are significantly positively related to the level of accounting information disclosure quality (AID quality).

In this research, the tangible assets of an enterprise are measured by the ratio of tangible assets to total assets (TngA/TA) and the natural logarithm of tangible assets (lnTngA) (

Table 1).

3.3.4. Profitability of Enterprise

The literature review has provided evidence that the profitability of the enterprise also affects disclosure quality.

Researchers (

Street and Bryant 2000;

Street and Gray 2002) have determined that studies conducted at the end of the last century demonstrated mixed results regarding the association between profitability and level of disclosure. Furthermore, current research results have varied too. For instance,

Nguyen et al. (

2020) agree with the agency theory, which states, “if enterprises operate effectively, the managers will proactively disclose more information”. Furthermore, these authors have presented the reverse view too: “the enterprises who do not well operate will also publish much to explain the situation of the company to shareholders”. Theoretical analysis conducted by

Hassan et al. (

2008) has also shown mixed results: Ali et al. (2003) (as cited by

Hassan et al. (

2008)) have provided “evidence of a positive relationship between profitability and compliance level”; Wallace and Naser (1995) (as cited by

Hassan et al. (

2008)) have identified “a negative relationship between these variables”.

It is important to point out that the empirical research results have varied too.

Hassan et al. (

2008),

Wang et al. (

2008),

Nandi and Ghosh (

2013), and

Leung et al. (

2015) have shown that profitability is positively related to disclosure quality. Conversely,

Dilling and Caykoylu (

2019) have found that profitability has a negative and significant relationship with disclosure quality. Furthermore,

Pivac et al. (

2017) have analysed and compared “the level of annual report disclosure quality for listed companies in selected European transition countries” (Croatia, Montenegro, Romania, Serbia, and Slovenia). In these countries, research results have varied, i.e., correlations between the DQI and financial performance indicators (ROE, ROA) were not significant for enterprises in all countries, except in Romania, where the correlation between ROA and DQI was negative and significant.

Based on these statements, the fifth hypothesis is formulated as follows:

Hypothesis 5 (H5). Profitability of enterprise is significantly positively related to the level of accounting information disclosure quality (AID quality).

The researchers have selected different measurement units to assess profitability: Return on equity (ROE), return on assets (ROA), and net profit margin are frequently used as the measurement unit of profitability by researchers. (1)

Street and Bryant (

2000),

Barako et al. (

2006),

Wang et al. (

2008),

Pivac et al. (

2017), and

Rep et al. (

2019) have used a return on equity (ROE) measurement unit. However, ROE calculation is different, for instance, (i) according to

Barako et al. (

2006),

Wang et al. (

2008), and

Rep et al. (

2019), ROE is defined as the ratio of net profit to equity; (ii) according to

Street and Bryant (

2000), ROE is defined as the ratio of net profit before tax to equity. (2)

Hassan et al. (

2008),

Leung et al. (

2015),

Pivac et al. (

2017), and

Nguyen et al. (

2020) have used return on assets (ROA). Furthermore, measurement units are selected differently, for instance,

Hassan et al. (

2008) used the ratio of profit before tax to total assets; meanwhile,

Nguyen et al. (

2020) have used the ratio of profit after tax-to-total assets). (3)

Pivac et al. (

2017) and

Dilling and Caykoylu (

2019) used the net profit margin that

Dilling and Caykoylu (

2019) described by the ratio of net profit to revenues.

In this research, the profitability of an enterprise is measured by three parameters (

Table 1): (i) The ratio of net profit to equity (ROE), (ii) the ratio of net profit to total assets (ROA), and (iii) the ratio of net profit to sales (NP/S).

3.3.5. Control Variables

In this research, the financial ratios and financial data of enterprises discussed in previous research are used as control variables. The following six control variables of an enterprise are collected (

Table 1): (i) Debt turnover (measured by the ratio of total liabilities-to-sales (TL/S)), (ii) tangible assets (measured as tangible assets per employee (TngAperEmp)), (iii) revenue (measured as sales per employee (SperEmp)), (iv) tangible assets turnover (measured by the ratio of sales to tangible assets (S/TngA)), (v) total assets turnover (measured by the ratio of sales to total assets (S/TA)), and (vi) own financing (measured by the ratio of total liabilities to equity (TL/E)).

3.4. Model Specification and Variable Measurement

To identify specific factors (enterprise’s characteristics) that have an impact on the AID quality, a panel regression model is used.

In this research, to test Hypotheses H1–H5, the invariant constant panel model, including (1) three disclosure quality indexes (DQI) as a dependent variable, (2) 12 independent variables, and (3) the control variables, is created (

Table 1):

where (1) a dependent variable—the disclosure quality index (

DQI)—is used to measure the

AID quality, (2) 12 independent variables are divided into the five following groups: (i) Size of enterprise (average annual number of employees (TEmp), the natural logarithm of total assets (lnTA), the natural logarithm of sales (lnS)), (ii) debt paying capacity of enterprise (the ratio of total liabilities to total assets (TL/TA), the ratio of long term liabilities to total assets) (LTL/TA), the ratio of current assets to current liabilities (CA/CL)), (iii) indebtedness of enterprise (natural logarithm of total liabilities (lnTL)), (iv) tangible assets of enterprise (the ratio of tangible assets to total assets (TngA/TA), the natural logarithm of tangible assets (lnTngA)), and (v) profitability of enterprise (the ratio of net profit to equity (ROE), the ratio of net profit to total assets (ROA), the ratio of net profit to sales (NP/S)). In the model, the six control variables (ConVar) are used.

Coefficient C is identical for all observed objects (enterprises); β1, β2, …, β12 represents the particular coefficient in a linear combination of 12 independent variables; j = 1 to 37 and corresponds to enterprises; t = 1 to 3 and corresponds to year; k = 1 to 6 and corresponds to control variables, and ε corresponds to error. Binary and multivariate regression models are established using the method of least squares. Having eliminated insignificant variables, the final panel regression model is formed.

The creation of a DQI factors’ panel regression model consists of three stages. (a) Firstly, binary panel linear regression models are constructed to reject insignificant variables. If certain independent or control variables highly or moderately correlate with each other, they cannot be applied in the same panel regression model. After primary analysis, for each of the five hypotheses (

Section 3.3.1,

Section 3.3.2,

Section 3.3.3 and

Section 3.3.4), one “best-performing” (based on t-value and

p-statistics) independent variable is selected ((i) if the relevant variable is not statistically significant according to the initial analysis but is the only one on the basis of which the certain hypothesis is tested, it is included in the model in any case; (ii) if all independent variables on which the certain hypothesis is tested are statistically insignificant, the “best performing” insignificant variable is selected for further analysis). (b) Secondly, several primary multivariate linear regression models are created for each DQI (i.e., for DQI1, DQI2 and DQI3). (c) Thirdly, after checking all reasonable combinations of variables, the final DQI factors’ models are created. Furthermore, in all of the final DQI models, the variables—specific factors (enterprise’s characteristics)—should be significant at least at the 90% confidence level.

It should be noted that this research is limited to panel estimation by using the invariant constant model (i.e., C is identical for all objects). The evaluation of DQI factors using the models with fixed effects (different Cj for each enterprise) and dynamic effects (same C but different error αj = C + vi), as well as the inclusion of additional internal and external factors, could increase statistical characteristics of the assessment of DQI factors, which could be a further direction for future research.

The descriptive statistics of dependent, independent, and control variables are presented in

Appendix B,

Table A4.

In total, 69.46% of enterprises notes of which were analysed were private limited liability companies, while 40.54% were public limited liability companies. Throughout the investigated period, the distribution between the types of enterprise remained unchanged. Most analysed enterprises (94.59% in 2007, 97.30% in 2008, and 89.19% in 2016, respectively) provide full notes. However, during the reporting period, the comparative share of enterprises providing a summary of notes had been increased (from 5.41% in 2007 to 10.81% in 2016). Here, “summary of notes” is considered to be “notes” where accounting policies and accounting principles are shortly described; however, other explanatory information is not provided. The section of accounting policies is presented in most of notes of enterprises; moreover, the comparative share of such enterprises increased slightly (94.59% in 2007, 97.30% in 2008 and 2016, respectively).

{kind=link}