1. Introduction

The agrifood products market has never before contained as many niches as it does at this moment in history. One of those niches, in particular, has been around for thousands of years. However, it only gained official label status in the 18th century in the form of geographical indications (GIs). Official designations of this nature have their origins in Portugal, with Port wine, which had its production rules and characteristics established by the Marquis of Pombal who created a specific public company to deal with its case. In France, the pioneering Portuguese spirit was echoed years later by standardizing a protection system for agrifood products and wines based on characteristics arising from their places of origin. According to

Barham (

2003), GIs establish their differentiation of products on natural, human and historical factors. The sum of these three factors comprises what

Allaire (

2018, p. 63), based on the work of

Goodman (

2002), refers to as “the immaterialization of food and the institutionalization of quality”, a concept that goes far beyond the specific soil and climate of a region capable of providing specific characteristics to certain products.

Although they date back thousands of years, this type of product has only recently gained official character under French, Portuguese and Italian legislation, among those with greater prominence. However, this market is too complex to be formed solely by the institutional factors.

Ilbery and Kneafsey (

1999) demonstrate that the niche market for local specialty food products (SFPs) is located in the intersection between producers and institutional and consumer networks. The point of intersection of all these networks of actors is in the arena of exchange. A significant number of works focus on the products or consumers. However, little attention has been given to the arena itself. For this reason, this work’s importance is to shed light on the materialization of commerce in the arena of economic action and the differences between Mercosur and the European Union on this matter.

Over the last few years, many efforts were taken to encourage the market to provide alternatives with intrinsic food values. One known origin-related path is localized agrifood systems (

Fernández-Zarza et al. 2021;

E. Barham and Sylvander 2011). Many scholars have studied the strategy of trust-building through GI. However,

Dias and Mendes (

2018) show that, despite the growing number of published articles, most of them focus on southern European countries, are concentrated on four topics and are predominately empirical. Thus, there is a lack of literature comparing Mercosur and the EU, electronic commerce regarding such products, as well as multiple product market analysis, since most works focus on a single or a few products (

Dias and Mendes 2018;

Roselli et al. 2018;

Teuber 2010;

Renard 1999;

Agostino and Trivieri 2014;

Addor and Grazioli 2002). As such, the present work seeks to help fill the gap in the literature about this issue. Although this market has the same conformation structure globally, apparently, each region of the globe has a different proportion of each element. For example, the GI market in the European Union (EU) has reached incomparable numbers of registers compared to all other regions. In South America, on the other hand, the Southern Common Market (Mercosur) has an even greater area of production and a greater diversity of agrifood products. However, this diversity apparently has not developed in this specific market. To better understand this market’s functioning, this work seeks to compare the difference between the performance of GI products and categories on this market exchange arena in Mercosur and the European Union by analyzing the e-retail supermarkets. To answer this question, this work understands that only a thorough investigation of this link in the market can provide the pieces of this complex puzzle. What are the characteristics of this market inin both blocs? What sort of goods do both markets address and sell? What are the commercialized products’ origins in both blocs? Due to little comparative attention having been paid to the matter in terms of economic blocs, this work focuses on the market arena for GI products and its differences between Mercosur and the EU.

To answer that question, this initial research paper proposes to deepen the existing research by looking at the diversity of product offerings on the websites of significant retail supermarkets from selected countries of both the EU and Mercosur in a quantitative manner. The investigation considers e-retail supermarkets in Portugal, Spain, France, Italy, Germany, Greece and Poland on the European side. In addition, the research looks into e-retail supermarkets from Argentina, Brazil, Paraguay and Uruguay on the South American side. In the sections that follow, the work uses economic sociology to illuminate the market issue. Finally, both economic blocs’ markets are analyzed to point out the differences between them on the practical effects of institutional support of Intellectual Property (IP) based on the data collected in the field.

By doing so, this work hopes to identify the practical functioning of the GI market in Mercosur and the EU’s electronic supermarkets. Additionally, economic sociology theory is used with the intention to reveal corporate control issues, the embeddedness of the state and productive groups relation to this economic niche, and the market-driven strategy of promoting specific product categories.

The paper starts by presenting the formation of agrifood niches through the changing of food production–consumption logic due to globalization, followed by how economic sociology tries to explain market functioning through the theory of markets and institutional influence. Additionally, it develops the state of the art by bringing present considerations of the GI market into the findings on labeling efforts to decommodify it.

After this, it explains the methodology used for collecting data from available online supermarkets to characterize the products, the categories found and the origins of those products. Additionally, it graphically explains the phases of analysis followed in the present work.

Subsequently, the results found for the analyzed data are displayed, the graphic results are presented, and the major figures discovered relating to the collected material are described. This section is followed by a discussion of these results, including analyzing them, matching them to the existing economic sociology literature, and their implications on the market. Finally, the work ends with a summary of the developed work, its findings and suggestions for future works and policies towards market evolution.

3. Methodology

As a comparative proposal of analysis, this work recognizes the necessity of adequate different realities. Social sciences often require the use of common concepts in both compared realities and acknowledge the sociocultural differences between them, and do not assume a universality (

Smelser 1967;

Mahoney 2007). Thus, this work compares the market in the same arena of the same modality of the IP protection of products and considers all the differences considered by

Fracarolli (

2021). Additionally,

Sartori (

1991) points out the need for a finalistic means of comparison, for which reason this work seeks to find out how the market in both regions differs and the reasons for that, including whether it could be improved.

An alternate comparative approach proposed by

Ragin (

2014) describes a modern construction of the comparison, based on the calibration, of the qualitative outcomes and the set-theoretic relations regarding the different realities. This way, the present work understands that a more in-depth explanation is required. Thus, it uses economic sociological tools as an interdisciplinary approach (

Smelser 2003) to address the problematic and leading causes and reasons, as the ones proposed by

Swinnen (

2007,

2010,

2016) on niche agrifood market formation and by

Fligstein (

1996,

2002,

2008a,

2008b) on how markets stabilize and are constructed. The quantitative data will be used to support the qualitative analysis. Hence, considering the contributions of both authors, the hypothesis assumed is that the EU’s market will have a significantly more endogenous influence on its products. Additionally, the countries from southern Europe will have a substantial dominance in the markets of both economic blocs.

This work uses mixed methods of quantitative and qualitative research design. It compares the categories of product offerings, their origin, the penetration of GI products, and the difference between both economic blocs. In addition, the work maps the sources of GI agrifood products, excluding wine, aromatized wines and spirits. Finally, the work also evaluates the cultural aspects involved in constructing the niche market regarding IP.

This research consists of the comparison of three essential aspects of GI in retail markets. The first one is to analyze the offerings of GI agrifood products advertised by web retail supermarkets. The second is to map the origins of these goods, comparing Mercosur and the EU. The third one is to analyze the GI systems according to their inside and outside influence on web retail super- and hypermarkets. The sum of these three aspects can indicate how institutions build GI agrifood markets in each bloc.

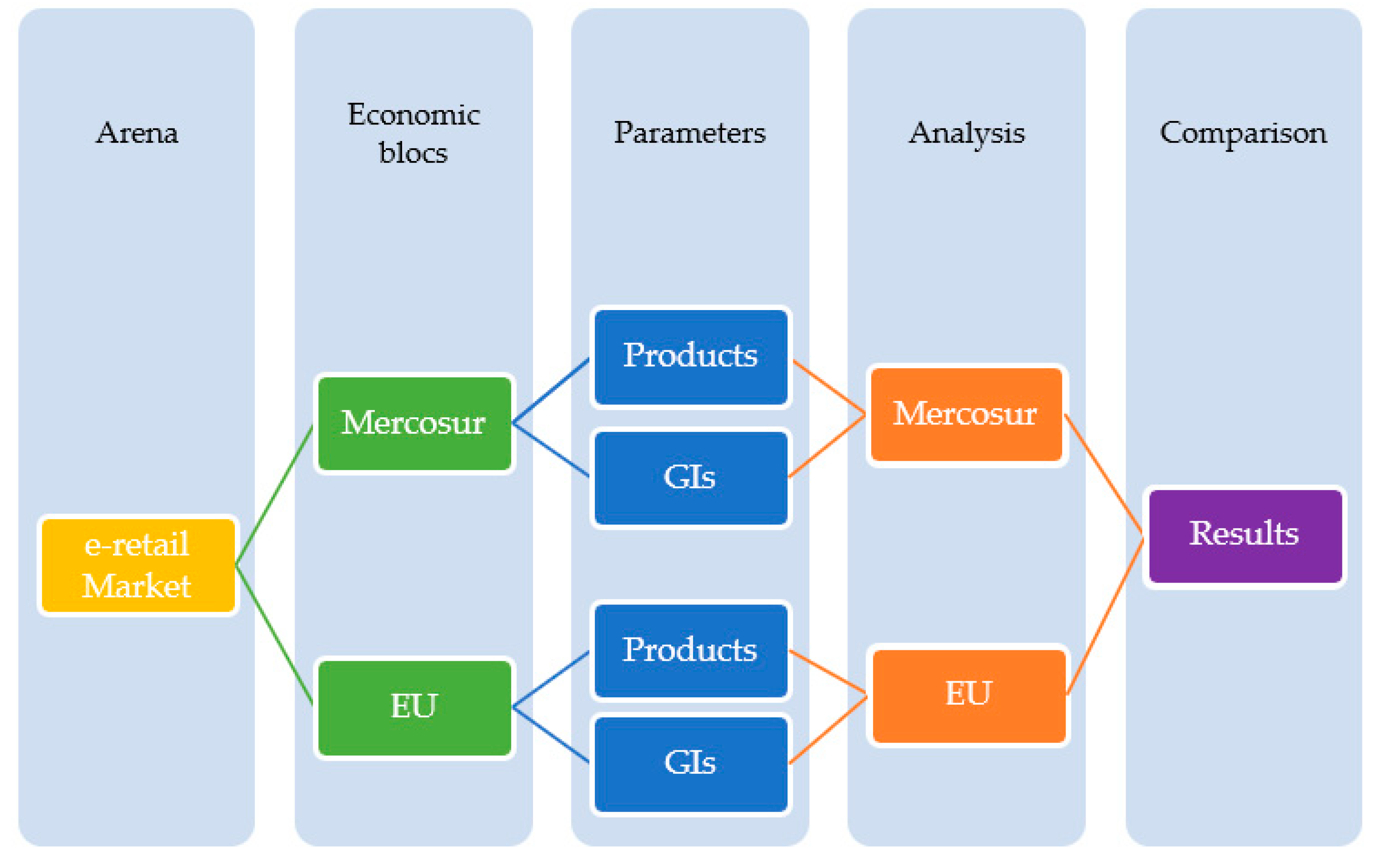

The analysis consists of five parts. Firstly, the arena of exchange where the transaction of goods happens is selected—in this case, the chosen arena is the super- and hypermarkets available online, i.e., the e-retail market. Secondly, the regions where these trades happen are chosen—since this work aims to compare two economic blocs, Mercosur and the EU, these are the regions of the randomly selected e-retailers. Thirdly, data relating to the number of products and the variety of GIs present in online retail supermarkets of these blocs is collected. Fourthly, the analysis of these indexes is undertaken in both categories, considering GI categories and their origin. Finally, the comparison between Mercosur and the EU is conducted. After that, a discussion of the findings takes place and possible outcomes are debated. Over the following subsections, we detail each step of this analytical work according to

Scheme 1.

Since “markets are socially constructed arenas where repeated exchanges occur between buyers and sellers under a set of formal and informal rules governing relations among competitors, suppliers, and customers” (

Fligstein and Calder 2015, p. 1), they also need to be also investigated while considering these biases. Thus, the intention is to collect data indicating the GI products markets’ differences from the perspective of both economic blocs.

Considering specific issues, it is necessary to clarify some details. This work involved a search for products and respective GIs on retail supermarkets and hypermarkets that allow web shopping. If the website requires an address to shop, the center of the country’s most populated city is used. All GI agrifood products registered on the EU or Mercosur database were considered. Only agrifood products were collected and considered for this work; wines, spirits, and aromatized wines were not considered.

However, before searching the products sold across all countries, it was necessary to find the existing GIs. To do that, it is crucial to understand that there is a single register source for the EU, but there are independent ones for each of Mercosur’s countries, according to Fracarolli (

Fracarolli 2021). Therefore, this work contemplated all EU registers and all registers in each Mercosur country. On the European side, this work examined the EU database at eAmbrosia (

European Commission 2020). Overseas, the considered data were from the available dataset from each authority from Argentina, Brazil, Paraguay and Uruguay (

INPI 2020;

Prosur Proyecta 2020;

Ministerio de Agricultura, Ganadería y Pesca 2020); however, Paraguay is still in the process of registering products and Uruguay only has registers of wine products. Since this work does not contemplate wines, spirits, or aromatized wines, there were no products from Uruguay or Paraguay.

For the data collection, we went through the websites of four major grocery retail supermarkets for all of the active members of Mercosur (Argentina, Brazil, Paraguay and Uruguay) and the most representative EU members (Italy, France, Spain, Portugal, Greece, Germany, and Poland). The criterion for choose these countries was the need to pick the most relevant GI markets of each. In the Mercosur case, all active members were selected due to most of the available countries allowing for comparison. Additionally, these countries chosen from the EU represent over 80% of the EU’s GI registers, which ensures a significant number of registrations for a relevant comparison. For each supermarket, all products with a GI label registered in the respective country were considered.

This work uses the EU criteria to separate the products into comparable categories available at the European Commission on eAmbrosia (

European Commission 2020). The categories for agrifood products are: 1.1 Fresh meat; 1.2 Meat products; 1.3 Cheeses; 1.4 Other products of animal origin; 1.5 Oils and fats; 1.6 Fruits, vegetables and cereals fresh or processed (FVC); 1.7 Fresh fish, mollusks and crustaceans and derived; 1.8 Others such as spices; 2.1 Beers; 2.2 Chocolate and derived; 2.3 Bread, pastry, cakes and alike; 2.4 Beverages from plant extracts; 2.5 Pasta; 2.6 Salt; 2.7 Natural gums and resins; 2.8 Mustard paste; 2.9 Hay; 2.10 Essential oils; 2.11 Cork; 2.12 Cochineal; 2.13 Flowers and ornamental plants; 2.14 Cotton; 2.15 Wool; 2.16 Wicker; 2.17 Scutched flax; 2.18 Leather; 2.19 Fur and; 2.20 Feathers.

3.2. Analysis

The proper analysis of the captured data in a single presentation of the numbers does not represent the market’s complexity. The use of graphical tools is significatively more representative and able to demonstrate in-depth aspects. Considering the broad-spectrum analysis, two approaches are necessary to bring light to this market. The first considers the number of GI products in the online markets of both Mercosur and the EU and the respective origins in each category. The second considers the diversity of GI registers in both economic blocs and their respective countries by category. To do so, using this data, a set of graphics will demonstrate the above mentioned.

The first analysis considers the number of products found over the 44 e-retail markets. Data will be analyzed from both Mercosur and the EU in terms of the origin of the found products and in terms of category representations on the product offerings. These data will show the most relevant type of products commercialized in Europe and Mercosur and which are the most appropriate sources of these products.

The second analysis relates to the diversity of the GI products commercialized in e-retail markets in both blocs. Data will be presented regarding the origin of the GIs found and the categories in which GI is sold in these markets. These results will show how these registers’ diversity is presented and how this is reflected in the e-retail market.

After all data and graphics are presented, the paper analyses the numbers, perspectives and meanings of all of the data. The data and graphics will show how the market behaves in terms of the number of products and the sector’s relevance. Each part of the graphics will appropriately represent the category’s share and its influence on this market. Afterward, in order to be comparable, both Mercosur and the EU will be put side by side on the treemap so they can be more intuitively represented. By doing so, the work focuses on the embedded aspects of local/global issues, such as the importance of niche markets. This methodology aims to clarify some aspects, such as the role of origin-related production pointed out by

McMichael (

1996) and the market’s consumer arena objective as questioned by Hinrichs (

Hinrichs 2000). Additionally, as demonstrated before by

Belletti et al. (

2017), this work’s results can improve the policy towards proper regulation and valorization through development by enhancing knowledge of this market.

3.3. Comparisons

After all data are collected and analyzed separately, quantitatively and qualitatively, it is possible to compare this research paper’s two main aspects. Firstly, what is the difference between Mercosur and the EU for the reality of GI product commerce in online retail supermarkets? By comparing the number of products, we expect to see the difference between both in terms of product offerings and in terms of diversity of products. By comparing GI registers, we hope to see the reflection of how effective the system is in reflecting the registers into the actual market.

Secondly, by examining the treemap graphics, the comparison between both blocs will show the actual niche formation: i.e., from whom, to whom, and the categories of goods that are more relevant to this market. The results are expected to show how significant the GI agrifood market is in the e-retail sphere in both economic blocs via a qualitative and quantitative approach.

4. Results

This collected data resulted from the scraping of 2184 products from 44 online supermarkets from 11 countries. This search presented the selling of 314 different GI registered products. GI products’ search was conducted on four of the most popular grocery retail supermarkets in each country. Although some other relevant supermarkets could have been part of this research, many did not have an online shop. The results shown above are separated initially into economic blocs and posteriorly by the number of products and GI diversity.

4.1. European Union

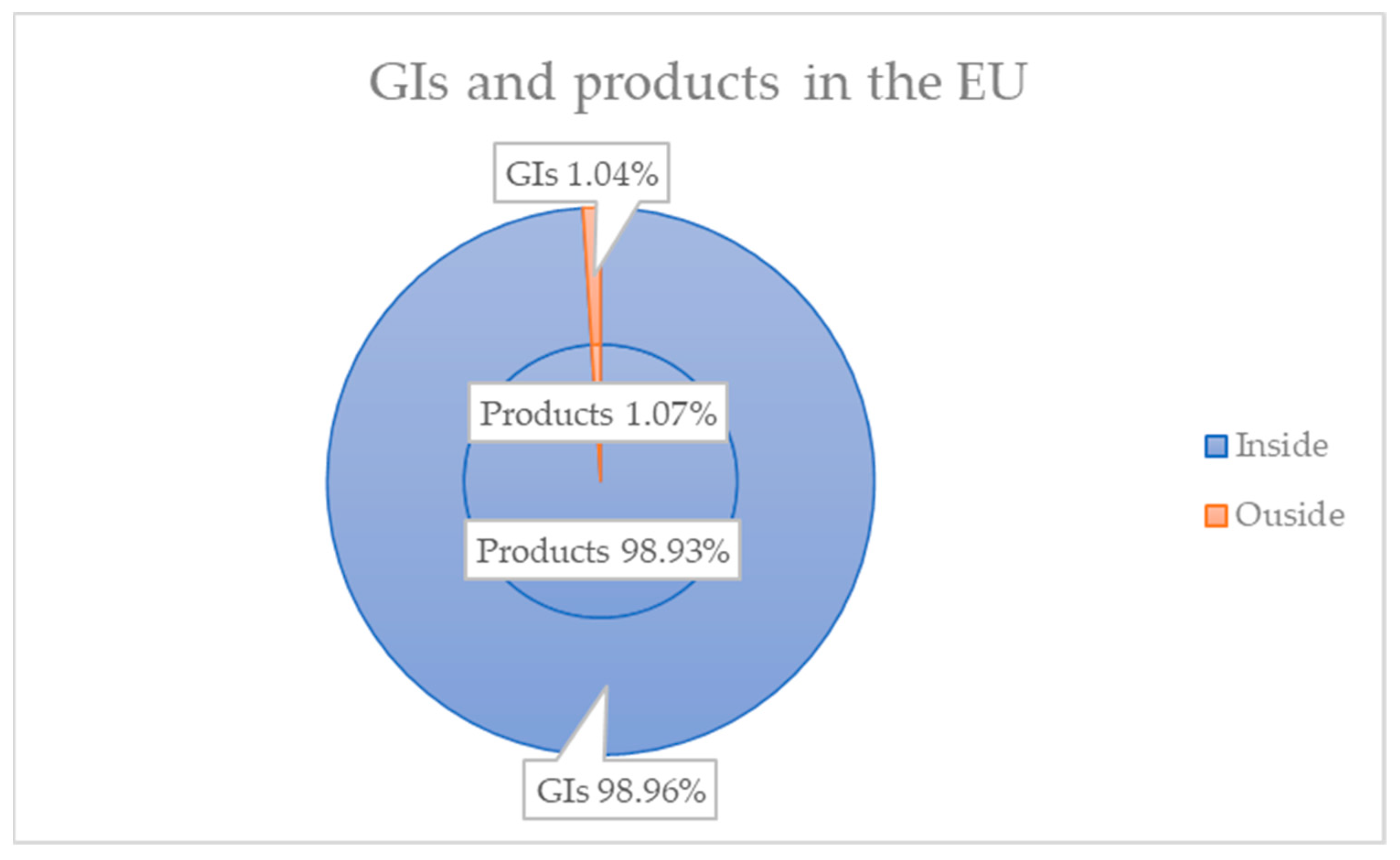

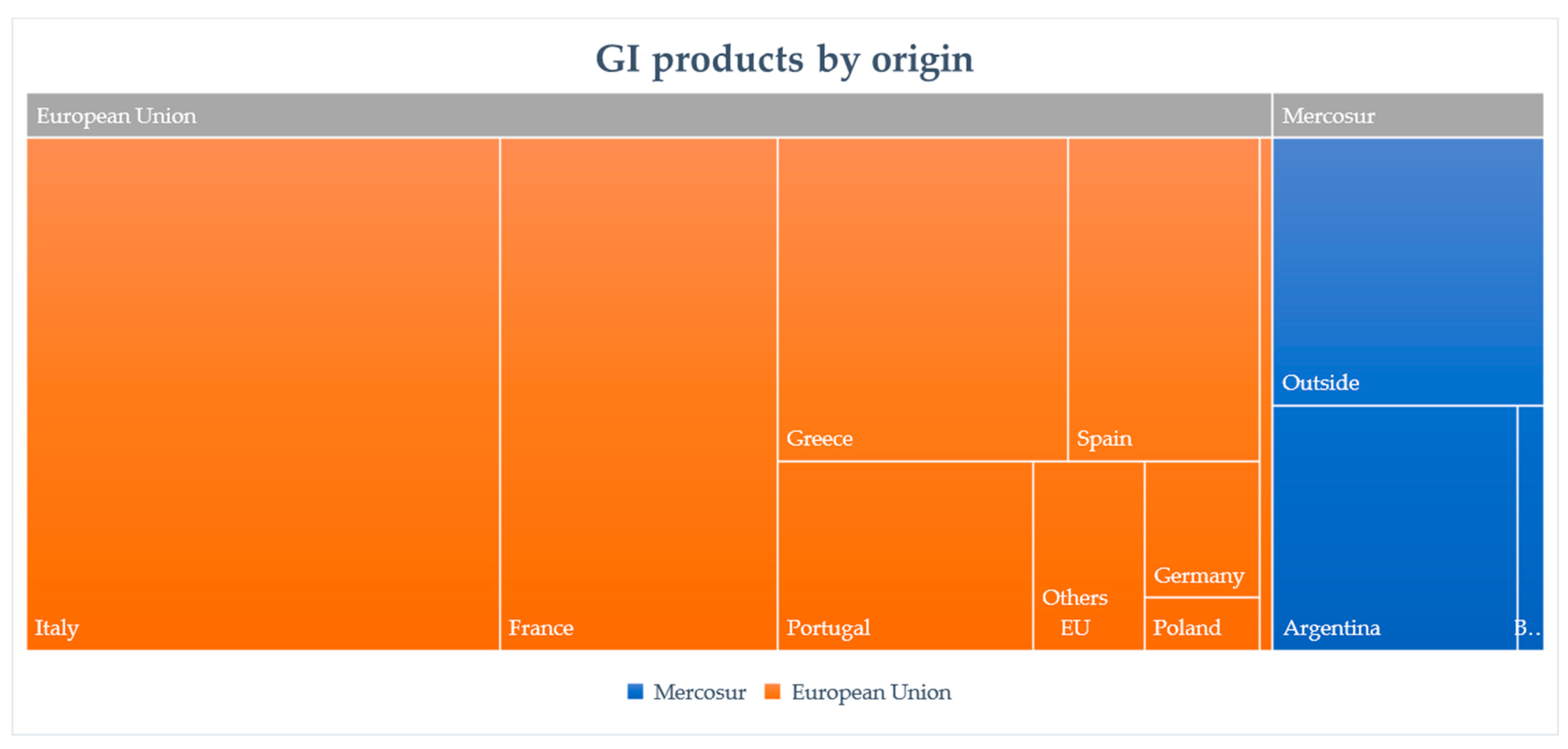

The empirical results of the data collection contained information from 28 online supermarkets across the eight countries. The survey found 1784 products labeled as GI products. From those products, 462, or 25.90%, were found in French supermarkets, with France being the country with the most products. Spain, on the other hand, with 128, or 7.17%, meaning that it was the country with the least number of products. Besides, of the 1706 GI products from the countries surveyed, the research found 59 other products from Austria, Denmark, Netherlands, and Ireland within the economic bloc, a total of 98,93% of the GI products from the bloc. Besides, seven other GI products from the United Kingdom (UK) and 12 from Cambodia were from outside the bloc, a total of 19 or 1.07%. No products from the Mercosur were found. Nonetheless, 1005 or 56.33% of the products belonged from the 1.3 category, the most relevant one. The categories 1.9, 2.0, 2.2, 2.4, 2.8, 2.9, 2.10, 2.11, 2.12, 2.13, 2.14, 2.15, 2.16, 2.17, 2.18, 2.19 and 2.20 presented zero products.

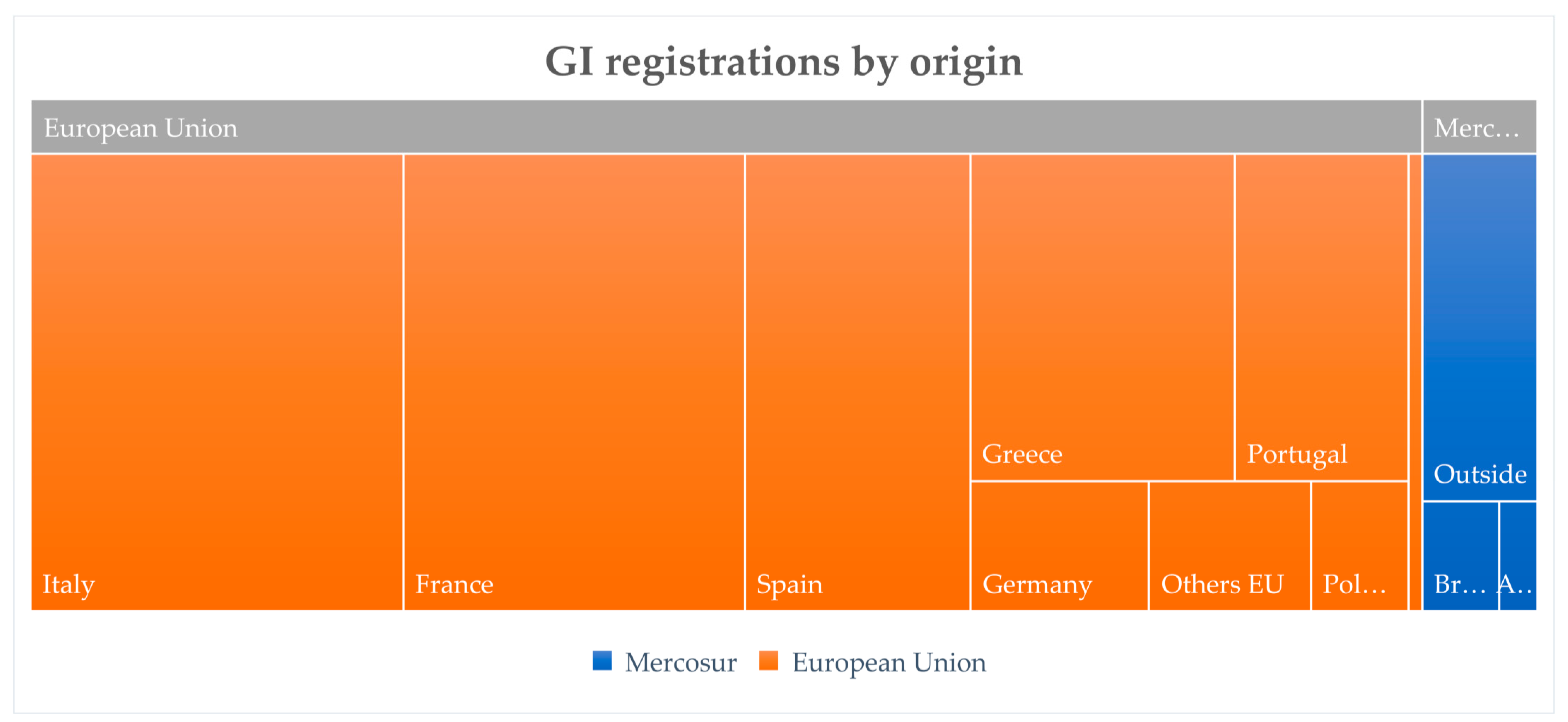

All these 1784 products constituted 289 different GIs. Besides the GIs from the surveyed countries, there were 276 different GIs from the surveyed EU countries, ten other GIs from other EU countries and three from outside the bloc. Italian markets showed 81, or 28.03%, different GIs from the researched countries, as the one with the greatest numbers. On the other hand, Poland has six, or 2.08%, different GIs, being the country with the lowest numbers. From the 10 GIs found from other EU countries, one belonged to the 1.2 category, and the other nine were found in the 1.3 category. With regards to the products from outside the bloc, the survey found two different GIs from the UK and one from Cambodia. Additionally, category 1.3 not only had the greatest number of products but was also the most numerous relevant category in the number of different GIs. Category 1.3 had 105 different GIs, or 36.33%. Since the categories 1.9, 2.0, 2.2, 2.4, 2.8, 2.9, 2.10, 2.11, 2.12, 2.13, 2.14, 2.15, 2.16, 2.17, 2.18, 2.19 and 2.20 presented zero products, no GIs could be summed up.

As presented, the variety of GIs from inside and outside the EU is significantly alike the number of products from inside and outside as well, as presented in

Figure 1.

Figure 1 shows that almost all of the products found in the survey come from countries that belong to the EU. Only about 1% of the products are from outside the bloc. The same happens when it comes to the varieties of GIs found in the EU e-retail markets survey. The GIs from outside the bloc found on the survey are barely representative, as it is only about 1%. This survey demonstrates how protective the bloc is of its own goods and how open it is to goods from outside. It demonstrates a severe protective system and the effectiveness of the EU policy towards valorization of inner goods.

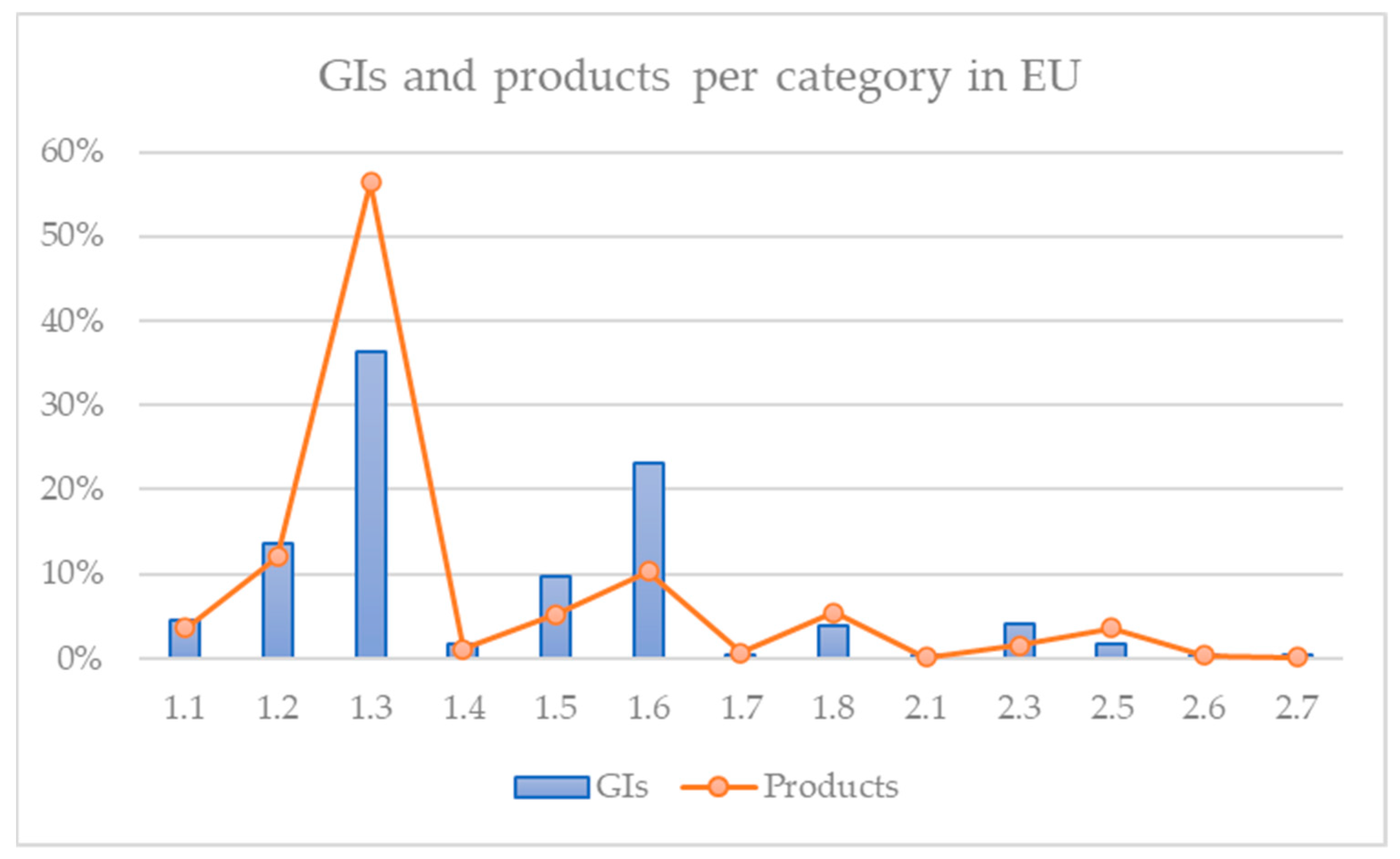

On the other hand, there is a minor difference between GI registers and the number of products in the EU’s e-retail markets regarding the categories of products. Such difference is clearly demonstrated in

Figure 2.

This second graph shows a different perspective. Concerning the products found over the course of the survey, it shows similar proportions of both products and varieties of GIs in each category. However, in terms of products, category 1.3 (cheese) has an evident distinctiveness from the others, consisting of almost 60% of products found. Furthermore, in terms of GI varieties categories 1.3 (cheese), 1.6 (FVC) and 1.2 (meat products) all consist of over 10% of products. However, these data also show the system’s concentration on promoting a few select categories, predominantly the cheese category.

4.2. Mercosur

The results of the Mercosur bloc presented significantly different findings from those of the EU. The empirical results of the data collected information from among the 16 online supermarkets of the four countries. The survey found 388 products labeled as GI products. From those products, 180, or 46.39%, were found in Argentine supermarkets, with Argentina being the country with most products. Paraguay, on the other hand, with 43, or 11.08%, was the country with the least number of products. Additionally, the GI products found from within the bloc were 185, or 47.68%. Besides, all other GI products found were from the EU, a total of 203 or 52.32%. The categories 1.1, 1.4, 1.7, 1.9, 2.0, 2.1, 2.2, 2.3, 2.4, 2.5, 2.6, 2.7, 2.8, 2.9, 2.10, 2.11, 2.12, 2.13, 2.14, 2.15, 2.16, 2.17, 2.18, 2.19 and 2.20 presented zero products.

All these 388 products constituted 25 different GIs. The GIs from Mercosur constituted a total of six, and the remaining 19 were all from the EU. From within the economic bloc, Brazilian markets showed three, or 50%, being the country with the highest numbers. Neither Paraguay nor Uruguay had its products available. All other 19 different GIs were: five in category 1.2; ten in category 1.3; two in category 1.5; one in category 1.6; and one in category 1.8. The EU countries with GI products available across Mercosur’s supermarkets were Italy, Spain, Greece, France, Denmark, and Portugal. Additionally, category 1.3 not only had the greatest number of products but was also the most numerous relevant category in terms of the number of different GIs. Nonetheless, 216 or 55.67% of the products belonged to category 1.8, the most relevant one, of which 169, or 78.24% of the 216 products were either coffee or Yerba Mate. All other products from this category were the Aceto Balsamico di Modena from Italy. Category 1.3 had 11 different GIs or 44% of all GIs found in Mercosur. Since the categories 1.1, 1.4, 1.7, 1.9, 2.0, 2.1, 2.2, 2.3, 2.4, 2.5, 2.6, 2.7, 2.8, 2.9, 2.10, 2.11, 2.12, 2.13, 2.14, 2.15, 2.16, 2.17, 2.18, 2.19 and 2.20 presented zero products, no GIs could be summed up.

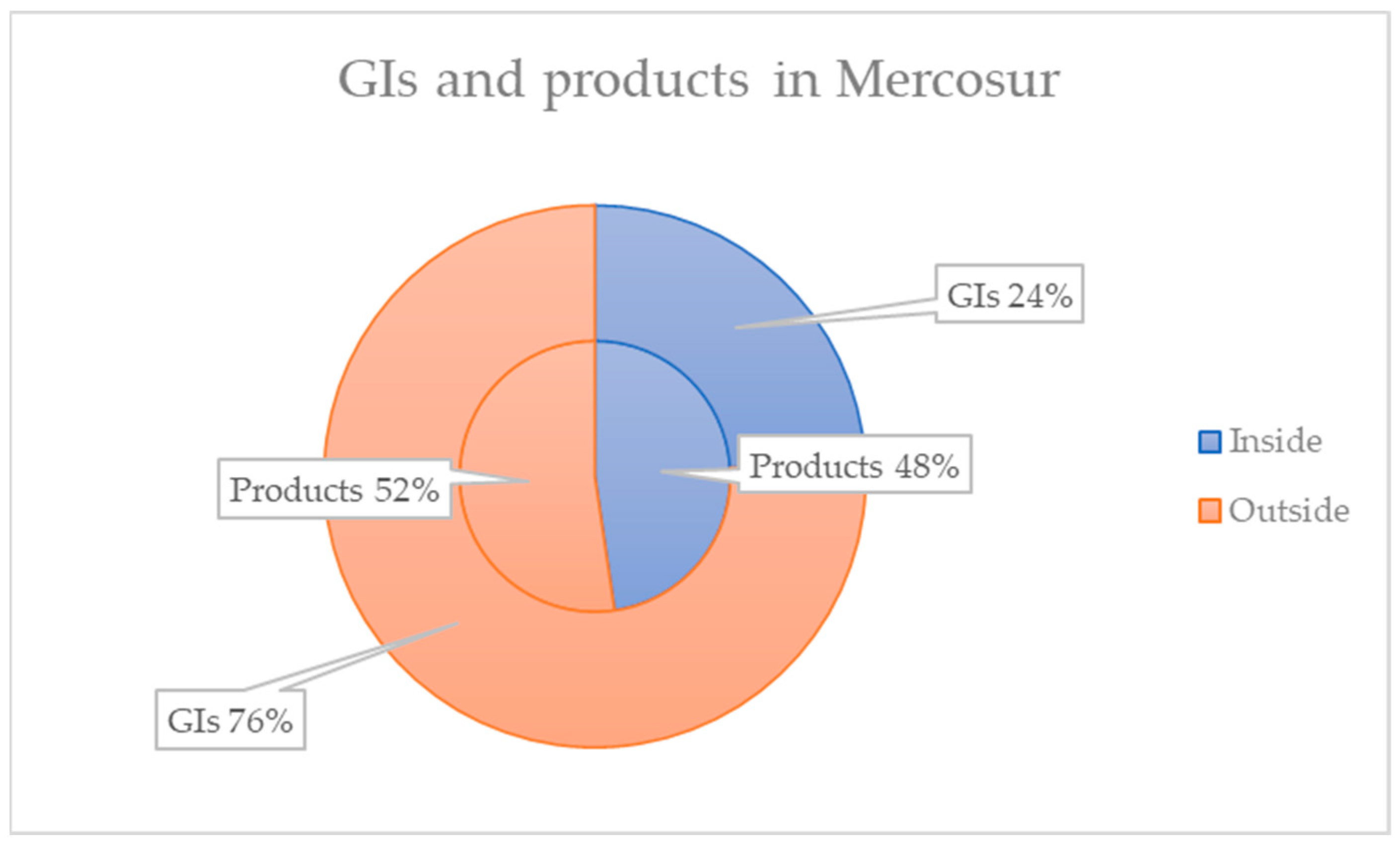

Conversely to the results presented in the above subsection, there is a significant difference between the number of products and the diversity of GI registers in Mercosur. Moreover, contrary to the EU, most products and GIs are from outside the economic bloc, as shown in

Figure 3.

On the Mercosur side, the data evidences a different situation from the EU. In terms of products, more than half of them were from outside the bloc. Likewise, the variety of GI that appeared in the results brings about a scenario where three-quarters of the GIs on the market come from outside the bloc. All of the products and GIs from outside the bloc come from the EU. This demonstrates the influence of the EU system over others, such as Mercosur. Additionally, the proportions demonstrated in this research show each system’s capacity to overcome one another.

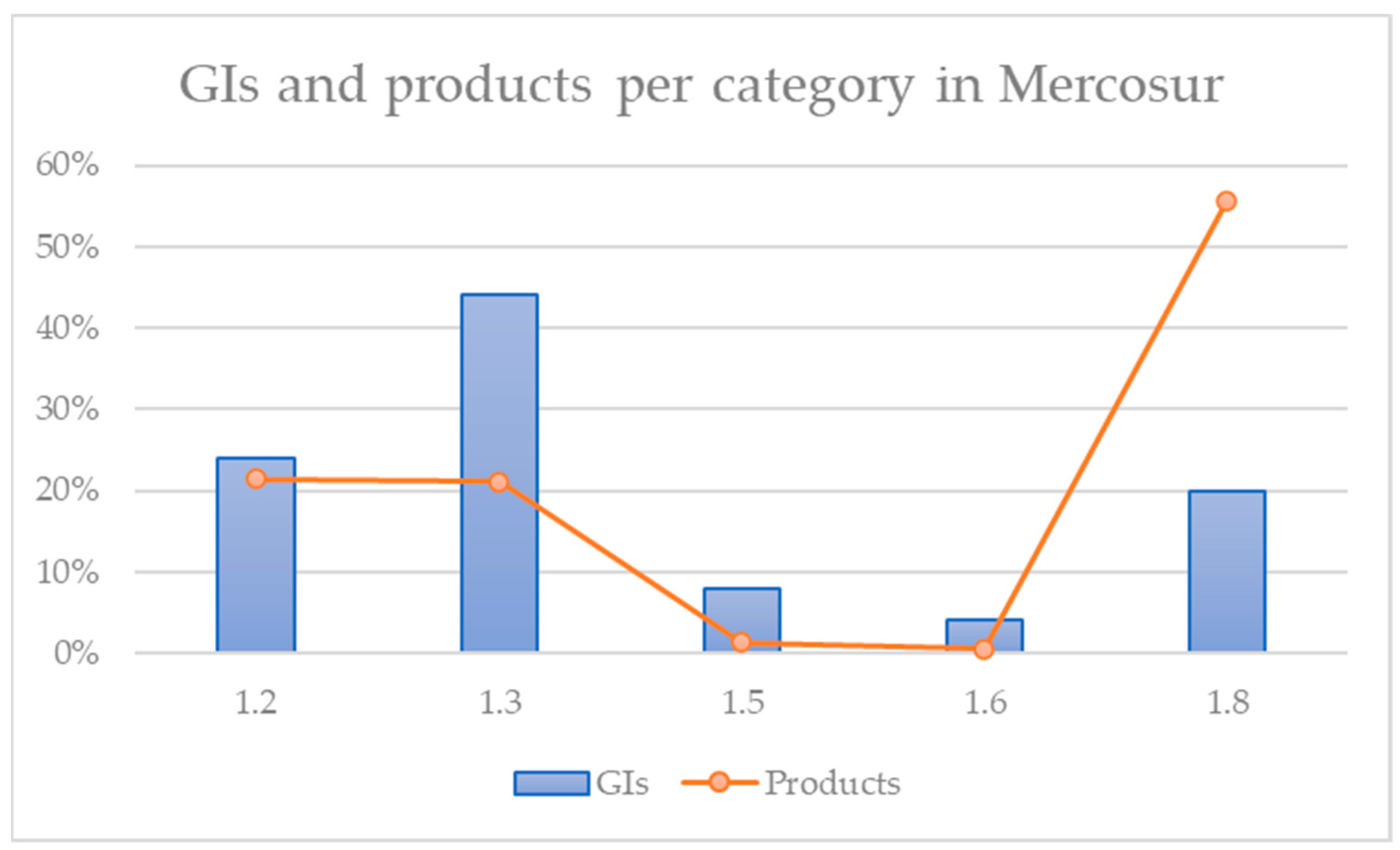

Regarding the categories that appeared on the South American side, fewer categories were present. Additionally, there is an unmatched proportion of GIs and products found between the categories 1.3 and 1.8, as demonstrated in

Figure 4.

In

Figure 4, the results present a disordered situation. Mercosur’s findings contained only five categories of products. Unlike the EU, Mercosur does not have registered products in all categories (

INPI 2020), and Paraguay and Uruguay have no registered agrifood products other than wine. Therefore, the results are more a sum of efforts than an aligned strategy. Even the category with the most products (1.8) is substantial due to only one product from inside the bloc (Yerba Mate, from Argentina) and a significant participation of a product from outside the bloc (Aceto Balsamico di Modena, from Italy). Moreover, over 40% of GIs found are European cheeses.

4.3. Overview

The overall results show a vast difference in GI products’ online market performance between Mercosur and EU. Meanwhile, the number of GI products found is 388 at Mercosur supermarkets and 1784 in the EU, representing 97 products per country for the former and 254.9 for the latter, as shown in

Figure 5. It shows the proportions of GI products by their origin found in each group of e-retail markets. The first observation allows the inference that most GI products found in the EU markets are from within its countries, mainly from the Mediterranean ones. On the other hand, in Mercosur’s markets, about half of GI products are from outside. The GI products from within are mainly from Argentina.

Besides the products, the issue of the origin and proportions of the wide variety of GIs present on the markets of each economic bloc is another important issue to consider. In

Figure 6, there is a clear demonstration of the data collected. This graphic shows that the products’ origins have a similarity between the number of products and the number of registered GIs present in each bloc. However, there are a few differences, such as the proportion of the variety of GI in Mercosur, which is now more abundant from countries outside the bloc.

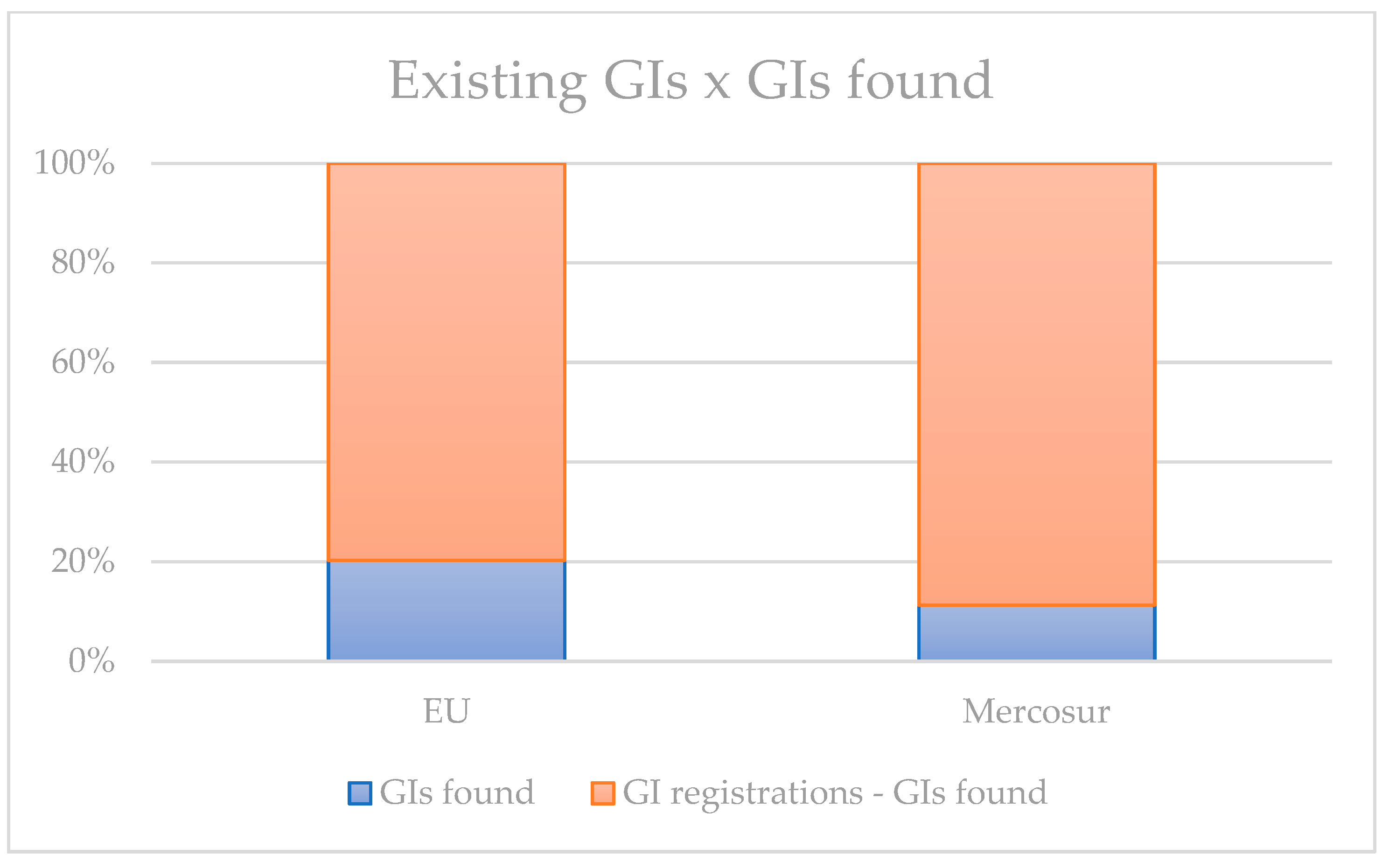

One other important aspect of the analysis is the issue regarding the number of registrations in each bloc and the number of GIs actually present on the e-retail market. As shown in

Figure 7, only a small portion of registered products appeared in the survey for both blocs.

Figure 7 shows that only 286, or 20.23%, GIs were found on the EU e-retail market from 1414 existing intrabloc registrations, while in Mercosur, only 6, or 11.32%, were found from 53 existing GIs. These results allow an inference that in the e-retail market, there is an absence of representation in both blocks, although, in Mercosur, the representation is even more fragile. This graph demonstrates that even a substantial number of registrations do not guarantee a product’s presence in the market—or at least in the e-retail market. Besides, this denotes that whichever economic bloc is in question has an underrepresentation of its protected products. However, considering the abundance of products in the absolute and relative terms that appeared on the survey, the results point to different reasons. The EU has demonstrated a significant number of products and GIs despite the poor results on representation. Therefore, the characteristics suggest that such a scenario is more related to a focused commercial strategy based on a robust institutional system, as is discussed later on. On the other side, considering the absence of products and barely representing GI varieties on major e-retail, the results suggest a discussion of the lack of systematic and coordinated policy towards developing the GI market. Nonetheless, all the possible causes and implications of such a path are discussed in the next section.

5. Discussion

The difference between the Mercosur and the EU is evident. Three aspects are crucial for understanding the differences between them: the number and diversity of GI products, the categories of these products and their GI diversity, and the products commercialized in this kind of arena.

The first one relates to the number of products.

Figure 1 and

Figure 3 show an enormous difference between the blocs on the number of products surveyed in e-retail markets. The EU presented 4.6 times more GI products than in the Mercosur region; however, this is not due to the number of countries, since the EU has 254.9 products per country and Mercosur has only 97. Additionally, the origin of those products is another important fact for this comparison. As presented in

Figure 5, only 19 products were from countries outside the bloc, while in Mercosur, the number of products from outside the bloc was 203, more than half of the total. All of the 203 products found in Mercosur’s markets were from the EU, and none of the foreign products in the EU were from Mercosur.

This asymmetry indicates that products’ presence is not from bilateral agreements but due to a nontariff protectionist strategy of the agrifood market developed by the EU, as endorsed by some works and more relevant in the Mediterranean region (

Josling 2006;

Huysmans and Swinnen 2019;

Huysmans 2020). Additionally, in the EU, the proportion of foreign products is similar to the variety of GI in the market. On the other hand, in Mercosur’s e-retail markets, the proportion of inside products in the market is twice the proportion of the variety of GIs. This is due to the abundance of one specific product from within, Argentine Yerba Mate, as demonstrated in category 1.8 of

Figure 4.

Consequently, such a scenario presents the assertiveness of

Granovetter’s (

1985) approach on the association of economics and social action. The clear difference between inner products in each bloc demonstrates that the market is not only a matter of supply and demand but construction of the field. The detachment of this niche category through IP rights configure a field as theorized by

Fligstein (

2001) and

Fligstein and McAdam (

2012). Thus, the stabilization of this market involves strengthening the social relationship between the productive class and the state, as supported by

Fracarolli (

2021) and the argument pointed by

Belletti et al. (

2017) on the influence on private and public interventions.

However, the creation of the GI label does not guarantee this new field. The institutional support of the state, as pointed by

Fracarolli (

2021), pushes the market stabilization and promotion not only within territories but towards a conception of control as conceptualized by

Fligstein (

2002) and tends to protectionist measures, as previously observed by

Swinnen (

2007,

2016) and

Huysmans and Swinnen (

2019).

The second aspect regards the products’ categories. There are significant differences between the economic blocs regarding the categories of products available via e-retail in both regions. In comparison, the EU has products in a broader diversity of categories. There were 13 categories of 30 on the electronic shelves of the EU. Among the products found, cheese products stand out, representing almost 60% of all products. On GI variety criteria, the cheese, FVC, meat products and oils represent more than 80% of GIs found, as shown in

Figure 2. Despite all categories, the products and GIs commercialized in e-retail supermarkets focus only on a few types of products. On the other side of the Atlantic Ocean, the scenario is even more restricted. Only five of all these categories had products on display in e-retail markets in Mercosur. Among these products found, such as the EU, the cheese category presented the most GIs on the market, as shown in

Figure 4. Products and GI registers in e-retail markets of Mercosur regarding categories. However, it did not reflect on the number of products on the market. Regarding the products’ criteria, category 1.8 had more than 50% of all found products. This is mainly due to the 153 “Yerba Mate” products and the 47 “Aceto Balsamico di Modena” products found in the supermarkets surveyed.

The difference in the variety of products found in both blocs brings the discussion onto the purposes of GI as a form of IP. Since fewer than half of the categories in both blocs had products available in e-retail markets, this raises a question on the reasons for such low performance and underrepresentation. Additionally, it needs to be asked where are these other products are sold and if they are sold. For such questions, further research is necessary. By number of registrations, wines, spirits and aromatized wines are the main focus of the EU GIs. However, this work looks only into agrifood products that exclude those beverages. There are few relevant protected categories for agrifood products presented by

Figure 2 and

Figure 4. The reasons for seeking such a modality of IP could be either counterfeit protection or economic enhancement and value-adding.

The results found in this research are in accordance with

Dias and Mendes’s (

2018) work regarding the variety of GI products. As discussed by

Meloni and Swinnen (

2018),

Huysmans and Swinnen (

2019) and

Josling (

2006), the southern countries of Europe stand out in this market. Therefore, it is a natural assumption that their product categories are brought into the spotlight. Such an event raises questions about the reasons for these categories to stand out, being important factors to consider in addition to the valuation premium due to the label, an ordinary object of studies (

Bureau and Valceschini 2003;

Crespi and Marette 2003;

Deselnicu et al. 2013;

Chilla et al. 2020). The distribution of product categories demonstrates the strength of the EU’s IP protection quality scheme and the strength of the federalism of the EU’s institutions (

Fligstein 2008a). However, the research showed that most GI registers in Mercosur and the EU are not reflected by the actual market, specifically in electronic supermarkets. Moreover, such performance shows that IP rights protection does not guarantee market share, and there are possible dominant groups within the influential groups. However, such an assumption requires further studies.

The last aspect regards the number of existing registrations and the number found on the e-retail survey. Despite the significant difference between the proportions of both blocs, both severely lack absolute representation. The EU has only 20% GIs found, and Mercosur has only 11% from the existing ones. The vast majority of products not found over this survey need to be deeply investigated. If not e-retail, what kind of market is their arena of commerce? Much study has been done on wines (

Agostino and Trivieri 2014;

Addor and Grazioli 2002;

Teuber 2011;

Meloni and Swinnen 2018) and other more consolidated agrifood markets (

Lamarque and Lambin 2015;

Roselli et al. 2018;

Dentoni et al. 2012;

Hughes 2006). Nevertheless, research on less famous products can bring light to the functioning of this market.

Further investigation is required on the current economic activity of GI registrations that did not appear in the survey. The variety of unrepresented products needs further investigation. The reasons for this could rely either on the failure of the value chain of economic activity, on strictly regional commerce or on the lack of socio-political performance to guarantee similar representation for other products in the same categories. Again, the stratification of these categories and the concentration of categories sustain

Swinnen’s (

2007,

2016) argument that the embeddedness of social organizations and state institutions develop arrangements that favor particular groups. The underrepresentation of such GI products enlightens the market on the matter of the results of embeddedness between groups of producers, commerce arenas and state institutions. Markets are social actions, as stated previously by

Granovetter (

1985),

Abramovay (

2004), and

Allaire (

2010), which require interventions by all involved parties in order to build and stabilize. The GI market is no different and this is reflected on e-commerce as demonstrated. Consequently, the EU has a more stabilized and solid market, despite a significant lack of registered GIs in the arena.

Therefore, considering the EU and Mercosur results, the market’s configuration approached points for strategic analysis. The EU, despite having a broader range of categories with significantly more registered GIs as well as translation of these GIs into products, there is a clear focus on goods such as cheese, meat products, oils and FVCs. On the other hand, Mercosur has only a few categories represented, not only in products available via e-retail but also on registrations (

Fracarolli 2021). The divergent focus on strategy between countries is reflected in a market that cannot develop its full potential. It indicates that the focus on some products may incentivize others to seek GI protection. The focus on categories of products can improve commerce and benefit others. This slow snowball effect can boost commerce relations and serve as a bargaining chip subject to include other matters, also requiring further investigation.

Nevertheless, the intensifying of trade can benefit “decommodified” networks of producers by cooperation. Such detachment of products allows the institutionalization of commerce to operate in an embedded way through the state, which can now bargain for differentiated economic treatment. In this case, the Mercosur–EU agreement in the final stage involving GI products could benefit the market, although, some interest groups with higher tier state relations may operate to set asymmetric standards for privileged actors (

Swinnen 2010,

2016).

6. Conclusions

This work aimed to compare Mercosur and the European Union in terms of the performance of GI products and categories in this market exchange arena by analyzing e-retail supermarkets. To do such work, the investigation surveyed 44 e-retail supermarkets in 11 countries, seven of which were from the EU and four from Mercosur, in order to compare the GI market of both economic blocs in terms of product offerings, variety of products and effectiveness of registration. It consisted of a five-part analysis, according to

Scheme 1. First, the research consisted of agrifood products labeled as GI, excluding wines, aromatized wines and spirits, resulting in 2184 products from 44 online supermarkets from 11 countries. This search presented the selling of 314 different GIs. Second, after the survey, the work classified the products according to the eAmbrosia database. Finally, it analyzed the collected data according to three essential aspects of GI in retail markets: GI offerings, the origin of the goods and the geographical influences from each bloc.

The survey of these websites revealed an expected difference between the two blocs. The differences are revelatory. The EU has a much more active GI market, well represented from within in terms of both products and GIs, and focused on specific goods categories, while Mercosur has a significantly less developed market shown on e-retail due to having fewer products and GIs in absolute and relative terms, a disadvantageous proportion of outside/inside products, and GI variety expressively for inner economy and production, along with a disordered strategy towards agrifood GI segments.

The global system leans toward expansionist capitalism, strengthening the mass production of agrifood goods by massification and standardization (

Bonanno and Constance 2001). However, it also results in a countermovement in search of different, more culturally relevant products. This phenomenon creates niche markets regulated by state or suprastate institutions in the case of GI products. These regulations are embedded between the state and interest groups of niche producers. Nevertheless, they can be beneficial for intensifying the trade in value-added products and supporting the primary sector on a broad spectrum, particularly smallholder agrifood farmers.

The evidence presented in this paper supports the premise initially stated that the EU and Mercosur have a significant market difference regarding the e-retail of GI products. The differences concern quantity, variety and representativity. Such differences find pathways by strengthening strategic sorts of goods that lead institutional mechanisms towards economic benefits. Despite the risk of agendas and equity treatments being hijacked by interest groups, state actions on economic and development policies can be beneficial to smallholder farmers and culture-related agrifood producers by institutionalizing the differentiation of these products. The difference in the category of products capable of pushing forward others still requires further investigation. However, a consistent strategy for the improvement of the economic bloc points to developing the whole protected system and products. The strengthening of the system can also serve as a positive commercial-driven strategy for the primary sector of the economy. Moreover, it can promote steps towards a culturally embedded with broader democratic spectrum in the agrifood sector. Likewise, by fostering such a niche economy, there can be a positive impact on other sectors such as tourism.

Additionally, the present work revealed three major issues regarding the present market. The first one relates to the number of products. The number of GI products that appeared on the survey on e-commerce in EU markets is significantly greater than in Mercosur. This is mainly due to the strength of the institutional arrangements of each bloc. Thus, the presence of GI products shows an apparent asymmetry of inner-bloc GI performance. The second aspect regards the products’ categories; here too the EU has a broader representation than Mercosur. However, even in this scenario, only a few categories were represented in e-retail in both economic blocs. This also denotes the cruciality of political institutions and their relations with the producers of such categories. The last aspect concerns the absence and underrepresentation of most GI products in e-retail major supermarkets of both blocs. This discovery, despite being relevant to scientific enlightenment, needs further investigations to clarify its causes. Furthermore, the reasons rely either on the failure of the value chain of economic activity, on strictly regional commerce, or lack of socio-political performance. Overall, the creation of the GI label does not guarantee that a new field, as in

Fligstein and McAdam’s (

2012) concept, prevails and finds favorable conditions in a niche market.

Finally, the present work brings novelty into the e-retail market of GI products in the EU and Mercosur. The mentioned findings present the importance of the socio-political construction of this market. It also points to the importance of market-oriented normativity for the development of GI products and their culturally embedded aspects. Such properly planned construction can promote the development of agrifood products.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}